Atherosclerosis Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 35.43 Billion |

| Market Size (2031) | USD 41.08 Billion |

| Growth Rate (2026 - 2031) | 3.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Atherosclerosis Drugs Market Analysis by Mordor Intelligence

The Atherosclerosis Drugs Market size was valued at USD 34.39 billion in 2025 and estimated to grow from USD 35.43 billion in 2026 to reach USD 41.08 billion by 2031, at a CAGR of 3.01% during the forecast period (2026-2031).

This measured pace reflects a maturing landscape in which generic statins lose exclusivity even as RNA-based therapeutics and gene-editing programs create new premium niches. Demand growth is anchored in the widening prevalence of atherosclerotic cardiovascular disease (ASCVD), the adoption of combination lipid-lowering regimens, and expanding reimbursement for precision biologics. Pipeline velocity has accelerated since 2024, with the first wave of small-interfering RNA (siRNA) and antisense oligonucleotide (ASO) agents demonstrating durable LDL-C and Lp(a) reductions. At the same time, price scrutiny in mature markets and affordability gaps in emerging economies temper headline expansion, directing volume toward cost-effective generics while leaving room for high-value therapies aimed at residual-risk populations. Digitally enabled adherence tools and hospital-based care pathways increasingly influence therapeutic choice and channel mix, reinforcing the clinical role of multidisciplinary cardiometabolic teams.

Key Report Takeaways

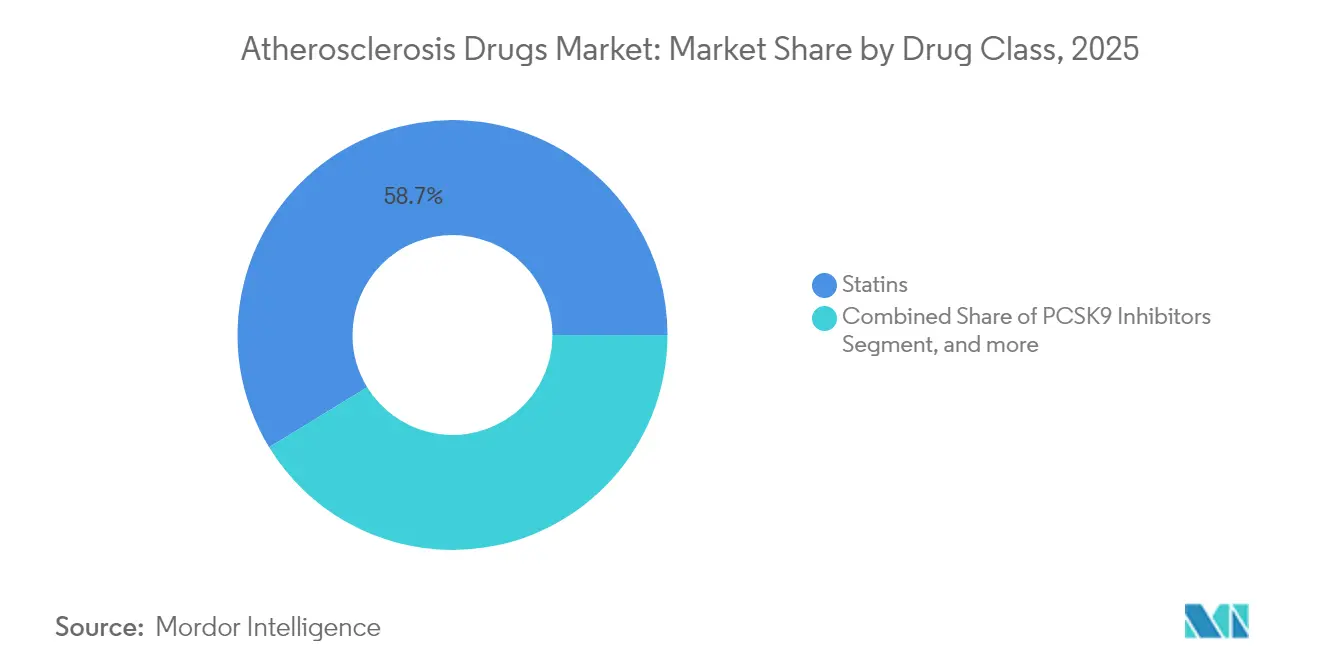

- By drug class, statins led with 58.74% of atherosclerosis drugs market share in 2025, while PCSK9 inhibitors are projected to expand at a 5.18% CAGR through 2031.

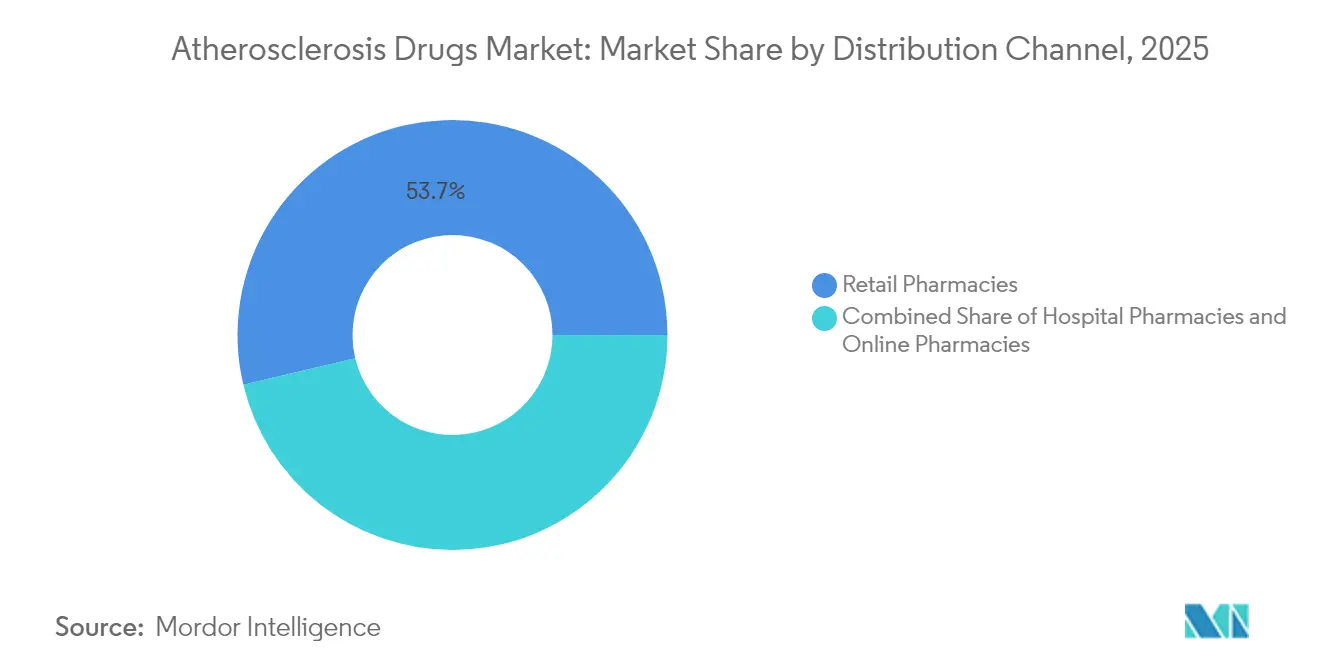

- By distribution channel, hospital pharmacies held 46.28% of the atherosclerosis drugs market share in 2025; online pharmacies record the highest projected CAGR at 6.52% to 2031.

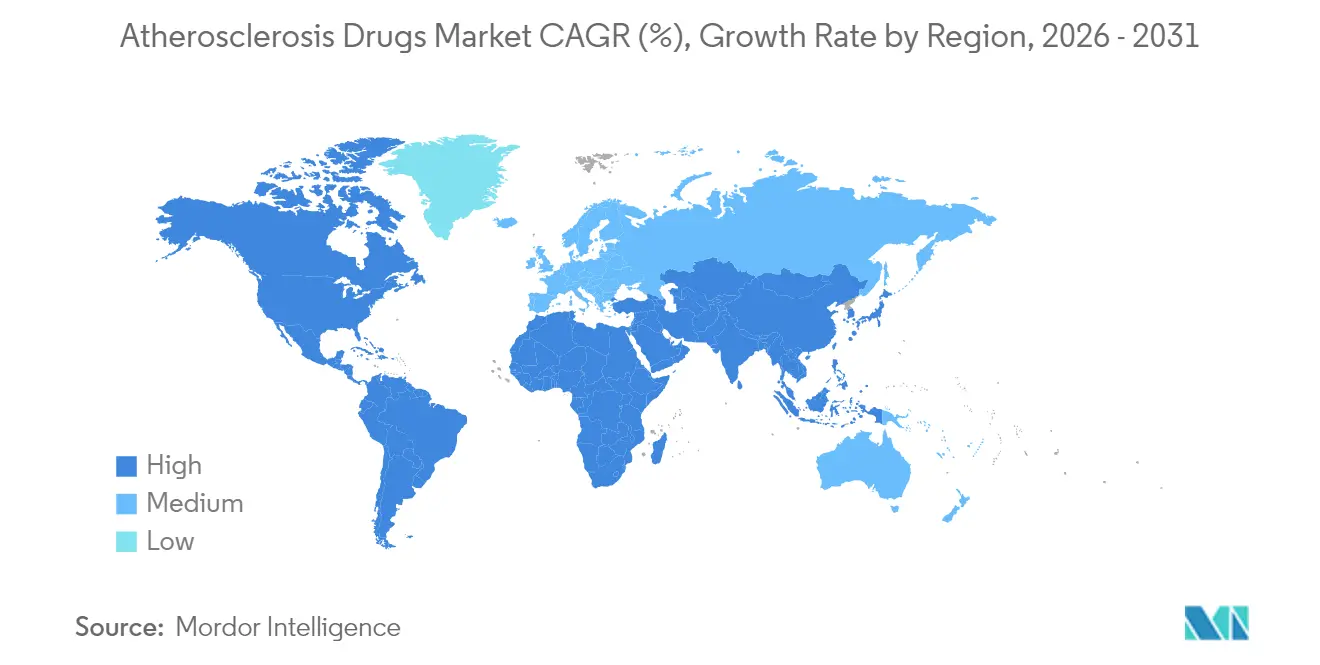

- By geography, North America accounted for 38.12% revenue share of the atherosclerosis drugs market in 2025, whereas Asia is set to progress at a 6.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Atherosclerosis Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of CVD & Aging Population | +0.8% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Guideline-Driven Uptake of Statins & PCSK9 Inhibitors | +0.6% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Higher Healthcare Spending & Drug Accessibility | +0.5% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Awareness Campaigns & Lipid-Screening Programs | +0.3% | Global, with early gains in developed markets | Short term (≤ 2 years) |

| RNA-Based Lipid-Lowering Therapies Pipeline Surge | +0.4% | North America & EU initially, global expansion | Long term (≥ 4 years) |

| Polygenic Risk Scoring Enabling Early Intervention | +0.2% | North America & EU, selective APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of CVD & Aging Population

Global life expectancy gains, urban sedentary lifestyles, and metabolic comorbidities combine to keep ASCVD the top cause of mortality worldwide. Low- and middle-income regions now account for 80% of cardiovascular deaths, creating structurally high unmet need for lipid-modifying therapies that are both affordable and scalable.[1]Editorial Board, “Global Burden of Atherosclerotic Cardiovascular Disease,” Global Heart, globalheartjournal.com The dual burden of diabetes and obesity escalates plaque formation and shifts onset to younger adults, extending lifetime drug exposure. Prevalence trends underpin sustained unit growth across the atherosclerosis drugs market, even as therapeutic intensity increases in elderly cohorts with polypharmacy constraints. Long-acting injectables and six-monthly siRNA regimens address adherence gaps common in chronic disease management, while fixed-dose oral combinations simplify treatment for primary-care settings in resource-constrained geographies.

Guideline-Driven Uptake of Statins & PCSK9 Inhibitors

The 2025 ACC/AHA guideline mandates high-intensity statins for acute coronary syndrome and advocates non-statin add-ons once LDL-C remains ≥70 mg/dL despite therapy.[2]Donald Lloyd-Jones, “2025 ACC/AHA Guideline for the Management of Acute Coronary Syndromes,” Journal of the American College of Cardiology, jacc.org Parallel European and International Lipid Expert Panel positions promote earlier dual-therapy initiation, broadening the eligible pool for PCSK9 inhibitors beyond historic statin-intolerant niches. Real-world registries demonstrate cardiovascular event reduction proportional to achieved LDL-C levels, reinforcing guideline influence on prescribing as payers reward goal attainment. Harmonized targets build a common language across regions, yet implementation still hinges on local reimbursement rules, physician familiarity, and health-technology-assessment outcomes.

Higher Healthcare Spending & Drug Accessibility

Asia-Pacific posted the largest cardiovascular drug outlay in 2024 on the back of fast-growing middle-class populations and universal-health-coverage rollouts. Government industrial policy, such as India’s Production Linked Incentive scheme, widens local manufacturing, lowers end-user prices, and drives generic penetration that anchors entry-level segments. Multinationals employ tiered pricing and regional joint ventures to defend premium brands while seeding long-term loyalty through patient-assistance programs. Private insurance expansion in urban China and Southeast Asia adds payor variety and increases uptake of novel biologics, especially in tertiary-care hospitals where cardiometabolic clinics operate at scale.

Awareness Campaigns & Lipid-Screening Programs

National cholesterol education initiatives and workplace screening bolster early disease detection, particularly in OECD markets where the relationship between LDL-C and cardiovascular risk is well publicized. Screening coverage jump-starts prescription cascades, augments statin volumes, and accelerates adoption of combination regimens among high-risk cohorts. Innovative campaign formats range from mobile clinics in rural India to AI-enabled patient stratification in United States integrated-delivery networks, narrowing treatment gaps and buoying atherosclerosis drugs market penetration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generic Erosion Post-Patent Expiry of Statins | -0.7% | Global, with highest impact in developed markets | Short term (≤ 2 years) |

| Poor Long-Term Adherence due to Side-Effects | -0.5% | Global, particularly affecting statin therapies | Medium term (2-4 years) |

| High Cost of Biologics in Low-Income Regions | -0.3% | APAC, MEA, and South America | Medium term (2-4 years) |

| Payer Push-Back on LDL-C Surrogate Endpoints | -0.2% | North America & EU, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Generic Erosion Post-Patent Expiry of Statins

Loss of exclusivity for atorvastatin and rosuvastatin demonstrated rapid price declines of more than 80% within 18 months of generic launch. Forthcoming expiries rivaroxaban in May 2025 and sacubitril/valsartan mid-2025 extend contractionary effects, squeezing brand revenues and shifting payer formularies toward lowest-cost options. Manufacturers pursue lifecycle-management tactics such as fixed-dose combinations and novel delivery forms in an effort to delay share attrition, yet these pivots rarely offset the steep volume shift to multisource products. While generics preserve therapy accessibility, they also compress overall atherosclerosis drugs market value in regions where statins dominate total prescriptions.

Poor Long-Term Adherence Due to Side-Effects

Statin-associated muscle symptoms occur in 5-30% of treated patients, but blinded crossover studies suggest true intolerance closer to 6-10%.[3]Ali Al-Mashhadi, “Statin Intolerance: True Incidence and Mechanistic Insights,” Journal of Advanced Research, journals.elsevier.com Fear of adverse reactions, medication fatigue, and polypharmacy discourage persistence, with discontinuation linked to 37% higher cardiovascular-event risk. Genetic screening for SLCO1B1 variants aids risk prediction yet remains under-utilized in routine practice. Second-line agents such as ezetimibe or bempedoic acid mitigate intolerance but entail additional cost and pill burden, complicating wide adoption in resource-constrained markets. The behavioral component of adherence thus remains a structural drag on sustained LDL-C lowering and, by extension, on the revenue trajectory of the atherosclerosis drugs market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Segment 1

Statins anchored 58.74% of the atherosclerosis drugs market share in 2025, owing to well-established efficacy, low cost, and broad guideline endorsement. The volume uplift they provide keeps the atherosclerosis drugs market size substantial despite headline price compression. PCSK9 inhibitors are forecast to deliver a 5.18% CAGR through 2031 on expanded indications for very high-risk patients and on payer acceptance of outcome-based contracting. Sales acceleration is also aided by maturing real-world evidence confirming 50-60% incremental LDL-C reductions on top of statins, translating into fewer cardiac events. Oral ATP-citrate lyase (ACL) inhibitors such as bempedoic acid attract statin-intolerant populations that previously lacked convenient alternatives, nudging prescription volumes higher in primary-care settings.

Pipeline momentum intensifies around RNA-based modalities: inclisiran solidifies a semi-annual dosing archetype, while ASOs targeting lipoprotein(a) line up for first global submissions in 2026. These additions enlarge the high-value biologic cohort and diversify the mechanism risk, offsetting some revenue lost to statin generics. Meanwhile, anti-inflammatory therapies like low-dose colchicine and monoclonal antibodies against IL-1β offer adjunctive pathways for risk reduction, hinting at multi-modal regimens that will expand the addressable pool. Collectively, innovation lengthens the premium tail of the atherosclerosis drugs market even as unit growth in legacy categories flattens.

By Distribution Channel: Digital Transformation Accelerates

Hospital pharmacies captured 46.28% revenue share in 2025 because acute coronary syndrome management, complex dual therapies, and specialty biologic handling require clinically integrated environments. Integrated cardiology clinics leverage on-site pharmacies to synchronize discharge prescriptions, minimizing early discontinuation and readmission risk. As a result, the atherosclerosis drugs market size linked to inpatient pathways remains robust. Retail pharmacies still move large statin volumes but confront tighter margins and staffing shortages that limit expansion into value-added services.

Online pharmacies, though accounting for a modest baseline, are projected to outpace all other channels at a 6.52% CAGR to 2031. Behavioral surveys reveal convenience and stock availability as primary purchase drivers, particularly among younger, tech-savvy chronic-disease cohorts. Digital-first players weave telehealth consultations, AI medication reminders, and next-day delivery into seamless care journeys, making them credible competitors for maintenance therapy refills. Traditional pharmacy chains respond with omnichannel offerings, repurposing brick-and-mortar outlets for clinical services while migrating fulfillment online. This evolution redistributes revenue streams inside the atherosclerosis drugs market and nudges manufacturers to redesign patient-support programs for digital touchpoints.

Geography Analysis

North America retained 38.12% of 2025 sales, sustained by guideline adoption, payer coverage for premium biologics, and a deep clinical-trial ecosystem that keeps innovation cycles short. The region benefits from FDA breakthrough designations that bring first-in-class treatments like CRISPR-based VERVE-102 to market ahead of other jurisdictions. Nevertheless, Medicare price negotiations and state-level importation initiatives heighten price elasticity, prompting strategic contracting and outcome-based deals. Digital adoption is high: remote lipid monitoring, prescription apps, and AI adherence coaching reinforce the value of combination regimens and help protect premium segments within the atherosclerosis drugs market.

Asia-Pacific is the fastest-growing region, with a 6.07% CAGR to 2031. Universal health coverage expansion, urbanization, and dietary westernization drive ASCVD prevalence, while local biosimilar PCSK9 launches improve affordability. India amplifies generic exports and internal demand, leveraging its PLI scheme to scale low-cost supply. Japan’s regulatory reforms incentivize multinational trial investment, though its rapidly aging population strains insurance budgets. Collectively, regional heterogeneity requires nuanced pricing and localization strategies but presents the single largest volume upside for the atherosclerosis drugs market.

Europe registers steady expansion supported by harmonized EMA guidelines and widespread public-health screening programs. Health-technology-assessment bodies impose stringent cost-effectiveness thresholds, fostering uptake of fixed-dose combinations and generics where outcome parity is demonstrated. Eastern European markets gain share as infrastructure improves, offering a growth relay as Western budgets tighten. Middle East & Africa and South America remain nascent but attractive in the long term. Cardiovascular disease awareness is rising, and private insurance penetration is widening in Gulf Cooperation Council states and Brazil, yet public-sector budgets lag, limiting the immediate uptake of high-cost biologics. Nonetheless, partnership models with government import agencies and local distributors lay the groundwork for future expansion of the atherosclerosis drugs market.

Competitive Landscape

Market concentration is moderate. Five global incumbents, Pfizer, Amgen, Novartis, Sanofi, and AstraZeneca, control the majority of premium biologics, while scores of generics makers dominate legacy statins. Consolidation continues: Eli Lilly’s USD 1.3 billion acquisition of Verve Therapeutics brings in vivo base-editing capacity aimed at single-shot LDL-C lowering, and Novo Nordisk’s EUR 1.02 billion purchase of Cardior Pharmaceuticals adds RNA-based myocardial-remodeling assets via direct company disclosure filings. Such deals pivot portfolios toward gene silencing, inflammatory modulation, and combinatorial mechanisms, bolstering differentiation as statin revenue compresses.

Technology integration emerges as a core differentiator. AI models accelerate target discovery and in-silico lead optimization, trimming preclinical timelines by up to 18 months according to company investor presentations. Companion-diagnostic development—especially genotype panels for statin intolerance and polygenic risk—creates stickier franchise ecosystems, aligning with precision-medicine reimbursement pathways. Digital therapeutic adjuncts, such as smartphone lipid-tracking apps, stabilize real-world adherence rates and generate actionable data for risk-share contracts.

Smaller biotechnology entrants attack white-space indications like elevated lipoprotein(a) and residual inflammatory risk. LIB Therapeutics posts positive phase 3 data on lerodalcibep, a small-dose monthly PCSK9 fusion protein that challenges established monoclonal-antibody incumbents. NewAmsterdam Pharma’s obicetrapib revives interest in CETP inhibition with high-density lipoprotein elevation coupled to LDL-C lowering. Competitive intensity therefore spans both price competition in commoditized statins and value competition in RNA- and gene-editing frontiers, keeping barriers to entry high yet dynamic within the atherosclerosis drugs market.

Atherosclerosis Drugs Industry Leaders

Pfizer Inc.

AstraZeneca

Merck & Co., Inc.

Amgen Inc.

Regeneron Pharmaceuticals, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: LIB Therapeutics Inc., a privately-held, late-stage biopharmaceutical company, announced promising clinical results for its lead candidate Lerodalcibep (LeroChol) a novel, small-dose, monthly PCSK9 inhibitor. The data were presented at the 2025 European Atherosclerosis Society (EAS) Meeting, held May 5–7 in Glasgow. This third-generation PCSK9 inhibitor is being developed to offer a more convenient and effective lipid-lowering therapy, with the potential to reshape treatment paradigms for patients with elevated LDL-C.

- May 2025: NewAmsterdam Pharma has announced late-breaking data from its BROADWAY and TANDEM pivotal studies, now published in leading peer-reviewed medical journals and presented at the 2025 European Atherosclerosis Society (EAS) Congress. These findings represent a major milestone in the company’s clinical program, reinforcing the therapeutic potential of its investigational therapies in addressing residual cardiovascular risk and lipid disorders.

- March 2025: AstraZeneca announced positive Phase IIb results for AZD0780, demonstrating 50.7% LDL cholesterol reduction when added to standard statin therapy. The oral PCSK9 inhibitor achieved LDL-C targets in 84% of participants compared to 13% on statins alone.

- January 2025: Cyclarity Therapeutics has officially launched its first human clinical trial aimed at curing atherosclerosis by targeting a particularly stubborn form of cholesterol buildup. This novel approach focuses on eliminating oxidized cholesterol, a key contributor to arterial plaque formation and cardiovascular disease progression. The trial marks a significant step forward in the pursuit of disease-modifying therapies for atherosclerosis, moving beyond symptom management toward a potential long-term solution.

Global Atherosclerosis Drugs Market Report Scope

As per the scope of the report, atherosclerosis is a hardening and narrowing of your arteries. It puts blood flow at risk as arteries get blocked. The Atherosclerosis Drugs Market is segmented by Drug Class (Anti-platelet Medications, Cholesterol-Lowering Medications, Fibric Acid and Omega-3 Fatty Acid Derivatives, Beta Blockers, Others) Distribution Channel (Retail Pharmacies, Hospital Pharmacies, and Online Pharmacies), and by Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Statins |

| PCSK9 Inhibitors |

| Bempedoic-acid & ACL inhibitors |

| Antiplatelet Agents |

| Omega-3 Fatty-acid Derivatives |

| RNA-based Therapies (ASO & siRNA) |

| Others |

| Retail Pharmacies |

| Hospital Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Statins | |

| PCSK9 Inhibitors | ||

| Bempedoic-acid & ACL inhibitors | ||

| Antiplatelet Agents | ||

| Omega-3 Fatty-acid Derivatives | ||

| RNA-based Therapies (ASO & siRNA) | ||

| Others | ||

| By Distribution Channel | Retail Pharmacies | |

| Hospital Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current atherosclerosis drugs market size and projected growth?

The atherosclerosis drugs market size stands at USD 35.43 billion in 2026 and is forecast to reach USD 41.08 billion by 2031, translating to a 3.01% CAGR.

Which drug class dominates the atherosclerosis drugs market?

Statins maintained leadership with 58.74% atherosclerosis drugs market share in 2025 because of broad guideline endorsement and low cost.

What is the fastest-growing segment within the atherosclerosis drugs market?

PCSK9 inhibitors are projected to grow at a 5.18% CAGR through 2031, driven by expanded high-risk indications and improved payer access.

Which region is expected to post the highest growth in the atherosclerosis drugs market?

Asia-Pacific is forecast to grow at 6.07% CAGR between 2026 and 2031 due to rising cardiovascular disease prevalence and improving healthcare access.

How is digital transformation influencing distribution channels?

Online pharmacies are the fastest-growing channel at a 6.52% CAGR to 2031, supported by telehealth integration, AI-driven adherence tools, and consumer preference for home delivery.

What emerging therapies could reshape the atherosclerosis drugs industry?

RNA-based siRNA and ASO agents targeting LDL-C and lipoprotein(a), along with gene-editing programs such as base editing, hold potential to deliver disease-modifying benefits and extend premium market segments within the next five years.

Page last updated on: