US Turf And Ornamental Protection Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

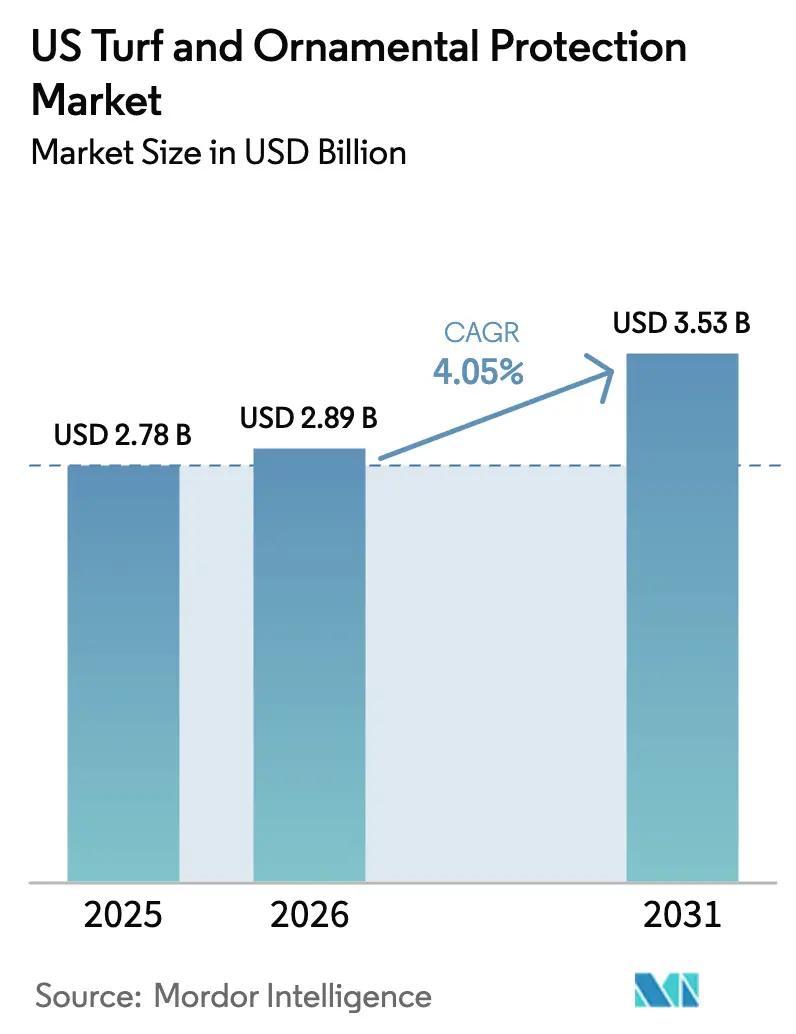

| Base Year Market Size (2025) | USD 2.78 Billion |

| Market Size (2026) | USD 2.89 Billion |

| Market Size (2031) | USD 3.53 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

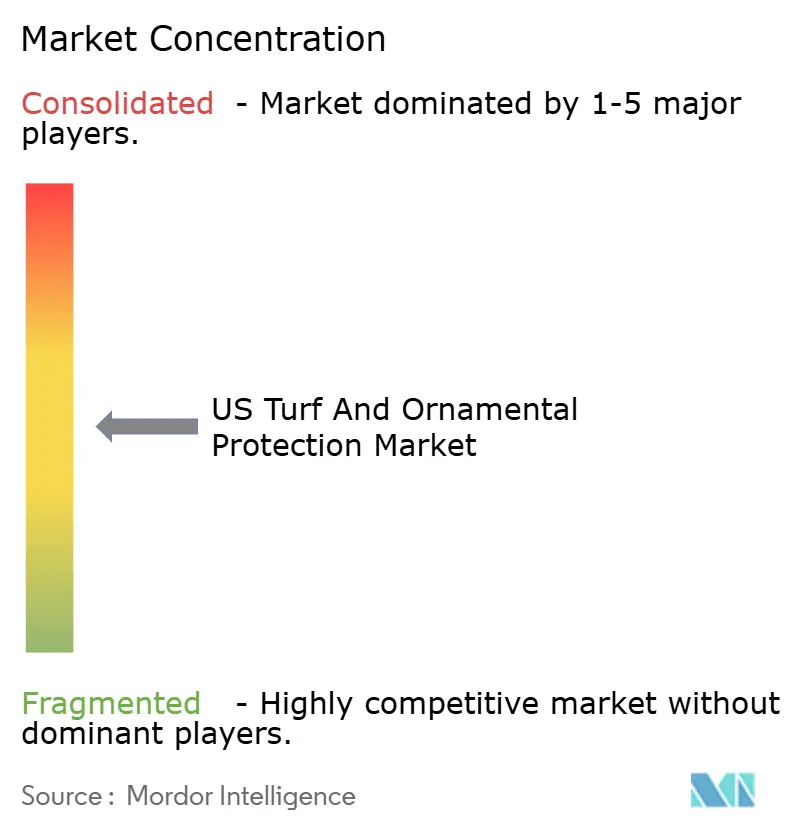

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Turf And Ornamental Protection Market Analysis by Mordor Intelligence

The US turf and ornamental protection market size was valued at USD 2.78 billion in 2025 and estimated to grow from USD 2.89 billion in 2026 to reach USD 3.53 billion by 2031, at a CAGR of 4.05% during the forecast period (2026-2031). The outlook reflects a decisive swing from blanket applications toward precision programs that integrate resistance management, low-drift delivery, and data-guided scheduling. Consolidation among professional lawn-care franchises is increasing product volumes, as national operators secure premium herbicide and fungicide rotations to maintain service quality. Golf course and sports-turf expansion adds structural demand, while state restrictions on gas-powered equipment accelerate the use of liquid chemistries that pair well with electric sprayers. At the same time, pollinator-friendly initiatives and AI-enabled diagnostics expand the addressable market for bio-insecticides and decision-support tools that sharpen efficacy per dollar spent[1]Source: Environmental Protection Agency, “Pesticide Registration Process,” epa.gov.

Key Report Takeaways

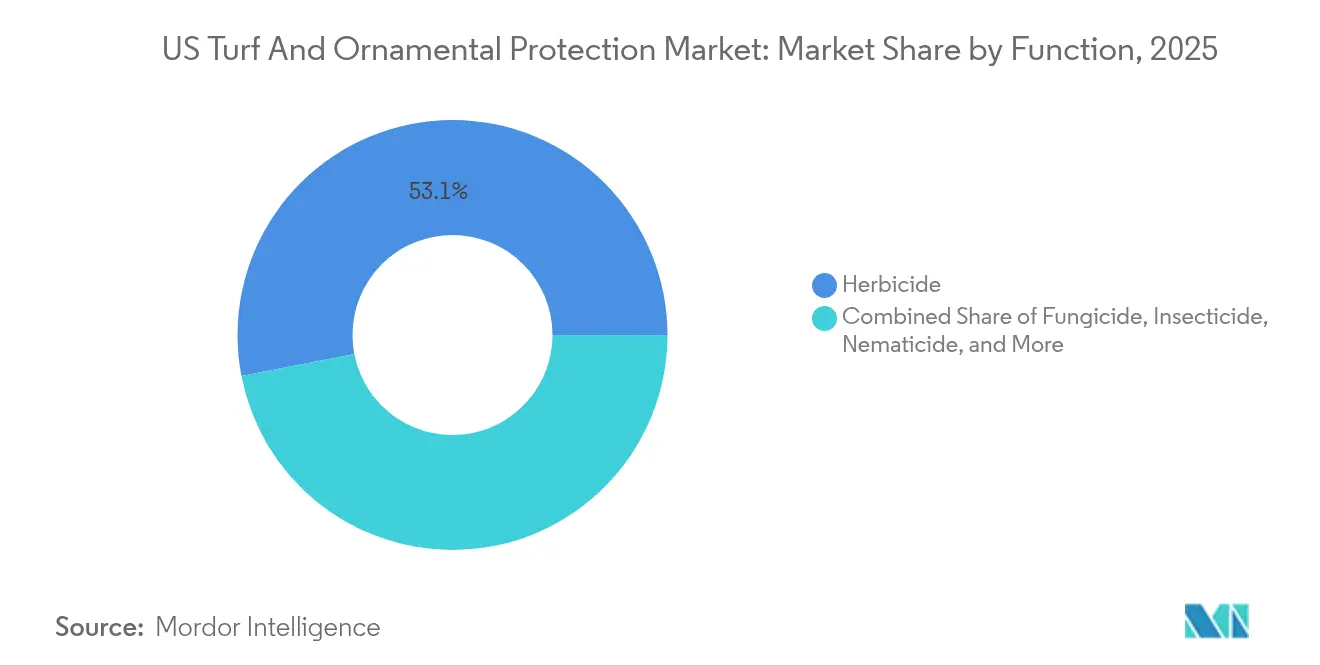

- By function, herbicides led the US turf and ornamental protection market share with 53.05% in 2025 and are projected to record the highest CAGR of 4.7% through 2031.

- By application mode, foliar treatments accounted for 40.18% of the US turf and ornamental protection market size in 2025, and soil treatment is projected to record the highest CAGR at 4.45% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Turf And Ornamental Protection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of herbicide-resistant weeds | +0.8% | Southeast and Southwest | Medium term (2–4 years) |

| Expansion of the professional lawn-care service industry | +1.2% | Suburban metro areas | Long term (≥ 4 years) |

| Growth of golf courses and sports turf acreage | +0.9% | Texas, Florida, California | Long term (≥ 4 years) |

| State bans on gas-powered lawn equipment are accelerating low-drift chemistries | +0.6% | California, New York, Northeast corridor | Short term (≤ 2 years) |

| Surge in AI-driven turf diagnostics platforms boosting chemical sales | +0.7% | Premium golf markets | Medium term (2–4 years) |

| Municipal pollinator-friendly city initiatives favoring targeted bio-insecticides | +0.5% | Urban corridors | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of herbicide-resistant weeds

Poa annua and goosegrass have evolved biotypes that survive popular actives, leaving unsightly stands that disrupt ball roll and turf uniformity[2]Source: University of Georgia Cooperative Extension, “Herbicide Resistance Management in Turf,” extension.uga.edu. Course superintendents now rotate at least four modes of action during a single growing season to halt resistance shifts. The practice lifts chemical spending because patented actives deliver reliable control while commanding premium prices. Retail distributors confirm a noticeable shift toward indaziflam and mesotrione, as these molecules offer year-round residual activity. Consulting revenue rises in parallel because managers pay for mapping and rotation plans that maximize each spray window. The same mindset is spilling into high-end residential lawns where customers demand tour-quality aesthetics.

Expansion of the professional lawn-care service industry

TruGreen, Lawn Doctor, and similar franchises now blanket most large metro areas, purchasing inputs through national contracts that guarantee volume tiers and preseason rebates. Central agronomy teams lock in specific fungicide, herbicide, and fatty-acid insecticide rotations, creating predictable warehouse pulls that smooth demand for suppliers. The arrangement reduces price sensitivity, since contractors value consistency and service documentation over lowest unit cost. Independent operators respond by marketing organic programs that feature bio-rational insecticides and seaweed biostimulants, carving out local identity rather than matching corporate firepower. This polarity widens the addressable market, as premium synthetics and eco-labels expand in tandem.

Growth of golf courses and sports turf acreage

After years of flat growth, 47 new courses opened in 2024, each requiring high-rate soil fumigation and repeated fungicide drenches during grow-in[3]Source: Golf Course Superintendents Association of America, “Golf Course Construction and Renovation Report,” gcsaa.org. Renovations on 312 existing sites further extend chemical demand because rebuilt greens, tees, and bunkers need pathogen protection until roots mature. Sports-field construction mirrors the pattern: hybrid surfaces combine natural and synthetic fibers yet still rely on aggressive weed, insect, and nematode control. Owners pursue twelve-month play schedules that leave little downtime, so spray programs are carefully stacked to maintain safe traction and color. Chemical makers now bundle seed, fertilizer, and pesticide packages targeted at these multi-year projects. The backlog of planned facilities signals a steady pull-through beyond 2026.

State bans on gas-powered lawn equipment are accelerating low-drift chemistries

California’s ban on new gasoline engines with a displacement of less than 25 horsepower took effect in 2024, forcing contractors to adopt battery-powered sprayers and robotic mowers[4]Source: California Air Resources Board, “Small Off-Road Engine Regulations,” arb.ca.gov. Liquid herbicides with drift-reducing surfactants are better suited for low-pressure nozzles than traditional granules, which require heavier spreaders. New York, Connecticut, and several Northeastern cities are following a similar path, accelerating efforts by suppliers to convert high-volume actives into flowable suspensions or microemulsions. Electric rigs often include pulse-width-modulated booms that vary output by square foot, so precise droplet sizing is critical. R and D teams are testing polymers that keep droplets intact at slower speeds, ensuring uniform coverage while extending battery life. Granular fertilizer-pesticide combos are losing shelf space as a result.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EPA and state pesticide re-registration hurdles | −0.7% | National | Long term (≥ 4 years) |

| Rising input-cost inflation for active ingredients | −0.9% | All regions | Short term (≤ 2 years) |

| Rapid uptake of autonomous mowing robots reducing herbicide demand on sports fields | −0.4% | Premium facilities | Medium term (2–4 years) |

| Micro-parcel delivery drone restrictions curbing aerial foliar treatments | −0.3% | Urban airspace | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent EPA and state pesticide re-registration hurdles

The enhanced federal docket now demands full-season pollinator feeding trials, groundwater fate modeling, and cumulative risk assessments before any active renewal moves forward. California layers volatile-organic-compound caps and drift-potential modeling on top, further lengthening review cycles. Large firms absorb the extra toxicology work by reallocating internal scientists; yet, start-ups often stall because third-party studies can cost over USD 4 million per molecule. Distributors anticipate gaps and place higher early-buy orders on actives nearing review to avoid potential outages. The lag favors incumbents and slows the turnover of older chemistries, muting near-term innovation.

Rising input-cost inflation for active ingredients

Ocean freight rates have declined from their 2024 highs, yet capacity for key intermediates in China and India remains constrained, resulting in delivered prices for azoxystrobin and fluopyram remaining 20% above pre-pandemic levels. Multi-year lawn-care contracts limit pass-through, so service providers compress overhead by leaning on generic blends and reduced-rate mixes. Some operators adopt slow-release granular carriers that extend intervals between sprays, trading higher material cost for labor savings. Manufacturers respond with rebate tiers tied to annual spend, locking customers into volume commitments that guarantee plant utilization. Volatility persists as currency swings and energy costs ripple through the supply chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Herbicides remain the pillar for resistance management.

Herbicides captured 53.05% of the US turf and ornamental protection market share in 2025, and are projected to record the highest CAGR of 4.7% through 2031. Reflecting their indispensable role in combating weeds that are continually adapting to new environments. Warm-season arenas in the Southeast rely heavily on residual pre-emergents, such as indaziflam and dithiopyr, which secure fairways for up to eight weeks. In contrast, cool-season venues utilize mesotrione for selective post-emergence control without bleaching. Broad distribution, predictable efficacy, and clear economic payback keep herbicides at the center of budget allocations even when prices spike.

Fungicides rank second, as wetter summers elevate the prevalence of dollar spot and brown patch, prompting superintendents to adopt multi-site mixtures that delay the onset of resistance. Insecticides advance unevenly: pollinator-safe larvicides gain in public parks, but broad-spectrum pyrethroids soften as municipalities tighten runoff rules. Nematicides post the quickest percentage rise because root-knot infestations drastically reduce green speed and shoot density; growers accept niche prices to protect revenue. Combo formulations that overlay fungicides on pre-emergent bases are poised to grow because they simplify labor scheduling.

By Application Mode: Foliar dominates, but soil treatments grow faster

Foliar sprays held 40.18% of the US turf and ornamental protection market size in 2025, due to their visible green-up effect within days, a benefit prized by golf committees and homeowners alike. Sprayers already roll daily for fertility and pigment passes, so folding in herbicides or fungicides adds little incremental labor. Precision booms equipped with section control cut overlap, reinforcing foliar economics on irregular fairway shapes.

Soil treatment held a 4.45% CAGR because it front-loads weed and nematode suppression, allowing staff to focus on cultural practices mid-season. Chemigation shines on fairways exceeding 40 acres where pivot or lateral-move lines already water nightly, delivering actives evenly while eliminating wheel-track compaction. Fumigation remains a niche yet essential process when reconstructing greens on sand-capped profiles, where pathogens thrive in sterile yet moisture-retentive layers. Seed-applied insecticides climb slowly, carried by the rise of overseeding into bermudagrass to maintain winter color. Managers increasingly layer both modes, deploying soil pre-emergents at renovation, then topping with foliar rescue sprays during heavy tournament schedules.

Geography Analysis

The Southeast commanded a significant portion of share of the US turf and ornamental protection market share in 2025, due to its eight-month growing seasons and year-round golf tourism, which stretch maintenance windows. Warm, humid conditions foster dollar spot, spring dead spot, and aggressive Poa annua encroachment, driving robust herbicide and fungicide rotations that seldom experience true dormancy. Residential new-builds in Florida and Georgia continue to feature St. Augustine and zoysia lawns that require dedicated broadleaf weed control programs. Even as counties impose nutrient runoff ordinances, chemical inputs remain essential to maintain property values and sports tourism revenue. The forecast of 4.05% CAGR through 2031 anchors nationwide growth, as the region combines high acreage with high intensity.

The Northeast is underpinned by affluent suburbs and densely scheduled collegiate sports calendars. Cool-season grasses germinate rapidly in April, requiring synchronized pre-emergent herbicides before soil temperatures reach 55°F and crabgrass germination occurs. A compressed spray calendar concentrates orders into spring and again in early fall, creating pronounced warehouse peaks that distributors manage through early-order discount programs. State restrictions on certain neonicotinoids and 2,4-D variants spur trials of bio-insecticides and iron-based broadleaf killers. Long winters invite snow mold, so superintendents still apply preventative fungicides before closing greens, preserving a lucrative December shipping lane.

Western states captured a significant portion in 2025, with California alone spanning multiple microclimates, from foggy coastal ryegrass to desert bermudagrass. Water scarcity influences chemical selection, steering users toward wetting-agent blends and soil penetrants that also serve as fungicide carriers. Regulatory oversight remains strict, with low-drift labeling and carbon-intensity audits often accompanying bid specifications. Pacific Northwest courses battle annual bluegrass weevil and dollar spot under prolonged dew periods, boosting systemic fungicide demand despite cooler temperatures. The balance of 12% sits in the Midwest and Mountain West, where shorter seasons cap application counts, yet unique pests like snow mold and alkali-soil weeds support focused portfolios. Altitude also moderates UV degradation, allowing for longer residual periods and wider spray intervals, which influence product choice.

Competitive Landscape

The US turf and ornamental protection market is characterized by moderate concentration, with the top five suppliers collectively holding a significant share of the market revenue in 2024. This leaves nearly half of the revenue for regional or niche specialists to capture through agile services and localized chemistry. Corteva Agriscience leads, leveraging a full seed-to-spray bundle and field agronomists who troubleshoot on-site within 24 hours. Nufarm follows, emphasizing post-patent actives positioned with proprietary surfactants that lift performance against tough weeds while keeping cost attractive. Environmental Science U.S., spun from Bayer assets, sits third and invests heavily in GPS-linked variable-rate sprayers that showcase product stewardship. BASF SE, FMC Corporation, and Environmental Science U.S. LLC (Cinven Group Limited) round out the next tier, each sharpening focus on novel modes of action to sidestep looming resistance issues.

Technology integration now defines competitive edge more than sheer portfolio breadth. Suppliers package cloud analytics that track spray timing, nozzle choice, and weather overlays, then benchmark results against anonymous peer courses. Customers can justify premium pricing because dashboards convert chemistry performance into quantifiable playability metrics such as stimpmeter speed and divot recovery days. Patent filings cluster around low-drift micro-encapsulations and dual-mode fungicides that satisfy EPA “reduced risk” labeling, permitting faster registration and marketing push. Firms with deep regulatory teams move first, creating a temporary moat as rivals compile the extensive pollinator and groundwater data now required.

Distribution strategy continues to splinter. National franchises prefer direct ship models with season-long consignment, while independent golf clubs still order through regional distributors that provide same-day delivery and nozzle calibration clinics. Some suppliers invest in e-commerce portals that integrate with AI diagnostics; orders auto-populate once a threshold of disease severity is triggers. Others secure growth through targeted acquisitions, such as Nufarm’s 2024 purchase of eight warehouses in the Southeast, which strengthened superintendent relationships and improved last-mile logistics. Amid these moves, customer loyalty hinges on technical support as much as price, so companies staff larger territories with Certified Crop Advisors who solve problems in real time.

US Turf And Ornamental Protection Industry Leaders

Nufarm Limited

Environmental Science U.S. LLC (Cinven Group Limited)

FMC Corporation

BASF SE

Corteva Agriscience

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Corteva announced an expanded label for HighNoon herbicide, making the reduced-risk liquid formulation available nationwide for control of more than 140 broadleaf weeds and annual grasses.

- October 2025: The U.S. EPA approved an expanded label for FMC’s Elevest insect control, extending use to additional specialty crops and permitting an in-furrow application method for row-crop soil pests.

- March 2025: Agmatix and BASF have formed a strategic partnership to develop an AI-powered digital tool that detects and predicts soybean cyst nematode infestations, integrating BASF’s crop protection expertise with Agmatix’s Axiom data engine.

US Turf And Ornamental Protection Market Report Scope

Fungicide, Herbicide, Insecticide, Molluscicide, Nematicide are covered as segments by Function. Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode.| Fungicide |

| Herbicide |

| Insecticide |

| Molluscicide |

| Nematicide |

| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

| Function | Fungicide |

| Herbicide | |

| Insecticide | |

| Molluscicide | |

| Nematicide | |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment |

Market Definition

- Function - Crop Protection Chemicals are apllied to control or prevent pests, including insects, fungi, weeds, nematodes, and mollusks, from damaging the crop and to protect the crop yield.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Turf and Ornamental crops in United States

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms