Wireless Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.16 Billion |

| Market Size (2031) | USD 32.29 Billion |

| Growth Rate (2026 - 2031) | 12.18% CAGR |

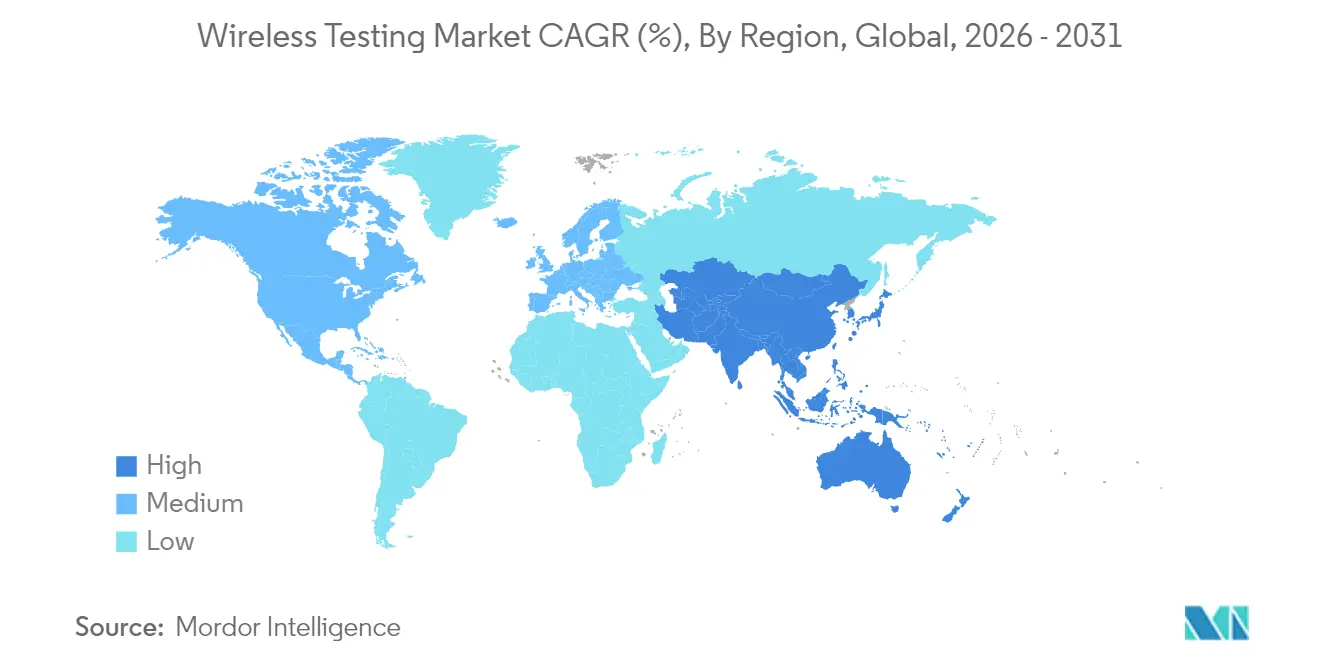

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

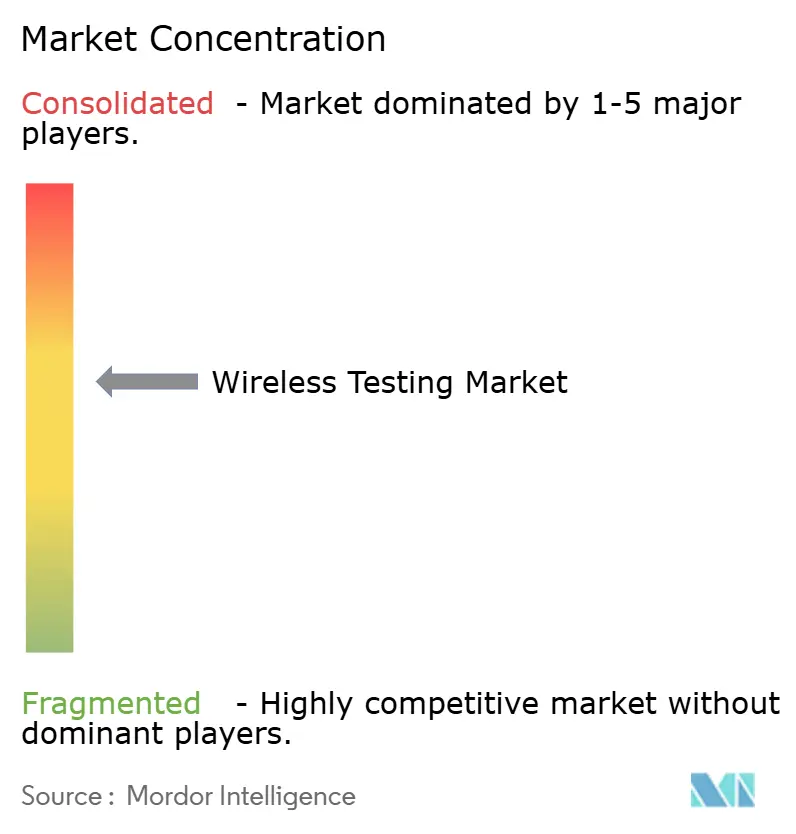

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wireless Testing Market Analysis by Mordor Intelligence

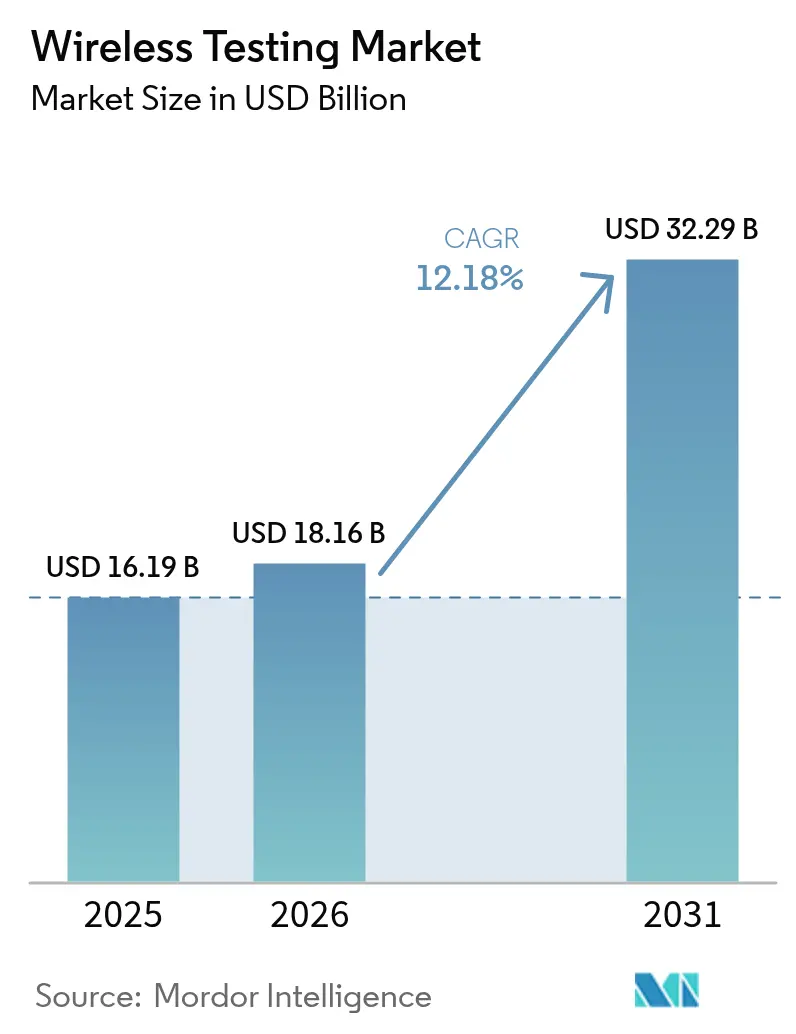

The Wireless Testing Market size is expected to grow from USD 16.19 billion in 2025 to USD 18.16 billion in 2026 and is forecast to reach USD 32.29 billion by 2031 at 12.18% CAGR over 2026-2031.

Ongoing migration to 5G-Advanced networks, the rapid spread of multi-radio IoT devices, and the European Union’s cybersecurity mandate for radio equipment are expanding verification scope well beyond traditional electromagnetic compatibility checks. At the same time, national operators in China, Japan, and the United States are investing billions of dollars in open-interface architectures that demand real-time validation of beamforming, massive-MIMO, and network-slicing performance under live traffic loads. These conditions are steering the wireless testing market away from reactive pass-fail compliance toward predictive, AI-driven validation frameworks capable of flagging service degradations before field rollout. Competitive dynamics now favor test houses and equipment vendors that can combine cloud-native automation, cybersecurity analytics, and end-to-end protocol expertise inside a unified service bundle.

Key Report Takeaways

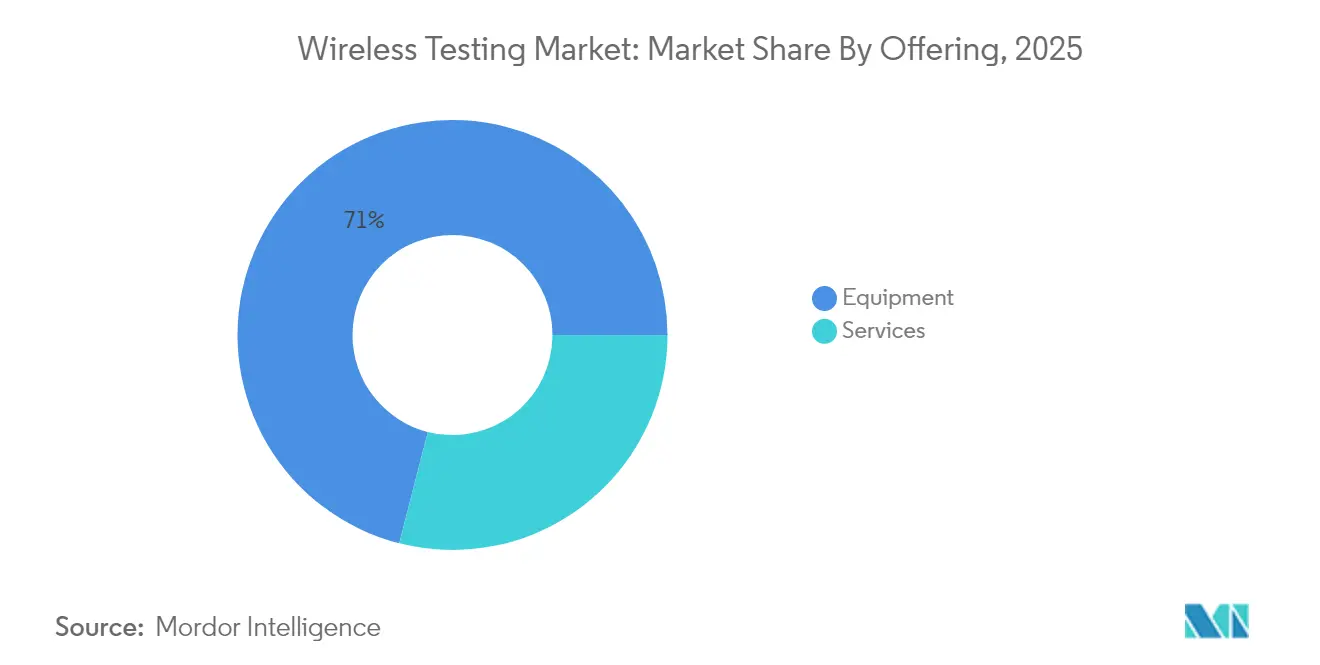

- By offering, equipment accounted for 71.02% of the wireless testing market share in 2025, while managed testing services are set to expand at an 11.05% CAGR through 2031

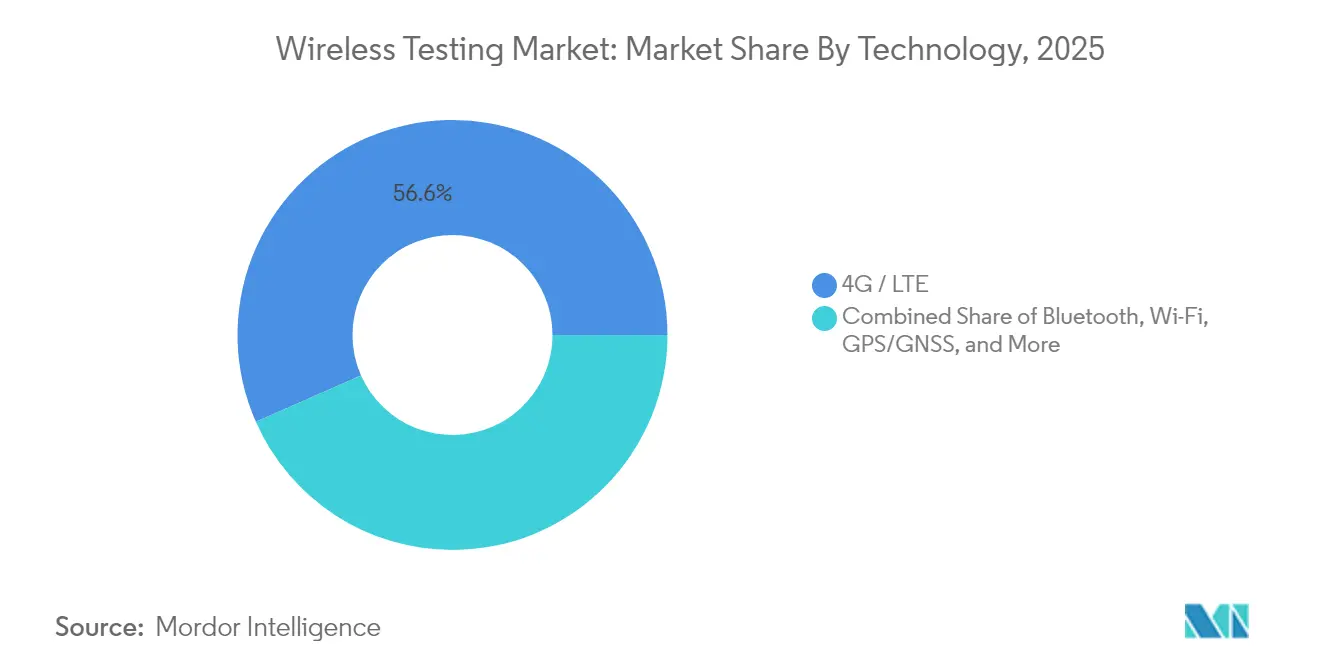

- By technology, cellular (LTE + 5G) held 56.62% revenue share in 2025; the 5G segment alone is projected to register an 18.2% CAGR to 2031

- By application, consumer electronics captured 33.55% of the wireless testing market size in 2025; automotive connectivity is advancing at a 14.72% CAGR between 2026-2031

- By geography, North America led with 32.18% revenue share in 2025, whereas Asia-Pacific is expected to log a 12.63% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wireless Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of 5G infrastructure | 3.20% | China and the United States deployment hubs | Short term (≤ 2 years) |

| AI-driven self-healing networks need predictive test analytics | 1.70% | Early adoption in developed markets worldwide | Long term (≥ 4 years) |

| Growing demand for cloud computing & IoT devices | 1.80% | North America & EU enterprise; APAC manufacturing | Long term (≥ 4 years) |

| Surge in private 5G / industrial wireless networks | 1.90% | North America & EU industrial corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of 5G Infrastructure

Global operators plan to invest USD 259 billion in 5G roll-outs across Asia-Pacific alone by 2030, pushing the wireless testing market toward ultra-wideband, multi-antenna calibration environments that can benchmark massive-MIMO throughput and beam-forming accuracy in near-real time. Japan’s NTT DOCOMO, KDDI, and SoftBank together budget more than USD 13 billion to reach nationwide population coverage, forcing test labs to simulate network-slicing latency and Open RAN interoperability within temperature-controlled chambers that mirror local climatic extremes. These operators now demand holistic validation that covers RF metrics, cloud-native core integration, and service-level key performance indicators. Vendors able to blend channel emulation, traffic generation, and cybersecurity scanning inside a single over-the-air test cycle are capturing premium contracts. As 5G-Advanced capabilities such as non-terrestrial networking materialize, scenario-based testing that blends satellite and terrestrial links is becoming table-stakes, pulling fresh revenue into the wireless testing market.

AI-Driven Self-Healing Networks Needing Predictive Test Analytics

Network orchestration suites now embed large-language-model agents that autonomously tune cell parameters, recover from outages, and reroute traffic, all without human triggers[3]Ericsson, “Autonomous Networks Powered by AI,” ericsson.com. Test strategies, therefore, pivot from static regression scripts to behavioural prediction under stochastic traffic loads. VIAVI Solutions and Northeastern University illustrate this shift by running a city-scale digital twin that spots anomalies minutes before they degrade throughput. Certification workflows must certify AI decision-paths, training-data integrity, and model bias across thousands of simulated failure events. This complexity lifts average engagement sizes, with buyers asking for continuous validation as a service rather than once-off device approvals. Providers that combine hardware-in-the-loop, containerized emulation, and explainable-AI dashboards are driving new benchmarks for wireless testing market competitiveness.

Growing Demand for Cloud Computing and IoT Devices

Enterprises accelerating cloud adoption run multitudes of battery-powered IoT sensors that hop between public and private networks, each with strict uptime and data-privacy thresholds. Test sequences must prove proper behavior across low-power states, co-existence with legacy radios, and resilience against coordinated cyberattacks mandated under the EU’s August 2025 Radio Equipment Directive. Device makers increasingly outsource this burden to third-party labs that maintain accreditation for emerging EN 18031 cybersecurity standards, stimulating high-margin service revenue. The result is a virtuous cycle where demand for predictive test analytics feeds back into continuous-integration pipelines, tightening bonds between firmware updates and validation certificates. As industrial IoT expands into condition monitoring and digital-twin asset tracking, the wireless testing market secures fresh spend from sectors that historically relied on wired links.

Surge in Private 5G/Industrial Wireless Networks

Manufacturing hubs across North America, Germany, and Southeast Asia deploy dedicated 3.5 GHz factory grids to automate machine vision and real-time robotics. These facilities require latency-focused acceptance tests that measure time-sensitive networking hand-offs, electromagnetic resilience near heavy machinery, and seamless handovers between indoor cells. Specialist labs offering onsite channel sounding, spectrum auditing, and client-edge performance monitoring win multi-year framework deals, elevating recurring revenue streams. Equipment suppliers are refreshing product lines with portable spectrum analysers and cloud-linked protocol decoders designed for ruggedized plant floors, reinforcing the wireless testing market momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced test equipment & skilled labour | -1.80% | Global; sharpest in developing regions | Long term (≥ 4 years) |

| RF-component supply-chain volatility is delaying calibration cycles | -1.10% | Asia-Pacific sourcing concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Test Equipment and Skilled Labour

Advanced 5G channel emulators and millimeter-wave signal generators now surpass USD 1 million per station, with lifetime support contracts adding 40% to ownership cost over five years. As test complexity rises, certified RF engineers command six-figure salaries that many domestic labs in emerging economies cannot match. Market leaders such as Keysight generated USD 4.98 billion in fiscal 2024 revenue, underscoring scale advantages that allow bulk component sourcing and multi-site asset utilization. Smaller competitors left to rent time on shared chambers face thin margins and elongated payback periods. This cost asymmetry encourages industry consolidation, with acquisition-driven platforms integrating regional labs into global networks to pool talent and equipment.

RF-Component Supply-Chain Volatility Delaying Calibration Cycles

Persistent shortages in low-phase-noise oscillators and high-frequency attenuators hamper scheduled recalibration of spectrum analysers, forcing test houses to extend maintenance windows and reschedule customer slots[4]SEMI, “Worldwide Semiconductor Equipment Outlook,” semi.org. Semiconductor equipment investments are forecast to reach USD 139 billion by 2026, yet allocation favors high-volume fabs, leaving niche RF parts in short supply. Qorvo’s 2025 pivot toward premium handset components illustrates how shifting fab priorities can obsolete legacy test fixtures mid-cycle, adding unexpected capital outlays. Labs operating on thin margins struggle to absorb these shocks, occasionally pausing accreditation renewals until fresh component batches arrive. Such disruptions trim capacity and stretch delivery lead-times, placing a drag on near-term wireless testing market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Equipment Dominance Faces Service Disruption

Equipment generated USD 11.5 billion in 2025, equal to 71.02% of wireless testing market share, but its grip is loosening as managed testing services outpace at an 11.05% CAGR through 2031. Capital-intensive signal generators, over-the-air chambers, and channel emulators form the backbone of every lab, yet buyers increasingly question ownership when firmware refresh cycles arrive annually. The wireless testing market size attributable to managed services will therefore close the gap as customers prioritize fast certification turnarounds over capital budgets. Tier-one vendors help this transition by bundling cloud-linked analytics dashboards, enabling remote monitoring of pass-fail metrics in near real time. In parallel, government-funded facilities such as the USD 21.7 million VALOR lab in Arizona open subscription-based access to specialty Open-RAN interoperability suites, accelerating the shift toward outcome-based engagements. For equipment makers, rental programs and usage-based pricing mitigate cannibalization while keeping utilization rates high.

Professional service providers leverage AI-assisted test-script generation and automated report templates to slash project cycle times. This agility resonates with start-ups launching multi-standard IoT gadgets that must secure global market entry within months. Meanwhile, established handset brands still purchase top-end gear to protect intellectual property, ensuring the equipment segment retains sizable absolute revenue even as its share declines. Overall, dual-track demand sustains the wireless testing market while encouraging hybrid business models that blend hardware leasing, managed compliance, and continuous regression testing on shared infrastructure.

By Technology: 5G Acceleration Outpaces Legacy Standards

4G/LTE protocols accounted for 56.62% of 2025 revenue, but inside that umbrella, the 5G slice will lift the wireless testing market size by an 18.2% CAGR to 2031. Sub-6 GHz and millimeter-wave test routines now include dynamic spectrum-sharing verification, non-stand-alone to stand-alone migration checks, and slicing-aware throughput analytics. Laboratories thus retool benches with vector-signal-analyser bandwidths exceeding 2 GHz and multi-antenna anechoic chambers large enough for 64T64R arrays. Rohde & Schwarz and Qualcomm recently demonstrated 13 GHz links for pre-6G use-cases, hinting at escalating frequency coverage requirements. Wi-Fi remains vital: tri-band Wi-Fi 7 adds 320 MHz channels and multi-link operation, demanding concurrent verification of 2.4 GHz, 5 GHz, and 6 GHz radios. Bluetooth Low Energy retains prominence in wearables, yet new high-speed modes require updated packet-error-rate and coexistence benchmarks that stretch legacy analysers.

The coexistence of cellular, Wi-Fi, UWB, and satellite links inside single devices forces combinatorial test matrices. Equipment vendors respond with modular architectures where software-defined radio cards swap in frequency-specific front ends, prolonging chassis life. Service providers differentiate by offering library-based simulation of country-specific regulatory masks, compressing certification timelines for global launches. Consequently, technology diversification solidifies recurring revenue streams, anchoring the wireless testing market against single-protocol downturns.

By Application: Automotive Transformation Drives Innovation

Consumer electronics still led with 33.55% revenue in 2025, yet connected-vehicle platforms will lift automotive test spend at a 14.72% CAGR. Vehicle-to-everything links must display sub-millisecond latency and functional-safety compliance under Doppler shifts and metallic multipath unique to moving chassis. This pushes labs to adopt hardware-in-the-loop rigs that inject synthetic traffic scenarios during over-the-air measurements. Bureau Veritas and Intertek deploy end-to-end suites covering NFC payment validation, Wi-Fi hotspot functionality, and 5G telematics security testing. Parallel demand persists from medical devices, aerospace, and smart-grid controllers, each enforcing its own coexistence and reliability checklists. Cross-industry learning accelerates innovation: test cases born in surgical implants now inform automotive cybersecurity audits, and vice versa. As autonomy levels climb, AI sensor-fusion stacks enter validation scope, opening another frontier for the wireless testing market.

Growth in enterprise network upgrades keeps IT & telecommunications spending steady, while energy utilities adopt LTE-M and NB-IoT meters to balance renewable inputs. Each vertical compound's protocol overlaps, making multi-standard certification indispensable. In response, certification bodies weave horizontal frameworks that reuse base RF tests across verticals, saving clients both time and cost and reinforcing long-term service contracts.

Geography Analysis

North America commanded 32.18% revenue in 2025 thanks to early 5G rollouts, large defense budgets, and an entrenched ecosystem of tier-one equipment vendors. Keysight’s USD 4.98 billion 2024 revenue underlines the depth of local R&D expenditure that continually spins off next-generation oscilloscopes and channel emulators. Federal support strengthens domestic labs, exemplified by the National Telecommunications and Information Administration backing VIAVI’s Open-RAN test center with USD 21.7 million, guaranteeing local access to future-proof validation environments. Automotive and aerospace primes further amplify demand by integrating secure private 5G networks inside production campuses, a trend that funnels complex compliance projects into regional service providers.

Asia-Pacific is shaping up as the fastest-growing territory, with a projected 12.63% CAGR. China Mobile, China Unicom, and China Telecom together plan more than USD 3 billion in 5G-Advanced upgrades during 2025, including 400,000 base-station refits that each require acceptance measurements for beamforming and edge-computing latency. Japan’s operators allocate an additional USD 14 billion for dense-urban coverage and Open-RAN pilots, creating parallel streams of lab and field-test activity. Manufacturing-heavy economies such as South Korea and Taiwan overlay private mid-band grids across chip fabs, spawning intricate coexistence checks between Wi-Fi 7, 5G, and industrial TSN protocols. Consequently, regional certification houses invest in multi-standard chambers and AI-enabled log-analysis engines to absorb surging workload, ensuring the wireless testing market maintains double-digit growth.

Europe retains a pivotal role by anchoring global regulatory frameworks. The Radio Equipment Directive’s August 2025 cybersecurity clauses mandate security vetting alongside RF and EMC checks, broadening test engagement scope and extending project timetables. Germany hosts leading manufacturers such as Rohde & Schwarz, which reported EUR 2.93 billion (USD 3.13 billion) in fiscal 2024 revenue and continues expanding turnkey Bluetooth and Wi-Fi suites. Nordic countries pioneer private 5G ports and mining sites, stimulating over-the-air interference studies under arctic conditions. Southern Europe accelerates smart-meter deployments, linking energy-sector needs with telecom test architectures. Together, these initiatives stabilize European demand and feed global standardization efforts that ultimately harmonize testing criteria, benefiting the wider wireless testing market.

Competitive Landscape

The wireless testing market exhibits moderate consolidation, with the top five providers controlling an estimated 55-60% of global revenue. Keysight, Rohde & Schwarz, and Anritsu uphold leadership through continuous instrument refreshes that stretch from sub-GHz spectrum to THz exploratory bands. Strategic partnerships amplify reach: Rohde & Schwarz teamed with Ceva to unveil the industry’s first Bluetooth over-the-air test mode, eliminating cabled fixtures, accelerating wearable device throughput checks. Similarly, VIAVI collaborates with ETS-Lindgren to integrate Massive-MIMO chambers that validate Open-RAN radio units under realistic array steering scenarios.

Software-centric entrants challenge incumbents by delivering cloud-hosted regression farms where engineers upload firmware and receive pass-fail analytics within hours. Their pay-per-use pricing resonates with IoT start-ups and regional handset makers, forcing legacy vendors to offer subscription tiers atop hardware. M&A activity remains brisk as scale economics reward broad protocol coverage and distributed lab footprints. Test houses snap up niche cybersecurity specialists to bundle penetration testing within certification packets, while instrument firms acquire AI start-ups that automate waveform analysis. Market differentiation now revolves around end-to-end capability: customers favor suppliers that certify physical layer metrics, simulate network behaviours, and audit data-protection compliance in one integrated workflow, reinforcing the wireless testing market’s shift toward holistic platforms.

Defensive strategies hinge on intellectual property protection and standards-body influence. Leading vendors chair 3GPP and IEEE working groups, shaping forthcoming protocol drafts to align with their measurement roadmaps. They also deploy digital marketplaces where third-party developers sell automated test scripts, raising switching costs. Competitive pressure nonetheless intensifies as open-source toolchains mature, allowing smaller labs to replicate baseline tests cheaply. Consequently, tier-one providers emphasize premium features such as AI-driven anomaly detection and quantum-safe security validation to preserve margin moat. Over the next five years, the wireless testing industry is likely to settle into an oligopoly of global platforms flanked by regional specialists serving high-regulation verticals.

Wireless Testing Industry Leaders

SGS SA

Bureau Veritas SA

Intertek Group plc

DEKRA SE

Anritsu Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Chroma ATE launched the HDRF3 platform for Wi-Fi 6E/7 and 5G FR1 testing, trimming software-migration time by 70% through AI-assisted code conversion.

- March 2025: Rohde & Schwarz and Ceva unveiled the first Bluetooth over-the-air UTP Test-Mode solution, streamlining high-volume production checks.

- February 2025: DEKRA acquired AT4 wireless to expand IoT and EMC capabilities across Industry 4.0 and Automotive 4.0 programs.

- January 2025: VIAVI and ETS-Lindgren deployed an RF-shielded anechoic chamber for Massive-MIMO testing at the federally funded VALOR Lab.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the wireless testing market as all revenues generated from purpose-built equipment and certified third-party services that examine radio devices or networks for conformance, performance, interoperability, electromagnetic compatibility, and safety across licensed and unlicensed bands, from legacy 2G up to emerging Wi-Fi 7 and 5G-Advanced systems.

Scope exclusions include pure-play software emulators that do not directly interact with RF signals, which have been left outside this assessment.

Segmentation Overview

- By Offering

- Equipment

- Wireless Device Testing

- Oscilloscopes

- Signal Generators

- Spectrum Analysers

- Network Analysers

- Wireless Network Testing

- Network Testers

- Network Scanners

- OTA Testers

- Wireless Device Testing

- Services

- Testing and Certification

- Managed Testing Services

- Calibration and Support

- Equipment

- By Technology

- Bluetooth

- Wi-Fi

- GPS/GNSS

- 4G/LTE

- 5G

- Other (2G, 3G, Zigbee, UWB etc.)

- By Application

- Consumer Electronics

- Automotive

- IT and Telecommunication

- Energy and Power

- Medical Devices

- Aerospace and Defence

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- GCC

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed lab managers at accredited test houses in North America, Europe, and Asia-Pacific, procurement heads at handset OEMs, and network quality engineers inside tier-1 operators. These discussions clarified average daily utilization rates, prevailing test fees, and the likely timing of Wi-Fi 7 and 5G RedCap upgrades, thereby refining model assumptions.

Desk Research

We began with detailed reviews of public-domain standards and filings from bodies such as the US Federal Communications Commission, the European Telecommunications Standards Institute, the International Telecommunication Union, and the Global Certification Forum, which outline mandatory test regimes for every major radio technology. Annual statistics from the GSMA on mobile connections, Gartner handset shipment tables, and import-export records from Volza helped us approximate the global device pool.

Regulatory dockets, patent families mined through Questel, and technical papers on IEEE Xplore were then combined with company 10-Ks, investor decks, and press coverage captured via Dow Jones Factiva to map spending patterns across verticals and regions. D&B Hoovers supplied financial splits for listed test vendors, anchoring service-revenue estimates. The secondary sources listed here are illustrative; many additional publications were checked to validate figures and close information gaps.

Market-Sizing & Forecasting

We applied a top-down build that scales the addressable device and infrastructure base (sourced from shipment and installed-base data) by technology-specific penetration of mandatory and voluntary tests, then values each bucket using blended ASPs. Select bottom-up cross-checks, such as rolling up disclosed revenues of leading labs and sampling factory test-station counts at contract manufacturers, were used to challenge and calibrate totals. Key drivers in the forecast include 5G base-station rollout meters, Wi-Fi 7 chipset ramp curves, regulatory revision cadence, and average test-hour pricing trends. Multivariate regression against these variables underpins the 2025-2030 projection.

Data Validation & Update Cycle

Outputs pass a two-step analyst peer review, variance checks against recent contract awards, and currency-normalized comparisons with independent trade metrics before sign-off. We refresh every twelve months, triggering interim updates when material events, such as a new spectrum mandate, shift demand meaningfully.

Why Mordor's Wireless Testing Baseline Earns Confidence

Published estimates often diverge because firms pick different technology scopes, assume varied test penetration rates, or lock models to dissimilar refresh years.

Key gap drivers include whether legacy 2G/3G revenues are still counted, how aggressively 5G private-network demand is projected, and the frequency at which average service prices are re-benchmarked. Our model integrates annual currency rebasing and mid-year regulatory shifts, while others freeze rates longer or extrapolate from limited geographies.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.19 B (2025) | Mordor Intelligence | - |

| USD 15.80 B (2024) | Regional Consultancy A | excludes managed testing services and uses 2024 FX averages |

| USD 22.64 B (2024) | Global Consultancy B | includes OTA sub-markets outside RF conformance and applies aggressive 5G device multipliers |

Taken together, the comparison shows how disciplined scope selection, annual refreshes, and dual-path validation enable Mordor Intelligence to provide a balanced, reproducible baseline that decision-makers can rely on with confidence.

Key Questions Answered in the Report

What is the current size of the wireless testing market?

The wireless testing market size stands at USD 18.16 billion in 2026 and is projected to reach USD 32.29 billion by 2031 at a 12.18% CAGR.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is forecast to post a 12.63% CAGR, powered by aggressive 5G-Advanced deployments in China and large-scale network modernization in Japan.

Why are managed testing services gaining traction over equipment sales?

Escalating protocol complexity and the high cost of owning millimeter-wave chambers make outsourced, outcome-based testing more economical for many device makers.

How do Europe’s 2025 cybersecurity rules affect wireless testing timelines?

The Radio Equipment Directive adds mandatory network-protection and data-privacy checks, extending certification cycles and raising demand for specialized security validation.

Which application area will offer the highest growth in testing demand?

Automotive connectivity leads with a projected 14.72% CAGR as vehicle-to-everything, ADAS, and autonomous driving functions require rigorous low-latency and safety compliance testing.

What technologies will shape next-generation test requirements?

5G-Advanced, Wi-Fi 7, satellite-integrated non-terrestrial networks, and AI-driven self-healing orchestration will all introduce multi-band, multi-layer scenarios that traditional test frameworks cannot address.

Page last updated on: