Ready To Assemble Furniture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

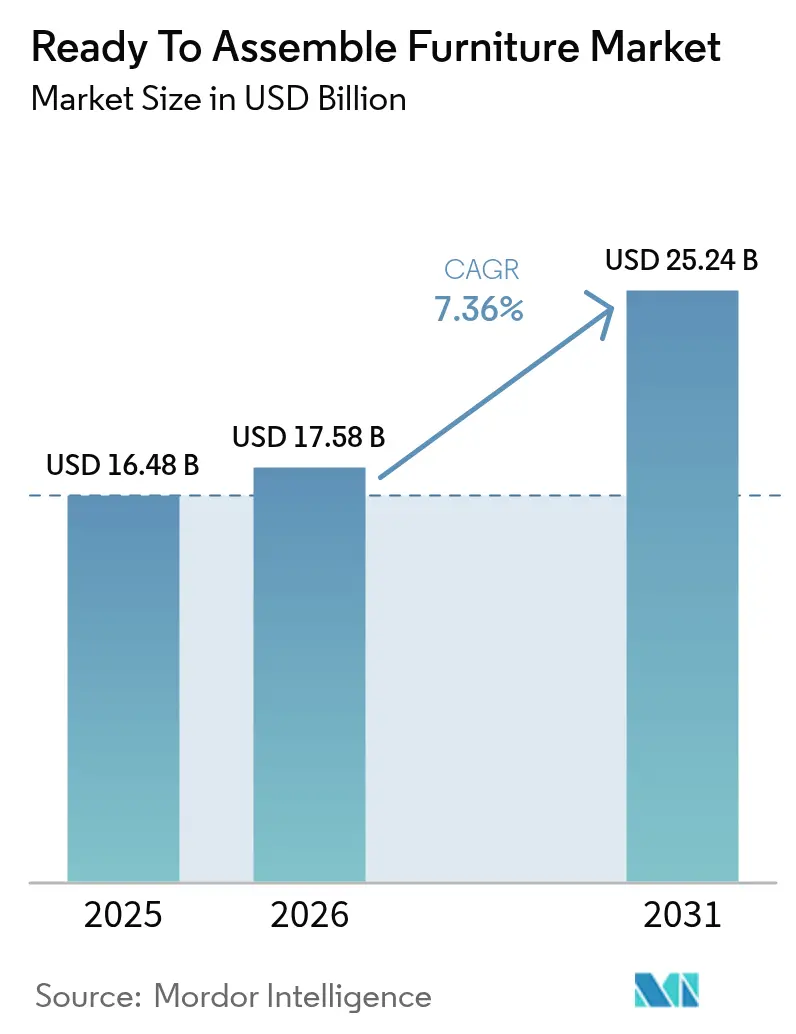

| Market Size (2026) | USD 17.58 Billion |

| Market Size (2031) | USD 25.24 Billion |

| Growth Rate (2026 - 2031) | 7.36% CAGR |

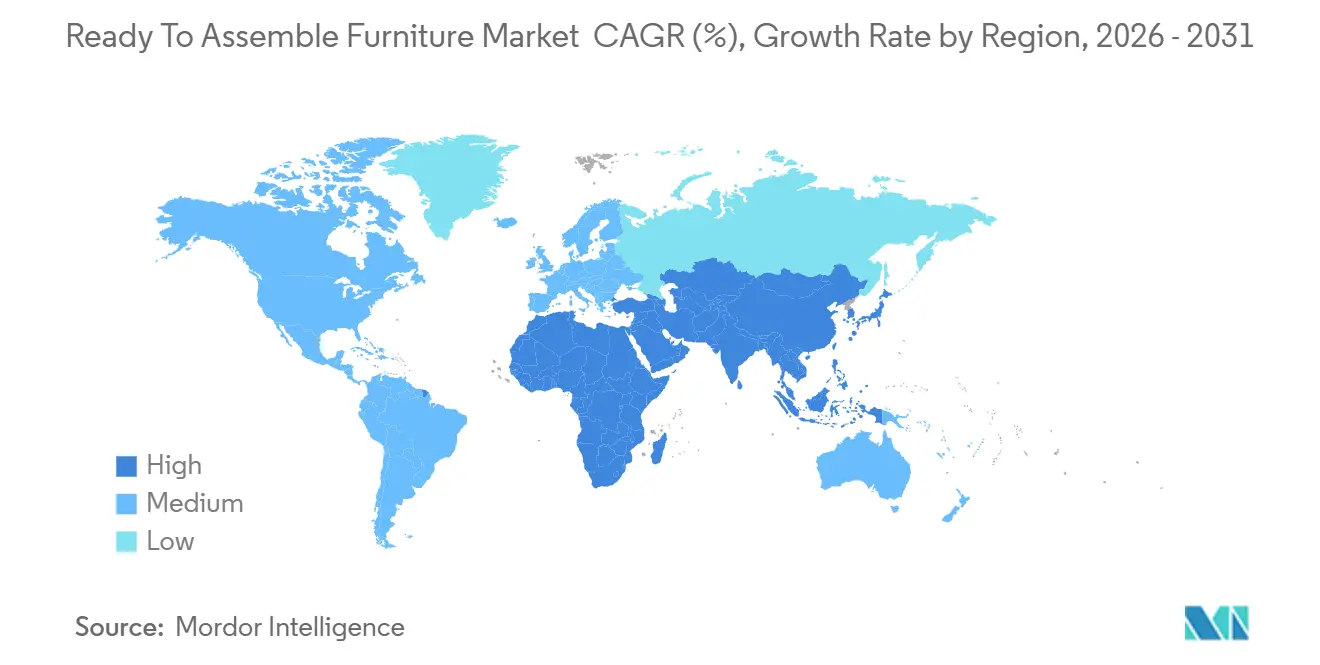

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

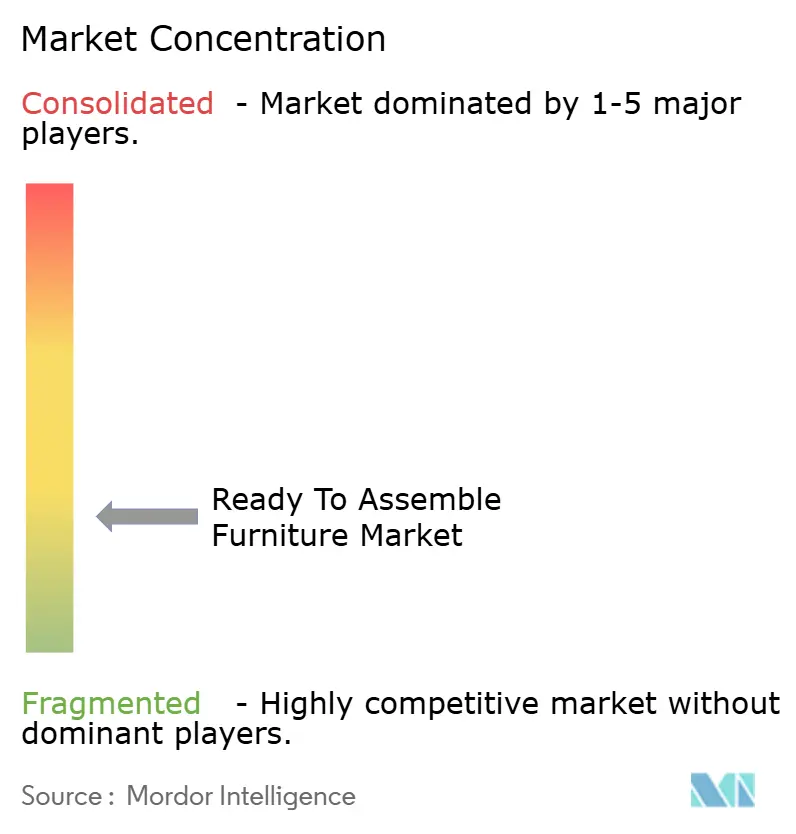

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ready To Assemble Furniture Market Analysis by Mordor Intelligence

The RTA furniture market size is expected to grow from USD 16.48 billion in 2025 to USD 17.58 billion in 2026 and is forecast to reach USD 25.24 billion by 2031 at 7.36% CAGR over 2026-2031. Momentum in the RTA furniture market benefits from a mix of compact urban living, direct-to-consumer models that compress cost-to-value, and design-for-repair regulations in the European Union that align with flat-pack and tool-free assembly. The channel mix continues to favor online, with online retail as the fastest-growing distribution channel through 2031, reinforcing the digital discovery, AR visualization, and quick-ship expectations that have reshaped the RTA furniture market. North America’s installed base and DIY culture underpin a sizable revenue pool, while Asia-Pacific’s faster pace suggests higher absolute volume growth over the forecast horizon. Design shifts toward faster, simpler assembly are now visible in flagship ranges and retail experiences that blend showrooming with digital fulfillment in the RTA furniture market, exemplified by new collections and omnichannel formats that validate the need for tactile evaluation alongside an e-commerce core[1]IKEA.COM https://www.ikea.com/global/en/stories/design/stockholm-2025-collection-250407.

Key Report Takeaways

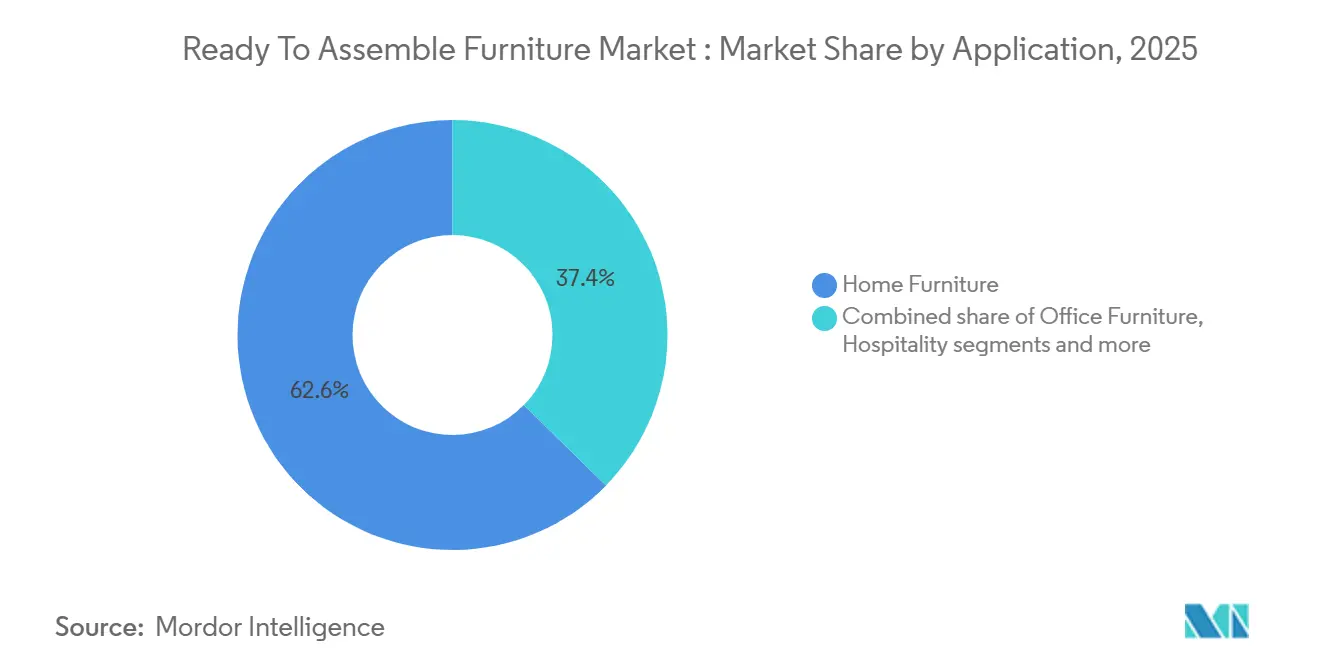

- By application, home furniture led with 62.65% of the RTA furniture market share in 2025, while office and commercial furniture is forecast to expand at a 7.35% CAGR to 2031.

- By material, wood-based panels accounted for 47.62% of the RTA furniture market share in 2025, and plastic and polymer products are projected to grow at a 6.63% CAGR to 2031.

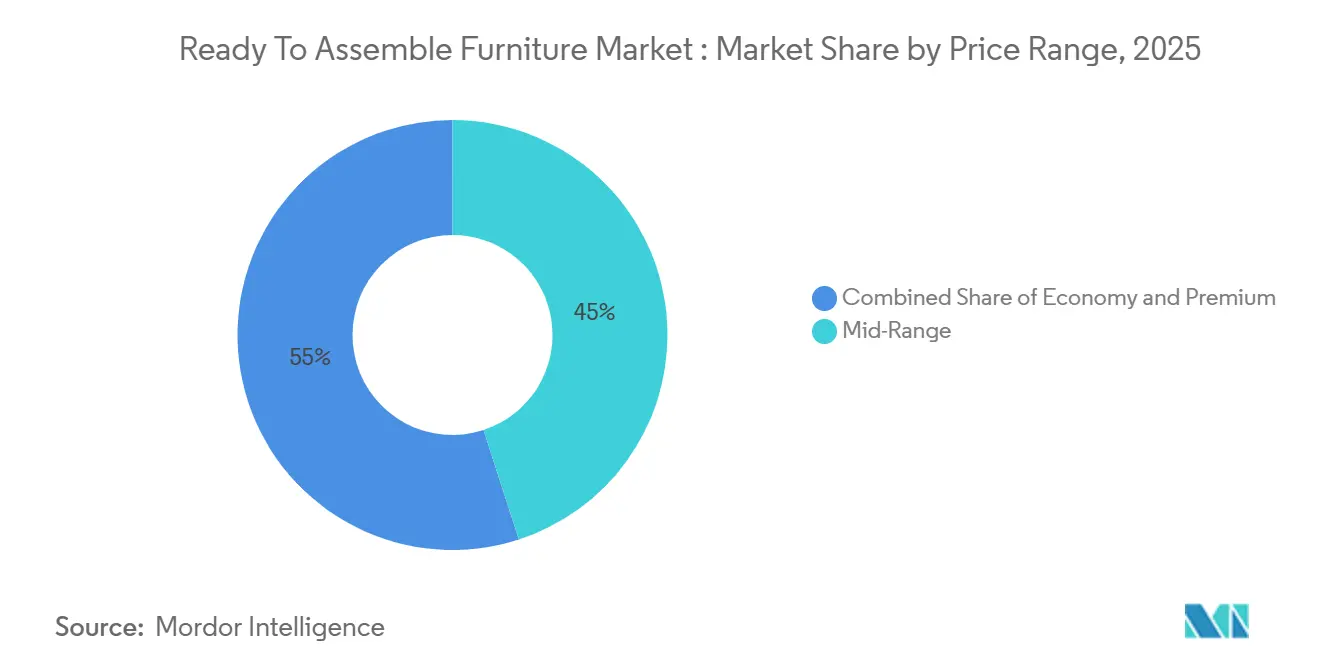

- By price range, mid-range products commanded 45% of the RTA furniture market share in 2025 and are projected to expand at a 6.71% CAGR to 2031.

- By distribution channel, B2C/Retail held 58% of the RTA furniture market share in 2025, while online retail is forecast to expand at an 8.17% CAGR through 2031.

- By geography, North America held 35% of the RTA furniture market share in 2025, and Asia-Pacific is forecast to expand at a 6.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ready To Assemble Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DIY and personalization culture expanding RTA adoption | +1.2% | Global, with early gains in North America (U.S., Canada), Western Europe (Germany, UK), and urban Asia-Pacific (China Tier-1 cities, South Korea) | Medium term (2-4 years) |

| Modular/multifunctional designs and affordability broaden use cases | +1.5% | APAC core (China, India, Japan), spill-over to North America and EU metropolitan areas, with shrinking apartment footprints | Medium term (2-4 years) |

| Sustainability and eco-friendly materials are shaping purchase decisions | +0.9% | North America & EU, driven by ESPR/DPP compliance and consumer preference for FSC/PEFC certification | Long term (≥ 4 years) |

| Residential construction and household formation underpin demand | +1.8% | Global, with pronounced impact in Asia-Pacific (India, Vietnam, Indonesia) and selective North American sunbelt metros | Short term (≤ 2 years) |

| EU ESPR/Digital Product Passports favoring repairable, traceable RTA | +0.6% | EU-27, with indirect influence on export-oriented manufacturers in Turkey, Poland, and China, is seeking EU market access | Long term (≥ 4 years) |

| Amazon SIPP packaging incentives are improving RTA unit economics | +0.4% | North America & EU, where Amazon’s logistics network is most dense | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

DIY and Personalization Culture Expanding RTA Adoption

Do-it-yourself norms and personalization impulses are expanding the appeal of flat-pack sets from a budget choice to a creative, flexible furnishing option for renters and owners alike. Tool-free systems lower the barrier to entry by enabling quick, stable, and repeatable assembly across multiple moves, which is important for urban renters who value convenience and portability in the RTA furniture market. Multiple flagship ranges now embed connector and wedge innovations that eliminate the need for power tools while maintaining fit, finish, and structural integrity across repeated assembly cycles, elevating perceived quality of self-assembled products. Neutral-finish programs and laminate solutions that accept customer finishing or refinishing have also grown, allowing buyers to tailor look and feel with lower cost and lower risk, which helps reduce returns and increase attachment purchases like hardware and inserts over time. Industry recognition for tool-less designs signals that ease-of-assembly is now a defining feature rather than a niche add-on, with award programs in 2024 validating connector systems that compress build times for a broad set of case goods in the RTA furniture market[2]G-MARK.ORG https://www.g-mark.org/en/gallery/winners/26871?unitCodes=10&years=2024. .

Modular/Multifunctional Designs and Affordability Broadening Use Cases

Space constraints in dense metros keep elevating the role of modular casework, expandable dining systems, and convertible seating that handle work, storage, and hosting within compact footprints. The RTA furniture market sees this in expanding ranges that emphasize reconfiguration, stackable units, and add-on modules that let consumers scale over time without full-room commitments, which aligns with incremental budgeting. Showcase collections have put flexibility at the center with pieces that can be assembled, extended, or re-shaped by hand, and retailers have paired these with showrooms that allow tactile evaluation to support higher-consideration purchases such as sofas and dining. The same retailers are investing in large-format stores that reinforce an omnichannel funnel, helping address showrooming and build confidence in big-ticket items, while digital channels continue to drive the majority of orders in the RTA furniture market. Over the forecast period, growth in modular ranges at mid-range price points is expected to outpace low-end commodity sets, as buyers seek durability and visual cohesion that can flex with household changes in the RTA furniture market.

Sustainability and Eco-Friendly Materials Shaping Purchase Decisions

Environmental criteria have moved into mainstream selection and compliance in key regions, with design-for-disassembly and traceability aligning with the construction and lifecycle of flat-pack systems. The RTA furniture market benefits where recycled content, lower-emissions binders, and circular take-back or refurbishment programs reinforce brand trust while meeting upcoming rulemaking schedules that prioritize repairability and verified sourcing. Product strategies that push toward recycled-wood particleboard and documented inputs help manufacturers reduce exposure to raw wood volatility and enhance compliance confidence for cross-border sales in Europe. Award milestones and public commitments around design simplicity and minimal tooling also support lower damage rates in transit and denser packing, which bring associated freight and carbon advantages in the RTA furniture market. Retailers and manufacturers that publish material disclosures and pursue programmatic upgrades to in-store and online experiences are set to benefit from stronger conversion rates when sustainability positioning is clear and verifiable.

Residential Construction and Household Formation Underpinning Demand

Household formation and homebuilding activity remain pivotal to purchase cycles for kitchens, storage, and home-office setups that are core to the RTA furniture market. U.S. building-materials tariffs have raised the cost basis for new homes, affecting downstream furnishing budgets and channel mix as buyers rebalance toward value and self-assembly options that stretch spend without deferring essential categories. As rates normalize and new home pipelines stabilize, replenishment and refresh cycles for bedrooms and living spaces are expected to broaden the buyer base for mid-range RTA assortments with durable laminates and modular expansion paths. E-commerce-led players report sustained customer engagement, and store openings in select metros are designed to improve attachment rates in higher-touch categories while preserving digital scale in the RTA furniture market[3]ABOUTWAYFAIR.COM https://www.aboutwayfair.com/category/company-news/wayfairs-physical-retail-expansion-continues-new-atlanta-store-coming-in-2026. In Asia-Pacific, urbanization and rising incomes form a strong multi-year base of first-time buyers for kitchens and wardrobes, where flat-pack solutions address budget and installation constraints while maintaining style consistency across small-room layouts in the RTA furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material and input cost volatility (wood panels, steel, freight) | -1.4% | Global, with acute pressure in North America (Canadian lumber tariffs) and Europe (energy-intensive MDF production) | Short term (≤ 2 years) |

| Competition from assembled and secondhand furniture options | -0.8% | North America & EU, where vintage/thrift culture and marketplace platforms are mature | Medium term (2-4 years) |

| U.S. tip-over stability standard (STURDY/ASTM F2057-23) raises compliance burden | -0.3% | National, with early gains in the U.S. domestic supply chain | Medium term (2-4 years) |

| U.S. AD/CVD duties on Chinese RTA cabinets/vanities are increasing import costs | -0.5% | North America, specifically the U.S., imports case goods from China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material and Input Cost Volatility (Wood Panels, Steel, Freight)

Manufacturers continue to navigate uneven panel pricing, metal hardware inputs, and freight variability that together compress margins and complicate SKU planning in the RTA furniture market. Steel remains a notable swing factor in drawer slides, hinges, and frames, with recent North American price dynamics prompting buyers to adjust contract duration and indexation to reduce exposure to spikes. Freight conditions are more stable than peak disruption, but routing shifts and localized equipment tightness still translate to longer lead times or higher costs for Asia–North America flows, which adds friction to quick-ship value propositions in the RTA furniture market. In North America, building-materials tariffs on wood and steel raise the baseline cost of new construction, which cascades into downstream furnishing costs and can shift buyers toward mid-range flat-pack options where assembly offsets sticker price pressure. Operators are responding with component verticalization, nearshore sourcing, and design simplification to reduce metal content or consolidate fasteners, which supports resilience in the RTA furniture market. Over the next two years, pricing discipline and SKU rationalization are expected to remain priorities as producers balance cost pass-through with conversion risk in price-sensitive categories.

Competition from Assembled and Secondhand Furniture Options

Consumers in mature markets have abundant access to assembled alternatives through white-glove delivery packages, which narrows the convenience gap that historically favored flat-pack sets in the RTA furniture market. Secondhand channels have also scaled and become easier to use, which supports blended purchasing that mixes new with vintage and exerts extra pressure on like-for-like RTA price points. In higher-consideration categories, omnichannel retailers are doubling down on showrooms to improve conversion through tactile evaluation while maintaining the speed and breadth of online assortments in the RTA furniture market. Product innovation provides a counterweight, as tool-free systems and quick-assembly fittings improve the user experience and reduce returns, helping defend share against turnkey offers in comparable price bands. Retailers that pair clear assembly experiences with modular upgrades and strong after-sales support are better positioned to retain customers who might otherwise default to assembled or secondhand purchases in the RTA furniture market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Office Segments Propel Hybrid-Work Furniture Surge

Home furniture accounted for 62.65% of 2025 revenues, reflecting the centrality of bedroom sets, kitchen cabinets, and storage units that anchor initial purchases in the RTA furniture market. Kitchen programs capture high-ticket value within this base, and brands have broadened modular cabinet offerings that fit standard appliances while enabling semi-custom layouts that match small urban footprints and starter-home budgets. Wardrobes remain vital in dense metros where built-in storage is limited, and online planning tools enable room-specific configuration, reducing returns and accelerating delivery in the RTA furniture market. Dining sets and expandable tables show steady demand driven by more at-home meals and flexible hosting, while living room storage continues to grow as households integrate media, work, and play into shared spaces. Across the segment, convenience and cost discipline keep the home category stable, and the RTA furniture market benefits where assembly is demonstrably quick and durable.

Office and commercial furniture is the fastest-growing application, with a 7.35% CAGR through 2031, supported by hybrid work adoption, employer reimbursements, and modular workstations that can move with employees or reconfigure for space optimization. Procurement teams value durability at mid-range price points and favor flat-pack options that reduce freight and onsite assembly time, elevating the RTA furniture market in corporate and small-business refreshes. Home-office subcategories also remain resilient across desks, ergonomic seating, and storage towers, especially where retailers combine omnichannel showrooming with fast digital fulfillment to capture higher-consideration purchases. As commercial landlords retrofit and right-size spaces, flexible partitions and mobile storage units gain traction, which extends the addressable base for tool-free systems in the RTA furniture industry. The application mix, therefore, balances the scale of home-related purchases with the faster pace of office and commercial settings, strengthening the overall growth profile of the RTA furniture market.

Note: Segment shares of all individual segments available upon report purchase

By Material: Plastic Composites Gain Ground on Sustainability Wave

Wood-based panels held a 47.62% share in 2025, underlining their entrenched role in case goods and cabinet construction for the RTA furniture market. Particleboard and MDF remain cost-effective substrates for laminated surfaces, and continuous-press production supports consistent quality and tight tolerances in mass-market lines. Regulatory pressure on emissions continues to influence resin selection and panel specifications, steering manufacturers toward binders and finishes that support lower-emission targets and material disclosures. Sourcing and traceability initiatives are also gathering pace in Europe, which benefits brands that can demonstrate recycled content and a verified chain of custody within the RTA furniture market. The result for wood-based materials is a measured mix of cost management and compliance investment that preserves performance advantages in core indoor applications.

Plastics and polymers are the fastest-growing material category, with a 6.63% CAGR through 2031, aided by lighter weight, weather resistance, and the long-term promise of verified recycled inputs for outdoor and storage lines. Weight reductions improve container utilization and handling efficiency, translating into meaningful delivery savings for bulky items in the RTA furniture market. As brands expand recycled-content claims and surface finishes that resist abrasion and moisture, plastics gain credibility beyond purely utilitarian items without displacing wood in core case goods. Metal components remain central to frames and functional hardware, and cost-control efforts have focused on part consolidation and multi-sourcing to address price swings that affect the RTA furniture market[4]GORDIAN.COM https://www.gordian.com/resources/steel-price-updates. . Taken together, the material landscape supports a balanced approach in which wood-based substrates hold the largest share, while polymers steadily gain ground on sustainability narratives and logistics advantages in the RTA furniture market.

By Price Range: Mid-Range Products Balance Aspiration and Accessibility

Mid-range products held a 45% share in 2025 and are forecast to grow at a 6.71% CAGR through 2031, reflecting the strongest trade-up behavior from entry-level sets in the RTA furniture market. The appeal lies in better laminates, edge treatments, and modular expandability that deliver a visible upgrade at a manageable price point, while still shipping flat and assembling quickly at home. These programs bridge buyer expectations for style consistency and functional performance with budgets that favor staged purchases, such as adding towers or extensions over time rather than committing to a full room. Durability gains lengthen replacement cycles, which improve customer satisfaction, reduce returns, and support attach rates for integrated accessories in the RTA furniture market. As raw-material costs normalize slowly, mid-range producers should retain pricing power through specification discipline and curated designs that emphasize quality and convenience.

Economy tiers maintain volume in price-sensitive regions and on online marketplaces, but inflated panel and hardware costs have squeezed margins, prompting value players to trim assortments and simplify designs in the RTA furniture industry. Premium RTAs remain a niche, where customization and branded aesthetics support higher prices, but they face direct competition from assembled alternatives marketed with concierge services. The net effect is a barbell pattern in some channels, though mainstream demand is consolidating around mid-range, where the balance of price, quality, and modular flexibility is strongest in the RTA furniture market. Over the forecast period, the mid-range is positioned to widen its lead if supply chains sustain on-time availability and consistent finish quality. Stronger online visualization and the option to experience key items in newly opened showrooms should reinforce these gains in the RTA furniture market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Online Retail Rewrites Go-to-Market Playbooks

B2C/Retail channels accounted for a 58% share in 2025, but within this mix, online retail is the standout, growing at an 8.17% CAGR through 2031 as digital-first models absorb showroom economics in the RTA furniture market. Online platforms benefit from larger assortments, social proof, and lower overhead, which enable sharper pricing in flat-pack categories where logistics density is a decisive advantage. Retailers are now augmenting the digital funnel with select large-format stores that provide tactile validation for high-consideration SKUs while keeping primary demand capture online in the RTA furniture market. Store networks with warehouse-style footprints remain relevant for immediate pickup and DIY-focused accessories, and these venues integrate closely with e-commerce for click-and-collect workflows that suit RTA purchases. Over time, the most resilient models are likely to blend channel strengths so that customers can discover, configure, and fulfill in the ways that best match their category and budget needs in the RTA furniture market.

B2B/Project channels continue to find traction in hospitality, offices, and residential programs where standardized, durable, and design-neutral collections reduce procurement complexity. Suppliers with vertically integrated component offerings now monetize scale by serving both finished-goods retail and B2B parts demand, diversifying revenue and stabilizing plant utilization in the RTA furniture market. As institutional buyers formalize sustainability criteria and consider lifecycle costs, tool-free assembly and repair-friendly designs stand out for their operational advantages in turnover and maintenance. Projects that phase installations can also leverage modularity to scale over time without stranding assets, which is an attractive feature in budget cycles that require flexibility in the RTA furniture market. The net effect is an ecosystem where retail and project channels reinforce each other through shared supply chains and overlapping product platforms.

Geography Analysis

North America held 35% of global revenue in 2025 and remains a core profit pool, though its forecast growth trails Asia-Pacific over 2026 to 2031 in the RTA furniture market. The United States dominates regional demand and supply dynamics, with tariffs on lumber and steel adding to the baseline cost of new construction and renovations, which shapes the mix of purchases and preferred channels for flat-pack goods. DIY culture and broad home-improvement retail networks underpin conversion for storage, office, and bedroom categories that ship well and assemble quickly. As omnichannel players open large-format locations in select metros, higher-consideration categories such as sofas and dining benefit from showroom validation while digital ordering continues to dominate volume in the RTA furniture market. Canada’s integrated panel capacity supports regional availability but has experienced episodic supply tightness, reinforcing the case for diversified sourcing and component inventories in the RTA furniture market. Over the forecast horizon, the region’s growth outlook is anchored by steady household formation and ongoing home-office refresh cycles across suburban and sunbelt markets.

Europe’s growth profile is shaped by sustainability and circular-economy policies that align well with design for disassembly, repair, and verified sourcing in the RTA furniture market. IKEA remains a dominant force, with fiscal-year 2025 revenue of EUR 26.3 billion (USD 28.4 billion) and a concentrated presence in Europe, where tool-free assembly strategies are prominent across new lines. Shifts in sourcing footprints follow policy and geopolitical changes, and brands with deeper traceability and recycled-content investments are positioned to avoid disruption and capture premium demand. Energy costs for panel production influence material choices, with particleboard often favored over more energy-intensive MDF in specific facilities, while import balancing from adjacent regions supplements local supply. The RTA furniture market in Europe also benefits from a mature e-commerce base and click-and-collect models that reduce last-mile costs on bulky items without requiring legacy showroom overhead. Over the forecast period, compliance readiness and sustainability credentials are likely to drive measurable differentiation and pricing power in the region.

Asia-Pacific is the fastest-growing region, with a 6.93% CAGR through 2031, and is projected to account for a large share of global volume in the RTA furniture market. Urbanization and new-household formation in India and Southeast Asia support first-time purchases of kitchens, wardrobes, and home-office sets, while capacity expansions across key panel categories stabilize availability. Consumer expectations for design and convenience keep rising, and retailers in the region are investing in footprint and assortment strategies that match the rapid growth trajectory of the RTA furniture market. Tool-free assembly and modular systems are especially resonant for renters and young buyers who relocate more frequently and prize flexible layouts. As regional producers build export pipelines and deepen local distribution, Asia-Pacific’s role as both a supply engine and a demand growth center continues to expand in the RTA furniture market.

Competitive Landscape

The RTA furniture market remains fragmented globally, with the top five players well below 40% combined market share, leaving room for regional specialists and private labels to compete on cost, availability, and cultural fit. IKEA anchors the category with fiscal-year 2025 revenue of EUR 26.3 billion (USD 28.4 billion) and sustained focus on tool-free assembly designs that align with repairability and ease-of-use imperatives across Europe and other core geographies. North American leaders have shifted strategies to better match input-cost dynamics and category mix, with one major manufacturer launching a B2B component venture to monetize its manufacturing scale and serve peer brands with drawer boxes, doors, and panels in addition to finished goods. This vertical extension diversifies revenue and helps hedge against tariff cycles that can disrupt import-dependent assortments in the RTA furniture market. Competitive levers have therefore expanded beyond pure price to include sourcing resilience, compliance readiness, and design simplicity, which translate to faster assembly and lower damage.

Restructuring is also evident among incumbents consolidating production footprints and reweighting toward import-led ranges as domestic cost structures erode competitiveness in the RTA furniture market. In 2025, a leading North American brand closed remaining domestic RTA production, took restructuring charges, and pivoted toward a leaner, import-focused approach that consolidates high-performing SKUs under a streamlined division with clearer margin goals in 2026. On the retail side, digital-first players moved into physical formats where showrooms help close higher-consideration purchases while the majority of orders still originate online. Parallel expansion by Scandinavian retailers into new countries strengthens competition across Europe, the Middle East, and the Americas, while store-level investments in digital capabilities underscore the long-term shift toward omnichannel engagement in the RTA furniture market.

Innovation that removes tools and reduces assembly time stands out as a source of differentiation for both product experience and logistics in the RTA furniture market. Connector systems that slash assembly time and eliminate the need for screws, lifting perceived quality, and making the prospect of self-assembly are appealing for a wider range of buyers. Retailers and brands that foreground these features in merchandising and instructions tend to see lower return rates and higher satisfaction. At the same time, component verticalization among manufacturers and curated, modular programs among retailers point to converging strategies that emphasize reliability, assembly simplicity, and replenishment speed as primary competitive variables in the RTA furniture market. The mix of fragmented supply and advancing product design suggests an ongoing opportunity for challengers that can marry cost control with clear quality and ease of use.

Ready To Assemble Furniture Industry Leaders

Sauder Woodworking Co.

Dorel Industries Inc. (Dorel Home)

Tvilum A/S

Nitori Holdings Co., Ltd.

IKEA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: JYSK announced plans to open 20 new stores across 10 countries. JYSK is not only updating its older stores to the modern 3.0 concept but is also gearing up for the upcoming autumn season as part of its ongoing expansion efforts.

- April 2025: IKEA unveiled its Stockholm 2025 collection, the largest edition to date with 96 pieces, featuring tool-free assembly via patented wedge dowel fittings and modular sofas developed through multiple prototypes to balance comfort and reconfigurability, directly addressing consumer demand for DIY convenience and flexible living-space solutions.

- March 2025: Wayfair announced the location of its second large-format store in Atlanta, Georgia, set to open in 2026, following the success of its Wilmette, Illinois, flagship that attracted more than 720,000 visitors in its first year and lifted Illinois furniture sales, validating its omnichannel strategy to combine digital-first operations with physical showrooming for high-consideration categories.

Global Ready To Assemble Furniture Market Report Scope

A complete background analysis of the Global RTA furniture market, which includes an assessment of the National accounts, economy, and the emerging market trends by segments, significant changes in the market dynamics, and the market overview is covered in the report.

| Home Furniture | Chairs |

| Tables (side, coffee, dressing, etc.) | |

| Beds | |

| Wardrobes | |

| Sofas | |

| Dining Tables / Dining Sets | |

| Kitchen Cabinets | |

| Other Home Furniture (bathroom, outdoor, etc.) | |

| Office Furniture | Chairs |

| Tables | |

| Storage Cabinets | |

| Desks | |

| Sofas & Other Soft Seating | |

| Other Office Furniture | |

| Hospitality Furniture | |

| Educational Furniture | |

| Healthcare Furniture | |

| Other Applications (public places, retail malls, government offices, etc.) |

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

| Economy |

| Mid-Range |

| Premium |

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Project |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Application | Home Furniture | Chairs |

| Tables (side, coffee, dressing, etc.) | ||

| Beds | ||

| Wardrobes | ||

| Sofas | ||

| Dining Tables / Dining Sets | ||

| Kitchen Cabinets | ||

| Other Home Furniture (bathroom, outdoor, etc.) | ||

| Office Furniture | Chairs | |

| Tables | ||

| Storage Cabinets | ||

| Desks | ||

| Sofas & Other Soft Seating | ||

| Other Office Furniture | ||

| Hospitality Furniture | ||

| Educational Furniture | ||

| Healthcare Furniture | ||

| Other Applications (public places, retail malls, government offices, etc.) | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By Price Range | Economy | |

| Mid-Range | ||

| Premium | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Project | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the size and growth outlook for the RTA furniture market from 2026 to 2031?

The RTA furniture market size is USD 17.58 billion in 2026 and is forecast to reach USD 25.24 billion by 2031 at a 7.36% CAGR, driven by compact living trends, online retail expansion, and design-for-repair alignment.

Which segment leads demand within the RTA furniture market today?

Home furniture leads with 62.65% of 2025 market share, reflecting stable demand for bedrooms, kitchens, and storage that anchor first-time purchases and refresh cycles.

Which region will grow the fastest in the RTA furniture market through 2031?

Asia-Pacific is the fastest-growing region, with a 6.93% CAGR through 2031, supported by urbanization, rising incomes, and capacity expansions that are elevating both supply and demand.

What materials and price tiers are shaping the trajectory of the RTA furniture market?

Wood-based panels held a 47.62% share in 2025, while plastics and polymers posted the fastest growth at 6.63%; mid-range products held a 45% share and are forecast to grow at a 6.71% CAGR.

How is channel strategy evolving across the RTA furniture market?

B2C/Retail accounted for 58% in 2025, and online retail is the fastest-growing, with an 8.17% CAGR through 2031; select large-format showrooms are being added to support higher-consideration purchases while keeping digital at the core.

What competitive moves stand out in the RTA furniture market since 2024?

IKEA’s Stockholm 2025 tool-free collection highlights assembly innovation, Sauder launched a B2B components unit, Dorel consolidated to an import-focused model, and Wayfair expanded into large-format stores to reinforce omnichannel reach.