Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

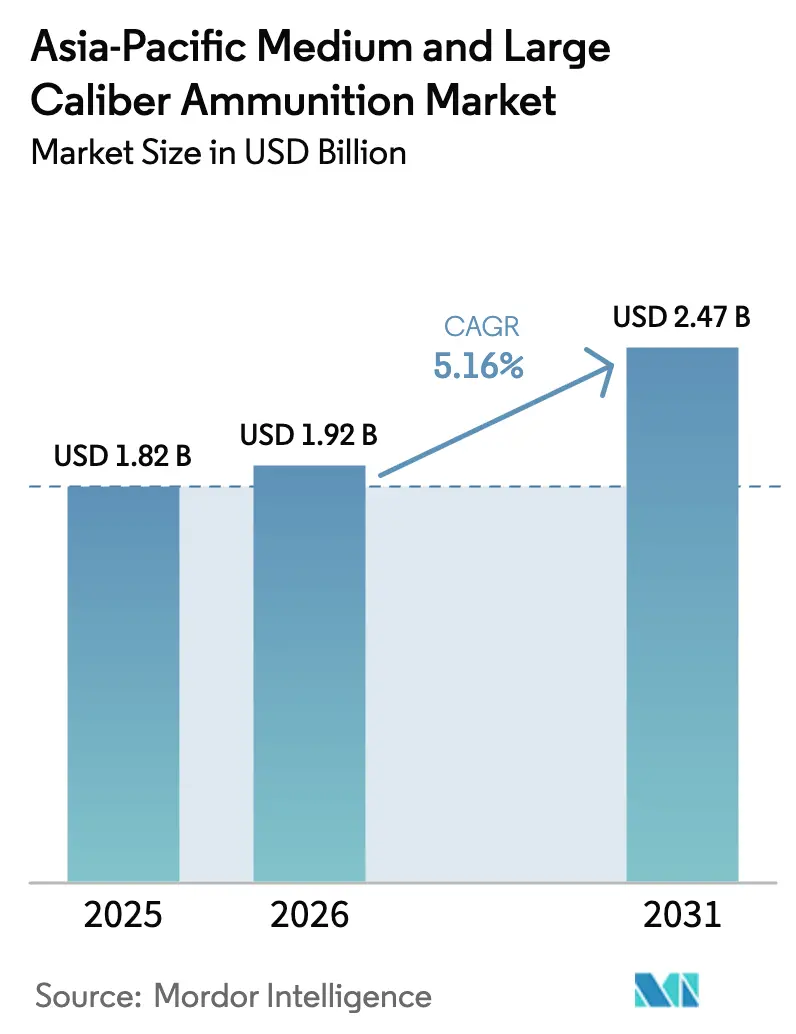

| Base Year Market Size (2025) | USD 1.82 Billion |

| Market Size (2026) | USD 1.92 Billion |

| Market Size (2031) | USD 2.47 Billion |

| Growth Rate (2026 - 2031) | 5.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Medium and Large Caliber Ammunition Market Analysis by Mordor Intelligence

The Asia-Pacific medium and large caliber ammunition market size is expected to grow from USD 1.82 billion in 2025 to USD 1.92 billion in 2026 and is forecasted to reach USD 2.47 billion by 2031 at a 5.16% CAGR over 2026-2031. This growth is driven by rearmament programs in countries such as Japan, Taiwan, India, and Australia, alongside initiatives to enhance domestic production capabilities, which reduce lead times and dependence on Foreign Military Sales (FMS) pipelines. Factors such as rapid naval modernization, the integration of AI-enabled fire-control systems, and insights from ammunition shortages in Ukraine are further boosting demand, particularly for 155mm artillery and 127mm naval rounds. However, rising copper and brass prices are increasing unit costs, while emerging investments in directed-energy systems pose a potential long-term challenge to substitution.

Key Report Takeaways

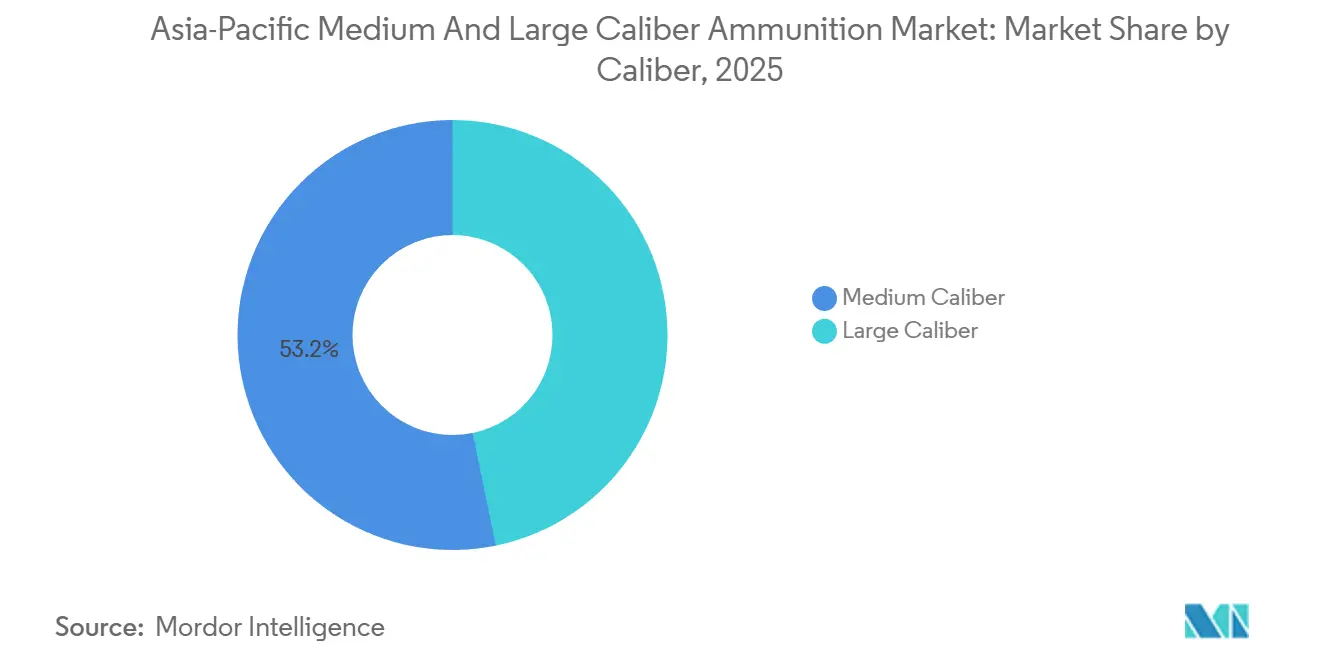

- By caliber, medium caliber led with 53.23% of the Asia-Pacific medium and large caliber ammunition market share in 2025, while large caliber is forecast to grow at a 6.55% CAGR through 2031.

- By product, artillery shells and mortars accounted for 38.95% of the Asia-Pacific medium and large caliber ammunition market in 2025; aerial bombs and grenades are projected to expand at a 6.04% CAGR through 2031.

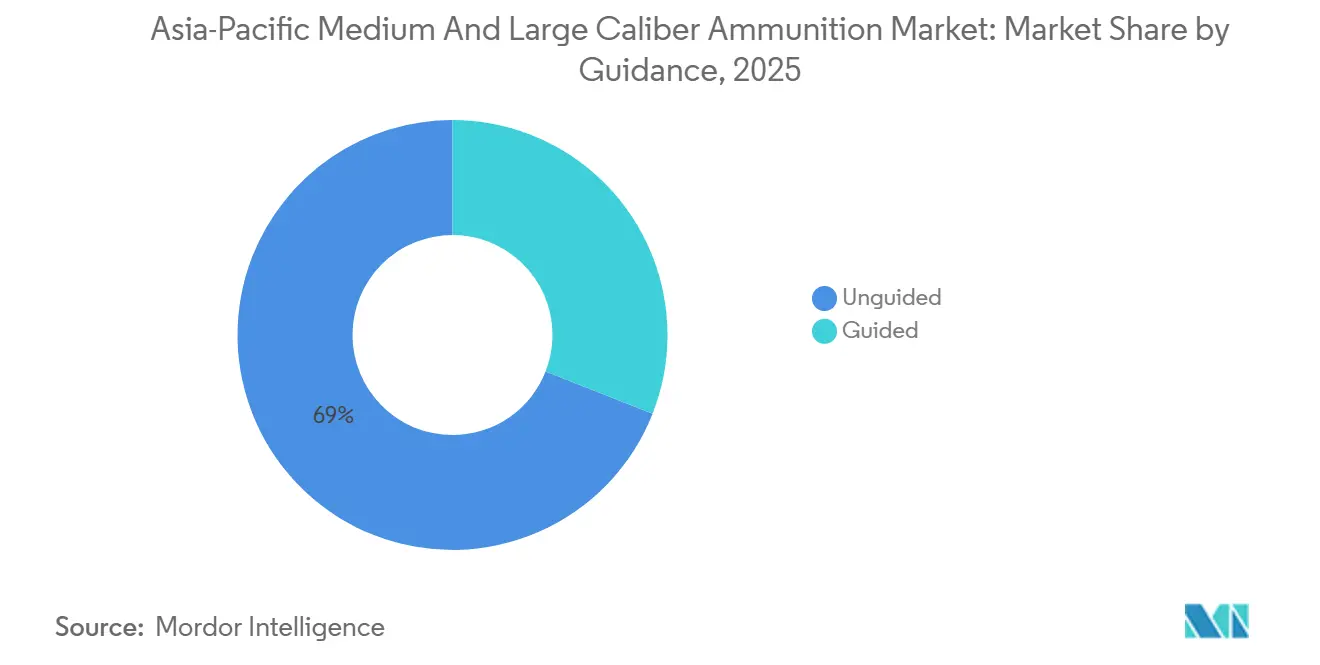

- By guidance, unguided rounds captured a 69.04% share in 2025, whereas guided munitions are forecast to grow at a 7.85% CAGR through 2031.

- By end-user, the military segment held an 86.95% share in 2025, while the law enforcement segment is projected to grow at a 6.01% CAGR through 2031.

- By platform, land systems represented 56.93% of 2025 revenue, yet airborne platforms are forecast to grow at a 6.58% CAGR through 2031.

- By geography, China accounted for 33.49% of regional spending in 2025, while India is projected to grow at a 6.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Medium and Large Caliber Ammunition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 2026+ rearmament cycles across Indo-Pacific defense forces | +1.20% | Japan, South Korea, Taiwan, Philippines, Australia | Medium term (2-4 years) |

| Surge in indigenous production and export hubs | +1.00% | India, South Korea, Australia, with export spill-over to Middle East and Southeast Asia | Long term (≥ 4 years) |

| Rapid naval modernization driving 76-127mm and 155mm naval rounds | +0.70% | China, India, Japan, South Korea, Australia | Medium term (2-4 years) |

| AI-enabled fire-control systems unlock demand for “Smart” shells | +0.60% | Global, with early adoption in India, South Korea, Japan | Long term (≥ 4 years) |

| Stockpile replenishment after Ukraine conflict lessons | +0.50% | Global, particularly Japan, South Korea, Australia | Short term (≤ 2 years) |

| Niche requirement for counter-UAV air-burst ammunition | +0.30% | India, South Korea, Taiwan, Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

2026+ Re-Armament Cycles Across Indo-Pacific Defence Forces

Tokyo's record USD 58 billion fiscal-2025 defense budget includes ammunition purchases equivalent to the combined total of the previous three years. This scale compels suppliers to secure copper and propellant contracts two years in advance to mitigate spot-market volatility. Taiwan's USD 11.1 billion FMS letter incorporates surge clauses that allow for quarterly call-offs, which enhance flexibility but complicate production scheduling for US prime contractors. South Korea increased its 155mm war-reserve target by 125,000 rounds for 2025, converting Poongsan's optional capacity expansion into committed throughput. The Philippines, an early-cycle participant, introduced 40% local-content requirements for ATMOS howitzer ammunition, prompting Israeli prime Elbit to collaborate with the government-owned Government Arsenal for filling operations. Across these nations, procurement activity is concentrated in 2026-2028, driving overtime shifts and forging-press utilization above 95% capacity. Post-2028, replenishment declines, but sustainment orders maintain baseline activity. This multi-year visibility supports a stable 1.2-point increase in the CAGR of the Asia-Pacific medium and large caliber ammunition market.

Surge in Indigenous Production and Export Hubs

India's Munitions India Limited (MIL) operates six hot-strip rolling lines for 155mm shell bodies and introduced automated ultrasonic flaw detection in 2025, resulting in a 30% reduction in rejection rates. Kalyani's NATO-grade exports demonstrated compliance with rigorous STANAG 4110 lot-acceptance standards, leading Poland to submit a follow-up inquiry for 25,000 rounds. South Korea's Poongsan doubled brass-case production and vertically integrated extrusion press maintenance to minimize downtime, a strategic response to elevated LME copper volatility. Australia's Thales-operated Benalla plant secured green power from a nearby solar farm, mitigating carbon-pricing penalties and reinforcing Canberra's industrial-sovereignty objectives. Collectively, these hubs reduce shipping times and ITAR-related risks, contributing a 1-point structural gain to the growth trajectory of the Asia-Pacific medium and large caliber ammunition market.

Rapid Naval Modernisation Driving 76-127mm and 155mm Rounds

Japan's Mogami-class frigates utilize 127mm Vulcano guided rounds, enabling land-attack missions traditionally reserved for cruise missiles. This shift alters fleet operational concepts and increases budgets for precision-guided munitions (PGMs). South Korea's KDX-III Batch II destroyers integrate 127mm guns with advanced fire-control radars, enhancing hit probability at ranges up to 100 km. Australia's Hunter-class project achieved 400-ton fuel savings by adopting lighter-weight 127mm rounds, driving recurring orders for low-drag base-bleed variants. China's Type 055 destroyers employ 130mm extended-range shells with base-bleed and rocket-assist options, sustaining domestic demand and supporting export variants for Pakistan. The Indian Navy, traditionally reliant on 76mm systems, is preparing a Request for Information (RFI) for 127mm systems to align with long-range surface-fire doctrines. This naval modernization is expected to contribute a 0.7-point increase to the Asia-Pacific medium and large caliber ammunition market CAGR through 2031.

AI-Enabled Fire-Control Systems Unlock Demand for “Smart” Shells

India's DRDO utilizes a digital twin of its 155mm projectile to simulate in-bore stress and external ballistics across 40,000 iterations, thereby reducing development time by eight months and enabling the production of sub-USD 10,000 smart shells. South Korea's K9 upgrade packages include on-weapon GPS antennae and encrypted Mil-GPS receivers, enabling course-correcting fuzes in flight and improving first-round effectiveness while reducing logistical demands. Japan's Ground Self-Defense Force (GSDF) integrates machine-learning algorithms in fire-direction centers to analyze weather, drone imagery, and historical dispersion data, dynamically selecting between unguided and guided shots for cost efficiency. Australia's Army is studying AI models to recommend the most cost-effective round mix for mission success, potentially saving USD 35 million in ammunition life-cycle costs over five years. These advancements compress the sensor-to-shooter loop from minutes to seconds, encouraging procurement of higher-cost smart shells while reducing overall quantities, resulting in a 0.6-point boost to market growth.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight ITAR-like export controls within Quad and EU | -0.40% | Global, with acute impact on US FMS recipients (Taiwan, Japan, Philippines) | Short term (≤ 2 years) |

| Persistent copper/brass cost inflation | -0.30% | Global, particularly affecting India, South Korea, Australia producers | Medium term (2-4 years) |

| Emerging directed-energy alternatives | -0.20% | US, Japan, South Korea, Australia | Long term (≥ 4 years) |

| Environmental push for lead-free formulations | -0.20% | Australia, Japan, South Korea, with EU-driven compliance spill-over | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tight ITAR-Like Export Controls Within Quad and EU

Australian project officers report an average wait of 270 days for US export licenses for forging dies used in 155mm shell production, necessitating interim reliance on legacy tooling. Taiwan's dependence on FMS has delayed shell deliveries, prompting discussions with India and South Korea for alternative supply chains. Japan eased its export regulations in 2025 but remains constrained by the ITAR for US-origin guidance kits, which delays the co-production of Excalibur rounds by at least 12 months. These export control challenges collectively reduce near-term CAGR by 0.4 points but simultaneously drive indigenous investments that offset the impact in the long term.

Persistent Copper/Brass Cost Inflation

Copper prices averaged USD 9,200 per ton in 2025, a 18% increase from 2023, significantly inflating the cost of brass cartridge cases, which constitute up to 40% of the total cost of a round.[1]London Metal Exchange, “Copper Prices,” lme.com Poongsan's margins declined by three points despite a nine-month forward-hedge program, highlighting the challenges of managing metal inflation. MIL renegotiated with India's Ministry of Defence to include an escalation clause tied to LME prices, passing through an 8% cost increase on 155mm shells. Australia's Benalla plant faced a 10% cost overrun, leading to a five-year copper supply agreement with BHP's Olympic Dam mine. Sustained input cost inflation reduces medium-term CAGR by 0.3 points, straining discretionary modernization budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Caliber: Firepower Shift Toward Heavy Tubes

Large caliber rounds accounted for 46.77% of 2025 revenue and are projected to grow at a 6.55% CAGR, potentially reaching parity with medium caliber by 2030. For instance, India’s ATAGS and Dhanush howitzers consume approximately 70,000 155mm shells annually during training, with guided upgrades significantly increasing the value per round.[2]Ordnance Factory Board, “155 mm Ammunition,” ofb.gov.in Additionally, Australia’s plan to deploy 75 M1A2 SEPv3 tanks necessitates an annual demand of around 18,000 120mm rounds, which were previously imported but will soon be produced domestically. This shift highlights the growing importance of local production capabilities in meeting the increasing demand for heavy-caliber ammunition.

Medium-caliber ammunition, ranging from 20mm to 57mm, supports infantry fighting vehicles, attack helicopters, and CIWS mounts. In 2025, the Directorate of Ordnance (Coordination & Services) supplied 2 million rounds of 30mm ammunition for the BMP-2 fleet, accounting for 12% of its annual ammunition revenue. However, the growing importance of networked fires and guided kits is driving the value of large-caliber ammunition, underscoring that future revenue splits will prioritize lethality over sheer volume in the Asia-Pacific medium- and large-caliber ammunition market. The shift toward guided and networked systems underscores the evolving nature of modern warfare and its impact on ammunition demand.

By Product: Programmable Munitions Garner Attention

Artillery shells and mortars accounted for 38.95% of total sales in 2025, with the Asia-Pacific medium and large caliber ammunition market for this category expected to grow steadily as military doctrines emphasize sustained fires. South Korea exported 800,000 155mm shells tied to K9 packages in 2025, demonstrating a production capacity capable of scaling up to meet NATO replenishment orders. This steady growth in artillery shells and mortars reflects the increasing reliance on sustained firepower in modern military strategies, particularly in regions with heightened geopolitical tensions.

Aerial bombs and grenades, though smaller in scale, are projected to achieve the fastest growth at a 6.04% CAGR. Taiwan’s deployment of 40mm programmable grenades at forward island garrisons highlights how niche counter-UAV requirements can evolve into significant procurement volumes. Additionally, India’s adoption of Rheinmetall’s AHEAD fuze in 35mm rounds establishes a recurring aftermarket for canister reloads, demonstrating how technology transfer fosters supplier dependency. Recoilless rifle ammunition, such as Saab’s Carl Gustaf 84mm rounds delivered to Australia, further diversifies revenue streams and provides a flexible procurement option unaffected by artillery barrel life cycles. These developments underscore the increasing significance of technological advancements and diversified product offerings in shaping the Asia-Pacific medium and large caliber ammunition market.

By Guidance: Precision’s Premium Gains Momentum

Unguided ammunition remains cost-effective for area denial, maintaining a 69.04% market share in 2025. However, the introduction of sub-USD 10,000 Indian smart shells may reduce price sensitivity and attract mid-tier users in Indonesia and Vietnam. This shift is gradually steering the Asia-Pacific medium and large caliber ammunition market toward guided munitions, although traditional high-volume ammunition will continue to play a significant role. The balance between cost-effectiveness and precision will continue to be a key factor influencing procurement decisions in the region.

Guided rounds are expected to grow at a 7.85% CAGR. For example, Japan’s purchase of 1,000 Excalibur shells in 2025 amounted to USD 120 million, equivalent to the value of 150,000 unguided M795 rounds. This significant investment in guided rounds highlights the premium placed on precision and efficiency in modern military operations.

By End-User: Military Demand Dominates but Para-Military Budgets Grow

Military organizations accounted for 86.95% of 2025 expenditure, supported by five-year capital budgets that shield procurement from short-term fiscal fluctuations. This stability in military spending ensures a consistent demand for ammunition, even during periods of economic uncertainty.

Law enforcement, with a forecasted 6.01% CAGR, is achieving incremental growth through United Nations peacekeeping reimbursements. These funds enable paramilitary units in countries like India and Thailand to enhance their firepower. For instance, India’s Central Reserve Police Force (CRPF) procured 12.7mm and 30mm rounds for armored vehicles in Kashmir, sustaining local production facilities during periods of reduced military orders. This parallel demand base enhances the resilience of the Asia-Pacific medium and large caliber ammunition market during cyclical downturns in defense spending. The growing role of paramilitary forces in maintaining internal security and participating in peacekeeping missions further underscores their importance as a key end-user segment.

By Platform: Airborne Arms Race Intensifies

Land platforms led the market, accounting for 56.93% of the 2025 revenue, driven by the need for artillery and tank resupply. For example, India’s Dhanush regiment allocates 180 live rounds per gun annually for training and operations. This consistent demand from land platforms highlights their critical role in sustaining the overall ammunition market.

Airborne platforms are expected to grow at a 6.58% CAGR as countries such as Australia, Japan, and India induct the AH-64E Apache helicopters, each equipped with a 30mm cannon that fires 300 rounds per sortie. Additionally, the increasing deployment of UCAVs, such as Wing Loong II and Bayraktar TB2, across Southeast Asia is boosting demand for lightweight 12.7mm belts and single-use 20mm pods. This trend is driving the Asia-Pacific medium and large caliber ammunition market toward sustained, sortie-driven replenishment cycles. The growing emphasis on airborne platforms reflects their strategic importance in modern military operations, particularly in regions with complex security challenges.

Geography Analysis

China accounted for 33.49% of 2025 revenue, benefiting from Norinco's vertically integrated supply chains, which helped maintain low per-unit costs.[3]Minnie Chan, “Norinco Expands Ammunition Production 2025,” South China Morning Post, scmp.com The country mitigated exposure to copper price fluctuations by utilizing its state reserves. While domestic R&D in guidance technology lags behind Western advancements, Beijing compensates by mass-producing unguided rounds, which are widely distributed to partner markets such as Pakistan and Myanmar. Additionally, the PLA Navy's 130mm extended-range shell program has driven demand for proprietary propellant blends, further strengthening domestic feedstock controls.

India is expected to achieve a 6.49% CAGR, the highest in the Asia-Pacific medium and large caliber ammunition market. This growth is supported by USD 1 billion in military orders and private-sector expansion initiatives. The DRDO's smart-shell program aims to address precision gaps while reducing dependency on US and European vendors, thereby curbing foreign currency outflows. Export credibility has improved following Kalyani's NATO sale, positioning India to fill supply gaps as traditional suppliers face ITAR-related restrictions.

Japan, South Korea, and Australia collectively contributed approximately 40% of regional revenue in 2025. Japan's cabinet-level focus on munitions stock transparency has accelerated delivery timelines. South Korea's Hanwha has established overseas production lines to mitigate currency risks and streamline logistics. Meanwhile, Australia's GWEO umbrella programs promote local manufacturing, aligning with its defense sovereignty objectives and potentially enabling exports to Pacific Island nations under security assistance agreements.

The rest of the Asia-Pacific region, including Thailand, Vietnam, Indonesia, and the Philippines, recorded mid-single-digit growth. Thailand's army is transitioning from legacy 105mm howitzers to M777s and ATMOS units, increasing demand for large-caliber ammunition. Vietnam continues to rely on Russian stockpiles but is exploring Indian and Korean suppliers for diversification. Indonesia's 15% increase in its ammunition budget supports purchases of 155mm and 30mm rounds for territorial defense. The Philippines utilizes US Foreign Military Financing to place rolling orders for 40mm grenades, ensuring smoother cash flow and reducing delivery risks.

Competitive Landscape

The Asia-Pacific medium and large caliber ammunition market is moderately fragmented, with competitive dynamics evolving steadily. Western companies continue to dominate the premium guided ammunition segment. For instance, BAE Systems manages the Excalibur program, Rheinmetall holds intellectual property for AHEAD programmable fuzes, and Thales specializes in base-bleed technology for 127mm naval rounds. Meanwhile, regional players are expanding their capabilities. MIL has introduced a new automated filling line capable of processing 5,000 shells daily, matching the production capacity of Western manufacturers. Hanwha's Australian joint venture is positioned to serve both domestic and export markets. At the same time, Poongsan leverages its surplus brass-case production to offer competitive pricing during periods of copper price volatility.

Key strategic efforts in the market focus on vertical integration and localization of intellectual property (IP). For example, Kalyani has licensed bottom-bore welding technology from German toolmaker KUKA, enabling the production of seamless shell bodies and reducing machine time by 18%. Poongsan has secured a 10-year copper ore offtake agreement with Rio Tinto, mitigating price fluctuation risks. Additionally, Thales' Benalla plant has transitioned to renewable energy sources to address potential carbon audits linked to export tenders. On the technological front, India's DRDO and Rheinmetall partnership has established local teams for fuze-logic development, enhancing upstream value capture.

The combined market share of the top five players is estimated at 50-55%, maintaining a balance in supply power. Buyers retain the ability to source from multiple suppliers, avoiding dependency on a single provider. However, incumbents continue to defend their market positions through faster certification processes and robust guided-round portfolios.

Asia-Pacific Medium and Large Caliber Ammunition Industry Leaders

BAE Systems plc

Munitions India Limited

Hanwha Corporation

Rheinmetall Denel Munition (Pty) Ltd. (Rheinmetall AG)

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Reliance Defence Ltd. and Düsseldorf-based Rheinmetall AG entered into a strategic partnership in the ammunition sector. The collaboration will involve Reliance supplying explosives and propellants for medium- and large-caliber ammunition to Rheinmetall.

- November 2024: The Australian government selected Thales as the preferred tenderer to establish a new domestic forging capability for 155mm M795 artillery ammunition. The 155mm M795 artillery ammunition, utilized for close-fire capabilities, is employed by Australia, the US, and other international allies in conjunction with the M777A2 light towed howitzer.

Asia-Pacific Medium and Large Caliber Ammunition Market Report Scope

Medium and large caliber ammunition includes cartridges, shells, and projectiles ranging from 20mm to 155mm. These are manufactured, filled, packaged, stockpiled, refurbished, or demilitarized for use in land, naval, and airborne weapon systems across the Asia-Pacific region. This market analysis encompasses the entire value chain, including forge-press case forming, fuze assembly, guidance kit integration, propellant loading, and final lot acceptance. It encompasses both new production rounds and activities related to reloading or disposal conducted by defense organizations and select paramilitary agencies in the region.

The Asia-Pacific medium and large caliber ammunition market is segmented by caliber, product type, guidance technology, end user, platform, and geography. By caliber, the market is categorized into medium caliber and large caliber. By product type, it is divided into rounds, artillery shells and mortars, and aerial bombs and grenades. Based on guidance technology, the market is segmented into guided and unguided ammunition. By end user, it is classified into military and law enforcement. By platform, it is segmented into land, naval, and airborne. The report also covers market sizes and forecasts for the Asia-Pacific medium and large caliber ammunition market in five countries across the region. For each segment, the market size is provided in terms of value (USD).

By Caliber

| Medium Caliber |

| Large Caliber |

By Product

| Rounds |

| Artillery Shells and Mortars |

| Aerial Bombs and Grenades |

By Guidance

| Guided |

| Unguided |

By End-User

| Military |

| Law Enforcement |

By Platform

| Land |

| Naval |

| Airborne |

By Geography

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Caliber | Medium Caliber |

| Large Caliber | |

| By Product | Rounds |

| Artillery Shells and Mortars | |

| Aerial Bombs and Grenades | |

| By Guidance | Guided |

| Unguided | |

| By End-User | Military |

| Law Enforcement | |

| By Platform | Land |

| Naval | |

| Airborne | |

| By Geography | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the forecast value for the Asia-Pacific medium and large caliber ammunition market in 2031?

The Asia-Pacific medium and large caliber ammunition market size is expected to grow from USD 1.82 billion in 2025 to USD 1.92 billion in 2026 and is forecasted to reach USD 2.47 billion by 2031 at a 5.16% CAGR over 2026-2031.

Which caliber category is accelerating fastest in Asia-Pacific?

Large caliber ammunition, fueled by 155 mm howitzer and 120 mm tank rounds, is expected to post a 6.55% CAGR through 2031.

Why are Asian militaries investing in guided 155 mm shells?

AI-enabled fire-control systems reduce rounds-per-target, making precision rounds economically viable despite high unit pricing.

How do ITAR restrictions influence regional supply chains?

Lengthy license approvals delay deliveries up to 18 months, prompting India, South Korea, and Australia to expand indigenous capacity.

Which country is the fastest-growing buyer of medium and large caliber ammunition?

India, supported by Atmanirbhar Bharat policies and new export wins, is forecasted at a 6.49% CAGR.

Are lasers a near-term threat to ammunition demand?

Directed-energy systems are entering niche roles like drone defense, but they only trim long-term growth by about 0.2 percentage points.

Page last updated on: