Ammunition Handling Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

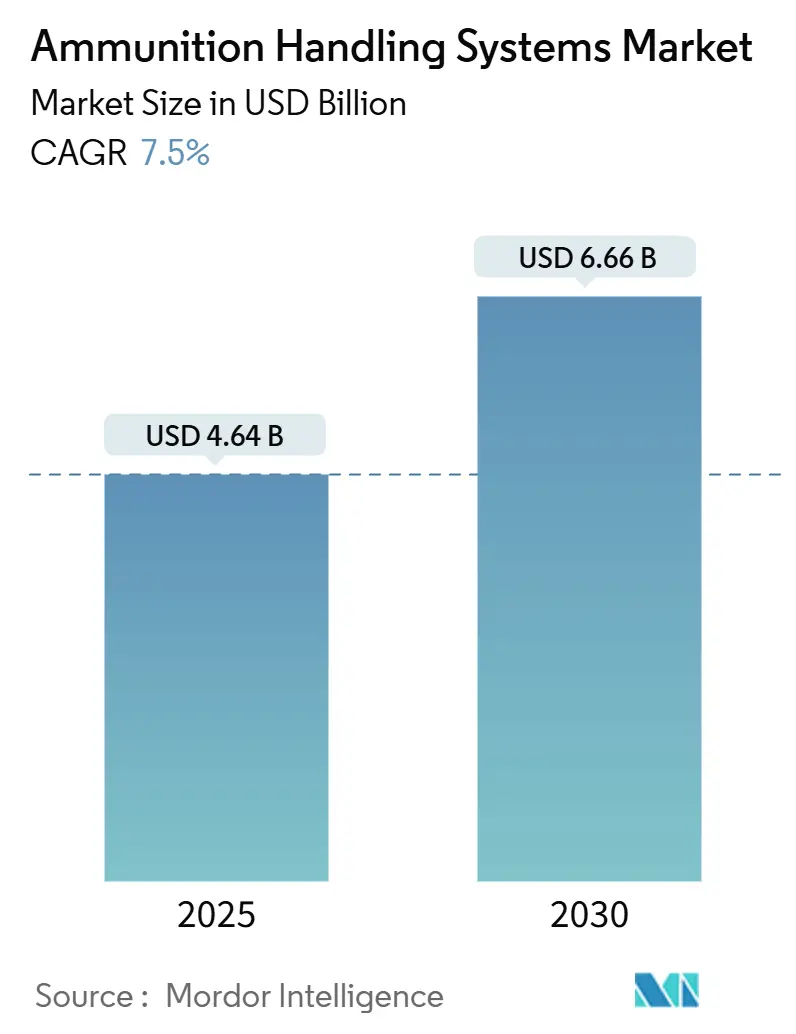

| Market Size (2025) | USD 4.64 Billion |

| Market Size (2030) | USD 6.66 Billion |

| Growth Rate (2025 - 2030) | 7.50% CAGR |

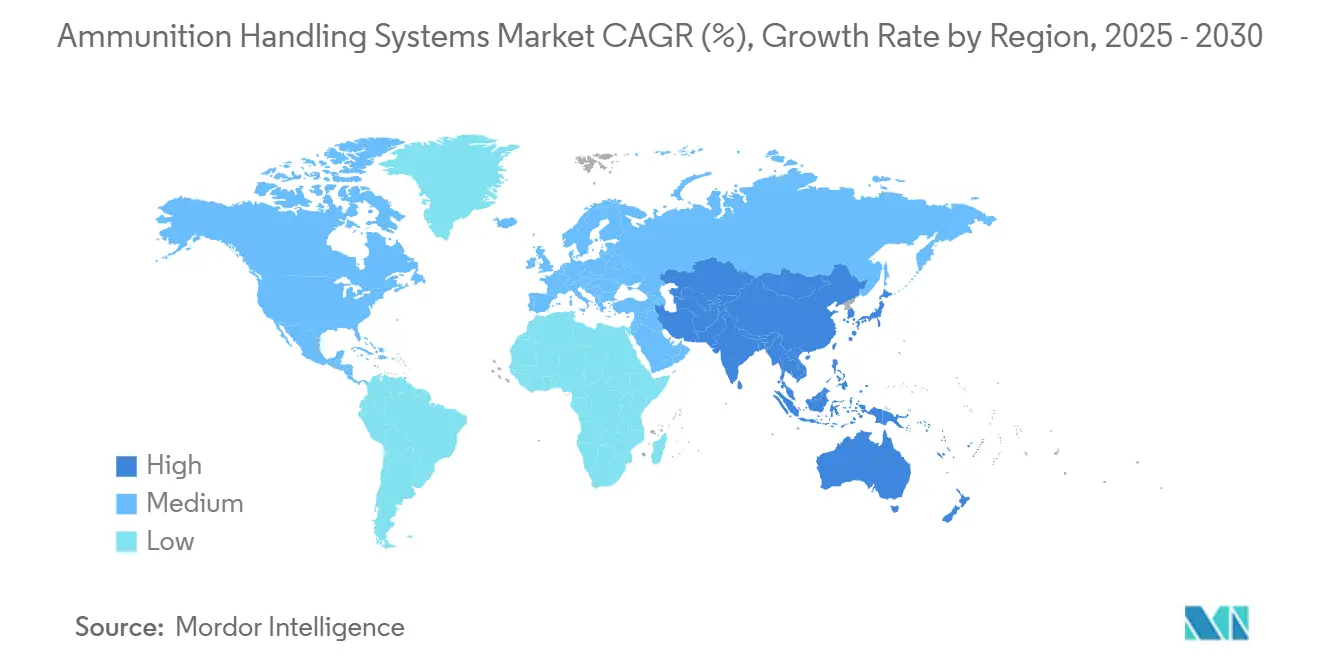

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ammunition Handling Systems Market Analysis by Mordor Intelligence

The ammunition handling systems market size stood at USD 4.64 billion in 2025 and is projected to reach USD 6.66 billion by 2030, advancing at a 7.50% CAGR over the forecast period. The three most influential factors underpinning the upward revenue trajectory are sustained increases in defense spending, urgent replacement of Cold–War–era platforms, and the shift toward servo-electric feeding architectures. Accelerated adoption of multi-caliber modular turrets, the spread of unmanned deck-mounted weapon stations, and the roll-out of innovative inventory-tracking software are reshaping technical baselines across land, naval, and airborne programs. Simultaneously, defense ministries insist on tighter through-life cost control, prompting OEMs to deliver lighter autoloaders, link-less magazines, and electric drive assemblies that trim fuel burn and scheduled maintenance. In parallel, supplier nations in North America and Europe are leveraging framework agreements to guarantee multi-year production runs. At the same time, Asia-Pacific customers press for industrial offsets that seed local assembly lines and nurture sovereign supply chains.

Key Report Takeaways

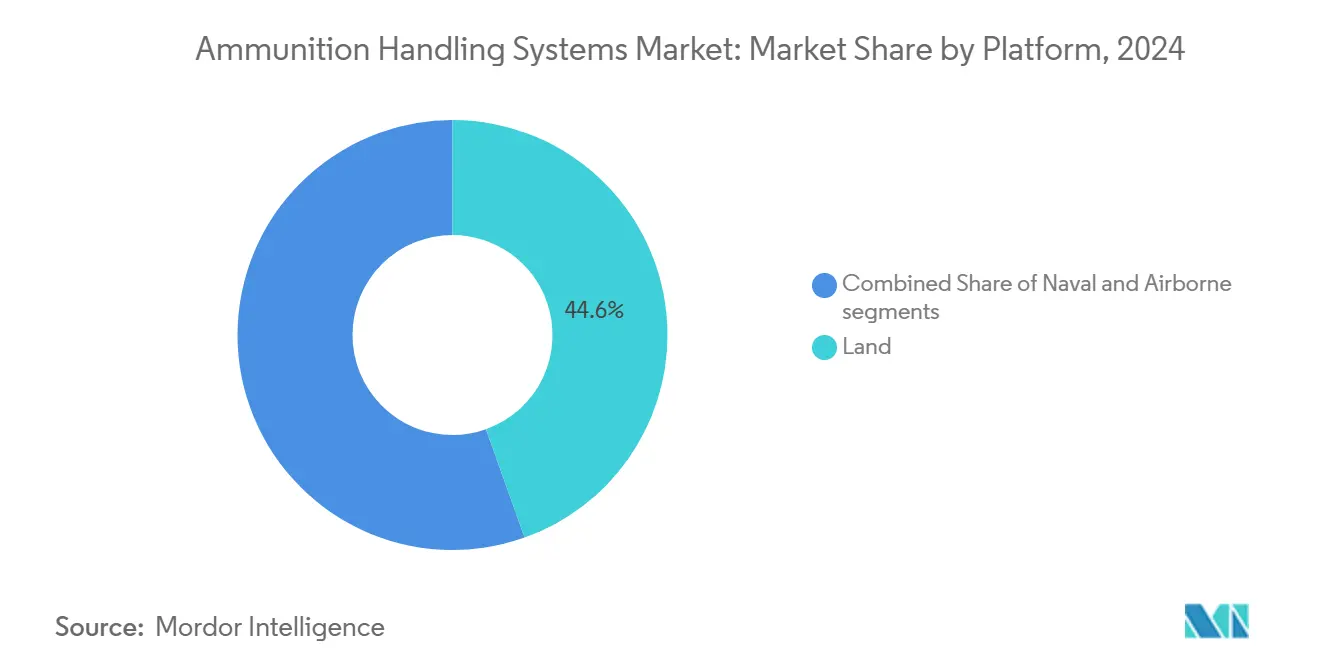

- By platform, land systems led with 44.56% revenue share in 2024; the airborne segment is forecasted to expand at a 9.21% CAGR through 2030.

- By weapon type, machine guns accounted for 31.78% of the ammunition handling systems market share in 2024, whereas Gatling guns posted the highest projected growth at 9.56% to 2030.

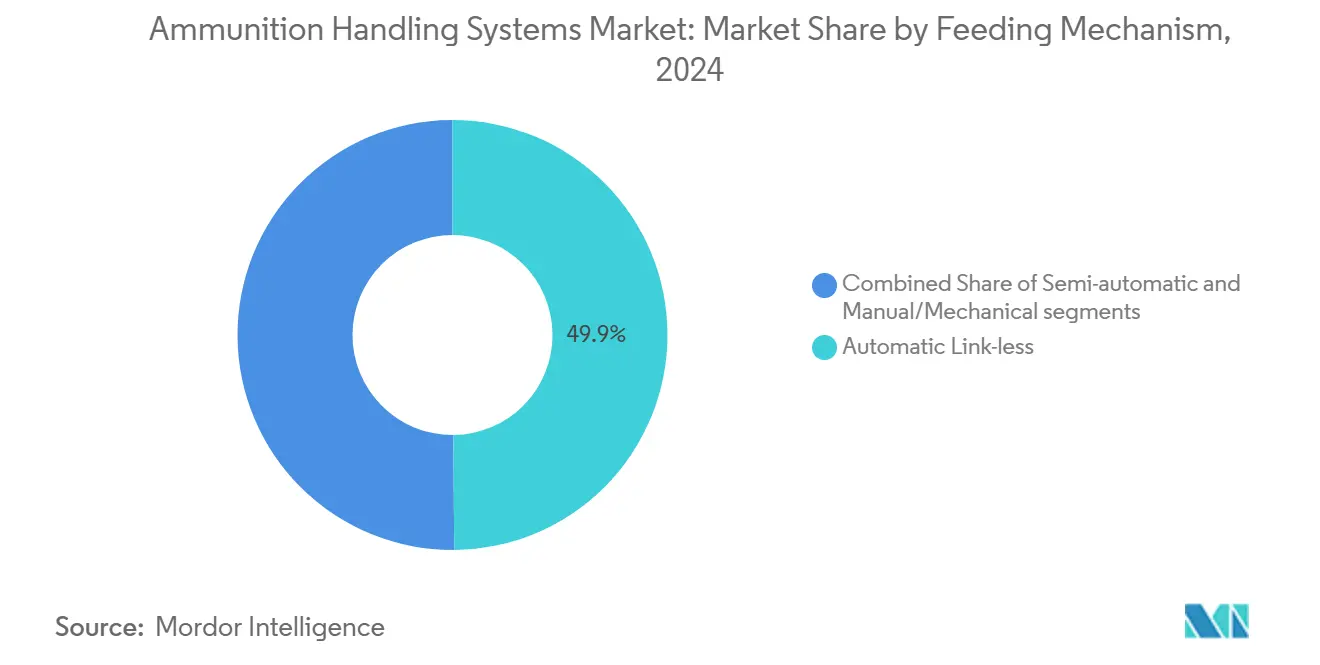

- By feeding mechanism, automatic link-less solutions captured 49.87% share of the ammunition handling systems market size in 2024 and are also advancing at a 9.12% CAGR.

- By component, loading systems commanded 35.64% of the ammunition handling systems market size in 2024, while auxiliary power units registered the fastest 8.78% CAGR.

- By end user, the military segment held 89.45% share in 2024 and continues to log the strongest 8.45% CAGR through 2030.

- By geography, North America commanded 37.65% of the market share in 2024, and Asia-Pacific recorded the highest 8.84% CAGR through 2030.

Global Ammunition Handling Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from next-generation combat vehicle programs | +1.1% | Global, early gains in North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Increased naval integration of unmanned deck-mounted remote weapon stations (RWS) | +0.9% | Global, especially APAC and Europe | Medium term (2–4 years) |

| Growing adoption of multi-caliber modular turret systems | +0.8% | North America and EU, expanding into APAC | Long term (≥ 4 years) |

| Shift from manual to servo-electric feed systems for cost and weight efficiency | +0.6% | Technologically advanced forces worldwide | Short term (≤ 2 years) |

| Expansion of smart munitions tracking and inventory management solutions | +0.5% | North America, Europe, gradually APAC | Medium term (2–4 years) |

| Defense offset policies promoting domestic automatic loader production | +0.4% | APAC core markets, MEA, selective EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand from next-generation combat vehicle programs

Platform developers are redesigning ammunition stowage around autoloaders that work with larger-caliber guns, telescoped rounds, and programmable fuses. The KF-51U Panther integrates twin rear magazines holding 25 proprietary 130 mm cartridges, a configuration that extends effective reach by 50% compared with legacy 120 mm tubes.[1]Rheinmetall AG, “KF-51U Panther Fact Sheet,” rheinmetall.com Similar design logic appears in the ASCALON 140 mm gun, where telescoped ammunition and a belt-less rammer cut barrel erosion and support rapid caliber swaps during mid-life upgrades.[2]KNDS Group, “ASCALON 140 mm Demonstrator Test Results,” knds-group.com These solutions decrease crew size, improve rate of fire, and harmonize with NATO interchangeability rules, making them a primary purchase argument for armies recapitalizing armored fleets. Emerging prototypes conform to ISO-9001 quality assurance and MIL-STD-1472 ergonomics, streamlining acceptance by multiple procurement agencies. These programs inject fresh volume into the ammunition handling systems market as nations lock in production slots for 2027–2032 deliveries.

Increased naval integration of unmanned deck-mounted remote weapon stations

Surface combatants now favor remotely operated turrets that combine day/night sensors, dual-feed mechanisms, and AI-supported fire control. The US Navy’s first Mk 38 Mod 4 installation demonstrates how autonomous loading drives higher on-station availability while reducing exposure of deck personnel. European yards follow suit with multipurpose launchers able to handle rockets, missiles, and loitering drones from containerized cells that share a 360-degree traverse ring. Remote weapon stations also migrate to offshore patrol vessels operated by Asia-Pacific customers that seek cost-effective counter-UAS capabilities. Fleet planners weigh these stations against legacy manually served guns, citing reduced crewing and faster target acquisition as decisive benefits. With global navies unveiling 30–50 new hulls yearly, the ammunition handling systems market gains a stable maritime revenue pillar.

Growing adoption of multi-caliber modular turret systems

Modular turrets enable rapid reconfiguration between 120 mm, 130 mm, and 140 mm barrels without redesigning the entire turret basket. Operators can tailor lethality to mission demands and futureproof vehicles against evolving armor threats. The technology relies on universal cradle interfaces, electric drives, and swing-in ammunition cassettes that accept smart rounds with airburst or top-attack profiles. Qualification testing in France, Germany, and South Korea validates robustness under NATO STANAG 4385 recoil limits, paving the way for serial production after 2027. Program offices appreciate the cost avoidance connected to mid-life growth paths, a dynamic that bolsters procurement arguments during budget cycles.

Shift from manual to servo-electric feed systems for cost and weight efficiency

Electric drives replace hydraulics in gun elevation, traverse, and ammunition rammer functions, trimming weight and maintenance hours. The US Army’s Paladin upgrade showcases a fully electric weapon control suite that aligns with MIL-STD-1275 power quality and interfaces seamlessly with digital fire-control computers. Suppliers highlight 25% lower life-cycle cost versus hydraulic alternatives, plus immunity to fluid leaks that complicate shipboard damage-control. These quantifiable gains accelerate the conversion of howitzers, turrets, and naval mounts, cementing a robust demand lane within the ammunition handling systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget reallocation toward cyber and space warfare capabilities | -0.6% | Advanced militaries worldwide | Medium term (2–4 years) |

| Complex retrofitting requirements for legacy military platforms | -0.5% | North America, Europe, some APAC fleets | Long term (≥ 4 years) |

| Export restrictions on high-capacity ammunition handling equipment | -0.4% | Global trade flows | Short term (≤ 2 years) |

| Thermal and electromagnetic interference challenges in electric drive magazines | -0.3% | Technologically advanced systems | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Budget reallocation toward cyber and space warfare capabilities

Defense planners in the United States and Europe are diverting incremental budget growth into artificial intelligence, satellite resilience, and cyber hygiene initiatives. Although top-line spending climbs, procurement officers juggle competing priorities, elongating award timelines for mechanical subsystems such as autoloaders. Contractors now present ammunition handling projects as enablers of data-centric battle management, stressing software-defined architectures to stay relevant. This recalibration tempers short-term revenue accrual yet reinforces the long-term imperative to fuse kinetic and digital effects inside a single fire-control loop.

Complex retrofitting requirements for legacy military platforms

Numerous howitzers, infantry vehicles, and naval mounts fielded during the 1980s require structural and electrical overhauls before accepting modern link-less magazines and electric rammers. The US Army’s 15-year organic-industrial-base plan underscores how multibillion-dollar depot upgrades precede widespread fleet refits.[3]US Army Materiel Command, “Organic Industrial Base Modernization Plan,” army.mil European arsenals face similar hurdles, prolonging the interim use of manual loaders. The retrofit burden—encompassing cabling, cooling, and cybersecurity hardening—subdues near-term shipment volumes, although it simultaneously generates a lucrative services backlog for engineering houses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Land Modernization Anchors Demand

The land segment generated 44.56% of the ammunition handling systems market, at USD 2.07 billion in 2024, underpinned by sustained main-battle-tank and self-propelled-artillery recapitalization programs. Newly built howitzers such as the M109A7 pair autoloaders with digital fire-control to achieve four-round volleys in under 60 seconds, a capability that attracts foreign military sales throughout NATO and APAC. Autoloader integration elevates the rate of fire while containing crew size at three, aligned with manpower-reduction directives. Supplier pipelines remain healthy through 2030 thanks to multiyear production options embedded in framework contracts.

Airborne platforms constitute the fastest-growing segment at 9.21% CAGR, propelled by expanded carriage of precision-guided munitions on manned fighters and remotely piloted aircraft. Link-less drum magazines feed 25 mm and 30 mm cannons on fifth-generation jets, leveraging composite housings that withstand high-g maneuvers without imposing weight penalties. Programs adopt MIL-STD-1760 data buses to share fuze-setting information between mission computers and gun control units, fostering ecosystem interoperability. Although absolute dollar volume trails land demand, the airborne sub-segment displays robust margins, reflecting stringent aerospace qualification requirements.

By Weapon Type: Machine-Gun Prevalence with Gatling Momentum

Machine guns dominated 2024 revenue by capturing 31.78% of the market, supported by almost universal installation on infantry fighting vehicles, patrol boats, and rotary-wing aircraft. Remote weapon stations featuring 12.7 mm or 7.62 mm belts employ dual-feed hoppers that enable instantaneous ammunition type changes, essential for escalation-of-force scenarios. Up-armoring projects in Eastern Europe and the Middle East keep replacement cycles brisk, while OEM upgrade kits introduce ceramic armor shielding around chutes and breech faces to enhance survivability.

Gatling guns exhibit the sharpest CAGR of 9.56% as militaries confront burgeoning drone swarms. Six-barrel 20 mm systems output 3,000 rounds per minute, demanding high-integrity link-less magazines to prevent feed starvation. Vendors respond with helical drum designs and brushless-motor actuation, shrinking time between cueing and first-round impact to sub-1-second benchmarks. Integration onto wheeled self-propelled anti-air platforms and littoral combat ships unlocks incremental addressable markets through at least 2030.

By Feeding Mechanism: Automatic Link-less Systems Lead Innovation

Automatic link-less solutions dominate the market by capturing 49.87% of market share and the highest growth curve of 9.12%, reflecting user preference for lighter ammunition packs, reduced mis-feed rates, and faster replenishment. Patented sprocket-type elevators stage rounds in plastic carriers, eliminating metallic disintegrating links that litter vehicle interiors and complicate egress. Sensors embedded along the feed path deliver round-count telemetry to the fire-control computer, enabling predictive resupply algorithms. Field feedback confirms 35% shorter reload cycles versus linked belts, a statistic that resonates with expeditionary units.

Semi-automatic and manual systems continue to equip training fleets and austere theaters with unreliable electrical power. However, adoption momentum heavily favors fully automatic architectures, particularly those compatible with adaptive-caliber turrets and advanced health-monitoring software. Suppliers diversify portfolios by offering drop-in conversion kits, smoothing the transition path for cost-sensitive customers.

By Component: Loading Systems Provide Structural Core

Loading systems—spanning vertical chain rammers, telescopic hydraulic pistons, and rotary breech auto-loaders—form the cornerstone of the ammunition handling systems industry. They attracted the most significant revenue slice due to their high unit selling price and criticality to platform performance. Tier-1 contractors couple mechanical loaders with ruggedized health-usage-monitoring sensors that log cycle counts and stress profiles, supporting condition-based maintenance regimes.

Auxiliary power units (APUs) experience the fastest growth of 8.78% CAGR as electrification spreads across turrets and naval mounts. High-density lithium-titanate batteries and low-RPM generators furnish steady current to drives, sensors, and data links while engines idle, satisfying stringent acoustic and thermal signatures. APUs also underpin silent-watch doctrines, granting crews extended surveillance periods without betraying position. Consequently, APU demand scales linearly with each new electric servo adoption.

By End User: Military Supremacy Sustains Volume

Military customers account for 89.45% of the market share and maintain the top CAGR of 8.45% because artillery, armor, and maritime branches face immediate readiness gaps. Framework contracts covering 155 mm modular charge plants and 130 mm smart-round facilities anchor predictable run-rates for prime contractors. Beyond Western alliances, India, Japan, and South Korea are broadening domestic production lines, often under licensed-manufacturing agreements that lock OEM technologies into sovereign supply chains.

Homeland security agencies and federal police forces generate modest revenue streams. Their purchases center on remote weapon stations for border vehicles and RFID-enabled armories that automate evidence-chain integrity. These contracts emphasize aftermarket software support and cyber accreditation rather than sheer mechanical throughput, differentiating them from core military procurement.

Geography Analysis

North America led the ammunition handling systems market with a 37.65% revenue share in 2024, anchored by multiyear US Army awards for Paladin self-propelled howitzers and medium-caliber cartridge production lines. Depot modernization under the Organic Industrial Base strategy injects fresh capital into machining centers, robotics, and quality-management software, lifting domestic absorption capacity. Canadian acquisition programs for 30 mm remote weapon stations and naval gun refits further contribute to regional momentum. Export compliance operates under International Traffic in Arms Regulations, yet allied reciprocity agreements smooth deliveries to NATO and AUKUS partners.

Europe occupies the second-largest position and remains a significant innovation hub, leveraging industrial collaboration among Germany, France, Spain, and Switzerland. Production of 155 mm artillery shells is scaling toward one million rounds annually by 2026, a benchmark that propels demand for modular charge loaders, logistics pallets, and remote quality inspections. The European Defence Fund co-finances R&D on servo-electric feed modules and cyber-secure turret controllers, underscoring Brussels’ objective to deepen technological sovereignty. While stringent environmental norms elevate compliance costs, they also spur OEMs to pioneer recyclable polymer cartridge cases and lead-free primers.

Asia-Pacific delivers the fastest regional CAGR at 8.84% through 2030. India’s Strategic Partnership model rewards bidders establishing local autoloader assembly, instructing at least 60% indigenous content in 10 years. South Korea continues to market its K9 Thunder howitzer and automated resupply-vehicle package across emerging economies, creating ripple demand for compatible feed modules. Japan funds next-generation naval gun research that prioritizes electromagnetic interference resilience, an attribute valuable to multinational naval coalitions. Across the region, defense ministries couple acquisition budgets with technology-transfer clauses, amplifying opportunities for subsystem suppliers conversant in offset frameworks.

Competitive Landscape

The industry displays moderate concentration: the five largest firms control most of global revenue, warranting sustained scrutiny from antitrust authorities, yet still leaving space for niche innovators. Prime contractors operate vertically integrated plants that machine barrels, cast metallic case segments, and assemble electronic controllers under one roof, driving scale efficiencies. Long-term performance-based logistics accords—covering 15–20 years of sustainment—create high switching costs for governments, reinforcing incumbency.

Strategic alliances between legacy manufacturers and software-defined-radio specialists herald a new wave of capability fusion. For example, turret builders now partner with cybersecurity startups to harden Ethernet backbones against malicious firmware injections. Simultaneously, additive-manufacturing bureaus capture pilot orders for titanium feed-tray subcomponents that shave 40% weight while preserving tensile strength. These partnerships compress design cycles and broaden solution catalogs, positioning participants to outmaneuver slower rivals.

White-space entrants concentrate on data-layer differentiation, offering API-ready inventory management suites that plug into enterprise resource planning systems. Their cloud-native architectures appeal to defense ministries determined to align ordnance depots with predictive-maintenance doctrines. While lacking metal-cutting heritage, these software vendors often secure minority stakes or memorandum-of-understanding portals with prime contractors seeking to modernize digital stacks. The competitive narrative thus revolves around an ecosystem where hardware robustness and software agility converge.

Ammunition Handling Systems Industry Leaders

BAE Systems plc

Moog Inc.

Leonardo S.p.A.

Curtiss-Wright Corporation

Rheinmetall AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BAE Systems received a SEK 600 million (USD 62 million) contract from Sweden's Defence Materiel Administration for BONUS precision-guided 155 mm munitions. The BONUS munitions target and destroy armored vehicles with precision at long range. This contract extends BAE's partnership with the Swedish Armed Forces and increases demand for ammunition handling systems that can manage advanced precision-guided artillery rounds.

- November 2023: BAE Systems plc secured a contract to supply multiple sets of Mk 45 Medium Caliber Gun systems and automated Ammunition Handling Systems (AHS) for the Hunter class frigates of the Royal Australian Navy.

Global Ammunition Handling Systems Market Report Scope

| Land |

| Naval |

| Airborne |

| Canons |

| Gatling Guns |

| Machine Guns |

| Main Guns |

| Launchers |

| Automatic Link-less |

| Semi-automatic |

| Manual/Mechanical |

| Loading Systems |

| Drive Assembly |

| Ammunition Storage Units |

| Auxiliary Power Units |

| Others |

| Military |

| Homeland Security and Law-Enforcement |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform | Land | ||

| Naval | |||

| Airborne | |||

| By Weapon Type | Canons | ||

| Gatling Guns | |||

| Machine Guns | |||

| Main Guns | |||

| Launchers | |||

| By Feeding Mechanism | Automatic Link-less | ||

| Semi-automatic | |||

| Manual/Mechanical | |||

| By Component | Loading Systems | ||

| Drive Assembly | |||

| Ammunition Storage Units | |||

| Auxiliary Power Units | |||

| Others | |||

| By End User | Military | ||

| Homeland Security and Law-Enforcement | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the ammunition handling systems market in 2025?

The market is valued at USD 4.64 billion in 2025 and is forecasted to reach USD 6.66 billion by 2030, registering a 7.50% CAGR.

Which platform generates the highest revenue?

Land-based platforms contribute the largest share, accounting for 44.56% of 2024 sales.

What feeding mechanism is gaining the most traction?

Automatic link-less solutions lead both in market share and growth, reflecting user demand for lighter, jam-resistant magazines.

Which region is growing the fastest?

Asia-Pacific posts the strongest 8.84% CAGR as India, Japan, and South Korea escalate procurement.

Why are servo-electric systems replacing hydraulics?

Electric drives lower maintenance, reduce weight, and integrate seamlessly with digital fire-control, resulting in life-cycle cost savings of roughly 25%.

Page last updated on: