Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

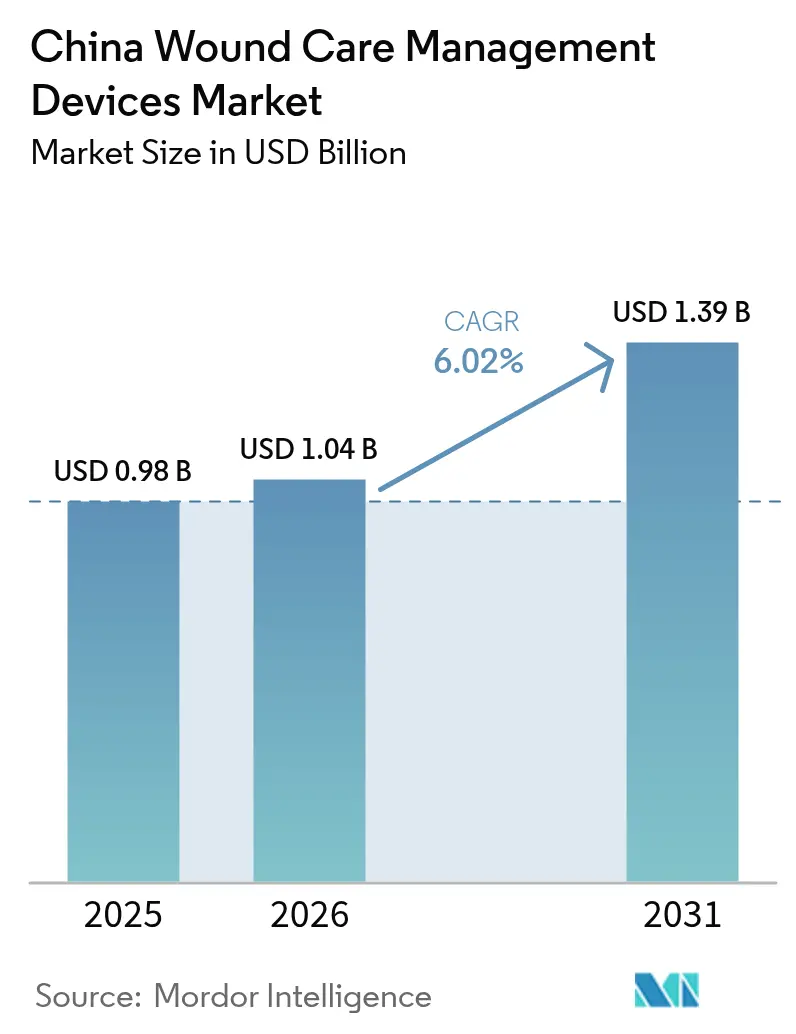

| Base Year Market Size (2025) | USD 0.98 Billion |

| Market Size (2026) | USD 1.04 Billion |

| Market Size (2031) | USD 1.39 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Wound Care Management Devices Market Analysis by Mordor Intelligence

The China wound care management devices market size was valued at USD 0.98 billion in 2025 and estimated to grow from USD 1.04 billion in 2026 to reach USD 1.39 billion by 2031, at a CAGR of 6.02% during the forecast period (2026-2031). That trajectory reflects accelerating hospital capacity expansion, surging chronic disease prevalence, and government payment reforms that reward faster healing over procedure volume. China supports 233 million diabetes patients—15.88% of its adult population in 2023—and, without intervention, prevalence could rise to 29.1% by 2050 [1]Yu-Chang Zhou, "The national and provincial prevalence and non-fatal burdens of diabetes in China from 2005 to 2023 with projections of prevalence to 2050," Military Medical Research, mmrjournal.biomedcentral.com. Wound-healing centers multiplied, signaling institutional readiness for advanced therapies. At the same time, Volume-Based Procurement (VBP) is cutting average prices for high-value consumables by roughly 70%, forcing suppliers to prove clear economic value. Digital health policies—66 enacted in 2023 alone—further stimulate demand for connected dressings and remote monitoring solutions.

Key Report Takeaways

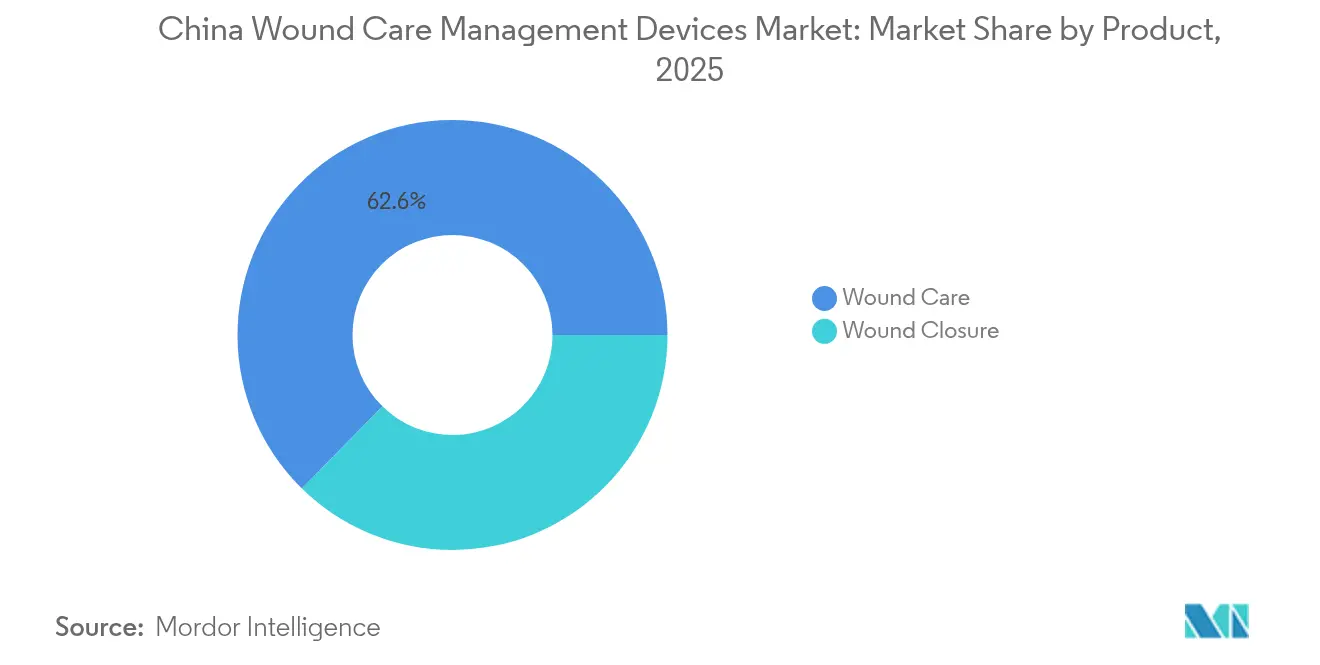

- By product category, advanced wound care captured 62.65% revenue share of the China wound care management devices market in 2025, while wound closure items are forecast to grow at a 6.75% CAGR through 2031.

- By wound type, chronic wounds commanded 58.74% of the market in 2025; acute wounds are expanding fastest at a 6.83% CAGR through 2031.

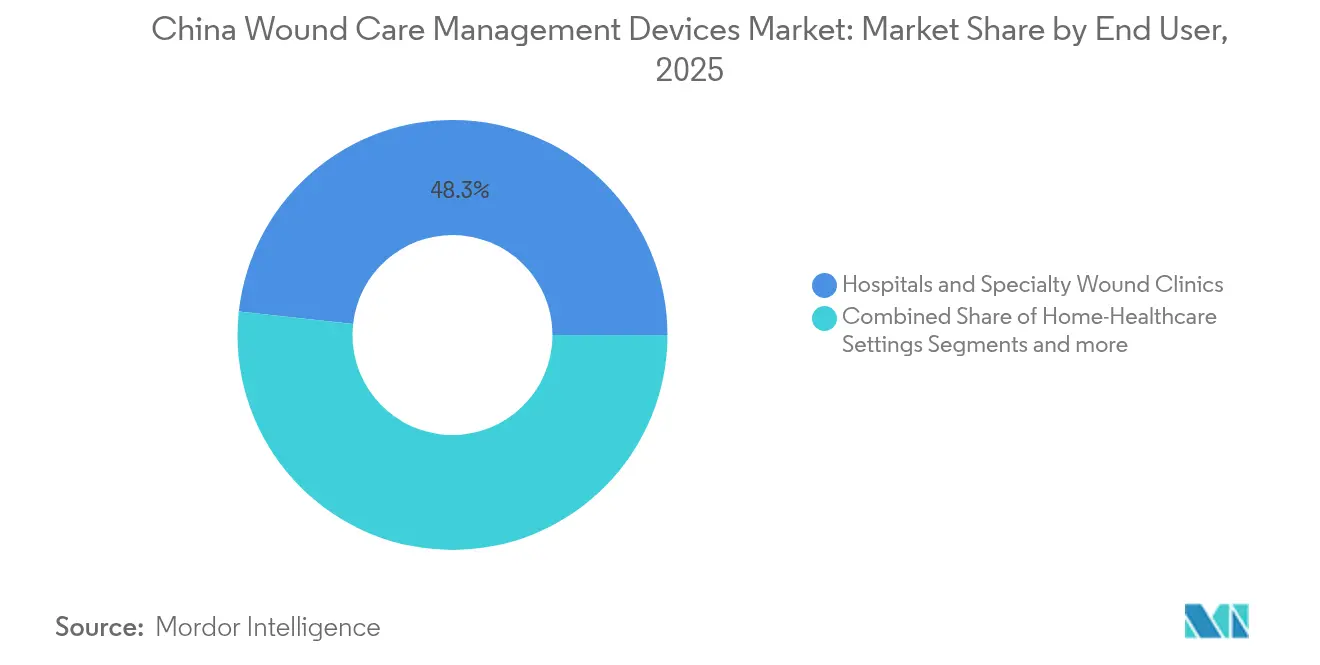

- By end-user, hospitals & specialty wound clinics accounted for 48.25% of the China wound care management devices market share in 2025, while home-healthcare settings are on track for a 6.99% CAGR to 2031.

- By mode of purchase, institutional procurement dominated with 59.88% market share in 2025; retail/OTC channels should climb at a 7.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of diabetes & chronic wounds | +1.8% | National; concentrated in eastern urban centers | Long term (≥ 4 years) |

| Demand for faster recovery & reduced hospital stay | +1.2% | Tier-1 and Tier-2 cities; expanding to Tier-3 | Medium term (2-4 years) |

| Ageing population & higher elective surgeries | +1.5% | National; acute impact in eastern provinces | Long term (≥ 4 years) |

| Growing technological advancements in wound care devices | +0.9% | Urban centers; gradual rural penetration | Medium term (2-4 years) |

| Government DRG payment reform accelerating adoption of advanced dressings | +0.7% | National implementation; pilot regions leading | Short term (≤ 2 years) |

| Rising e-commerce penetration of wound supplies in tier-3/4 cities | +0.4% | Primarily tier-3 and tier-4 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Diabetes & Chronic Wounds

Diabetes prevalence increased from 7.53% in 2005 to 13.67% in 2023, inflating demand for the China wound care management devices market. Diabetic-foot treatment cost per patient jumped, while amputation rates almost tripled, prompting hospitals to shift toward preventive dressings and negative-pressure systems. Close to 100 million Chinese suffer chronic wounds every year, and diabetic ulcers have overtaken trauma as the primary cause. Evidence of superior healing in southern provinces drives region-specific adoption strategies. Collectively, these dynamics underpin sustained growth for the China wound care management devices market.

Demand for Faster Recovery & Reduced Hospital Stay

Complex-wound inpatients average 12 days of hospitalization versus seven for ordinary admissions, with median medical costs exceeding RMB 6,500. Hospitals therefore invest in technologies that shorten recovery. Modified negative-pressure therapy has trimmed healing time by almost three days and halved treatment expenses. Smart bandages such as the iCares system detect complications several days earlier than clinical observation. These solutions align with Diagnosis-Related Group (DRG) payment reforms that reward outcomes, helping expand the China wound care management devices market in metropolitan hubs.

Ageing Population & Higher Elective Surgeries

China’s 65+ cohort is swelling [2]Shihua Luo, "Forecast of total health expenditure on China’s ageing population: a system dynamics model," BMC Health Services Research, bmchealthservres.biomedcentral.com, driving both chronic wounds and surgical procedures. Class III Level A hospitals increased significantly, boosting surgical capacity. Preventive negative-pressure therapy cuts surgical-site infections by 74% among high-risk patients. Bioelectrical smart bandages achieve 99.75% closure by day 14, outperforming standard care. Aging-driven healthcare spending forecasts sustain long-run momentum for the China wound care management devices market.

Growing Technological Advancements in Wound Care Devices

Smart dressings now integrate pH, temperature, and drug-delivery functions [3]Md. Imran Hossain, "Smart bandage: A device for wound monitoring and targeted treatment," ScienceDirect, sciencedirect.com. Machine-learning models predict wound healing with over 98% accuracy, guiding personalized regimens. Self-growing hydrogel adhesives strengthen for 120 hours while inducing angiogenesis in diabetic wounds. Forty-eight AI medical devices earned Chinese approval in 2023, a 50% annual increase. Nanozyme dressings capable of modulating wound micro-environments mark the next innovation wave.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent registration (NMPA Class III) & reimbursement hurdles | -1.4% | National; affecting all market participants | Long term (≥ 4 years) |

| High price sensitivity in public tenders | -0.8% | National; concentrated in public hospital procurement | Medium term (2-4 years) |

| Emerging domestic OEMs triggering price wars in negative-pressure devices | -0.6% | National; acute impact in tier-1 and tier-2 cities | Short term (≤ 2 years) |

| Shortage of wound care specialists | -0.5% | National; severe impact in western and rural regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Registration (NMPA Class III) & Reimbursement Hurdles

Advanced dressings classified as Class III must undergo extensive trials, often extending approval by up to two years. New 2024 procurement rules require local patents and manufacturing, effectively sidelining many multinationals. Price negotiations led by the National Healthcare Security Administration resulted in average 63% cuts for novel therapies, squeezing margins. Commercial insurance covers just 7.7% of innovative-device costs, forcing patients to pay nearly half out-of-pocket. These hurdles temper growth, especially for premium imports within the China wound care management devices market.

High Price Sensitivity in Public Tenders

VBP rounds have slashed high-value consumable prices by about 70%. In winner-take-all tenders, the lowest bidders secure volumes, sidelining costlier advanced solutions. Public hospitals—holding 60.44% procurement share—now emphasize unit price over clinical evidence, curbing the adoption of innovative dressings. Smith+Nephew flagged VBP-driven China headwinds even as global advanced-wound revenue rose 3.8% in Q1 2025. Domestic firms reply with low-cost negative-pressure systems, triggering price wars that dent the China wound care management devices market’s value pool.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Advanced Therapies Anchor Growth

Advanced wound care retained a 62.65% share of the China wound care management devices market in 2025. Studies show negative-pressure therapy achieves 99.75% closure versus 94% for conventional methods, reinforcing clinical preference. Hospitals also favor antimicrobial hydrofibers such as Aquacel Ag+ for chronic ulcers, citing faster granulation. Advanced dressings’ higher upfront cost is offset by shorter length-of-stay incentives under DRG payment reform, supporting wider adoption in tertiary centers.

The wound-closure segment, though smaller, is forecast to rise at a 6.75% CAGR. Tissue adhesives and absorbable sealants gain traction for minimally invasive surgery, and automated staplers improve operating-room efficiency. Liquid-diode smart bandages that channel exudate one way while reading pH levels represent the next leap. Taken together, product innovation underpins enduring expansion of the China wound care management devices market.

By Wound Type: Chronic Dominance, Acute Momentum

Chronic conditions accounted for 58.74% of the China wound care management devices market size in 2025, led by diabetic foot ulcers with an 8.1% annual incidence among diabetics. Specialized centers and city-level reimbursement pilots are scaling advanced dressings, although northern provinces still report slower healing. Pressure ulcers remain a costly inpatient problem, elevating demand for breathable silicone foams.

Acute wounds are projected to expand at 6.83% CAGR, reflecting increased elective surgery and improved emergency trauma care. Prophylactic negative-pressure systems reduce surgical-site infection by 74%, reinforcing hospital adoption. Dynamically phase-adaptive hydrogels that harden on impact but soften for remodeling shorten closure times in burn units. Such performance advantages sustain the acute segment’s outsized contribution to incremental growth within the China wound care management devices market.

By End User: Decentralization Reshapes Demand

Hospitals and specialty wound clinics generated 48.25% of the China wound care management devices market share in 2025, capitalizing on multidisciplinary expertise and high-acuity case loads. Yet home-healthcare settings will post a 6.99% CAGR through 2031 as policymakers back integrated community care. Remote glucose monitoring cut HbA1c among diabetics, demonstrating telehealth’s role in wound prevention. Home-based negative-pressure systems face cost and training hurdles, but uptake is rising in affluent coastal cities.

Long-term-care facilities serve a growing geriatric cohort, where proactive dressings reduce pressure-ulcer incidence. Telemedicine platforms knit these settings together, though 27.69% of online consultations still end incomplete, indicating workflow refinements ahead. Advancements in user-friendly smart dressings promise smoother decentralization of the China wound care management devices market.

By Mode of Purchase: E-Commerce Accelerates Retail Growth

Institutional procurement retained 59.88% of the China wound care management devices market in 2025, but continued VBP rounds compress margins. Hospitals juggle the tension between lowest-price mandates and DRG savings, favoring products that prove total-cost advantages.

Retail and OTC channels should achieve a 7.11% CAGR as e-commerce platforms widen access in tier-3 and tier-4 cities. China’s healthcare IT industry surpassed RMB 800 billion in 2024, underpinning logistics for same-day wound-dressing delivery. Consumer-grade smart bandages with Bluetooth connectivity enable at-home monitoring, lowering clinic visits and reinforcing the decentralizing trend across the China wound care management devices market.

Geography Analysis

Regional inequality shapes adoption patterns across the China wound care management devices market. The eastern seaboard, housing most Class III Level A hospitals, captures the lion’s share of advanced-therapy sales, while western provinces lag in specialist density. Medical resource primacy averages 2.30, evidencing concentration in large metros.

Shanghai has narrowed equipment disparities but still clusters high-end wound-care devices in urban districts. Shenzhen’s community-hospital model raises suburban access and could be replicated for wound care. In Hainan’s rural counties, Health All-in-One kiosks boosted visits by 37.85% and revenue by 54.03%, hinting at scalable tele-wound-care solutions.

Digital channels mitigate some disparities: online pharmacies deliver negative-pressure kits to tier-4 locales within two days and offer video tutorials. Provincial policies vary- Jiangsu offers partial reimbursement for smart dressings, whereas Gansu does not- creating a patchwork of financing that suppliers must navigate. Despite gaps, accelerating infrastructure investment and telehealth adoption should gradually even out penetration, broadening the base of the China wound care management devices market.

Competitive Landscape

The China wound care management devices industry is moderately fragmented, with VBP compressing prices and awarding high volumes to a handful of lowest-bidding vendors. Multinationals such as Smith+Nephew cite China procurement headwinds, even while their global advanced wound division grew 3.8% in Q1 2025. Johnson & Johnson MedTech reported similar challenges as anti-corruption probes tightened hospital relationships.

Domestic firms leverage lower production costs and rapid regulatory pathways to outbid foreign rivals. Some local OEMs introduced negative-pressure systems priced 40% below imported equivalents, winning provincial tenders. Regulatory amendments now require local patents and plants, further tilting the field toward Chinese manufacturers.

Innovation remains a differentiator. Solventum’s V.A.C. Peel & Place dressing extends wear to seven days, easing application and trimming nurse time. Convatec posted 6.7% organic wound-care growth in H1 2024, fueled by Aquacel Ag+ and InnovaMatrix launches. University of Nottingham Ningbo’s battery-free Janus dressing exemplifies academia-industry collaboration that could spawn local commercialization paths. Over the next five years, suppliers that combine cost competitiveness with digital-health integration will secure durable positions in the China wound care management devices market.

China Wound Care Management Devices Industry Leaders

-

Medtronic PLC

-

Smith & Nephew PLC

-

Convatec Inc.

-

Coloplast

-

Solventum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Convatec begins a global educational collaboration with the Wound, Ostomy and Continence Nurses Society (WOCN), with Chinese programmes launching in 2025.

- February 2025: Smith+Nephew confirms that new U.S. tariffs on Chinese imports will dent revenue for its wound division due to significant China-based manufacturing.

- November 2024: University of Nottingham Ningbo China unveils a battery-free multifunctional microfluidic Janus wound dressing capable of real-time exudate management.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our analysts define the China wound care management devices market as the annual revenue generated from advanced and traditional dressings, negative-pressure wound therapy pumps and disposables, oxygen and electro-stimulation systems, sutures, staplers, sealants, tissue adhesives, and related closure devices that are used to treat acute or chronic skin, tissue, and post-surgical wounds across all care settings. We convert every data point to constant-2024 US dollars to remove exchange-rate noise, and we track only new product sales, not refurbished equipment or home-made dressings.

Scope exclusion: consumer first-aid strips and cosmetic skin patches are excluded because they are bought for minor cuts rather than clinically managed wounds.

Segmentation Overview

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Detailed Research Methodology and Data Validation

Primary Research

Several semi-structured interviews with hospital wound-care nurses, procurement managers in tier-1 and tier-3 cities, domestic OEM executives, and regional distributors allowed us to validate unit prices, gauge negative-pressure therapy adoption, and fine-tune assumptions on volume-based procurement (VBP) price cuts. Responses also clarified stocking patterns in long-term care and home health channels.

Desk Research

We began with publicly available datasets from the National Health Commission on inpatient surgical volumes, the Chinese Diabetes Society's prevalence surveys, and the National Medical Products Administration device registry, which signal installed base and price ceilings. Trade statistics from China Customs and the UN Comtrade portal helped us map import penetration of advanced dressings, while demographic baselines came from the National Bureau of Statistics and UN Population Prospects. Supplementary insights were drawn from peer-reviewed journals such as the Chinese Journal of Burns and trade association briefs. Company financial snapshots were sourced through D&B Hoovers. This list is illustrative, not exhaustive; many other secondary sources supported verification.

Market-Sizing & Forecasting

We apply a top-down build that starts with procedure counts and diabetes-linked prevalence, then layers penetration-rate assumptions for each device type. Results are cross-checked with selective bottom-up roll-ups of sampled average selling price multiplied by volume from leading suppliers. Key variables feeding the model include: 1) diabetic foot ulcer incidence, 2) elective surgery backlog release, 3) VBP tender price reductions, 4) hospital bed additions, and 5) retail e-commerce share for dressings. Forecasts to 2030 are generated through multivariate regression blended with ARIMA smoothing, and our team stress tests scenarios with clinicians to bridge data gaps where bottom-up evidence is thin.

Data Validation & Update Cycle

Outputs undergo anomaly checks, peer review, and a senior analyst sign-off. The model is refreshed annually, and we trigger interim updates when NMPA approvals, major VBP rounds, or reimbursement code changes materially shift demand. Before publication, a fresh data sweep ensures clients receive the latest view.

Why Our China Wound Care Management Baseline Deserves Trust

Published estimates often diverge because firms slice the market differently, use varied refresh cadences, or overlook recent VBP pricing shocks.

Key gap drivers include narrower product scopes, older base years, and reliance on import logs without reconciling booming domestic production, which Mordor's methodology captures through both hospital-level interviews and registry audits.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.98 B (2025) | Mordor Intelligence | - |

| USD 0.57 B (2025) | Regional Consultancy A | Omits device segments such as NPWT and closure systems; limited hospital discharge data |

| USD 0.67 B (2024) | Global Consultancy B | Bundles traditional first-aid dressings and applies APAC average prices; older baseline year |

These comparisons show that Mordor's disciplined scope selection, variable tracking, and yearly refresh provide a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the current size of the China wound care management devices market?

The China wound care management devices market size is USD 1.04 billion in 2026 and is forecast to reach USD 1.39 billion by 2031.

Which product segment leads the market today?

Advanced wound care products hold 62.65% of 2025 revenue, underlining hospital preference for dressings and negative-pressure systems that accelerate healing.

Why are retail and OTC channels growing so quickly?

E-commerce platforms extend device access into tier-3 and tier-4 cities, driving a 7.11% CAGR for retail purchases through 2031 as consumers embrace home-based care.

How is Volume-Based Procurement affecting suppliers?

VBP rounds cut device prices by about 70%, forcing manufacturers to compete mainly on cost and to demonstrate clear total-cost savings to win hospital tenders.

Which geographic areas offer the most untapped potential?

Western and inland provinces lag in specialist density, making them attractive for tele-enabled wound solutions and lower-priced advanced dressings as infrastructure improves.

What technological trends will shape future market growth?

Smart dressings with embedded sensors, AI-guided wound assessment, and self-growing hydrogel adhesives are expected to drive adoption by shortening healing times and supporting remote monitoring.

Page last updated on: