Isosorbide Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.74 Billion |

| Market Size (2031) | USD 1.07 Billion |

| Growth Rate (2026 - 2031) | 7.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

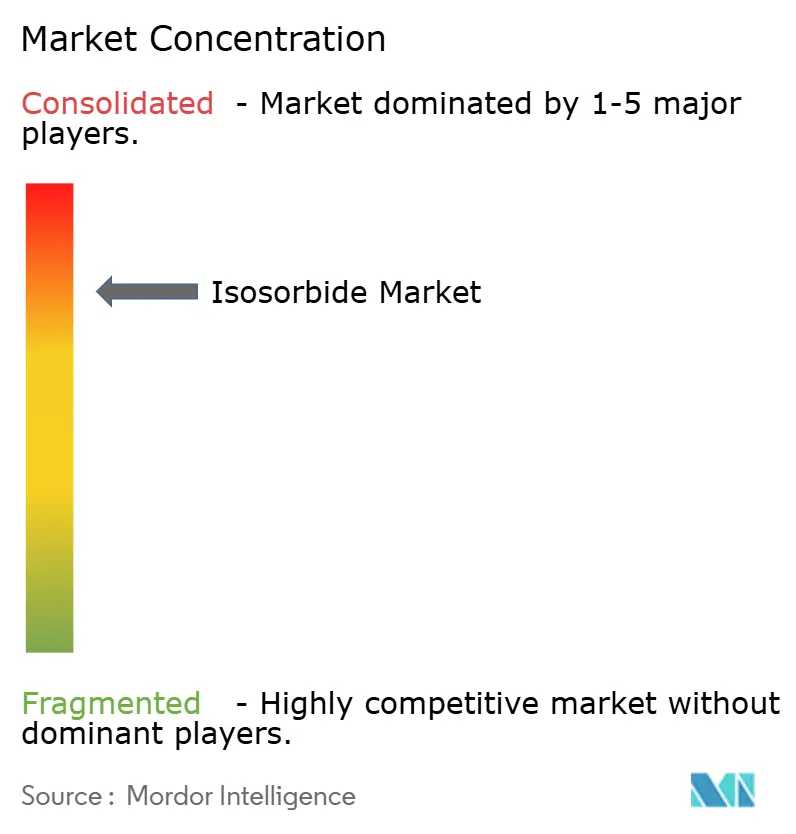

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

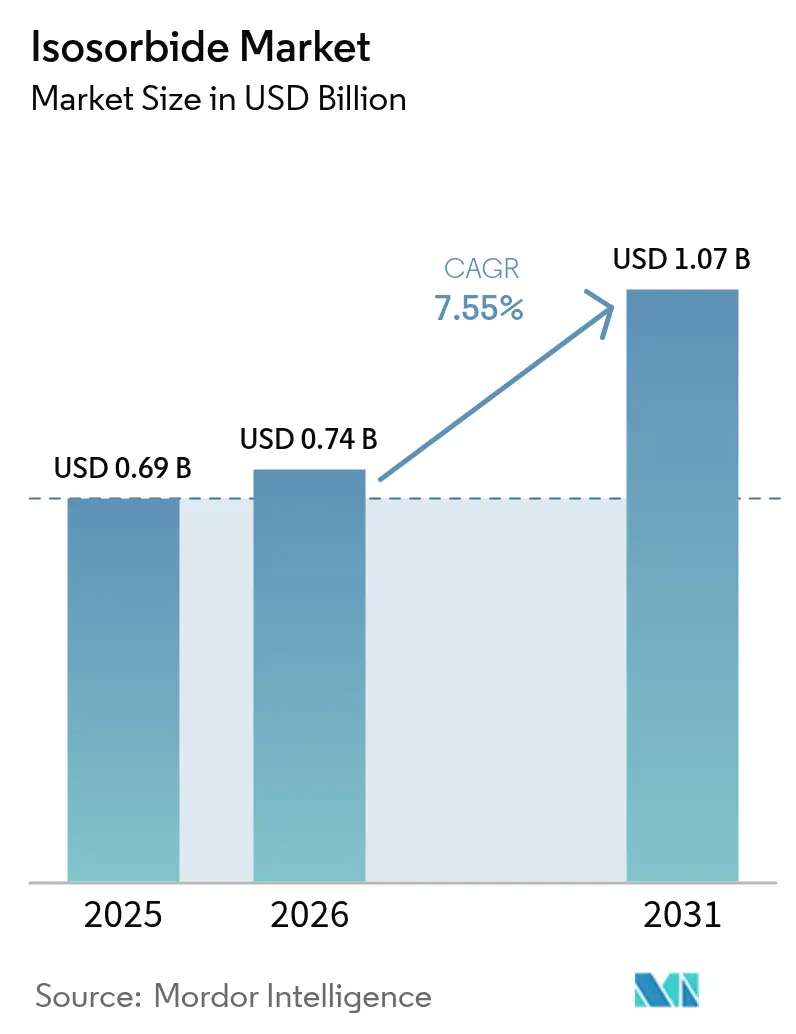

Isosorbide Market Analysis by Mordor Intelligence

Isosorbide market size in 2026 is estimated at USD 0.74 billion, growing from 2025 value of USD 0.69 billion with 2031 projections showing USD 1.07 billion, growing at 7.55% CAGR over 2026-2031. Rapid progress in bio-based polymer technologies, stricter global rules on fossil-derived chemicals, and rising consumer preference for sustainable packaging accelerate adoption across packaging, automotive, electronics, and healthcare uses. Asia-Pacific continues to drive volume through well-established sorbitol capacity, while Europe’s policy focus on a circular economy unlocks premium demand in high-performance plastics. Continuous-flow dehydration units, heterogeneous acid catalysts, and improved purification steps are trimming production costs, making the isosorbide market more competitive with petroleum alternatives. Concurrently, regulatory approvals for food-contact polymers and extended-release cardiovascular drugs have widened the molecule’s addressable space, reinforcing stable, long-term growth.

Key Report Takeaways

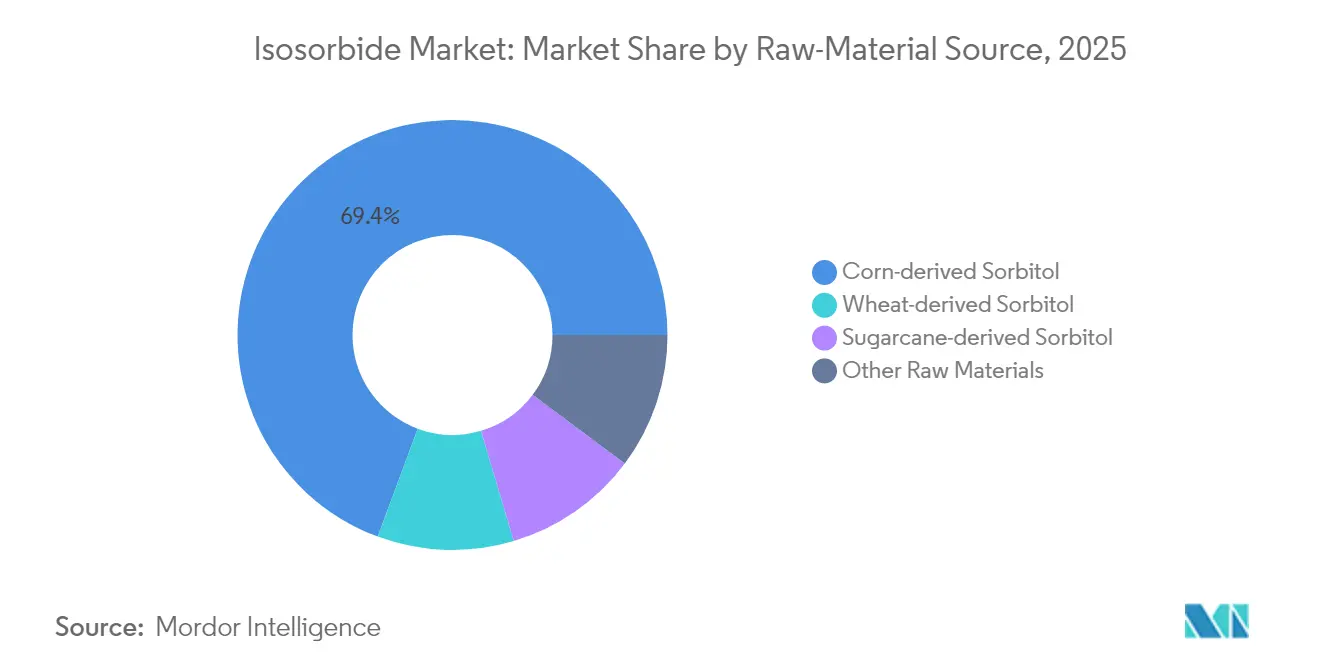

- By raw-material source, corn-based sorbitol captured 69.35% revenue share in 2025; sugarcane-based sorbitol is poised for a 8.62% CAGR through 2031.

- By application, PEIT held 43.70% of isosorbide market share in 2025, whereas polycarbonate grades are forecast to grow at a 10.35% CAGR from 2026 to 2031.

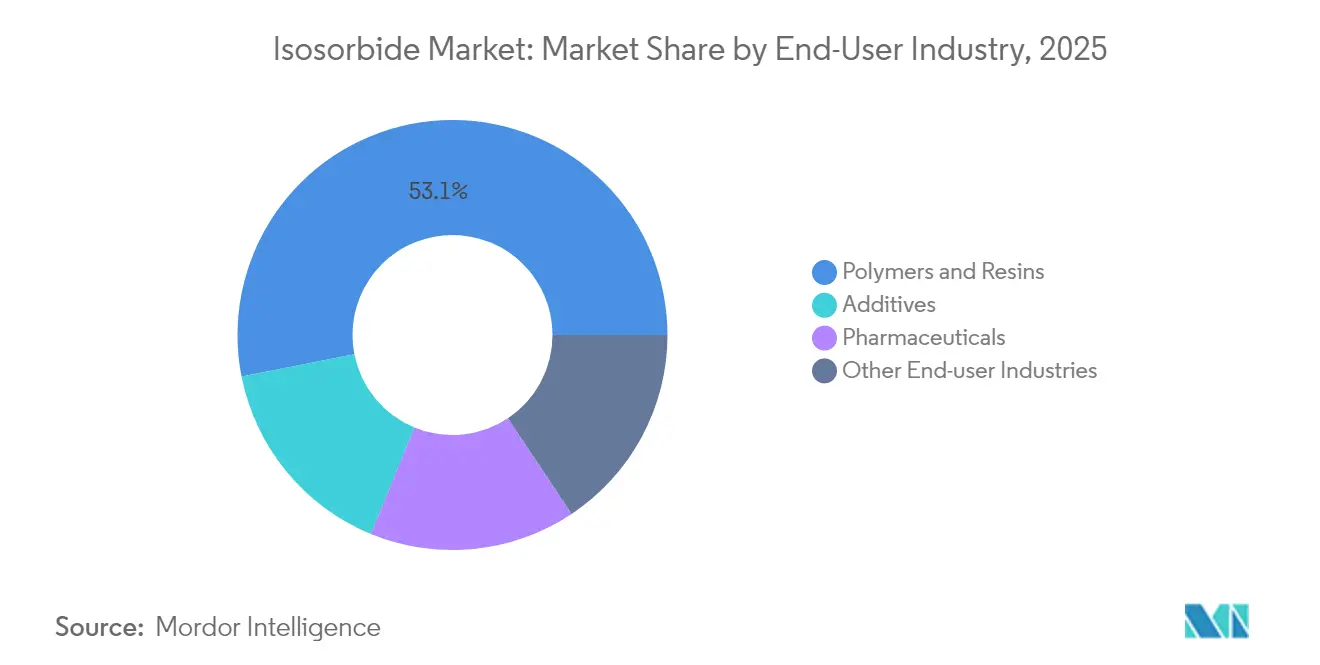

- By end-user industry, polymers and resins commanded 53.10% share of the isosorbide market size in 2025, while pharmaceuticals are projected to expand at a 9.12% CAGR to 2031.

- By geography, Asia-Pacific led with 38.75% revenue in 2025 and is on track for an 8.05% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Isosorbide Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainable shift to bio-based polymers | +2.1% | Global, with early adoption in Europe & North America | Long term (≥ 4 years) |

| Rising pharmaceutical demand for isosorbide nitrates | +1.8% | Global, concentrated in aging populations | Medium term (2-4 years) |

| Global BPA restrictions driving demand for isosorbide polycarbonates | +1.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Adoption in 3-D printing photopolymers | +1.2% | North America & Europe, with APAC growth | Long term (≥ 4 years) |

| Carbon-credit premiums for biobased PET producers | +0.8% | EU & North America, emerging in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sustainable Shift to Bio-Based Polymers

Multiple governments and large brand owners have prioritized net-zero targets, prompting sustained interest in biobased polymer chains. Fifteen European biorefinery projects backed by the Circular Bio-based Europe Joint Undertaking are scaling commercial output, while partnerships such as Neste and Lotte Chemical aim to replace fossil naphtha with renewable feedstocks[1]European Commission, “Circular Bio-based Europe Joint Undertaking,” europa.eu . Global biopolymer production reached 4.4 million tonnes in 2023 and is projected to climb swiftly, securing a structural runway for isosorbide adoption in rigid and flexible packaging, electronics housings, and performance fibers.

Rising Pharmaceutical Demand for Isosorbide Nitrates

Growing incidences of cardiovascular disease in aging populations sustain steady uptake of isosorbide dinitrate and mononitrate therapies. Recent FDA labeling updates improve dose schedules, strengthening patient adherence and reinforcing the safety profile of these vasodilators[2]U.S. Food and Drug Administration, “Approved Drug Products with Therapeutic Equivalence Evaluations,” fda.gov. Extended-release formulations, already integral to chronic angina care, preserve price stability and create a high-margin slice of the isosorbide market, supporting overall revenue resilience.

Global BPA Restrictions Driving Demand for Isosorbide Polycarbonates

Regulations limiting bisphenol A in food-contact and infant products push manufacturers toward safer diol building blocks. The FDA recognizes isosorbide-based polymers for repeat-use containers, and Mitsubishi Chemical’s DURABIO grades demonstrate superior clarity and low yellowing. This alignment of regulation and performance feeds sustained double-digit growth in optical, automotive, and consumer electronics glazing.

Adoption in 3-D Printing Photopolymers

Research teams have produced 90% bio-content photopolymers by integrating isosorbide with itaconic acid diols, achieving mechanical parity with petro-based resins. As industrial additive manufacturing migrates toward greener inputs, specialty formulators view isosorbide as a way to meet ESG procurement criteria without sacrificing dimensional accuracy or surface quality.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns around isosorbide derivatives | -1.1% | Global, with heightened scrutiny in regulated markets | Medium term (2-4 years) |

| High catalytic conversion & purification cost | -0.7% | Global, particularly affecting emerging market adoption | Long term (≥ 4 years) |

| Competition from furan-based bio-monomers | -0.9% | Global, with stronger impact in Europe & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Around Isosorbide Derivatives

While neat isosorbide holds food-contact clearance, certain nitrates and diester derivatives face ongoing toxicology reviews. Regulators continue to examine migration levels from novel polymer blends, prolonging time-to-market for next-generation packaging and medical devices. The resulting approval cycles and pharmacovigilance obligations temporarily temper expansion in heavily regulated channels.

High Catalytic Conversion & Purification Cost

Dehydrating sorbitol to isosorbide needs precise temperature control and acid catalysis, then energy-intensive refinements to meet optical-grade purity. Heterogeneous carbon-based catalysts now reach 82.7% yields, and pilot continuous-flow reactors shorten residence times, yet capital requirements remain high. These cost hurdles slow penetration into low-margin packaging films when crude oil prices soften.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw-Material Source: Feedstock Evolution Shapes Cost Curve

Corn-derived sorbitol accounted for 69.35% of the volume in 2025, thanks to an abundant maize supply, mature hydrogenation assets, and logistical proximity to North American polymer converters. At the segment level, the isosorbide market size connected to corn feedstocks is expected to grow in line with overall consumption, although the relative share diminishes slightly as alternative sugars enter the mix. Sugarcane-based sorbitol, supported by tropical agronomy and favorable crop carbon metrics, is projected to grow at a 8.62% CAGR, capturing interest from European buyers seeking lower embedded emissions.

Wheat-derived sorbitol retains a smaller foothold, supported by integrated starch mills across Western Europe that prefer local raw material procurement for cost stability. Emerging exploration of cellulosic and waste-sugar routes signals a future diversification of inputs, potentially cushioning price volatility. Continuous gain-of-function work on yeast strains and enzymatic pathways promises incremental yield improvements, which in turn strengthen feedstock flexibility for isosorbide producers.

By Application: Performance Polymers Anchor Demand

PEIT accounted for 43.70% of the global isosorbide market share in 2025, underlining its central role in sustainable bottle and film applications. The isosorbide market size tied to PEIT is forecast to expand steadily as beverage brands roll out plant-based containers and integrate recycled content streams. Polycarbonate use cases, led by DURABIO panels and consumer gadget casings, are advancing at a 10.35% CAGR, driven by BPA restrictions and market preference for enhanced impact performance. Polyurethane modifiers leverage isosorbide’s rigid bicyclic core to craft non-isocyanate formulations with improved abrasion resistance.

Complementary niches, such as isosorbide succinate resins and diesters, cater to high-temperature engineering plastics and pharmaceutical intermediates, supporting specialized growth within the broader isosorbide market. Ongoing research in 3D printing photopolymers demonstrates the molecule’s versatility across additive manufacturing, while detergents and cosmetics rely on monoester variants for biodegradable surfactant properties. These evolving pathways diversify revenue streams and build resilience against fluctuations in single applications.

By End-User Industry: Polymers and Resins Dominate the Isosorbide Market

Polymers and resins accounted for 53.10% of revenue in 2025, reflecting the large-scale deployment of isosorbide diaromatics in rigid bottles, automotive bezels, and electronic housings. This volume segment remains pivotal to capacity utilization and underpins economies of scale across the isosorbide market. Pharmaceutical demand, although accounting for a smaller share, is projected to grow at a 9.12% CAGR as extended-release vasodilators and combination therapies target the expanding geriatric population. The resulting premium price points offset lower tonnage, thereby bolstering the overall margin of the Isosorbide Market, which expands due to its diverse applications and robust demand.

Additive customers utilize isosorbide as a chain extender, plasticizer, and stabilizer in complex polymer systems, providing formulators with a bio-based route to maintain mechanical performance while meeting eco-label criteria. Emerging verticals, notably 3-D printing resins and specialty esters for personal care, introduce additional pathways to monetize the molecule’s unique rigidity and hydrophilicity. Together these segments broaden market exposure and insulate suppliers from single-industry downturns, further strengthening the isosorbide market.

Geography Analysis

Asia-Pacific captured 38.75% of global revenue in 2025 and is poised for an 8.05% CAGR through 2031, fueled by China’s large-scale investments in bio-materials and expanding regional demand for high-performance plastics. The isosorbide market size in the region benefits from deep sorbitol supply chains, proximity to corn and sugarcane feedstocks, and nation-level strategies such as Malaysia’s Chemical Industry Roadmap 2030 that prioritize value-added specialty chemicals. Japanese resin producers continue to commercialize high-clarity polycarbonate parts, thereby reinforcing the growth of premium applications.

North America leverages its established corn wet-milling assets, advanced catalytic research and development, and supportive bioproduct tax credits to sustain steady demand across packaging, automotive, and medical device applications. Collaboration between petrochemical firms and agricultural processors accelerates scale-up of integrated biorefinery complexes, anchoring local supply security. Meanwhile, Europe emphasizes strict sustainability standards and circular-economy directives. The region’s preference for bio-attributed polymer chains nurtures a high-value segment of the isosorbide market, particularly within food-contact packaging and infant products.

South America, endowed with competitive sugarcane yields, emerges as a cost-effective hub for future sorbitol production. Pilot isosorbide units co-located with ethanol mills are under evaluation, positioning the continent to address both domestic and export demand.

Middle East & Africa show gradual adoption, hinging on rising urbanization and government-led diversification initiatives that encourage chemical manufacturing beyond oil derivatives. Progress in these regions remains tied to infrastructure, policy clarity, and feedstock availability, yet offers long-term upside to global market balance.

Competitive Landscape

The isosorbide market demonstrates high concentration as a handful of players control large-scale output while niche innovators cultivate specialty grades. Roquette’s 20,000 tonne annual capacity anchors global supply and ensures consistent quality for volume buyers in packaging and automotive. Mitsubishi Chemical Corporation differentiates through DURABIO polycarbonate, translating isosorbide chemistry into premium optical sheets, smartphone housings, and interior trim that command higher margins.

Technology investment centers on continuous-flow dehydration reactors, heterogeneous acid catalysts, and downstream purification to pharmaceutical standards. Recent lab-to-pilot scale work with ruthenium-phosphine complexes has achieved kilogram-scale epimerization using minimal precious metal loading, hinting at further cost reductions. Regional specialists in South Korea and Thailand have begun licensing such advances to expand local production, tightening supply chains in Asia-Pacific.

Isosorbide Industry Leaders

ADM

Mitsubishi Chemical Corporation

Novaphene

Roquette Frères

Ecogreen Oleochemicals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Zydus Lifesciences announced that it had secured final USFDA approval for 30 mg, 60 mg, and 120 mg isosorbide mononitrate extended-release tablets.

- January 2024: Samyang Innochem announced that it received ISCC Plus certification for its isosorbide line, confirming traceable bio-based content.

Global Isosorbide Market Report Scope

Isosorbide is a white, crystalline, polyol that can be produced from acid-catalyzed dehydration of a compound obtained from the hydrogenation of glucose called sorbitol. It finds its major application in the construction, automotive, and pharmaceutical industries. The isosorbide market is segmented by application, end-user industry, and geography. By application, the market is segmented into Strong and Fuming. By application, the market is segmented into Polyethylene Isosorbide Terephthalate (PEIT), Polycarbonate, Polyurethane, Polyesters Isosorbide Succinate, Isosorbide Diesters, and Other Applications. By end-user industry, the market is segmented into Polymers and Resins, Additives, Pharmaceuticals, and Other End-user Industries. The report also covers the market size and forecasts for the isosorbide market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| Corn-derived Sorbitol |

| Wheat-derived Sorbitol |

| Sugarcane-derived Sorbitol |

| Other Raw Materials |

| Polyethylene Isosorbide Terephthalate (PEIT) |

| Polycarbonate |

| Polyurethane |

| Polyesters Isosorbide Succinate |

| Isosorbide Diesters |

| Other Applications |

| Polymers and Resins |

| Additives |

| Pharmaceuticals |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest and Middle-East and Africa |

| By Raw-Material Source | Corn-derived Sorbitol | |

| Wheat-derived Sorbitol | ||

| Sugarcane-derived Sorbitol | ||

| Other Raw Materials | ||

| By Application | Polyethylene Isosorbide Terephthalate (PEIT) | |

| Polycarbonate | ||

| Polyurethane | ||

| Polyesters Isosorbide Succinate | ||

| Isosorbide Diesters | ||

| Other Applications | ||

| By End-User Industry | Polymers and Resins | |

| Additives | ||

| Pharmaceuticals | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest and Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current Isosorbide Market size?

The market is valued at USD 0.74 billion in 2026 and is projected to reach USD 1.07 billion by 2031.

Which application currently leads demand in the isosorbide market?

Polyethylene Isosorbide Terephthalate (PEIT) leads, accounting for 43.70% of 2025 revenue.

Why is Asia-Pacific the largest regional market for isosorbide?

The region combines abundant corn and sugarcane feedstocks, mature sorbitol facilities, and supportive bio-economy policies, resulting in 38.75% market share in 2025.

How do BPA regulations influence isosorbide demand?

Restrictions on bisphenol A drive swift adoption of isosorbide-based polycarbonates, which offer comparable or superior optical and mechanical properties.

Page last updated on: