ENT Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 30.43 Billion |

| Market Size (2031) | USD 39.69 Billion |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

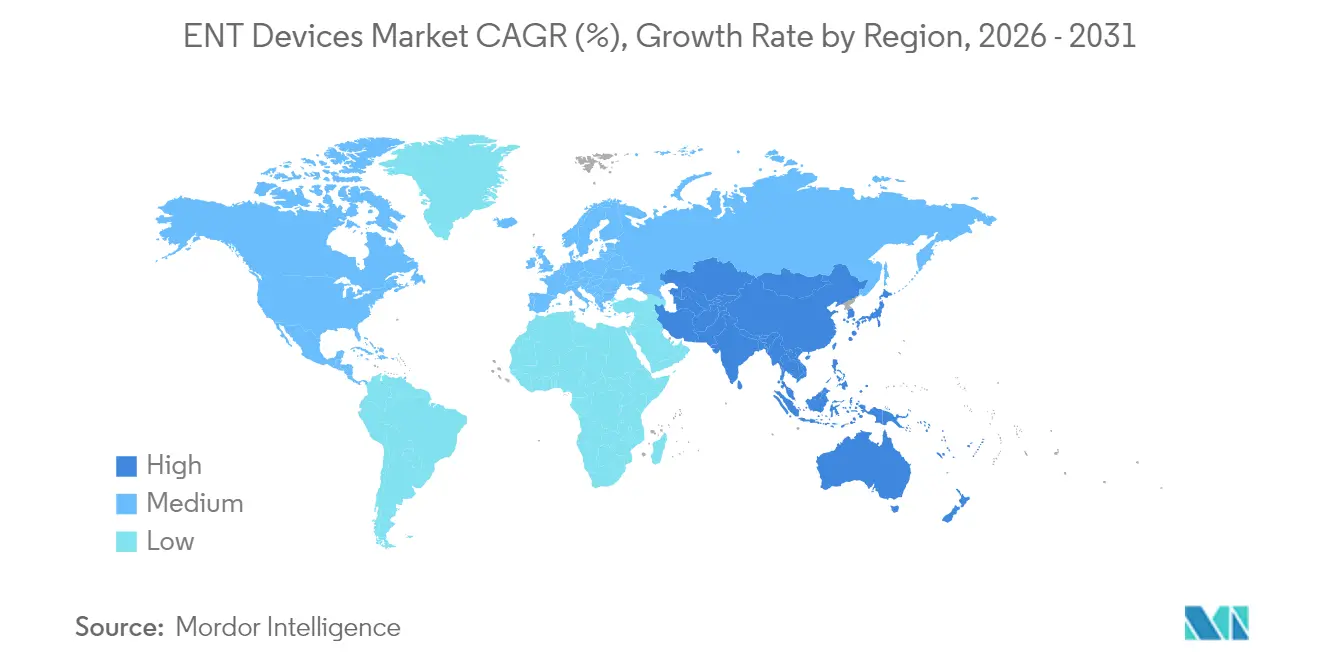

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

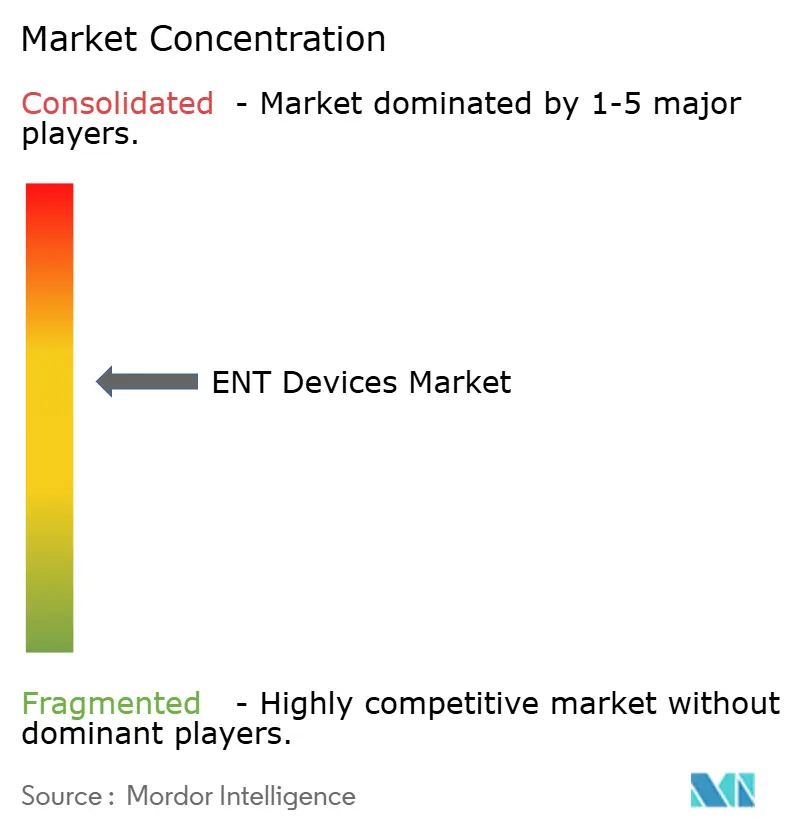

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ENT Devices Market Analysis by Mordor Intelligence

ENT devices market size in 2026 is estimated at $30.43 billion, growing from 2025 value of $28.85 billion with 2031 projections showing USD 39.69 billion, growing at 5.46% CAGR over 2026-2031. Robust demand stems from the expanding pool of age-related auditory and sinonasal disorders, steady procedure volumes across hospitals and ambulatory centers, and the rapid infusion of artificial intelligence into routine ENT tools. AI-enabled hearing aids that adjust to real-world listening environments, hyperspectral endoscopes that reveal tissue microstructures, and balloon sinus dilation kits that speed post-operative recovery collectively raise clinical expectations and spur replacement purchases. Parallel gains in home-based care, exemplified by smartphone-linked devices that permit remote programming, widen patient access and support recurring revenue models inside the ENT devices market. Volume growth is further anchored by Asia-Pacific’s infrastructure build-out, North America’s reimbursements that now cover over-the-counter aids, and surgically focused innovations that shorten operating-room time.

Key Report Takeaways

- By product category, hearing aids led with 31.60% revenue share in 2025; implantable devices are projected to expand at a 9.04% CAGR between 2026-2031.

- By age group, adults accounted for 39.50% of the ENT devices market share in 2025, while geriatrics are poised to advance at a 7.38% CAGR through 2031.

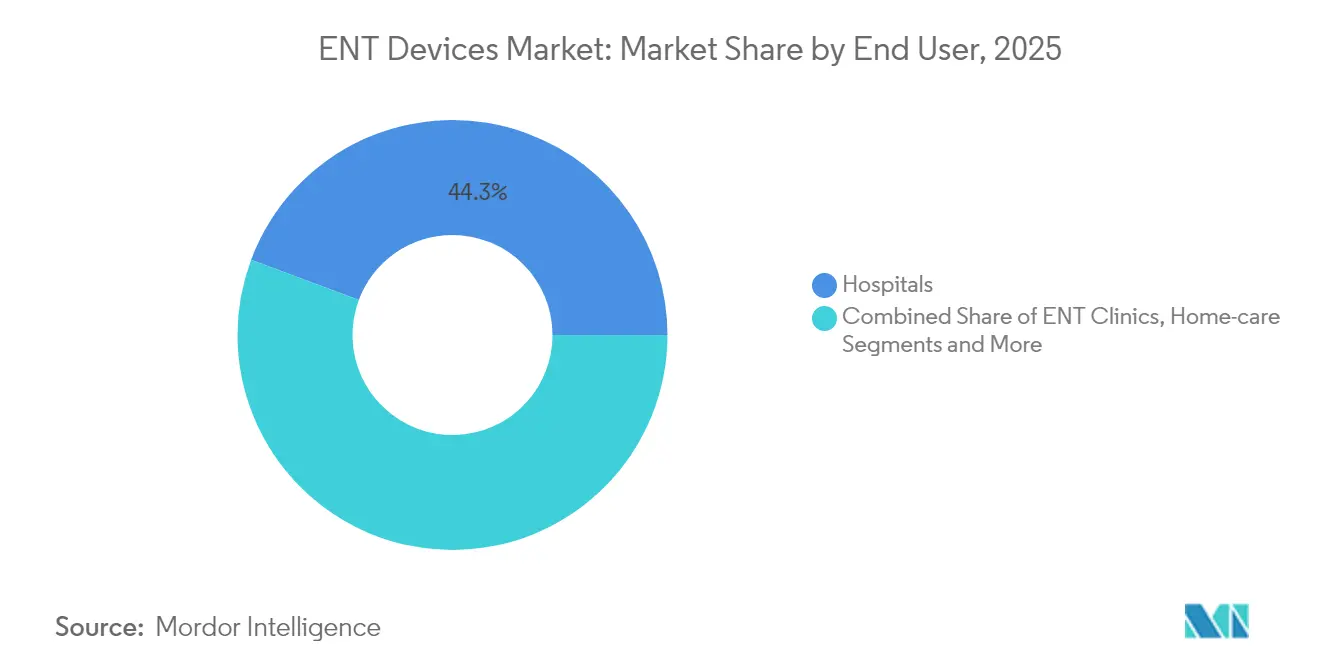

- By end user, hospitals retained 44.30% share of the ENT devices market size in 2025 and home-care solutions are advancing at a 7.65% CAGR to 2031.

- By geography, North America commanded 37.70% of the ENT devices market in 2025; Asia-Pacific is forecast to register a 6.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global ENT Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of ENT disorders | +1.8% | Global, higher in North America and Europe | Long term (≥4 years) |

| Technological advancements in ENT devices | +1.5% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Rising adoption of minimally invasive procedures | +1.0% | Global, higher in developed markets | Medium term (2-4 years) |

| Rising awareness campaigns and health programs | +0.8% | Global, variable by literacy levels | Short term (≤2 years) |

| Rising Adoption of Telemedicine | +0.5% | Global, with higher impact in remote/rural areas | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of ENT Disorders

Aging populations and deteriorating urban air quality have raised the incidence of chronic rhinosinusitis, otitis media, and sensorineural hearing loss. Hospital registries confirm earlier presentation in metropolitan clinics, while rural patients still arrive with advanced pathologies that often require more invasive interventions. Across the ENT devices market, this epidemiology sustains baseline demand for imaging scopes, balloon dilation kits, and programmable hearing aids. Public health agencies therefore prioritize early screening, which in turn elevates diagnostic instrument placements and stimulates follow-on sales of consumables.

Technological Advancements in ENT Devices

Digital signal processors, narrow-beam microphones, and 4D motion sensors now embed inside premium hearing aids, allowing real-time environmental classification and noise suppression that improve speech recognition. In operating theaters, rigid endoscopes capable of hyperspectral imaging distinguish perfused mucosa from malignancies, enhancing resection margins while limiting bleeding. These breakthroughs reinforce the ENT devices market as a technology-driven arena: manufacturers differentiate through software updates, cloud-based fitting portals, and module-ready components that clip into existing surgical stacks.

Rising Adoption of Minimally Invasive Procedures

Patients increasingly favor techniques that avoid external incisions, catalyzing the shift to balloon sinus dilation, endoscopic ear tube placement, and radiofrequency turbinate reduction. Payers support these methods because length of stay drops, postoperative narcotic use declines, and complication rates fall. Device suppliers respond by bundling disposable navigation probes with imaging software, enabling otolaryngologists to treat chronic sinusitis in office suites[1]Noah Medical, “Predictions in Healthcare: The Rise of Endoluminal Robotics,” noahmed.com. The ENT devices market therefore migrates revenue from capital equipment to single-use accessories and service contracts.

Rising Awareness Campaigns and Health Programs

National initiatives encouraging adults to check their hearing at pharmacies have reduced stigma and revealed unmet need among mild-to-moderate loss sufferers. When combined with 2024 regulations permitting over-the-counter hearing aids, retail channels now route consumers directly to self-fitting devices. Manufacturers amplify these programs via social media tutorials that demystify cochlear implantation, encouraging eligible seniors to pursue surgical candidacy sooner. Heightened consumer literacy thus accelerates adoption across the ENT devices market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of devices | -1.2% | Global, higher in emerging markets | Long term (≥4 years) |

| Device sterilization and maintenance challenges | -0.7% | Global, higher in resource-constrained settings | Medium term (2-4 years) |

| Social Stigma Around Hearing-Aid Use in Emerging Markets | -0.3% | Primarily Asia-Pacific, Middle East, and Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Cost of Devices

Fully implanted cochlear systems often list above USD 25,000, a figure beyond the reach of many uninsured adults. Even in countries with national health plans, wait lists persist when reimbursement caps lag inflation. Consequently, only a fraction of clinically eligible patients receive implants, dampening volume expansion inside the ENT devices market. Legislative proposals to reclassify active middle-ear devices as prosthetics aim to unlock Medicare funding and could gradually narrow affordability gaps.

Device Sterilization and Maintenance Challenges

Reusable scopes and suction instruments demand meticulous cleaning cycles that many outpatient centers struggle to maintain. Breakdowns add further downtime because calibrating miniaturized optics requires factory-level expertise. To mitigate risk, some hospitals adopt ultraviolet cabinets validated specifically for ENT endoscopes, while others shift to disposable sheaths despite added per-case expense. The resulting operational burden tempers purchasing decisions, nudging the ENT devices market toward hybrid ownership and outsourced service models.

Segment Analysis

By Product: Hearing Aids Sustain Leadership While Implantables Accelerate

The hearing-aid segment generated the largest slice of the ENT devices market size with 31.60% revenue in 2025. Cloud-linked firmware updates, lithium-ion rechargeable batteries, and AI-guided scene detection keep replacement cycles near four years, supporting steady unit demand. At the premium tier, integrated health sensors track cardiac rhythm and step counts, expanding device value beyond amplification. Sales also benefit from consumer electronics entrants who position self-fit models next to smartphones, an approach that widens channel exposure without cannibalizing clinic-fitted premium lines.

Implantable devices accounted for a smaller base yet posted the highest forward momentum with a 9.04% CAGR outlook. Innovations such as totally implanted cochlear systems remove external processors, boosting cosmetic appeal and swimming convenience. Surgeons appreciate magnet-guided electrode arrays that reduce cochlear trauma and shorten programming sessions. Favorable long-term outcomes foster payer acceptance, propelling multi-year growth inside the ENT devices market. Diagnostic instruments retain significant share; portable optical-coherence-tomography otoscopes now reveal middle-ear effusions at primary-care desks, broadening early intervention. Surgical device uptake follows the minimally invasive trend, especially balloon sinus kits that occupy ambulatory centers seeking rapid turnover.

Note: Segment shares of all individual segments available upon report purchase

By Age Group: Adult Dominance Continues While Geriatrics Drive Incremental Gains

Adults aged 18-64 captured 39.50% of ENT devices market share in 2025 because occupational noise exposure, allergic rhinitis, and chronic tonsillitis peak within working years. This cohort values discreet aesthetics and app-based adjustments, steering product development toward micro-receiver designs and remote fine-tuning. Clinics leverage tele-audiology to deliver follow-ups that fit busy schedules, lowering attrition rates and sustaining recurring revenue.

The geriatric population propels future expansion with a projected 7.38% CAGR as life expectancy lengthens and comorbidities accumulate. Balance disorders, presbycusis, and dysphagia necessitate complex diagnostics, encouraging hospitals to install vestibular chairs and fiberoptic endoscopic swallowing test systems. Manufacturers tailor interfaces with larger buttons, voice prompts, and auto-gain algorithms that compensate for reduced dexterity and cognitive load. Pediatric demand remains clinically vital though proportionally smaller; universal newborn screening pushes early amplification, protecting language development and justifying public subsidies.

By End User: Hospitals Hold Scale Advantage While Home Care Outpaces

Hospitals controlled 44.30% of the ENT devices market size in 2025, buoyed by tertiary-care capabilities for implant sessions, revision surgeries, and neurotology cases. Capital purchasing committees favor integrated operating-room platforms that link navigation, endoscopy, and suction through a single console, reducing training complexity. Inpatient volumes remain stable for skull-base and airway reconstruction procedures, anchoring recurring instrument demand.

Home-care settings register the fastest trajectory at 7.65% CAGR as Bluetooth-enabled aids, self-directed cerumen management kits, and cloud-monitored sleep apnea interfaces allow therapy outside institutional walls. Insurers reimburse virtual checkups when outcome data prove equivalent, shifting revenue downstream toward direct-to-consumer fulfillment. ENT clinics preserve mid-market relevance by offering specialized diagnostics unavailable in primary care, while ambulatory surgical centers attract balloon sinus and tonsillectomy cases with bundled cash pricing that appeals to high-deductible plans. Collectively, these dynamics diversify revenue sources throughout the ENT devices market and mitigate macroeconomic shocks.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America led the ENT devices market with 37.70% revenue share in 2025. Extensive insurance coverage, veteran tele-audiology networks, and a vibrant research ecosystem accelerate adoption cycles. FDA authorization of consumer earbuds equipped with hearing-aid software underscores regulatory agility and primes retailers for expanded audiology aisles. Hospital groups invest in spectral-imaging endoscopes and revision-ready implant suites to retain referral flows, reinforcing regional spending momentum.

Europe remains a substantive contributor. Public payer systems reimburse most implant costs, though stringent evidence requirements slow initial roll-outs of novel technologies. Regional manufacturers emphasize miniaturization and eco-friendly packaging to align with environmental directives. Cross-border clinical consortia pool data, refining surgical guidelines and informing device redesigns that travel globally through the ENT devices market.

Asia-Pacific represents the fastest-growing arena with a 6.95% CAGR outlook. Government-backed insurance in China now covers bone-anchored hearing solutions, while India’s Ayushman Bharat program subsidizes sinus surgeries at district hospitals. Domestic suppliers scale mid-tier offerings that balance durability with affordability, narrowing urban–rural access gaps. Start-ups in Korea and Singapore leverage robotics to navigate narrow nasal cavities, exporting intellectual property through licensing deals. Middle East and Africa move gradually yet benefit from teaching-hospital frameworks in Gulf states that import advanced suites and train regional surgeons. South America shows mixed progress as Brazil modernizes otology centers while neighboring countries grapple with funding constraints.

Competitive Landscape

The ENT devices market exhibits moderate concentration; the top five manufacturers command significant combined revenue. Cochlear’s 2024 purchase of a rival’s cochlear implant line consolidates surgical share and integrates a complementary patent portfolio, tightening supplier influence over magnet designs and sound-processor chipsets. Meanwhile, mid-size players specialize in balloon dilation or ultraviolet disinfection, carving niches beyond full-line portfolios[3]Cochlear Limited, “Cochlear Completes Acquisition of Oticon Medical Cochlear Implant Business,” cochlear.com.

Competitive differentiation hinges on software ecosystems that update remotely and log usage analytics. Firms allocate double-digit revenue shares to research, pursuing full-body health metrics inside earpieces and robot-assisted navigation for complex skull-base access. Consumer-electronics entrants introduce price tension at the lower amplification tiers, yet premium medical models maintain margin leadership through clinician-mediated fitting and multi-channel reimbursement.

Supply-chain resilience emerges as a strategic priority after microphone shortages in 2024. Component companies diversify fab locations and pre-approve alternative ASIC footprints, reducing single-source risk. Sustainability pledges become procurement criteria; vendors highlight recyclable housings and rechargeable batteries that eliminate zinc-air waste. In this environment, scale delivers procurement leverage, while specialization secures protected revenue corridors, collectively shaping the trajectory of the ENT devices market.

ENT Devices Industry Leaders

Cochlear Ltd

Medtronic PLC

Olympus Corporation

Stryker Corporation

WS Audiology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Knowles Corporation completed the divestiture of its consumer MEMS microphone business, a move expected to reshape hearing-aid component sourcing.

- November 2024: Envoy Medical received FDA clearance to launch a pivotal study evaluating the fully implanted Acclaim cochlear device, eliminating all external hardware.

Global ENT Devices Market Report Scope

As per the scope of the report, ENT devices refer to special equipment used for detection, therapy, or surgery of any disorders related to the ear, nose, or throat. They also refer to synthetic materials and prosthetic devices used to restore any dysfunction of an ear, nose, or throat, and aid in correcting any problems with hearing, smelling or speaking. The ENT Devices Market is segmented by Product (Diagnostic Devices, Surgical Devices, Hearing Aids, Image-guided Surgery Systems, and Other Products), End User (Hospitals, ENT Clinics, and Other End User) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Diagnostic Devices | Endoscopes (Rigid, Flexible) |

| Hearing Screening Devices (OAE, Tympanometry) | |

| Surgical Devices | Powered Surgical Instruments |

| Balloon Sinus Dilation Systems | |

| CO? & Diode Lasers | |

| ENT Supplies & Consumables (Stents, Ear Tubes) | |

| Hearing Aids | Behind-the-Ear (BTE) |

| In-the-Ear / In-the-Canal (ITE/ITC) | |

| Receiver-in-Canal (RIC) | |

| Over-the-Counter (OTC) Hearing Aids | |

| Implantable Devices | Cochlear Implants |

| Bone-Anchored Hearing Aids (BAHA) | |

| Image-Guided Surgery Navigation Systems | |

| Other Products |

| Pediatric (0-17 Years) |

| Adult (18-64 Years) |

| Geriatric (65+ Years) |

| Hospitals |

| ENT Clinics |

| Ambulatory Surgical Centers (ASCs) |

| Home-care |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Diagnostic Devices | Endoscopes (Rigid, Flexible) |

| Hearing Screening Devices (OAE, Tympanometry) | ||

| Surgical Devices | Powered Surgical Instruments | |

| Balloon Sinus Dilation Systems | ||

| CO? & Diode Lasers | ||

| ENT Supplies & Consumables (Stents, Ear Tubes) | ||

| Hearing Aids | Behind-the-Ear (BTE) | |

| In-the-Ear / In-the-Canal (ITE/ITC) | ||

| Receiver-in-Canal (RIC) | ||

| Over-the-Counter (OTC) Hearing Aids | ||

| Implantable Devices | Cochlear Implants | |

| Bone-Anchored Hearing Aids (BAHA) | ||

| Image-Guided Surgery Navigation Systems | ||

| Other Products | ||

| By Age Group | Pediatric (0-17 Years) | |

| Adult (18-64 Years) | ||

| Geriatric (65+ Years) | ||

| By End User | Hospitals | |

| ENT Clinics | ||

| Ambulatory Surgical Centers (ASCs) | ||

| Home-care | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current valuation of the ENT devices market?

The ENT devices market size reached USD 30.43 billion in 2026 and is projected to grow steadily through 2031.

Which product category generates the most revenue in ENT devices?

Hearing aids account for the largest share, delivering 31.60% of global revenue in 2025 due to continuous feature upgrades and short replacement cycles.

Which region is expanding the fastest for ENT solutions?

Asia-Pacific is the fastest-growing region, supported by healthcare infrastructure investment and a 6.95% forecast CAGR between 2026-2031.

Why are implantable devices gaining momentum?

Fully implanted cochlear systems improve aesthetics and convenience, driving a 9.04% segment CAGR over the next five years.

How is home-based care influencing market dynamics?

Smartphone-linked hearing aids, remote programming, and tele-audiology services are pushing a 7.65% CAGR in the home-care end-user segment.

What factors restrain broader adoption of advanced ENT technology?

High upfront device costs and the stringent sterilization requirements for reusable equipment remain primary barriers, especially in emerging markets.

Page last updated on: