Market Overview

| Study Period | 2019 - 2030 |

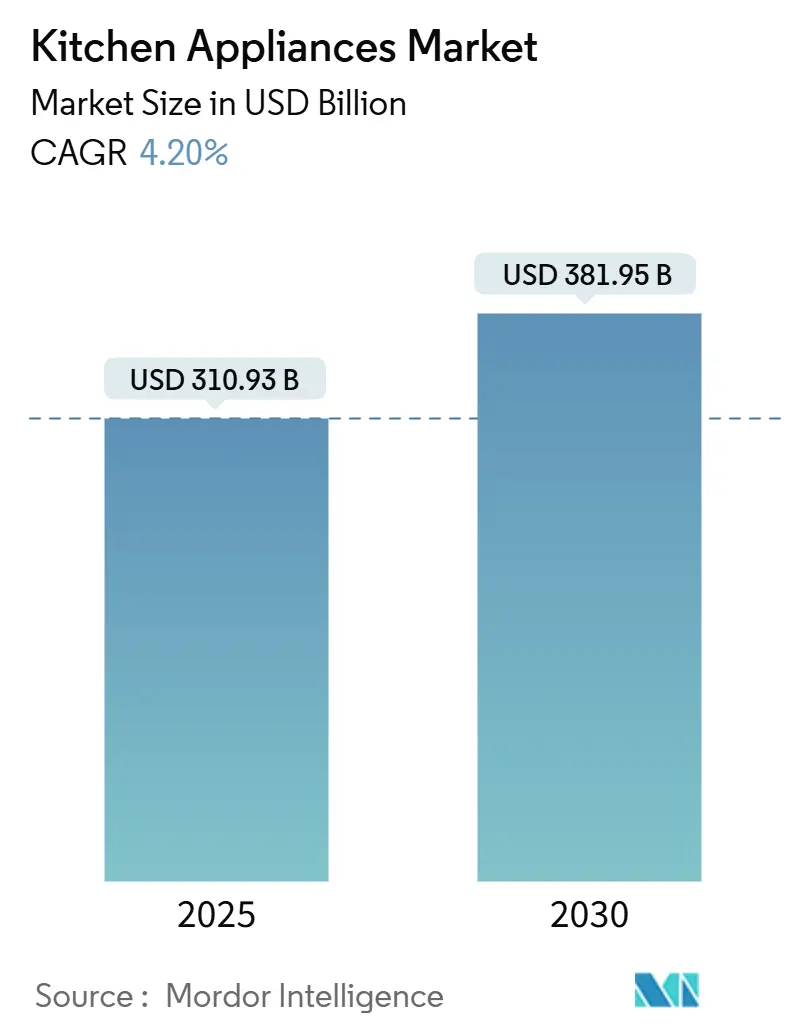

| Market Size (2025) | USD 310.93 Billion |

| Market Size (2030) | USD 381.95 Billion |

| Growth Rate (2025 - 2030) | 4.20% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Kitchen Appliances Market Analysis by Mordor Intelligence

The Kitchen Appliances Market size is estimated at USD 310.93 billion in 2025, and is expected to reach USD 381.95 billion by 2030, at a CAGR of 4.20% during the forecast period (2025-2030). The measured pace signals a sector that now grows more through replacement cycles than new household formation, yet product innovation keeps demand steady. Regulations that tighten energy-use thresholds, especially in the United States and European Union, stimulate early replacements as consumers seek compliant models. Urbanization, rising single-person households, and an appetite for compact multifunctional designs keep unit volumes healthy in space-constrained cities. At the same time, embedded carbon labels and smart-home integration allow manufacturers to command premium pricing, even as they face cost pressure from supply-chain uncertainty and rising competition. Together, these forces shape a resilient, innovation-driven kitchen appliances market.

Key Report Takeaways

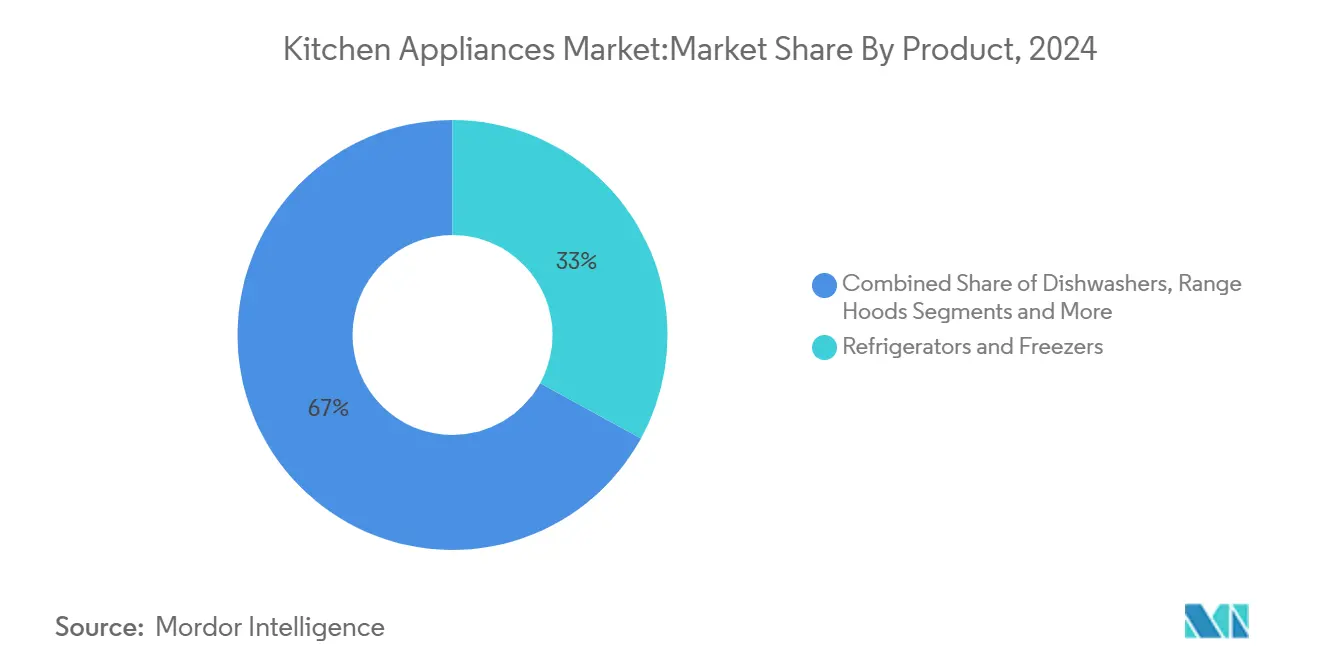

- By product, refrigerators and freezers led with 33% kitchen appliances market share in 2024, while ovens are set to grow at a 4.9% CAGR through 2030.

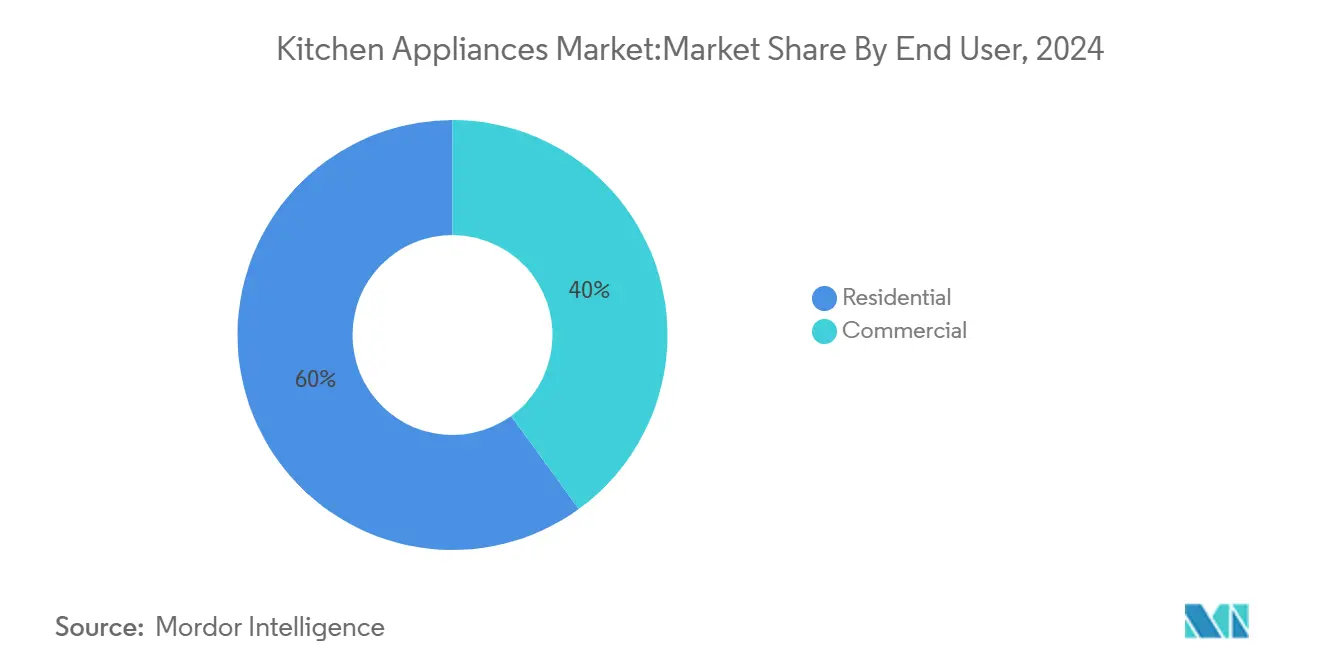

- By end user, the residential segment accounted for 60% of the kitchen appliances market share in 2024; commercial applications are advancing at a 5.2% CAGR to 2030.

- By distribution channel, B2C retail captured 68% of the kitchen appliances market size in 2024; online sub-channels within retail are growing at 6.1% CAGR between 2025-2030.

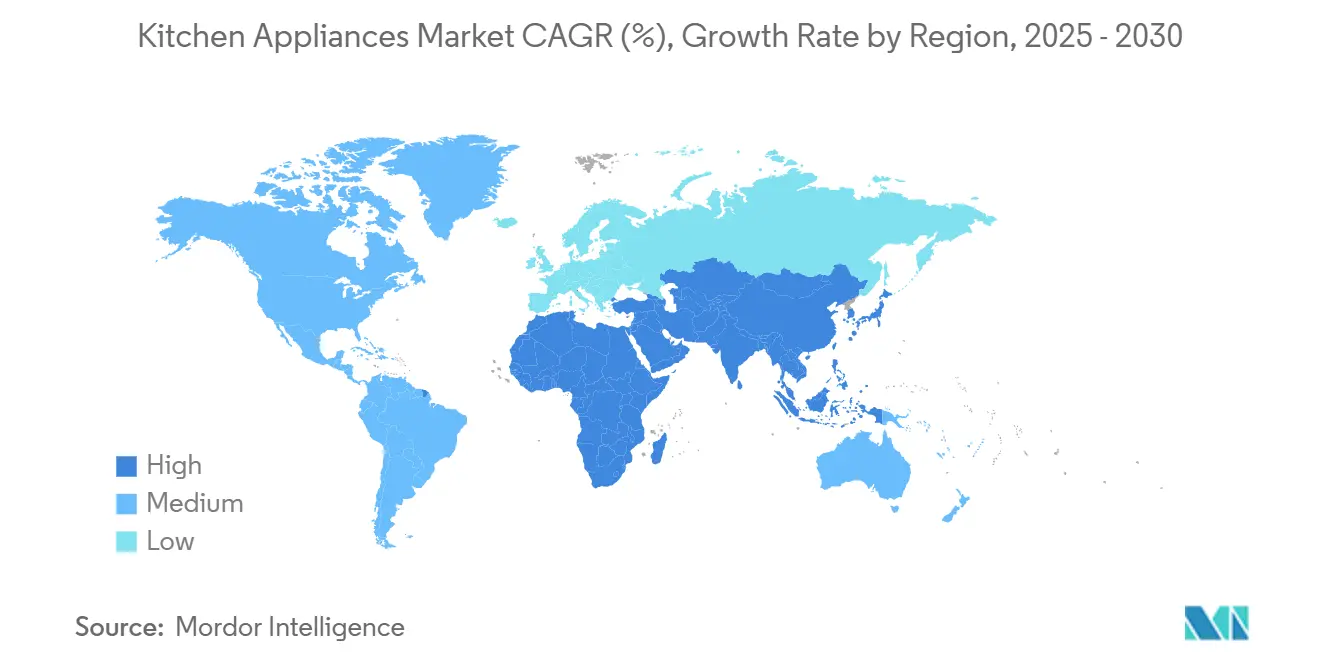

- By geography, North America held 32% revenue share in 2024, but Asia-Pacific is expanding at a 5.6% CAGR to remain the fastest-growing regional kitchen appliances market.

Global Kitchen Appliances Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising household expenditure on kitchen renovations | +0.8% | North America, Europe, spill-over to urban Asia-Pacific | Medium term (2-4 years) |

| Growing demand for smart and connected appliances | +1.2% | Global, with early gains in North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Energy-efficiency regulations boosting replacement sales | +0.9% | North America, EU core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Rapid urbanization and growth in residential construction | +0.7% | Asia-Pacific core, spill-over to Middle East and Africa and Latin America | Long term (≥ 4 years) |

| Surge in single-person households driving compact appliance sales | +0.5% | Global urban centers, concentrated in developed markets | Medium term (2-4 years) |

| Embedded carbon labeling influencing premium adoption | +0.3% | EU core, expanding to North America and select Asia-Pacific markets | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rising Household Expenditure on Kitchen Renovations

Kitchen renovation budgets climbed to a median USD 60,000 in 2024, up 9% year-on-year, as homeowners view remodels as long-term value rather than discretionary spend. Based on a survey of over 1,600 respondents, home remodeling and design platform Houzz found that homeowners in 2025 are investing in large, luxury kitchen spaces. Larger budgets favor built-in suites that integrate cooktops, refrigeration, and dishwashers behind custom panels. Because 53% of renovating households now change kitchen layout, demand for modular, space-efficient appliances grows in tandem. Professional contractors influence roughly 86% of renovation purchases, shifting decision-making toward holistic packages over individual units. The trend endures while housing supply stays tight, channeling capital that would otherwise fund home purchases into replacement of legacy appliances.

Growing Demand for Smart and Connected Appliances

Smart connectivity has moved from novelty to baseline in the kitchen appliances market. Samsung’s 2025 Bespoke AI line detects more than 30 food items to automate storage decisions and lower power draw using AI Energy Mode. GE Appliances’ SmartHQ platform connects ovens, refrigerators, and small appliances, letting users launch guided recipes or schedule maintenance remotely [1]Source: GE Appliances, “Advantium and SmartHQ Innovations,” geappliancespressroom.com. Yet consumer adoption remains tempered by privacy worries, prompting the United States Federal Communications Commission to introduce the Cyber Trust Mark in 2025 for connected devices. Brands that marry security by design with intuitive interfaces are positioned to command durable premiums.

Energy-Efficiency Regulations Boosting Replacement Sales

Government mandates accelerate turnover. The U.S. Department of Energy now requires 30% less energy in new electric cooktops sold after January 2028 [2]Source: U.S. Department of Energy, “DOE Finalizes Strong New Standards for Cooking Products,” energy.gov. Europe’s Ecodesign for Sustainable Products Regulation broadens criteria to durability and recyclability, forcing manufacturers to redesign for longer service life while maintaining efficiency. Canada’s parallel rules, phased through 2029, align with North American requirements and simplify compliance strategies for multinational brands. Early movers monetize compliant inventory at higher price points and avoid penalties that could erode margin.

Rapid Urbanization and Growth in Residential Construction

New urban housing stimulates first-time purchases. Asia-Pacific accounts for most new city dwellers, lifting demand for smaller, stackable appliances that suit compact floor plans. In 2025, single-family housing starts are forecast to rise 2.5% in the United States, while remodeling activity could grow 7% as owners upgrade existing stock. Innovative designs—such as rechargeable countertop ovens—remove installation barriers and appeal to renters. Manufacturers that prioritize smaller footprints, multi-mode functionality, and quiet operation benefit most from this demographic shift.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense price competition compressing margins | -0.6% | Global, particularly acute in Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| Supply-chain disruptions and component shortages | -0.4% | Global, concentrated in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Rising cybersecurity concerns in smart ecosystems | -0.3% | Developed markets with high smart penetration | Medium term (2-4 years) |

| Increasing scrutiny on right-to-repair rules | -0.2% | EU core, expanding to North America and select Asia-Pacific markets | Long term (≥ 4 years) |

Source: Mordor Intelligence

Intense Price Competition Compressing Manufacturer Margins

Tariff uncertainty and aggressive promotions pressure average selling prices worldwide. Ranges and refrigerators imported into the United States could see 8-25% duty hikes in 2025, but brands plan large rebates to blunt sticker shock. Chinese exporters shipped 4.48 billion units in 2024, up 20.8%, amplifying the low-cost supply that squeezes incumbent mid-range portfolios. Retailers deepen private-label penetration, forcing national labels to trade volume for profit or shift upscale.

Supply-Chain Disruptions and Component Shortages

China controls more than 90% of global rare-earth magnet supply and has tightened export checks, risking production halts if inventories run low by mid-2025. Semiconductor availability remains volatile, prompting appliance designers to engineer boards around chips they can procure rather than ideal components. Regional dual-sourcing and higher inventory buffers raise costs, but brands with diversified footprints recover faster and keep shelves stocked.

Segment Analysis

By Product: Refrigeration Dominance Meets Oven Innovation

The refrigeration category held 33% of the kitchen appliances market in 2024 thanks to its essential status and high replacement cost. Ovens, however, are forecast to rise at a 4.9% CAGR to 2030, outpacing other major categories. Smart oven models now combine convection, microwave, and air-fry modes in a single cavity, raising average selling prices. Voice-controlled temperature adjustment features help address cooking accuracy and reduce energy waste.

Refrigerators evolve through modular panel systems and internal cameras that monitor spoilage. Meanwhile, dishwashers gain steam-finish cycles and adjustable racks that improve accessibility for users with limited reach. Cooktops lean into induction for speed and precision, while range hoods integrate air-quality sensors that trigger automatically. Small kitchen gadgets also grow quickly as consumers seek countertop convenience. Together, these product innovations sustain revenue even as mature households only replace rather than add units.

Note: Segment shares of all individual segments available upon report purchase

By End User: Commercial Acceleration Outpaces Residential Stability

Residential buyers accounted for 60% of 2024 revenue, yet commercial kitchens will expand at a 5.2% CAGR through 2030 as hospitality rebounds. Quick-service chains now install robotic fryers and automated beverage stations to counter labor scarcity and keep output consistent. Commercial customers upgrade more frequently, giving suppliers an annuity stream for heavy-duty lines.

Homeowners continue remodeling instead of moving. The kitchen appliances market size for built-in suites is expected to expand as homeowners pursue cohesive aesthetics. Crossover designs—professional-grade ranges scaled for domestic gas or electric hookups—blur historical boundaries between the two segments. Commercial tech often debuts in restaurants, then migrates into premium homes a cycle later, making R&D investment efficient across both audiences.

By Distribution Channel: Digital Transformation Accelerates Online Growth

B2C outlets captured 68% of sales in 2024, but their online extensions are posting 6.1% annual gains. Younger buyers research models on manufacturer sites, then value same-day pick-up at local stores. Retailers such as Sur La Table deploy AI chat tools that raise average order value by over 7% by steering shoppers to higher-spec bundles.

Exclusive brand showrooms focus on high-touch demos and installation services, defending margin against price-led e-tailers. Manufacturers also push direct-to-consumer storefronts for accessories, water filters, and extended warranties, where they own the customer relationship and data. The omnichannel future rewards players who synchronize inventory, price, and service levels seamlessly across physical and digital touchpoints.

Geography Analysis

North America controlled 32% of global revenue in 2024, driven by high penetration and a culture of frequent replacement. Utility rebates accelerate demand for ENERGY STAR-rated units, while smart-home ecosystems lift premium segments. Tariff volatility may lift import costs, yet manufacturers often absorb duty spikes through production shifts. Competitive rivalry compressed Whirlpool’s U.S. margins in late 2024, prompting cost-cutting and brand mix adjustments at Whirlpool.

Asia-Pacific is on track for a 5.6% CAGR, the fastest among major regions, as rising middle-class incomes convert first-time buyers into upgraders. India’s consumer-durables sales have gained momentum with easier credit and rapid urban housing delivery. China remains the manufacturing engine; exports climbed 20.8% in 2024, reinforcing cost leadership and allowing regional brands to penetrate Latin America and Africa [3]Source: CCECCIC, “China Home Appliance Export Report 2024,” cceccic.com. Southeast Asian markets, notably Indonesia, offer tailwinds from demographic youth and modern retail expansion.

Europe shows balanced growth but tighter sustainability rules. The upcoming right-to-repair directive forces appliance makers to stock parts for at least seven years, reshaping service supply chains. Whirlpool’s partnership with Arçelik to create Beko Europe rebalances its footprint and concentrates R&D on energy-efficient platforms. Consumer demand skews toward induction cooktops and heat-pump dryers as households aim to lower energy bills amid rising utility rates.

Competitive Landscape

Global leadership remains with Electrolux, Haier, Whirlpool, Samsung, and LG, yet the kitchen appliances market is only moderately concentrated. These firms leverage scale in procurement and distribution, but mid-tier challengers erode share by targeting niche pain points. SharkNinja, for instance, recorded 29.7% net-sales growth in Q4 2024 and 80.3% growth in food-prep appliances by focusing on disruptive form factors and aggressive marketing.

Technology is the key battleground. GE Appliances earned a cybersecurity award in late 2024 for its SmartHQ architecture, strengthening consumer trust in connected ecosystems GE Appliances. Samsung invests heavily in AI-enabled vision systems that automate inventory management inside refrigerators.

Supply-chain strategies split the cohort. Some firms, such as LG, onshore critical board assembly to mitigate semiconductor risk, while others form joint ventures to secure rare-earth magnet supply. Premium positioning and circular-economy credentials also differentiate brands; those with take-back or refurbished-unit businesses may soften any revenue loss from right-to-repair policies.

Kitchen Appliances Industry Leaders

-

Whirlpool Corporation

-

Haier Group (incl. GE Appliances)

-

LG Electronics

-

Electrolux AB

-

Samsung Electronics

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Frigidaire debuted its first air-purifier line, broadening Electrolux Group’s reach beyond traditional kitchen categories Electrolux Group.

- February 2025: Samsung unveiled its full Bespoke AI lineup at KBIS 2025, including AI Family Hub+ refrigerators and a slide-in induction range with enhanced connectivity.

- February 2025: GE Appliances introduced SmartHQ AI Coffee Assistant and Flavorly AI recipe generator, integrated with Instacart shopping GE Appliances.

- December 2024: Weber and Blackstone Products agreed to merge, combining barbecue and outdoor-griddle expertise under Blackstone leadership.

Global Kitchen Appliances Market Report Scope

Kitchen appliances are the tools and machines used to prepare, cook, and store food. Rising technological advances have made kitchen work more accessible and resulted in the development of various appliances for use in kitchen units.

The kitchen appliance market is segmented by product (refrigerators and freezers, dishwashers, food processors, mixers and grinders, microwave ovens, grills and roasters, and water purifiers), distribution channel (multi-brand stores, exclusive stores, and online), end user (residential and commercial), and geography (North America (United States, Canada, Mexico, and Rest of North America), Europe (United Kingdom, Germany, Italy, and Rest of Europe), Asia-Pacific (India, China, Japan, Australia, and Rest of Asia-Pacific), Middle East & Africa (South Africa, United Arab Emirates), and South America (Brazil, Colombia, and Mexico)). The report also covers the market sizes and forecasts for the kitchen appliance market in value (USD) for all the above segments.

| By Product | Large Kitchen Appliances | Refrigerators & Freezers | |

| Dishwashers | |||

| Range Hoods | |||

| Cooktops | |||

| Ovens | |||

| Other Large Kitchen Appliances | |||

| Small Kitchen Appliances | Food Processors | ||

| Juicers and Blenders | |||

| Grills and Roasters | |||

| Air Fryers | |||

| Coffee Makers | |||

| Electric Cookers | |||

| Toasters | |||

| Electric Kettles | |||

| Countertop Ovens | |||

| Other Small Kitchen Appliances (bread makers, waffle makers, egg cookers, etc.) | |||

| By End User | Residential | ||

| Commercial | |||

| By Distribution Channel | B2C/Retail | Multi-brand Stores | |

| Exclusive Brand Outlets | |||

| Online | |||

| Other Distribution Channels | |||

| B2B (directly from the manufacturers) | |||

| By Geography | North America | Canada | |

| United States | |||

| Mexico | |||

| South America | Brazil | ||

| Peru | |||

| Chile | |||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| BENELUX (Belgium, Netherlands, and Luxembourg) | |||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |||

| Rest of Europe | |||

| Asia-Pacific | India | ||

| China | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |||

| Rest of Asia-Pacific | |||

| Middle East And Africa | United Arab of Emirates | ||

| Saudi Arabia | |||

| South Africa | |||

| Nigeria | |||

| Rest of Middle East And Africa | |||

By Product

| Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | |

| Range Hoods | |

| Cooktops | |

| Ovens | |

| Other Large Kitchen Appliances | |

| Small Kitchen Appliances | Food Processors |

| Juicers and Blenders | |

| Grills and Roasters | |

| Air Fryers | |

| Coffee Makers | |

| Electric Cookers | |

| Toasters | |

| Electric Kettles | |

| Countertop Ovens | |

| Other Small Kitchen Appliances (bread makers, waffle makers, egg cookers, etc.) |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B (directly from the manufacturers) |

By Geography

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East And Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the kitchen appliances market?

The kitchen appliances market was valued at USD 310.93 billion in 2025 and is forecast to reach USD 381.95 billion by 2030.

Which product category is growing fastest?

Ovens are the fastest-growing category, expected to post a 4.9% CAGR through 2030 thanks to smart, multi-mode features.

Why are smart appliances gaining traction?

Consumers adopt smart models for energy savings, convenience, and ecosystem integration, while recent cybersecurity labeling helps build trust.

Which region will expand the most?

Asia-Pacific is set for the strongest regional growth at a 5.6% CAGR, driven by rising urban incomes and first-time purchases.

How are regulations shaping market dynamics?

Tighter energy-efficiency and right-to-repair rules accelerate replacement of older units, while forcing manufacturers to design more durable, repairable products

What is the biggest risk for manufacturers?

Margin pressure from intense price competition and supply-chain volatility remain the most immediate risks, underscoring the need for cost-efficient operations and diversified sourcing.