Market Overview

| Study Period | 2020 - 2031 |

|---|---|

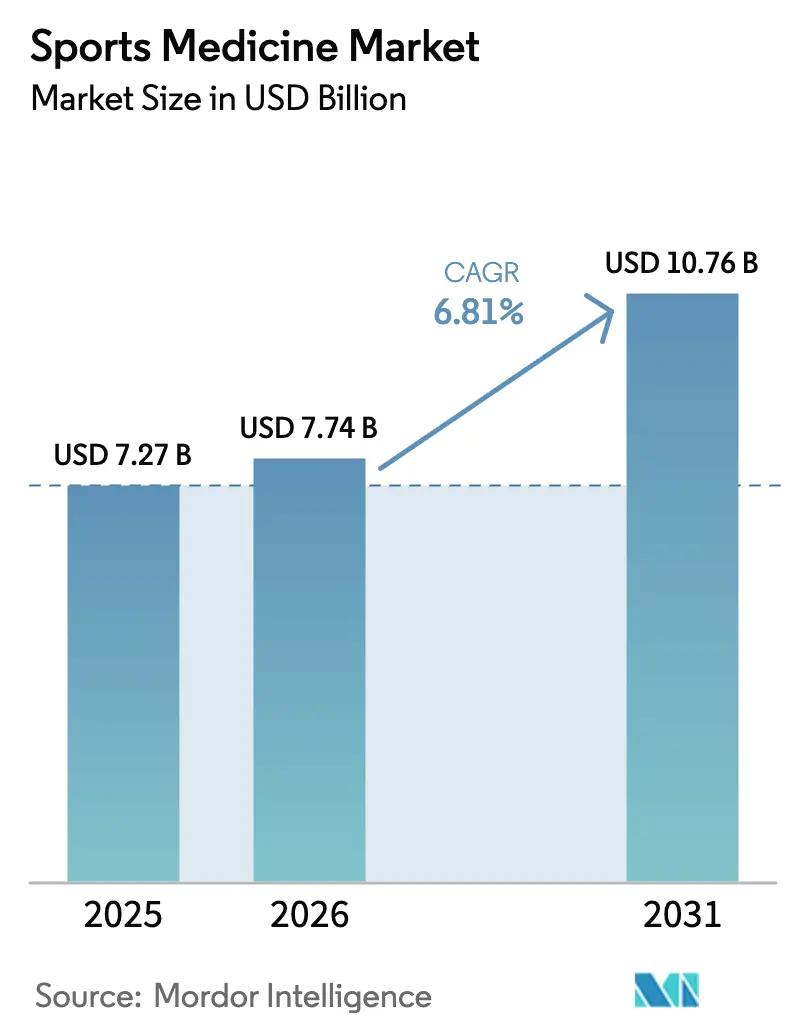

| Market Size (2026) | USD 7.74 Billion |

| Market Size (2031) | USD 10.76 Billion |

| Growth Rate (2026 - 2031) | 6.81% CAGR |

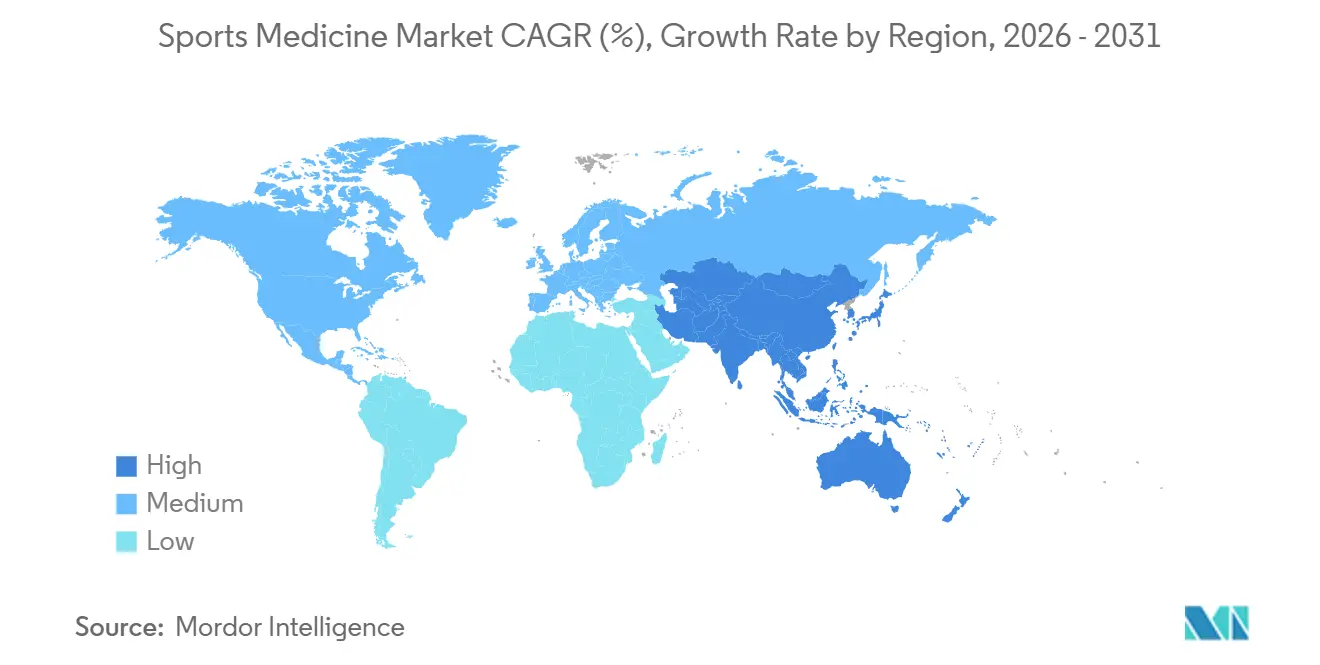

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sports Medicine Market Analysis by Mordor Intelligence

The Sports Medicine Market size is projected to be USD 7.27 billion in 2025, USD 7.74 billion in 2026, and reach USD 10.76 billion by 2031, growing at a CAGR of 6.81% from 2026 to 2031.

A persistent rise in musculoskeletal disorders, the migration of high-volume orthopedic procedures to ambulatory surgery centers, and growing acceptance of biologic regeneration platforms underpin this growth. Market expansion also benefits from private payers rewarding outpatient efficiency, professional leagues investing in predictive injury analytics, and an increased willingness among consumers to pay for minimally invasive treatments. Orthopedic majors continue to expand their portfolios through acquisitions that accelerate the time-to-market for implants, robotics, and digital rehabilitation ecosystems. Heightened regulatory scrutiny in Europe and price pressure from bundled payments in the United States temper margins; yet, unmet clinical needs and technology-driven efficiencies sustain the sector’s long-term momentum.

Key Report Takeaways

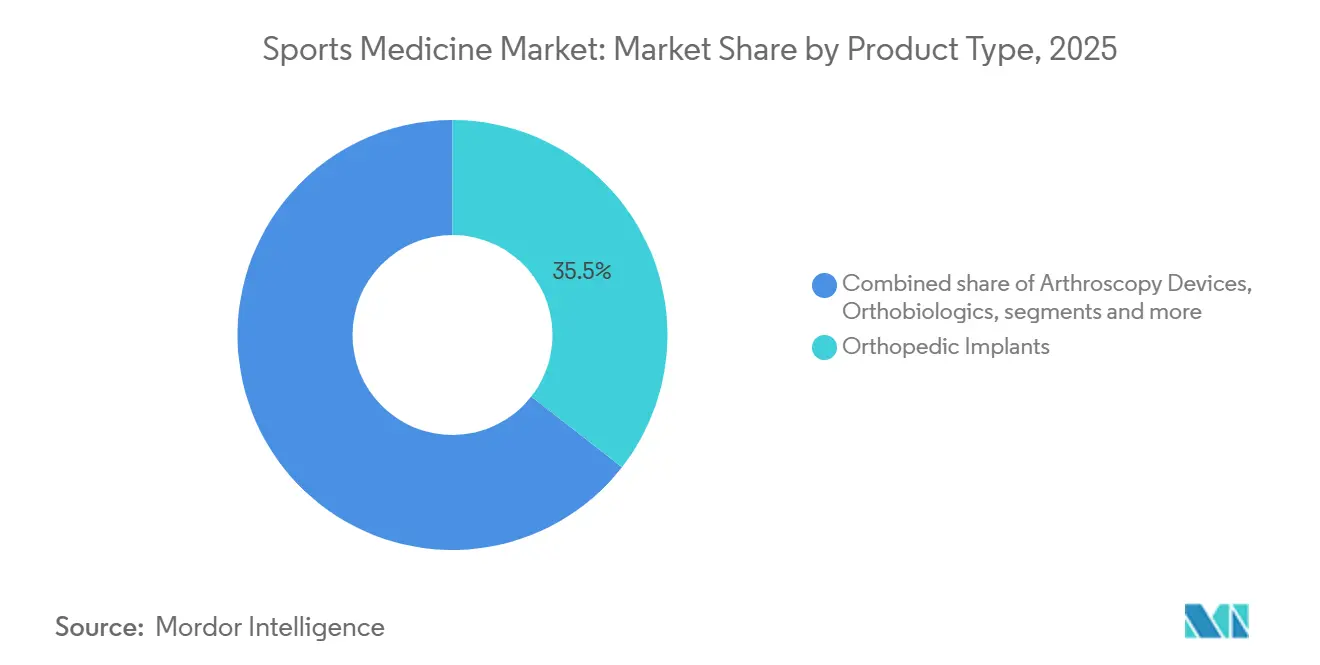

- By product type, orthopedic implants led with a 35.54% revenue share in 2025; orthobiologics are forecast to expand at an 8.54% CAGR through 2031.

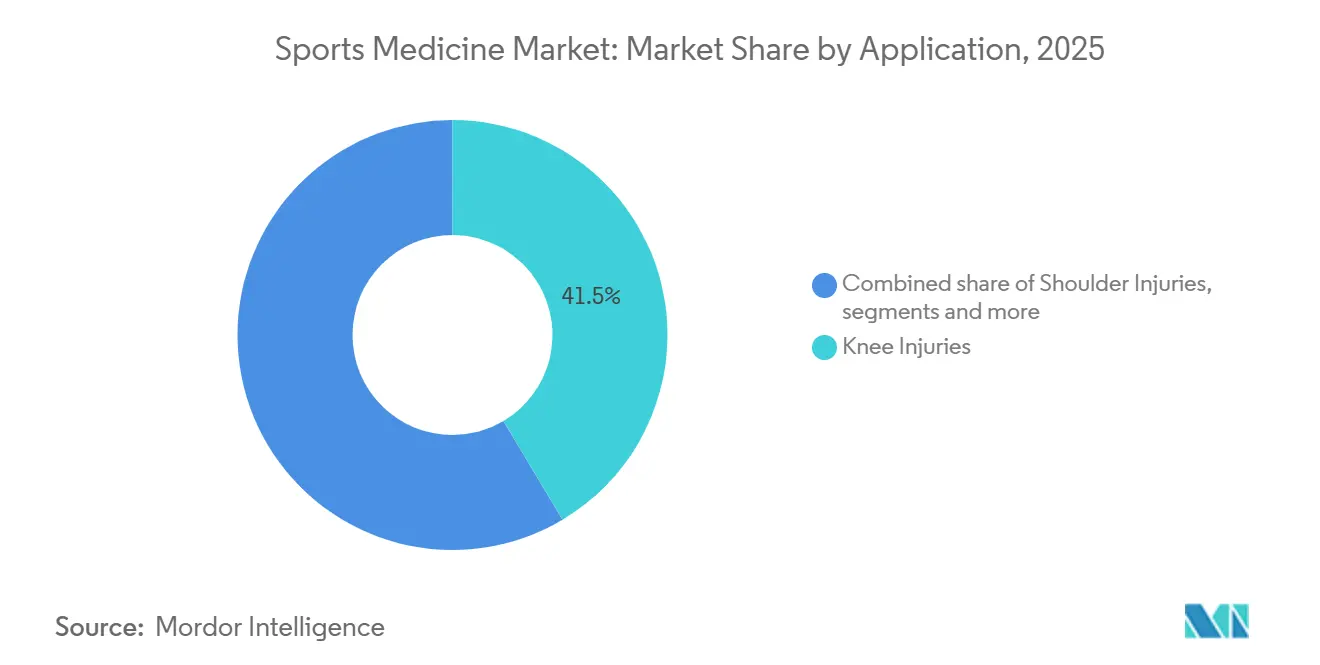

- By application, knee injuries captured 41.46% of the sports medicine market share in 2025, while foot and ankle procedures are set to grow at an 8.67% CAGR through 2031.

- By end user, hospitals accounted for 46.43% of the sports medicine market size in 2025, and ambulatory surgery centers are projected to advance at a 9.32% CAGR through 2031.

- By geography, North America led with a 40.32% revenue share in 2025; however, the Asia-Pacific region is on track for the fastest growth, with a 7.65% CAGR, closing much of the gap by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Sports Medicine Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating burden of musculoskeletal and sports-related injuries | +1.0% | Global, with acute concentration in North America and Europe due to aging demographics | Long term (≥ 4 years) |

| Shift toward minimally invasive arthroscopic procedures | +1.2% | North America, Europe, APAC urban centers with advanced surgical infrastructure | Medium term (2-4 years) |

| Advances in regenerative and biologic therapies | +1.1% | North America and Europe leading clinical adoption; APAC following with regulatory approvals | Long term (≥ 4 years) |

| Rising investments in professional leagues and fitness infrastructure | +0.7% | North America (NFL, NBA), Europe (Premier League), APAC (China, India fitness boom) | Medium term (2-4 years) |

| Ambulatory surgery center expansion accelerating outpatient procedures | +0.9% | North America dominant; emerging in Western Europe and select APAC markets | Short term (≤ 2 years) |

| AI-powered motion analysis and predictive injury prevention tools | +0.6% | North America professional sports; gradual diffusion to elite training facilities globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Burden of Musculoskeletal and Sports-Related Injuries

More than 1.71 billion people lived with musculoskeletal conditions in 2024, making it the leading cause of disability worldwide. Sports participation contributes to injury prevalence, with approximately 252,000 anterior cruciate ligament reconstructions performed annually in the United States, and female athletes facing up to an eight-fold higher risk due to biomechanical and hormonal factors[1]American Academy of Orthopaedic Surgeons, “ACL Reconstruction Statistics,” aaos.org. Chronic pain affected 24.3% of American adults in 2024, ensuring a steady flow of orthopedic consultations, imaging, and interventions. Deferred demand emerges as adolescent sports injuries often require surgical care decades later, underscoring the durable volume pipeline. Across income strata, unmet clinical needs remain high, ensuring baseline growth even when reimbursement policies fluctuate.

Shift Toward Minimally Invasive Arthroscopic Procedures

Arthroscopy now dominates soft-tissue repair because sub-centimeter incisions reduce the risk of infection, shorten recovery time, and support same-day discharge. Johnson & Johnson MedTech added real-time analytics to arthroscopic towers in 2024, converting instrument motion data into training feedback that shortens learning curves. Zimmer Biomet’s ROSA Shoulder, cleared by the FDA in 2024, cuts operative time by 15% and improves implant positioning accuracy, making reverse total shoulder arthroplasty suitable for outpatient settings. CMS increased ambulatory surgery center payments by 2.6% for 2025, closing the gap with hospital outpatient departments and incentivizing the migration of procedures. Payers endorse bundled reimbursement because arthroscopy reports low complication rates, aligning cost control with patient outcomes. The technology shift prompts manufacturers to update their product mixes to include visualization systems, single-use shavers, and sterile-packed implant kits.

Advances in Regenerative and Biologic Therapies

The FDA granted expanded pediatric indications to Miach Orthopaedics’ BEAR implant in March 2025, reinforcing confidence in biologic scaffolds that heal native ligaments rather than replace them[2]U.S. Food and Drug Administration, “BEAR Implant De Novo Classification Request,” fda.gov. Regenity Biosciences earned 510(k) clearance for its RejuvaKnee meniscal scaffold in October 2024, providing tissue ingrowth benefits for active, younger patients. Smith+Nephew’s Agili-C biphasic implant, acquired with CartiHeal in 2024, targets focal cartilage defects without metallic hardware. ClinicalTrials.gov listed more than 150 studies involving mesenchymal stem cells for knee osteoarthritis in 2025, signaling a robust pipeline. Private insurers now reimburse platelet-rich plasma for tendinopathy after conservative therapies fail, expanding eligibility beyond elite athletes. Premium pricing attached to these biologics aligns with value-based models that penalize early revisions, positioning regenerative products as cost-effective over a patient’s lifetime.

Rising Investments in Professional Leagues and Fitness Infrastructure

Professional franchises quantify injury risk as a determinant of wins and asset value. The National Football League, utilizing Amazon Web Services, introduced the Digital Athlete simulation across all 32 clubs in 2023, running millions of biomechanical scenarios to inform practice loads and equipment specifications. China’s Healthy China 2030 vision continues to finance community sports medicine clinics and youth rehabilitation centers. India’s urban millennials drive fitness club memberships, inadvertently boosting overuse injuries that funnel cases into orthopedic pathways. Corporate wellness programs in North America and Europe embed onsite physiotherapy and ergonomic audits, seamlessly converting early-stage injuries into reimbursable interventions. Investments in public and private training facilities reduce barriers to medical evaluation, thereby expanding the overall footprint of the sports medicine market.

Restraints Impact Analysis of Sports Medicine Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High costs and reimbursement uncertainty | -0.6% | Global, with acute pressure in North America due to bundled payments; Europe facing budget constraints | Short term (≤ 2 years) |

| Stringent region-specific regulatory requirements | -0.4% | Europe (MDR compliance), Asia-Pacific (varied approval pathways), North America (FDA post-market surveillance) | Medium term (2-4 years) |

| Limited adoption of digital rehabilitation among aging cohorts | -0.2% | Global, particularly acute in regions with lower digital literacy and internet penetration | Medium term (2-4 years) |

| Proliferation of low-cost counterfeit bracing devices online | -0.3% | Global e-commerce platforms; enforcement gaps in Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Costs and Reimbursement Uncertainty

Bundled payment models cap episode spending and penalize institutions for post-operative complications, forcing aggressive implant price negotiations and standardization around lower-cost systems. Private insurers adopt reference-based pricing, limiting reimbursement irrespective of brand, eroding manufacturer leverage over premium features. Prior authorization delays for platelet-rich plasma and stem-cell injections discourage small practices that lack dedicated billing staff, thereby constraining the volume of biologics. Japan’s biennial reimbursement reviews cut specific arthroscopy rates in 2024, illustrating international volatility that complicates revenue forecasting. Ambulatory surgery centers operate on slim margins, demanding flexible consignment and risk-sharing terms from suppliers. These dynamics prompt device makers to validate their superiority through registries and real-world evidence, thereby increasing the cost of market access.

Proliferation of Low-Cost Counterfeit Bracing Devices Online

The UK Medicines and Healthcare products Regulatory Agency issued a warning in March 2024 about counterfeit LifeVac devices, highlighting broader threats to knee braces and compression garments sold on global e-commerce platforms[3]Medicines and Healthcare products Regulatory Agency, “Counterfeit Medical Devices Warning,” gov.uk. Fake listings often mimic authentic imagery and citations, confusing consumers and undermining the brand equity of legitimate manufacturers. Many items display forged “FDA registration” certificates that misrepresent regulatory status, exposing buyers to substandard materials and inadequate support. Customs inspections intercept bulk shipments, yet small parcels bypass scrutiny, creating enforcement blind spots. Authentic brands respond by adding holographic labels and blockchain provenance systems, which drive up costs without yielding direct revenue gains. Counterfeiting, therefore, erodes pricing power and inflates compliance expenses in an already margin-pressured segment of the sports medicine market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Sports Medicine Market Segment Analysis

By Product Type:

Biologics Outpace Hardware in Growth VelocityOrthopedic implants contributed the largest 35.54% revenue share of the sports medicine market in 2025 because surgeons remain reliant on screws, plates, and suture anchors for durable mechanical fixation. Nevertheless, orthobiologics secured the steepest growth trajectory, aided by expanding clinical proof points and higher reimbursement adoption. The sports medicine market size for regenerative orthobiologics is projected to rise from USD 1.2 billion to USD 2.3 billion over the forecast period, highlighting the pivot toward biologically driven repair. Hospitals and outpatient centers are integrating point-of-care preparation systems for PRP and bone-marrow concentrates, reducing procedure times while maintaining sterility. Larger device firms are adding biologic grafts, collagen scaffolds, and synthetic extenders to their implant lines, confirming that future portfolio competitiveness hinges on blending metal fixation with biologic augmentation.

Surgeon education remains a crucial enabler because technique variation can hamper outcome reproducibility. Leading academic centers now include orthobiologic modules in fellowship curricula, emphasizing patient selection and standardized injection protocols. Simultaneously, healthcare payers analyze registries to confirm long-term cost offsets from faster return-to-sport and reduced re-operations. Such data, once mature, will clarify reimbursement pathways and further accelerate orthobiologic penetration across the sports medicine market.

By Application:

Knee Dominance Persists, Extremities AccelerateKnee procedures accounted for a 41.46% revenue share of the sports medicine market in 2025, driven by high volumes of anterior cruciate ligament (ACL) repair, meniscal tear surgery, and cartilage preservation. Foot and ankle procedures will expand at an 8.67% CAGR through 2031, buoyed by Zimmer Biomet’s acquisition of Paragon 28, which brought APEX 3D total ankle replacements and SMART 28 surgical planning into one portfolio. Shoulder interventions benefit from robotic precision and bioinductive patches, which raise healing rates and carve a wider outpatient niche. Hip and groin pathologies, often treated arthroscopically for labral tears, gain popularity as younger athletes seek motion-preserving solutions. Smaller segments, such as the elbow and wrist, serve niche populations, including overhead throwers and snowboarders, but still contribute to steady demand for specialized implants and soft-tissue anchors.

Gender-specific injury patterns influence product development, with female athletes facing higher ACL rupture risk due to anatomical and neuromuscular differences, prompting companies to explore graft options tailored to female anatomy. Foot and ankle innovation is fueled by minimally invasive bunion repair and patient-specific ankle systems that promise anatomical alignment and faster ambulation. Shoulder surgeons are embracing biologic augmentation patches, such as Smith+Nephew’s REGENETEN, to enhance tendon healing and lower re-tear rates. Hip arthroscopy benefits from the use of endoscopic instruments that access the joint through small portals, enabling preservation of the labrum in younger, active patients. Spine-adjacent sports medicine remains limited, but it is gaining traction as endoscopic techniques reduce recovery times for herniated discs in elite athletes.

By End User:

ASCs Capture Outpatient MigrationHospitals accounted for 46.43% of the sports medicine market size in 2025, supporting complex trauma, multi-ligament reconstructions, and high-acuity cases that require overnight monitoring. Ambulatory surgery centers will expand at a 9.32% CAGR to 2031 as bundled payments reward efficient outpatient care and infection rates stay below 1%. Home-based rehabilitation leverages remote monitoring platforms but faces adoption hurdles among older populations that prefer in-person guidance. Training facilities and occupational clinics offer point-of-injury triage and prevention services yet account for a modest slice of procedural revenue.

CMS payment parity narrows the financial gap between ASCs and hospital outpatient departments, thereby accelerating the migration of procedures. Device makers align with this shift by providing pre-sterilized, disposable kits that reduce turnover time and eliminate the need for central sterile processing. Hospitals respond by forging joint-venture ASCs or revamping existing wings into dedicated outpatient hubs, although certificate-of-need laws in certain U.S. states constrain expansion. Home care uptake correlates with digital literacy and internet penetration, variables that lag among seniors who constitute a large orthopedic patient cohort. Wearable sensors and tele-coaching apps, such as Zimmer Biomet’s mymobility, demonstrate improved range-of-motion adherence but still depend on caregiver assistance in many households.

Geography Analysis

North America Sports Medicine Market

North America remained the most significant regional contributor, accounting for 40.32% of the market in 2025. The National Football League’s collaboration with Amazon Web Services underscores a data-driven approach to injury prevention that reverberates across collegiate and youth programs, boosting demand for predictive analytics. CMS continues to refine bundled payment models, promoting price transparency and encouraging implant suppliers to validate clinical value. Dense ASC networks and widespread private insurance coverage facilitate the rapid adoption of outpatient services. Corporate wellness initiatives that include onsite physiotherapy further enlarge the addressable patient base because early-stage injuries receive immediate evaluation and referral.

APAC Sports Medicine Market

Asia-Pacific advances at a 7.65% CAGR to 2031. China funds neighborhood rehabilitation centers under the Healthy China 2030 initiative, encouraging early intervention and expanding public access to orthopedic care. Japan, with nearly one-third of its population aged 65 years or older, sustains demand for joint preservation but faces reimbursement cuts that prompt hospitals to adopt cost-effective implants. India’s expanding middle class fuels health club memberships, heightening overuse injuries and increasing private orthopedic practice revenue. Regulatory environments differ: China’s fast-track approvals aid domestic innovation, while Japan’s Pharmaceuticals and Medical Devices Agency maintains rigorous evidence thresholds that favor companies with multinational clinical operations.

Europe, Middle East and South America Sports Medicine Market

Europe experiences uneven growth due to the costs of complying with the Medical Device Regulation and public budget constraints. Large systems in Germany and France deploy robotic surgery but must justify the premium expense of implants under capped reimbursement. The Middle East invests in orthopedic centers to capitalize on medical tourism, while Brazil’s private hospitals in São Paulo and Rio de Janeiro adopt minimally invasive arthroscopy, despite currency fluctuations. Combined, these regions present a mosaic of reimbursement policies and infrastructure maturity that influence product launch sequences and pricing strategies.

Regulatory Landscape

Sports medicine products are regulated mainly as medical devices, covering implants, arthroscopy systems, physical medicine devices, and rehabilitation technologies. In the United States, the FDA continued to refine device classifications in 2026, including a final order reclassifying non-invasive bone growth stimulators from Class III to Class II effective May 18, 2026. This shifts many manufacturers from PMA expectations toward the 510(k) pathway with defined special controls. The FDA also issued 2026 final orders codifying Class II classifications for additional orthopedic categories, for example absorbable metallic bone fixation fasteners, reinforcing a risk-based approach that clarifies evidentiary and post-market expectations for commonly used fixation and adjunct devices.

In Europe, MDR compliance remains a gating factor for implants and procedure-enabling devices, with continued reliance on notified body capacity, clinical evaluation requirements, and post-market surveillance obligations. The European Commission published Delegated Regulation (EU) 2026/1359, which updates the list of Class IIb implantable devices exempted from individual technical documentation assessment. This eases review burden for selected implantable categories used in orthopedic fixation, such as screws, plates, and anchors, while keeping MDR controls in place. Alongside MDR implementation, quality-system and risk-management alignment to internationally recognized standards, for example ISO 13485, remains a foundational requirement for global market access across sports medicine portfolios.

Value Chain Analysis

The sports medicine value chain runs from specialty materials and components, including titanium, cobalt-chrome alloys, PEEK, sutures, and polymers, through design and verification, machining or additive manufacturing and surface finishing, sterilization and packaging, and then downstream distribution via hospital and ambulatory surgery center (ASC) sales channels, group purchasing organizations, and specialty distributors. OEMs, such as Stryker, Zimmer Biomet, Smith+Nephew, Johnson and Johnson MedTech, and Arthrex, typically combine in-house manufacturing with contract manufacturing organizations for implants, instruments, and select arthroscopy components, while service providers support sterilization, logistics, and field inventory management of reusable instrument sets.

Operational friction points highlighted across 2024-2025 include dependence on imported inputs, sterilization capacity constraints, and logistics disruptions. These conditions have pushed manufacturers toward dual-sourcing and regional manufacturing footprints, including nearshoring into Mexico and Costa Rica, to reduce transit risk and tariff exposure. Regulatory and traceability requirements are also shaping supply-chain processes: in Europe, EUDAMED readiness, including actor registration and UDI workflows, increases the focus on clean master data and labeling discipline, while in the United States, FDA reclassification of certain physical medicine devices, such as non-invasive bone growth stimulators, moves the compliance workstream toward 510(k) submissions and special controls. That, in turn, affects documentation, supplier qualification, and post-market surveillance planning.

Competitive Landscape

Market leaders include Stryker, Zimmer Biomet, Smith+Nephew, and Johnson & Johnson MedTech, which control core implant and arthroscopy lines. Meanwhile, specialists such as Arthrex, Miach Orthopaedics, and Paragon 28 occupy high-growth niches. Zimmer Biomet’s USD 1.1 billion purchase of Paragon 28 in November 2024 added extremity expertise, and the simultaneous integration of Monogram Technologies reinforces personalized implant capabilities. Stryker’s acquisitions of Artelon and Vertos Medical in 2024 expanded biologic scaffolds and outpatient spine devices, broadening exposure to ASC volumes. Smith+Nephew’s CartiHeal takeover underscores a strategic pivot into regenerative platforms to delay joint replacement.

Digital rehabilitation remains fragmented. Zimmer Biomet’s mymobility app leads in surgeon adoption but encounters resistance from older patients worried about data privacy. Counterfeit knee braces pose a threat to legitimate vendors, compelling anti-fraud spending that shrinks margins. Differentiation increasingly hinges on AI-driven planning systems, such as Stryker’s Mako and OrthoSensor’s force sensors, which translate subjective surgical feel into measurable parameters. Smaller innovators, such as Responsive Arthroscopy, embed analytics into towers, offering real-time instrument guidance without the capital burden of full robotics. European regulatory complexity shapes competition as companies with in-house quality and vigilance teams navigate the Medical Device Regulation more efficiently than under-resourced rivals, tilting market share toward large incumbents.

Sports Medicine Industry Leaders

Johnson & Johnson Services Inc.

Arthrex InSmith+Nephew Plcc.

Stryker Corporation

Zimmer Biomet Holdings Inc.

Johnson & Johnson Services Inc.

- *Disclaimer: Major Players sorted in no particular order

Sports Medicine Market Companies Covered in this Report

- Anika Therapeutics

- Arthrex

- Breg

- Conmed

- Enovis Corporation (DJO Global)

- Integra LifeSciences

- Johnson & Johnson

- Karl Storz

- Medtronic

- Mueller Sports Medicine

- Performance Health Holding Inc.

- Smith+Nephew Plc

- Stryker

- Zimmer Biomet

Market Opportunities and Future Outlook

There is a clear whitespace at the intersection of sports medicine procedures and the longitudinal recovery pathway, where providers and payers increasingly want objective, trackable outcomes rather than device-only differentiation. Recent market activity supports this shift. In May 2026, RIVANNA received FDA 510(k) clearance for the Accuro XV musculoskeletal ultrasound system, an AI-enabled portable point-of-care platform that can broaden access to earlier MSK evaluation in outpatient clinics, training environments, and prehab or rehab settings. Separately, recovery programs that integrate continuous biometrics with rehabilitation workflows, such as the Kinomatic and WHOOP RESTORE pilot announced in July 2026, point to a commercial opening for device makers and software partners to add monitoring and adherence tools to procedure volumes.

Sports medicine also has opportunity in portfolio densification around high-volume indications, particularly knee and shoulder, through acquisitions, fixation innovations, and biologic or regenerative platforms with real-world evidence. Smith+Nephew completed its acquisition of Integrity Orthopaedics in January 2026, adding Tendon Seam technology to deepen its shoulder repair offering alongside established platforms, and Miach Orthopaedics continues to build clinical credibility for the BEAR implant with registry-based evidence. Together, these moves suggest ongoing whitespace for integrated procedure kits, combining implants with biologic augmentation and enabling tools designed for ASC throughput, and for evidence generation, including registries and long-term follow-up, that supports reimbursement and formulary positioning under bundled-payment and value-based procurement models.

Recent Industry Developments in Sports Medicine Market

- May 2026: Zimmer Biomet received U.S. FDA 510(k) clearance for expanded capabilities of its ROSA Shoulder System, advancing robotically assisted steps such as glenoid preparation and humeral resection. The update strengthens Zimmer Biomet's shoulder ecosystem and supports greater standardization in outpatient shoulder workflows as robotics adoption broadens beyond flagship hospital sites.

- January 2026: Smith+Nephew completed the acquisition of Integrity Orthopaedics, adding Tendon Seam rotator cuff repair technology to its sports medicine and shoulder repair portfolio. The deal expands Smith+Nephew's breadth in soft-tissue repair and increases cross-selling potential with established offerings such as REGENETEN and related instrumentation.

- July 2024: Georgia Institute of Technology launched OrthoPreserve, a startup focused on developing meniscus implants aimed at preventing long-term complications from meniscus tears. The launch adds to the regenerative pipeline feeding cartilage and meniscal preservation, a key innovation lane for younger, active patients who seek alternatives to early joint replacement.

Sports Medicine Market Report Scope and Research Methodology

Market Definition and Coverage

In this methodology, the sports medicine market is counted as revenues tied to diagnosing, treating, and rehabilitating sports and activity related musculoskeletal injuries. Coverage includes specialized devices, implants, biologics, bracing, and therapy support products across care settings.

Scope exclusions: We exclude general fitness goods and consumer wearables that are sold only for lifestyle tracking and do not have a direct clinical use in sports injury care.

Segments Covered in This Report

- By Product Type

- Orthopedic Implants

- Arthroscopy Devices

- Orthobiologics

- Braces & Supports

- Bandages & Tapes

- Other Product Types

- By Application

- Knee Injuries

- Shoulder Injuries

- Foot & Ankle Injuries

- Hip & Groin Injuries

- Elbow Injuries

- Hand & Wrist Injuries

- Spine Injuries

- Other Injuries

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Home Care Settings

- Other End User

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest Of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest Of Asia-Pacific

- Middle East And Africa

- GCC

- South Africa

- Rest Of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest Of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base for injury volumes, procedure intensity, and medical device utilization patterns that sit behind demand. We leaned on public sources such as the World Health Organization, the US Centers for Disease Control and Prevention, the OECD health statistics series, and national health ministry portals for utilization and care setting context.

To make the model practical, we also reviewed customs and trade statistics portals for device import and export signals. We used peer reviewed orthopedic and sports medicine journals for treatment pathways, and publicly available company filings and investor presentations for product mix and exposure clues. In parallel, we referenced paid subscriptions for company financials and general news and financials to cross check timelines, launches, and reported revenue direction. These desk sources are illustrative, and many additional public references were used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary interviews and surveys were done with stakeholders across the sports medicine value chain, including distributors, clinicians involved in arthroscopy and orthopedics, rehabilitation service providers, and procurement professionals at hospitals and ambulatory surgical centers. Coverage was balanced across major demand regions so that assumptions on procedure mix, price ranges, and adoption of braces, biologics, and rehab tools could be challenged and then aligned before finalizing the totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | APAC: 50% |

| Mid tier: 49% | Functional/Unit leaders: 35% | EMEA: 32% |

| Smaller Players: 15% | Managers: 53% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where procedure and injury care volumes are reconstructed by region, then mapped to typical sports medicine treatment pathways across implants, arthroscopy devices, orthobiologics, braces and supports, and rehabilitation related products. Once that demand pool is framed, it is converted to value using region specific average selling price ranges and a realistic mix split by care setting.

To keep the model grounded, a selective bottom-up check was then applied using sampled supplier revenue exposure, channel checks on price bands, and product category shipment signals where visible. Gaps were handled by using proxy adoption rates from comparable countries with similar care infrastructure. Key inputs used in the model include arthroscopy and orthopedic procedure trends, sports and activity injury incidence, outpatient versus inpatient share, reimbursement and out-of-pocket patterns for braces and therapy products, and price progression for implants and biologics by region. Forecasting relies mainly on scenario analysis, shaped by primary inputs on how fast ambulatory surgical centers expand, how treatment shifts toward minimally invasive approaches, and how pricing changes under payer pressure.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, and then checked for outliers at the country and category level before consolidation to the global total. When a variance is seen, the assumptions are revisited, and re-contacts are triggered with selected experts to confirm whether the change is structural or only timing related.

A multi step analyst review is followed so that the same logic is applied across regions, with final sign off after consistency checks on volumes, pricing, and category shares. The report is refreshed annually, and interim updates are made when material events occur. After that, a final freshness pass is completed before delivery to clients.

Mordor Intelligence's Global Sports Medicine Market Market Size Measured Against Other Published Estimates

Published sports medicine market values often do not match, even when the time period looks similar, because each publisher sets its own inclusion rules and pricing logic. Differences usually come from what is counted as sports medicine (implants and arthroscopy devices only, or also braces, tapes, and rehabilitation support), and how procedure volume and ASP movement are treated across regions.

Some sources are broader and fold in accessory supplies and monitoring and evaluation items that can sit outside clinical sports injury treatment. In Mordor Intelligence's build, the total is anchored to clinically used sports injury care products and settings, and consumer wearables sold only for lifestyle tracking are kept out of the number, which shifts the headline value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.74 B (2026) | |

| Industry Research Publisher A | USD 6.78 B (2025) | Uses a different anchor year and a broader product basket that includes accessories and monitoring and evaluation categories, which can pull totals down or up depending on how clinical versus retail sales are treated. |

| Industry Research Publisher B | USD 6.10 B (2024) | Starts from an earlier base year and often reports a more conservative near term ramp, and its category mapping groups products into high level buckets that can undercount rehabilitation linked revenue when it is bundled within care delivery. |

Taken together, the spread mainly reflects year selection and what is treated as in scope, rather than a true disagreement on demand direction. By keeping inputs traceable to procedure intensity, injury care pathways, and region specific price ranges, the final estimate stays repeatable and easier to audit as assumptions change over time.

Key Questions Answered in the Report

What size will sports medicine reach by 2031?

It is projected to be valued at USD 10.76 billion in 2031, reflecting a 6.81% CAGR over 2026-2031.

Which product segment shows the fastest growth in sports medicine?

Orthobiologics post the quickest pace, registering an expected 8.54% CAGR through 2031, thanks to surgeon preference for joint-preserving biologic therapies.

Why are ambulatory surgery centers becoming key venues for orthopedic care?

Lower facility fees, infection rates below 1%, and CMS payment parity improvements are pushing more arthroscopies and ligament repairs into ASCs.

How is Asia-Pacific contributing to overall expansion?

Investments under China's Healthy China 2030 plan, Japan's large senior population, and India's rising gym memberships lift the region at a 7.65% CAGR.

What role does AI play in sports injury treatment and prevention?

Platforms such as Stryker's Mako SmartRobotics and the NFL-AWS Digital Athlete analyze motion data to improve implant alignment and predict high-risk play patterns.

Which regulatory trend poses the biggest challenge for device makers?

Europe's Medical Device Regulation adds stricter post-market surveillance and delays legacy product recertification, raising compliance costs for smaller suppliers.

Page last updated on: