North America RTA Furniture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

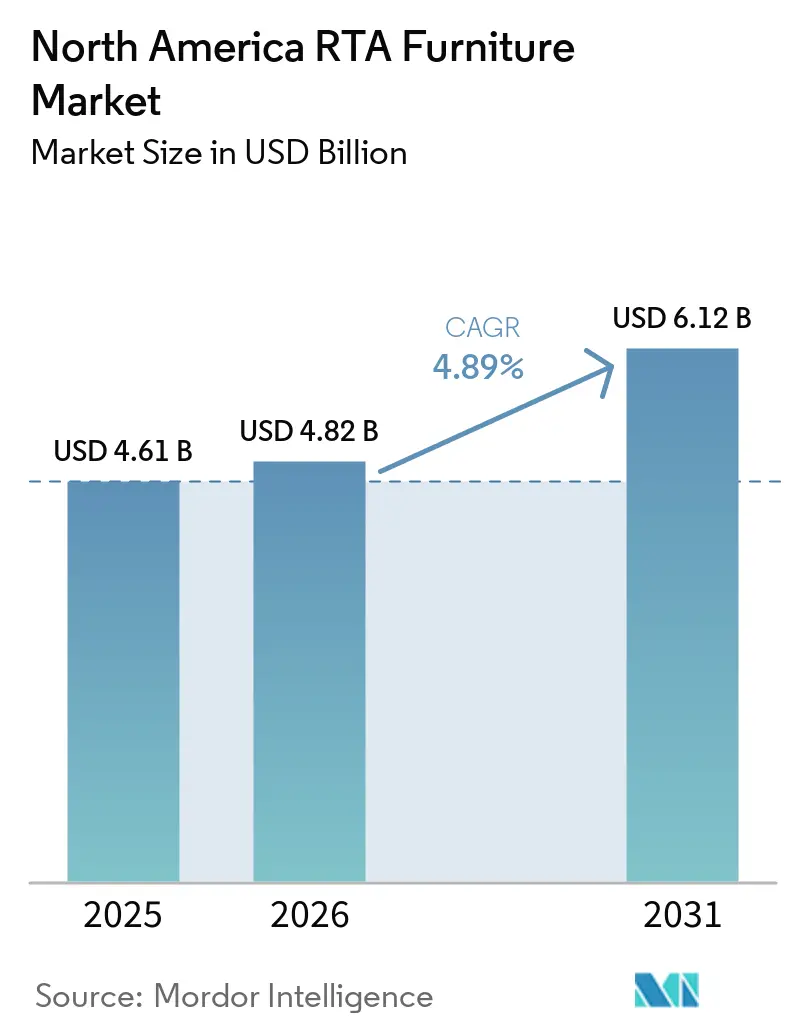

| Base Year Market Size (2025) | USD 4.61 Billion |

| Market Size (2026) | USD 4.82 Billion |

| Market Size (2031) | USD 6.12 Billion |

| Growth Rate (2025 - 2030) | 4.89% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America RTA Furniture Market Analysis by Mordor Intelligence

The North America RTA furniture market size is projected to expand from USD 4.61 billion in 2025 and USD 4.82 billion in 2026 to USD 6.12 billion by 2031, registering a CAGR of 4.89% between 2026 and 2031. E-commerce scale continues to shape the North America RTA furniture market as consumers adopt click-and-collect and faster ship-to-home options that reduce delivery windows and lift conversion rates in major metros. Online penetration in the United States retail market rose through 2025, supporting flat-pack adoption across large parcel categories that benefit from standardized packaging and lower last-mile costs. Nonstore retailer gains also show that digital channels can outgrow store-based peers during adverse weather or short-lived demand shocks, reinforcing the value of omnichannel readiness for the North America RTA furniture market. At the same time, compliance with the STURDY Act and formaldehyde emission limits requires engineering investment, supplier alignment, and third-party testing, which elevates barriers to entry and rewards well-capitalized brands. Price adjustments in 2025 by major brands helped defend volume in core categories, while material innovation and tool-free assembly systems now reduce assembly friction and returns in the North America RTA furniture market.

Key Report Takeaways

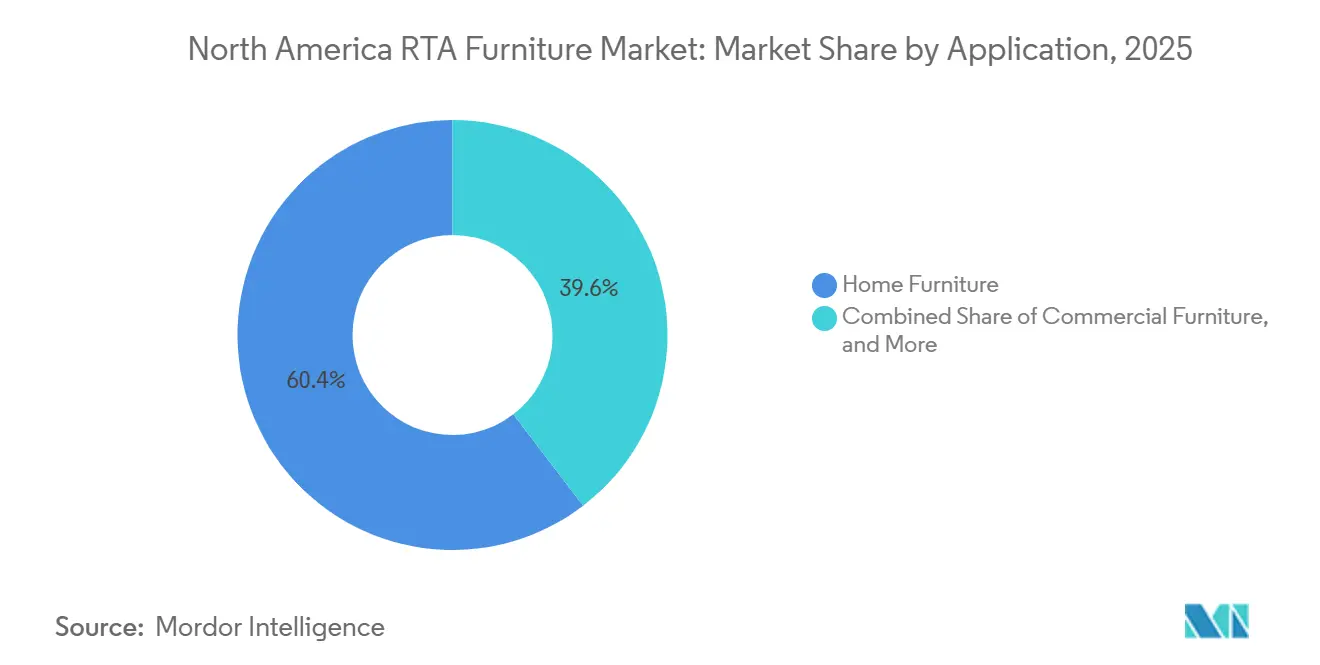

- By application, home furniture led with 60.41% of the North America RTA furniture market share in 2025, whereas office and commercial furniture is projected to expand at 5.34% CAGR between 2026 and 2031.

- By material, wood-based products held 45.92% of the North America RTA furniture market share in 2025, whereas plastic and polymer are forecast to grow at 5.83% CAGR through 2031.

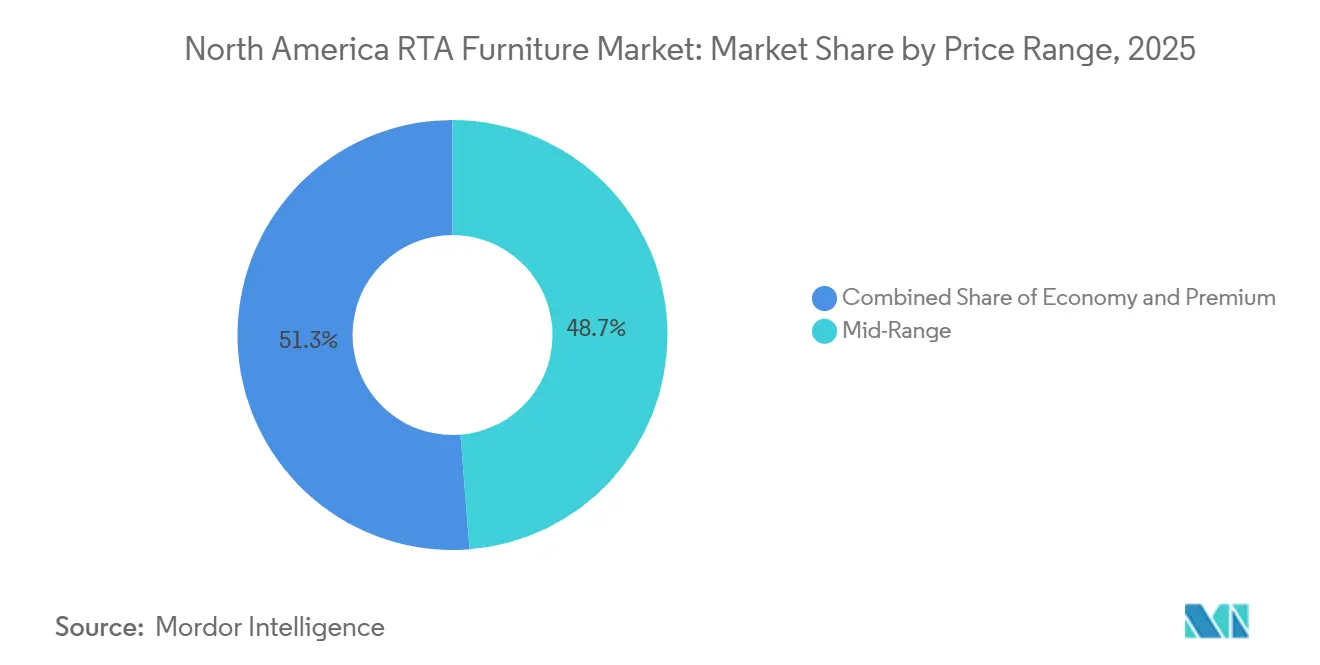

- By price range, mid-range captured 48.74% of the North America RTA furniture market share in 2025, whereas mid-range is expected to grow at 5.74% CAGR over 2026 to 2031.

- By distribution channel, business-to-consumer retail accounted for 60.12% of the North America RTA furniture market share in 2025, whereas online retail is set to expand at 6.42% CAGR to 2031.

- By geography, the United States contributed 84.82% of the North America RTA furniture market share in 2025, whereas Mexico is projected to increase at 5.91% CAGR during 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with North america representing one of the more structurally developed among them. The global report on ready to assemble furniture market by Mordor Intelligence reflects how these regional layers combine into a single system.

North America RTA Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce scale and omnichannel acceleration in furniture | +1.2% | Global, strongest in US metropolitan clusters | Medium term (2-4 years) |

| Urban densification, smaller living spaces, and mobility fueling modular, space-saving designs | +0.9% | North America core, spill-over to suburban multifamily | Long term (≥ 4 years) |

| Cost-to-value advantage and logistics savings of flat-pack formats | +0.8% | National, with early gains in mid-Atlantic, Great Lakes, Pacific Northwest | Short term (≤ 2 years) |

| Sustainability preferences favoring certified wood and design-for-disassembly | +0.6% | US coastal regions, Canadian urban markets | Medium term (2-4 years) |

| Tool-free click assembly systems and standardized hardware lowering assembly friction and returns | +0.5% | Global, with adoption led by e-commerce channels | Short term (≤ 2 years) |

| Retailers' private-label RTA expansion in home centers and mass merchants lifting shelf space | +0.7% | United States, extending to Canadian big-box | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce Scale and Omnichannel Acceleration in Furniture

United States e-commerce share increased in full-year 2025, reinforcing the channel shift that benefits flat-pack models sized for parcel networks and streamlined warehouse operations, and this momentum supports the North America RTA furniture market as consumers coordinate in-store trials with online fulfillment. Nonstore retailers posted year-over-year growth in early 2026, indicating durable digital demand even when discretionary categories show pockets of volatility in stores, which underpins ongoing investment in fulfillment hubs and click-and-collect programs. IKEA recorded 4.6 billion website visits in fiscal 2024, up 21% from the prior year, alongside 899 million store visits, an outcome consistent with a hybrid journey that moves from online research to in-store verification to scheduled delivery in the North America RTA furniture market. Inter IKEA also reduced average wholesale prices by 10% in fiscal 2024, which helped lift volumes in the second half despite revenue headwinds, showing price elasticity in large-parcel home categories[1]Inter IKEA Group, “Inter IKEA Group Financial Summary FY24,” Inter IKEA Group, inter.ikea.com. For multi-brand suppliers, liquidity constraints and tariff uncertainty weighed on e-commerce execution in 2025, while omnichannel partners increased their mix due to store-enabled returns and local delivery options that reduce last-mile costs in the North America RTA furniture market. These demand patterns favor integrated retailers that can flex inventory across physical and digital shelves while keeping reverse logistics in check.

Urban Densification, Smaller Living Spaces, and Mobility Fueling Modular, Space-Saving Designs

Smaller units in high-density markets and elevated residential mobility are reshaping product requirements toward modular systems that disassemble without damage and reassemble with minimal wear, a fit for the North America RTA furniture market. Office and institutional spending remained stable across 2025, measured at the industry level, with hybrid work influencing compact, adjustable solutions that double for home offices and collaborative hubs BIFMA.ORG. IKEA introduced a foldable PAX wardrobe frame tested for multiple disassembly cycles, addressing renter moves while maintaining structural integrity and finish durability. SONGMICS HOME launched its toolless K-PRO line in 2025 and demonstrated assembly time reductions for TV stands and bedside tables to about 10 minutes, which aligns well with renters and students who relocate every few years[2]PR Newswire, “SONGMICS HOME Launches New TOOLLESS Furniture Series,” PR Newswire, prnewswire.co.uk. Välinge Innovation’s Threespine click furniture technology, adopted by FORTE and rolled out in modular wardrobes, removes screws and cam locks in favor of interlocking panels, which reduces setup errors and helps manufacturers meet emerging durability and repairability expectations. In Canada, furniture retail activity in late 2025 increased on a month-over-month basis, signaling sustained urban demand for compact, efficient designs that are central to the North America RTA furniture market.

Cost-to-Value Advantage and Logistics Savings of Flat-Pack Formats

Flat-pack designs raise container and trailer utilization, which reduces per-unit freight expense and warehouse cube, and these gains underpin pricing in the North America RTA furniture market. Sauder Woodworking runs a cogeneration plant that converts wood scrap into electricity, has eliminated landfill wood waste for three decades, and supports a large-scale domestic manufacturing footprint that enables rapid replenishment and value-oriented pricing. Input costs moved in 2024 and 2025, with mixed tailwinds and headwinds: panel prices eased while global freight remained volatile, a combination that required careful assortment planning to protect gross margins[3]SEDAR+, “Dorel Annual Information Form 2024,” SEDAR+, sedarplus.ca. One supplier consolidated manufacturing and restructured its home segment, including facility changes and SKU rationalization, to refocus on faster-moving, higher-margin imported items while maintaining service for core retail partners. Freight dislocations and near-term tariff adjustments also required temporary pricing actions and tighter working capital, which favored operators with scale inventory programs and diversified port-of-entry coverage in the North America RTA furniture market. As upstream costs moderate and logistics networks normalize, flat-pack’s inherent cube efficiency should continue to offer a structural cost edge.

Sustainability Preferences Favoring Certified Wood and Design-for-Disassembly

Growing awareness about responsible forest sourcing and circular design is influencing material choices in the North America RTA furniture market. FSC reported more than 159 million hectares under forest management certification and tens of thousands of chain-of-custody certificates worldwide in 2024, with strong participation from larger retailers that can pull certification through complex global supply chains[4]Forest Stewardship Council, “FSC Annual Report 2024,” Forest Stewardship Council, fsc.org. The Sustainable Furnishings Council and National Wildlife Federation’s Wood Furniture Scorecard highlighted companies with robust sourcing policies, including top performers that lean on FSC-certified inputs and transparent reporting practices. IKEA raised recycled content in particleboard to above 30% in fiscal 2024, with some suppliers at 100%, and expanded capacity for PAX wardrobes using recycled share boards, which is a lever for carbon reduction in high-volume product lines. The brand also tightened chemical policies on coatings for paper foils and laminate coverings and continued work on phasing out PFAS in cookware and bakeware by 2026, consistent with a broader substitution trend in home goods. Sauder Woodworking’s carbon reduction progress and energy scheduling improvements demonstrate how operational discipline can support decarbonization while preserving cost-to-value positioning in the North America RTA furniture market. These initiatives pair well with design-for-disassembly so customers can move, repair, or recycle products without compromising safety or performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material and freight cost volatility impacting pricing and availability | -0.9% | Global, with acute pressure on import-dependent manufacturers | Short term (≤ 2 years) |

| Durability perceptions and assembly complexity increasing returns and service costs | -0.6% | United States and Canada, concentrated in e-commerce | Medium term (2-4 years) |

| Competitive pressure from fully assembled and secondhand furniture channels | -0.5% | National, with concentrated impact in price-sensitive segments | Medium term (2-4 years) |

| Compliance costs from United States stability standards and trade duties increasing product complexity | -0.4% | United States, with ripple effects for Canada and Mexico suppliers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw Material and Freight Cost Volatility Impacting Pricing and Availability

Panel prices, resin inputs, and international freight showed uneven moves across 2024 and into 2025, challenging planners to protect margins while avoiding stockouts in the North America RTA furniture market. Company disclosures indicated easing in particleboard in 2024 with expectations for further declines in 2025, but container freight remained volatile, creating mismatches in input costs across the same bill of materials. One supplier recorded material restructuring charges in 2024 and worked through negative working capital and banking covenant pressure, which added urgency to SKU rationalization and a leaner distribution footprint. Trade policies that impose duties on certain origin categories or metals also influence landed cost and list pricing, pushing some manufacturers to adopt tariff recovery charges or pass-through adjustments. These effects tend to be most visible in commodity casework and storage where shoppers compare by size and finish rather than by brand, limiting headroom for price increases in the North America RTA furniture market. As freight networks normalize and input markets settle, flat-pack’s efficiency remains a tool to stabilize pricing while preserving value.

Durability Perceptions and Assembly Complexity Increasing Returns and Service Costs

Consumers judge ready-to-assemble products on durability and ease-of-setup, and shortfalls in either raise return rates that strain reverse logistics in the North America RTA furniture market. The STURDY Act codified stability testing and anti-tip devices for clothing storage units 27 inches or taller, increasing the engineering and component requirements for compliance and making wall anchoring and interlocks standard practice across relevant SKUs. ASTM F2057-23 details testing that simulates a 60-pound child’s weight on carpet, and it reinforces the need for counterweights, wider bases, and drawer interlocks within common designs. These features improve safety but add parts and steps, which can increase setup time or error risk if consumers skip anti-tip installations, a factor that online channels must address with clear instructions and service options. In 2025, a major supplier reported wider losses in its home segment on lower volumes and availability issues, highlighting the cost of service problems and complex transitions during restructuring programs. Tool-free systems from innovators are gaining ground to solve this pain, but large legacy assortments still use cam locks and screws that require care and time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Hybrid Workspace Reshapes Office Demand Trajectory

Office and commercial furniture is forecast to grow at 5.34% CAGR during 2026 to 2031, outpacing home furniture even though home furniture accounted for 60.41% share in 2025, and this mix shift sits at the core of the North America RTA furniture market. Hybrid work requires height-adjustable desks, ergonomic chairs, and modular storage in homes, while companies reconfigure headquarters for collaboration zones, team benches, and flexible soft seating. Industry tracking showed business and institutional sales near stable levels through 2024, supporting a durable base for workplace refresh spending that cycles alongside lease renewals and re-stacks. A leading office furniture brand recorded 2% organic growth in the Americas in fiscal 2025 and maintained a substantial backlog, suggesting project timing rather than demand disappearance, and the signal is constructive for the North America RTA furniture market. Hospitality, education, and healthcare continue to deploy RTA casegoods, storage, and seating to support seasonal refreshes and rapid expansions without complex installation trades.

In home categories, chairs, tables, beds, wardrobes, and dining sets each respond to different lifecycles and space constraints in the North America RTA furniture market. IKEA’s PAX wardrobe innovations support repeated disassembly and reassembly for renters, while SONGMICS K-PRO targets fast setup in small rooms to simplify moves and reduce damage risk. Dining and living casework lean into extendable and modular functions that fit urban apartments, and RTA kitchen storage continues to benefit from frameless construction that maximizes usable interior volume. Outdoor and bathroom segments favor moisture-resistant materials and simple assembly so owners can install without specialized tools or installers. The North America RTA furniture market benefits from this application diversity because it spreads demand across multiple rooms, use cases, and seasons.

By Material: Engineered Composites Balance Cost and Performance Amid Sustainability Push

Wood-based products held 45.92% share in 2025, spanning particleboard, MDF, hardwood plywood, and solid wood, while plastics and polymers are projected to rise at 5.83% CAGR through 2031 as brands meet moisture resistance and weight targets in the North America RTA furniture market. Metals remain vital for structure and motion hardware, with program-level innovations to reduce steel quantity and emissions intensity while maintaining load performance in drawers and beds. Recycled content share in particleboard reached above 30% for a large retailer in fiscal 2024, with select suppliers at 100%, and plants expanded output for high-volume wardrobe systems that carry recycled inputs. MDF and other composite panels must meet TSCA Title VI and CARB Phase 2 emission limits with third-party certification and ongoing quality control, aligning compliance programs with daily production in the North America RTA furniture market.

On the plastics side, polypropylene and HDPE enable thin-wall parts, stackability, and weatherproofing with fewer secondary finishing steps, which lowers unit cost at scale and broadens color availability. SONGMICS reported a one-third reduction in production resources by eliminating plastic-wrapped metal parts in its toolless system, a change that cuts waste and simplifies packing and picking. Wood remains preferred in living, dining, and bedroom for warmth and texture, but engineered veneers over composite cores provide a cost-to-value alternative that travels and assembles well. Sauder Woodworking’s co-generation system and landfill-free wood waste record show how panel-intensive programs can decarbonize operations while protecting throughput in the North America RTA furniture market. FSC certification growth and scorecard recognition continue to raise expectations for traceability, even though a minority of evaluated brands reached top tiers, which leaves room for improvement as demand shifts toward verified sources.

By Price Range: Mid-Tier Captures Value-Conscious Upgraders Amid Bifurcated Demand

Mid-range pricing held 48.74% share in 2025 and is expected to grow at 5.74% CAGR through 2031, signaling a strong pull from value-conscious households that want durability without premium price points in the North America RTA furniture market. The mid-tier avoids the trade-offs of ultra-budget boards that may warp after one move while remaining more accessible than solid-hardwood builds with long lead times. Inter IKEA’s 10% average wholesale price reduction in fiscal 2024 lifted volume in the second half, supporting the idea that timely price actions can unlock demand even in categories where purchases are deferrable. At the economy end, simplifications reduce cost but can show in fit-and-finish under everyday loads, while the premium tier justifies pricing with solid woods, soft-close hardware, and strong joinery.

Brand strategies in the North America RTA furniture market reflect this spread. A large multi-category supplier is focusing on imported items with higher margins and a tighter brand and SKU set, a move that supports pricing and clarity for retail partners. Zinus continued to highlight innovations recognized by third-party editorial awards for cooling and hybrid constructions, which helps the brand communicate value to shoppers sensitive to comfort and temperature. Private-label development at big-box and specialty retailers also allows tailored features at mid-tier price points that balance cost, durability, and assembly speed. The North America RTA furniture market shows that shoppers will pay a modest premium for tool-free assembly, thicker panels, and better hardware, especially when backed by strong delivery and service options. As mid-tier share expands, brands that deliver verifiable quality and simpler setup should keep gaining.

By Distribution Channel: Digital Infrastructure Reshapes Last-Mile Economics

Business-to-consumer retail accounted for 60.12% share in 2025, and online retail is forecast to grow at 6.42% CAGR, underscoring that click-and-collect and configurators are changing buyer behavior in the North America RTA furniture market. Home centers dedicate significant floor space to storage and organization solutions, while specialty retailers pair curated assortments with delivery and assembly services that remove setup barriers for time-poor customers. IKEA opened 56 new sales locations in fiscal 2024, including smaller urban formats and Plan and Order points, which tighten the loop between online planning and in-person consultation for complex casework. Digital share of total United States retail sales increased through 2025, and fourth-quarter e-commerce sales grew year over year, confirming ongoing channel shift toward faster delivery and in-cart assembly add-ons that lift average order values in the North America RTA furniture market.

Multi-brand suppliers with constrained liquidity reported declines in e-commerce in mid-2025 due to supply constraints and tariff dynamics, while integrated retailers expanded their omnichannel mix by leveraging stores as fulfillment and return hubs. As B2B and project channels pursue predictable lead times and compliance documentation at scale, the online channel continues to grow faster for DIY-ready home office, bedroom, and storage products. Large format mass merchants continue to widen aisle-level options for ready-to-assemble mattresses and casework, which supports more frequent replenishment of high-turnover SKUs. The North America RTA furniture market therefore relies on distribution agility, blending floor presence for tactile proof with digital tools to plan, buy, and schedule delivery and assembly.

Geography Analysis

The United States accounted for 84.82% of North America revenue in 2025, supported by a large manufacturing and distribution footprint and the retail reach of home centers and mass merchants that dedicate expansive space to RTA storage and casework, which drives the North America RTA furniture market. A leading office manufacturer reported 22 key sites supporting production and distribution in the region, while federal safety enforcement and emission rules shape product design in mass bedroom and storage categories. Census data show manufacturers’ shipments of furniture and related products increased in the fourth quarter of 2025 year over year, but after-tax profits declined, which signals margin pressure from inputs and compliance costs.

Canada is forecast to grow at a moderate pace as manufacturing and retail activity sustain demand in urban centers, which supports ongoing participation in the North America RTA furniture market. Statistics Canada reported furniture manufacturing shipments increased year over year in January 2026 on a seasonally adjusted basis, against a broader decline in total manufacturing sales that month. Retail data in late 2025 indicated month-over-month and year-over-year gains in furniture sales, which align with resilient urban household spending in Toronto, Vancouver, and Montreal. Retail commodity sales for home-adjacent categories, including furniture and housewares, also rose year over year in the third quarter of 2025, indicating steady consumer activity despite macro uncertainty. On the supply side, one multinational restructured and closed its Cornwall, Ontario RTA plant in 2025, consolidating manufacturing and back-office operations while targeting earnings improvement in 2026, which reflects a shift toward leaner footprints in the North America RTA furniture market.

Mexico is the fastest growing market at a projected 5.91% CAGR, buoyed by rising household consumption of furniture and household articles and a strong manufacturing base, which together strengthen the North America RTA furniture market. National accounts showed a real increase in 2024 furniture-related household consumption and robust manufacturing value added, indicating healthier fundamentals for domestic demand and export capacity. On the commercial side, BIFMA’s tracking of Mexico’s business and institutional furniture segment shows steady levels through 2024, reflecting corporate and education procurement that supports a base of local makers and suppliers.

Competitive Landscape

For incumbent companies to maintain and expand their market share, a multi-faceted approach combining product innovation, digital transformation, and sustainable practices is essential. Market leaders must focus on developing smart ready-to-assemble furniture solutions, implementing advanced manufacturing technologies, and creating seamless omnichannel experiences. The ability to offer customization options while maintaining cost efficiency through automated production processes has become crucial. Companies must also strengthen their last-mile delivery capabilities and after-sales services to enhance customer satisfaction and build brand loyalty.

Emerging players can gain ground by focusing on niche market segments and leveraging digital platforms to reach customers directly. Success in this market requires addressing the growing demand for sustainable products, offering innovative assembly solutions, and providing superior customer service. The industry faces moderate substitution risk from traditional furniture, making it crucial for companies to emphasize the convenience and value proposition of RTA furniture. While regulatory requirements around product safety and environmental standards continue to evolve, companies that proactively adapt their processes and materials to meet these standards will gain competitive advantages.

North America RTA Furniture Industry Leaders

Sauder Woodworking Co.

Dorel Industries (Dorel Home)

IKEA

Bestar (eSolutions Furniture)

South Shore Furniture

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The United States Environmental Protection Agency proposed updates to its Formaldehyde Emission Standards for Composite Wood Products, adding ISO 12460-2:2024 as a new quality control method and aligning several voluntary standards to current editions.

- October 2025: Twin Star Home, a ZCG portfolio company, acquired Walker Edison through a court-supervised auction, integrating Walker Edison’s e-commerce platform and design pipeline with Twin Star’s infrastructure and licensed brands including duraflame, John Deere, and Craftsman

- October 2025: Välinge Innovation reported further adoption of Threespine click furniture technology in Japan, including expanded collaboration with Nitori, signaling continued growth in Asian markets

- June 2025: Dorel ceased manufacturing at its Cornwall, Ontario RTA facility and accelerated a restructuring program to streamline operations and refocus its product line.

North America RTA Furniture Market Report Scope

RTA (ready-to-assemble) furniture comprises furniture retailed in a flat-pack, unassembled state. Each piece comes complete with essential hardware, assembly instructions, and, occasionally, the requisite tools. The design ethos behind RTA furniture is to enable straightforward assembly at home, eliminating the necessity for specialized expertise or professional intervention.

By product type, the market is segmented into residential and commercial. By residential, the market is segmented into tables, chairs and sofas, storage units/cabinets, beds, and other residential products, and by commercial, the market is segmented into workstations, chairs, and other commercial products. By material type, the market is segmented into wood furniture, metal furniture, plastic furniture, and other material furniture. By distribution channel, the market is segmented into B2B/directly from the manufacturers, B2C/retail channels, and other distribution channels. By B2C/retail channels, the market is segmented into home centers, specialty stores, and online. By country, the market is segmented into the United States, Canada, and Mexico. The report offers the market size in value terms in USD for all the abovementioned segments.

| Home Furniture | Chairs |

| Tables (side, coffee, dressing, etc.) | |

| Beds | |

| Wardrobes | |

| Sofas | |

| Dining Tables / Dining Sets | |

| Kitchen Cabinets | |

| Other Home Furniture (bathroom, outdoor, etc.) | |

| Office Furniture | Chairs |

| Tables | |

| Storage Cabinets | |

| Desks | |

| Sofas & Other Soft Seating | |

| Other Office Furniture | |

| Hospitality Furniture | |

| Educational Furniture | |

| Healthcare Furniture | |

| Other Applications (public places, retail malls, government offices, etc.) |

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

| Economy |

| Mid-Range |

| Premium |

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Project |

| United States |

| Canada |

| Mexico |

| By Application | Home Furniture | Chairs |

| Tables (side, coffee, dressing, etc.) | ||

| Beds | ||

| Wardrobes | ||

| Sofas | ||

| Dining Tables / Dining Sets | ||

| Kitchen Cabinets | ||

| Other Home Furniture (bathroom, outdoor, etc.) | ||

| Office Furniture | Chairs | |

| Tables | ||

| Storage Cabinets | ||

| Desks | ||

| Sofas & Other Soft Seating | ||

| Other Office Furniture | ||

| Hospitality Furniture | ||

| Educational Furniture | ||

| Healthcare Furniture | ||

| Other Applications (public places, retail malls, government offices, etc.) | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By Price Range | Economy | |

| Mid-Range | ||

| Premium | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Project | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the current size and expected growth for the North America RTA furniture market?

The North America RTA furniture market size is projected to expand from USD 4.61 billion in 2025 and USD 4.82 billion in 2026 to USD 6.12 billion by 2031, registering a 4.89% CAGR between 2026 and 2031.

Which application segments are leading and growing fastest in the North America RTA furniture market?

Home furniture held 60.41% share in 2025, while office and commercial furniture is forecast to grow at 5.34% CAGR between 2026 and 2031.

What materials are driving performance improvements in the North America RTA furniture market?

Wood-based products led with 45.92% share in 2025, and plastic and polymer materials are expected to grow at 5.83% CAGR due to moisture resistance and weight advantages.

How are regulations shaping product design in the North America RTA furniture market?

Stability requirements under the STURDY Act and formaldehyde emission limits under TSCA Title VI and CARB Phase 2 necessitate interlocks, anti-tip devices, and certified low-emission panels, increasing engineering rigor and testing.

Which price tier is expanding fastest in the North America RTA furniture market?

The mid-range captured 48.74% share in 2025 and is expected to grow at 5.74% CAGR through 2031, supported by value seeking consumers who want durability and simple assembly.

What distribution channels are most important in the North America RTA furniture market?

B2C held 60.12% share in 2025, and online retail is projected to grow at 6.42% CAGR, powered by click-and-collect, configurators, and faster delivery that improve conversion.

Page last updated on: