Europe Consumer Packaging Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

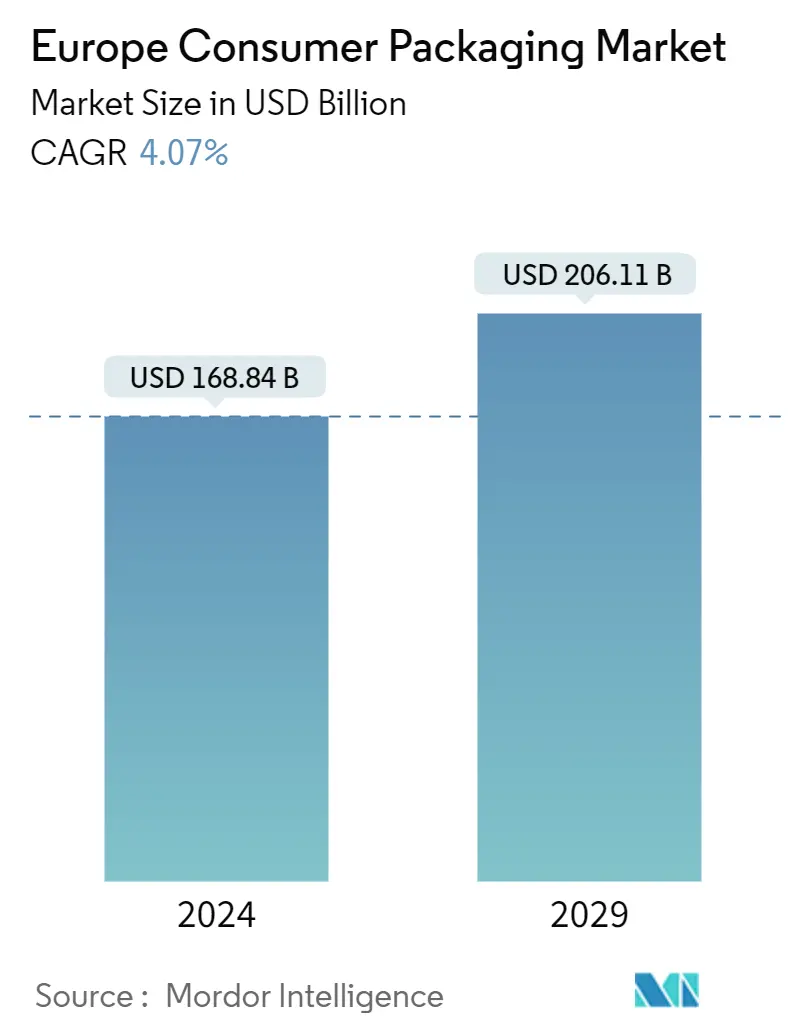

| Market Size (2024) | USD 168.84 Billion |

| Market Size (2029) | USD 206.11 Billion |

| CAGR (2024 - 2029) | 4.07 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Europe Consumer Packaging Market News

The Europe Consumer Packaging Market size is estimated at USD 168.84 billion in 2024, and is expected to reach USD 206.11 billion by 2029, growing at a CAGR of 4.07% during the forecast period (2024-2029).

- Technological innovations, sustainability trepidations, and attractive economics are the factors driving the growth of consumer packaging. Packaging plays a crucial role in the consumer goods industry in making the product appealing to the potential buyer and delivering products to the consumer that are sufficiently sophisticated, safe, convenient, and appropriate.

- Plastic packaging has become popular among consumers, as it is lightweight and unbreakable, making it easier to handle. Even significant manufacturers prefer plastic packaging, owing to the lower cost of production. Moreover, introducing polymers, such as polyethylene terephthalate (PET) and high-density polyethylene (HDPE), expands plastic packaging applications. However, reducing the amount of environmentally harmful polymers used in packaging is one of the most researched areas in the consumer packaging market.

- Furthermore, the European Union is pioneering the plastic market with its drive toward circular economy principles. It is mainly focused on plastic waste, as the high-volume, single-use item plastic packaging has come under scrutiny. Multiple strategies are being advanced to address this issue, including substituting alternative materials, investing in the development of bio-based plastics, designing packaging that is easier to process in recycling, and improving the recycling and processing of plastic waste.

- The raw materials market continues to be under considerable strain. Market demand remains high, coupled with reduced supply, and this continues to keep material prices at rates never previously seen across Europe. Recycled plastic prices fluctuate due to changes in demand, which can be attributed to the price of virgin plastics. Demand for recycled plastic will increase in times of higher prices for virgin plastic, leading to its increased cost.

Europe Consumer Packaging Market Trends

The Cosmetics Segment is Anticipated to Witness Significant Growth

- The shift toward e-commerce growth reflects the expansion of order mix, greater complexity, and more packaging diversity. Labor and seasonality also affect the ability of fulfillment operations to meet orders, complicating packaging and resulting in increased damages. Furthermore, network shipping constraints and rising costs are expected to continue. More customization and unique solutions may be needed to compete effectively and achieve customer loyalty.

- The potential market for organic and natural cosmetic products is currently in Europe, driven by the shifting consumer preferences toward the beauty industry throughout time. According to a poll by Global Web Index on more than 2,300 web users from the United Kingdom who routinely purchase organic and natural cosmetics, 80% of them do so out of concern for their health and the environment. The European cosmetics market is anticipated to flourish going forward and hold onto its top spot in the next years due to its big consumer base.

- The European Tube Manufacturers Association (ETMA) indicated market stability in the first half of 2023. Positive development was observed in demand from the cosmetics and dental care markets, with an increase of about 2% each. In terms of sustainable progress within the tube market, it is evident that the quantities required for plastic tubes cannot be achieved through mechanical recycling of used plastic packaging alone. In addition, the challenging political and economic backdrop persists. Even though there is a notable decrease in incoming orders, the order backlog remains substantial. The market outlook for the latter half of the year is uncertain, as alleged by ETMA.

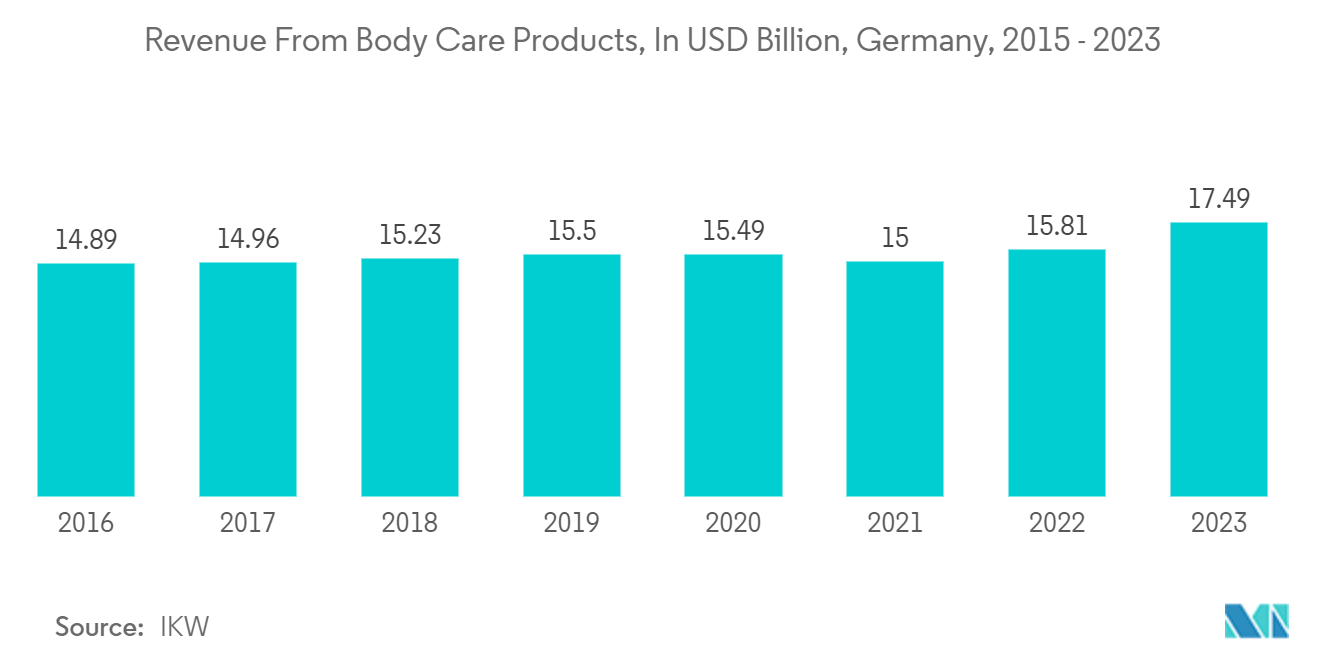

- According to IKW, a provider of in-depth shopper and consumer insights, in 2023, body care products generated a revenue of roughly USD 17.49 billion in Germany compared to 2017, which was around USD 14.96 billion. With a rising demand for body care products, there will be a corresponding increase in the demand for cosmetic packaging. Packaging is a crucial aspect of cosmetic products, and as the consumption of body care products grows, manufacturers will require more innovative and appealing packaging solutions.

Poland to Witness Significant Market Growth

- Poland is one of the significant markets for European consumer packaging vendors. This is due to the high rate of investment in advanced and innovative packaging across its various end-user industries and the country's growing focus on lightweight, portable, flexible, and environment-friendly packaging.

- The country has witnessed multiple investments by various market players and the rising demand for consumer packaging in various industries, such as food and beverages.

- The earlier capacity of UFlex's packaging films plant in Poland was 30,000 TPA, and an additional 10.4-m BOPET line of 45,000 TPA has been commissioned, making UFlex's subsidiary Flex Films one of the largest BOPET manufacturers in the European Union.

- Many Polish packaging companies are also expanding their geographical presence by opening new manufacturing units, which is expected to boost the scope of the region's flexible packaging market. For instance, Plast-Box Group, one of Poland's and Europe's prominent plastic packaging producers, opened a new warehouse and logistics center near Warsaw with an area of over 3,800 sq. m.

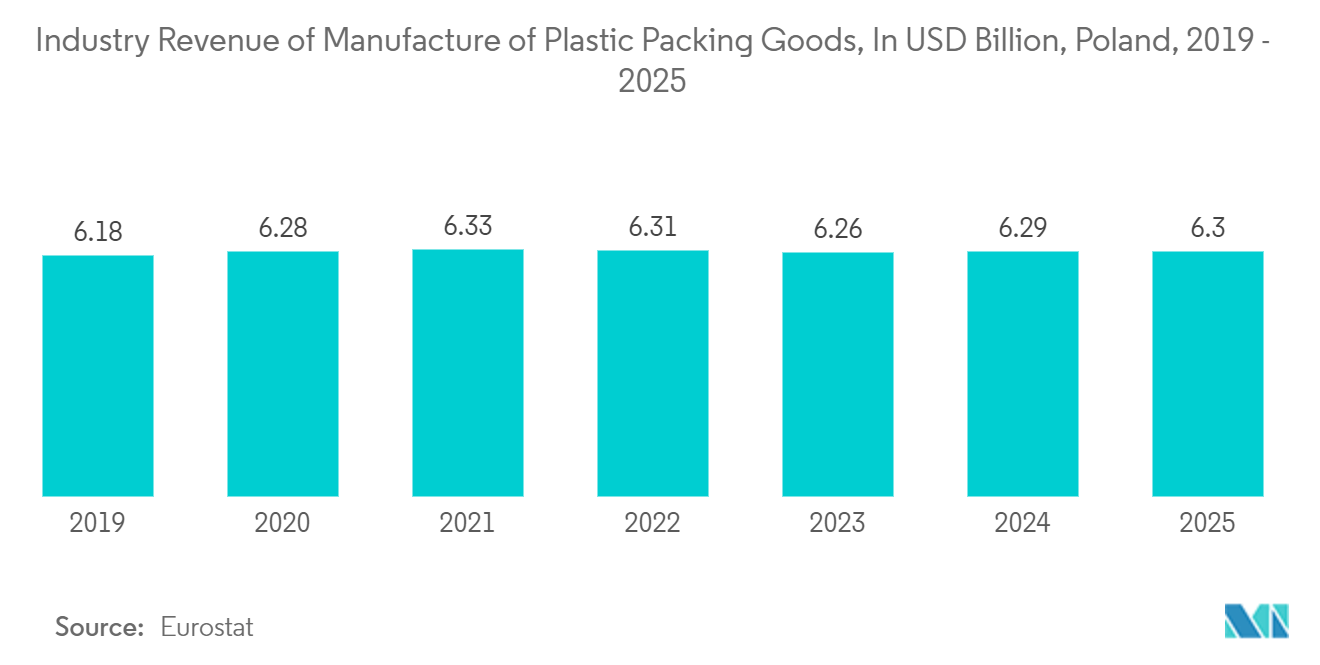

- According to Eurostat, the revenue from manufacturing plastic packing goods in Poland is projected to amount to approximately USD 6.29 billion by 2025. Increased production of plastic packaging goods in Poland will lead to better integration within the supply chain. This will result in more efficient manufacturing processes, reduced costs, and improved overall supply chain management, benefiting the entire European consumer packaging market.

Europe Consumer Packaging Industry Overview

The consumer packaging market in Europe is fragmented due to the presence of many vendors. This report offers information about the competitive environment among players in this market and analyzes key consumer packaging companies and their products.

- In April 2024, International Paper announced the acquisition of DS Smith to form a distinct corrugated packaging enterprise with a strong presence in North America and Europe. The agreement aims to create a company primarily generating revenue from environmentally friendly fiber-based packaging, constituting around 90% of its total revenue.

- In October 2023, Tetra Pak announced the introduction of a range of innovative postbiotic food solutions through its collaboration with AB Biotek Human Nutrition & Health. Postbiotics can be integrated with food processing in a powder form at the mixing stage of ultra-high temperature (UHT) products, such as beverages, dairy products, ice cream, and cheeses.

Europe Consumer Packaging Market Leaders

Huhtamaki Group

International Paper Company

Constantia Flexibles Group GmbH

Amcor Group GmbH

The Tetra Pak Group

*Disclaimer: Major Players sorted in no particular order

Europe Consumer Packaging Market News

- February 2024: Gerresheimer, an innovative systems and solutions provider and global partner for the pharma, biotech, and cosmetics industries, launched its sustainable packaging solution. This solution features the Gx Amsterdam glass jar paired with the bio-based forewood closure, chosen for an inventive cosmetic product by the German start-up 4peoplewhocare.

- February 2024: ProAmpac, a company specializing in flexible packaging and material sciences, launched a sustainable solution called 'ProActive Recyclable FibreSculpt' in Europe. This high-barrier fiber-based solution is tailored for various thermoforming applications and is for products like sliced cheese, chilled cooked meats, cold cuts, and fish.

- November 2023: A shrink film using recycled plastic material from waste fishing gear was developed by Duo, a packaging consultancy and manufacturer, with Danish recycling company Plastix. Duo is projected to use Plastix Oceanix's recycled plastic, which is 98% marine waste, such as fishing nets and ropes, to produce shrink film for the outer packaging of foodstuffs and beverages.

Europe Consumer Packaging Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increased Demand for Flexible Plastic Packaging Solutions Across End-user Industries

5.1.2 Growing Utilization of Distribution Channels such as Convenience Stores and E-commerce

5.2 Market Restraints

5.2.1 Increasing Price Volatility of Raw Materials

6. MARKET SEGMENTATION

6.1 Material

6.1.1 Plastic

6.1.1.1 Material Type

6.1.1.1.1 PE (Polyethylene)

6.1.1.1.2 PP (Polypropylene)

6.1.1.1.3 PVC (Poly Vinyl Chloride)

6.1.1.1.4 PET (Polyethylene Terephthalate)

6.1.1.1.5 Other Material Types

6.1.1.2 By Type

6.1.1.2.1 Rigid Plastic Packaging

6.1.1.2.2 Flexible Plastic Packaging

6.1.2 Paper

6.1.2.1 Type

6.1.2.1.1 Carton Board

6.1.2.1.2 Containerboard and Linerboard

6.1.2.1.3 Other Types

6.1.3 Glass

6.1.4 Metal

6.1.4.1 Type

6.1.4.1.1 Cans

6.1.4.1.2 Caps and Closures

6.1.4.1.3 Other Types

6.2 End-user Industry

6.2.1 Food

6.2.2 Beverage

6.2.3 Pharmaceutical and Healthcare

6.2.4 Cosmetics, Personal Care, and Household Care

6.3 Country***

6.3.1 United Kingdom

6.3.2 Germany

6.3.3 France

6.3.4 Italy

6.3.5 Poland

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 Huhtamaki Oyj

7.1.2 Amcor Group GmbH

7.1.3 The Tetra Pak Group

7.1.4 International Paper Company

7.1.5 Constantia Flexibles Group GmbH

7.1.6 Sealed Air Corporation

7.1.7 DS Smith PLC

7.1.8 Mondi Group

7.1.9 Ardagh Group

7.1.10 Crown Holdings Inc.

7.1.11 Massilly Holding SAS

7.1.12 Tubex GmbH

7.1.13 Owens-Illinois Inc.

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

Europe Consumer Packaging Industry Segmentation

The consumer packaging market refers to the industry that produces packaging materials and solutions for consumer goods. This market is crucial in protecting, preserving, and promoting products for sale and use. Consumer packaging encompasses a wide range of materials, including paper, cardboard, plastic, glass, and metal, which are used to create various types of packaging, such as boxes, bottles, cans, pouches, and more.

The consumer packaging market is segmented by material (plastic [material type {polyethylene, polypropylene, polyvinyl chloride, polyethylene terephthalate, other material types}], [type {rigid plastic packaging, flexible plastic packaging}], paper [type {carton board, containerboard, linerboard, and other types}], glass, and metal [type {cans, caps, and closures, other types}]), end-user industry (food, beverage, pharmaceutical and healthcare, and cosmetics, personal care, and household care), and country (United Kingdom, Germany, France, Italy, Poland, and Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Material | |||||||||||||

| |||||||||||||

| |||||||||||||

| Glass | |||||||||||||

|

| End-user Industry | |

| Food | |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Cosmetics, Personal Care, and Household Care |

| Country*** | |

| United Kingdom | |

| Germany | |

| France | |

| Italy | |

| Poland |

Europe Consumer Packaging Market Research FAQs

How big is the Europe Consumer Packaging Market?

The Europe Consumer Packaging Market size is expected to reach USD 168.84 billion in 2024 and grow at a CAGR of 4.07% to reach USD 206.11 billion by 2029.

What is the current Europe Consumer Packaging Market size?

In 2024, the Europe Consumer Packaging Market size is expected to reach USD 168.84 billion.

Who are the key players in Europe Consumer Packaging Market?

Huhtamaki Group, International Paper Company, Constantia Flexibles Group GmbH, Amcor Group GmbH and The Tetra Pak Group are the major companies operating in the Europe Consumer Packaging Market.

What years does this Europe Consumer Packaging Market cover, and what was the market size in 2023?

In 2023, the Europe Consumer Packaging Market size was estimated at USD 161.97 billion. The report covers the Europe Consumer Packaging Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Europe Consumer Packaging Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Consumer Packaging in Europe Industry Report

Statistics for the 2024 Consumer Packaging in Europe market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Consumer Packaging in Europe analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.