Consumer Goods and Services

29th JulyUnlocking Growth in India’s Luxury Beauty & Skincare Market

3 Min Read

The Sweden Cosmetics Market Report is Segmented by Product Type (Facial Make-Up, Eye Make-Up, Lip and Nail Make-Up Products), Category (Mass, Premium), Distribution Channel (Supermarkets/Hypermarkets, Specialty Beauty Stores, Online Retail Stores, Others), Ingredient Type (Conventional, Natural/Organic), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

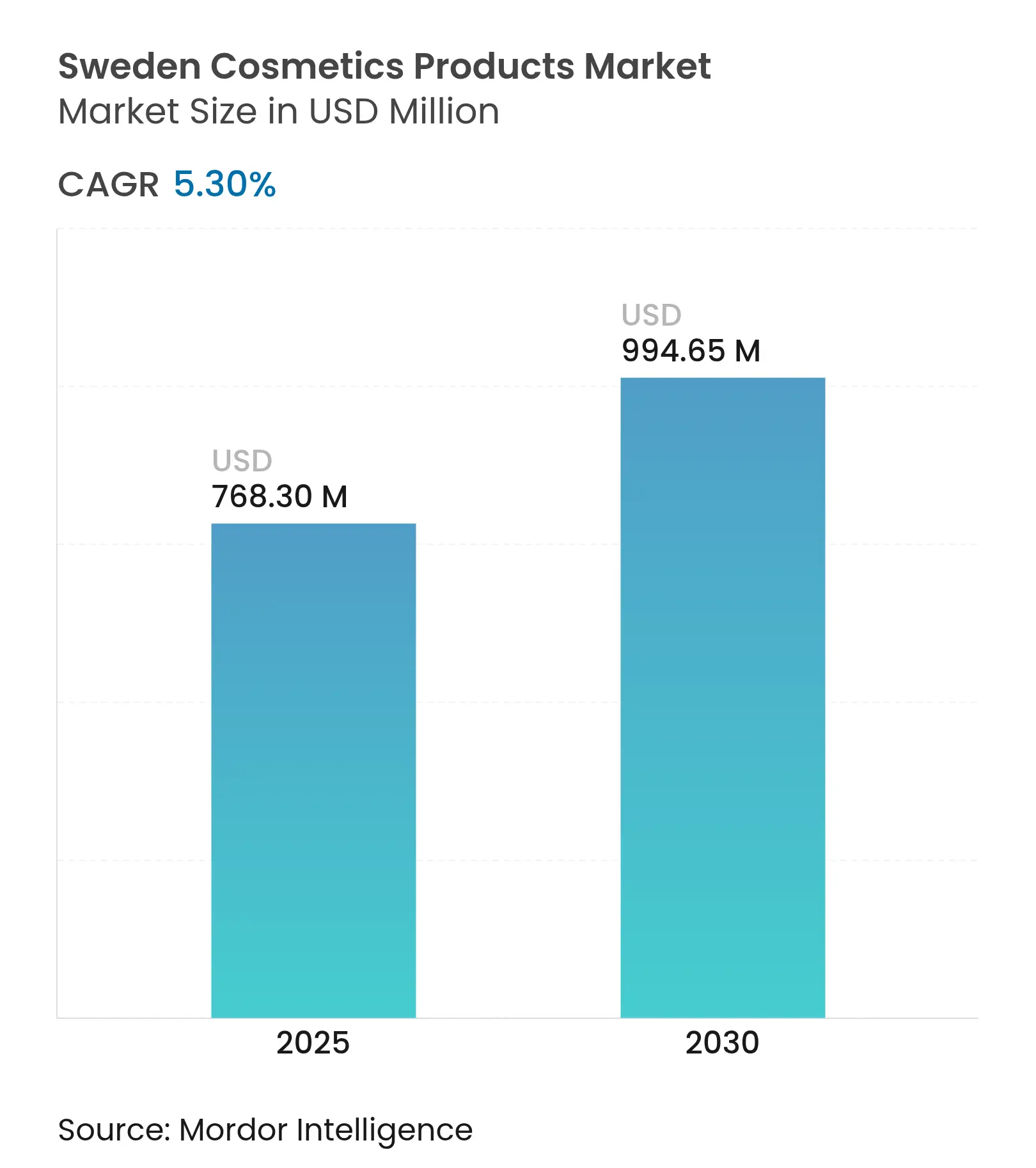

| Market Size (2025) | USD 768.30 Million |

| Market Size (2030) | USD 994.65 Million |

| Growth Rate (2025 - 2030) | 5.30 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Sweden cosmetics market size stood at USD 768.3 million in 2025 and is forecast to advance to USD 994.65 million by 2030, expanding at a 5.30% CAGR over the period. Elevated demand for premium, clean-label formulations, steady male-grooming uptake, and rapid digital commerce adoption keep growth momentum intact despite higher household debt servicing costs and EU packaging-rule compliance expenses. Sustainability imperatives encourage brands to replace fossil-based ingredients with marine- and plant-derived alternatives, while specialty retailers strengthen loyalty programs to offset online channel gains. Tight regulation remains a dual force—raising operating costs but protecting brand trust—so companies that harmonize innovation with compliance secure competitive advantages. Currency volatility, coupled with inflation-linked import costs, further differentiates locally manufactured offerings that minimize exposure to the SEK’s swings.

Key Report Takeaways

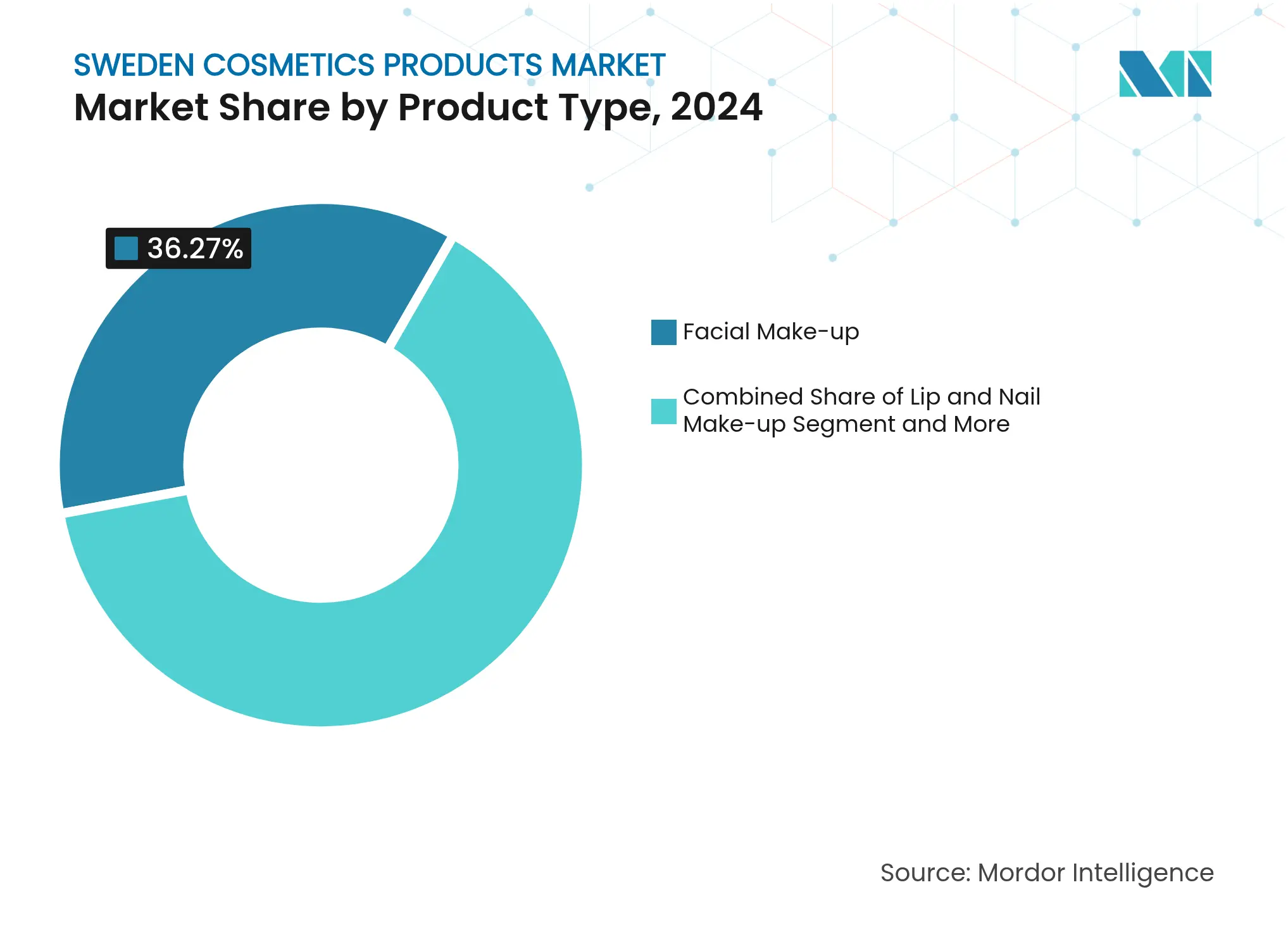

By product type, facial makeup led with 36.27% of the Sweden cosmetics market share in 2024, while lip and nail makeup products are projected to record a 6.30% CAGR through 2030.

By category, mass products captured 67.84% revenue share in 2024; premium items are poised to grow at a 7.12% CAGR to 2030.

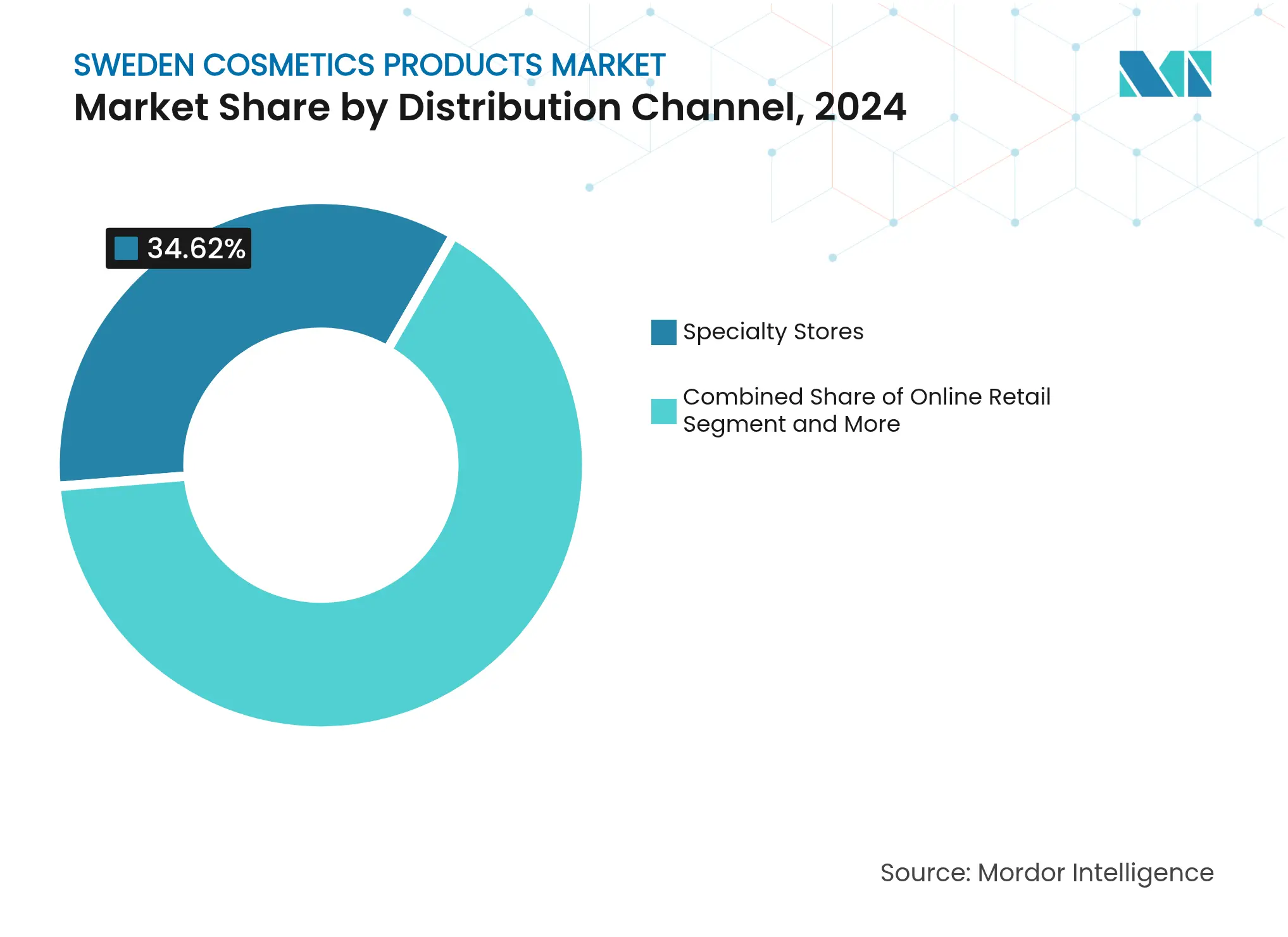

By distribution channel, specialty beauty stores held 34.62% share of the Sweden cosmetics market size in 2024, whereas online retail is expected to post an 8.13% CAGR during the forecast window.

By ingredient type, conventional components accounted for 81.73% share in 2024 and natural/organic ingredients are on track for a 7.81% CAGR through 2030.

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Premium- and clean-beauty appetite surge

Premium- and clean-beauty appetite surge

| +1.2% | National, with early gains in Stockholm, Göteborg, Malmö | Medium term (2-4 years) |

% Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

National, with early gains in Stockholm, Göteborg, Malmö

|

Impact Timeline

:

Medium term (2-4 years)

|

Technological advancements in product formulations

Technological advancements in product formulations

| +0.8% | National, with R&D concentration in Stockholm region | Long term (≥ 4 years) | |||

EU-led sustainable-packaging push

EU-led sustainable-packaging push

| +0.7% | EU-wide, with Sweden as early adopter | Medium term (2-4 years) | |||

Male-grooming adoption in middle-aged Swedes

Male-grooming adoption in middle-aged Swedes

| +0.6% | National, with urban concentration | Short term (≤ 2 years) | |||

Stockholm refill-infrastructure pilots

Stockholm refill-infrastructure pilots

| +0.4% | Regional, Stockholm metropolitan area | Medium term (2-4 years) | |||

Tax-rebate incentive for "low-hazard" chemical

profiles

Tax-rebate incentive for "low-hazard" chemical

profiles

| +0.3% | National | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Premium- and Clean-Beauty Appetite Surge

Swedish consumers increasingly prioritize premium formulations with transparent ingredient lists, driving market premiumization despite macroeconomic headwinds that typically constrain discretionary spending. This trend manifests through Nordic Swan Ecolabel adoption, where cosmetic product criteria were updated in November 2024 to exclude synthetic polymer microparticles and strengthen restrictions on environmentally hazardous substances. The appetite surge reflects broader Scandinavian values alignment between personal care choices and environmental consciousness, creating sustainable competitive advantages for brands that authentically integrate clean beauty positioning with functional performance. IDUN Minerals exemplifies this positioning, achieving Nordic Swan certification while maintaining dermatologist-recommended formulations for sensitive skin types. Premium segment acceleration at 7.12% CAGR through 2030 indicates this trend's durability beyond economic cycles, supported by Swedish consumers' willingness to pay price premiums for verified sustainability claims and locally-produced alternatives.

Technological Advancements in Product Formulations

Innovation in cosmetic formulations accelerates through Swedish biotechnology developments, particularly in marine-derived ingredients and upcycled materials that address both performance and sustainability requirements. Swedish Algae Factory's commercial-scale production of Algica represents a breakthrough in diatom-based cosmetic ingredients, offering light-altering properties, SPF enhancement, and controlled-release capabilities while maintaining COSMOS approval for natural cosmetics. Research at KTH Royal Institute of Technology demonstrates parallel innovation in plant-based pigments, with KAFFAGE coffee by-product materials achieving comparable coverage to synthetic alternatives while providing additional skincare benefits including antioxidant capacity and anti-glycation properties. These technological advances position Swedish companies at the forefront of next-generation cosmetic ingredients that satisfy both regulatory requirements and consumer preferences for natural, multifunctional formulations. Disruptive Materials' Upsalite technology further exemplifies Swedish innovation leadership, winning the 2024 Maverick Influencer Ingredient Award while providing simultaneous absorption of lipophilic and hydrophilic substances for improved cosmetic performance.

EU-led Sustainable-Packaging Push

The EU Packaging and Packaging Waste Regulation, entering force in February 2025 with application beginning August 2026, fundamentally reshapes cosmetic packaging requirements across Sweden. Mandatory recyclability standards, minimum recycled content targets, and extended producer responsibility obligations create compliance costs while driving innovation in sustainable packaging solutions. Swedish companies gain competitive advantages through early adoption of circular packaging designs, as demonstrated by På(fyll)'s Nordic collaborative reusable packaging service that enables subscription-based refill models for household and personal care products. The regulatory push coincides with EU Directive 2024/825 on misleading green claims, which prohibits self-created sustainability labels and requires third-party verification for environmental claims, eliminating greenwashing opportunities while rewarding authentic sustainability investments. Billerud's Swedish cartonboard production capacity expansion, including the KM7 machine ramp-up at Gruvön, positions domestic suppliers to meet increased demand for recyclable premium packaging materials.

Male-Grooming Adoption in Middle-aged Swedes

Male skincare engagement accelerates among Swedish men aged 35-55, driven by increased health consciousness and reduced stigma around male beauty routines. Apotek Hjärtat's January 2025 survey revealed that 19% of Swedish men actively attend to skin health, though 29% report low knowledge of proper skincare routines, rising to 37% among men aged 18-29. This knowledge gap creates market opportunities for brands offering simplified, education-focused male grooming solutions, as evidenced by Mr Bear Family's success with natural ingredient formulations and affordable luxury positioning from its Gothenburg base. The demographic shift reflects broader Nordic masculinity evolution, where self-care practices gain social acceptance while maintaining practical, no-nonsense approaches that align with Swedish cultural values. Middle-aged male adoption particularly drives premium segment growth, as this demographic possesses higher disposable income and willingness to invest in quality formulations that address age-related skin concerns without complex multi-step routines.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Tight EU/Swedish chemical-safety rules

Tight EU/Swedish chemical-safety rules

| -0.9% | EU-wide, with Sweden as strict enforcer | Long term (≥ 4 years) |

% Impact on CAGR Forecast

:

-0.9%

|

Geographic Relevance

:

EU-wide, with Sweden as strict enforcer

|

Impact Timeline

:

Long term (≥ 4 years)

|

Import-cost inflation & SEK volatility

Import-cost inflation & SEK volatility

| -1.1% | National, affecting international brands | Short term (≤ 2 years) | |||

Second-hand beauty swap groups cannibalising sales

Second-hand beauty swap groups cannibalising sales

| -0.3% | Urban areas, particularly Stockholm region | Medium term (2-4 years) | |||

Rising concerns over counterfeit products

Rising concerns over counterfeit products

| -0.4% | National, with online channel concentration | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Tight EU/Swedish Chemical-Safety Rules

Sweden's stringent implementation of EU cosmetics regulations, combined with national restrictions like the microplastics ban enforced by the Swedish Chemicals Agency (KEMI), creates compliance burdens that particularly impact smaller brands and international entrants. The Swedish microplastics prohibition covers all plastic particles under 5mm in cleansing, peeling, or polishing products, with no lower size limit, requiring comprehensive reformulation for affected products. EU Regulation 1223/2009 mandates extensive safety assessments, Product Information Files, and Cosmetic Product Notification Portal submissions, while Swedish language labeling requirements add localization costs for international brands. The regulatory complexity intensifies through EU Urban Wastewater Treatment Directive 2024/3019, requiring cosmetics producers to bear 80% of quaternary treatment costs for micropollutant removal by 2028, adding operational expenses that may discourage market entry.

Import-Cost Inflation & SEK Volatility

Currency fluctuations and elevated import duties create margin pressures for international cosmetics brands, particularly those sourcing from non-EU markets where Swedish customs imposes 25% VAT plus potential customs duties up to 20% on goods exceeding SEK 1,800 value. The Riksbank's analysis of US trade tariff impacts highlights Sweden's export vulnerability, with potential 16% decline in exports under blanket tariff scenarios, while retaliatory measures could affect kaolin clay imports essential for cosmetics manufacturing. IMF projections show Swedish household debt servicing costs rising from under 4% of disposable income in 2021 to approximately 8% by late 2023, constraining discretionary spending on premium cosmetics while elevated borrowing costs reduce business investment in inventory and expansion. These macroeconomic pressures particularly impact specialty retailers and premium brands that rely on imported ingredients or finished products, creating competitive advantages for domestic manufacturers with local supply chains.

By Product Type: Facial Makeup Dominance Meets Lip Innovation

Facial makeup maintains market leadership with 36.27% share in 2024, driven by Swedish consumers' preference for natural-finish foundations and multi-functional products that align with minimalist Nordic beauty aesthetics. The segment benefits from IsaDora's consumer-involvement initiatives, including focus groups at their Malmö headquarters that expanded shade ranges for Wake Up the Glow Luminous Foundation to address undertone diversity and broader skin tone spectrum needs. Swedish Algae Factory's Algica technology integration into facial products provides SPF-boosting properties and light-scattering effects that enhance coverage while maintaining clean beauty credentials, supporting premium segment growth within facial makeup categories.

Lip and nail makeup products emerge as the fastest-growing segment at 6.30% CAGR through 2030, reflecting increased emphasis on statement colors and long-wearing formulations that withstand Sweden's climate conditions. The Body Shop's expansion of refillable Peptalk Lipstick collections in aluminum cases demonstrates market appetite for sustainable lip products, while nail polish innovations focus on quick-dry formulations and chip-resistant technologies that appeal to active Swedish lifestyles. Eye makeup and other facial categories maintain steady growth through technological advances in waterproof formulations and sensitive-skin compatibility, supported by IDUN Minerals' dermatologist-recommended approach and Nordic Swan certification that validates ingredient safety claims.

Note: Segment shares of all individual segments available upon report purchase

By Category: Mass Market Stability Versus Premium Acceleration

Mass category products command 67.84% market share in 2024, reflecting Swedish consumers' value-conscious approach to everyday beauty essentials and the strong presence of accessible brands through KICKS Group's extensive retail network of over 250 Nordic stores. The mass segment's stability stems from established distribution relationships and consumer loyalty to functional products that deliver reliable performance at accessible price points, particularly in basic skincare and color cosmetics categories where brand switching costs remain low.

Premium categories accelerate at 7.12% CAGR through 2030, driven by Swedish consumers' increasing willingness to invest in verified clean beauty formulations and sustainable packaging innovations. CAIA Cosmetics' flagship store opening on Stockholm's Biblioteksgatan exemplifies premium segment expansion, offering experiential retail with Beauty Sessions priced at SEK 650-1,100 that combine product education with personalized application services. The premium acceleration reflects broader Nordic trends toward conscious consumption, where higher price points signal quality, sustainability, and ethical production practices that align with Swedish values. Luxury segment growth benefits from international brands' recognition of Swedish consumers' sophisticated beauty knowledge and willingness to pay premiums for innovative formulations, sustainable packaging, and cruelty-free certifications that meet Nordic ethical standards.

By Distribution Channel: Specialty Expertise Meets Digital Convenience

Online retail emerges as the fastest-growing distribution channel at 8.13% CAGR through 2030, accelerated by enhanced logistics capabilities and sustainability initiatives like fossil-free delivery options pioneered by Lyko Group's Swedish operations. Lyko's transition to exclusively fossil-free delivery in February 2022 influenced transport providers including PostNord to develop sustainable services, demonstrating how market leaders can drive industry-wide environmental improvements while maintaining customer satisfaction. The channel's growth benefits from Swedish consumers' high digital adoption rates and preference for convenient, information-rich shopping experiences that enable ingredient research and review consultation before purchase decisions.

Specialty stores maintain 34.62% market share in 2024 through expert consultation services and experiential retail formats that online channels cannot replicate. KICKS Group's integration of Skincity's professional skincare expertise into its retail operations demonstrates how specialty retailers adapt by enhancing service offerings and expanding into higher-margin categories that benefit from in-person consultation. The channel's resilience stems from Swedish consumers' appreciation for knowledgeable beauty advisors and the tactile evaluation opportunities that remain essential for color matching and texture assessment. Supermarkets and hypermarkets serve convenience-driven purchases, while other channels including pharmacies gain importance for sensitive skin and dermatologically-tested products that benefit from healthcare-adjacent positioning and professional recommendations.

Note: Segment shares of all individual segments available upon report purchase

By Ingredient Type: Conventional Foundation Supports Natural Growth

Natural and organic ingredients represent the fastest-growing segment at 7.81% CAGR through 2030, driven by Swedish consumers' environmental consciousness and regulatory support through Nordic Swan Ecolabel criteria that favor naturally-derived formulations. The segment benefits from domestic innovation in marine-derived ingredients like Swedish Algae Factory's Algica and plant-based alternatives like KAFFAGE coffee by-products that provide functional benefits while meeting clean beauty requirements. Nordic Swan guidance emphasizes life-cycle environmental assessment over origin-based classifications, encouraging ingredient selection based on overall environmental footprint rather than natural versus synthetic distinctions.

Conventional ingredients maintain 81.73% market share in 2024, providing the formulation foundation and performance reliability that enable natural ingredient integration without compromising product efficacy. The segment's dominance reflects the technical challenges of achieving desired sensory properties, stability, and safety profiles using exclusively natural ingredients, particularly in color cosmetics and long-wearing formulations where synthetic components remain essential for performance. Conventional ingredients benefit from established supply chains, regulatory approval histories, and cost advantages that support mass market accessibility while natural alternatives gradually gain market share through premium positioning and sustainability-focused consumer segments. The coexistence of conventional and natural ingredients within formulations allows brands to optimize performance while incrementally increasing natural content percentages as technology advances and consumer acceptance grows.

Sweden's cosmetics market revenue is predominantly driven by Stockholm, Göteborg, and Malmö, thanks to their dense populations, robust spending power, and extensive retail presence. In Stockholm, product-development labs and refill pilot hubs thrive, attracting an early adopter clientele eager for circular trials like På(fyll). Additionally, luxury department stores, strategically located near the capital's cultural districts, benefit from a steady influx of tourist purchases. Göteborg, with its port and manufacturing legacy, is home to firms like Mr Bear Family and Swedish Algae Factory. These companies leverage their closeness to maritime research clusters and export logistics corridors. Meanwhile, Malmö, acting as a conduit to continental Europe, not only streamlines cross-border e-commerce but also offers diverse consumer panels essential for validating shade ranges. Even smaller secondary cities contribute, hosting localized specialty retail and pop-up events that keep brand awareness alive outside the major metros.

Owing to Nordic integration, retailers like KICKS and Lyko can utilize shared warehousing across Sweden, Norway, and Finland, optimizing their inventory and logistics. Yet, distinct national characteristics remain; for instance, Swedish consumers are more receptive to refill schemes and tax rebates on low-hazard chemicals compared to their Danish counterparts, shaping product assortments. While EU's cross-border regulatory alignment eases compliance for Nordic product launches, the varying recycling infrastructures necessitate customized packaging formats for each market.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Market Concentration

In Sweden's cosmetics market, a moderate consolidation level of 6/10 sees global giants mingling with nimble domestic players. L’Oréal taps into KICKS for extensive distribution, while Estée Lauder capitalizes on travel-retail avenues, recently bolstered by Rituals’ debut standalone airport outlet in Sweden. KICKS’s loyalty app adeptly analyzes consumer behavior, predicting replenishment cycles and enhancing supplier trade negotiations. New entrants carve a niche through deep-rooted sustainability and direct storytelling. CAIA, riding on influencer endorsements, quickly gained national traction. Meanwhile, NOOMI Stockholm’s innovative waterless serums cater to carry-on liquid restrictions, appealing to jet-setters. Tech collaborations are on the rise: IsaDora has woven in Bower’s AI recycling feature, allowing shoppers to earn rewards by scanning empty containers, thus marrying brand loyalty with eco-conscious waste sorting.

In a bid to stay competitive, multinationals are localizing their R&D efforts. Unilever, for instance, is trialing Scandinavian fragrance variants with a focus on reduced allergens. Exclusive retail agreements are heating up: Lyko clinches online first-to-market rights for select Estée Lauder brands, while KICKS locks in exclusivity for Swedish Algae Factory’s enhanced products in brick-and-mortar outlets. Brands lacking credible eco-certifications face potential shelf removal, as Swedish retailers uphold a commitment to scientifically validated sustainability benchmarks.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

Cosmetics are mixtures of chemical compounds derived from either natural sources or synthetic ones. Cosmetics have various purposes such as those designed for personal and skin care is used to cleanse or protect the body or skin.

The Sweden cosmetics products market is segmented by product type, category, and distribution channel. Based on product type, the market is segmented into color cosmetics and hair styling and coloring products. The color cosmetics segment is further segmented into facial make-up products, face bronzers, and lipstick products. The hair styling and coloring products segment is further segmented into hair colors and styling products. Based on category, the market is segmented into mass and premium. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, pharmacy and drug stores, convenience/grocery stores, online retail stores, and other distribution channels.

The report offers market size and forecasts for the cosmetics products market in value (USD million) for all the above segments.

Unlocking Growth in India’s Luxury Beauty & Skincare Market

3 Min Read

Unlocking Opportunities in the Headwear Market

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.