Therapeutic Vaccine Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

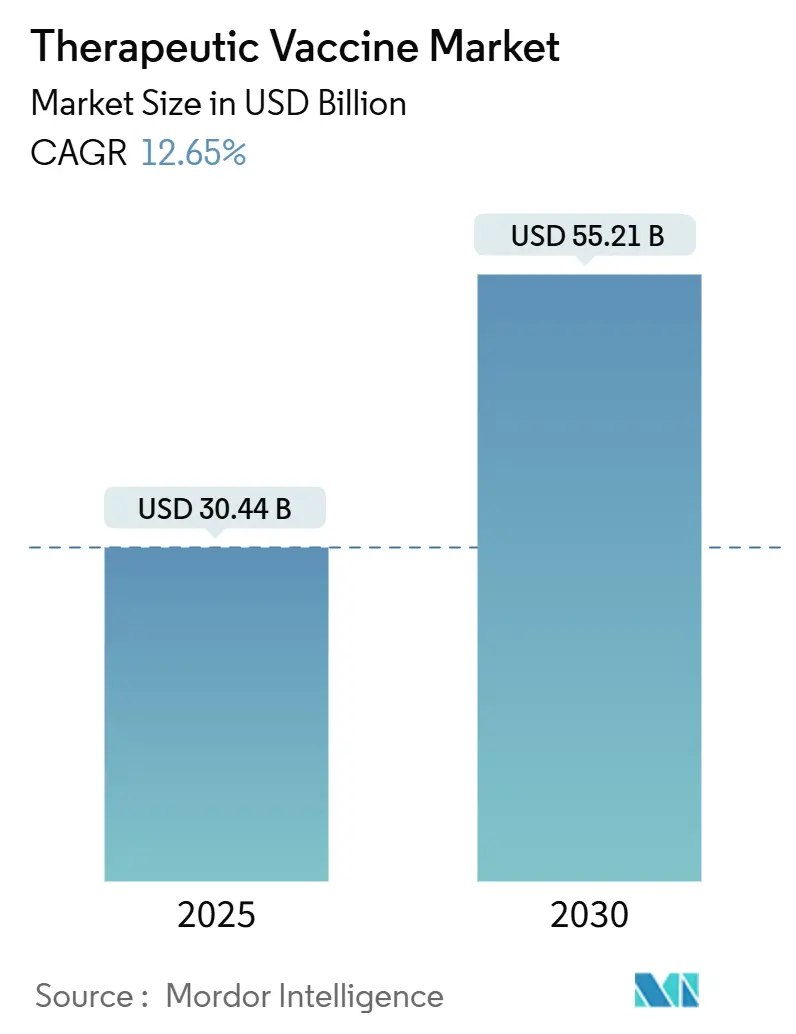

| Market Size (2025) | USD 30.44 Billion |

| Market Size (2030) | USD 55.21 Billion |

| Growth Rate (2025 - 2030) | 12.65% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Therapeutic Vaccine Market Analysis by Mordor Intelligence

The therapeutic vaccines market reaches USD 30.44 billion in 2025 and is forecast to attain USD 55.21 billion by 2030, advancing at a 12.65% CAGR. Demand expands as companies shift from preventive inoculation toward treatment-focused immunotherapy platforms that tackle active disease, particularly cancer and chronic viral infections. Breakthrough mRNA approvals, together with AI-assisted neo-antigen discovery, shorten development cycles and improve clinical precision, bolstering investor confidence and prompting regulators to formalize expedited pathways. Manufacturing capacity added during the pandemic now underpins rapid scale-up for new pipelines, while government programs such as Project NextGen supply non-dilutive capital that reduces early-stage risk. Competitive advantage accrues to firms that integrate R&D, clinical manufacturing, and cold-chain distribution, allowing faster launch of modular, personalized regimens across multiple indications [1]U.S. Food and Drug Administration, "2024 Biological License Application Approvals," fda.gov.

Key Report Takeaways

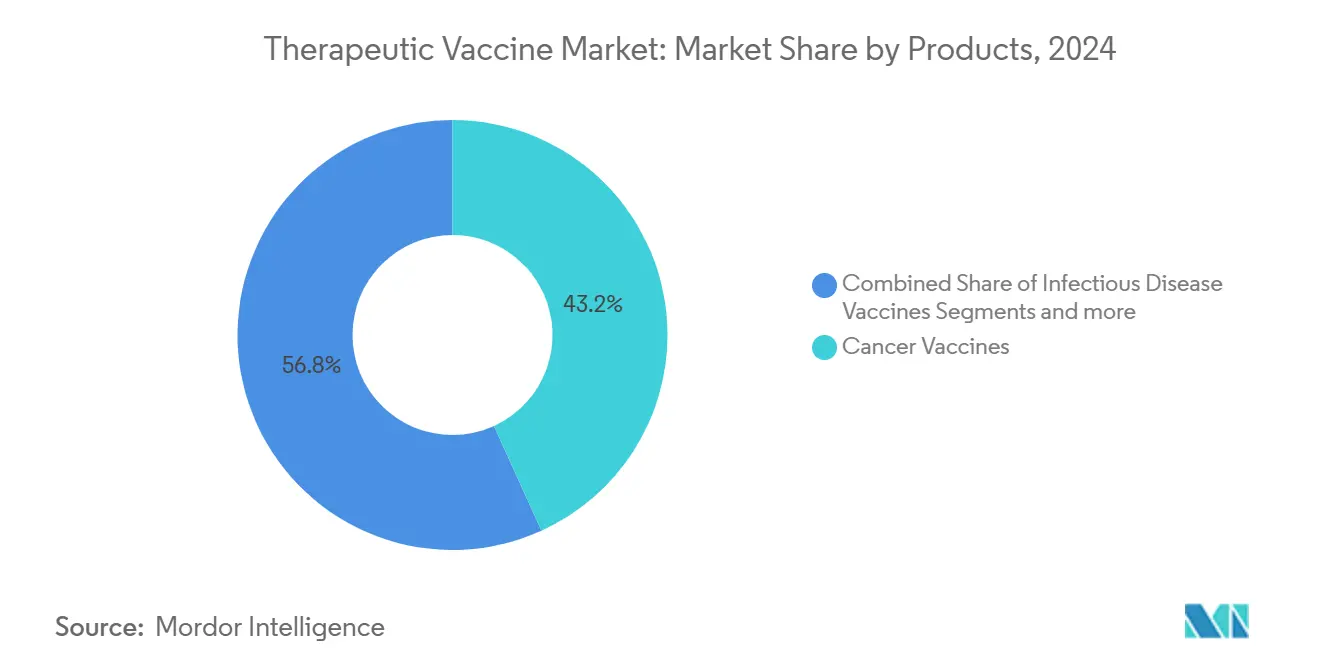

- By product category, cancer vaccines led with 43.21% of therapeutic vaccines market share in 2024; infectious-disease candidates are projected to expand at a 13.45% CAGR through 2030.

- By technology, allogeneic platforms held 65.34% revenue share of the therapeutic vaccines market in 2024, while autologous approaches record the fastest 13.44% CAGR to 2030.

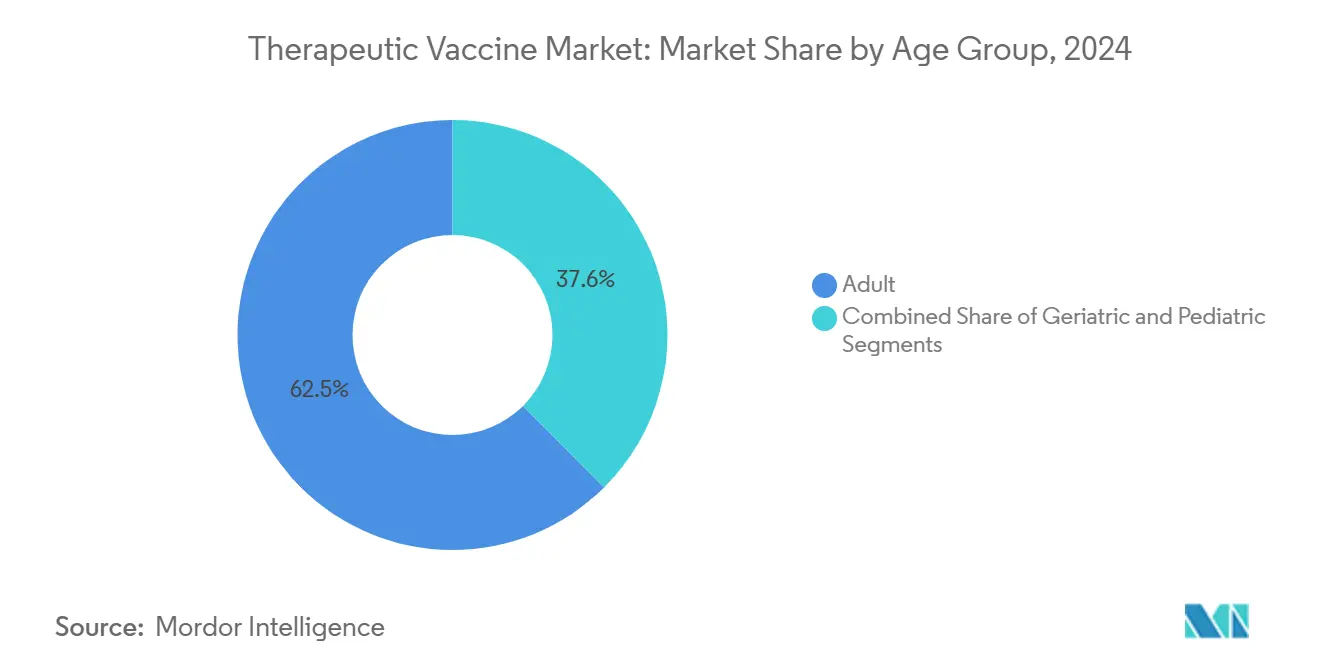

- By age group, adult patients accounted for 62.45% of the therapeutic vaccines market size in 2024; pediatric applications are growing at a 13.67% CAGR through 2030.

- By distribution channel, public programs controlled 68.91% of 2024 demand, whereas private settings are advancing at a 13.34% CAGR to 2030.

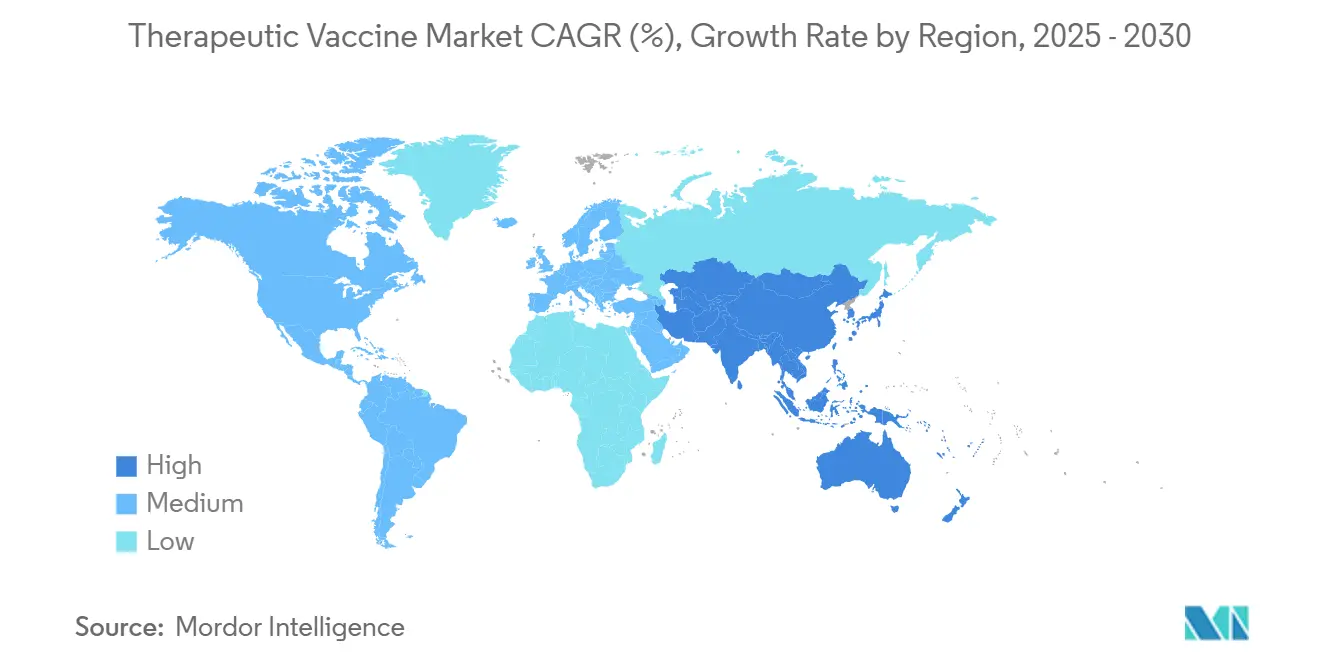

- By geography, North America maintained 41.76% revenue leadership in 2024; Asia-Pacific shows a 13.69% CAGR, the fastest regional trajectory to 2030.

Global Therapeutic Vaccine Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic & infectious diseases | +2.1% | Global, concentrated in aging populations across North America, Europe and APAC | Long term (≥ 4 years) |

| Government funding intensification for vaccine R&D | +1.8% | North America & EU, spillover to APAC and emerging markets | Medium term (2-4 years) |

| Pharma/biotech surge in oncology vaccine pipelines | +1.5% | Global, R&D centered in North America & Europe | Long term (≥ 4 years) |

| Breakthrough mRNA-based therapeutic vaccine approvals | +1.2% | North America & EU leadership | Short term (≤ 2 years) |

| AI-driven neo-antigen discovery accelerating personalization | +0.8% | North America & EU tech hubs | Medium term (2-4 years) |

| On-site modular micro-factory manufacturing models | +0.6% | Early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic & Infectious Diseases

Global aging drives higher cancer incidence, while evolving pathogens sustain viral and bacterial disease burdens. Therapeutic vaccines address these unmet needs by training the immune system to combat existing illness rather than preventing exposure. Oncology, chronic hepatitis B, and recurrent genital herpes comprise high-volume targets where durable responses lessen lifelong drug therapy [2]World Health Organization , "Cancer," who.int. Public health authorities view therapeutic regimens as budget-friendly once-or-limited-course alternatives to chronic medication, encouraging reimbursement frameworks that reward curative potential. The result is sustained expansion of the therapeutic vaccines market across both developed and middle-income economies.

Government Funding Intensification for Vaccine R&D

The United States launched Project NextGen with USD 5 billion earmarked for next-generation platforms, including therapeutic applications beyond prevention. BARDA’s milestone-based awards prioritize dual-use technologies able to pivot between pandemic response and chronic-disease therapy, accelerating GMP build-outs and de-risking scale-up. Similar instruments appear in the EU Horizon framework, while CEPI coordinates global clinical-trial standardization that shortens multi-country approvals. Public money now supplies early-stage capital that private investors historically avoided, fortifying the therapeutic vaccines market against downturns.

Pharma/Biotech Surge in Oncology Vaccine Pipelines

Checkpoint inhibitors created proof of concept for immune-mediated cancer control; therapeutic vaccines now amplify these responses. Moderna and Merck’s mRNA-4157/Keytruda combo advanced to Phase 3 melanoma trials in 2025, widening application into lung and colorectal settings [3]Moderna Inc., "Moderna & Merck Announce 3-Year Data For mRNA-4157 (V940)," modernatx.com. Big-pharma partnerships supply late-stage resources, while platform biotech firms iterate multiple candidates from shared libraries, lowering per-asset risk. These pipeline expansions reinforce sustained double-digit growth within the therapeutic vaccines market.

Breakthrough mRNA-Based Therapeutic Vaccine Approvals

FDA authorization of the first mRNA therapeutic vaccine in 2025 validated lipid-nanoparticle delivery, immunogenicity, and manageable safety profiles. Pandemic-era facilities now transition to oncology and chronic-infection products, shortening time-to-market compared with de-novo bioreactors. The coding flexibility of mRNA supports rapid personalization and facilitates mix-and-match combination regimens, improving patient-specific outcomes and intensifying competitive differentiation across the therapeutic vaccines market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-intensive, high-risk clinical development cycle | -1.9% | Global, amplified where venture funding is scarce | Long term (≥ 4 years) |

| Stringent multi-jurisdictional regulatory hurdles | -1.3% | Global, complexity across US-EU-APAC | Medium term (2-4 years) |

| Shortage of GMP viral-vector / plasmid capacity | -0.9% | Global, clustered in major biopharma hubs | Short term (≤ 2 years) |

| Late-stage I-O trial failures dampening sentiment | -0.7% | Global investor markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive, High-Risk Clinical Development Cycle

Therapeutic vaccines require multi-year, multimillion-dollar investments before pivotal data emerge. Biological manufacturing often commits USD 100 million ahead of approval, straining balance sheets of early-stage firms. Immunological variability raises late-phase attrition rates above those for small molecules, complicating valuation models and prompting cautious syndicates. Consequently, some pipelines slow, offsetting a portion of forecast growth within the therapeutic vaccines market.

Stringent Multi-Jurisdictional Regulatory Hurdles

Therapeutic vaccines sit at the intersection of biologics, cell therapy, and combination product statutes. FDA guidance continues to evolve, whereas EMA maintains distinct advanced-therapy rules that diverge from US requirements. Companies must often repeat quality audits for each jurisdiction, inflating timelines and compliance costs. Harmonization efforts advance but remain incomplete, tempering smaller entrants’ ability to globalize quickly.

Segment Analysis

By Products: Cancer Vaccines Lead Market Transformation

Cancer vaccines delivered USD 13.2 billion in 2025, equal to 43.21% of therapeutic vaccines market size, affirming oncology as the anchor of commercial adoption. The segment benefits from validated antigens, robust biomarker infrastructure, and reimbursement aligned to high-value indications. Combination regimens with checkpoint inhibitors enhance response durability, cementing cancer’s contribution to the broader therapeutic vaccines market. Infectious-disease therapeutics, although smaller at USD 7.1 billion, expand at 13.45% CAGR as chronic hepatitis B and herpes candidates advance. Autoimmune and neurological categories remain nascent yet critical for pipeline diversity, attracting platform developers eager to leverage shared manufacturing and regulatory learning curves. Overall, diversified product baskets reduce portfolio risk and help sustain long-term expansion within the therapeutic vaccines industry.

A second-order effect is the reallocation of venture dollars toward inverse and tolerance-inducing vaccines, targeting diseases such as multiple sclerosis where existing therapies only manage symptoms. Neurological projects—including tau and alpha-synuclein vaccines—progress through mid-stage trials, reinforcing confidence that immunotherapy can address protein-aggregation disorders. Together these dynamics sustain investor appetite, accelerate science translation, and increase the proportion of revenues derived from non-oncology indications by the end of the decade.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Allogeneic Platforms Dominate Despite Autologous Growth

Allogeneic constructs generated USD 19.9 billion in 2025, equivalent to 65.34% of therapeutic vaccines market size, owing to standardized, off-the-shelf formats that simplify distribution. Their economies of scale produce lower per-dose cost and faster lot release, attractive for large public tenders. Autologous approaches, however, record a 13.44% CAGR through 2030 as sequencing and manufacturing automation shrink lead times. Patient-specific neo-antigens improve precision, particularly in solid tumors, yielding higher objective-response rates that justify premium pricing. Hybrid architectures emerge: shared lipid-nanoparticle cores paired with individualized mRNA inserts, thereby balancing scalability and personalization. As AI algorithms further refine epitope selection, autologous and “semi-personalized” formats are expected to raise their share of the therapeutic vaccines market.

Platform convergence also fosters operational agility. Facilities now host multi-modal suites able to switch between plasmid DNA, mRNA, and protein subunit runs within the same cleanroom footprint. This flexibility reduces idle capacity and supports lean manufacturing economics, traits that will be essential as pipelines become increasingly indication-specific.

By Age Group: Adult Applications Drive Current Demand

Adults generated 62.45% of 2024 revenue as cancer prevalence and chronic viral burden skew toward older populations. Payer policies favor therapeutic vaccines that reduce lifelong antiviral or immunosuppressive regimens, boosting adult uptake. Pediatric volumes remain smaller but are expanding at 13.67% CAGR, supported by regulatory incentives, orphan-disease focus, and growing parental acceptance of immunomodulatory treatments for conditions such as pediatric glioma. Formulation science tailors adjuvant strength and dosing frequency to developing immune systems, overcoming historical safety concerns and widening the therapeutic vaccines market.

Parallel research explores geriatric-targeted formulations aimed at overcoming immunosenescence. Cytokine-enhanced lipid nanoparticles and higher-dose regimens seek to restore T-cell activity, potentially unlocking new demand segments as populations age further across OECD nations.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Public Sector Maintains Control

Public programs, principally government health services and multilateral procurement entities, secured 68.91% of doses in 2024, leveraging centralized cold-chain assets and bulk purchasing power. They remain pivotal for high-prevalence indications such as hepatitis B, where broad access offsets low per-dose pricing. Private facilities, including specialty oncology clinics and personalized-medicine centers, grow at 13.34% CAGR as autologous and combination regimens require individualized logistics. Home-infusion options are under investigation, signalling future diversification of distribution models and incremental expansion of the therapeutic vaccines market.

Partnership structures evolve accordingly. Manufacturers supply public payers under volume-based rebates while deploying nurse-practitioner programs inside private centers to coordinate cell collection and on-site dosing. The resulting hybrid ecosystem preserves equitable access while enabling high-margin personalized therapies.

Geography Analysis

North America contributed 41.76% of global revenue in 2024 on the strength of FDA breakthrough designations, concentrated VC funding, and rapid enrollment networks. Project NextGen and BARDA grants sustain academic-industry hubs from Boston to San Diego, while expansions such as Merck’s USD 1 billion Durham plant and Pfizer’s USD 465 million Kalamazoo upgrade create surplus fill-finish capacity. Reimbursement frameworks encourage early adoption, exemplified by CMS transitional-coverage rules for FDA-cleared breakthrough products.

Europe follows with substantial public-private consortia and Horizon Europe grants guiding translational research. EMA’s PRIME and Conditional Approval programs align with value-based pricing pilots in Germany and France, enabling earlier market entry for high-need indications. Facilities such as WACKER’s EUR 100 million mRNA center in Halle bolster continental supply security. However, fragmented national payer negotiations can delay uniform access, tempering uptake relative to North America.

Asia-Pacific posts the fastest 13.69% CAGR through 2030, anchored by China’s regulatory modernization and manufacturing-cost advantage. Local biotechs leverage patent linkage to co-develop with Western firms, while new CDMO campuses in Singapore and South Korea supply global clients. Japan’s aging demographic and premium reimbursement for oncology care lift unit prices, offsetting slower volume growth. Regional governments also fund cold-chain upgrades, broadening capacity for both domestic and export markets and reinforcing Asia-Pacific’s rising influence in the therapeutic vaccines market.

Competitive Landscape

The field is moderately fragmented, with the top five firms controlling an estimated 45% of 2024 revenue. Large pharmaceuticals—including Merck, GSK, and Pfizer—co-develop mRNA and viral-vector pipelines with platform biotechs, exchanging milestone payments for downstream profit splits. Vertical integration intensifies: companies lock in lipid nanoparticle IP, secure plasmid supply, and acquire specialty CDMOs, insulating margins and ensuring slot availability during surge demand.

Biotech specialists differentiate through proprietary antigen-selection algorithms and device-assisted delivery, such as electroporation patches that raise cellular uptake. AI-native entrants partner early with diagnostic firms to match vaccines to tumor mutational burden, creating comprehensive treatment ecosystems. Meanwhile, academic spin-outs supply novel adjuvant chemistries, often licensed back by big pharma for global distribution. FDA approval of Anktiva in combination with BCG for bladder cancer in 2025 validates synergistic regimens, encouraging cross-company alliances.

Pricing power varies by indication. Oncology commands premium reimbursement, while infectious-disease therapeutics rely on volume. Companies thus balance portfolios, maintaining cash-flow stability while pursuing high-risk, high-return personalized programs. Continued M&A is expected as incumbents fill technology gaps and consolidate manufacturing nodes, nudging the therapeutic vaccines market toward higher concentration by 2030.

Therapeutic Vaccine Industry Leaders

-

Phio Pharmaceuticals Corp.

-

GSK plc.

-

Merck & Co., Inc.

-

Pfizer Inc.

-

Agenus Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Patients with advanced skin cancer in England will enter trials for the needle-free DNA vaccine iSCIB1+, part of an expanded NHS program accelerating therapeutic vaccine evaluation.

- March 2025: Merck opened a dedicated vaccine production facility to support its expanding therapeutic vaccine pipeline, adding capacity to mitigate industry-wide constraints.

- June 2024: WACKER inaugurated an mRNA competence center in Halle, Germany, investing over EUR 100 million to enable annual output of more than 200 million doses.

- February 2024: Helmholtz Munich and partners began a Phase I trial of TherVacB, a therapeutic vaccine targeting chronic hepatitis B, to assess safety and immunogenicity in healthy volunteers.

Global Therapeutic Vaccine Market Report Scope

As per the scope of the report, a therapeutic vaccine is applied after an infection or disease occurs in order to induce antiviral immunity and alter the course of the disease. Therapeutic vaccines are used to cure diseases because, rather than immunizing for future disease protection, they work with the patient's own immune system to fight infection. The therapeutic vaccine market is segmented by products (autoimmune disease vaccines, neurological disease vaccines, cancer vaccines, infectious disease vaccines, and other products), technology (allogeneic vaccines and autologous vaccines), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Autoimmune Disease Vaccines |

| Neurological Disease Vaccines |

| Cancer Vaccines |

| Infectious Disease Vaccines |

| Other Products |

| Allogeneic Vaccines |

| Autologous Vaccines |

| Adult |

| Pediatric |

| Geriatric |

| Public |

| Private |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Products | Autoimmune Disease Vaccines | |

| Neurological Disease Vaccines | ||

| Cancer Vaccines | ||

| Infectious Disease Vaccines | ||

| Other Products | ||

| By Technology | Allogeneic Vaccines | |

| Autologous Vaccines | ||

| By Age Group | Adult | |

| Pediatric | ||

| Geriatric | ||

| By Distribution Channel | Public | |

| Private | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the therapeutic vaccines market?

The market is valued at USD 30.44 billion in 2025 and is projected to reach USD 55.21 billion by 2030.

Which product segment drives the largest revenue?

Cancer vaccines lead with 43.21% market share in 2024 due to strong clinical validation and high oncology demand.

Which region is expanding fastest?

Asia-Pacific records the highest 13.69% CAGR through 2030, propelled by manufacturing advantages and regulatory modernization.

What technology holds the majority share?

Allogeneic platforms control 65.34% of 2024 revenue, although autologous formats grow more quickly at 13.44% CAGR.

How are governments influencing market growth?

Programs such as the USD 5 billion Project NextGen fund next-generation platforms, lowering early-stage risk and accelerating commercialization.

What are the main challenges facing companies?

High capital requirements, complex multi-region regulations, and limited GMP vector capacity continue to restrain near-term growth prospects.

Page last updated on: