Xanthates Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

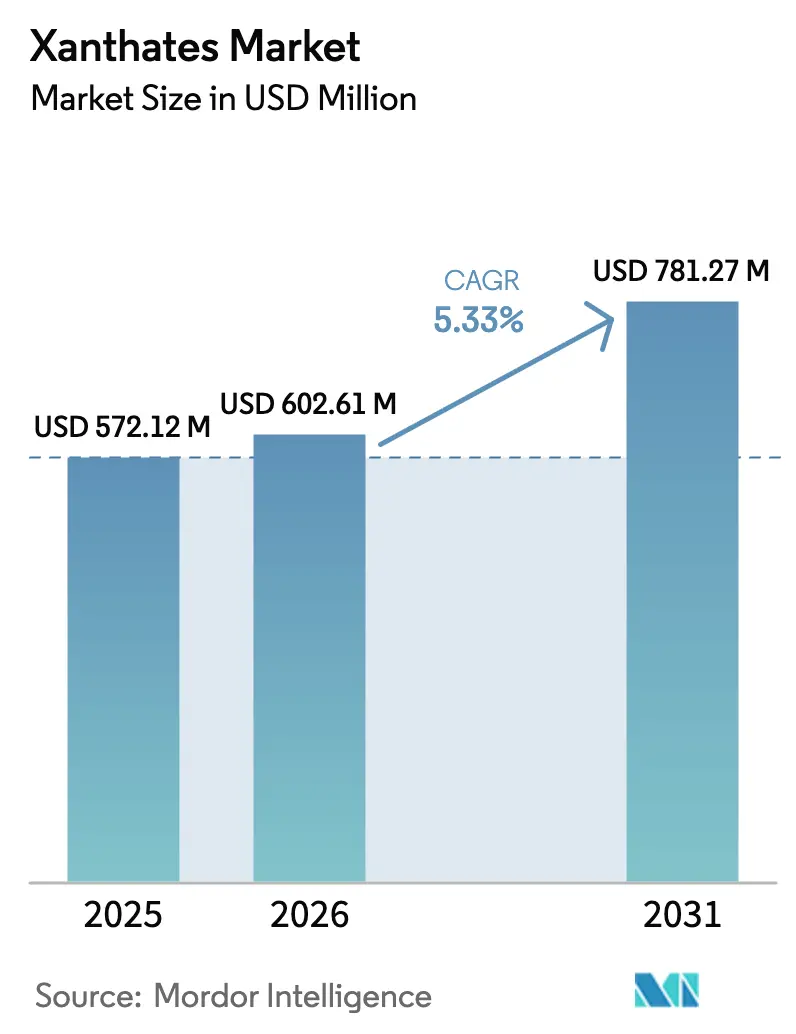

| Market Size (2026) | USD 602.61 Million |

| Market Size (2031) | USD 781.27 Million |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

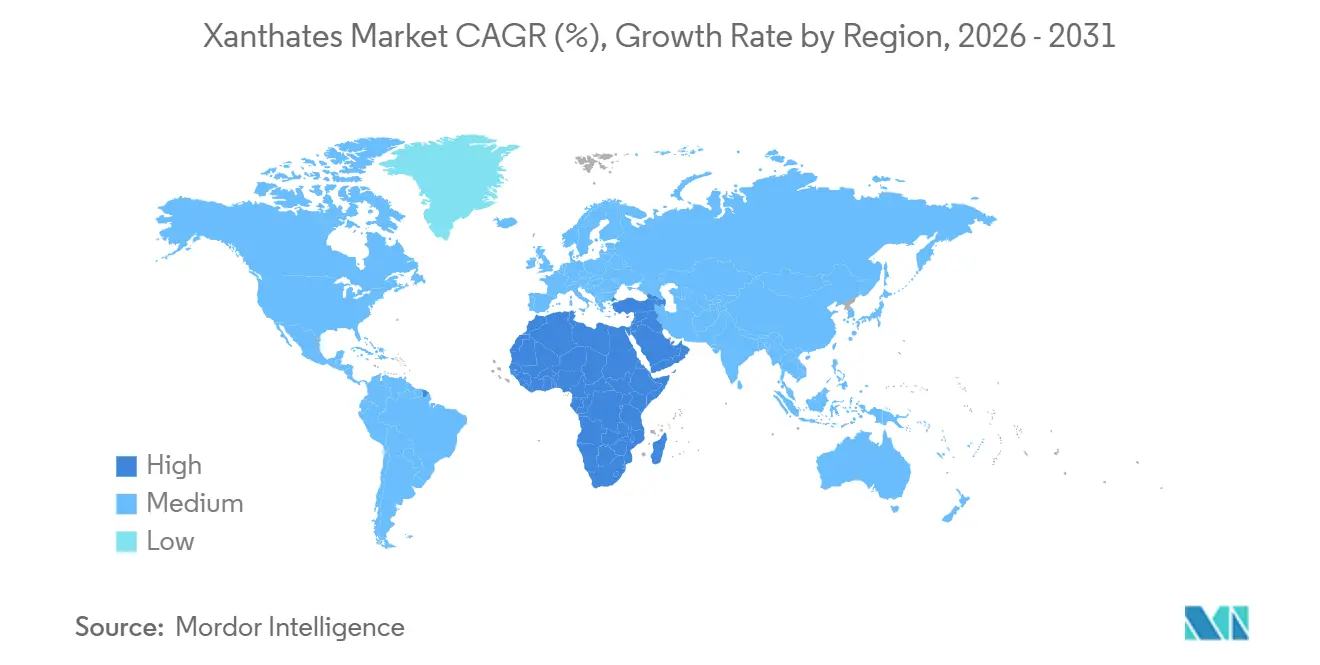

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

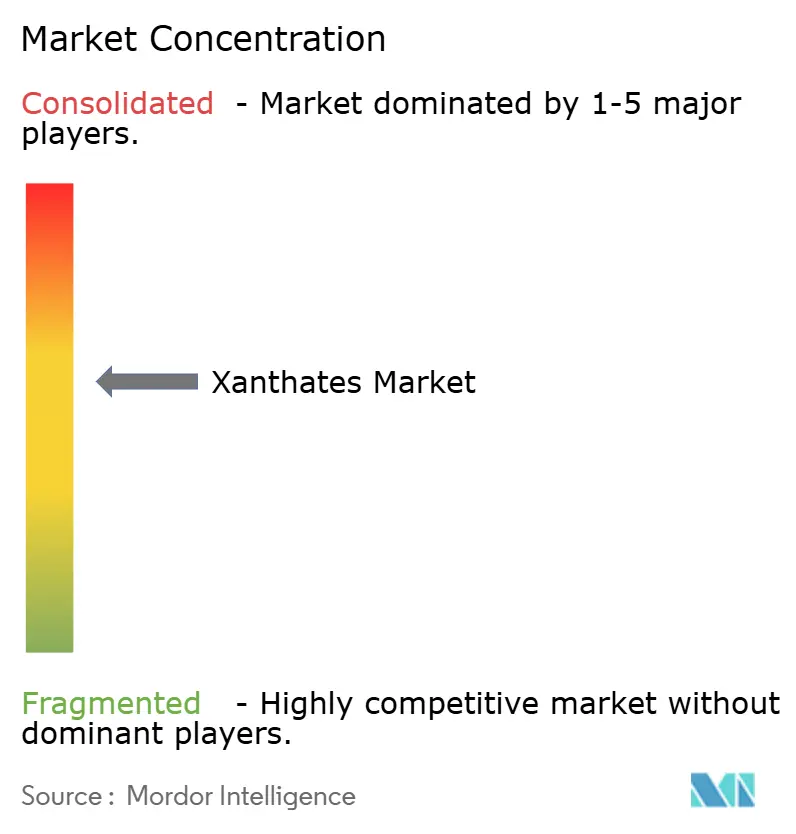

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Xanthates Market Analysis by Mordor Intelligence

The Xanthates Market size is projected to expand from USD 572.12 million in 2025 and USD 602.61 million in 2026 to USD 781.27 million by 2031, registering a CAGR of 5.33% between 2026 to 2031. Collector demand is surging in the Democratic Republic of Congo (DRC), Zambia, Chile, and Peru, driven by new flotation circuits for copper, cobalt, and lithium. These projects are pushing sulfide-ore throughput beyond historical levels. While the Asia-Pacific region continues to anchor consumption, the Middle-East is poised to outpace all others. This shift is evident as Congolese concentrators and Zambian smelter-feed operations expand their reagent budgets. Liquid xanthate formulations are becoming increasingly popular. They mitigate dust-handling risks and reduce carbon-disulfide (CS₂) off-gassing. This trend aligns with the United States and European Union's stringent limits on occupational exposure and tailings water. Concurrently, artificial-intelligence (AI) dosing platforms are boosting overall collector consumption. They achieve this by maximizing net present value from lower-grade stockpiles, even as the intensity of reagents per tonne decreases.

Key Report Takeaways

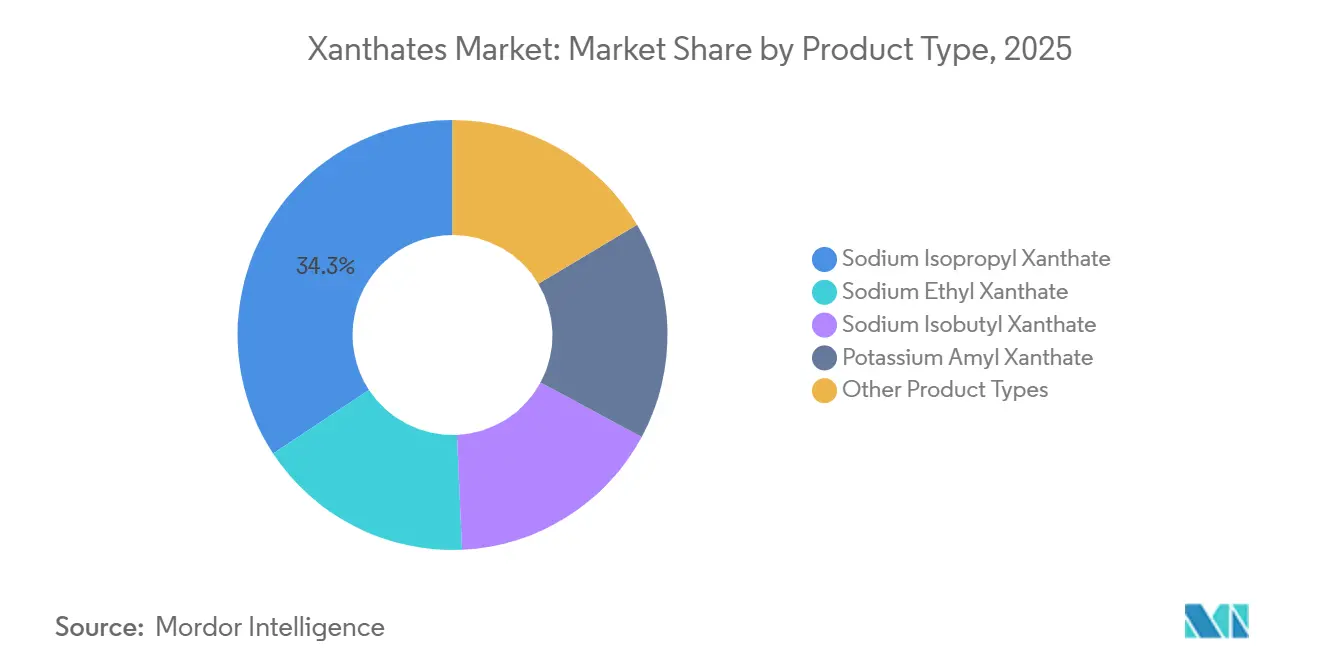

- By product type, sodium isopropyl xanthate led with 34.28% of the xanthates market share in 2025, while potassium amyl xanthate is projected to expand at a 6.18% CAGR (2026-2031).

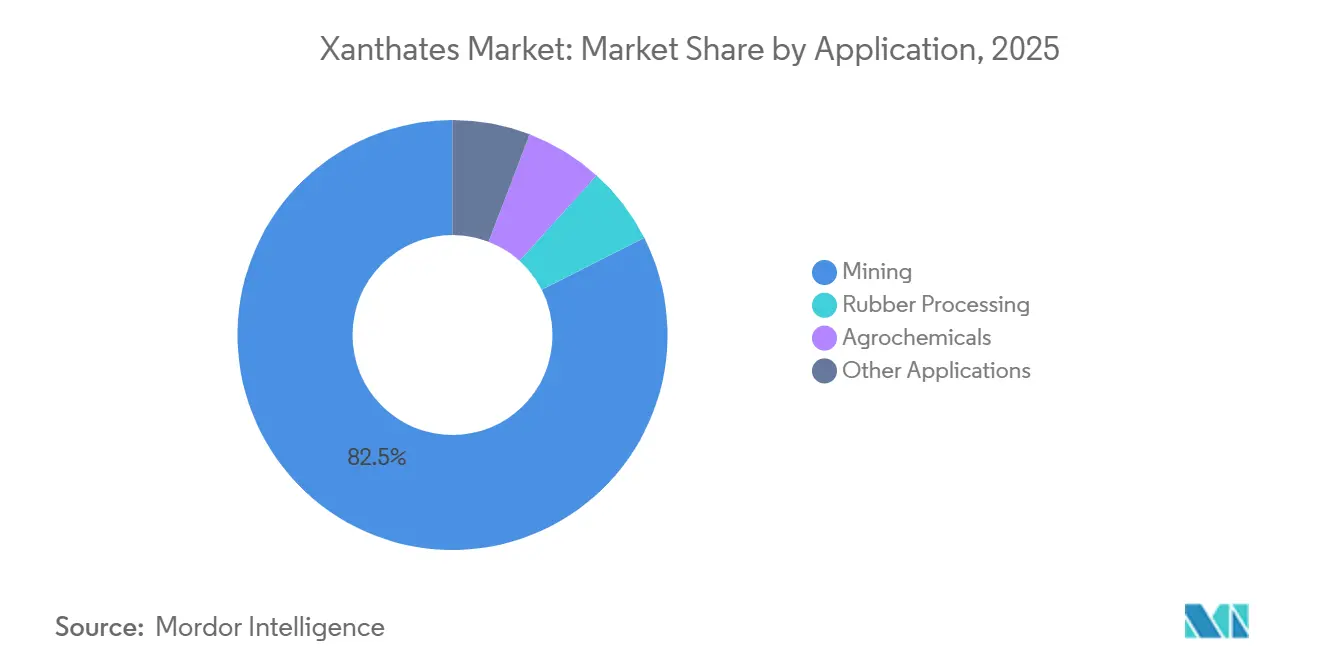

- By application, mining accounted for 82.47% of the xanthates market size in 2025, and agrochemicals are advancing at a 6.24% CAGR (2026-2031).

- By geography, Asia-Pacific led with 46.38% of the xanthates market share in 2025, while the Middle-East and Africa are projected to expand at a 5.93% CAGR (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Xanthates Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming critical-minerals projects in Africa and Latin America | +1.8% | Sub-Saharan Africa (DRC, Zambia, South Africa), Andean corridor (Chile, Peru, Argentina), spill-over to Brazil | Medium term (2-4 years) |

| Shift to liquid xanthate logistics at remote mines | +0.9% | Global, with early gains in Atacama Desert (Chile), Pilbara (Australia), northern Canada, high-altitude Peru | Short term (≤ 2 years) |

| AI-optimised reagent dosing boosting collector consumption | +1.2% | North America, Europe, APAC core (China, Australia), early adoption in South Africa | Medium term (2-4 years) |

| Surge in alkaline battery recycling requiring xanthate leaching aids | +0.6% | APAC (China, South Korea, Japan), spill-over to EU and North America | Long term (≥ 4 years) |

| Tightening Asia-Pacific supply of carbon-disulfide feedstock inflates prices | +0.7% | Asia-Pacific (China, India, Southeast Asia), indirect impact on global pricing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Booming Critical-Minerals Projects in Africa and Latin America

In 2025, Ivanhoe Mines' Kamoa-Kakula complex in the DRC achieved an annualized copper output. By 2027, the complex is set to roll out a Phase 3 concentrator, which is expected to increase the demand for sodium isopropyl xanthate. Simultaneously, capacity expansions at Chile's Centinela and Quebrada Blanca Phase 2, along with Argentina's PSJ Cobre Mendocino development, are projected to collectively augment copper-concentrate output by 2027. This growth is anticipated to drive new collector offtake during the forecast period of 2026–2031. With these advancements, the Andean-Corridor and the Central-African Copperbelt are solidifying their positions as leading players in the xanthates market.

Shift to Liquid Xanthate Logistics at Remote Mines

Clariant's HOSTAFLOT liquid grades have streamlined operations by eliminating the need for on-site dissolution tanks and reducing reagent preparation time[1]Clariant, “HOSTAFLOT Liquid Collectors,” clariant.com. These advantages have been realized at lithium brine operations in Chile and iron ore sites in Australia. In Peru's high-Andes copper belt, both Antamina and Las Bambas reported a notable drop in reagent-handling incidents after transitioning to pre-dissolved sodium isopropyl xanthate. Furthermore, these liquid collectors, by curbing CS₂ volatilization, help mines comply with the European Union's stringent cap of 50 mg/m³, and OSHA's average limit of 20 ppm over time. This regulatory push is catalyzing a rapid shift in the product mix toward liquid solutions.

AI-Optimized Reagent Dosing Boosting Collector Consumption

By 2025, Syensqo's SmartFloat platform, which recalibrates dosing every 15 minutes, improved metal recovery at a platinum concentrator in South Africa[2]Syensqo, “SmartFloat AI Dosing Platform,” syensqo.com. This enhancement enabled the profitable treatment of lower-grade stockpiles, leading to an overall increase in reagent volume, even as per-tonne usage decreased. Meanwhile, Draslovka's MetOptima controller supported an increase in annual xanthate purchases, coinciding with a throughput expansion at a copper mine in Chile. Such data-driven strategies not only prioritize higher-purity grades and tailored blends but also underscore the trend of premiumization in the xanthates market.

Surge in Alkaline Battery Recycling Requiring Xanthate Leaching Aids

In 2025, the Ministry of Industry and Information Technology in China set a goal to gather a substantial share of spent alkaline batteries. This initiative led to an increase in hydrometallurgical capacities, utilizing sodium-ethyl xanthate to enhance the zinc dissolution rates. In the same year, South Korea processed a significant volume of cells, leveraging sodium-ethyl xanthate per tonne of feedstock to optimize the leach kinetics. Although a minor segment, this niche grew at twice the pace of traditional mining demand during the forecast period of 2026–2031, broadening the xanthates market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commercialisation of ligand-based xanthate-free collectors | -1.1% | Global, led by Chile, Australia, Canada pilot deployments, spreading to Europe and North America | Medium term (2-4 years) |

| EU tailings directive lowering allowable CS₂ emissions | -0.7% | European Union member states, United Kingdom, with compliance pressure extending to candidate countries (Serbia, North Macedonia) | Short term (≤ 2 years) |

| On-site CS₂ cracking units enabling captive collector synthesis | -0.5% | Chile, Peru, Australia (large-scale copper operations), emerging interest in DRC and Zambia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commercialisation of Ligand-Based Xanthate-Free Collectors

In Chilean pilot trials, Solvay’s Aero MX 5004 thionocarbamate outperformed sodium isopropyl xanthate, achieving higher copper recovery. Additionally, it successfully reduced tailings CS₂ levels to below the permissible limit, adhering to the DS 90 water-quality standard. Meanwhile, in 2025, BASF’s Lupromin-D hydroxamates enabled a nickel mine in the Philippines to completely eliminate xanthate from its oxide circuits. With dosing levels significantly reduced compared to conventional methods and a decrease in waste-treatment costs, the mine realized notable operating savings. This is particularly significant in regions with stringent emissions regulations, which in turn curtail the long-term growth of the xanthates market.

EU Tailings Directive Lowering Allowable CS₂ Emissions

By December 2026, the 2024 revision of the Extractive Waste Directive mandates a cap of 50 mg/m³ CS₂ for closed-loop water systems. Germany and France are expected to impose significant penalties for any violations. Boliden, a Swedish company, is investing in retrofitting its Aitik mine and discontinuing powder grades. Additionally, Sirius Minerals' Woodsmith project, secured in its 2025 permit, has opted for fatty-acid collectors. This decision indicates a potential decline in the future European demand for powder xanthates during the forecast period of 2026–2031.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Isopropyl Dominance Faces Amyl Disruption

In 2025, sodium isopropyl xanthate commanded a 34.28% share of the xanthates market, driven by its superior selectivity in copper-pyrite separation and a strong presence in porphyry deposits. This leading grade forms the backbone of premium blended-collector systems, achieving recovery gains over sodium-ethyl counterparts. Potassium amyl xanthate has emerged as the fastest-growing player, boasting a 6.18% CAGR through 2031. Its edge comes from a stronger adsorption on fine-grained sulfides, particularly in refractory gold and intricate polymetallic ores. Sodium isobutyl xanthate remains a favored choice in lead-zinc flowsheets, notably in Australia’s Broken Hill and China’s Yunnan Province. Its mid-chain length strikes an ideal balance between power and selectivity. Meanwhile, sodium ethyl xanthate, despite its cost-effectiveness, is losing traction in premium copper and gold circuits. These circuits are now leaning toward stricter CS₂ limits and enhanced metallurgical performance.

Potassium salts are gaining traction in the xanthates market, primarily due to their heightened solubility. This attribute reduces handling volumes, a significant logistical advantage for remote mining sites in Africa and Australia. Another burgeoning segment is blended formulations. For instance, a 60:40 mix of isopropyl and amyl xanthate boosted combined copper-zinc recovery at a Peruvian polymetallic mine in 2025. This success underscores suppliers' momentum toward tailored pre-mixes. Such developments indicate that innovations focusing on chain length, solubility, and blending techniques will reshape the competitive landscape of the xanthates market.

By Application: Mining Hegemony Masks Agrochemical Momentum

In 2025, mining, leveraging the indispensable role of collectors in over 1,200 active sulfide concentrators worldwide, commanded a dominant 82.47% share of the xanthates market. Within the mining sector, copper flotation took the lead, followed by gold, lead-zinc, and nickel-cobalt. Rubber processing secured the second position, employing zinc xanthates and sodium isobutyl grades as low-temperature vulcanization accelerators, which are vital for automotive seals and components in electric vehicles.

Agrochemicals, while currently holding a modest market share, are projected to expand at a compound annual growth rate (CAGR) of 6.24% during the forecast period of 2026–2031. Regulatory efforts to phase out persistent chelants have heightened the appeal of xanthates, particularly in biodegradable soil-remediation sprays and controlled-release fertilizers. Pilot projects in China and the European Union demonstrated that xanthate coatings, when compared to urea-only systems, reduced nutrient run-off and increased tonnage. Beyond these primary sectors, niche applications such as paper-recycling flotation aids and pharmaceutical intermediates account for a minor segment of the overall xanthates market.

Geography Analysis

In 2025, the Asia-Pacific region led the market, capturing 46.38% of total revenue. China's integrated clusters, with their robust xanthate capacity, primarily fueled exports to neighboring nations such as Indonesia, Vietnam, and the Philippines. In India, demand surged due to expansions at Hindustan Zinc’s Rampura Agucha and Coal India’s fine-coal flotation projects, resulting in increased collector offtake. Australia emerged as a self-sufficient sub-market, with BHP and Rio Tinto predominantly sourcing liquid xanthates from Orica and Coogee Chemicals. This strategic choice aimed to mitigate hazards in their operations located in Pilbara and Queensland.

While the Middle-East and Africa held a smaller market share, they boasted the fastest projected CAGR of 5.93% during the forecast period of 2026–2031. This growth was fueled by expansions at DRC’s Kamoa-Kakula and Zambia’s Kansanshi and Enterprise, which anticipated a heightened demand for collectors by 2028. In South Africa, Bushveld's platinum group augmented xanthate dosages via column flotation to compensate for reduced mechanical agitation. Simultaneously, Saudi Arabia's Ma’aden phosphate operations shifted from gravity methods to xanthate-assisted flotation, diversifying the regional reagent landscape.

North America made a significant contribution to the 2025 revenue, driven by projects in Arizona and Utah (copper and molybdenum), Ontario (gold), and zinc operations in Alaska and the Yukon. Europe experienced stagnation; while mine closures in Poland and Finland balanced out the baseline usage, new ventures like Woodsmith avoided xanthates to evade CS₂ issues. South America, with a substantial market share, witnessed Codelco's widespread xanthate consumption across its divisions. The company is considering a strategic shift, aiming to substitute a segment of its sodium isopropyl volumes with Aero MX thionocarbamates starting in 2026, in line with its Scope 3 objectives. Additionally, persistent infrastructure challenges, notably the Copperbelt rail bottlenecks, elevated freight premiums and ignited interest in on-site synthesis. If this method gains traction, it holds the potential to diminish merchant volume.

Competitive Landscape

The xanthates market is moderately consolidated. However, this landscape still offers regional players opportunities in logistics-sensitive niches. While Chinese producers leverage unit-price discounts to dominate Southeast Asia's nickel laterite market and capture a significant share of African copper tenders, they face increasing compliance challenges in the European Union and the United States, primarily due to their powder-centric portfolios. On-site synthesis is poised to be a game-changer. Industry leaders in Chile are considering CS₂ plants, a move that could disrupt a significant portion of global merchant volumes by 2030. However, this ambition depends on securing capital expenditures and meeting regulatory approvals. In response, suppliers are increasing liquid capacity, investing in hybrid collector research and development, and integrating AI technologies. These efforts align with the xanthates industry's shift towards stricter environmental, safety, and digital-performance standards.

Xanthates Industry Leaders

SNF Group

Amruta Industries

Orica Limited

Charles Tennant & Company

QiXia TongDa Flotation Reagent Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Kemcore is setting up a new chemical manufacturing facility in Palapye, Botswana, to locally produce essential mining reagents, including xanthates. This initiative aims to reduce dependency on imports and streamline regional supply chains. Production is expected to begin in 2027.

- February 2024: Orica’s acquisition of Cyanco, a major sodium cyanide producer, is expected to impact the Xanthates market by enhancing Orica’s Mining Chemicals business. This expansion will double production capacity, strengthen the global supply network, and improve service to gold mining industries in North America and other key regions.

Global Xanthates Market Report Scope

Xanthates are a group of chemicals used in the mining industry for the flotation and processing of sulfide and metallic ores. They are commonly used in combination with formulations of dithiophosphates to improve yield, concentrate quality, and flotation rate. It separates as foam and settles out.

The xanthates market is segmented by product type, application, and geography. By product type, the market is segmented into Sodium Ethyl Xanthate, Sodium Isopropyl Xanthate, Sodium Isobutyl Xanthate, Potassium Amyl Xanthate, and Other Product Types. By application, the market is segmented into Mining, Rubber Processing, Agrochemicals, and Other Applications. The report also covers the market size and forecasts for the market in 15 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| Sodium Ethyl Xanthate |

| Sodium Isopropyl Xanthate |

| Sodium Isobutyl Xanthate |

| Potassium Amyl Xanthate |

| Other Product Types |

| Mining |

| Rubber Processing |

| Agrochemicals |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Sodium Ethyl Xanthate | |

| Sodium Isopropyl Xanthate | ||

| Sodium Isobutyl Xanthate | ||

| Potassium Amyl Xanthate | ||

| Other Product Types | ||

| By Application | Mining | |

| Rubber Processing | ||

| Agrochemicals | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current global demand for the xanthates market and its expected growth by 2031?

Demand is forecast to rise from USD 602.61 million in 2026 to USD 781.27 million by 2031, reflecting a 5.33% CAGR.

Which product type is gaining the most traction for refractory gold ores?

Potassium amyl xanthate is projected to grow at a 6.18% CAGR to 2031 because its longer carbon chain delivers stronger adsorption on fine-grained sulfides.

Why are liquid xanthate formulations displacing powders?

Liquids eliminate dust-explosion hazards, slash reagent-prep time 40%, and help mines meet strict CS₂ emission caps enforced by OSHA and the European Union.

What drives the rapid uptake of AI dosing platforms?

Systems such as SmartFloat and MetOptima fine-tune reagent addition in real time, boosting metal recovery and justifying expanded flotation throughput, which ultimately lifts total xanthate purchases.

How might on-site CS₂ cracking units alter supply dynamics?

If capital and permitting hurdles are overcome, captive CS₂ plants could reduce delivered costs significantly, potentially diminishing merchant xanthate volumes by a notable margin by 2030.

Page last updated on: