Market Overview

| Study Period | 2021 - 2031 |

|---|---|

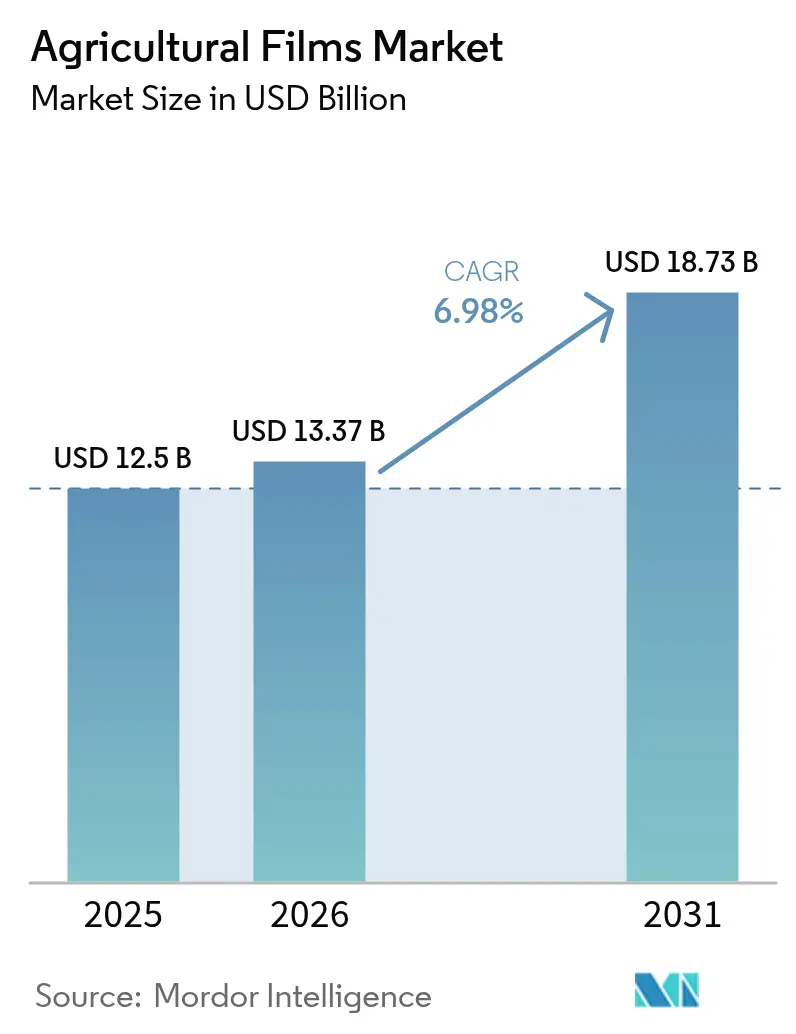

| Market Size (2026) | USD 13.37 Billion |

| Market Size (2031) | USD 18.73 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

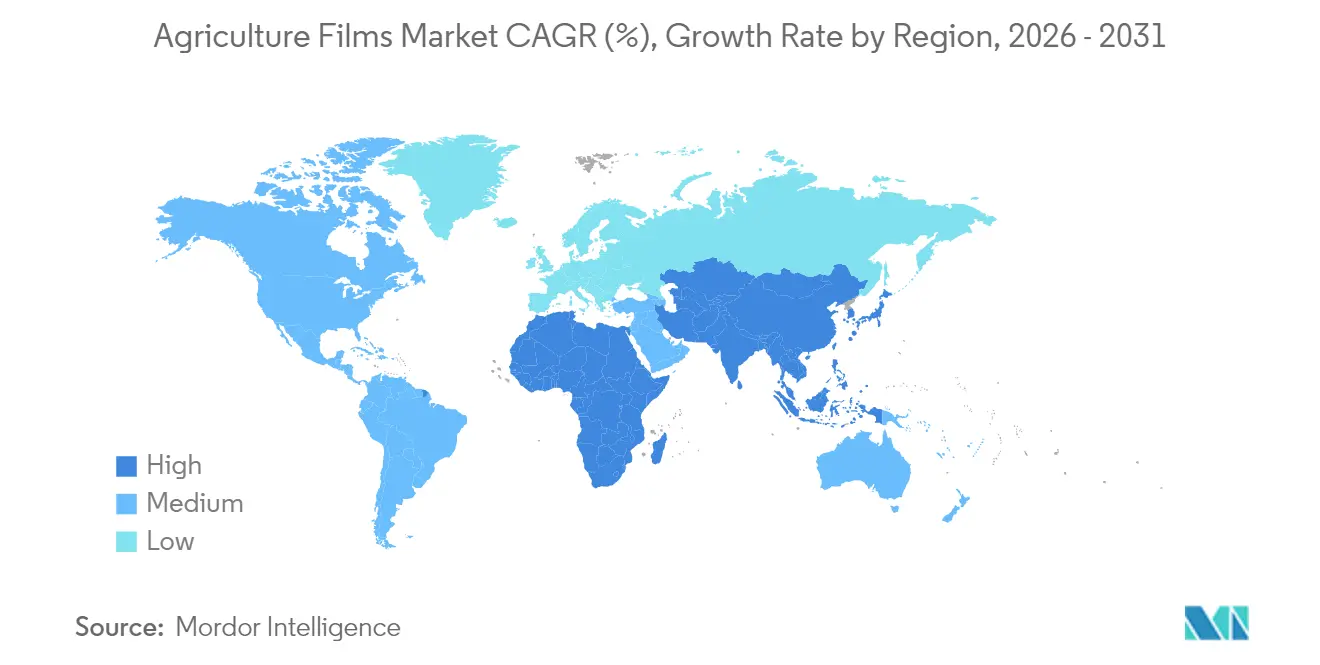

| Fastest Growing Market | Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Films Market Analysis by Mordor Intelligence

The agricultural films market size is expected to grow from USD 12.50 billion in 2025 to USD 13.37 billion in 2026 and is forecast to reach USD 18.73 billion by 2031 at 6.98% CAGR over 2026-2031. Current momentum is driven by the rapid adoption of greenhouses in land-constrained regions, rising water-stress mitigation through mulching, and continued innovation in advanced polyethylene (PE) chemistries that enhance optical, mechanical, and barrier properties while reducing thickness. Governments channel subsidy programs toward protected cultivation, accelerating capital investment in controlled-environment structures and driving compound demand for specialty greenhouse covers, diffusive mulches, and oxygen-barrier silage wraps. Resin producers, film extruders, and equipment manufacturers collaborate on multilayer formulations that incorporate recycled content, thereby strengthening circular economy credentials without compromising crop protection attributes. However, price volatility in ethylene feedstocks, tightening disposal regulations, and the high capital intensity of hi-tech greenhouse infrastructure create headwinds that manufacturers must offset with cost-effective downgauging, sourcing diversification, and new biodegradable offerings.

Key Report Takeaways

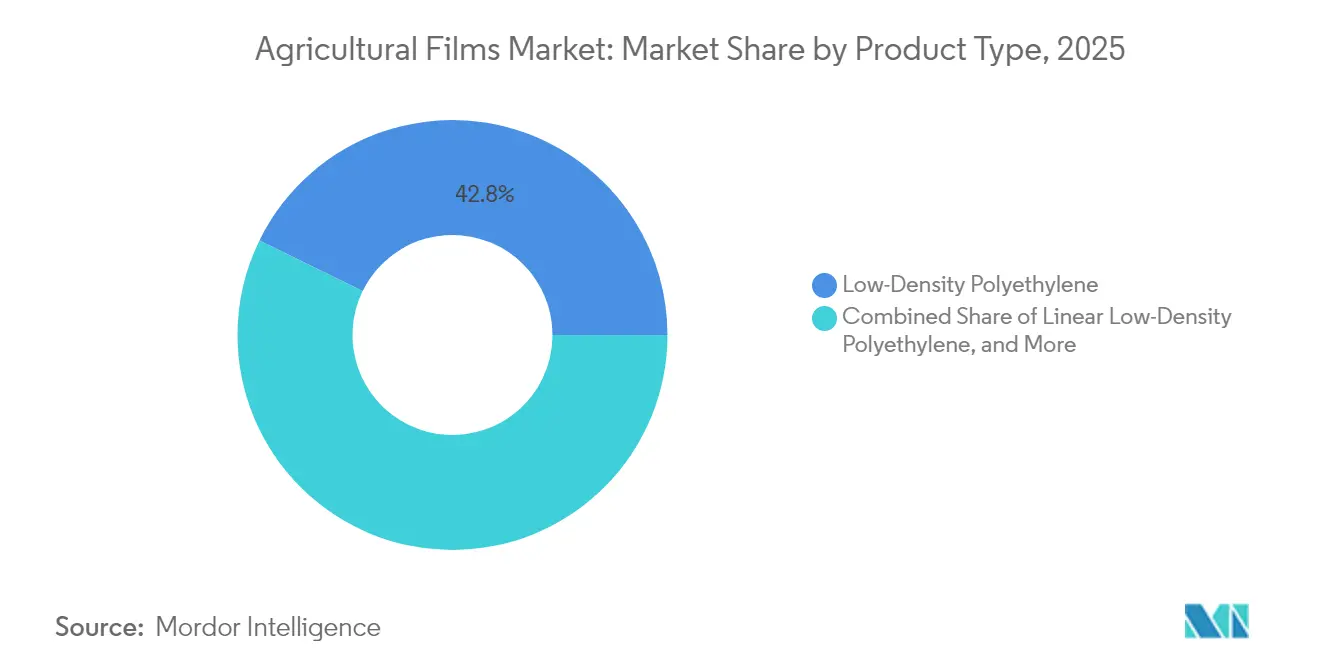

- By type, Low-Density Polyethylene led with 42.75% of the agricultural films market share in 2025, while Reclaims is forecast to expand at an 8.35% CAGR through 2031.

- By thickness, the 80 µm to 150 µm range captured 55.35% revenue share in 2025, while those above 150 µm are projected to register a 7.22% CAGR to 2031.

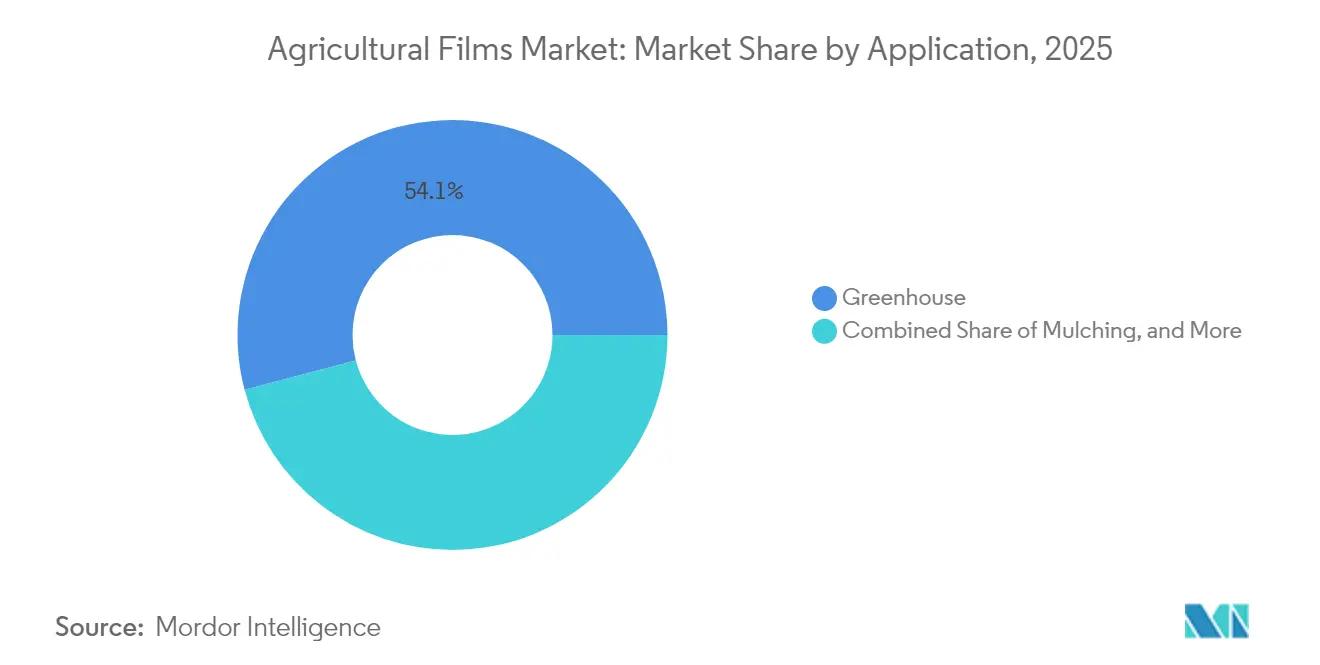

- By application, greenhouse cultivation accounted for a 54.10% share of the agricultural films market size in 2025, and mulching is projected to grow at a 7.48% CAGR to 2031.

- By geography, Asia-Pacific held 37.10% revenue share in 2025. Africa is anticipated to post the fastest 8.85% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agricultural Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of greenhouse cultivation | +1.8% | Global, with a concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Growing popularity of mulching to curb evaporation | +1.2% | Global, particularly in water-stressed regions | Short term (≤ 2 years) |

| Government subsidies for protected cultivation | +1.0% | Asia-Pacific, Africa, select Europe regions | Medium term (2-4 years) |

| Surge in demand for photo-selective spectral films | +0.9% | North America, Europe, and advanced Asian markets | Long term (≥ 4 years) |

| Farm-level shift toward recycled-content films | +0.7% | Europe, North America, with spillover to Asia | Medium term (2-4 years) |

| Carbon-credit monetization for biodegradable films | +0.6% | Europe, North America, and the emerging Asia-Pacific region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of greenhouse cultivation

Protected cultivation now extends from high-value horticulture to staple crops, delivering yield increases of 25–40% and supporting year-round supply continuity[1]Source: Yujin Park and Erik S. Runkle, “Spectral-Conversion Film Potential for Greenhouses,” PLOS ONE, journals.plos.org. Automation and artificial-intelligence climate controls lower labor inputs, enabling mid-scaled growers to enter the segment. Substrate-based systems eliminate soil-borne disease vectors and require sterile barrier films with superior impermeability, spurring demand for multilayer PE structures. Cannabis, nutraceutical, and pharmaceutical crops command premium film specifications that optimize wavelength management, thermal retention, and diffused light distribution. Greenhouse operators in British Columbia forecast an 18% vegetable-output lift by 2025 through renewable-energy integration that further lowers operational overhead.

Growing popularity of mulching to curb evaporation

Plastic mulch films cut irrigation volumes 30–50% in arid zones and increasingly underpin regeneration practices within conservation agriculture. Global consumption has surpassed 2 million metric tons, with Asia accounting for the bulk due to intensive vegetable systems. Reflective films lower soil-surface temperatures 4–6 °C, extending cropping windows in heat-stressed climates. Biodegradable innovations meet organic-certification needs and reduce labor associated with film retrieval, though elevated cost remains an adoption hurdle. Variable-rate mulch applicators paired with precision agriculture data help growers optimize film thickness and placement, reinforcing resource-efficiency goals. Chinese directives mandating thicker mulch to improve recyclability push material science toward higher-strength formulations that withstand multiple cycles.

Government subsidies for protected cultivation

Targeted financial incentives cover up to 80% of greenhouse construction costs in select Asian programs, catalyzing capital flow into high-specification polyhouse projects. African export-oriented horticulture receives concessional credit that accelerates greenhouse uptake and boosts foreign-exchange earnings from floriculture and fresh-produce shipments. Philippine smart-greenhouse cost-benefit studies demonstrate internal rates of return above 19% for mushroom production, illustrating strong payback potential when value-chain integration is achieved. Subsidy frameworks embed minimum technical standards that lift baseline film quality and stimulate domestic manufacturing of UV-stabilized, diffusion-enhanced covers.

Surge in demand for photo-selective spectral films

Quantum-dot and luminescent films convert under-utilized green wavelengths into red photons, raising light-use efficiency and boosting tomato yields in commercial trials. Integrating photovoltaic layers enables co-generation of electricity, offsetting greenhouse operating costs and aligning with carbon-neutral objectives. Crop-specific “light recipes” optimize flowering, pigmentation, and nutritional density, widening the addressable market beyond ornamentals to leafy greens and specialty herbs. Patent filings for spectral modification technologies continue to climb, signaling persistent innovation rivalry and long-term product-pipeline depth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial investment in greenhouse infrastructure | -1.4% | Global, particularly in developing regions | Short term (≤ 2 years) |

| Environmental concerns over the disposal of PE films | -1.1% | Europe, North America, and emerging in Asia | Medium term (2-4 years) |

| Volatility in ethylene feedstock pricing | -0.8% | Global, with regional supply chain variations | Short term (≤ 2 years) |

| Lack of standardized film recovery logistics | -0.6% | Global, most acute in developing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High initial investment in greenhouse infrastructure

Hi-tech greenhouses demand USD 2,500–4,000 per m² compared with USD 400–500 for low-tech counterparts, posing steep upfront barriers for smallholders. Beyond construction, climate controls, fertigation, and energy systems can consume 40% of annual revenue, challenging profitability when produce prices fall. Limited collateral and high interest rates restrict access to credit, especially in frontier economies. Equipment leasing models and pay-as-you-grow service contracts ease the capital strain but require robust extension support. Financial viability varies by crop, and shiitake mushrooms yield internal returns, yet melons remain unprofitable under identical cost structures.

Environmental concerns over disposal of PE films

An estimated 9% of United States agricultural film waste enters recycling streams, and contamination rates up to 80% hinder material recovery. Soil-embedded fragments can persist for over a decade, posing risks to long-term fertility and raising concerns about microplastics[2]Source: Martin Geyer, “Plastic Mulch Films in Agriculture,” MDPI, mdpi.com. The European Union's plastic-packaging tax, currently set at USD 283 per metric ton, increases disposal costs and encourages growers to adopt alternative materials. Biodegradable options command price premiums and may exhibit lower mechanical robustness, which can slow down substitution in heavy-duty applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: LDPE Maintains Lead while Reclaims Accelerate

Low-Density Polyethylene held 42.75% agricultural films market share in 2025, underpinned by its balanced cost-to-performance ratio and ease of extrusion into covers. The material’s dominance stems from superior optical clarity and elongation properties that minimize mechanical stress during installation. The industry’s pivot to sustainability is catalyzing an 8.35% CAGR for Reclaims through 2031, aided by multilayer designs that embed recycled content without compromising crop-facing functionality. Chemical advances in compatibilizers allow higher PCR ratios, mitigating odor and gel issues that historically constrained recycled-PE uptake.

Linear-Low-Density Polyethylene adds puncture resistance requested by silage users, while Ethyl Vinyl Acetate copolymers impart enhanced light diffusion for premium greenhouse films. High-density polyethylene and specialized resins, such as polyamide, address niche requirements for structural rigidity and solvent resistance, but remain cost-limited. Rising demand for downgauged films drives the need for high-melt-strength grades that sustain tensile integrity at reduced thickness, thereby compressing resin usage metric tons per hectare and lowering the overall plastic footprint.

By Thickness: Durability Drives Premium Gauge Adoption

The 80 µm to 150 µm band captured 55.35% agricultural films market share in 2025, delivering a cost-to-performance sweet spot that satisfies mainstream greenhouse, mulching, and silage operations. Growers value moderate puncture resistance that withstands mechanized laying machines and occasional foot traffic without inflating purchase budgets. This thickness class aligns well with single-season horticulture cycles and facilitates easy retrieval for recycling programs, making it the default option across diversified farming landscapes.

Segments above 150 µm are set to expand at a 7.22% CAGR, marginally outpacing the overall agricultural films market. Heavy-gauge films now protect mega-greenhouses in wind-prone coastal corridors where material failure could halt production and incur multi-million-dollar crop damage. Sub-80 µm products continue to serve low tunnels and frost-protection shrouds where growers value minimal material cost for short rotations, yet the trend across capital-intensive ag pivots toward total cost of ownership, supporting durability-focused gauges that promise multi-season survivability.

By Application: Greenhouse Dominance amid Rapid Mulching Uptake

Greenhouse films accounted for 54.10% of the agricultural films market size in 2025, driven by the intensive cultivation of vegetables, floriculture, and emerging pharmaceutical crops that require high light transmission and anti-condensation properties. Photoselective and near-infrared-reflective technologies reduce internal heat load, thereby decreasing energy expenditure for cooling in warm climates. Mulching segments are scaling at a 7.48% CAGR, as water-scarcity pressures incentivize moisture-retention strategies across row crops, orchards, and vineyards. Regulatory moves restricting the open-field burning of PE residues have accelerated interest in soil-degradable alternatives, and trials have shown that biodegradable mulches match San Marzano tomato yields while simplifying post-harvest field preparation.

Silage films remain a steady yet innovation-rich niche, with oxygen-barrier multi-layer wraps reducing dry-matter losses by up to 65% compared to mono-layer PE. Downgauging via performance PE grades, such as ExxonMobil’s Exceed S, lowers material costs for large dairy operations while maintaining puncture resistance. Other specialty applications include low tunnels that accelerate early-season harvests and fumigation films that restrict pesticide volatilization.

Geography Analysis

Asia-Pacific held 37.10% of the agricultural films market in 2025, driven by extensive greenhouse acreage in China and subsidy-backed modernization programs in India, Japan, and South Korea. Regional manufacturers have cost advantages and benefit from a localized supply of stabilizer additives and extrusion machinery, enabling rapid product iteration. Domestic innovation focuses on diffusive films that counteract high solar-irradiation intensity while optimizing crop photosynthetic efficiency. Government programs targeting plastic waste reduction prompt the development of thicker, recyclable mulch variants, cementing local research collaborations between resin producers and agricultural institutes.

Africa represents the fastest-growing territory with a projected 8.85% CAGR through 2031, supported by horticultural export expansion and favorable trade preferences. Kenya's floriculture valorizes protected cultivation, generating and guiding neighboring economies toward greenhouse models. South African bioplastics leverage duty-free access under the African Growth and Opportunity Act, offering cost-competitive biodegradable inputs for regional film converters. Despite growth potential, endemic infrastructure gaps in film retrieval and recycling constrain circular-economy ambitions.

Europe and North America illustrate mature yet dynamic markets where sustainability regulation spurs continual material advancement. The European Commission's 2025 update to food-contact regulations imposes stricter purity thresholds, compelling film formulators to refine additive packages and contamination-control protocols. Middle East investments in water-efficiency and year-round production use high-diffusion covers paired with desalinated or recycled water in closed-loop systems, while South American and Oceanian niche segments favor specialty mulch and silage products aligned with export-driven produce quality requirements.

Regulatory Landscape

Regulation is increasingly shaping material selection, labeling, and end-of-life pathways for agricultural films, particularly in mulching applications where microplastics and soil contamination concerns drive scrutiny. In the European Union, Commission Delegated Regulation (EU) 2024/2787 integrated soil-biodegradable mulch films into the Fertilising Products Regulation framework (under a dedicated component material category). This formalized performance and labeling expectations for certified soil-biodegradable products and pushed suppliers toward standardized conformity documentation.

Standards updates and adjacent policy changes also affect film formulation and supply chain practices. BS EN 13206:2025 updates requirements and test methods for thermoplastic covering films used in agriculture and horticulture, influencing qualification protocols for greenhouse covers and other protective films sold into regulated procurement and subsidy-linked programs. In parallel, Commission Regulation (EU) 2026/1123 introduces new labeling requirements for plant protection products (applicable from 2028). While it does not directly regulate films, it reinforces traceability and compliance practices across crop-protection inputs that film suppliers increasingly align with when marketing integrated protected-cultivation solutions.

Competitive Landscape

The market is moderately fragmented, with no dominant global player, enabling regional converters to hold meaningful shares in local distribution networks. Consolidation is gaining pace, exemplified by the USD 650 million synergy-targeted all-stock merger between Amcor and Berry Global that elevates combined R&D expenditure to USD 180 million annually[3]Source: Amcor Plc., “Amcor and Berry to Combine,” amcor.com. The enlarged entity prioritizes downgauged, recycled-content agricultural structures and reinforces supply security through backward integration in resin compounding.

Incumbents differentiate by investing in proprietary additive packages. BASF SE's pending divestiture of its agricultural activities underscores the strategic optimization of its portfolio while preserving access to ecovio compostable technologies. Novamont's collaboration with Bayer CropScience on Mater-Bi ties biodegradable materials to crop-input portfolios, broadening total solution offerings for growers in 2024.

Strategic moves emphasize vertical integration, as resin suppliers partner with extrusion-line manufacturers to accelerate the time-to-market for next-generation multilayer agricultural lines. Capital allocation also favors chemical-recycling startups that convert contaminated film waste into naphtha-equivalent feedstocks, advancing closed-loop ambitions. Patent filings in spectral films and oxygen-barrier technologies intensify, and intellectual-property portfolios become acquisition targets for growth-oriented producers.

Agricultural Films Industry Leaders

BASF SE

Plastika Kritis SA

Armando Alvarez Group

RKW Group

Amcor plc (Berry Global Inc.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Sustainability compliance is creating room for dual-portfolio strategies, combining conventional high-performance PE films (downgauged, multi-layer, and additive-enhanced) with certified soil-biodegradable and recycled-content alternatives. The EU decision in 2024 to formally recognize soil-biodegradable mulch films within the Fertilising Products Regulation framework increases the value of certification-ready formulations and verification support, especially for growers and distributors selling into programs with technical minimums for protected cultivation and mulching. The market also has opportunity for service-led models that reduce contamination and improve recovery rates, since film recycling performance remains constrained by collection and cleanliness barriers in major farming regions.

Performance-led innovation also supports premium greenhouse and silage segments where growers pay for measurable outcomes like longer field life, tighter light management, and lower spoilage risk. Demand signals already reflected in the current landscape include rapid adoption of protected cultivation supported by subsidies that can cover up to 80% of greenhouse construction costs in select Asian programs, as well as a faster-growing reclaims mix within the product portfolio. Suppliers that pair stabilizer packages (UV, thermal, and chemical resistance) with downgauging and circularity claims are positioned to win specifications in capital-intensive greenhouses and large-scale silage operations, where downtime and product loss carry outsized economic impact.

Recent Industry Developments

- April 2026: BASF expanded its HALS and NOR HALS manufacturing capacities for plastics, supporting higher availability of UV-stabilization chemistries used to extend the service life of agricultural films in high-irradiation and chemically intensive farm environments. This expansion strengthens supply assurance for converters producing thin-gauge and premium greenhouse, mulch, and silage structures that depend on consistent stabilizer performance.

- August 2025: BASF launched Tinuvin NOR 211 AR for agricultural plastics, targeting durability under intense UV exposure, thermal stress, and contact with inorganic chemicals used in crop management and disinfection. This product introduction supports converters upgrading to longer-life films and helps differentiate premium film grades as disposal and replacement costs come under greater scrutiny.

- July 2024: BASF unveiled Tinuvin NOR 211 AR as a new stabilizer solution for plasticulture applications, positioning it for adoption in agricultural films exposed to harsh field conditions. The launch reinforced the competitive focus on additive-led performance improvements as growers and greenhouse operators demand longer service intervals and more predictable film behavior across seasons.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We define the agricultural films market as polymer film materials sold for on-farm and horticulture uses, including crop protection, soil management, and feed preservation, with revenues counted at the point of sale to end users or distributors.

Scope exclusions: We exclude durable non-film agricultural covers and non-agriculture plastic packaging that is not used for greenhouse, mulching, silage, or similar farm applications.

Segmentation Overview

- By Product Type

- Low-Density Polyethylene

- Linear Low-Density Polyethylene

- High-Density Polyethylene

- Ethyl Vinyl Acetate / Ethylene Butyl Acrylate

- Reclaims (Recycled PE)

- Other Types (Polypropylene Agricultural Films, Polyamide Agricultural Films, Ethylene Vinyl-Alcohol Copolymer Resins, and PVC)

- By Thickness

- Up to 80 µm

- 80-150 µm

- Above 150 µm

- By Application

- Greenhouse

- Mulching

- Silage

- Other Applications (Low Tunnels, Fumigation)

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market structure and establish practical guardrails for volumes, pricing, and regional adoption. We referenced public agriculture statistics and area indicators linked to film usage, such as protected cultivation area and crop area, along with plastics and polymer production indicators.

Typical sources included public releases and databases such as FAOSTAT, USDA, Eurostat, UN Comtrade, and country agriculture ministries, followed by company annual reports, investor presentations, association websites, and reputable press coverage. Where needed, paid subscriptions were used for company financials and intelligence, patent databases, and shipment-level import and export checks to validate trade-linked film flows. The sources listed here are illustrative only, and many other public and paid references were used to collect, validate, and clarify data points during the work.

Primary Interviews and Surveys

Primary work focused on validating application splits for greenhouse, mulching, and silage, then pressure-testing pricing logic for common resin types and film thickness ranges. We spoke with film manufacturers, converters, distributors, and large buyers across key regions, which helped us correct gaps from secondary data and align assumptions to observed purchasing patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 14% | APAC: 45% |

| Mid tier: 48% | Functional/Unit leaders: 36% | EMEA: 30% |

| Smaller Players: 14% | Managers: 50% | Americas: 25% |

Market-Sizing & Forecasting

Sizing started with a top-down build where regional demand pools were reconstructed from crop and protected cultivation area indicators, typical film replacement cycles, and usage intensity by application, then translated into value using region-specific price ranges. To keep the totals realistic, we corroborated the outputs with selective bottom-up checks using sampled supplier revenues, channel feedback on shipment direction, and simple ASP-to-volume approximations for major applications.

Key inputs that were tracked and updated include protected cultivation area growth, mulching penetration by crop type, silage adoption in dairy and forage regions, resin price movement for common polyethylene grades, and the share of reclaim content used in film formulations. Forecasts were built using scenario analysis supported by expert views on yield improvement focus, water-saving practices, and policy pushes on plastics use and recycling, then smoothed to avoid unrealistic step-changes. Where bottom-up gaps appeared due to private-company opacity, we filled them using capacity signals and trade movement patterns, and then rechecked the implied per-hectare consumption against interview benchmarks.

Data Validation & Update Cycle

Model outputs were checked against independent signals such as polymer demand direction, import and export patterns for film products, and regional agriculture activity trends, and then variances were investigated before sign-off. When an outlier was detected, we revisited the specific assumption behind it, and re-contacted industry participants if the change could materially shift application shares or prices.

Each report goes through multi-step analyst reviews, followed by a final consistency pass so definitions, units, and currency timing stay aligned across regions. Reports refresh annually, and interim updates are made when material events occur, such as major resin price shocks, policy changes on agricultural plastics, or sudden shifts in protected cultivation expansion.

Mordor Intelligence's Agricultural Films Market Estimate Compared With Other Published Estimates

Published estimates for agricultural films often do not match because the counted products, the year selected for the headline number, and the way pricing is normalized across regions can differ. Even when the application labels look similar, the underlying assumptions on thickness mix, reclaim share, and replacement rates can shift totals by a noticeable amount.

The main gap comes from whether recycled-content reclaims and adjacent farm cover materials are blended into the total value, where Mordor Intelligence counts reclaims within film types but avoids adding non-film agricultural covers, and this changes the final market total when other sources bundle the wider plastics spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.37 B (2026) | |

| Industry Publisher A | USD 11.85 B (2024) | Uses an earlier current-year headline and a shorter forecast window, and the value can stay lower if pricing is averaged without fully reflecting film thickness mix and resin-linked price movement by region. |

| Industry Publisher B | USD 12.80 B (2023) | Anchors on a different base year and may include broader end-use labels, which can shift totals depending on whether non-film covers or adjacent plastics are blended into agricultural films spend. |

The table shows that year choice and scope alignment are the biggest drivers of the spread, followed by how pricing is carried forward as resin costs change. By tying assumptions to area, replacement cycles, and application-level usage intensity, the estimate remains traceable to clear variables and repeatable checks.

Key Questions Answered in the Report

What is the current value of the agricultural films market?

The market is valued at USD 13.37 billion in 2026 and is forecast to reach USD 18.73 billion by 2031.

Which material holds the largest share in agricultural films?

Low-Density Polyethylene leads with 42.75% share due to its cost-to-performance balance and processing versatility.

Why are greenhouse films growing faster than other applications?

Greenhouse films benefit from expanding protected cultivation that delivers higher yields and year-round production, especially in land-constrained and climate-volatile regions.

Which region is the fastest-growing for agricultural films?

Africa is projected to post an 8.85% CAGR through 2031 driven by export-oriented horticulture and supportive trade incentives.

How are sustainability pressures influencing film materials?

Manufacturers are incorporating post-consumer recycled polyethylene and developing biodegradable formulations to meet regulatory and brand owner targets for circularity.

Page last updated on: