Crowdfunding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

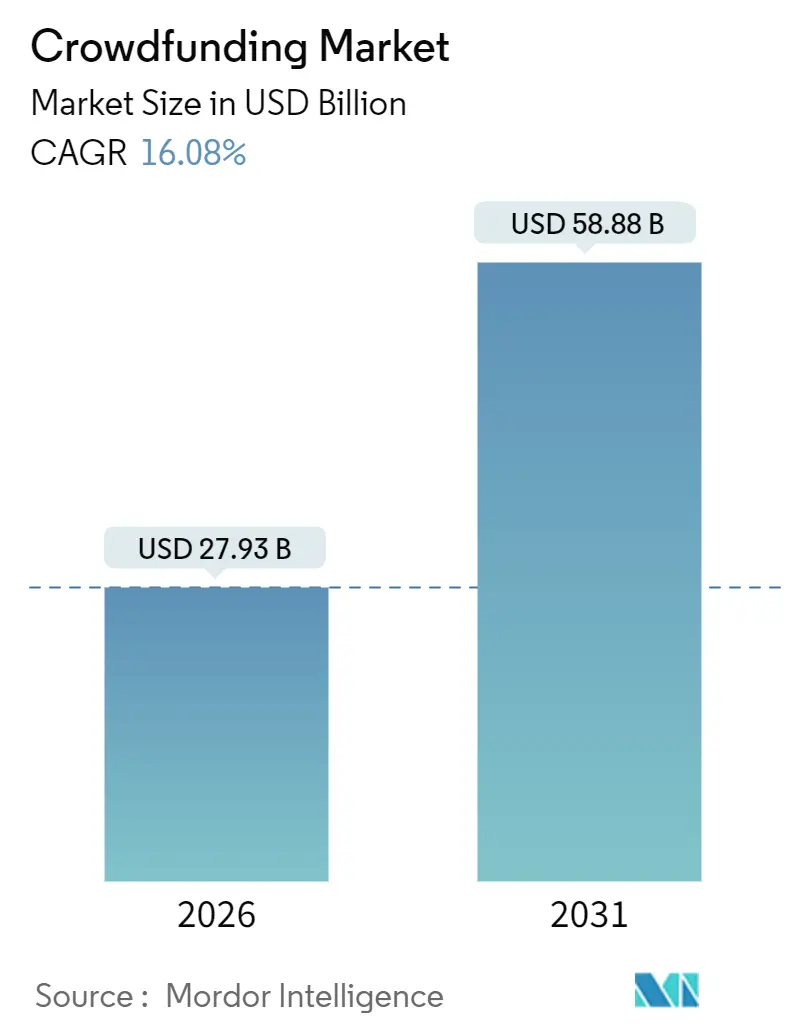

| Market Size (2026) | USD 27.93 Billion |

| Market Size (2031) | USD 58.88 Billion |

| Growth Rate (2026 - 2031) | 16.08% CAGR |

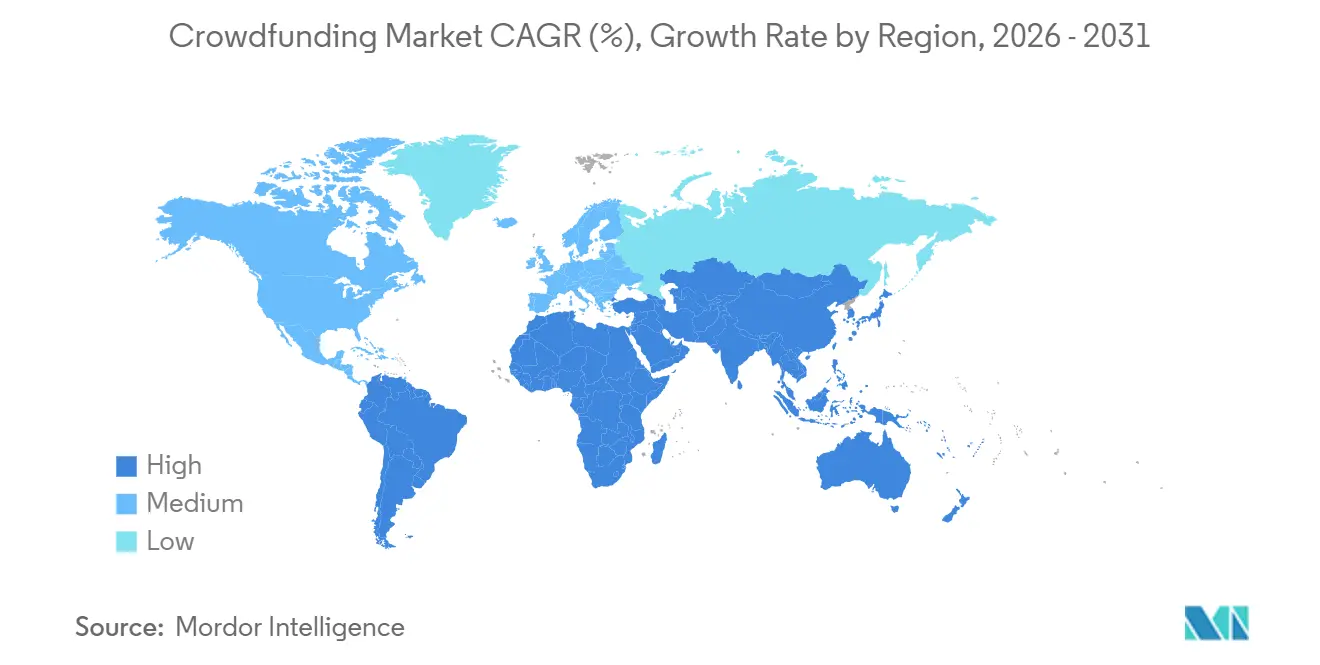

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Crowdfunding Market Analysis by Mordor Intelligence

The crowdfunding market size is USD 27.93 billion in 2026 and is forecast to reach USD 58.88 billion by 2031, expanding at a 16.08% CAGR through the outlook period. This robust trajectory reflects regulatory harmonization in Europe, blockchain-enabled fractional ownership in Asia Pacific, and artificial-intelligence-driven campaign optimization that jointly lift success rates and widen investor participation. Asia Pacific retains leadership on the crowdfunding market with its mobile-first culture, dense micro-investment networks, and tokenization-friendly rules, while Africa posts the fastest regional growth as payment-gateway access improves. Hybrid structures that embed smart-contract capabilities are steadily eroding the dominance of traditional reward campaigns, and institutional investors are entering the crowdfunding market at scale as secondary-market pathways increase liquidity. Cloud-native platforms now underpin most transaction volumes, enabling real-time risk monitoring and cross-border KYC orchestration.

Key Report Takeaways

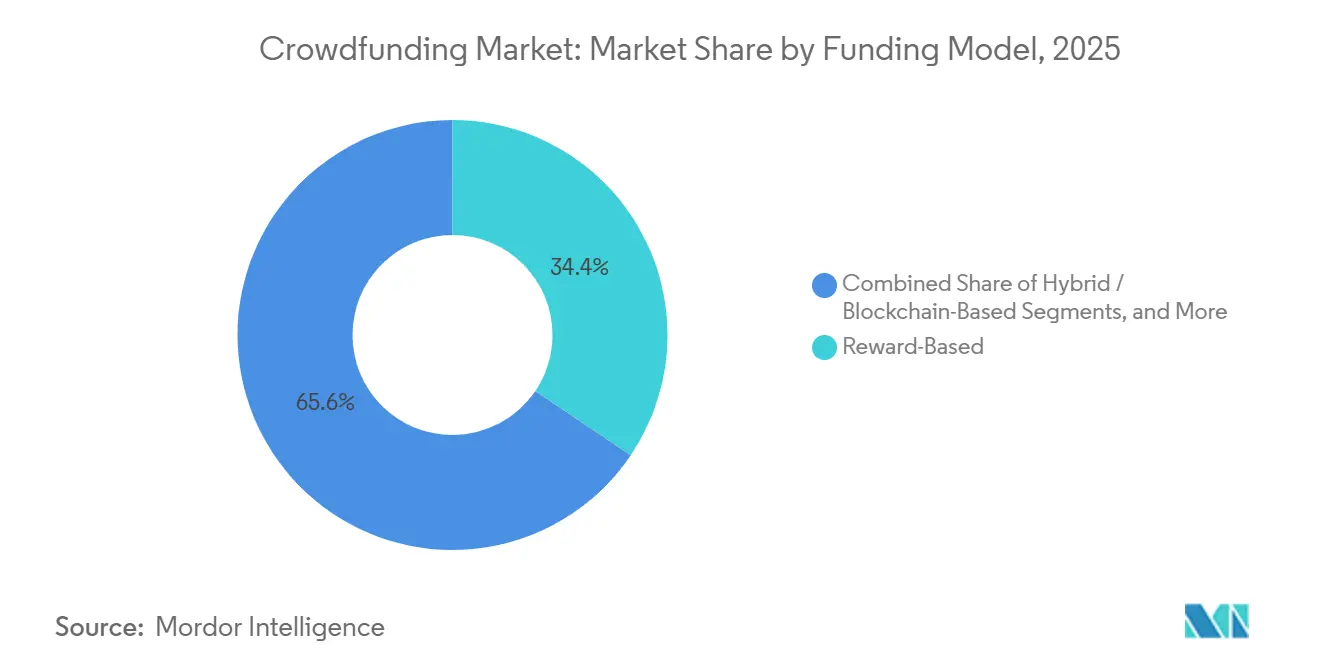

- By funding model, reward-based campaigns led with 34.44% revenue share in 2025, while hybrid structures are advancing at a 16.22% CAGR through 2031.

- By investment size, micro investments held 50.24% of the crowdfunding market share in 2025; large-ticket campaigns above USD 1 million are forecast to expand at a 17.06% CAGR to 2031.

- By platform deployment, cloud-based architecture captured 72.69% share of the crowdfunding market size in 2025 and is growing at a 17.56% CAGR through 2031.

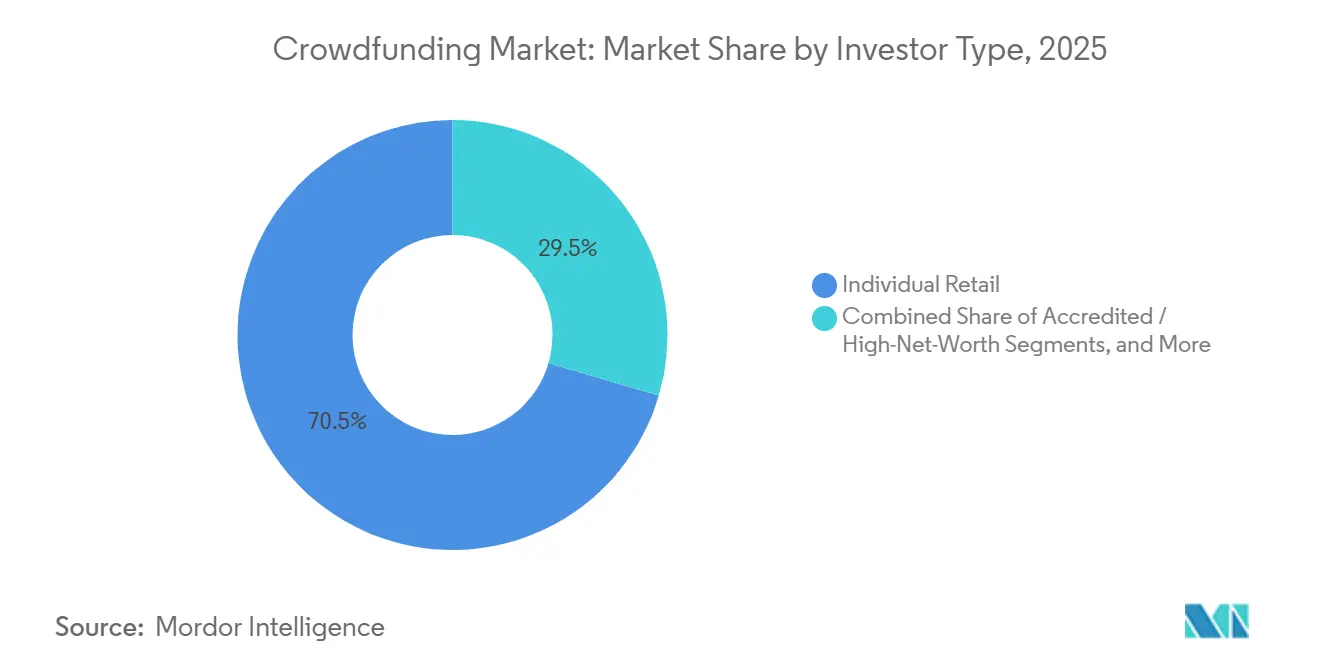

- By investor type, retail investors accounted for 70.46% share in 2025, whereas institutional participation is recording the highest CAGR of 16.88% through 2031.

- By application sector, technology and innovation dominated with 30.12% share in 2025, yet real-estate campaigns are advancing at a 16.46% CAGR toward 2031.

- By geography, Asia Pacific commanded 50.28% share in 2025, while Africa remains the fastest growing region at a 17.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Crowdfunding Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social-media virality boosts reward campaigns | +2.1% | North America and Europe | Short term (≤ 2 years) |

| EU-wide ECSP regulation unlocks cross-border equity crowdfunding | +2.8% | Europe, spill-over to Middle East and Africa | Medium term (2-4 years) |

| AI-powered campaign analytics lift success rates | +2.5% | Global | Medium term (2-4 years) |

| Blockchain tokenization enables fractional real estate | +3.0% | Asia Pacific core, spill-over to North America and Middle East | Long term (≥ 4 years) |

| Corporate ESG commitments fund social-impact projects | +1.9% | Africa and South America | Medium term (2-4 years) |

| Rising adoption of Shariah-compliant platforms | +1.7% | Middle East, Malaysia, Indonesia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU-Wide ECSP Regulation Unlocking Cross-Border Equity Crowdfunding

The European Crowdfunding Service Providers Regulation 2020/1503 offers a single passport that lets platforms reach investors across all member states without opening local entities. This lowers legal overhead, aggregates liquidity, and expands issuer reach, all while capping offering size at EUR 5 million (USD 4.24 million) and mandating standardized disclosures.[1]Financial Services Agency, “Regulatory Reforms for Start-Ups,” fsa.go.jp Seedrs and Crowdcube now penetrate Southern and Eastern Europe, while regulators in the Gulf and Africa benchmark the framework to accelerate convergence. Persistent divergence in AML interpretations still raises compliance duplication, favoring platforms with large legal teams.

AI-Powered Campaign Analytics Increasing Success Rates Globally

Machine-learning engines parse historical pledge data and real-time engagement metrics to optimize pricing, reward tiers, and launch timing. Peer-reviewed studies show a 15-20-percentage-point lift in success rates for AI-enhanced campaigns. Natural-language models refine pitch quality, while anomaly detection blocks fake backers and duplicate wallets. These dual functions enhance investor trust and drive adoption in markets previously hamstrung by fraud.

Emergence of Blockchain Tokenization Enabling Fractional Real Estate in Asia Pacific

Tokenization splits high-value property into low-denomination digital securities. Japan’s 2024 reforms raised the small-offering cap to JPY 500 million (USD 3.35 million), clearing a path for security-token offerings under the crowdfunding market. Singapore’s MAS guidance likewise clarifies when tokens qualify as securities, enabling platforms such as RealX to market units cross-border. Smart contracts automate rental payouts and compliance, making fractional property stakes liquid and transparent.

Corporate ESG Commitments Channeling Funds Into Social-Impact Campaigns

Multinationals are routing sustainability budgets into campaigns that finance solar mini-grids, community clinics, and smallholder farming, often matching retail contributions to double the proceeds. Transparent reporting satisfies disclosure rules and boosts brand equity. Dependence on a handful of corporate backers nonetheless poses concentration risk if priorities shift during economic downturns.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High platform fraud losses undermine trust | -2.3% | Asia Pacific, parts of South America and Africa | Short term (≤ 2 years) |

| Fragmented KYC/AML rules raise compliance costs | -1.8% | Europe and United States | Medium term (2-4 years) |

| Crowdfunding fatigue reduces donation conversion | -1.5% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Restricted payment-gateway access in Africa | -1.4% | Africa, selective South America and Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Platform Fraud Losses Undermining Investor Trust in Asia Pacific

Fraudulent campaigns and misappropriation of funds persist where supervision lags transaction volumes. Some operators bypass requirements for segregated accounts and audits, eroding confidence among repeat backers. Japan’s Securities and Exchange Surveillance Commission has tightened oversight, yet enforcement remains uneven, allowing rogue platforms to arbitrage weak jurisdictions.

Fragmented KYC/AML Rules Elevating Compliance Costs

The ECSP passport does not harmonize identity checks, so platforms juggle 27 divergent KYC rulebooks and must tailor workflows country-by-country, driving up legal spend.[2]U.S. Securities and Exchange Commission, “Early-Stage Investors,” sec.gov U.S. operators face analogous friction when reconciling federal exemptions with state “blue-sky” laws, limiting smaller entrants. Platforms onboarding investors from multiple member states must maintain parallel compliance workflows, each tailored to national regulator expectations, and bear the cost of duplicative legal reviews and technology integrations

Segment Analysis

By Funding Model: Hybrid Structures Re-Define Capital Access

Reward campaigns accounted for a 34.44% crowdfunding market share in 2025, yet hybrid tokens are advancing at a 16.22% CAGR as smart contracts blend perks with equity rights. Equity rounds benefit from the SEC’s 2021 rule change allowing raises up to USD 5 million, broadening the crowdfunding market. Debt-based models meet underserved borrowers in emerging economies, while donation drives surge during health crises.

Hybrid offerings satisfy investor hunger for upside and liquidity. Republic now converts perks into equity through rolling funds, and Japan’s new small-offering regime expressly accommodates token offerings. Tax clarity and secondary-market rules remain works in progress, adding operational complexity even as adoption accelerates.

Note: Segment shares of all individual segments available upon report purchase

By Investment Size: Institutional Capital Scales Large-Ticket Campaigns

Micro pledges below USD 10,000 still form 50.24% of transaction count, but large-ticket rounds over USD 1 million show a 17.06% CAGR as pension funds and family offices embrace the crowdfunding market. SEC reforms that drop caps for accredited investors encourage seven-figure checks. Small investments between USD 10,000 and USD 250,000 serve accredited angels and syndicates that pool capital to access deal flow curated by platforms, while medium-sized investments between USD 250,000 and USD 1 million bridge the gap between angel rounds and institutional Series A financings.

Platforms respond with tiered KYC, side letters, and cap-table integrations acceptable to sophisticated allocators. AngelList reports that one-third of its seed deals involve AI startups, illustrating how institutional flows favor high-growth themes. The risk is crowding out retail backers who value community over financial returns.

By Platform Deployment: Cloud Infrastructure Enables Real-Time Compliance

Cloud implementations captured 72.69% of the crowdfunding market size in 2025 and grow at 17.56% CAGR as operators favor scalable data centers with embedded AML utilities. Elastic capacity keeps sites responsive during viral launches, and multi-region nodes meet data-residency mandates. Cloud platforms integrate third-party identity-verification services, sanctions-screening databases, and fraud-detection algorithms that reduce manual review workloads and accelerate investor onboarding from days to minutes.

On-premise installations remain among institutions that value direct control but face higher capex and slower feature rollouts. Japan’s Payment Services Act now allows cloud-hosted third-party custodians, further tilting the competitive field toward cloud natives.

By Investor Type: Retail Dominance Gives Way to Institutional Flows

Retail still commands 70.46% share, emblematic of the crowdfunding market’s democratized origins, yet institutional capital is growing fastest at 16.88% CAGR. Accredited investors occupy a middle tier, and corporate strategics leverage campaigns for early product validation. Accredited and high-net-worth individuals occupy a middle tier, participating in equity and real-estate crowdfunding campaigns that require investor certification but offer higher return potential and secondary-market liquidity.

Kalshi’s USD 1 billion raise in December 2025 underscores mainstream appetite for new models that fuse trading with crowdfunding mechanics. Nonetheless, preferential terms demanded by institutions can dilute the egalitarian ethos central to crowdfunding.

Note: Segment shares of all individual segments available upon report purchase

By Application Sector: Real Estate Outpaces Technology in Growth

Technology and innovation held 30.12% share in 2025, but real estate is expanding at a 16.46% CAGR as tokenization lowers entry thresholds. Food and beverage, media, and healthcare enjoy steady volumes, while social-impact projects harness corporate ESG matches to amplify donor reach.Food and beverage campaigns attract consumer-product entrepreneurs launching direct-to-consumer brands, while media and entertainment projects fund film productions, music albums, and gaming titles that offer backers exclusive content and creative input.

Japan’s liberalized offering caps reduce costs for tokenized property sales, giving real estate a structural advantage. Automated rent distribution and transparent ledgers entice both retail and institutional buyers into the crowdfunding market.

Geography Analysis

Asia Pacific commands half of global volume, driven by mobile wallets, supportive sandbox regulations, and the 2024 Japanese reforms that quadrupled small-offering limits. The region’s blockchain hubs Singapore, Hong Kong, and Tokyo host security-token exchanges that deepen liquidity and anchor the crowdfunding market. Fraud concerns remain pronounced in China and parts of Southeast Asia, yet AI-powered monitoring is narrowing the trust gap.

Africa’s 17.54% CAGR stems from mobile-money ubiquity and corporate ESG inflows. Platforms integrate M-Pesa rails to accept pledges without bank accounts, broadening reach. However, high network fees and restricted card gateways in West Africa raise operating costs, delaying expansion into francophone countries.[3]Milaap, “Trust and Transparency,” milaap.org

North America benefits from a deep base of accredited investors and the SEC’s relaxed caps, fueling mega rounds that blur lines with venture capital. Europe leverages the ECSP passport to knit fragmented markets, but divergent AML rules keep compliance costs high, consolidating share among larger operators.

South America faces currency volatility, so Brazilian and Argentine platforms now offer stablecoin-denominated campaigns to hedge inflation. The Middle East’s Shariah-compliant structures are gaining traction, especially in the Gulf, where asset-backed profit-sharing aligns with Islamic finance principles.

Competitive Landscape

The crowdfunding market remains fragmented, with Kickstarter and Indiegogo defending legacy reward niches while Republic, Seedrs, and Fundable vie for equity dominance. Kickstarter’s June 2024 shake-up that replaced seven senior officers reveals mounting pressure to reignite growth as rewards plateau.

Republic’s purchase of Seedrs in 2024 forged a trans-Atlantic powerhouse positioned to exploit the ECSP passport, while Kalshi’s USD 1 billion war chest underscores momentum for prediction-based models that merge crowdfunding with market speculation. Technology differentiation clusters around AI scoring engines, blockchain custody, and cloud-native compliance.

Platforms that integrate sanctions screening, biometric KYC, and automated AML monitoring retain investor trust and gain regulatory goodwill. Institutional capital intensifies rivalry; platforms offering co-investment rights, board seats, and secondary liquidity attract pension funds, while retail-centric portals emphasize community perks. Barriers to entry rise as multi-jurisdictional rules favor well-capitalized operators with robust legal teams.

Crowdfunding Industry Leaders

Kickstarter PBC

Indiegogo Inc

Fundable LLC

Crowdcube Limited

GoFundMe Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Kalshi raised USD 1 billion at an USD 11 billion valuation, reflecting institutional appetite for alternative crowdfunding mechanisms.

- March 2025: SQUID closed a EUR 1.69 million crowdfunding round on Crowdcube, onboarding 2,624 investors and proving platform reach among first-time backers.

- March 2025: Nothing launched its second community equity round on Crowdcube, mirroring its Series B valuation and illustrating cross-border compliance hurdles for U.S., Canadian, Indian, and Japanese participants.

- January 2025: The Securities Commission Malaysia emphasized equity crowdfunding and peer-to-peer financing as crucial mechanisms for micro, small, and medium enterprise growth in its 2024 annual report, signaling governmental support for alternative financing expansion across Southeast Asian markets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global crowdfunding market as the total annual funds successfully raised on online platforms that facilitate reward, equity, debt / peer-to-peer, and donation campaigns for businesses, projects, and social causes. The figure includes pledges collected in primary currencies and later converted to USD at prevailing yearly averages.

Scope exclusion: Offline charity drives and consumer loans issued outside recognized crowdfunding regulations are not covered.

Segmentation Overview

- By Funding Model

- Reward-Based

- Equity-Based

- Debt / P2P Lending

- Donation-Based

- Hybrid / Blockchain-Based

- Real-Estate-Specific Crowdfunding

- By Investment Size

- Micro (Less Than USD 10 k)

- Small (USD 10 k - 250 k)

- Medium (USD 250 k - 1 m)

- Large (Greater Than USD 1 m)

- By Platform Deployment

- Cloud-Based

- On-Premise

- By Investor Type

- Individual Retail

- Accredited / High-Net-Worth

- Institutional

- Corporate Strategic

- By Application Sector

- Technology and Innovation

- Food and Beverage

- Media and Entertainment

- Real Estate and Construction

- Healthcare and Life Sciences

- Social Impact and Non-Profit

- Consumer Products and Fashion

- Other Application Sectors

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Southeast Asia

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

To validate desk findings, we conduct structured discussions with platform compliance heads, campaign creators, angel investors, and fintech regulators across North America, Europe, and fast-growing Asian markets. Insights on average ticket size changes, campaign success ratios, and emerging blockchain models help us refine assumptions and close information gaps.

Desk Research

We begin by compiling platform-level disclosures from sources such as United States Form-CF filings, the U.K. Financial Conduct Authority data portal, European Commission ECSPR registers, and crowd-platform transparency dashboards. Macro context is enriched with World Bank Findex adoption rates, International Monetary Fund digital-payment statistics, and trade association briefs from the Crowdfunding Professional Association.

Next, Mordor analysts dive into company filings and press releases harvested through Dow Jones Factiva and D&B Hoovers, then scan academic journals and OECD working papers that track alternative finance flows. These references illustrate typical campaign sizes, fee structures, and regional regulatory shifts. The list above is illustrative, not exhaustive, and many additional public records inform our desk work.

Market-Sizing & Forecasting

The core model applies a top-down and bottom-up blend. We start by aggregating yearly funds raised per country, reconstructed from regulatory filings and platform dashboards, then project missing regions using internet-penetration driven adoption curves. Results are cross-checked against sampled supplier roll-ups of fee revenue multiplied by implied gross funds to test reasonableness before adjustments. Key drivers include campaign success rate trends, average contribution per backer, number of active platforms, regulatory caps, and smartphone penetration. A multivariate regression links these variables to historical funding volumes, and its coefficients power the 2025-2030 forecast scenarios. Data voids are bridged with carefully bracketed ranges discussed with industry experts.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, variance checks against independent indicators, and a sign-off call. Reports refresh each year, with interim revisions triggered by material regulatory or macro events. Before release, an analyst performs a fresh sweep so clients receive the latest view.

Why Mordor's Crowdfunding Baseline Scores Unmatched Decision-Making Trust

Published estimates often differ because firms pick distinct scopes, currencies, and refresh cadences. Some track only platform fee revenue, others mix broader alternative-finance pools, and many rely on outdated exchange rates.

Key gap drivers in the crowdfunding space include whether donation campaigns are counted, how cross-border flows are treated, the depth of geographic coverage, and the inflation path applied to average contribution values. Mordor's study captures the full funding volume, applies uniform IMF currency tables, and is updated annually, which collectively raise comparability.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 24.05 B (2025) | Mordor Intelligence | |

| USD 2.14 B (2024) | Global Consultancy A | Tracks only platform fee revenue and omits Asia & Latin America |

| USD 1.60 B (2024) | Trade Journal B | Focuses on crowdfunding software sales; excludes donation campaigns |

The comparison shows that when narrower scopes or limited regions are applied, totals shrink markedly. By anchoring figures to complete campaign proceeds and a transparent, annually refreshed model, Mordor Intelligence offers decision-makers a balanced, reproducible baseline they can trust.

Key Questions Answered in the Report

How large is the global crowdfunding market in 2026?

The crowdfunding market size stands at USD 27.93 billion in 2026 and is projected to double by 2031.

Which region leads current crowdfunding volumes?

Asia Pacific holds 50.28% of 2025 transaction value, supported by mobile payments, micro-investments, and tokenization rules.

What funding model is growing fastest?

Hybrid blockchain-enabled structures are expanding at a 16.22% CAGR as they combine reward perks with equity and secondary-market liquidity.

How are institutional investors influencing the space?

Institutional capital is the fastest-growing investor segment at 16.88% CAGR, driving larger ticket sizes and secondary-market development.

Which application sector shows the strongest growth momentum?

Tokenized real-estate projects are advancing at a 16.46% CAGR, outpacing technology campaigns due to lower entry thresholds and automated rent distributions.

What is the main regulatory catalyst in Europe?

The ECSP Regulation creates a single EU passport for platforms, simplifying cross-border equity crowdfunding and expanding the addressable investor base.