Market Overview

| Study Period | 2021 - 2031 |

|---|---|

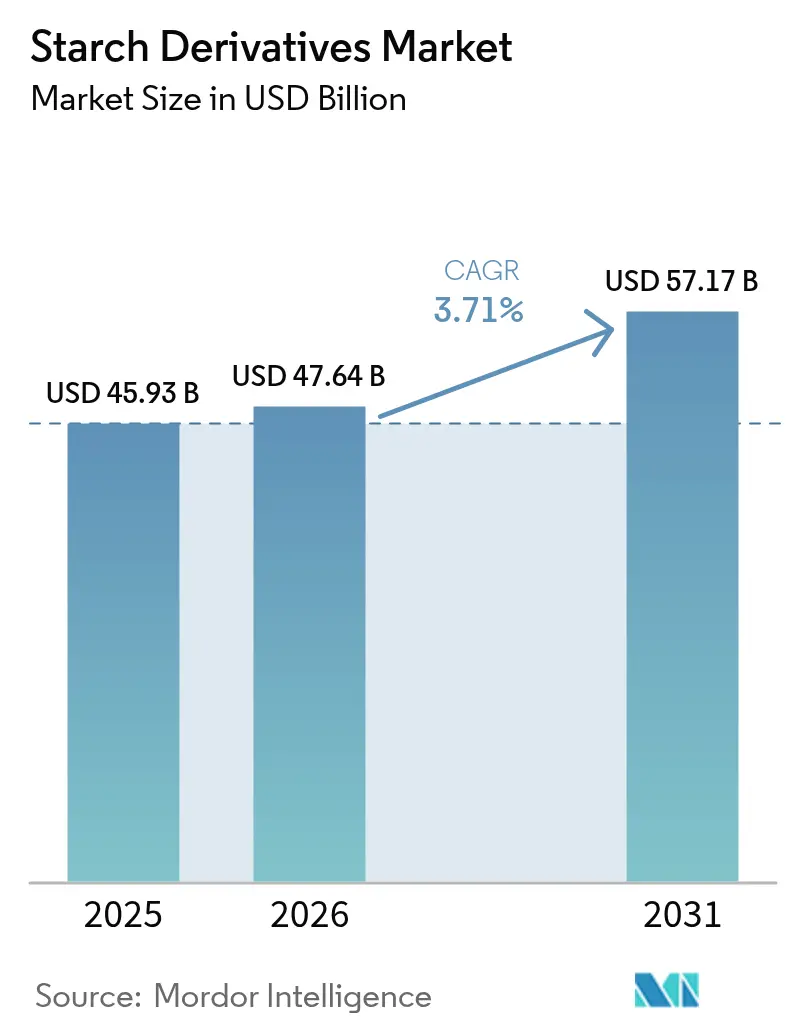

| Market Size (2026) | USD 47.64 Billion |

| Market Size (2031) | USD 57.17 Billion |

| Growth Rate (2026 - 2031) | 3.71% CAGR |

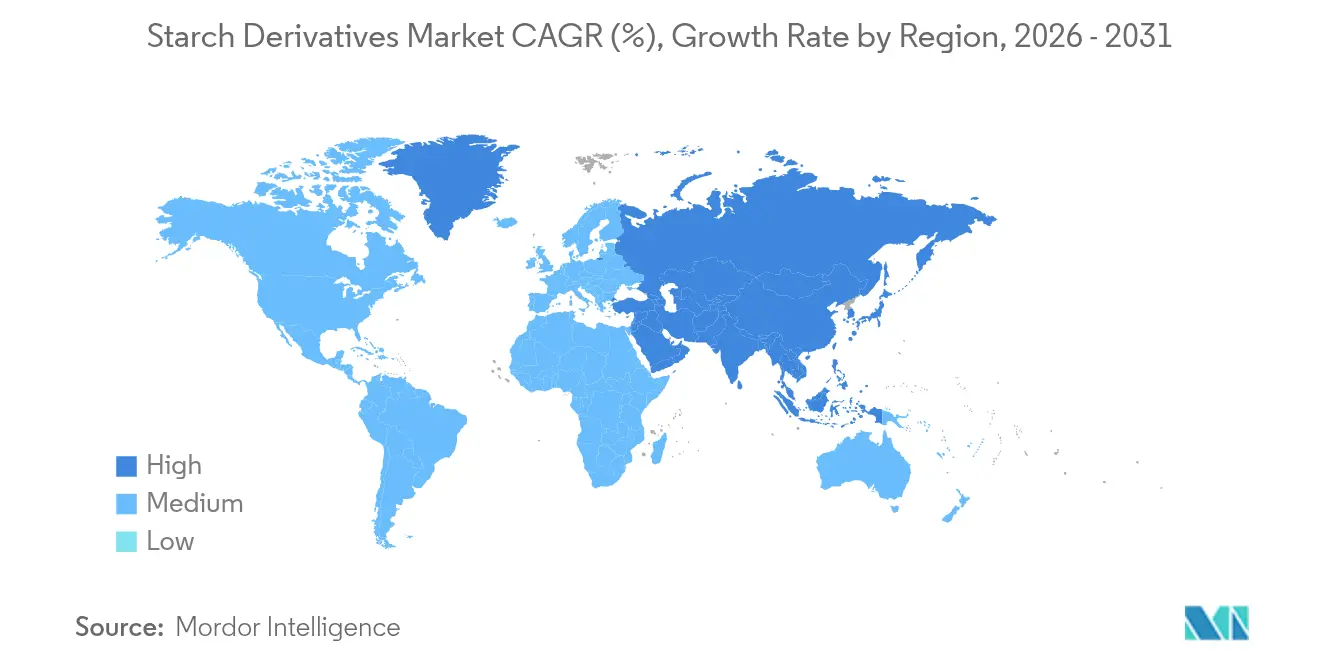

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Starch Derivatives Market Analysis by Mordor Intelligence

The starch derivatives market size is expected to grow from USD 45.93 billion in 2025 to USD 47.64 billion in 2026 and is forecast to reach USD 57.17 billion by 2031 at 3.71% CAGR over 2026-2031. Moderate but steady expansion reflects the transition from bulk commodities to specialty derivatives that command premium pricing. Regulatory agencies now favor plant-based inputs, enabling broader use of maltodextrin, cyclodextrin, and glucose syrups in food, beverage, and pharmaceutical formulations. Investment continues to move toward enzymatic processing that lowers energy use and simplifies compliance with environmental rules. North American suppliers benefit from a mature Food and Drug Administration (FDA) framework, while Asia-Pacific manufacturers gain momentum through harmonized safety standards and rising nutraceutical demand. Across all regions, clean-label and non-GMO positioning is no longer optional; it has become a key competitive lever for branded ingredient suppliers that target global food and drug customers.

Key Report Takeaways

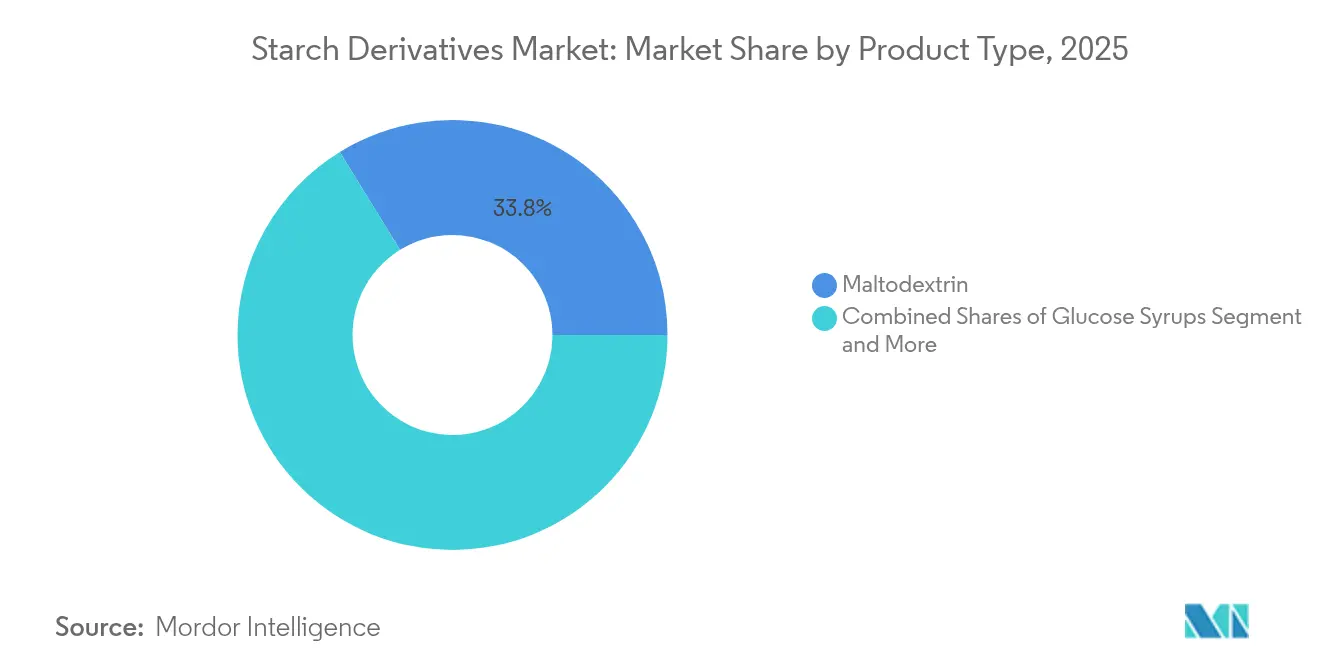

- By type, maltodextrin held 33.78% of the starch derivatives market share in 2025, while cyclodextrin is projected to grow at a 4.92% CAGR from 2026-2031.

- By source, maize dominated with a 62.61% share in 2025; tapioca is set to expand at a 4.7% CAGR through 2031.

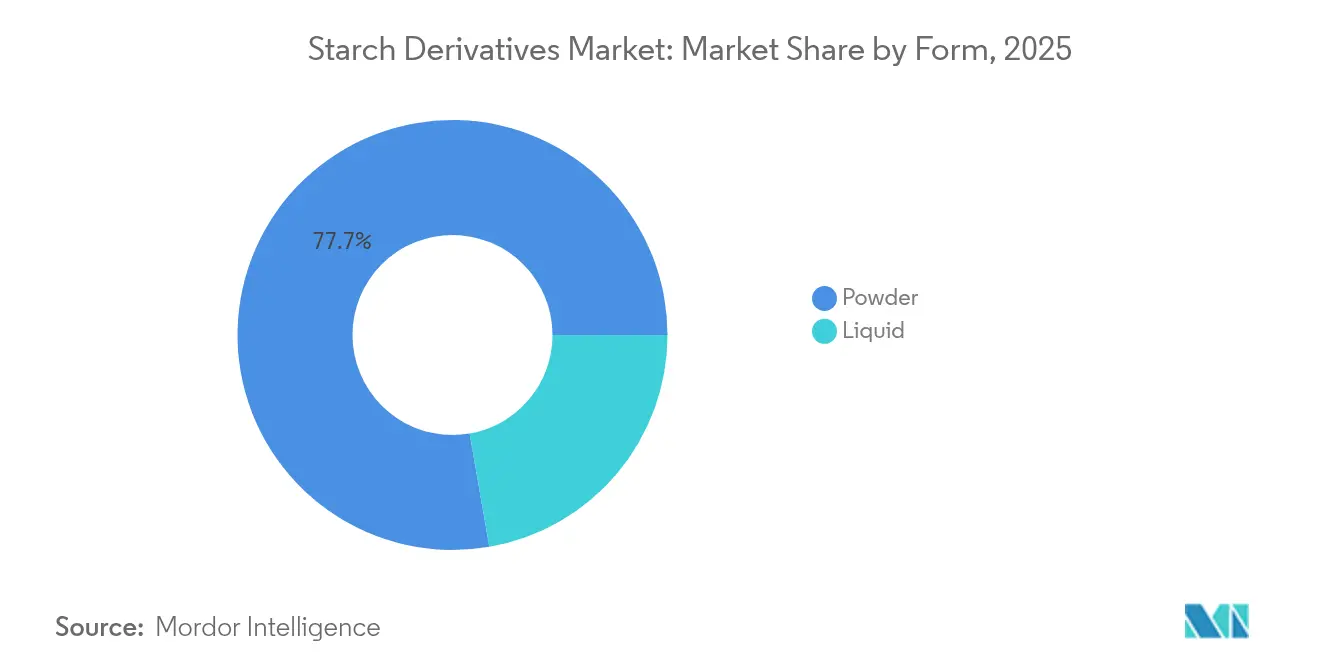

- By form, powder accounted for 77.74% revenue in 2025, whereas liquid derivatives are forecast to post a 4.45% CAGR to 2031.

- By application, food and beverage captured 65.55% of the starch derivatives market size in 2025, and pharmaceutical applications will register the fastest 5.18% CAGR between 2026-2031.

- By geography, North America led with a 35.96% share in 2025; Asia-Pacific is expected to rise at a 5.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Starch Derivatives Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Natural Sweeteners in Food and Beverage | +0.8% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

| High Demand for Starch-Based Glucose Syrup in Bakery and Confectionary | +0.6% | Global, concentrated in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Increased Adoption of High Fructose Corn Syrup (HFCS) in Beverage Formulation | +0.5% | North America & Latin America primarily | Short term (≤ 2 years) |

| Multi-Functional Benefits Associated with Starch Derivatives | +0.7% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Amplifying Demand for Clean Label and Non-GMO Ingredients | +0.9% | North America & Europe leading, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Technological Advancements in Enzymatic Processing of Starch | +0.4% | Global, with innovation centers in Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Natural Sweeteners in Food and Beverage

Regulatory frameworks increasingly favor naturally-derived sweeteners over synthetic alternatives, with the FDA's Generally Recognized as Safe (GRAS) designation streamlining approval pathways for starch-based sweetening systems. The FDA's classification of maltodextrin as a non-sweet saccharide polymer with dextrose equivalent below 20 positions it advantageously against synthetic alternatives in food applications. Consumer preference shifts toward natural ingredients drive reformulation initiatives across beverage categories, creating sustained demand for starch-derived texturizing agents that maintain mouthfeel while reducing synthetic additive content. The trend extends beyond beverages into functional foods, where clean-label requirements drive specification of naturally-derived starch modifications over chemically-processed alternatives. Regulatory bodies' emphasis on ingredient transparency strengthens the competitive position of starch derivatives in applications requiring natural ingredient declarations.

High Demand for Starch-Based Glucose Syrup in Bakery and Confectionary

Bakery and confectionery applications leverage glucose syrups' unique functional properties, particularly their ability to control crystallization and extend shelf life while maintaining compliance with food safety regulations. The FAO's Codex Alimentarius standards recognize glucose syrups as essential functional ingredients in processed foods, supporting their adoption across global markets. Enzymatic processing innovations enable glucose syrup production with tailored dextrose equivalent values, allowing manufacturers to optimize sweetness intensity and browning characteristics for specific applications while maintaining regulatory compliance. European food safety frameworks favor naturally-derived glucose syrups over synthetic alternatives in premium confectionery segments, creating market differentiation opportunities. The application's technical complexity and regulatory requirements create barriers to entry, enabling established players with approved formulations to maintain pricing power while expanding into adjacent categories.

Increased Adoption of High Fructose Corn Syrup (HFCS) in Beverage Formulation

HFCS adoption in beverage formulation reflects regulatory acceptance and established safety profiles, with FDA approval supporting its use across multiple food categories despite evolving consumer preferences. The ingredient's superior solubility and flavor enhancement properties make it indispensable for carbonated soft drinks and energy beverages, where functional requirements align with regulatory specifications. Regional regulatory differences create market segmentation opportunities, with established approval pathways in North American markets supporting continued growth while European markets maintain stricter labeling requirements. The FDA's food additive regulations provide clear guidelines for HFCS usage levels, enabling manufacturers to optimize formulations within approved parameters. Regulatory stability in key markets supports long-term supply agreements and production planning, despite evolving consumer preferences toward natural alternatives.

Amplifying Demand for Clean Label and Non-GMO Ingredients

Clean label requirements fundamentally alter starch derivative specifications, with regulatory frameworks like the EU's Novel Food Regulation strengthening natural ingredient positioning by requiring extensive safety documentation for synthetic alternatives. The USDA's National Organic Program standards create certification pathways for organic starch derivatives, enabling premium pricing for certified ingredients that meet consumer expectations. EFSA's[1]European Food Safety Authority, "Extension of use of isomalto-oligosaccharide as a novel food according to Regulation (EU) 2015/2283", www.efsa.com safety assessments of food additives increasingly favor naturally-derived ingredients with established safety profiles, creating competitive advantages for starch-based alternatives over synthetic additives. Regulatory frameworks emphasizing ingredient transparency strengthen the competitive position of starch derivatives in applications requiring natural ingredient declarations. Supply chain transparency requirements, supported by regulatory traceability standards, become competitive differentiators for companies investing in sustainable sourcing programs.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Agricultural Raw Material Costs Affect Industry Profitability | -0.7% | Global, with highest impact in commodity-dependent regions | Short term (≤ 2 years) |

| Health Concerns Linked to High Fructose Corn Syrup Consumption | -0.4% | North America & Europe primarily | Medium term (2-4 years) |

| Rising Consumer Shift Away from Artificial Additives | -0.3% | Developed markets leading, expanding globally | Long term (≥ 4 years) |

| Allergy Risks and Labeling Requirements for Various Starch Additives | -0.2% | Global, with strictest requirements in EU & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Agricultural Raw Material Costs Affect Industry Profitability

Raw material price volatility significantly impacts starch derivative profitability, with agricultural commodity markets subject to weather-related disruptions and geopolitical tensions affecting global supply chains. USDA[2]U.S. Department of Agriculture, “World Agricultural Supply and Demand Estimates,” usda.gov crop reports indicate significant yield variations in key starch-producing regions, directly affecting raw material availability and pricing for downstream processors. Corn starch markets demonstrate particular sensitivity to agricultural policy changes and trade regulations, with price fluctuations creating margin pressure for integrated processors. Weather-related disruptions in key agricultural regions force manufacturers to maintain higher inventory levels, increasing working capital requirements and reducing operational flexibility. Government agricultural support programs and trade policies create additional uncertainty in raw material pricing, requiring sophisticated hedging strategies to manage cost volatility.

Rising Consumer Shift Away from Artificial Additives

Consumer preferences increasingly favor naturally-derived ingredients, supported by regulatory frameworks that require clear labeling of synthetic additives and processing aids. European Union [3]European Commission, “Regulation (EU) No 1169/2011 on Food Information to Consumers,” ec.europa.euregulations on food additives create stricter approval pathways for synthetic ingredients while maintaining streamlined processes for naturally-derived alternatives. The FDA's food additive approval process increasingly emphasizes safety data for synthetic compounds while maintaining GRAS pathways for natural ingredients with established safety profiles. This regulatory environment creates competitive advantages for starch-based alternatives over synthetic additives in applications requiring clean-label positioning. Government consumer protection agencies' emphasis on ingredient transparency strengthens market demand for naturally-derived starch modifications over chemically-processed alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Pharmaceutical Applications Drive Specialty Growth

Cyclodextrin emerges as the fastest-growing segment with 4.92% CAGR through 2031, driven by FDA approvals for pharmaceutical applications where its unique molecular structure enables drug solubility enhancement and controlled release formulations. The FDA's recognition of cyclodextrins as safe excipients in drug delivery systems supports commercial viability across multiple therapeutic categories. Maltodextrin commands 33.78% market share in 2025, reflecting its versatility as a bulking agent and flavor carrier with established GRAS status across food applications. Glucose syrups maintain steady demand in bakery applications, supported by FAO Codex standards that recognize their functional benefits in processed foods. Dextrins benefit from expanding industrial uses in adhesives and biodegradable packaging, where environmental regulations favor naturally-derived alternatives.

Recent regulatory approvals for cyclodextrin-based pharmaceutical formulations demonstrate the segment's evolution toward sophisticated drug delivery platforms, with applications extending across multiple therapeutic areas. The type segmentation increasingly reflects regulatory compliance requirements rather than traditional commodity categories, with specialty derivatives commanding premium pricing through technical differentiation and established approval pathways. Modified cyclodextrins receive regulatory recognition for enhanced solubility properties, creating opportunities for application-specific derivatives in pharmaceutical and nutraceutical markets.

By Source: Regulatory Compliance Drives Diversification

Tapioca represents the fastest-growing source at 4.7% CAGR through 2031, benefiting from its naturally gluten-free properties and compliance with clean-label regulations across global markets. Maize dominates with a 62.61% market share in 2025, supported by established USDA quality standards and a comprehensive supply chain infrastructure that ensures consistent quality and regulatory compliance. Wheat-based derivatives serve specialized applications in European markets, where EU quality standards support premium positioning in food applications. Potato starch commands premium pricing in applications requiring superior film-forming properties, supported by regulatory recognition of its functional benefits. Rice starch gains importance in Asian markets, where local food safety regulations support its use in traditional and modern food applications.

Source diversification strategies reflect regulatory risk management considerations, with companies maintaining multiple source approvals to ensure supply chain resilience despite regulatory changes. The comparative regulatory status of different starch sources creates market segmentation opportunities, with organic and non-GMO certifications enabling premium positioning in health-conscious consumer segments. Regulatory frameworks governing agricultural inputs and processing methods increasingly influence source selection decisions, favoring suppliers with comprehensive compliance programs.

By Form: Processing Regulations Shape Market Dynamics

Liquid derivatives grow at 4.45% CAGR through 2031, driven by industrial processing applications where FDA good manufacturing practice guidelines favor continuous processing systems. Powder form maintains dominance with 77.74% market share in 2025, reflecting regulatory advantages in storage stability and transportation compliance across international markets. The form segmentation reflects regulatory requirements for food safety and quality control, with powder forms offering advantages in microbiological stability and shelf life extension. Processing regulations increasingly influence form selection, with liquid forms preferred in applications requiring precise dosing and mixing under controlled conditions.

Recent developments in processing technology enable form modifications that comply with environmental regulations while maintaining functional performance characteristics. The choice between powder and liquid forms increasingly depends on regulatory compliance requirements, with liquid forms advantageous in pharmaceutical applications requiring sterile processing conditions. Innovation in form development includes regulatory-compliant encapsulation technologies that protect sensitive derivatives during storage and transportation.

By Application: Regulatory Pathways Enable Pharmaceutical Growth

Pharmaceutical applications emerge as the fastest-growing segment with 5.18% CAGR through 2031, driven by FDA and EMA approval pathways that recognize starch derivatives as safe and effective excipients in drug formulations. Food and beverage applications command 65.55% market share in 2025, supported by comprehensive regulatory frameworks that establish safety parameters for starch-based ingredients across multiple food categories. Personal care applications benefit from FDA cosmetic regulations that recognize starch derivatives' functional properties in topical formulations. Animal feed applications provide stable demand for lower-grade derivatives, supported by USDA feed safety regulations that ensure product quality and safety.

The pharmaceutical segment's growth reflects regulatory acceptance of cyclodextrin-based formulations, with established approval pathways enabling commercial viability across therapeutic categories. Within food applications, regulatory frameworks increasingly favor naturally-derived starch modifications over synthetic alternatives, creating competitive advantages for compliant suppliers. Application diversification strategies enable companies to leverage regulatory expertise across multiple sectors while reducing dependence on single application categories.

Geography Analysis

North America maintains market leadership with 35.96% share in 2025, supported by comprehensive FDA regulatory frameworks that establish clear pathways for starch derivative approval across food and pharmaceutical applications. The region benefits from USDA agricultural quality standards that ensure consistent raw material supply and established good manufacturing practices that support export competitiveness. Regulatory stability in pharmaceutical applications creates competitive advantages for North American suppliers, with FDA approval pathways enabling premium positioning in global markets. The region's mature regulatory environment supports innovation in specialty applications while maintaining safety standards that ensure consumer protection.

Asia-Pacific emerges as the fastest-growing region with 5.02% CAGR through 2031, driven by regulatory harmonization initiatives across ASEAN markets that create standardized approval pathways for starch derivatives. Regional food safety frameworks increasingly align with international standards, reducing compliance costs for multinational suppliers while ensuring product quality and safety. The region's growth reflects expanding pharmaceutical manufacturing capabilities supported by regulatory frameworks that recognize international quality standards. Government initiatives promoting food processing industrialization create demand for technically sophisticated starch derivatives that comply with evolving safety requirements.

Europe demonstrates steady growth supported by comprehensive EFSA safety assessments that establish clear guidelines for starch derivative applications across food and pharmaceutical sectors. The region's stringent regulatory framework creates barriers to entry while protecting established suppliers with approved product portfolios and comprehensive compliance programs. EU environmental regulations favor biodegradable starch-based materials over petroleum-based alternatives, creating market opportunities for sustainable packaging applications. The region's focus on sustainability drives regulatory support for naturally-derived starch modifications that comply with circular economy principles and environmental protection standards.

Competitive Landscape

The starch derivatives market shows low fragmentation score. This structure stems from regulatory barriers that benefit established companies possessing comprehensive approval portfolios and quality control systems. The competitive landscape focuses on regulatory compliance and technical differentiation rather than price, as companies invest in quality assurance capabilities and regulatory expertise to serve premium market segments. Companies with existing FDA and EFSA approvals maintain competitive advantages, while new entrants face high regulatory compliance costs that limit market entry. The leading companies in the starch derivatives market, such as Archer Daniels Midland Company, Cargill, Incorporated, Ingredion Inc., and Tate & Lyle Plc, distinguish themselves through innovation, broad product portfolios, and substantial production capacities.

These players focus on developing new applications of starch derivatives in emerging sectors like biofuels and bioplastics, which enhances their market share. Additionally, their ability to adapt to evolving consumer preferences, particularly in the food industry, by offering clean-label and non-GMO starch derivatives, positions them as market leaders. The starch derivatives production processes employed by these companies are continuously refined to improve efficiency and sustainability.

A significant trend in the starch derivatives market is the shift toward sustainable and clean-label products, driven by consumer demand for healthier and environmentally friendly options. Companies are investing in sustainable sourcing of raw materials and improving production efficiency to reduce their environmental footprint. Another critical success factor is the ability to customize products to meet specific industry requirements, especially in the rapidly evolving food and beverage sector. Firms that can align with these trends are poised for continued growth and market leadership.

Starch Derivatives Industry Leaders

-

Archer Daniels Midland Company

-

Cargill, Incorporated

-

Ingredion Inc.

-

Tate & Lyle Plc

-

Roquette Frères S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Arla Foods Ingredients received approval from the US Food & Drug Administration for its whey protein hydrolysates, designed to aid in allergy management and promote gut comfort in infant formula. The FDA confirmed that four ingredients from the company's Peptigen and Lacprodan ranges qualify as peptones under the US Code of Federal Regulations. Consequently, these ingredients are authorized for use in early life nutrition.

- June 2024: Tate & Lyle announced USD 1.8 billion acquisition of CP Kelco to create leading global specialty food and beverage solutions business, expanding capabilities in sweetening and fortification applications.

- May 2024: Omnia Europe SA, a global manufacturer of specialty starch and derivatives catering to the food, feed, and bioindustrial sectors, is headquartered in Constanta, Romania. In response to the evolving market demands for plant-based, nutritional, and cost-efficient solutions, the company announces strategic investments aimed at diversifying its product and solutions portfolio. These investments are made with a commitment to safety, responsibility, and sustainability.

- January 2024: Green Plains Inc., a pioneer in ag-tech, finalized the construction of the industry's inaugural full-scale Clean Sugar Technology (CST) installation at its biorefinery in Shenandoah, Iowa. This groundbreaking facility boasts the industry's first low-carbon dextrose and glucose process at a dry mill, achieving a carbon footprint up to 40% lower than competing alternatives. Furthermore, innovations from their majority-owned subsidiary, Fluid Quip Technologies (FQT), provide Green Plains with a competitive edge in producing diversified, high-quality ingredients.

Global Starch Derivatives Market Report Scope

Starch derivatives refer to modifications that alter the chemical structure of specific d-glucopyranosyl units within the molecule. Typically, these modifications encompass processes like oxidation, esterification, or etherification.

The market is studied for different type of starch derivatives such as maltodextrin, cyclodextrin, glucose syrups, hydrolysates, modified starch, and others. The different sources through which starch derivative are derived includes corn, wheat, cassava, potato and other sources. Its wide application in different end user industries such as food and beverage, feed, paper industry, pharmaceutical industry, bioethanol, cosmetics, and other industrial applications. Also, the market for starch derivatives is further studied for potential countries under each region, including North America, Europe, Asia Pacific, South America, and the Middle East And Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Type

| Glucose Syrups |

| High Fructose Corn Syrup (HFCS) |

| Maltodextrin |

| Cyclodextrin |

| Dextrins |

| Others |

By Source

| Maize |

| Wheat |

| Potato |

| Tapioca |

| Others |

By Form

| Powder |

| Liquid |

By Application

| Food and Beverage | Bakery |

| Confectionary | |

| Beverage | |

| Others | |

| Pharmaceutial | |

| Personal Care and Cosmetics | |

| Animal Feed | |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Type | Glucose Syrups | |

| High Fructose Corn Syrup (HFCS) | ||

| Maltodextrin | ||

| Cyclodextrin | ||

| Dextrins | ||

| Others | ||

| By Source | Maize | |

| Wheat | ||

| Potato | ||

| Tapioca | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| By Application | Food and Beverage | Bakery |

| Confectionary | ||

| Beverage | ||

| Others | ||

| Pharmaceutial | ||

| Personal Care and Cosmetics | ||

| Animal Feed | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the starch derivatives market?

The starch derivatives market is valued at USD 47.64 billion in 2026 and is projected to reach USD 57.17 billion by 2031.

Which product type leads the market?

Maltodextrin holds the largest 33.78% share, supported by widespread use as a bulking agent in beverages and instant foods.

Which region is growing the fastest?

Asia-Pacific is forecast to expand at a 5.02% CAGR from 2026-2031, driven by harmonised regulations and growing nutraceutical demand.

Why are cyclodextrins gaining momentum?

Regulatory approvals for cyclodextrin-based drug delivery systems enhance solubility and extend release, driving a 4.92% CAGR for this segment.

Page last updated on: