Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 3.10 Billion |

| Market Size (2030) | USD 5.40 Billion |

| Growth Rate (2025 - 2030) | 11.80% CAGR |

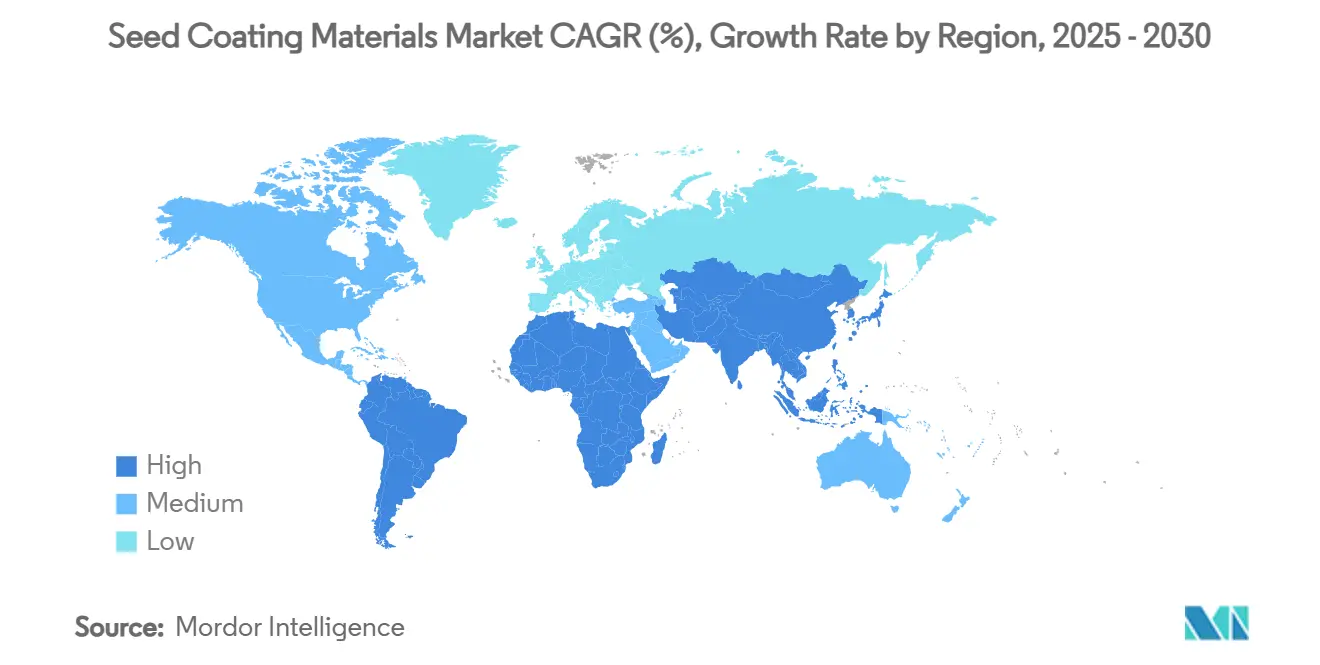

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Seed Coating Materials Market Analysis by Mordor Intelligence

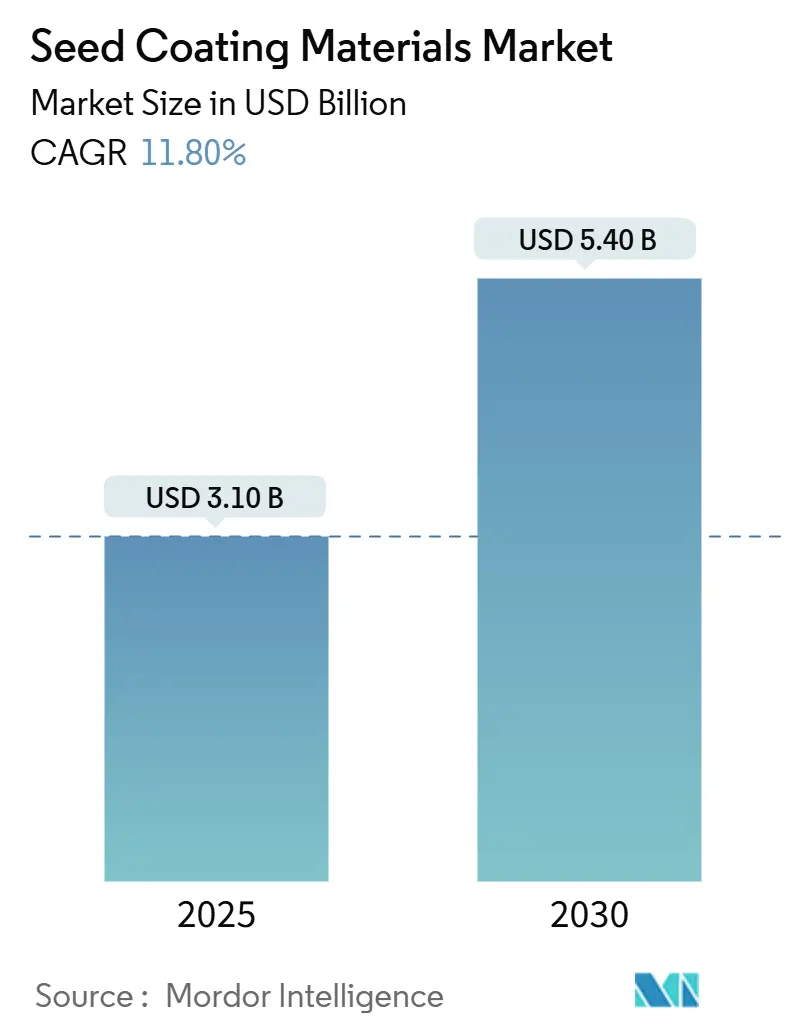

The seed coating material market is valued at USD 3.10 billion in 2025 and is forecast to reach USD 5.40 billion by 2030, expanding at an 11.80% CAGR. Growth is powered by precision-agriculture adoption, stricter environmental regulations, and rapid innovation in polymer as well as bio-based chemistries. European microplastic restrictions are accelerating the pivot toward biodegradable binders, while Brazil’s bio-input policies are reinforcing demand for plant-derived and microbial films. Nanotechnology and super-absorbent gels are turning coatings into multifunctional platforms that protect genetics, enhance germination, and improve water efficiency. Asia-Pacific and South America are registering the fastest uptake as growers modernize to manage climate variability and input costs; North America maintains scale leadership through integrated trait and coating packages in corn, soybean, and canola applications.

Key Report Takeaways

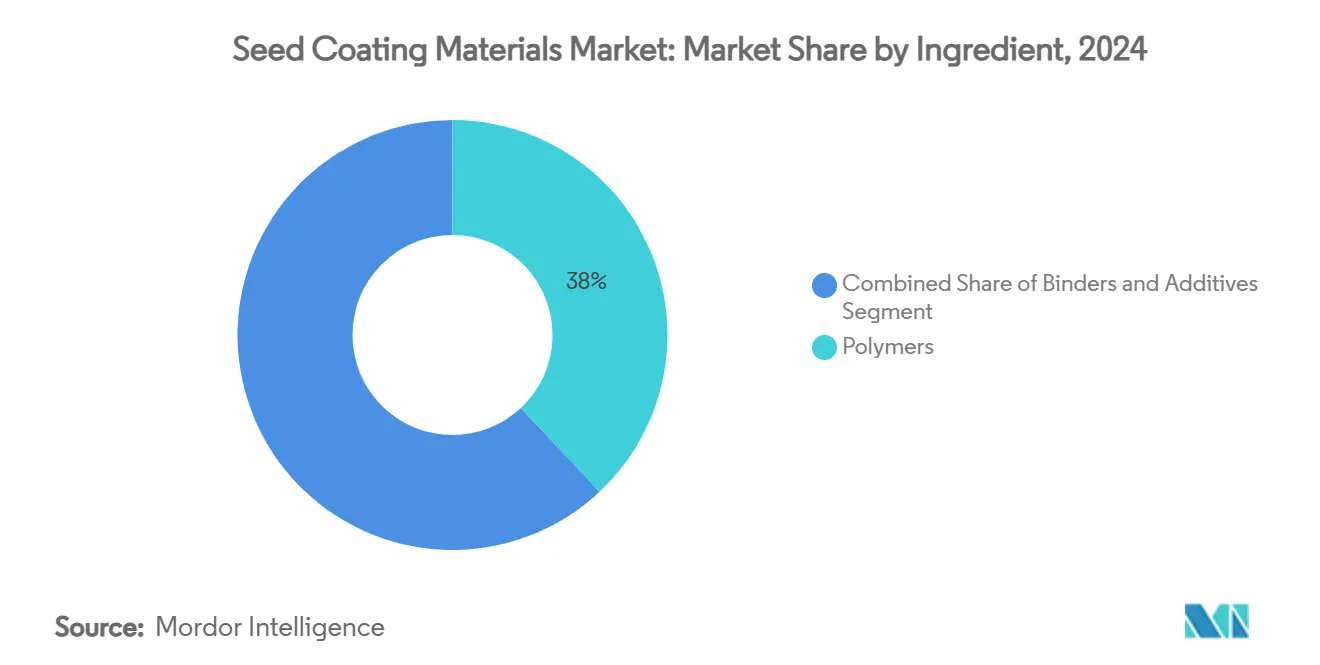

- By ingredient, polymers led with 38% revenue share in 2024; super-absorbent polymer gels are projected to expand at a 14.2% CAGR through 2030.

- By process, film coating held 55% of the seed coating material market share in 2024, while pelleting records the highest projected CAGR at 15.5% through 2030.

- By coating type, synthetic coatings held 61% of the seed coating material market share in 2024, while bio-based coatings are forecast to grow at a 14.5% CAGR through 2030.

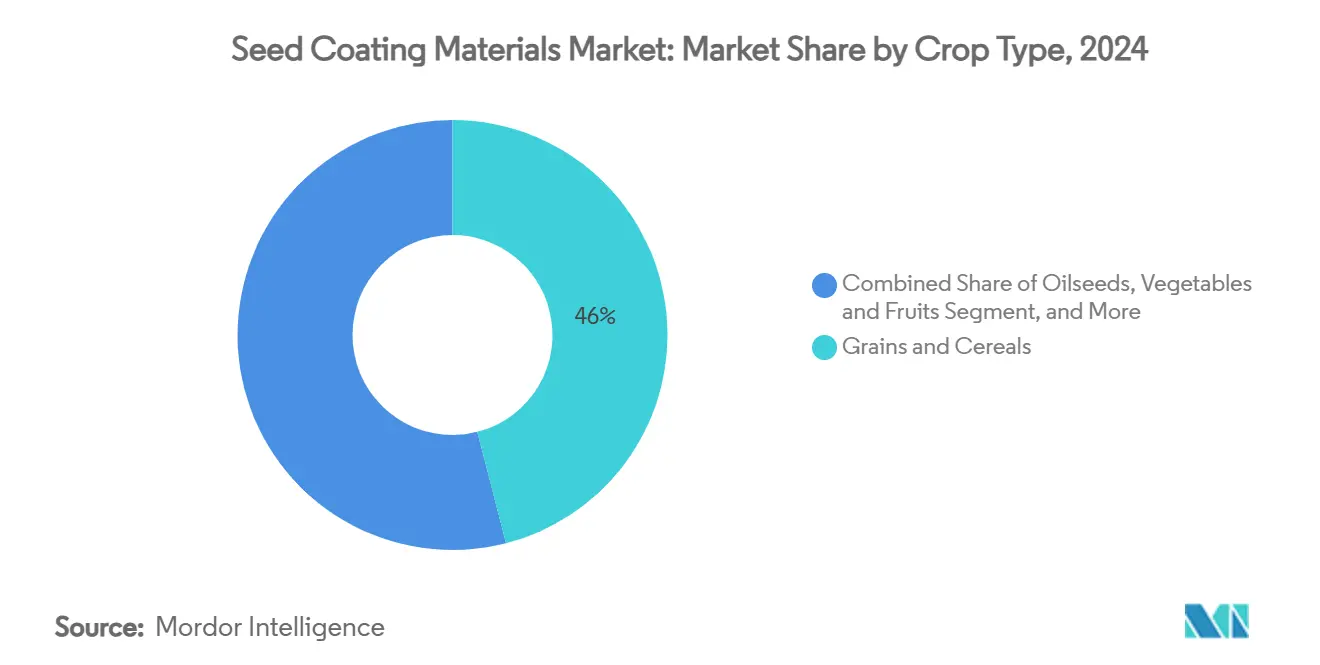

- By crop type, cereals and grains dominated with 46% revenue share in 2024, whereas fruits and vegetables are poised for an 11.8% CAGR to 2030.

- By function, seed protection accounted for a 63% share of the seed coating material market size in 2024, and enhancement is advancing at a 13.8% CAGR through 2030.

- By geography, Asia-Pacific is forecast to grow at an 11.5% CAGR from 2025 to 2030, while North America retained a 35% share in 2024.

- The top five suppliers, BASF SE, Bayer CropScience, Syngenta, Clariant International, and Croda International, collectively controlled 63% of the 2024 global revenue.

Global Seed Coating Materials Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-quality seed demand from hybrid and GM seed expansion | +2.5% | North America and Asia-Pacific | Medium term (2-4 years) |

| Rapid shift toward sustainable agriculture practices | +2.2% | Europe and North America | Long term (≥ 4 years) |

| Continuous innovations in polymer and bio-based film technologies | +1.8% | North America and Europe | Medium term (2-4 years) |

| Imminent bans on microplastics accelerate eco-friendly coating R and D | +1.5% | Europe expanding globally | Short term (≤ 2 years) |

| Adoption of super-absorbent polymers for climate-resilient cropping | +1.2% | Arid regions worldwide | Medium term (2-4 years) |

| Carbon-credit programs incentivizing microbial-coated seeds | +1.0% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High-quality seed demand from hybrid and GM seed expansion

More than 30 countries approved commercial GM cultivation by late 2024, including Kenya’s BT cotton and Ghana’s GM cowpea, widening the premium-seed footprint worldwide[1]Source: International Service for the Acquisition of Agri-biotech Applications, “Global Status of Commercialized Biotech Crops 2024,” isaaa.org. The Environmental Protection Agency cleared new plant-incorporated protectants such as Brevibacillus laterosporus proteins for corn, signaling a smoother pathway for next-generation traits[2]Source: U.S. Environmental Protection Agency, “Biopesticide Registration Improvements,” epa.gov. As genetic value rises, growers seek coatings that ensure uniform emergence, protect high-cost traits, and simplify precision planting, reinforcing demand across the seed coating material market.

Rapid shift toward sustainable agriculture practices

Brazil’s bio-inputs segment reached BRL 5 billion (USD 1 billion) in the 2023-2024 season, posting 15% annual growth and proving that biologicals can succeed at scale. Federal Law No. 15 070/2024 now offers a dedicated framework and funding for bio-inputs. Similar policy signals in Europe and the United States are steering investment toward plant-based polymers, starch binders, and microbial films that lower environmental footprints without sacrificing field performance.

Continuous innovations in polymer and bio-based film technologies

Zinc-oxide nanoparticles boosted germination by 43% in controlled trials, while silicon-coated carbon quantum dots achieved 71% aphid mortality alongside crop growth promotion. Ingredion’s starch binder matches synthetic adhesion and carries compostability certification. These advances enable lighter coatings, improved nutrient release, and reduced dust, sustaining momentum in the seed coating material market.

Imminent bans on microplastics accelerate eco-friendly coating R and D

The European Union banned intentionally added microplastics in agricultural inputs from October 2023, with full compliance due by 2028. Incotec has already commercialized microplastic-free technologies for vegetable seeds and plans to extend them to field crops by 2026. Research into carbohydrate-based super-absorbents shows equivalent germination boosts while eliminating persistent polymers[3]Source: Royal Society Open Science, “Carbohydrate Super-absorbents for Seeds,” royalsocietypublishing.org.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of petro-derived binders and pigments | -1.7% | Import-dependent markets | Short term (≤ 2 years) |

| Complex global registration for multi-component formulations | -1.3% | All major markets | Medium term (2-4 years) |

| Limited shelf-life of biological actives on-seed | -1.1% | Tropical and humid regions | Medium term (2-4 years) |

| Costly reformulations to meet upcoming EU-27 microplastic rules | -0.8% | Europe and exporters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile prices of petro-derived binders and pigments

Natural-gas price swings and freight bottlenecks at the Panama and Suez canals have inflated chemical feedstock costs by up to 30%, squeezing margins for synthetic-coating producers. Smaller firms without multi-region supply contracts face the greatest exposure, prompting a pivot toward locally sourced starch binders. Although bio-based inputs carry higher purchase prices today, their cost profile is more stable, nudging procurement away from petroleum-linked materials in the seed coating material market.

Complex global registration for multi-component formulations

The EPA often requires multi-year data packages for new activities, delaying rollouts and tying up R and D capital. Emerging economies lack harmonized rules, forcing duplicative dossiers that favor large firms with dedicated regulatory teams. Companies must also finance extensive environmental fate and residue studies to meet country-specific guidelines, pushing development costs into the tens of millions of USD. Varied provisions on data protection and confidential business information complicate submissions further, increasing legal risk and extending time-to-market.

Segment Analysis

By Ingredient: Polymers Drive Performance Innovation

Polymers generated 38% of 2024 revenue within the seed coating material market. Super-absorbent polymer gels are the fastest-rising ingredient class, surging at a 14.2% CAGR. Binders follow at 29.4%, while additives hold 12%. The ingredient mix is shifting toward starch-based binders, biodegradable polymers, and nanoparticle additives that elevate value capture. Zinc oxide and chitosan complexes have improved germination by 43%, showcasing the potential of nano-enabled coatings. Overall, the seed coating material market size for super-absorbent gels is expected to nearly double by 2030.

Premium pricing is strongest where polymers solve multiple pain points—adhesion, moisture control, and nutrient delivery, in a single pass. Suppliers of starch and hemicellulose binders are winning early contracts, especially in Europe, where buyers seek microplastic-free inputs ahead of 2028 enforcement. In Asia-Pacific, cost-sensitive growers still rely on polyvinyl acetate films, but subsidy programs tied to sustainability are nudging a gradual pivot toward bio-based options. As ingredient portfolios diversify, cross-licensing deals between chemical firms and microbial start-ups are accelerating time-to-market for next-generation formulations inside the seed coating material market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Process: Film Coating Dominates Precision Applications

Film coating captured 55% of 2024 process revenue due to its thin, uniform layers and compatibility with high-speed planters. Pelleting is projected to register a 15.5% CAGR as vegetable, flower, and small-seed acreage grows. Encrusting remains vital for cereals at a 24% share. Automation, real-time sensors, and low-dust formulations are widening performance gaps, helping firms command higher prices in the seed coating material market.

Regional equipment preferences shape process demand: pelleting machines dominate in greenhouse-heavy Netherlands, while drum film coaters lead in North American corn plants. Latin America is upgrading from batch coaters to continuous lines to keep pace with export seed standards, lifting throughput by 25% and trimming coating overuse. Vendors offering Internet-of-Things retrofits—temperature probes, airflow monitors, and feed-rate algorithms—are cutting downtime and cementing service revenues. These enhancements reinforce buyer confidence, supporting the seed coating material market share gains of process innovators.

By Function: Protection Leads, Enhancement Accelerates

Seed protection retained a 63% share of 2024 spending, underscoring the critical value of pathogen and pest control. Enhancement is the breakout category, advancing at a 13.8% CAGR as growers pursue vigor boosters and microbial consortia. Carbon credit programs reward coatings that improve soil carbon, linking agronomic benefits with environmental revenue streams.

Formulators now bundle biological fungicides with growth promoters to create dual-benefit coatings that shorten payback periods for growers. Trials in Australian wheat showed a 6-day emergence advantage when phosphite biostimulants were layered over systemic fungicides. Retailers report that enhancement-plus-protection SKUs fetch 15-20% higher margins, contributing disproportionately to the seed coating material market size. As digital scouting tools quantify stand counts and early vigor, data feedback loops will further validate premium functional stacks.

By Crop Type: Cereals Lead, Specialty Crops Accelerate

Cereals and grains held 46% revenue in 2024, while fruits and vegetables are slated for an 11.8% CAGR to 2030. Oilseeds follow at 28% as soybean acreage expands in the Americas. Specialty horticulture is opening space for color-coded pelleted seeds that aid automated transplanters, widening premium opportunities in the seed coating material market.

Demand patterns diverge by farming system. Broad-acre cereals favor low-cost film coats that carry systemic actives, whereas high-value vegetable seeds justify multi-layer pelleting with micronutrients and color branding. The expansion of controlled-environment agriculture in Gulf states is spurring orders for antifungal coatings that work under high humidity, while African groundnut programs focus on rhizobium-infused films to boost nitrogen fixation. These varied crop needs encourage suppliers to tailor SKUs, protecting seed coating material market share across diverse end-use segments.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Coating Type: Synthetic Dominates, Bio-based Surges

Synthetic systems delivered 61% of 2024 sales but face steady erosion as bio-based coatings grow at a 14.5% CAGR. Hemicellulose and plant-oil polymers meet abrasion benchmarks and comply with upcoming microplastic rules, enabling early movers to secure price premiums. Raw-material economics are driving the transition: crude-linked acrylic resins saw double-digit price swings in 2024, whereas corn-starch feedstock costs were comparatively stable. Large seed brands now request life-cycle assessments from coating vendors, favoring biopolymers with low greenhouse-gas footprints.

Pilot lots of lignin-based films in Canadian canola reduced dust by 35%, earning positive feedback from planter OEMs focused on operator safety. As regulatory credits for biodegradable inputs emerge, the seed coating material market share of bio-based technologies is set to climb faster than current forecasts imply.

Geography Analysis

North America held 35% of the 2024 seed coating material market share, supported by precision planting, trait stacking, and the widespread use of integrated coating packages. Suppliers bundle films, microbials, and lubricants within multi-year seed contracts, locking in steady adoption at a 9% CAGR through 2030. Corn, soybean, and canola account for most treated hectares, and recent vertical integration moves, such as Bayer’s Alberta canola facility, keep value in the region. Public-private funding for climate-smart farming also channels acreage toward premium coatings that improve stand establishment and water efficiency.

Asia-Pacific is the fastest-growing region, advancing at an 11.5% CAGR and now representing the second-largest seed coating material market size after North America. China’s seed revitalization strategy and India’s 6.5 lakh-hectare rise in 2025 summer sowing are scaling demand for hybrid seed treatments. Government subsidies on precision planters and drought-resilient varieties push the adoption of film and pelleting technologies across rice, wheat, and horticulture crops. Local formulators partner with multinational ingredient suppliers to customize starch binders and color additives for regional planting equipment.

South America follows with a 10.8% CAGR, led by Brazil, where bio-inputs grew 15% in 2023-2024 and support eco-labeled coatings for soybean and corn exports. Europe’s stringent microplastic ban is reshaping recipes, prompting early movers to secure compliant brands and pass on cost premiums to value-chain partners. Africa posts a 10.2% CAGR, although fragmented regulations slow market penetration; alliances with regional research institutes help suppliers validate microbial coatings under tropical storage conditions. Collectively, these regional dynamics diversify revenue streams while sustaining the global growth outlook for seed treatment technologies.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The seed coating material market shows moderate concentration: the five leaders hold 63% of the 2024 revenue. BASF SE leads through its broad polymer portfolio and service labs. Bayer CropScience follows with its SeedGrowth bundle. Syngenta's position is strengthened by Incotec’s microplastic-free coatings. Clariant follows via high-purity pigments, while Croda leverages bio-based adjuvants. Mid-tier specialists such as Germains, Roquette, Michelman, and Nufarm target niche crops and regional formulations. Strategic moves highlight consolidation and focus. Bayer purchased a canola coating site in Alberta to tighten vertical control. Syngenta divested FarMore to Gowan SeedTech, freeing resources for broad-acre innovation. BASF filed patents for heteroaryl compounds aimed at insect pests.

Mid-tier specialists, including Germains, Roquette, Michelman, and Nufarm, are carving niches by pairing crop-specific coatings with regional agronomic services. Germains focuses on color-coded pelleting for leafy-green seeds in protected horticulture, whereas Roquette scales pea-starch binders for European vegetable producers. Michelman partners with planter OEMs to certify low-dust primers, and Nufarm bundles biological actives with its Australian cereal seeds. These focused plays keep competitive pressure on the majors and push innovation cycles faster.

Large players are also reshaping portfolios through M and A and open-innovation alliances. Syngenta’s sale of its FarMore vegetable platform to Gowan SeedTech frees capital for broad-acre R and D, while BASF’s patent filings on heteroaryl insecticides hint at future trait-coating integrations. Bayer’s Alberta canola facility signals renewed interest in vertical control, and Clariant’s venture fund is scouting biodegradable pigment start-ups to future-proof its range. Together, these moves show a market where scale, sustainability credentials, and rapid technology transfer will decide share gains in the seed coating material market.

Seed Coating Materials Industry Leaders

-

BASF SE (BASF Group)

-

Bayer CropScience AG (Bayer AG)

-

Syngenta AG (Incotec owner)

-

Clariant International (Clariant AG)

-

Croda International (Croda Group)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Syngenta divested FarMore vegetable seed treatment to Gowan SeedTech while retaining proprietary supply rights.

- November 2024: Bayer acquired a canola treating and packaging facility in Coaldale, Alberta.

- December 2024: The Indian Institute of Oilseeds Research launched a nutrient-releasing biopolymer seed coating that can raise yields by 25-30% and licensed the technology to two domestic seed companies for nationwide rollout.

- January 2024: Lucent BioSciences launched Nutreo's biodegradable micronutrient coating.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we treat the seed coating materials market as the value generated from binders, polymers, additives, and colorants that are purposely applied as a discrete layer on commercial crop seed, either by film-coating, encrusting, or pelleting, to deliver protection or enhancement benefits before sowing.

All aftermarket seed dressings, on-farm slurry mixes, and standalone biological inoculants sold without a coating matrix are kept outside this calculation.

Segmentation Overview

- By Ingredient

- Binders

- Bentonite

- Polyvinyl Acetate

- Polyvinylpyrrolidone

- Methyl Cellulose

- Styrene-Butadiene Rubber

- Acrylics

- Waxes / Wax Emulsions

- Polymers

- Film-forming Polymers

- Super-absorbent Polymer Gels

- Additives

- Seed Planting Lubricants (Silicon, Talc, Graphite)

- Fertilizer Enhancers (Micronutrient Dispersant, N-Inhibitor, Solvents)

- Adjuvants

- Colorants

- Binders

- By Process

- Film Coating

- Encrusting

- Pelleting

- By Function

- Seed Protection

- Seed Enhancement

- By Crop Type

- Grains and Cereals

- Oilseeds

- Fruits and Vegetables

- Other Crops

- By Coating Type

- Synthetic

- Bio-based

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

To refine model inputs, we interview coating formulators, contract treaters, and farm-supply dealers across North America, Europe, Brazil, India, and Australia. Their insights on polymer price pass-through, film-coating versus pelleting share shifts, and grower adoption triggers let us challenge desk estimates and fine-tune regional penetration curves.

Desk Research

Our analysts sift through freely available yet authoritative data streams such as USDA crop acreage surveys, Eurostat pesticide statistics, FAOSTAT commodity balances, and ISF trade papers to size the sown seed pool and typical treatment penetration. Company 10-Ks, patent filings captured through Questel, and Dow Jones Factiva news archives supply pricing clues and technology timelines, while trade-body briefs from CropLife International and the American Seed Trade Association clarify regulatory milestones that shape ingredient uptake. The sources named here illustrate, not exhaust, the secondary backbone we reference.

Market-Sizing & Forecasting

We begin with a top-down construct that rebuilds the demand pool from certified seed output, average treatment rate (kilograms of coating per metric ton of seed), and ingredient blended value; selective bottom-up roll-ups of supplier shipments and sampled ASP × volume checks act as guardrails. Key variables like hectares under precision planting, polymer-to-bio-binder substitution ratios, EU microplastic phase-out deadlines, and cereal seed replacement cycles feed a multivariate regression that projects value through 2030. Where bottom-up totals diverge beyond a ±5 % band, assumptions are revisited with interviewees before final lock.

Data Validation & Update Cycle

Every draft passes a two-level analyst review in which outliers are flagged against historical series, competitor filings, and customs codes. Models refresh annually, yet trigger events, such as regulatory bans, large M&A, or a ≥10 % raw-material price swing, prompt an interim update so clients always see our freshest view.

Why Mordor's Seed Coating Materials Baseline Inspires Confidence

Published numbers vary because firms choose dissimilar ingredient baskets, coating processes, and refresh frequencies.

Scope breadth, price defaults, and assumed coating rates shift totals further.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.10 B (2025) | Mordor Intelligence | - |

| USD 2.19 B (2025) | Global Consultancy A | Omits bio-based binders; applies single flat ASP across regions |

| USD 2.21 B (2025) | Industry Journal B | Uses seed volume for top five crops only; refresh cadence biennial |

| USD 2.68 B (2025) | Regional Consultancy C | Relies on manufacturer shipment lists without adjusting for distributor mark-ups |

The comparison shows how narrower scope or slower updates compress totals.

By combining continually refreshed public statistics with expert cross-checks and dual-track modeling, Mordor delivers a transparent, balanced baseline that decision-makers can retrace and replicate.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the size of the seed coating material market in 2025?

It stands at USD 3.1 billion in 2025 and is projected to reach USD 5.4 billion by 2030, growing at an 11.8% CAGR.

Which ingredient segment is expanding the fastest?

Super-absorbent polymer gels lead growth at a 14.2% CAGR because they store water and help crops withstand drought.

How will EU microplastic rules affect seed coatings?

Formulators must remove intentional microplastics by 2028, accelerating the shift toward biodegradable and bio-based binders.

Which region shows the highest growth potential?

Asia-Pacific is forecast to expand at an 11.5% CAGR, driven by hybrid-seed adoption in China, India, and Southeast Asia.

What share of the market do the top five companies control?

BASF SE, Bayer CropScience, Syngenta, Clariant International, and Croda International together command 63% of global revenue.

How are carbon credits influencing coating demand?

Microbial films that raise soil carbon allow growers to claim offset revenue, adding an extra incentive to adopt advanced coatings.

Page last updated on: