Data Center Liquid Cooling Market Size

| Study Period | 2019 - 2029 |

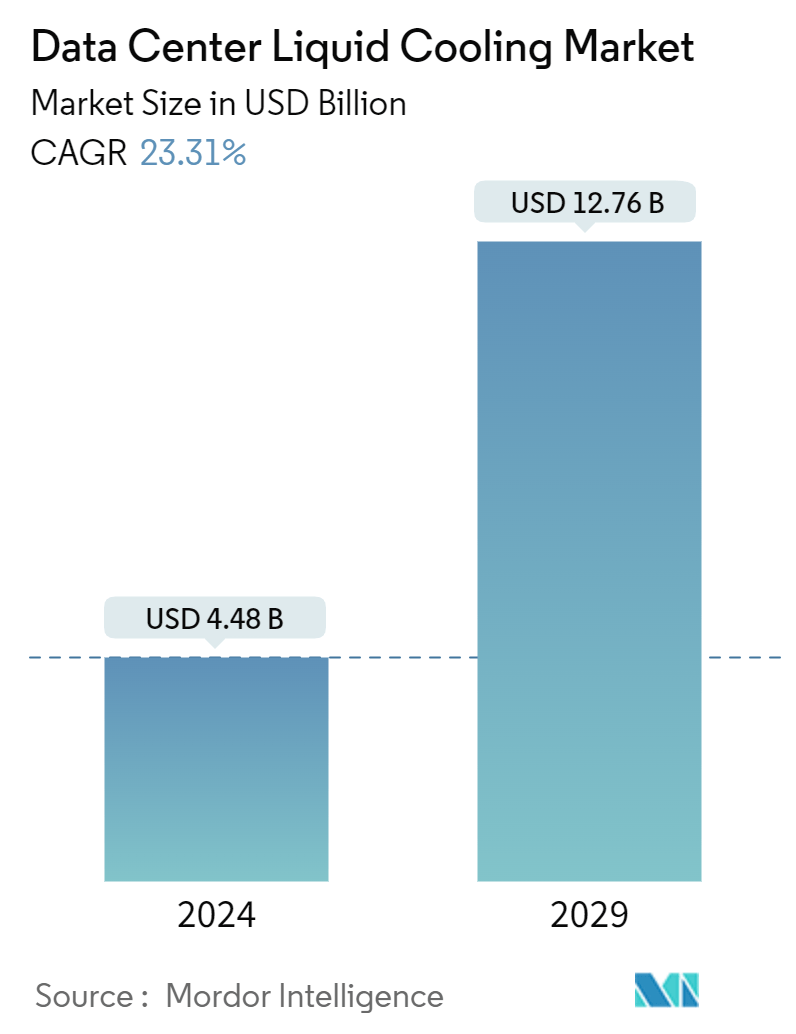

| Market Size (2024) | USD 4.48 Billion |

| Market Size (2029) | USD 12.76 Billion |

| CAGR (2024 - 2029) | 23.31 % |

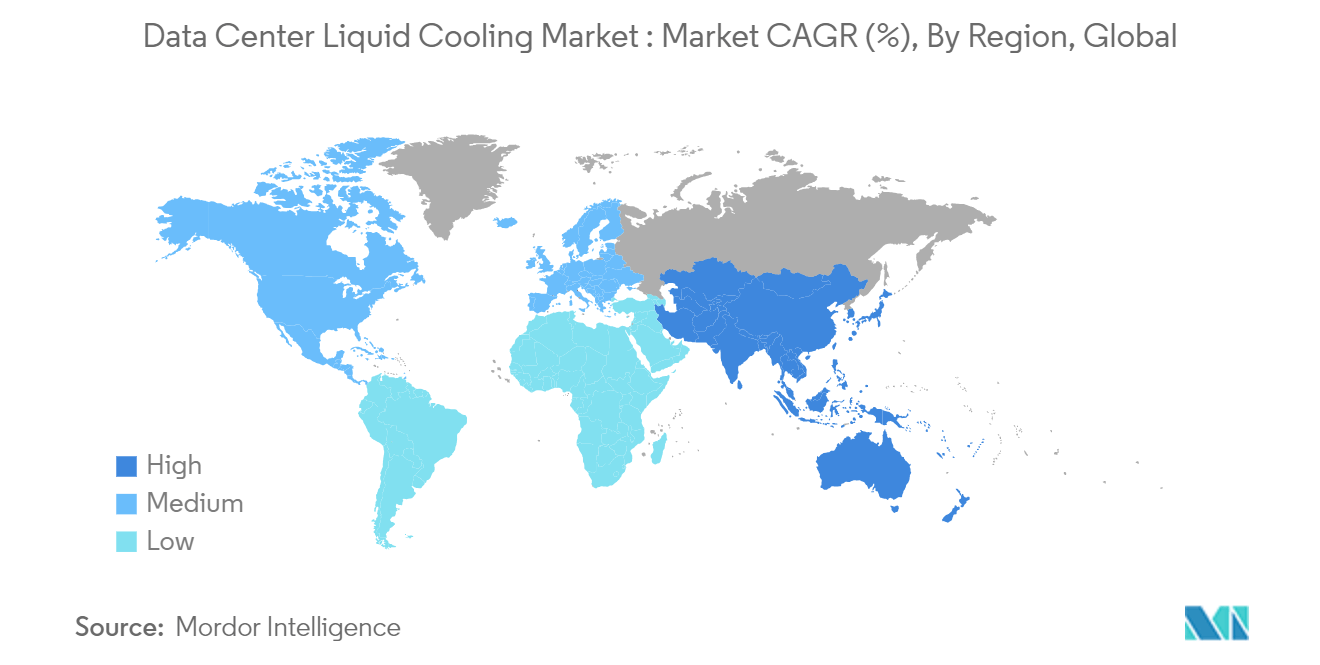

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Data Center Liquid Cooling Market Analysis

The Data Center Liquid Cooling Market size is estimated at USD 4.48 billion in 2024, and is expected to reach USD 12.76 billion by 2029, growing at a CAGR of 23.31% during the forecast period (2024-2029).

The need for data centers has grown as the population grows increasingly connected and dependent on digital infrastructure. Effective cooling solutions are urgently needed to ensure optimal performance and avoid expensive downtime due to the data center development and growth spike.

- Data center growth has been significantly aided by the uptake of cloud computing solutions and the spread of big data analytics. Businesses increasingly rely on cloud-based services and storing enormous amounts of data for processing and research. For instance, to meet the rising demand, cloud industry giants like Amazon Web Services (AWB), Microsoft Azure, and Google Cloud Platform continuously extend their data center footprints.

- Growing developments in IT infrastructure in emerging economies, such as India, Hong Kong, China, Indonesia, and other emerging countries, are likely to boost the demand for data centers. The demand for data centers is expected to increase due to the adoption of the cloud model, which has cost and operational benefits for the IT industry.

- Data center operators are wary of potential downtime losses while shifting to new cooling systems. Hence, they overlook operational expenditures and continue using outdated cooling systems. This trend slows the adoption of new technologies that are perceived to be untested.

- A new wave of post-pandemic digital transformation among businesses is expected to drive the market. Many companies have started to rely on third-party colocation facilities to house their data centers, and there’s a growing trend towards hybrid IT – combining the power of hosted centers with multi-cloud environments.

Data Center Liquid Cooling Market Trends

Edge Computing to Witness Significant Growth

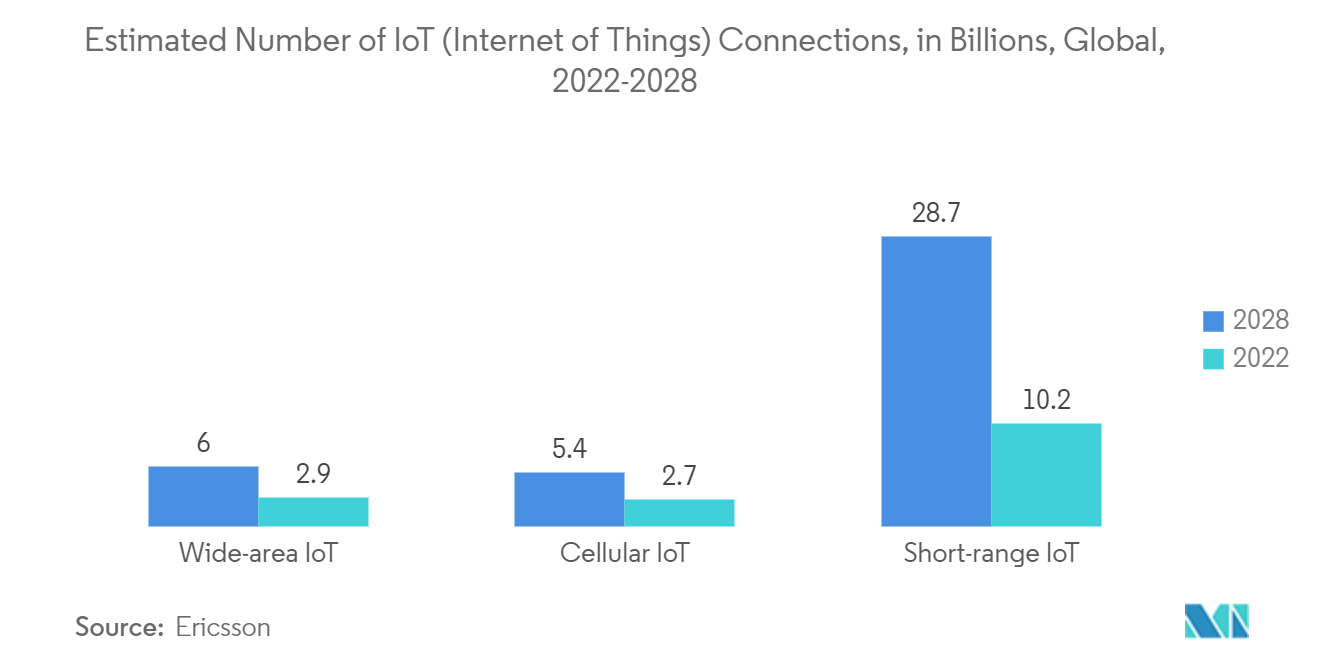

- In the forecast period, organizations are expected to witness rapid growth in the number of IP-connected mobile and machine-to-machine (M2M) devices, which will handle significant amounts of IP traffic.

- The demand is expected to rise for faster Wi-Fi service and application delivery from online providers. Also, some M2M devices, such as autonomous vehicles, will require real-time communications with local processing resources to guarantee safety.

- The deployment of edge data centers benefits many new technologies, including fifth-generation (5G) networks and the Internet of Things (IoT), as the adoption of (IoT) connections is expected to more than double, with the number of wide-area IoT 6 billion by 2028. and Industrial Internet of Things (IIoT) of devices, autonomous vehicles, virtual and augmented reality, artificial intelligence and machine learning, data analytics, and video streaming and surveillance.

- Moreover, the emergence of 5G wireless infrastructure has urged data center operators to opt for edge computing infrastructure to work with networks offering lower latency and higher resiliency. Multi-access edge computing (MEC) aids network services in connecting to users closely. Hence, the demand for efficient edge data centers is expected to be augmented by many factors, including the introduction of 5G technology across the world and the growing trend of autonomous or self-driving vehicles and smart cities.

- However, a key requirement of large-scale edge computing roll-outs will be low operating costs. In edge deployments, immersive liquid cooling is known to provide dramatic energy-saving benefits.

- The reliability and no-touch features of liquid cooling solutions will match the need for extended mean time to maintenance and longer intervention intervals needed for viable operation and management of remotely located equipment.

North America to Hold the Largest Market Share

- North America is an early adopter of newer technologies. The data center investors are increasingly investing in liquid immersion and direct-to-chip cooling solutions. The importance of edge data centers has been aided by the emergence of 5G networks worldwide, and the United States is among the earliest adopters of the technology. Many operators in the United States, such as EdgePresence, EdgeMicro, and American Towers, have started investing in these centers.

- The mobile data traffic in the United States increased considerably over the years, from 1.26 exabytes per month of data traffic in 2017 to 7.75 exabytes per month of data traffic by 2022, as reported by Cisco Systems. Ericsson says this data traffic is expected to triple further by 2030. Thus, the distributed cloud that may secure the low latency and high bandwidth required to connect such scale easily is coming into action.

- The United States is witnessing massive growth in internet usage by people and businesses. The country is the largest market in data center operations, and it continues to grow due to the higher consumption of data by end-users. The growing popularity of the Internet of Things (IoT) is a significant driver for the US hyper-scale data center market, leading to additional facilities that can support exabytes of data generated by both business users and consumers.

- The United States will be the fastest-growing data center market in the region in the coming years. The significant drivers of data center construction in the United States. have been recent economic incentives and tax benefits. Approximately 27 states leverage these factors to attract data center projects. In addition, the heavy tax breaks implemented in the United States indicate a government-front aim to construct new mega data centers or renovate existing ones. Such instances in the market create more of a need for data center liquid cooling services in the region.

Data Center Liquid Cooling Industry Overview

The data center liquid cooling market is fragmented and highly competitive and consists of several significant players like Alfa Laval Corporate AB, LiquidStack Inc., Asetek Inc. A/S, AsperitasChilldyne Inc., etc. In terms of market share, few important players currently dominate the market. The widely deployed cooling system is still air cooling, and liquid cooling systems have a relatively small share in the overall cooling landscape. As relatively high costs are considered market challenges, the immersion cooling systems market is estimated to have a significant threat of substitutes.

- March 2024 - Summer announced its membership in the recently established Liquid Cooling Coalition (LCC), a premier industry forum comprised of stakeholders, including industrial coolant producers, original equipment manufacturers, original device manufacturers, high-performance computing application operators, and data center providers.

- March 2024 - Vertiv, a significant provider of critical infrastructure and continuity solutions, is now a Solution Advisor: Consultant partner in the Nvidia Partner Network (NPN), providing more comprehensive access to Vertiv’s experience and complete power and cooling solutions portfolio.

Data Center Liquid Cooling Market Leaders

Alfa Laval Corporate AB

LiquidStack Inc.

Asetek Inc. A/S

Asperitas

Chilldyne Inc.

*Disclaimer: Major Players sorted in no particular order

Data Center Liquid Cooling Market News

- April 2024 - Mitsubishi Electric Corporation announced that its wholly owned subsidiaries Mitsubishi Electric Hydronics & IT Cooling Systems S.p.A. and Mitsubishi Electric Europe B.V. acquired AIRCALO, an air-conditioning company in France. Going forward, Mitsubishi Electric expects to expand and upgrade its hydronic HVAC systems business in the diversifying European market.

- October 2023 - Intel and Submer collaborated to establish a formidable foundation for single-phase immersion technology, which achieved a groundbreaking advancement in the form of the Forced Convection Heat Sink (FCHS) package. Set to revolutionize data center cooling, the FCHS reduces the quantity and cost of components required for comprehensive heat capture and the dissipation of chips with Thermal Design Power (TDP) exceeding 1,000 W.

Data Center Liquid Cooling Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Evolution Of Data Center Cooling

4.1.1 Air Conditioners/Handlers

4.1.2 Chillers And Economizer Systems

4.1.3 Liquid Cooling Systems

4.1.4 Row/Rack/Ddoor/Over-head Cooling Systems

4.2 Overview of Data Center Cooling Market

4.3 Energy Consumption, Computing Density Metrics and Key Considerations For Liquid Cooling

4.4 Industry Stakeholder Analysis

4.5 Industry Attractiveness - Porter's Five Forces Analysis

4.5.1 Bargaining Power of Buyers

4.5.2 Bargaining Power of Suppliers

4.5.3 Threat of New Entrants

4.5.4 Degree of Competition

4.5.5 Threat of Substitutes

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Development of IT Infrastructure in the Region

5.1.2 Emergence of Green Data Centers

5.2 Market Restraints

5.2.1 Costs, Adaptability Requirements, and Power Outages

5.3 Assessment of COVID-19 Impact on the Industry

6. OUTLOOK OF REAR DOOR HEAT EXCHANGERS (RDHX) IN DATA CENTERS

6.1 Technical Comparison of RDHx and Liquid Cooling (Direct and Indirect) in Data Centers

6.2 Recent Developments by Data Center Cooling Technology Vendors in the Context Of RDHx and Liquid Cooling Market

6.3 Approximate Global Market Share of RDHx (in USD Billion)

6.4 List of Key RDHx Vendors (Business Overview, Portfolio and Recent Developments)

7. DIRECT COOLING OR IMMERSION COOLING MARKET

7.1 Direct Cooling Market Overview And Estimate

7.2 Immersion Cooling - Key Application

7.2.1 High-performance Computing

7.2.2 Edge Computing

7.2.3 Cryptocurrency Mining

7.3 Immersion Cooling Fluids

7.3.1 Fluorocarbon-based Fluids

7.3.2 Hydrocarbons Fluids

8. INDIRECT OR DIRECT-TO-CHIP COOLING MARKET

8.1 Indirect Cooling Market Overview and Estimates

8.2 Indirect or Direct-to-chip Cooling Key Applications

9. MARKET SEGMENTATION

9.1 By Geography***

9.1.1 North America

9.1.2 Europe

9.1.3 Asia

9.1.4 Australia and New Zealand

9.1.5 Latin America

9.1.6 Middle East and Africa

10. COMPETITIVE LANDSCAPE

10.1 Company Profiles*

10.1.1 Alfa Laval Corporate AB

10.1.2 LiquidStack Inc.

10.1.3 Asetek Inc. A/S

10.1.4 Asperitas

10.1.5 Chilldyne Inc.

10.1.6 CoolIT Systems Inc.

10.1.7 Fujitsu Ltd.

10.1.8 Mikros Technologies

10.1.9 Kaori Heat Treatment Co. Ltd

10.1.10 Lenovo Group Limited

10.1.11 LiquidCool Solutions Inc.

10.1.12 Midas Green Technologies

10.1.13 Iceotope Technologies Ltd

10.1.14 USystems Ltd (Legrand Group)

10.1.15 Rittal GmbH & Co. KG

10.1.16 Schneider Electric

10.1.17 Submer Technologies & Submer Inc.

10.1.18 Vertiv Group Corp.

10.1.19 Wakefield Thermal Solutions Inc.

10.1.20 Wiwynn Corporation

10.1.21 3M Company

10.1.22 Engineered Fluids Inc.

10.1.23 Green Revolution Cooling Inc.

10.1.24 Solvay SA

11. COOLING TECHNOLOGY INNOVATIONS ACROSS THE VALUE CHAIN

12. INVESTMENT ANALYSIS AND MARKET OUTLOOK

Data Center Liquid Cooling Industry Segmentation

Data center liquid cooling involves the installation of IT hardware, such as memory, drives, and CPUs, directly into non-conductive dielectric liquids, which cool the system. The heat generated from these systems is directly transferred to coolants, reducing the need for active cooling components, such as heat sinks, fans, and interface materials commonly used for air cooling.

The data center liquid cooling market is segmented by type (indirect or direct-to-chip cooling, direct cooling or immersion cooling, rare door heat exchanger), application (high-performance computing, edge computing, cryptocurrency mining), and geography (North America, Europe, Asia-Pacific, and Rest of the World). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| By Geography*** | |

| North America | |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Data Center Liquid Cooling Market Research FAQs

How big is the Data Center Liquid Cooling Market?

The Data Center Liquid Cooling Market size is expected to reach USD 4.48 billion in 2024 and grow at a CAGR of 23.31% to reach USD 12.76 billion by 2029.

What is the current Data Center Liquid Cooling Market size?

In 2024, the Data Center Liquid Cooling Market size is expected to reach USD 4.48 billion.

Who are the key players in Data Center Liquid Cooling Market?

Alfa Laval Corporate AB, LiquidStack Inc., Asetek Inc. A/S, Asperitas and Chilldyne Inc. are the major companies operating in the Data Center Liquid Cooling Market.

Which is the fastest growing region in Data Center Liquid Cooling Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Data Center Liquid Cooling Market?

In 2024, the North America accounts for the largest market share in Data Center Liquid Cooling Market.

What years does this Data Center Liquid Cooling Market cover, and what was the market size in 2023?

In 2023, the Data Center Liquid Cooling Market size was estimated at USD 3.44 billion. The report covers the Data Center Liquid Cooling Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Data Center Liquid Cooling Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Data Center Liquid Cooling Industry Report

Statistics for the 2024 Data Center Liquid Cooling market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Data Center Liquid Cooling analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.