Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

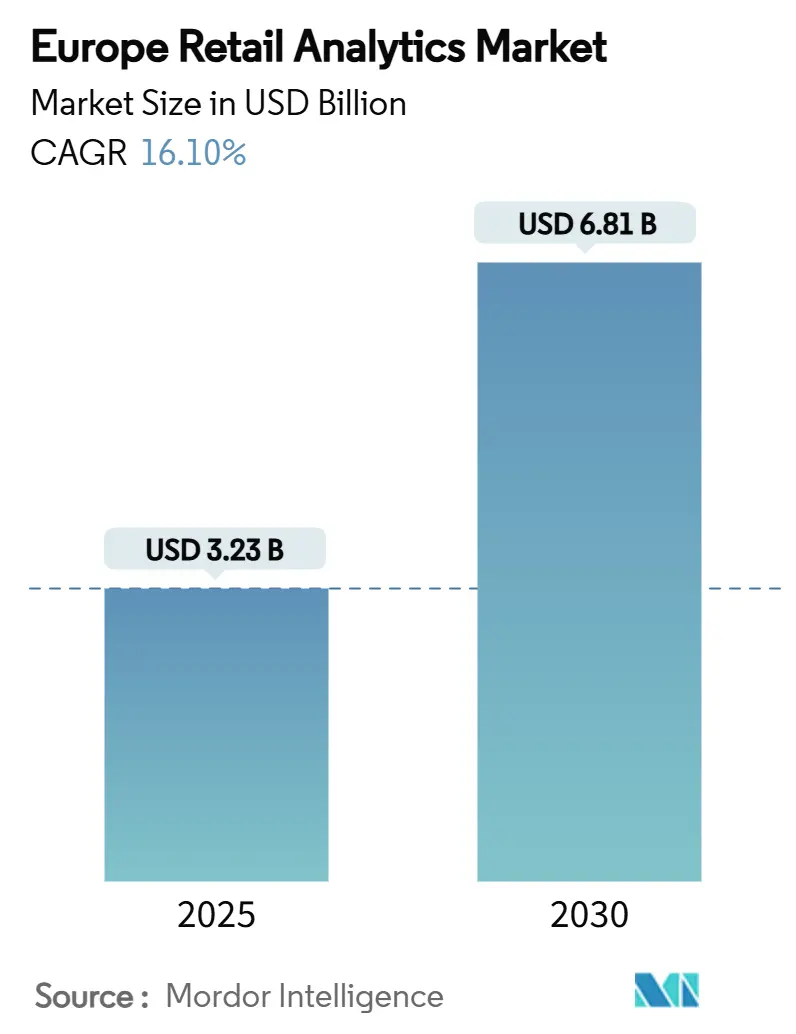

| Market Size (2025) | USD 3.23 Billion |

| Market Size (2030) | USD 6.81 Billion |

| Growth Rate (2025 - 2030) | 16.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Retail Analytics Market Analysis by Mordor Intelligence

The Europe retail analytics market size stood at USD 3.23 billion in 2025 and is projected to reach USD 6.81 billion by 2030, registering a 16.1% CAGR during the forecast period. Ongoing digital-market reforms, elevated energy prices, and the EU Digital Markets Act are steering retailers toward advanced data platforms that improve operating margins and regulatory compliance. Cloud platforms underpin this transition because they scale on demand, integrate disparate data types, and cut capital expenditure. Edge analytics is spreading through hypermarkets as retailers push real-time shelf monitoring, while AI-enabled dynamic pricing helps defend gross margins in an inflationary environment. Country dynamics remain heterogeneous: Germany drives spending today, but Italy, Spain, and several Central and Eastern European countries are expanding faster. A widening gap in data-science talent and stricter privacy enforcement could restrain the pace of deployments for some operators.

Key Report Takeaways

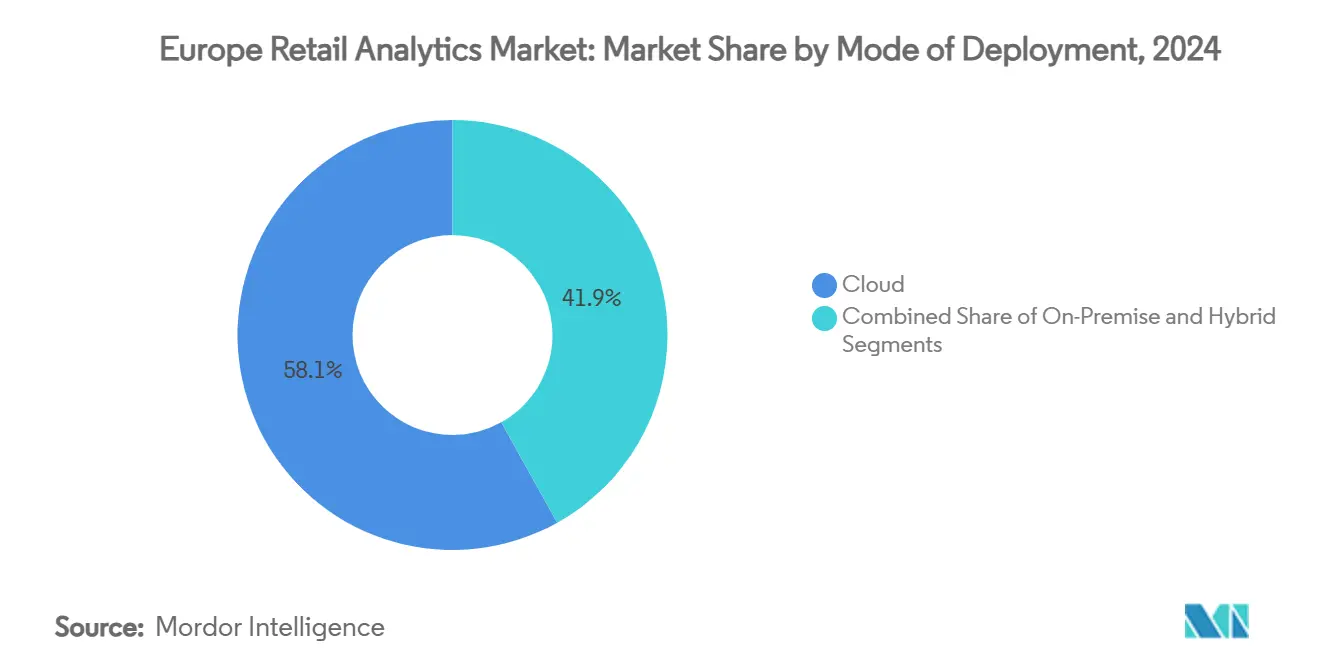

- By mode of deployment, cloud accounted for 58.1% of Europe's retail analytics market share in 2024; hybrid models are forecast to show the highest 18.2% CAGR through 2030.

- By module type, Marketing and Customer Insights held 29.6% revenue share of the Europe's retail analytics market size in 2024, while Supply-Chain and Fulfilment is projected to accelerate at a 17.3% CAGR to 2030.

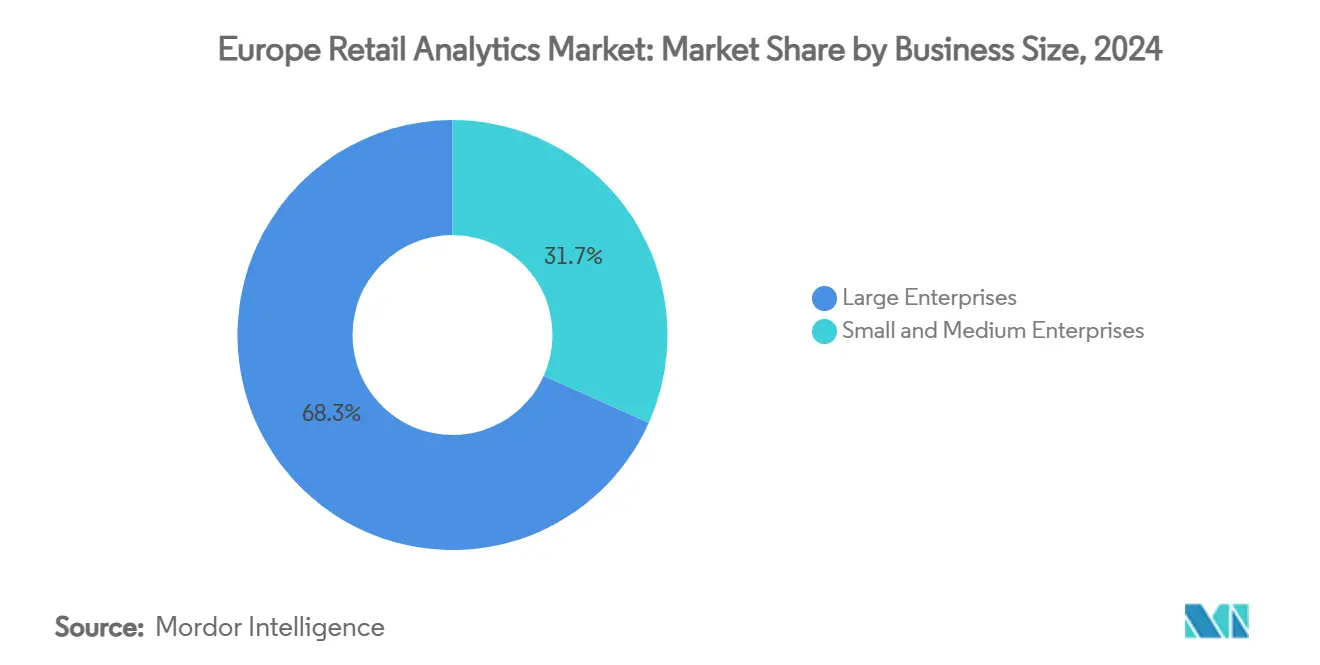

- By business size, large enterprises commanded 68.3% of Europe's retail analytics market size in 2024; small and medium enterprises will grow at an 18.3% CAGR over 2025-2030.

- By retail format, brick-and-mortar retained 48.7% of Europe's retail analytics market share in 2024, yet omnichannel channels are forecast to expand the fastest at 17.5% CAGR to 2030.

- By country, Germany led with 34.3% of Europe's retail analytics market revenue share in 2024; Italy is set to post the strongest 17.4% CAGR through 2030.

Europe Retail Analytics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-driven personalization lifts in-store conversion | +3.2% | Germany, France, United Kingdom | Medium term (2–4 years) |

| AI-powered pricing engines optimise margins | +2.8% | EU-wide; strongest in Germany and Italy | Short term (≤ 2 years) |

| Proliferation of edge analytics for real-time shelf monitoring | +2.1% | Western Europe chains | Medium term (2–4 years) |

| Unified commerce mandates single view of customer | +2.5% | Germany, United Kingdom, France | Long term (≥ 4 years) |

| EU Digital Markets Act pushes first-party data control | +1.9% | EU-27 | Long term (≥ 4 years) |

| Energy-efficiency analytics to curb soaring utility bills | +1.8% | Northern and Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-driven personalization lifts in-store conversion

Retailers deploying cloud-based recommendation engines now feed in-store behavior into the same decision hubs that analyze web journeys, enabling real-time offers at the shelf or check-out. Early adopters report conversion uplifts between 15% and 25%, which in turn drives budget reallocation from blanket promotions to targeted incentives. Successful programs rely on privacy-by-design architectures that tag consent, aggregate profiles, and maintain local data residence. Demand concentrates in Germany, France, and the United Kingdom, where high shopper density and loyalty-card maturity provide rich data streams. Vendors that simplify identity resolution across legacy point-of-sale feeds and e-commerce logs capture most of the growth. The resulting personalization loop supports the broader shift toward experience-led differentiation rather than price competition.

AI-powered pricing engines optimise margins in inflationary Europe

Food and general merchandise margins came under pressure when euro-area food inflation peaked at 15% in early 2024. [1]European Central Bank, “What were the drivers of euro area food price inflation over the last two years?,” ecb.europa.eu Retail finance departments that embraced algorithms capable of re-pricing SKUs hourly saw 3-5% margin relief even as input costs remained volatile. The European Central Bank confirms that firms alter prices more frequently during high-inflation periods, reinforcing the commercial logic for analytics platforms that automate elasticity modelling. Dynamic engines ingest competitor crawls, energy surcharges, and real-time demand to suggest optimal shelf prices and markdown cadences. Retailers in Germany and Italy moved fastest because of intense discounter competition, setting a regional template others now follow. Cloud deployment dominates because inference workloads spike during promotion events and must scale without hardware bottlenecks.

Proliferation of edge analytics for real-time shelf monitoring

Hypermarkets and DIY chains are embedding computer-vision cameras and electronic shelf labels connected via 5G micro-cells. Carrefour's 2025 rollout of VusionGroup EdgeSense across a 70,000-SKU hypermarket reduced out-of-stocks by about 55%, while price-tag dyssynchrony fell almost to zero. The case crystallized a clear ROI model: labor savings, higher on-shelf availability, and automated planogram compliance. Western European retailers now pilot similar architectures as bandwidth costs decline. Edge processing trims latency and mitigates data-sovereignty concerns because imagery is processed locally. Vendors with containerized analytics stacks that can run on ARM or x86 gateways, therefore, hold a defensible competitive position.

Unified commerce mandates single view of customer

Order-management system (OMS) vendors that stitch online and store stock pools attract strong venture funding; OneStock’s USD 81 million raise in 2024 illustrates this momentum. Retailers using unified OMS report sales uplifts near 30% because lost-sale scenarios decline once staff can promise inventory across the entire network. The European retail analytics market benefits because OMS generates a consolidated data layer that feeds forecasting, markdown, and loyalty models. German, French, and UK omnichannel leaders focus on real-time event streaming so that web, app, and cashier systems write into the same ledger within milliseconds. Over the long term, this architectural shift will blur channel silos and force analytics vendors to deliver holistic customer lifetime-value dashboards.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of retail data-science talent pool | −2.1% | Germany, France, United Kingdom, Ireland, Poland | Medium term (2–4 years) |

| Data-privacy tightening under GDPR and ePrivacy | −1.8% | EU-27 | Long term (≥ 4 years) |

| Legacy POS fragmentation impedes integration | −1.5% | Regional traditional chains | Medium term (2–4 years) |

| Capital-expenditure freeze among SME retailers | −1.2% | Southern and Eastern Europe SMEs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of retail data-science talent pool

Three-quarters of German retailers reported hiring delays for data roles in 2024, and similar patterns surfaced in France and the United Kingdom. [2]Next Level Jobs EU, “Top 5 EU Countries Facing AI Skill Shortages,” nextleveljobs.eu Competition from fintech and deep-tech verticals raises salary benchmarks beyond what many retailers can absorb. Vendors respond by embedding automated model-building and natural-language query layers so that category managers can run forecasts without writing code. Managed-service engagements gain traction as well, with providers offering fractional data scientists on subscription. Over the medium term, EU-funded reskilling initiatives could ease constraints, but until then, platform usability remains a key purchase criterion inside the European retail analytics market.

Data-privacy tightening under GDPR and forthcoming ePrivacy Regulation

Several data-protection authorities banned the default use of legacy web analytics tools in 2024 because of trans-Atlantic data-transfer concerns. Retailers must now localize datasets or apply advanced pseudonymization, making infrastructure choices more complex and expensive. Compliance costs hit SMEs disproportionately, trimming their analytics budgets in the short term. Vendors with in-memory anonymization engines, consent APIs, and audit trails gain share because they simplify regulatory audits. Over the long term, privacy-by-design architectures could become a competitive advantage, but for now, they lengthen deployment cycles and suppress the European retail analytics market revenue growth potential by roughly 1.8 percentage points.

Segment Analysis

By Mode of Deployment: Cloud-first strategies accelerate modernization

Cloud options drew 58.1% of spending in 2024, confirming that most retailers prefer outsourcing compute and storage layers for analytics workloads. The Europe retail analytics market size attributed to cloud is forecast to climb at an 18.2% CAGR until 2030 as enterprises migrate batch reporting, AI training and real-time event streaming pipelines off-premise. Much of the momentum comes from periodic promotional surges—Black Friday, Singles’ Day, or private-label loyalty drives—that stress legacy data centers. SAP’s EMEA cloud revenue jumped 30% year-over-year in Q1 2025, mirroring this migration trend. [3]Investing.com, “SAP Q1 2025 presentation: cloud growth accelerates, operating profit soars 60%,” investing.com On-premise clusters still run in fashion and luxury houses with stringent intellectual-property controls, yet their share will shrink as confidential-computing chips harden public-cloud security postures. Hybrid architectures bridge the gap where in-store cameras process images locally but upload aggregated metrics to central lakes, supporting GDPR locality and low-latency decisions.

Scalability explains the near-term advantage, but cost discipline sustains it. Retailers exposed to energy spikes discovered that moving compute off-site neutralizes power volatility, because hyperscalers hedge electricity contracts longer term. That financial predictability resonates with finance chiefs tasked to safeguard EBITDA while reinvesting in growth. Vendor competition now shifts to value-added services—verticalized data models, pre-trained pricing algorithms, and one-click dashboards for merchandisers. These differentiators will shape revenue capture inside the cloud portion of the Europe retail analytics market over the next five years.

Note: Segment shares of all individual segments available upon report purchase

By Module Type: Customer insights dominate, supply-chain use cases gain speed

Marketing and Customer Insights secured 29.6% revenue in 2024 because retailers target loyalty retention and individualized promotions amid relentless competition. The module’s predictive-segmentation engines and path-to-purchase attribution models remain foundational for omnichannel strategies. Yet, Supply-Chain and Fulfilment is expected to clock a 17.3% CAGR to 2030, the fastest among all modules, as retailers reengineer networks for resilience. Henkel’s EUR 4 million saving through data-driven energy optimization in 2024 showcase tangible ROI.

Strategy and Planning dashboards knit KPIs from merchandising, finance, and operations into board-level scorecards, creating a change-management backbone. Merchandising and Category Optimization modules use AI to simulate basket affinities and recommend assortment refreshes every season. Store-operations analytics—especially computer vision for shrinkage—is picking up speed as unionized retailers look to automate repetitive audits. Financial Management modules, including real-time gross-margin tracking, remain essential, particularly in food retail, where dozens of commodity inputs move daily. Together, these sub-segments illustrate how the Europe retail analytics industry delivers value across both revenue growth and cost-containment objectives.

By Business Size: Democratization widens access to advanced analytics

Large enterprises still generated 68.3% of Europe retail analytics market size in 2024, reflecting their broad store footprints and cross-border e-commerce operations that require scalable intelligence platforms. They run thousands of dashboards, ingest billions of rows daily, and often deploy custom machine-learning pipelines on top of packaged software. However, SMEs will outpace them with an 18.3% CAGR through 2030 as the barrier to entry falls. Managed-service models bundle software, data-engineering labor, and training into one fee that aligns with SME cash flow.

Surveys published in 2024 showed that European SMEs combining AI, IoT, and big data analytics enjoyed revenue lifts above 30%. The finding emboldens lenders and public agencies to extend digital-readiness grants, further catalyzing adoption. Vendors tailor lite versions of their suites with drag-and-drop canvas, guided onboarding, and industry templates. Once connected, SMEs can level the playing field against discount giants by running daily sell-through forecasts, markdown simulations, and basket analysis to refine promotions.

By Retail Format: Omnichannel models reshape physical-digital boundaries

Physical stores accounted for 48.7% of Europe retail analytics market share in 2024. Technologies such as queue-length prediction, heat-mapping, and computer-vision shelf auditing have become standard for large grocers and DIY chains. Yet, the omnichannel sub-segment is forecast to expand 17.5% annually as retailers knit click-and-collect, home delivery, and ship-from-store into one promise. Successful omnichannel operators pivot their data architecture to event streaming that captures every interaction—web, app, kiosk, or call center—in a single ledger, thereby fueling consistent recommendations and accurate available-to-promise (ATP) logic.

Pure-play e-commerce continues to grow but at a slower pace, reflecting high saturation and mounting profitability concerns. Analysts expect omnichannel convergence to siphon incremental budget from siloed online analytics toward unified platforms. For vendors, the imperative is to deliver inventory, customer, and payment micro-services that plug seamlessly into headless front-end stacks while maintaining sub-second response times in store.

Geography Analysis

Germany’s early adoption of unified commerce and dynamic pricing explains its dominant 34.3% revenue share in 2024. Retailers such as REWE, Lidl, and Douglas deepened edge analytics pilots in 2025, linking store cameras directly to central data lakes through 5G private networks. Talent scarcity remains the biggest brake, pushing chains toward vendor-managed model-ops services.

Italy shows the steepest trajectory with 17.4% CAGR expected through 2030 as fashion, grocery, and specialty stores embrace cloud POS and real-time personalization. Government-backed digital-voucher schemes cover up to 50% of SaaS subscription fees, lowering entry hurdles for independent supermarkets and pharmacies. Domestic tech vendors integrate tax receipting, fiscal-printer interfaces, and e-invoicing, aligning solutions with local compliance norms and thereby accelerating sales cycles.

The United Kingdom and France continue to pioneer automation. UK grocers added AI packing robots and large-scale camera grids in 2025, improving pick accuracy and safety. [4]The Guardian, “Robot packers and AI cameras: UK retail embraces automation to cut staff costs,” theguardian.com French hypermarkets expanded electronic-shelf-label deployments and invested in real-time price automation after labor-cost spikes. Spain, Poland, and the Nordics invest heavily in fulfillment analytics to handle cross-border e-commerce surges. Collectively, these dynamics reinforce the need for localized language models, tax logic, and GDPR-compliant data hosting.

Competitive Landscape

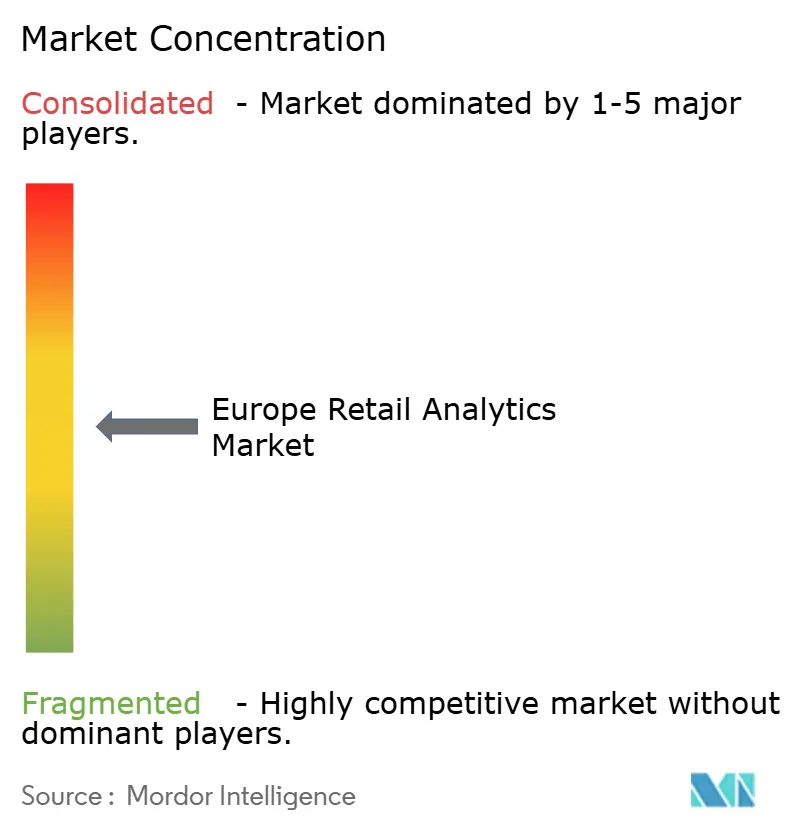

The Europe retail analytics market displays moderate concentration. SAP, Oracle, IBM and Microsoft combine platform breadth, cloud infrastructure and enterprise relationships to secure long-term contracts, often bundling analytics into ERP or CRM renewals. Oracle revealed a multi-cloud database agreement that could add USD 30 billion annual revenue from 2028, underscoring market appetite for integrated stacks.

Specialist vendors carve out niches by moving faster in edge analytics, computer vision, and energy optimization. VusionGroup locked a EUR 1 billion amendment with Walmart U.S. in 2025 to accelerate EdgeSense deployment, demonstrating that product leadership can open global scale even beyond Europe. RetailNext advances in traffic-counting and shopper-path analytics, while QlikTech’s hybrid-cloud dashboards win customers seeking quick time-to-insight without heavy data-engineering overhead.

Start-ups such as Belive.ai and Shopic concentrate on camera-based shelf monitoring and smart carts, respectively. Their AI models run on lightweight edge devices, minimizing cloud egress fees and latency—two critical buying factors for grocers with slim margins. As privacy demands intensify, vendors tout confidential-computing chips, homomorphic encryption add-ons, and local inference to outflank larger rivals, slower to productize privacy features. Given that the top five players control an estimated 35-40% of revenue, the market earns a concentration score of 5, indicating balanced competitive intensity with ample room for specialist expansion.

Europe Retail Analytics Industry Leaders

SAP SE

Oracle Corporation

IBM Corporation

SAS Institute Inc.

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Oracle disclosed a multi-cloud deal expected to deliver more than USD 30 billion in annual revenue from fiscal 2028, boosting demand for cloud-based retail analytics infrastructure.

- June 2025: Carrefour completed the first full-store EdgeSense rollout in Europe, spanning 70,000 electronic shelf labels and 500 cameras at its Villabé hypermarket.

- May 2025: Oracle unveiled new cloud services tailored to retail lenders, extending its analytics suite into risk and collections management.

- May 2025: SAP reported Q1 2025 cloud revenue of EUR 4.993 billion, up 27%, with EMEA contributing 30% growth.

- April 2025: VusionGroup secured a EUR 1 billion amendment with Walmart for accelerated EdgeSense and VusionCloud deployment.

- February 2025: Peek and Cloppenburg Düsseldorf selected Oracle Cloud to modernize store analytics and customer engagement.

- December 2024: VusionGroup partnered with The Fresh Market to equip 166 U.S. stores with Vusion 360 solutions by end-2025.

Europe Retail Analytics Market Report Scope

Retail analytics provides analytics tools to the retail industry on business trends, patterns, and performance. Retail business analytics enable retailers to leverage data-driven insights from their businesses and customers to improve consumer experience, increase sales, and optimize business operations. The retail analysis provides important analytical data for marketing and procurement decisions, such as inventory levels, consumer demand, supply chain movements, and sales.

The Europe Retail Analytics Market is segmented By Mode of Deployment (On-Premise, On-Demand), Type (Solutions, Services), Module Type (Strategy & Planning, Marketing, Financial Management, Store Operations, Merchandising, Supply Chain Management), Business Type (Small & Medium Enterprises, Large-scale organizations), and Country (united kingdom, Germany, France, Others).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Mode of Deployment

| On-Premise |

| Cloud |

| Hybrid |

By Module Type

| Strategy and Planning |

| Marketing and Customer Insights |

| Financial Management |

| Store Operations and Loss Prevention |

| Merchandising and Category Optimisation |

| Supply-Chain and Fulfilment |

By Business Size

| Small and Medium Enterprises |

| Large Enterprises |

By Retail Format

| Brick-and-Mortar |

| E-Commerce |

| Omnichannel Retail |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Mode of Deployment | On-Premise |

| Cloud | |

| Hybrid | |

| By Module Type | Strategy and Planning |

| Marketing and Customer Insights | |

| Financial Management | |

| Store Operations and Loss Prevention | |

| Merchandising and Category Optimisation | |

| Supply-Chain and Fulfilment | |

| By Business Size | Small and Medium Enterprises |

| Large Enterprises | |

| By Retail Format | Brick-and-Mortar |

| E-Commerce | |

| Omnichannel Retail | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe retail analytics market today?

The Europe retail analytics market size was USD 3.23 billion in 2025 and is projected to reach USD 6.81 billion by 2030.

Which deployment model is growing the fastest?

Cloud deployments will post an 18.2% CAGR through 2030 as retailers favor scalable, pay-as-you-go infrastructure.

What is the leading module in terms of revenue?

Marketing & Customer Insights held 29.6% of 2024 spend because personalization and loyalty analytics drive quick ROI.

Which country offers the highest growth opportunity?

Italy is forecast to grow at a 17.4% CAGR thanks to government digital-voucher schemes and expanding cloud adoption.

What restrains analytics uptake among European retailers?

Talent shortages, legacy POS fragmentation and stricter GDPR enforcement are the main barriers, jointly shaving several percentage points off potential growth.

Who are the key technology suppliers?

SAP, Oracle, IBM and Microsoft dominate platform deals, while VusionGroup and QlikTech excel in edge and visualization niches.

Page last updated on: