Liquid Roofing Market Size

| Study Period | 2019-2029 |

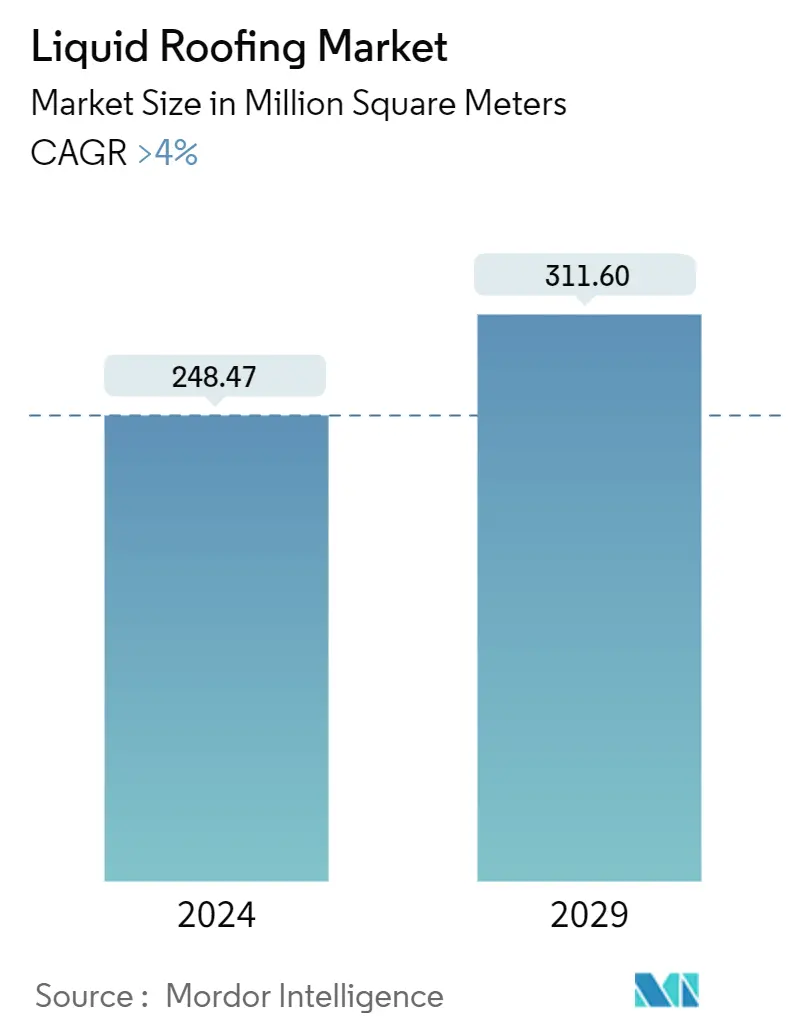

| Market Volume (2024) | 248.47 Million square meters |

| Market Volume (2029) | 311.60 Million square meters |

| CAGR (2024 - 2029) | > 4.00 % |

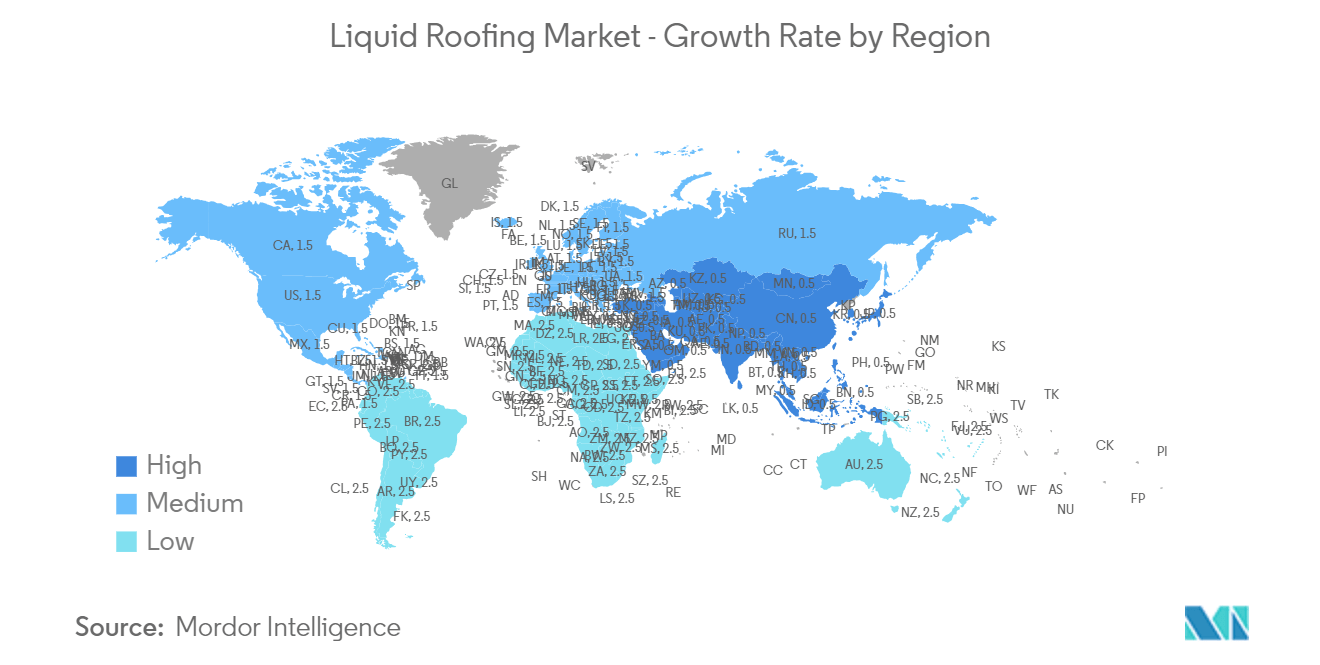

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Liquid Roofing Market Analysis

The Liquid Roofing Market size is estimated at 248.47 Million square meters in 2024, and is expected to reach 311.60 Million square meters by 2029, growing at a CAGR of greater than 4% during the forecast period (2024-2029).

The initial impact of COVID-19 was a demand slump in the liquid roofing market in 2020. However, the market showed signs of recovery in 2021 and 2022, and the long-term outlook appears positive.

Increasing consumer awareness of benefits such as lifespan extension, temperature reduction, and ease of maintenance is driving the residential demand for the liquid roofing market.

However, the volatility in the cost of the raw material may hinder the growth of the liquid roofing market in the near future.

The growing need to reduce carbon footprints across the globe is likely to provide opportunities for the liquid roofing market over the next five years.

The Asia-Pacific region dominates the liquid roofing market, owing to the increasing consumption of liquid roofing from countries like China, India, etc.

Liquid Roofing Market Trends

Residential Segment to Dominate the Market

- The residential sector stands to be the dominating segment owing to the large-scale consumption of liquid roofing in the construction industry.

- Beneficial attributes like long-term roofs, lower maintenance costs, and more value as life cycle costs decrease with liquid roofing. Increasing awareness and acceptability among consumers regarding liquid roofing is expected to drive market growth.

- Among types, the silicone coating is utilized in structures and building roofs due to its advantages over other fluid membranes, such as weathering resistance, UV protection, volatile organic compound tolerance, and durability, and provides construction owners with an alternative to an expensive re-roofing project.

- Refurbishing and renovation of old buildings have increased investments in the building and construction industry and are anticipated to contribute to a rise in market demand in the upcoming years.

- Asia-Pacific countries like China, India, and South Korea have been registering strong growth in construction and remodeling activities, and the requirement for a liquid roofing market is projected to increase in this region in the forecast period.

- Factors such as rapid urban migration in major economies, increased government spending in the real estate market for residential construction, and the growing demand for high-class residential homes are likely to benefit the growth of the construction industry.

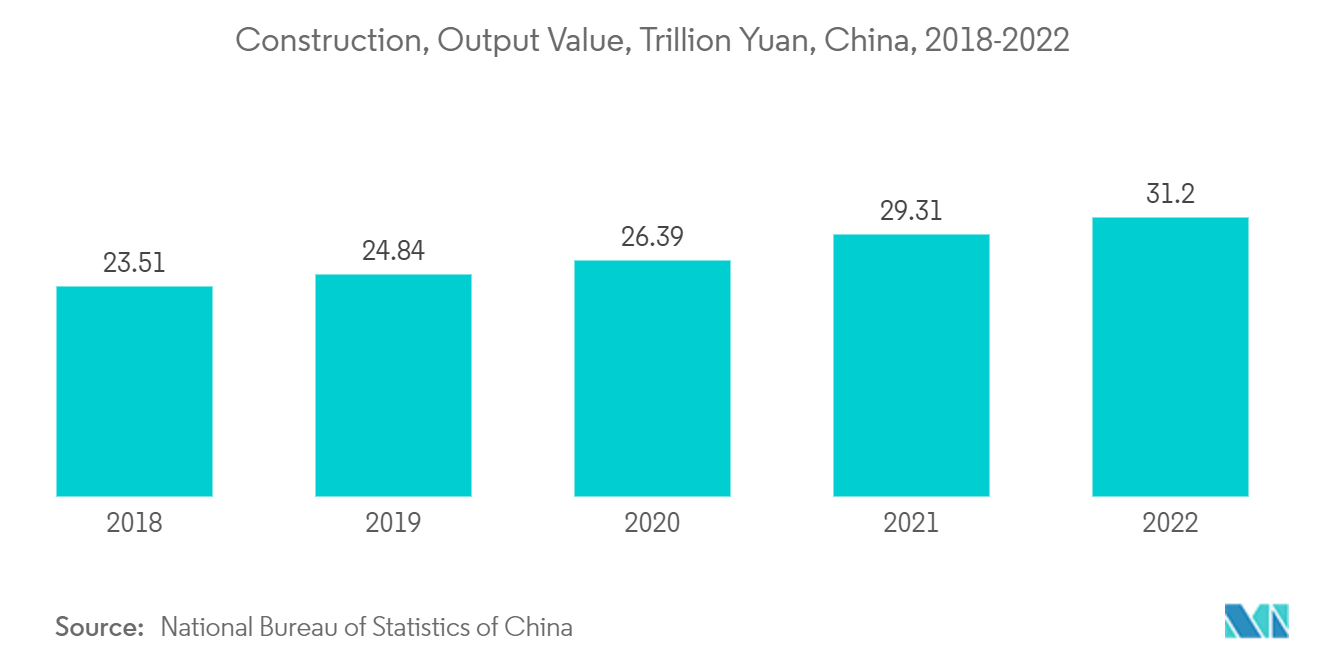

- In 2022, the construction output value in China achieved its peak at around CNY 31.2 trillion.

- In North America, the United States has a major share in the construction industry. Besides the United States, Canada and Mexico contribute significantly to the construction sector investments.

- The annual value of residential construction in the United States was valued at USD 908 billion in 2022, an increase of 13% compared to USD 803 billion in 2021.

- In Canada, various government projects, including the Affordable Housing Initiative (AHI), New Building Canada Plan (NBCP), and Made in Canada, are set to hugely support the sector’s expansion. In August 2022, the Canadian government announced a significant investment of more than USD 2 billion to fund three important initiatives that will collectively help to develop approximately 17,000 houses for families across the nation, including thousands of affordable housing units.

- In 2022, according to the American Institute of Architects (AIA) Consensus Construction Forecast, construction spending on buildings grew by an estimated 9% in 2022, and it is anticipated to grow by an additional 6% in 2023. This outlook is slightly more optimistic than forecasted at the beginning of 2022. This was largely due to strong growth in the manufacturing sector and growing strength in retail facilities.

- Europe's construction sector grew by 2.5% in 2022, owing to new investments from the European Union Recovery Fund. Business confidence picked up in early 2022 and is expected to reach pre-COVID-19 levels despite price pressures at most EU construction firms. Moreover, as the COVID-19 crisis abates and builders become less reluctant to invest in new corporate buildings and renovate existing properties, non-residential construction is expected to pick up the pace, thus supporting overall growth in the construction market.

Asia-Pacific Region to Dominate the Market

- According to Oxford Economics, the global construction industry is expected to grow by USD 4.5 trillion, or 42%, between 2020 and 2030. Additionally, China, India, the United States, and Indonesia are expected to account for 58.3% of global growth in construction between 2020 and 2030.

- Factors such as expansion in the residential and commercial construction sector will drive the market growth in the region.

- Liquid roofing systems are highly tenable, lower maintenance costs, are proven to be more durable than other waterproofing systems, are long-lasting, and aid in the prevention of uneven spots, bumps, any overlaps over the roof surface, etc.

- Rising government plans for advancing infrastructures, such as Vietnam's Socio-Economic Development Plan, Indonesia's National Medium-Term Development Plan, Philippine Development Plan, and other country's plans are expected to drive market growth.

- Emerging demand for energy-efficient structures, expanding awareness about the cost-effectiveness of liquid roofing, and increasing construction activities worldwide will further accelerate the liquid roofing market in the forecast period.

- India's construction industry was valued at over three trillion Indian rupees in the fourth quarter of 2022. This was a significant increase compared to 2020 when the value shrank due to the COVID-19 pandemic. The country’s construction and manufacturing industries were among the worst hit at the time. However, the industry seemed to recover quickly and returned to pre-crisis level again.

- China's construction industry, one of the world's largest, has experienced significant growth in recent decades. China is undergoing rapid urbanization and industrialization, increasing construction activities such as residential, commercial, and infrastructure construction. In recent years, however, the construction industry has been under constant pressure from property developers' deleveraging measures, leading to more sustainable construction practices.

- In China, the infrastructure projects in development or execution of over USD 25 million as of May 2022 were worth over USD 5 trillion. The United States and India were the following countries on the list, with around USD 2 trillion worth of infrastructure projects. In contrast, the country with the highest number of big infrastructure projects was India.

- Hence, all such market trends are expected to drive the demand for liquid roofing market in the region during the forecast period.

Liquid Roofing Industry Overview

The Liquid Roofing Market is partially fragmented in nature. The major players (not in any particular order) include Kemper System Ltd, Johns Manville (Berkshire Hathaway Company), GAF, Saint-Gobain Weber, and BASF SE.

Liquid Roofing Market Leaders

Kemper System Ltd

Johns Manville (A Berkshire Hathaway Company)

Saint-Gobain Weber

BASF SE

GAF

*Disclaimer: Major Players sorted in no particular order

Liquid Roofing Market News

- Oct 2023: Langley introduced a new Langley PU Liquid Waterproofing system, which allows the application of a 25-year system in just two coats. This significantly decreases install time compared to many other liquids in the market where a three-coat system is required.

- Oct 2023: BASF partners with Oriental Yuhong to develop solar roofing membranes used in buildings. The new development aims to meet China’s rapidly growing demand for rooftop solar panels. As the country’s solar PV installations reached a record high of 51 gigawatts, with rooftops accounting for more than one-third of the installed capacity in 2022, the quality of TPO roofing membranes, including their waterproofing performance, has become critical.

Liquid Roofing Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Residential Segment

4.1.2 Increasing Consumer Awareness for Liquid Roofing

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Unfavorable Conditions Arising Due to COVID-19 Outbreak

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products

4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Volume)

5.1 Type

5.1.1 Polyurethane Coatings

5.1.2 Acrylic Coatings

5.1.3 Bituminous Coatings

5.1.4 Silicone Coatings

5.1.5 Epoxy Coatings

5.1.6 Other Types (Modified Silane Polymers, EPDM Rubbers, Elastomeric Membranes, Cementitious Membranes, and Epoxy Coatings)

5.2 Application

5.2.1 Domed Roofs

5.2.2 Pitched Roof

5.2.3 Flat Roofed

5.3 End-user Industry

5.3.1 Residential

5.3.2 Commercial

5.3.3 Industrial/Institutional

5.3.4 Infrastructure

5.4 Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Malaysia

5.4.1.6 Thailand

5.4.1.7 Indonesia

5.4.1.8 Vietnam

5.4.1.9 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 France

5.4.3.4 Italy

5.4.3.5 Spain

5.4.3.6 NORDIC

5.4.3.7 Turkey

5.4.3.8 Russia

5.4.3.9 Rest of Europe

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Colombia

5.4.4.4 Rest of South America

5.4.5 Middle-East and Africa

5.4.5.1 Saudi Arabia

5.4.5.2 South Africa

5.4.5.3 Nigeria

5.4.5.4 Qatar

5.4.5.5 Egypt

5.4.5.6 UAE

5.4.5.7 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)/Ranking Analysis**

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Akzo Nobel NV

6.4.2 Alumasc Building Products

6.4.3 BASF SE

6.4.4 BMI UK & Ireland

6.4.5 GAF

6.4.6 GreenShield

6.4.7 Johns Manville (A Berkshire Hathaway Company)

6.4.8 Kemper System Ltd

6.4.9 Laydex

6.4.10 Liquid Roofing Systems LTD

6.4.11 Saint-Gobain Weber

6.4.12 SIG Design and Technology (Part of SIG PLC)

6.4.13 Sika AG

6.4.14 Langley

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Growing Need to Reduce Carbon Footprints

7.2 Other Opportunities

Liquid Roofing Industry Segmentaion

Liquid roofing is the process of waterproofing a roof by the application of a hydrophobic liquid roof coating. It can be applied to most roof styles, including flat, pitched, and domed roofs. It is the process of applying coatings to the roof to prolong its lifetime, lower the temperature (also lowering energy requirement and pollution), and make the surface easier to clean and maintain.

Liquid roofing Market is segmented into type, application, and geography. By type, the market is segmented into polyurethane coatings, acrylic coatings, bituminous coatings, silicone coatings, epoxy coatings, and others. By application, the market is segmented into domed roofs, pitched roofs, and flat roofs. By end-user industry, the market is segmented into residential, commercial, industrial/institutional, and infrastructure. The report also covers the market size and forecasts for the Liquid Roofing Market in 27 countries across the Asia-Pacific region. For each segment, the market sizing and forecasts were made on the basis of volume (SQM).

| Type | |

| Polyurethane Coatings | |

| Acrylic Coatings | |

| Bituminous Coatings | |

| Silicone Coatings | |

| Epoxy Coatings | |

| Other Types (Modified Silane Polymers, EPDM Rubbers, Elastomeric Membranes, Cementitious Membranes, and Epoxy Coatings) |

| Application | |

| Domed Roofs | |

| Pitched Roof | |

| Flat Roofed |

| End-user Industry | |

| Residential | |

| Commercial | |

| Industrial/Institutional | |

| Infrastructure |

| Geography | |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

|

Liquid Roofing Market Research FAQs

How big is the Liquid Roofing Market?

The Liquid Roofing Market size is expected to reach 248.47 million square meters in 2024 and grow at a CAGR of greater than 4% to reach 311.60 million square meters by 2029.

What is the current Liquid Roofing Market size?

In 2024, the Liquid Roofing Market size is expected to reach 248.47 million square meters.

Who are the key players in Liquid Roofing Market?

Kemper System Ltd, Johns Manville (A Berkshire Hathaway Company), Saint-Gobain Weber, BASF SE and GAF are the major companies operating in the Liquid Roofing Market.

Which is the fastest growing region in Liquid Roofing Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Liquid Roofing Market?

In 2024, the Asia Pacific accounts for the largest market share in Liquid Roofing Market.

What years does this Liquid Roofing Market cover, and what was the market size in 2023?

In 2023, the Liquid Roofing Market size was estimated at 238.53 million square meters. The report covers the Liquid Roofing Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Liquid Roofing Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Liquid Roofing Industry Report

Statistics for the 2024 Liquid Roofing market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Liquid Roofing analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.