Artillery Ammunition Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

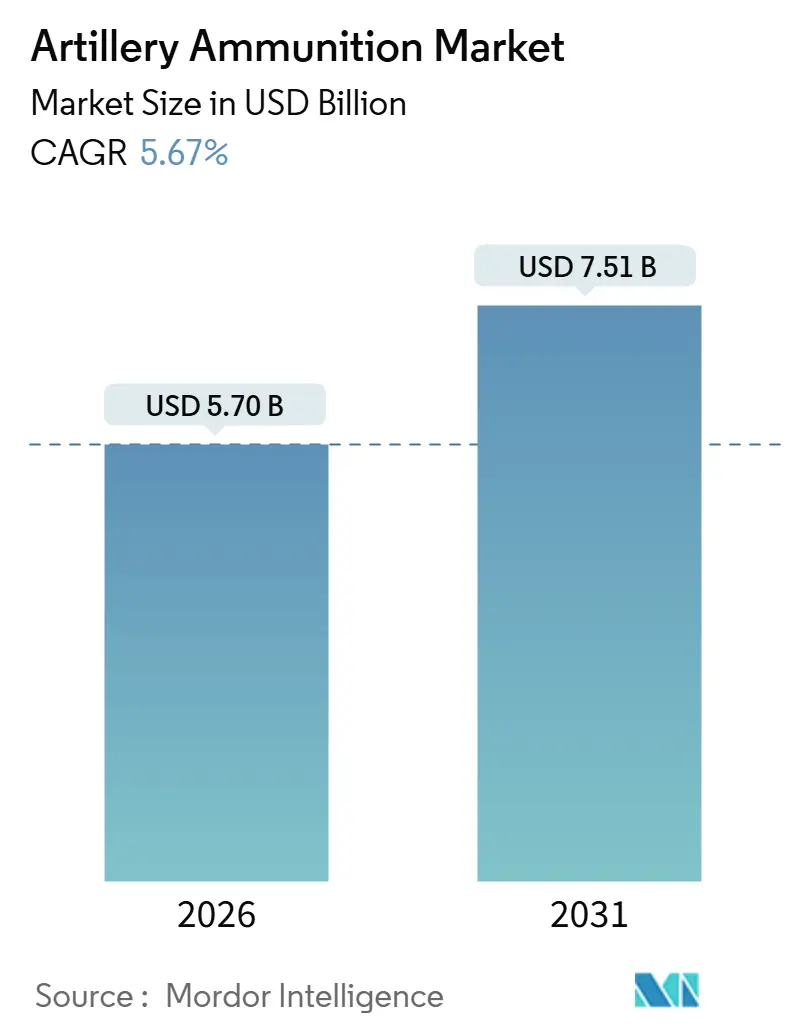

| Market Size (2026) | USD 5.70 Billion |

| Market Size (2031) | USD 7.51 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artillery Ammunition Market Analysis by Mordor Intelligence

The artillery ammunition market size stood at USD 5.70 billion in 2026 and is projected to reach USD 7.51 billion by 2031, expanding at a 5.67% CAGR during the forecast period. Heightened consumption rates in Ukraine, combined with multi-year rearmament programs in NATO and key Indo-Pacific nations, pull procurement away from platform upgrades and toward sustained shell production. Framework agreements, such as Rheinmetall’s USD 10.1 billion deal with the Bundeswehr and the US Army’s plan to produce 100,000 155 mm rounds per month by late 2025, anchor visibility for suppliers, encouraging green-field investments in propellant, fuze, and machining. Precision-guided programs are reshaping demand toward rounds that engage targets beyond 70 kilometers, while NATO standardization around the Modular Artillery Charge System (MACS) is trimming logistics footprints and improving barrel safety margins. Competitive intensity is rising as governments invoke defense-production acts to onshore manufacturing, forcing incumbents to license know-how locally and newcomers to secure insensitive-munition-compliant formulations to qualify for alliance tenders. Raw-material volatility in nitrocellulose and copper, as well as export-control frictions on advanced fuzes, remain margin-pressure points but have not slowed order momentum to date.

Key Report Takeaways

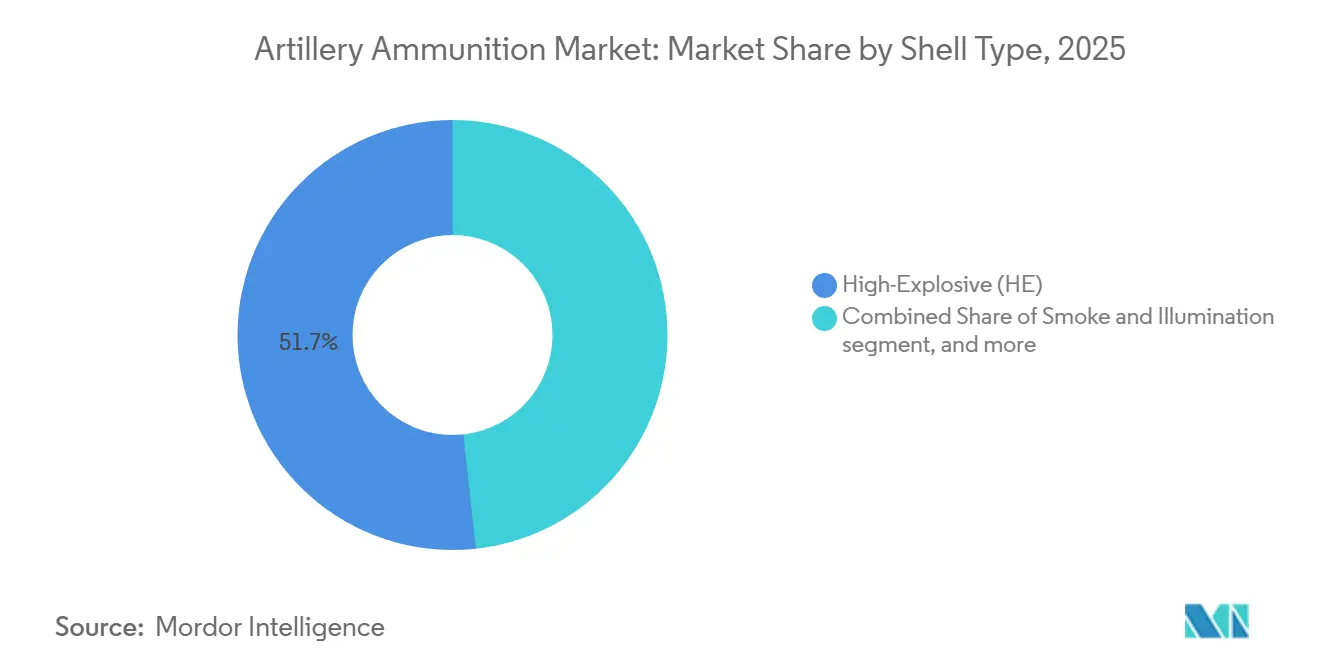

- By shell type, high-explosive (HE) rounds led with 51.74% of the artillery ammunition market share in 2025, while precision-guided shells are forecasted to advance at a 5.58% CAGR through 2031.

- By guidance mechanism, unguided projectiles accounted for 59.05% of the artillery ammunition market size in 2025, whereas GPS-guided variants are projected to post a 6.41% CAGR between 2026 and 2031.

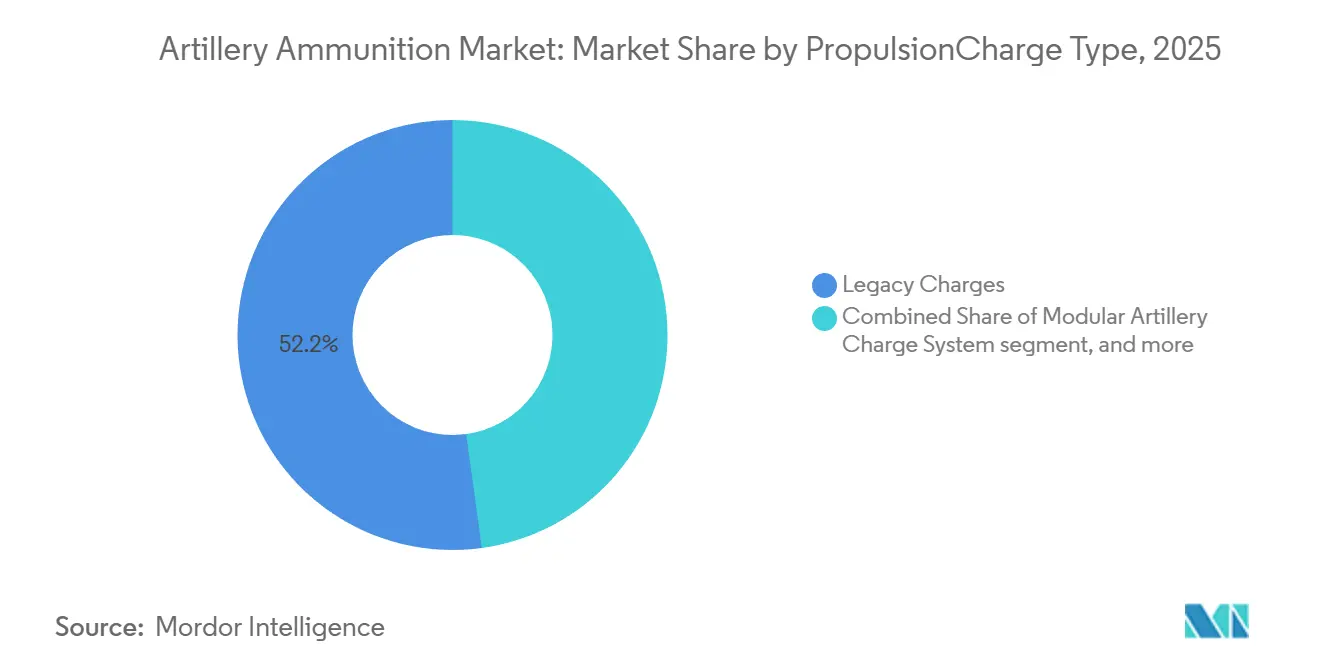

- By propulsion, legacy charges captured 52.18% revenue share in 2025; MACS-compatible propellant sets are expected to expand at a 5.68% CAGR to 2031.

- By platform, self-propelled howitzers commanded 49.79% of 2025 demand, yet rocket artillery ammunition is anticipated to grow at a 5.74% CAGR during the forecast window.

- By geography, North America held 37.61% revenue share in 2025, while Asia-Pacific is the fastest-growing region with a 5.17% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Artillery Ammunition Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating great-power competition and high-tempo munitions expenditure | +1.2% | Global, Europe and Indo-Pacific focal points | Long term (≥ 4 years) |

| Surge in long-range precision-fire programs | +0.9% | North America and Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Modernization of 155 mm logistics chains and modular charge systems | +0.8% | Global, NATO-aligned nations | Medium term (2-4 years) |

| Rising defense budgets in Asia-Pacific and Eastern Europe | +1.1% | APAC core, Eastern Europe | Long term (≥ 4 years) |

| NATO qualification of insensitive-munitions propellants unlocking new suppliers | +0.6% | NATO member and candidate states | Medium term (2-4 years) |

| Additive-manufactured driving bands lowering barrel wear and shell cost | +0.5% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Great-Power Competition and High-Tempo Munitions Expenditure

Russia’s output reaching 250,000 shells per month by mid-2024 and NATO’s pledge to deliver 2 million 155 mm rounds to Ukraine by March 2025 exposed historic stockpile gaps that now dictate procurement priorities.[1]Stockholm International Peace Research Institute, “SIPRI Military Expenditure Database 2024,” sipri.org The US alone appropriated USD 3 billion to expand facilities in Scranton and Lake City, increasing monthly production from 28,000 rounds in early 2023 to a target of 100,000 rounds by late 2025.[2]U.S. Army, “Fiscal 2025 Excalibur Procurement Justification,” defense.gov EU instruments such as the USD 117 million ASAP fund co-finance new lines in member states, while Taiwan and South Korea ramp up budgets to buffer against regional flashpoints.[3]European Commission, “Act in Support of Ammunition Production (ASAP),” europa.eu Long-term, multiyear contracts now underwrite capital-intensive propellant and fuze investments that would have been commercially unviable under peacetime consumption patterns. The artillery ammunition market, therefore, benefits from unprecedented demand certainty across at least one complete planning cycle, anchoring the current 5-year capacity-build trend.

Surge in Long-Range Precision-Fire Programs

The US Extended Range Cannon Artillery effort, re-branded in 2024, integrates XM1113 rocket-assisted and XM1155-SC precision rounds to reach 70 kilometers, with IOC slated for 2027. BAE Systems shipped Excalibur S lots featuring semi-active laser seekers, while Leonardo’s Vulcano family secured USD 235 million in domestic orders after NATO qualification. General Atomics demonstrated a ramjet-assisted 150-kilometer shell costing under USD 100,000, eroding the cost-per-target advantage of tactical missiles. These programs collectively cut rounds-per-effect ratios, shifting value from metalwork to guidance subsystems and stimulating hybrid-guidance R&D against GPS denial. Suppliers able to internalize fuze and seeker production capture higher margins and face lower exposure to export controls.

Modernization of 155 mm Logistics Chains and Modular Charge Systems

NATO's adoption of the M231/M232 MACS streamlines ammunition SKUs and reduces propellant-handling hazards, with the US Army awarding a USD 218 million expansion contract in 2023. Germany added 200,000 MACS-compatible shells in June 2024 to harmonize PzH 2000 logistics, and Poland reduced propellant variants by 40% across K9PL and Krab fleets. Insensitive munition compliance further lowers magazine fire insurance premiums and allows denser depot stacking, which is critical for nations with limited bunkers. The streamlined chain enhances coalition interoperability, underpinning NATO's broader ambition for plug-and-play ammunition interchangeability by 2030.

Rising Defense Budgets in Asia-Pacific and Eastern Europe

Military expenditure in the Asia-Pacific region rose to USD 683 billion in 2024, while Eastern Europe logged a 17% year-on-year budget surge, surpassing any regional increase since 1990. India allocated USD 7.4 billion for artillery programs in fiscal 2025, South Korea approved USD 2.6 billion for the K9 Thunder ammunition, and Poland topped NATO at 4.2% of its GDP in 2024, which led to the establishment of a USD 665 million domestic plant. These budgets are structural, driven by threat assessments that stretch beyond single-year appropriations. Consequently, the artillery ammunition market secures long-tail demand extending well into the next decade.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent ITAR/Wassenaar controls on fuzes and base-bleed assemblies | -0.7% | Global, acute for non-NATO buyers | Long term (≥ 4 years) |

| Volatile nitrocellulose and copper prices pressuring margins | -0.6% | Global, affects small-scale producers | Short term (≤ 2 years) |

| Chronic shortage of triple-base propellant mixing capacity (M31) | -0.8% | United States and Europe focus | Medium term (2-4 years) |

| Fire-safety insurance premiums for ageing ECM magazines | -0.4% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent ITAR/Wassenaar Controls on Fuzes and Base-Bleed Assemblies

Category I controls lengthen license cycles up to 18 months, delaying Turkish and South Korean exports that embed US-origin GPS fuzes. Roketsan redesigned its HE-ERFB projectile to circumvent ITAR parts, sacrificing range, while Bharat Electronics invested USD 85 million in Pune to localize artillery fuzes, extending NATO-compliance testing into 2027. Export-control frictions fragment the supply base and incentivize second-tier producers to field lower-performance but license-free alternatives, limiting unit-value upside for premium suppliers.

Volatile Nitrocellulose and Copper Prices Pressuring Margins

Nitrocellulose spot prices spiked 32% between January 2024 and March 2025 after a fire in Poland removed 8,000 metric tons of annual output.[4]ICIS Editorial, “Nitrocellulose Market Tightens on Regulatory Clampdown,” icis.com Copper traded above USD 10,200 per metric ton in February 2024, lifting the driving-band cost by USD 12 per shell. Suppliers without hedging saw 200-300 basis-point margin erosion, prompting contract renegotiations or early exit from fixed-price deals. The global capacity of 180,000 metric tons of nitrocellulose remains at least 40,000 tons short of projected 2028 artillery demand, suggesting persistent price pressure absent new production facilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Shell Type: High-Explosive Dominance Amid a Precision Pivot

High-explosive (HE) rounds accounted for 51.74% of the artillery ammunition market share in 2025 as they remain indispensable for suppression, area denial, and quick-response missions. Precision-guided shells, though still a minority, are forecast to grow at a 5.58% CAGR as doctrinal shifts emphasize first-round effects and ammunition conservation. The United States Army’s USD 1.2 billion purchase of 36,000 Excalibur rounds between 2024 and 2026 illustrates the budgetary swing toward GPS-guided options that replace multiple unguided rounds per target. Smoke, illumination, and practice rounds continue to support combined-arms training cycles, while DPICM sales shrink under the Convention on Cluster Munitions. Base-bleed and rocket-assisted projectiles are attracting Asia-Pacific users, such as India, which cleared its 48-kilometer base-bleed round for serial production in 2027.

Precision-guided munitions (PGMs) expand manufacturer margins due to the high value of embedded sensors, but they also intensify ITAR exposure and supply-chain complexity. Budget-constrained militaries in Africa and Latin America continue to favor high-explosive bulk orders, ensuring that legacy production lines run in parallel with smart-munition assembly. The dual-speed dynamic keeps the artillery ammunition market diversified across price points and technologies, reducing total demand volatility.

By Guidance Mechanism: GPS-Guided Systems Gain Ground

Unguided projectiles represented 59.05% of 2025 revenue, reflecting fleet compatibility and unit cost below USD 1,200 per shell. GPS-guided shells are expected to grow 6.41% CAGR through 2031 on the back of Raytheon’s Arizona line expansion and XM1155-SC adoption. Laser-guided variants offer moving-target engagement but require line-of-sight (LOS) illumination, which complicates their use in contested electromagnetic environments. Hybrid GPS-INS solutions mitigate jamming, evidenced by Elbit’s SIGMA contract with a European NATO member. Electronic warfare in Ukraine highlights the need for redundancy, prompting suppliers to adopt multi-mode guidance despite increased costs.

Unguided rounds keep relevance for saturation and suppression fire, particularly against soft targets where precision provides marginal benefit. Nevertheless, interoperability rules, such as STANAG 4425, push even value-tier buyers toward at least partially GPS-friendly inventories, ensuring a steady erosion of the unguided share over time, despite ongoing volume purchases.

By Propulsion/Charge Type: MACS Redraws the Supply Chain

Legacy charges still made up 52.18% of 2025 consumption, but MACS is forecasted to capture new-production dominance at a 5.68% CAGR, standardizing increments across alliance inventories. Insensitive munition properties reduce mishaps by 60%, while palletized logistics shrink convoy requirements by 30% in forward areas. Extended charges offer a bridge for legacy guns, evidenced by India’s 130 mm M46 range extension to 38 kilometers. Environmental rules such as the EU’s REACH legislation accelerate the shift, imposing reformulation costs that legacy-charge producers struggle to absorb without volume guarantees.

The MACS ecosystem also boosts after-market revenue in gas-check pads, igniter bags, and packaging, creating incremental value for suppliers able to scale modular components. Nations outside NATO, particularly in Africa and Latin America, continue to use bagged charges due to their lower upfront cost. However, second-hand platform imports from Europe will gradually introduce MACS compatibility into these markets.

By Platform Type: Rocket Artillery Momentum Accelerates

Self-propelled howitzers retained a 49.79% share of 2025 demand, upheld by mobility advantages in counter-battery environments. Yet, rocket artillery ammunition is slated for a 5.74% CAGR through 2031 as Lockheed Martin’s USD 1.1 billion GMLRS contract illustrates. South Korea’s K239 Chunmoo exports are expected to embed derivative ammunition demand exceeding USD 500 million through 2028. Towed systems such as the M777A2 uphold niche roles for airborne forces, while mortars and naval guns continue to carve out close-support and maritime-fire niches.

The artillery ammunition market size for rocket artillery rounds is expanding fastest in Europe and the Indo-Pacific, where deep-fire doctrine values coverage of 70 kilometers or more. Platform specificity complicates interchangeability: a shell tuned to the PzH 2000’s 52-caliber barrel can underperform in a 39-caliber K9 Thunder, necessitating multi-variant inventories and prompting suppliers to maintain engineering depth across various barrel lengths.

Geography Analysis

North America generated 37.61% of 2025 revenue, primarily driven by the US Department of Defense's (DoD's) USD 3 billion initiative to increase monthly 155 mm output to 100,000 by late 2025. Transfers exceeding 2 million shells to Ukraine by the end of 2024 create backfill orders that sustain high output rates even after the immediate conflict phase. The artillery ammunition market size within the US pre-positioned stocks in Guam, Japan, and Australia is expected to grow as Pacific defense planning matures. Canada's CAD 850 million (USD 621.83 million) M777A2 buy embeds a decade-long ammunition stream, whereas Mexico's budget keeps its M101 and M114 fleets operational but static.

Asia-Pacific is forecasted to grow at a 5.17% CAGR, buoyed by India's commitment to double 155 mm shell capacity to 240,000 rounds by 2027 and South Korea's KRW 1.2 trillion (USD 836.50 million) ammunition contract portfolio extending to 2030. Japan's 16% budget increase funds Type 19 howitzer ammunition, and China's Norinco operates six dedicated artillery-rocket plants that feed export orders, which, although opaque, intensify competition across Africa and Latin America. Deterrence-driven budgets in Taiwan and Australia implicitly lock in long-term shell requisitions, adding resilience to regional demand even under shifting political coalitions.

Europe's resurgence is underpinned by the USD 51.44 billion SAFE loan and Rheinmetall's Bundeswehr framework, positioning the bloc to rival North America in volume output by 2028. Poland's partnership plant aims for 150,000 shells annually by 2027, Germany's 200,000-round MACS order stimulates subcontracting across the region, and the UK invests GBP 300 million (USD 404.89 million) in Glascoed for 152 mm lines. France, Sweden, and Norway each tie national funding to Ukrainian resupply, creating predictable multi-year order books while distributing capacity to mitigate the risk of single-facility reliance. Russian production continues at scale, targeting a narrow export club that limits overlap with NATO buyer pools.

Competitive Landscape

Global capacity remains moderately concentrated, with Rheinmetall AG, BAE Systems plc, General Dynamics Corporation, Nammo AS, and Elbit Systems Ltd. controlling a majority of the installed shell output. However, localization mandates are driving new entrants and joint ventures. Rheinmetall’s Lithuania plant and BAE Systems’ Polish JV signal a pivot to distributed manufacturing that reduces political risk and aligns with host-nation content rules. Nammo leverages Norwegian state backing to scale up insensitive munition propellant. At the same time, Elbit Systems wins a share through the vertical integration of guidance electronics, as evidenced by its USD 270 million rocket artillery contract in 2024. Patent activity increased by 34% between 2023 and 2025, with Northrop Grumman leading in precision algorithms and Rheinmetall in formulations, demonstrating R&D differentiation beyond mere scale.

Price pressure emerges from Chinese state-owned Norinco, whose 155 mm shells undercut Western units by 30% in African tenders, though quality and ITAR-denied guidance tech still limit penetration into alliance markets. Additive-manufacturing startups are pursuing copper driving bands and aluminum-lithium fuze casings, offering 10-18% cost savings once volume ramps up by 2027, potentially reshaping entry barriers for low-volume niche suppliers. Incumbents respond through royalty-based licensing, ensuring they capture margin even when domestic offsets mandate local assembly.

Artillery Ammunition Industry Leaders

Rheinmetall AG

General Dynamics Corporation

BAE Systems plc

Elbit Systems Ltd.

Nammo AS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: MSM Group North America secured a USD 635 million contract from the US Army to design, construct, and inaugurate the Future Artillery Complex (FAC) at the Iowa Army Ammunition Plant.

- June 2024: ST Engineering secured contracts exceeding USD 100 million to provide NATO-standard 155mm ammunition to European nations.

- June 2024: KNDS France secured a contract from the French procurement agency Direction générale de l'armement (DGA) to aid in the development of the KATANA high-precision guided ammunition. Set to be available for purchase within the next two years, this 155mm ammunition boasts cutting-edge guidance technology, ensuring pinpoint accuracy within a few meters.

Global Artillery Ammunition Market Report Scope

Artillery ammunition refers to the type of ammunition that is designed to be fired from artillery cannons, which has an effect over long distances. There are many different types of artillery ammunition, but this type is usually highly explosive and designed to shatter into fragments upon impact, thereby maximizing damage. Common types of artillery ammunition include high explosives, smoke, illumination, and practice rounds. Some artillery rounds are designed as cluster munitions.

The artillery ammunition market is segmented based on shell type, guidance mechanism, propulsion/charge type, platform type, and geography. By shell type, the market is segmented into high-explosive (HE), smoke and illumination, dual-purpose improved conventional munition (DPICM), base-bleed/rocket-assisted projectile (RAP), sensor-fuzed/cluster, precision-guided, and practice/blank. By guidance mechanism, the market is segmented by unguided, GPS-guided, laser-guided, and inertial/hybrid. By propulsion/charge type, the market is segmented into legacy charges, Modular Artillery Charge System (MACS), and extended range and submunition rounds. By platform type, the market is segmented into towed howitzers, self-propelled howitzers, mortars (greater than 81 mm), rocket artillery (MRL), and naval guns. The report also covers the market sizes and forecasts for the artillery ammunition market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| High-Explosive (HE) |

| Smoke and Illumination |

| Dual-Purpose Improved Conventional Munition (DPICM) |

| Base-Bleed/Rocket-Assisted Projectile (RAP) |

| Sensor-Fuzed/Cluster |

| Precision-Guided |

| Practice/Blank |

| Unguided |

| GPS-Guided |

| Laser-Guided |

| Inertial/Hybrid |

| Legacy Charges |

| Modular Artillery Charge System (MACS) |

| Extended Range and Submunition Rounds |

| Towed Howitzers |

| Self-Propelled Howitzers |

| Mortars (Greater than 81 mm) |

| Rocket Artillery (MRL) |

| Naval Guns |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Shell Type | High-Explosive (HE) | ||

| Smoke and Illumination | |||

| Dual-Purpose Improved Conventional Munition (DPICM) | |||

| Base-Bleed/Rocket-Assisted Projectile (RAP) | |||

| Sensor-Fuzed/Cluster | |||

| Precision-Guided | |||

| Practice/Blank | |||

| By Guidance Mechanism | Unguided | ||

| GPS-Guided | |||

| Laser-Guided | |||

| Inertial/Hybrid | |||

| By Propulsion/Charge Type | Legacy Charges | ||

| Modular Artillery Charge System (MACS) | |||

| Extended Range and Submunition Rounds | |||

| By Platform Type | Towed Howitzers | ||

| Self-Propelled Howitzers | |||

| Mortars (Greater than 81 mm) | |||

| Rocket Artillery (MRL) | |||

| Naval Guns | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the artillery ammunition market today?

The artillery ammunition market is valued at USD 5.70 billion in 2026 and is on track to reach USD 7.51 billion by 2031, reflecting a 5.67% CAGR.

Which shell type earns the highest revenue?

High-explosive (HE) rounds lead with 51.74% share of 2025 revenue.

What is driving the shift toward GPS-guided ammunition?

Long-range and precision-fire programs and the need to conserve stockpiles are pushing adoption, resulting in a forecast 6.41% CAGR for GPS-guided shells through 2031.

Why is Asia-Pacific the fastest-growing region?

Sustained defense-budget growth in India, South Korea, and Japan, coupled with export-linked demand from K9 Thunder programs, is propelling a 5.17% CAGR outlook.

How are raw-material prices affecting producers?

A 32% spike in nitrocellulose and elevated copper costs cut margins by up to 300 basis points for suppliers without long-term hedges.

Which companies dominate current supply?

Rheinmetall AG, BAE Systems plc, General Dynamics Corporation, Nammo AS, and Elbit Systems Ltd. collectively control about 55% of installed capacity.

Page last updated on: