Global Wound Care Biologics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

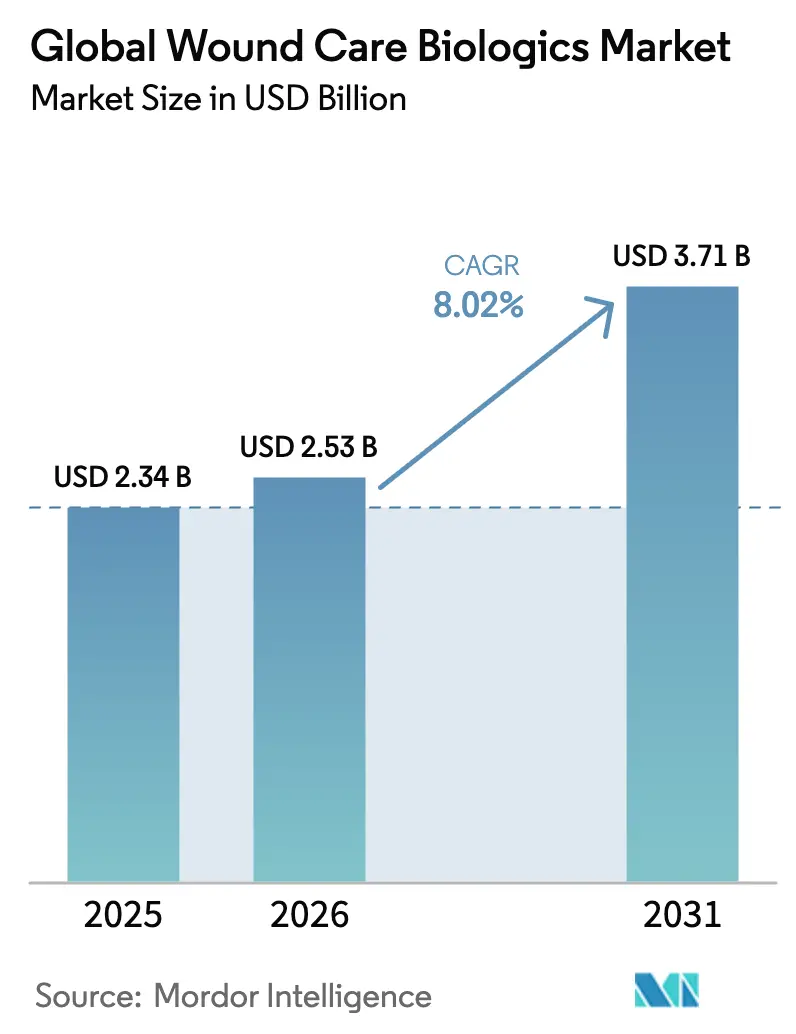

| Market Size (2026) | USD 2.53 Billion |

| Market Size (2031) | USD 3.71 Billion |

| Growth Rate (2026 - 2031) | 8.02% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Wound Care Biologics Market Analysis by Mordor Intelligence

Wound care biologics market size in 2026 is estimated at USD 2.53 billion, growing from 2025 value of USD 2.34 billion with 2031 projections showing USD 3.71 billion, growing at 8.02% CAGR over 2026-2031. Momentum stems from expanding clinical evidence that biologic matrices, xenografts, and growth-factor dressings shorten healing time and reduce infection risk compared with conventional dressings. Mandatory Local Coverage Determinations (LCDs) issued by the Centers for Medicare & Medicaid Services (CMS) in April 2025 require proof of 50% wound-area reduction within four weeks before reimbursements are approved, which weeds out marginal products and redirects budgets toward options with published outcomes. Product innovation is intensifying, guided by FDA plans to reclassify antimicrobial dressings into stricter device classes, prompting manufacturers to prioritize resistance-mitigation features. Meanwhile, the U.S. Department of Defense’s USD 1.66 billion Chemical and Biological Defense Program budget accelerates battlefield-to-bedside translation of trauma-oriented biologics.

Key Report Takeaways

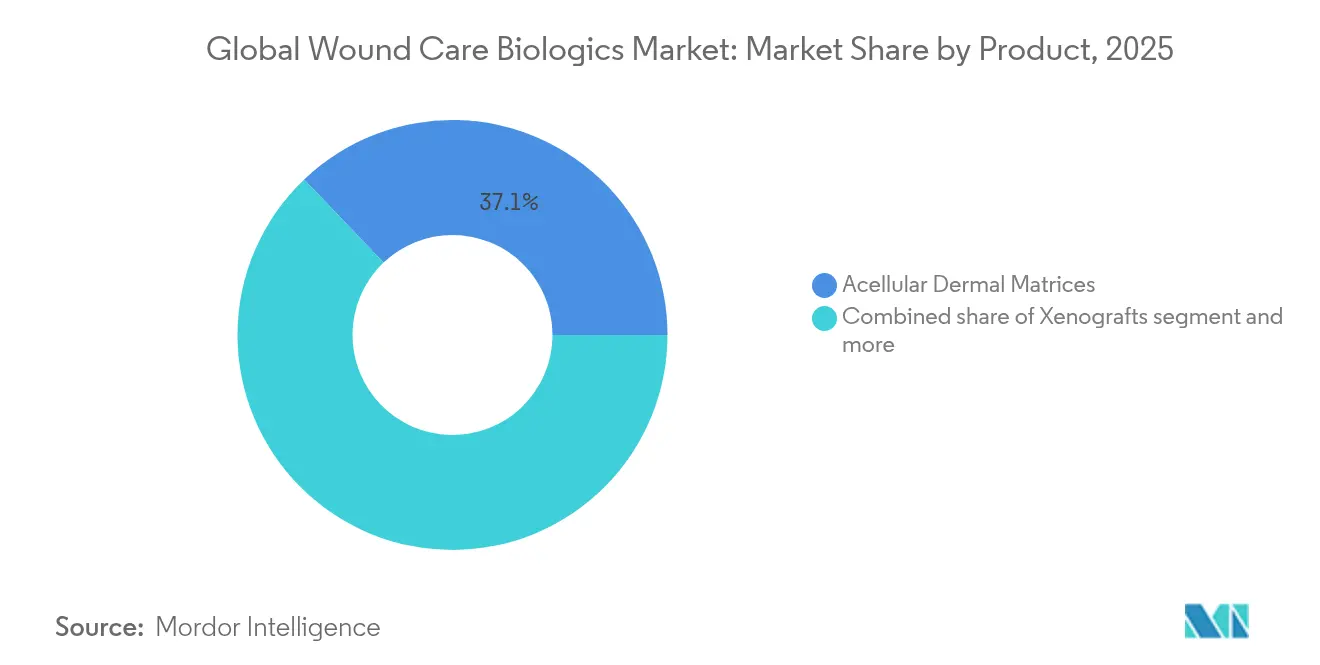

- By product, acellular dermal matrices led with a 37.12% of the wound care biologics market share in 2025; xenografts are forecast to expand at a 10.23% CAGR through 2031.

- By wound type, ulcers accounted for 62.15% of the wound care biologics market size in 2025, while burns are advancing at a 9.21% CAGR through 2031.

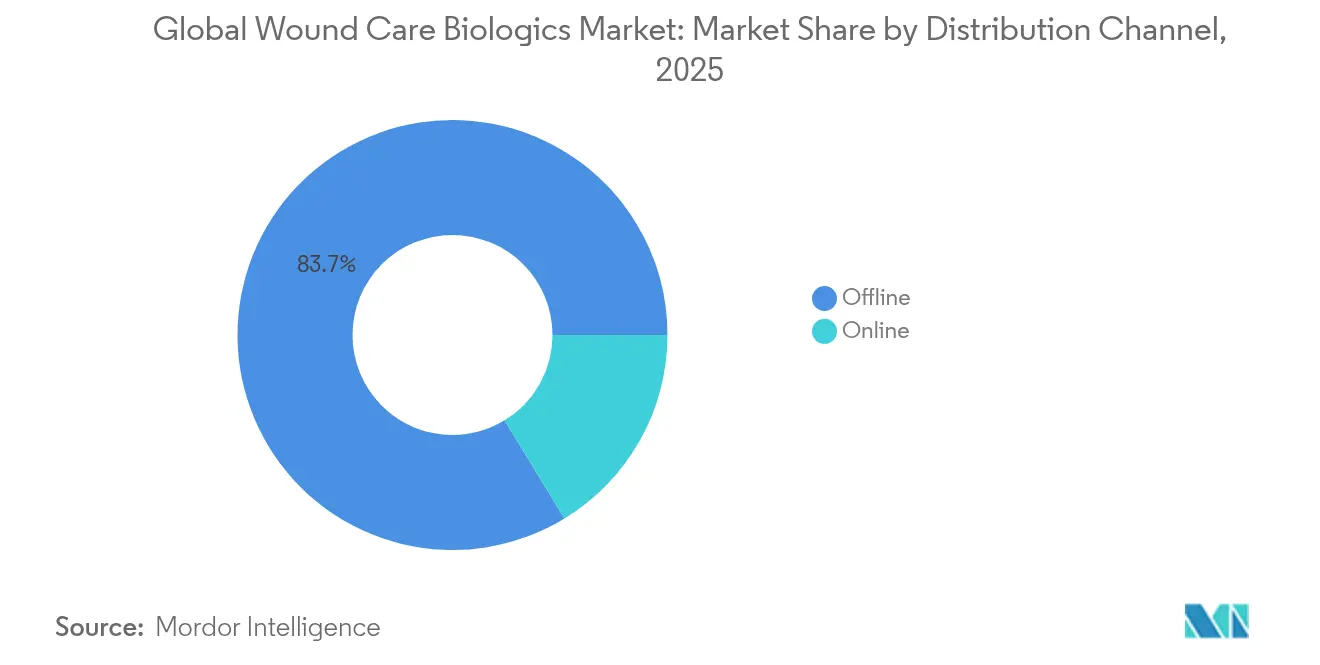

- By distribution channel, offline sales held 83.72% of revenue in 2025, whereas online platforms are registering a 9.58% CAGR to 2031.

- By end-user, hospitals and clinics captured 63.88% of revenue in 2025; ambulatory surgical centers are projected to grow at a 8.98% CAGR through 2031.

- By geography, North America dominated with 44.38% revenue share in 2025; Asia-Pacific is the fastest-growing region at a 9.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Global Wound Care Biologics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence of Diabetic Foot Ulcers | +2.1% | Global, led by North America and Asia-Pacific | Long term (≥ 4 years) |

| Government Reimbursement Expansions for Advanced Wound Care | +1.8% | North America & EU, emerging in Asia-Pacific | Medium term (2-4 years) |

| Increasing Incidence of Burns & Road-Traffic Injuries | +1.3% | Asia-Pacific core, spill-over to MEA & South America | Medium term (2-4 years) |

| Rising Adoption of Fish-Skin Xenografts | +1.1% | Global, early uptake in North America & Europe | Medium term (2-4 years) |

| Surge in Battlefield & Disaster-Response Procurement | +0.9% | North America, technology transfer to allies | Short term (≤ 2 years) |

| Shift from Inpatient to Outpatient Wound Centers | +0.7% | North America & EU, gradual Asia-Pacific rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Diabetic Foot Ulcers

Escalating diabetes incidence keeps chronic ulcers front-of-mind for payers and providers. CMS now requires a documented 50% area reduction after four weeks of standard care before covering biologic dressings[1]Centers for Medicare & Medicaid Services, “Local Coverage Determination for Cellular and Tissue-Based Products,” cms.gov, anchoring biologics in step-therapy protocols, and rewarding formulations with randomized-trial data. Platelet-derived growth-factor gels show 48% complete-healing rates versus 25% with conventional dressings, a difference that resonates in value-based purchasing. Japan’s early adoption of basic fibroblast growth factor reinforces the commercial payoff when regulation and reimbursement converge. Asia-Pacific’s population is aging, and surging diabetes prevalence intensifies demand curves. Parallel growth of outpatient wound centers channels purchasing toward biologics with quick-healing properties, ensuring formulary placement in ambulatory settings.

Increasing Incidence of Burns & Road-Traffic Injuries

Rising industrial accidents and climate-related disasters have pushed burns to the fastest-growing wound type at a 9.75% CAGR to 2030. Emergency departments are moving toward biologic matrices that lower infection risk and accelerate granulation. FDA clearance of plant-based Traumagel[2]PR Newswire, “FDA Approves Traumagel for Military and Civilian Use,” prnewswire.com for battlefield trauma underscores civilian adoption of defense-driven biotech. Copper-impregnated matrices outpace traditional silver dressings in wound-closure speed and have earned approvals in more than 25 countries. Emerging-market trauma units favor cost-efficient xenografts that require minimal cold-chain logistics yet deliver high epithelialization rates.

Government Reimbursement Expansions for Advanced Wound Care

CMS’s 2025 outpatient payment update introduces codes for caregiver-training time, acknowledging that biologic dressings demand specialized application skills. Europe’s cross-country harmonization around CE-marked biologics opens multi-jurisdiction marketing with one dossier, compressing launch timelines. The Alliance of Wound Care Stakeholders continues to lobby for fair payment on autologous platelet-rich plasma, signaling where manufacturers can bridge evidence gaps. ConvaTec’s public welcome of delayed LCD enforcement[3]ConvaTec Group, “ConvaTec Welcomes the Postponement of Local Coverage Determinations on Skin Substitutes in the United States,” ConvaTec Group, convatecgroup.com suggests that well-capitalized firms see tighter evidence rules as a moat rather than a hurdle.

Surge in Battlefield & Disaster-Response Procurement of Biologics

Defense contracts fund rapid prototyping of hemostatic and regenerative dressings; the Pentagon allocates USD 1.66 billion for chemical-biological defense[4]U.S. Department of Defense, “Chemical and Biological Defense Program Budget Justification FY 2025,” U.S. Department of Defense, comptroller.defense.gov in fiscal 2025, with a line item for wound therapeutics. KCI USA’s USD 340 million Federal Supply Schedule award illustrates scale. Disaster-response agencies now seek shelf-stable biologics deployable by non-specialists, prompting product engineering around room-temperature storage, single-use applicators, and color-change indicators for bacterial load.

Restraints Impact Analysis of Global Wound Care Biologics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure & Product Cost | -1.4% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Stringent Tissue-Bank Regulations | -0.8% | North America & EU, spill-over to regulated markets | Medium term (2-4 years) |

| Supply-Chain Fragility For Placental / Amniotic Raw Material | -0.6% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Growing Antimicrobial-Resistance Scrutiny | -0.5% | Global, regulators in North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure & Product Cost

The United States spends USD 96.8 billion each year treating chronic wounds, yet reimbursement caps force clinicians to ration biologics across patients. LCDs restrict usage to eight applications within 12-to-16-week episodes, compelling product selection based on probability of full closure within that window. ConvaTec’s 6.7% wound-care revenue growth in the first half of 2024 shows that competitively priced biologics can still win share amid budget pressure. In emerging markets, tiered-pricing models that align with local purchasing power are becoming critical for market entry.

Stringent Tissue-Bank Regulations

The FDA proposal to classify antimicrobial dressings with higher resistance risk as Class II or III devices lengthens approval times and raises compliance costs. Tissue-bank audits, especially for amniotic-derived products, can shutter supply chains overnight. These hurdles drive interest in synthetic and biosynthetic scaffolds that bypass human-tissue sourcing and enjoy clearer regulatory pathways.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Global Wound Care Biologics Market Segment Analysis

By Product:

Matrices Hold the Lead, Xenografts AccelerateAcellular dermal matrices retained a 37.12% wound care biologics market share in 2025, buoyed by widespread surgeon familiarity and payer coverage for reconstructive needs. Xenografts—propelled by fish-skin pioneers such as Kerecis—are expanding at a 10.23% CAGR, outpacing all other categories. Placental and amniotic membranes face episodic shortages as tissue-bank scrutiny intensifies, steering formulary committees toward synthetic scaffolds that promise consistent supply. FDA clearance of only one growth-factor product (Regranex) leaves a white space for next-generation carriers able to stabilize sensitive proteins while meeting new antimicrobial standards.

Growth-factor sprays are being reformulated with polymer micro-capsules to prolong bioactivity in exudative wounds. Hybrid biosynthetic dressings combine silicone backings with fish-skin grafts, enabling rapid drainage without sacrificing moisture balance. Within hospital value-analysis committees, total cost-of-care calculators highlight shorter length-of-stay when biologic matrices are deployed early, helping justify higher acquisition prices. Xenograft suppliers emphasize disease-specific protocols—diabetic foot ulcers, pressure injuries, and oncology excisions—providing targeted clinical pathways that resonate with evidence-based purchasing. As payer audits intensify, products capable of delivering documented 50% area reduction within four weeks will secure coding priority, reinforcing the segment hierarchy inside the wound care biologics market.

By Wound Type:

Ulcer Dominance Faces a Burn UpswingUlcers represented 62.15% of the wound care biologics market size in 2025, confirming their primacy in the wound care biologics market. Within that group, diabetic foot ulcers account for the largest patient pool owing to global diabetes escalation. CMS’s LCD requires proof of prior standard-care failure, effectively channeling biologic spend toward refractory ulcer cohorts. In contrast, burns are on a 9.21% CAGR trajectory—the swiftest within the wound care biologics industry—driven by rising factory incidents in Asia and heat-related disasters elsewhere.

The wound care biologics market size for burn indications is expected to double by 2031 as trauma centers integrate biologics into first-line protocols. Copper-infused matrices deliver shorter epithelialization times against silver dressings, a finding now replicated across 25 regulatory jurisdictions. Military-origin hydrogels suitable for austere settings have migrated to community ERs, reinforcing the burn segment’s momentum. Conversely, pressure ulcers in long-term care settings require cost-attenuated biologics, pushing suppliers toward volume-based contracts with nursing-home networks.

By Distribution Channel:

Offline Still Dominates, Digital Gains SpeedOffline procurement retained 83.72% of the wound care biologics market share in 2025 because biologics need cold-chain custody and clinician hand-off. Yet online portals are growing at 9.58% annually, propelled by telehealth wound-consult models established during the pandemic. Hospital purchasers appreciate e-catalog integrations that automate just-in-time inventory and embed LCD compliance prompts at checkout. Direct-to-consumer channels are rising for maintenance therapies, allowing diabetics to reorder collagen dressing refills using mobile apps that photograph wounds and recommend quantities via embedded AI. The spread of remote-patient-monitoring codes lets providers bill for virtual check-ins when patients upload images, deepening digital-channel adoption. Payment integrity modules inside e-commerce platforms flag off-label usage, protecting providers from post-payment audits and enhancing trust in the online model.

Manufacturers are co-locating regional fulfillment hubs with third-party logistics providers to cut delivery times below 24 hours for critical biologic orders. Temperature-controlled smart packaging logs ambient data, satisfying traceability mandates. Partnerships between telehealth software firms and biologic suppliers embed one-click order buttons inside wound-assessment dashboards, turning clinical recommendations into seamless procurement. Emerging-market clinicians rely on mobile marketplaces that accept micro-batch orders, democratizing access without large inventory commitments. These advances ensure the wound care biologics market can progressively re-balance toward digital channels without compromising handling integrity.

By End-User:

Hospital Strength Meets Outpatient VelocityHospitals and clinics generated 63.88% of the wound care biologics market share in 2025 by managing complex wounds needing surgical debridement and high-acuity biologics. Ambulatory surgical centers (ASCs) are registering the fastest growth at 8.98% CAGR as CMS shifts more procedures to outpatient codes. Within the ASCs, surgeons appreciate biologics that enable same-day discharge with lower infection odds.

Home-care use is expanding thanks to caregiver-training CPT codes and simplified single-application matrices suited for family administration. Specialty wound centers layer AI analytics onto high-resolution photography, triaging patients remotely and deploying biologic kits via overnight courier. Payers see fewer readmissions when post-acute providers use regenerative substrates early, strengthening reimbursement alignment in non-hospital settings.

Geography Analysis

North America Wound Care Biologics Market

North America’s 44.38% of the wound care biologics market size in 2025 rested on mature payer frameworks and broad clinical familiarity with biologics. Yet forecast growth moderates to an 7.78% CAGR as penetration approaches ceiling levels. The VA’s USD 340 million contract with KCI USA underscores government muscle in shaping formularies. Canada leverages Health Canada-FDA reciprocity to accelerate approvals, while Mexico’s private hospitals import U.S.-cleared fish-skin grafts to serve self-pay patients.

Europe Wound Care Biologics Market

Europe is tracking an 8.07% CAGR, supported by CE-mark harmonization that lets manufacturers sell across 27 states using a unified dossier. Germany and the United Kingdom remain volume anchors, but Southern Europe shows quicker percentage growth as austerity budgets loosen. Value-based procurement consortia compare total cost of closure rather than unit price, favoring biologics with trial-backed healing rates. Scandinavian health systems spearhead real-world registries that feed reimbursement recalibration every two years.

APAC Wound Care Biologics Market

Asia-Pacific leads on growth at 9.84% CAGR. China upgrades hundreds of county hospitals with burn units equipped for xenograft application as part of its Healthy China 2030 plan. Japan’s long history with basic fibroblast growth factor eases acceptance of new biologics, while India’s multi-tier price corridors encourage domestic production of collagen matrices. Australia’s Medicare Benefits Schedule newly covers outpatient biologic dressing reviews, expanding rural uptake. Collectively, these forces shift future revenue weight toward Asia, diversifying the wound care biologics market’s geographic footprint.

Mordor Intelligence provides coverage of the global wound care biologics market across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The market sits in a mid-consolidated posture. Organogenesis, Smith+Nephew, Integra LifeSciences, ConvaTec, and Kerecis constitute the top tier, with periodic scale-up via acquisitions such as Gentell’s purchase of Integra’s traditional dressings line. LCD evidence thresholds compel heavy R&D spending; players unable to fund multicenter trials retreat or become acquisition targets. Technology differentiation is pivoting toward multifunctionality—matrices impregnated with antimicrobial ions, hydrogels incorporating controlled-release growth factors, and silicone-backed fish-skin grafts that drain exudate without maceration.

Regulatory shifts also shape rivalry. FDA’s antimicrobial reclassification favors incumbents that already possess biocompatibility data, raising barriers for small entrants. Supply-assured xenografts from non-human sources help firms sidestep tissue-bank volatility and resonate with global regulators wary of donor variability. Digital-care adjuncts—AI wound-sizing algorithms bundled with dressings—offer a service moat beyond the commodity of collagen.

Cost-of-care narratives dominate sales-pitch themes. Products that cut average healing time by even two weeks unlock savings on nursing hours and antibiotics, a message that wins tender points under value-based payment. Manufacturers therefore invest in post-market registry data to document real-world economic gains, wielding those metrics in Payer Evidence Dossiers when renegotiating contracts.

Global Wound Care Biologics Industry Leaders

Convatec Group plc

Integra LifeSciences

Kerecis Ehf

Mölnlycke AB

Smith & Nephew plc

- *Disclaimer: Major Players sorted in no particular order

Global Wound Care Biologics Market Companies Covered in this Report

- Avita Medical

- B. Braun

- Bioventus Inc.

- Coloplast

- Convatec Group plc

- Essity

- Grifols

- Integra LifeSciences

- Kerecis Ehf

- Lynch Biologics

- Marine Polymer Technologies

- Medline Industries

- MiMedx Group Inc.

- Mölnlycke AB

- MTF Biologics

- Organogenesis Holdings

- Skye Biologics Holdings

- Smiths Group

- Solventum Corporation

- Stryker

Recent Industry Developments in Global Wound Care Biologics Market

- April 2025: CMS contractors finalized LCD limits, capping biologic use at eight applications over 12-to-16 weeks and requiring 50% area reduction with standard care before approval.

- August 2024: Traumagel received FDA approval for battlefield and civilian trauma control, exemplifying dual-use biologic pathways.

- May 2024: ConvaTec reported positive data from an advanced-wound-care study, reinforcing its evidence-led growth strategy.

- February 2024: Kerecis launched Shield Standard, a fish-skin graft with silicone backing for chronic and acute wounds.

Global Wound Care Biologics Market Report Scope

As per the scope of the report, wound care biologics refer to products that are used for controlling and healing infections. Wound healing is a complex process involving inflammation, accumulation of tissue, deposition of collagen, and formation of epithelial cell layers. The Wound Care Biologics Market is Segmented by Product (Biological Skin Substitutes and Topical Agents), Wound Type (Ulcers, Surgical and Traumatic Wounds, and Burns), End-User (Hospitals/Clinics, Ambulatory Surgical Centers, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

Segmentation Overview

| Acellular Dermal Matrices |

| Amniotic & Placental Membranes |

| Xenografts |

| Synthetic & Biosynthetic Scaffolds |

| Growth-Factor & Cell-based Topical Agents |

| Other Products |

| Ulcers | Diabetic Foot Ulcers |

| Venous Ulcers | |

| Pressure Ulcers | |

| Other Ulcers | |

| Surgical & Traumatic Wounds | |

| Burns |

| Online |

| Offline |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Home-Care Settings |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Acellular Dermal Matrices | |

| Amniotic & Placental Membranes | ||

| Xenografts | ||

| Synthetic & Biosynthetic Scaffolds | ||

| Growth-Factor & Cell-based Topical Agents | ||

| Other Products | ||

| By Wound Type | Ulcers | Diabetic Foot Ulcers |

| Venous Ulcers | ||

| Pressure Ulcers | ||

| Other Ulcers | ||

| Surgical & Traumatic Wounds | ||

| Burns | ||

| By Distribution Channel | Online | |

| Offline | ||

| By End-User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Home-Care Settings | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How are recent CMS Local Coverage Determinations reshaping purchasing decisions for wound care biologics?

The LCDs tie reimbursement to documented wound-area reduction after four weeks of standard care, so hospitals now prioritize biologics backed by strong clinical evidence and clear protocols.

What product features are gaining traction among clinicians treating chronic ulcers?

Clinicians increasingly prefer biologic dressings that pair regenerative scaffolds with antimicrobial elements, reducing infection risk while accelerating tissue formation.

Why are fish-skin xenografts attracting interest from supply-chain managers?

Fish-skin sources bypass human-tissue regulations and cold-chain constraints, offering more predictable availability and fewer compliance hurdles for procurement teams.

How is the outpatient shift influencing formulation requirements for advanced dressings?

Products now emphasize ease of application, single-use packaging, and room-temperature stability to suit ambulatory surgical centers and home-care environments.

Which competitive strategies are market leaders using to defend share against new entrants?

Established firms bundle digital wound-assessment tools and post-market data registries with their products, creating an integrated care ecosystem that’s difficult for newcomers to replicate.

What impact does antimicrobial-resistance scrutiny have on product development pipelines?

Manufacturers are investing in copper, peptide, and controlled-release technologies to meet forthcoming resistance standards and secure smoother regulatory pathways.

Page last updated on: