Cardiovascular Drugs Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

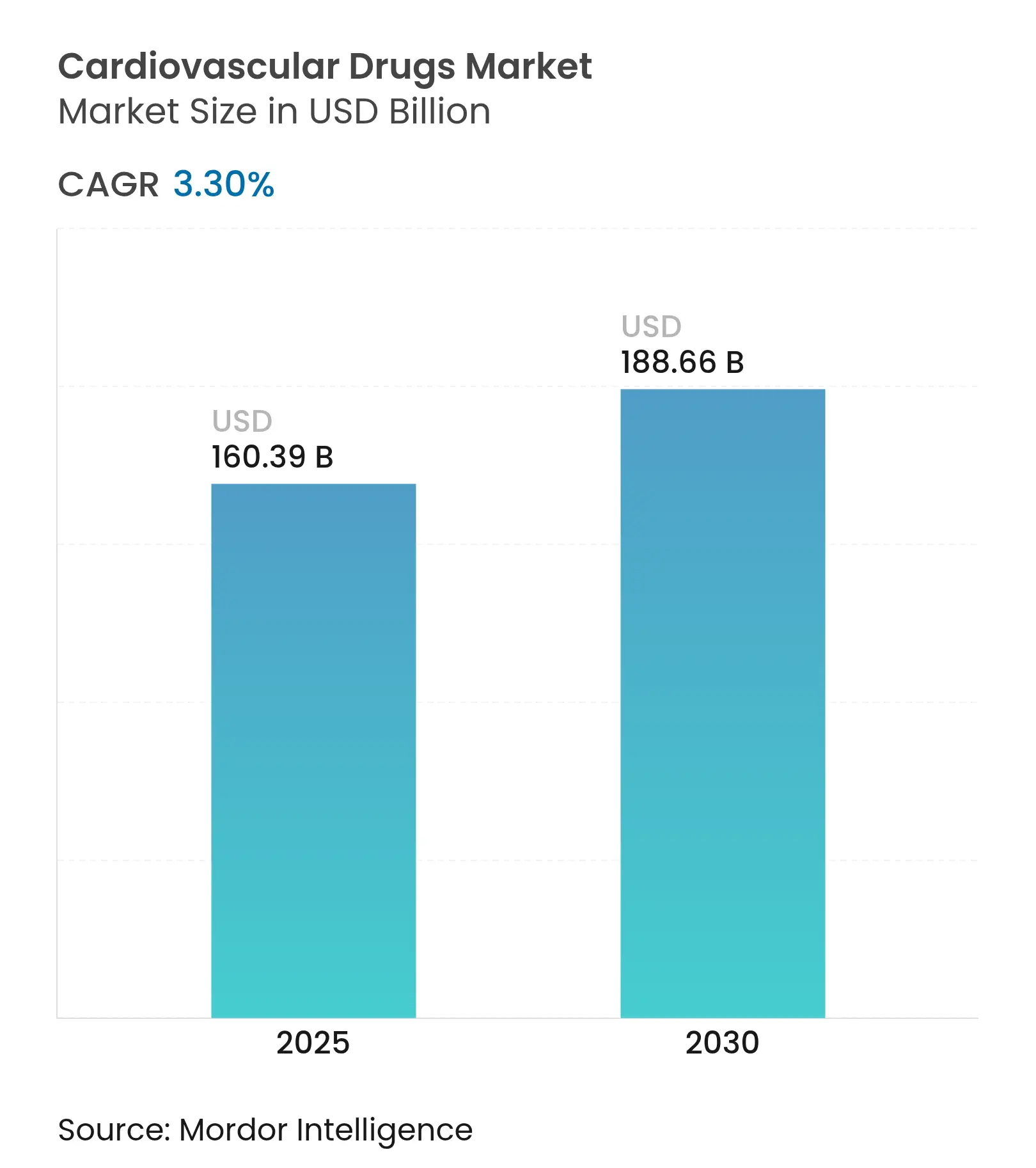

| Market Size (2025) | USD 160.39 Billion |

| Market Size (2030) | USD 188.66 Billion |

| Growth Rate (2025 - 2030) | 3.30 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

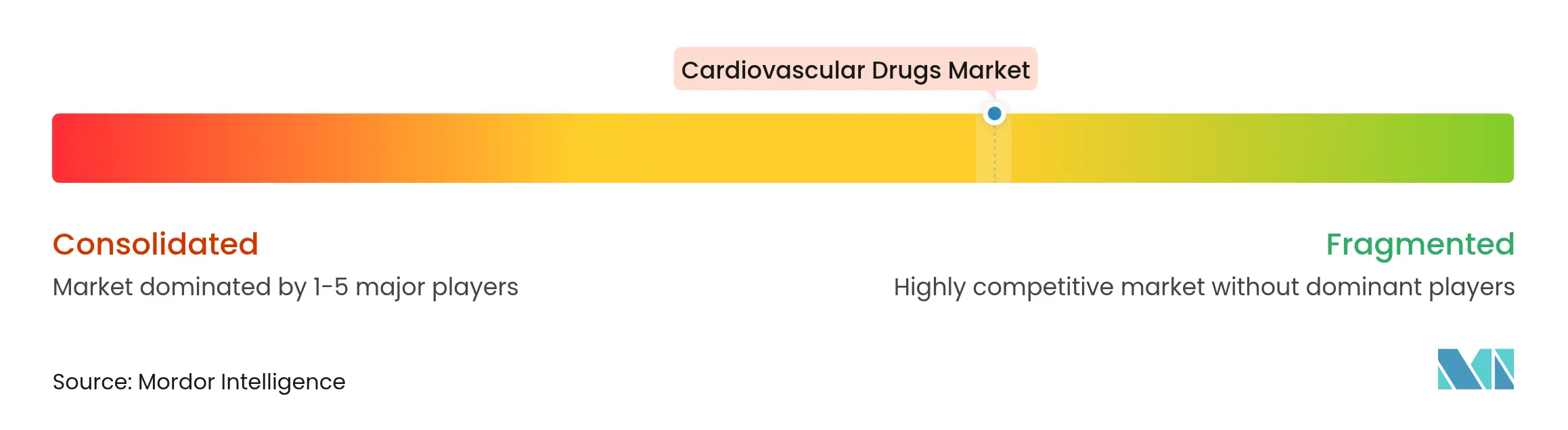

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Cardiovascular Drugs Market Analysis by Mordor Intelligence

Steady top-line growth conceals deep changes shaped by population ageing, accelerated innovation cycles, and policy shifts that reward real-world evidence over traditional trial endpoints. Demand remains dominated by anticoagulants; yet factor XI inhibitors, mineralocorticoid receptor antagonists, and GLP-1 receptor agonists are redefining therapeutic boundaries. Digital distribution, supply-chain localisation, and AI-enabled discovery tools are widening competitive gaps between data-driven multinationals and smaller firms. At the same time, mounting patent-expiration risks and single-region API dependence temper near-term optimism, obliging manufacturers to balance lifecycle-management investments with next-generation pipeline bets.

Key Report Takeaways

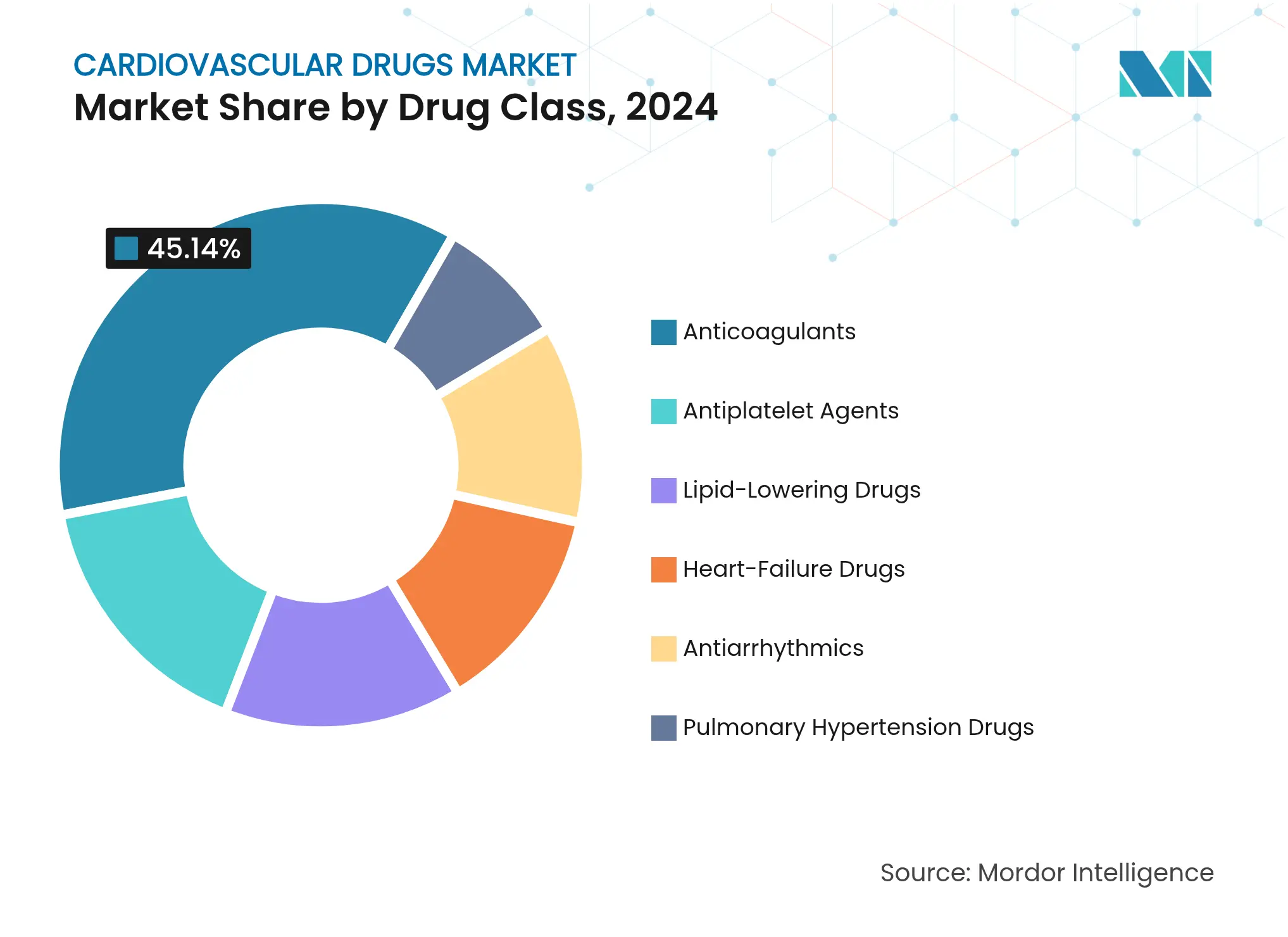

- By drug class: Anticoagulants led with 45.14% cardiovascular drugs market share in 2024, while heart-failure drugs are set to grow fastest at a 3.70% CAGR through 2030.

- By disease indication: Hypertension therapies held 28.90% of the cardiovascular drugs market size in 2024; heart-failure treatments are advancing at a 4.01% CAGR to 2030.

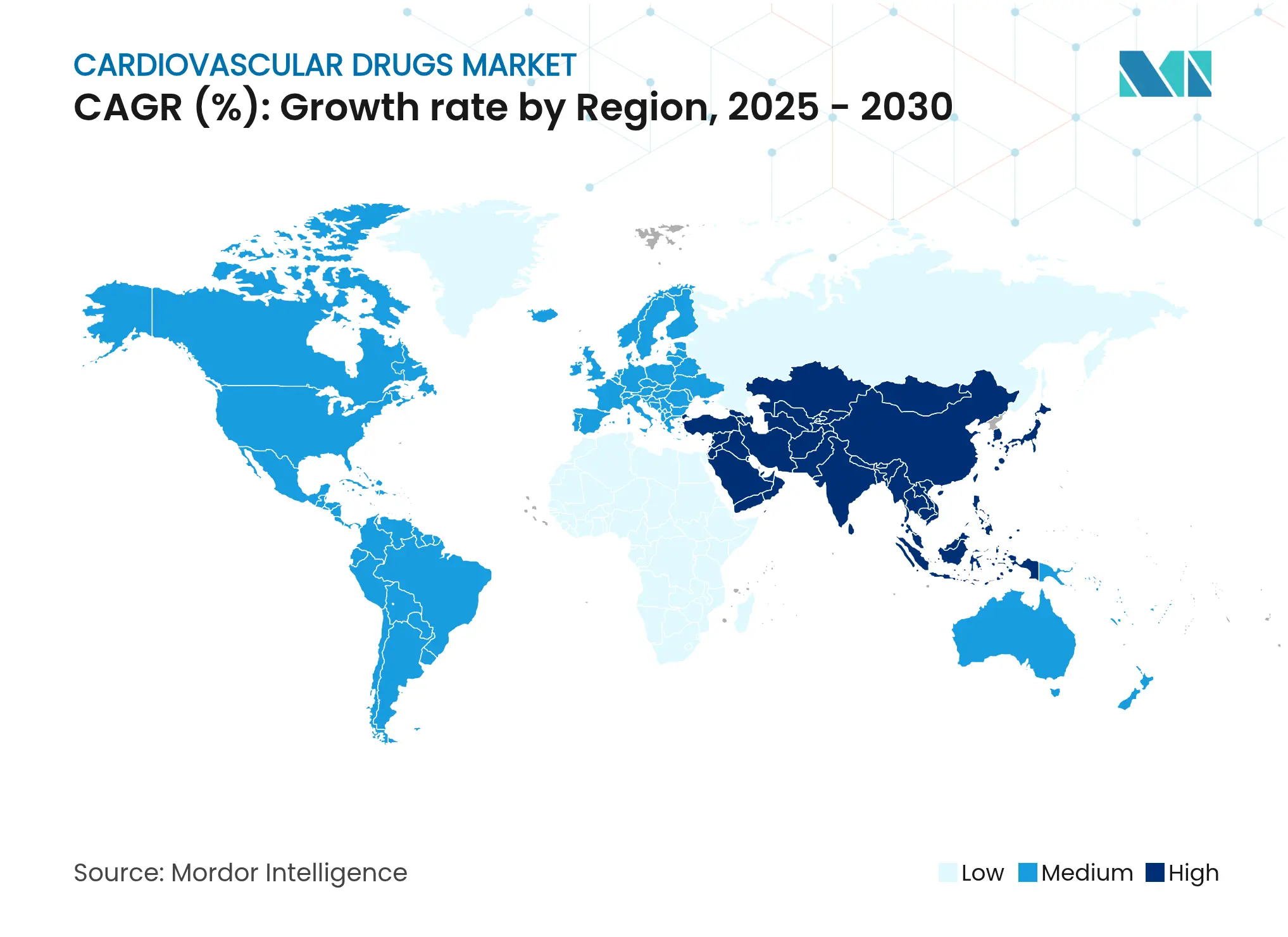

- By geography: Asia-Pacific captured 34.35% share of the cardiovascular drugs market in 2024 and is forecast to post the highest 5.25% CAGR through 2030.

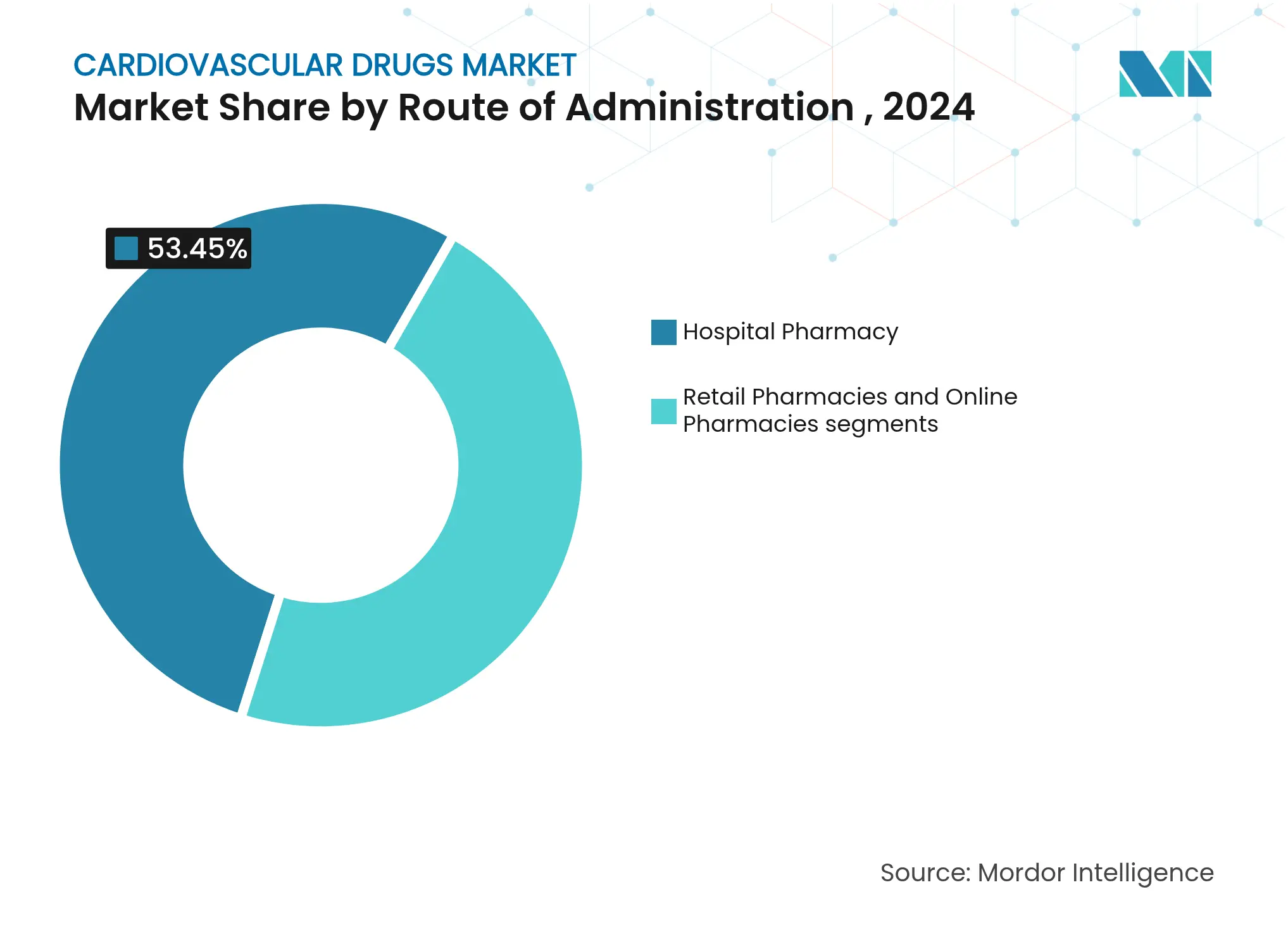

- By distribution channel: Hospital pharmacies accounted for 53.45% share of the cardiovascular drugs market size in 2024; online pharmacies are expanding at a 4.67% CAGR on the back of telehealth adoption

Global Cardiovascular Drugs Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Age-related rise in CVD prevalence Age-related rise in CVD prevalence | +0.80% | North America; Europe; Asia-Pacific | Long term (≥ 4 years) | (~) % Impact on

CAGR Forecast:+0.80% | Geographic Relevance:North America; Europe; Asia-Pacific | Impact Timeline:Long term (≥ 4 years) |

Rapid uptake of NOACs and SGLT2 inhibitors Rapid uptake of NOACs and SGLT2 inhibitors | +0.60% | Global, led by developed markets | Medium term (2–4 years) | |||

Expanding reimbursement in emerging regions Expanding reimbursement in emerging regions | +0.40% | Asia-Pacific; Latin America; MEA | Medium term (2–4 years) | |||

Regulatory reliance on real-world evidence Regulatory reliance on real-world evidence | +0.30% | North America; EU | Short term (≤ 2 years) | |||

AI-driven in-silico repurposing AI-driven in-silico repurposing | +0.20% | Global innovation hubs | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence of CVDs in Ageing Populations

Heart-failure cases are projected to reach 8.5 million Americans by 2030, up from 6.7 million in 2025. Older patients often present with multiple comorbidities, driving uptake of combination regimens and personalised dosing strategies. Asia-Pacific mirrors this demographic trend, reinforcing chronic-disease management demand. Payers in developed markets already reimburse advanced agents for complex cases, implying durable volume growth across the cardiovascular drugs market.

Rapid Uptake of NOACs & SGLT2 Inhibitors

Novel oral anticoagulants continue to displace warfarin, while SGLT2 inhibitors move beyond diabetes care into heart-failure management, evidenced by finerenone’s 16% event-reduction in FINEARTS-HF[2]Source: Bayer AG, “Pharma Growth Strategy,” bayer.com . GLP-1 agonists such as semaglutide secured FDA approval for cardiovascular death-risk reduction, underscoring the convergence of metabolic and cardiovascular treatment pathways. This therapeutic overlap opens new addressable niches within the cardiovascular drugs market

Regulatory Reliance on Real-World Data for Label Expansions

The FDA’s final guidance on electronic-registry use allows cardiovascular label extensions without dedicated randomised trials, provided datasets meet quality thresholds [1]Source: U.S. Food and Drug Administration, “Real-World Data: Assessing Electronic Health Records and Medical Claims Data,” fda.gov. Firms investing in advanced data-analytics platforms can accelerate indication additions, enhancing return on existing assets within the cardiovascular drugs market.

Expanding Reimbursement in Emerging Markets

China’s National Reimbursement Drug List delivered 63% average price cuts alongside broader coverage, while India’s price reforms improved access to empagliflozin combinations npaa.gov.in. Brazil’s local-manufacturing preference margins add further impetus. Collectively, these actions unlock large untreated patient pools, amplifying volume upside for companies equipped with local-partner models.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Patent expiries & generic erosion Patent expiries & generic erosion | -0.70% | Developed markets | Short term (≤ 2 years) | (~) % Impact on

CAGR Forecast:-0.70% | Geographic Relevance:Developed markets | Impact Timeline:Short term (≤ 2 years) |

High cost of biologic & gene-based therapies High cost of biologic & gene-based therapies | -0.40% | Emerging markets | Medium term (2–4 years) | |||

Single-region API sourcing risk Single-region API sourcing risk | -0.20% | Global | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Patent Expiries & Generic Erosion of Blockbuster Brands

Lupin’s generic rivaroxaban launch may capture up to 60% share in its first year, trimming brand revenues and placing pricing pressure across the anticoagulant class within the cardiovascular drug market. Similar dynamics await Entresto and Corlanor, compelling incumbents to pursue value-based contracting and indication diversification.

High Cost of Biologic & Gene-Based CV Therapies

Acoramidis cut mortality by 42% in transthyretin cardiomyopathy trials, yet payers weigh its budget impact carefully. Tiered-pricing and outcomes-linked agreements become prerequisites for wide adoption, particularly in lower-income settings.

Segment Analysis

By Drug Class: Anticoagulants Lead Despite Generic Pressure

Anticoagulants held 45.14% cardiovascular drugs market share in 2024, underscoring their central role in thromboembolic prophylaxis across diverse indications. The cardiovascular drugs market size for anticoagulants is expected to face near-term revenue compression once additional rivaroxaban generics arrive, pushing branded players toward next-generation factor XI inhibitors. Abelacimab reduced bleeding 62–69% versus rivaroxaban, positioning the agent as a differentiated alternative. Meanwhile, heart-failure drugs’ 3.70% CAGR reflects clinician confidence in mineralocorticoid receptor antagonists and SGLT2 inhibitors for preserved-ejection-fraction patients.

Second-tier categories show diverging paths. Antihypertensives enjoy broadened guideline thresholds, supporting steady volume growth. Lipid-lowering agents experience renewed momentum thanks to oral PCSK9 candidates like MK-0616 now in Phase 3 trials. Pulmonary-hypertension drugs benefit from rare-disease incentives, while antiarrhythmics gain relevance through device-drug integration that improves adherence and monitoring.

Note: Segment shares of all individual segments available upon report purchase

By Disease Indication: Heart Failure Emerges as Growth Engine

Hypertension maintained 28.90% share of the cardiovascular drugs market size in 2024, mirroring its broad prevalence across age cohorts. Yet heart-failure therapeutics are set to expand at 4.01% CAGR, anchored by finerenone and GLP-1 agents that address previously unmet needs. The cardiovascular drugs market is expected to see GLP-1 agonists such as tirzepatide deliver meaningful outcomes in non-diabetic heart-failure patients, widening the eligible population. Coronary-artery-disease treatments adopt anti-inflammatory strategies to tackle residual risk, and dyslipidemia care evolves toward RNA-based modalities targeting lipoprotein(a).

By Route of Administration: Injectable Growth Challenges Oral Dominance

Oral products still account for 78.50% of cardiovascular drugs market revenue; however, injectables are growing at 4.25% CAGR as complex biologics require parenteral delivery. Long-acting subcutaneous devices improve adherence, and on-body injectors add convenience, thereby elevating patient acceptance. The cardiovascular drugs market share of injectables is therefore likely to rise, particularly for PCSK9 inhibitors and novel gene-silencing agents.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Transformation Accelerates Online Growth

Hospital pharmacies retained 53.45% dominance in 2024 because acute-care protocols rely on in-house dispensing. Conversely, online channels are advancing at 4.67% CAGR as prescription-management apps, teleconsultations, and AI-based adherence reminders gain traction. The cardiovascular drugs market is adopting hybrid fulfilment models, combining doorstep delivery with periodic clinical check-ins, which widens access for chronic-care patients.

Geography Analysis

Cardiovascular Drugs Market in North America

Asia-Pacific led the cardiovascular drugs market with 34.35% share in 2024, and its 5.25% CAGR outpaces all other regions thanks to China’s procurement reforms and India’s infrastructure expansion. Local firms now secure 71% of new NRDL listings, signalling stronger domestic competitive pressure for multinationals. Japan’s streamlined approval timelines further ease market entry for cutting-edge therapies, promoting steady uptake of GLP-1 agents and next-generation anticoagulants.

North America remains a pivotal innovation hub in the cardiovascular drug market, underpinned by reimbursement frameworks that quickly absorb breakthrough therapies. Nonetheless, the Inflation Reduction Act introduces price-negotiation uncertainty that may reshape launch-sequence strategies for high-value cardiovascular assets.

Europe benefits from harmonised regulatory pathways that accelerate parallel submissions, though Brexit-related logistics adjustments persist. Latin America’s policy moves toward domestic production—exemplified by Brazil’s preference margins—create dual imperatives of localisation and cost control. The Middle East and Africa record incremental gains aligned with cardiovascular-disease awareness campaigns, yet infrastructure gaps still limit high-cost biologic penetration.

Competitive Landscape

Market Concentration

The cardiovascular drugs industry features moderate consolidation as Pfizer, Bristol Myers Squibb, and Novartis leverage AI-driven discovery alliances to sustain their pipelines. Merck’s USD 200 million licensing deal for an oral lipoprotein(a) inhibitor exemplifies proactive portfolio diversification. Pfizer’s collaboration with Ultromics demonstrates how machine learning enhances patient identification for amyloidosis therapeutics.

White-space entrants target factor XI inhibition and RNA-based heart-failure therapies, evidenced by Novo Nordisk’s USD 1.1 billion acquisition of Cardior. Meanwhile, digital-health partnerships multiply as companies wrap drugs in data-enabled service models that support adherence and outcomes monitoring.

Supply-chain vulnerabilities exposed during the pandemic spur localisation initiatives and dual-sourcing contracts to mitigate single-region API dependence. Firms with diversified manufacturing footprints secure preferential procurement status in risk-averse health systems, consolidating competitive advantage in the cardiovascular drug market.

Cardiovascular Drugs Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Merck reported positive Phase 3 CORALreef LDL-C results for enlicitide decanoate, positioning the agent as a potential blockbuster cholesterol therapy.

- May 2025: Abbott gained FDA clearance for the Tendyne transcatheter mitral-valve system, enabling valve replacement without open surgery.

- March 2025: Merck licensed HRS-5346 from Jiangsu Hengrui, investing USD 200 million upfront to advance an oral lipoprotein(a) inhibitor

Table of Contents for Cardiovascular Drugs Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising prevalence of CVDs in ageing populations

- 4.2.2Rapid uptake of NOACs & SGLT2 inhibitors

- 4.2.3Expanding reimbursement in emerging markets

- 4.2.4Regulatory reliance on real-world data for label expansions

- 4.2.5AI-driven in-silico repurposing accelerating CV pipeline

- 4.3Market Restraints

- 4.3.1Patent expiries & generic erosion of blockbuster brands

- 4.3.2High cost of biologic & gene-based CV therapies

- 4.3.3Single-region API sourcing creating supply-chain risk

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Suppliers

- 4.7.3Bargaining Power of Buyers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts

- 5.1By Drug Class (Value)

- 5.1.1Antihypertensives

- 5.1.2Anticoagulants

- 5.1.3Antiplatelet Agents

- 5.1.4Lipid-Lowering Drugs

- 5.1.5Heart-Failure Drugs

- 5.1.6Antiarrhythmics

- 5.1.7Pulmonary Hypertension Drugs

- 5.2By Disease Indication (Value)

- 5.2.1Hypertension

- 5.2.2Coronary Artery Disease

- 5.2.3Heart Failure

- 5.2.4Arrhythmia

- 5.2.5Dyslipidemia

- 5.2.6Venous Thrombo-Embolism

- 5.3By Route of Administration (Value)

- 5.3.1Oral

- 5.3.2Injectable / IV

- 5.3.3Transdermal & Others

- 5.4By Distribution Channel (Value)

- 5.4.1Hospital Pharmacies

- 5.4.2Retail Pharmacies

- 5.4.3Online Pharmacies

- 5.5By Geography (Value)

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Competitive Benchmarking

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1Pfizer

- 6.4.2Bristol Myers Squibb

- 6.4.3Novartis

- 6.4.4AstraZeneca

- 6.4.5Johnson & Johnson

- 6.4.6Merck & Co.

- 6.4.7Bayer

- 6.4.8Eli Lilly

- 6.4.9Boehringer Ingelheim

- 6.4.10Sanofi

- 6.4.11AbbVie

- 6.4.12Amgen

- 6.4.13Daiichi Sankyo

- 6.4.14Novo Nordisk

- 6.4.15GSK

- 6.4.16Takeda

- 6.4.17Abbott Laboratories

- 6.4.18Roche

- 6.4.19Servier

- 6.4.20Otsuka Pharma

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Drug Class (Value)

- Antihypertensives

- Anticoagulants

- Antiplatelet Agents

- Lipid-Lowering Drugs

- Heart-Failure Drugs

- Antiarrhythmics

- Pulmonary Hypertension Drugs

- Antihypertensives

- By Disease Indication (Value)

- Hypertension

- Coronary Artery Disease

- Heart Failure

- Arrhythmia

- Dyslipidemia

- Venous Thrombo-Embolism

- Hypertension

- By Route of Administration (Value)

- Oral

- Injectable / IV

- Transdermal & Others

- Oral

- By Distribution Channel (Value)

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Hospital Pharmacies

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- China

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's Cardiovascular Drugs Baseline Commands Confidence

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 160.39 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 155.96 B (2025) | Global Consultancy A | Narrower drug-class coverage and limited field validation | ||

USD 153.70 B (2024) | Industry Research B | Excludes hospital tender sales and holds ASP constant |