White Biotech Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

| Market Size (2025) | USD 351.43 Billion |

| Market Size (2030) | USD 444.74 Billion |

| Growth Rate (2025 - 2030) | 4.82% CAGR |

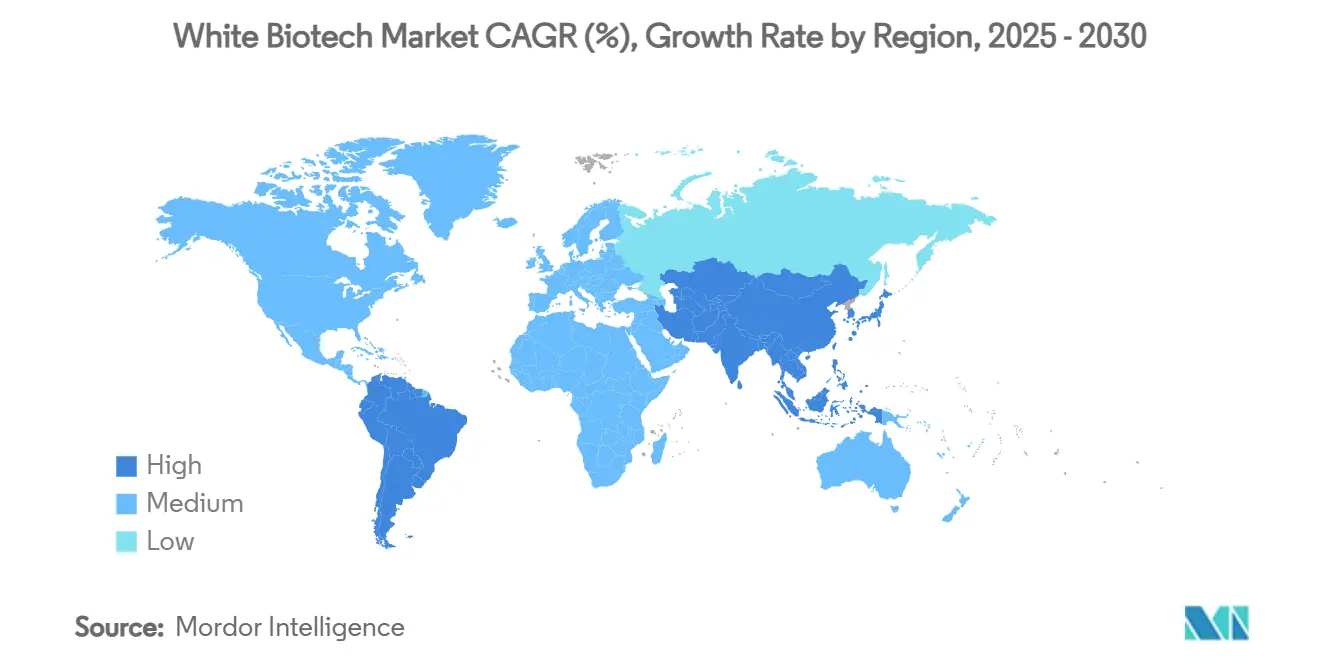

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

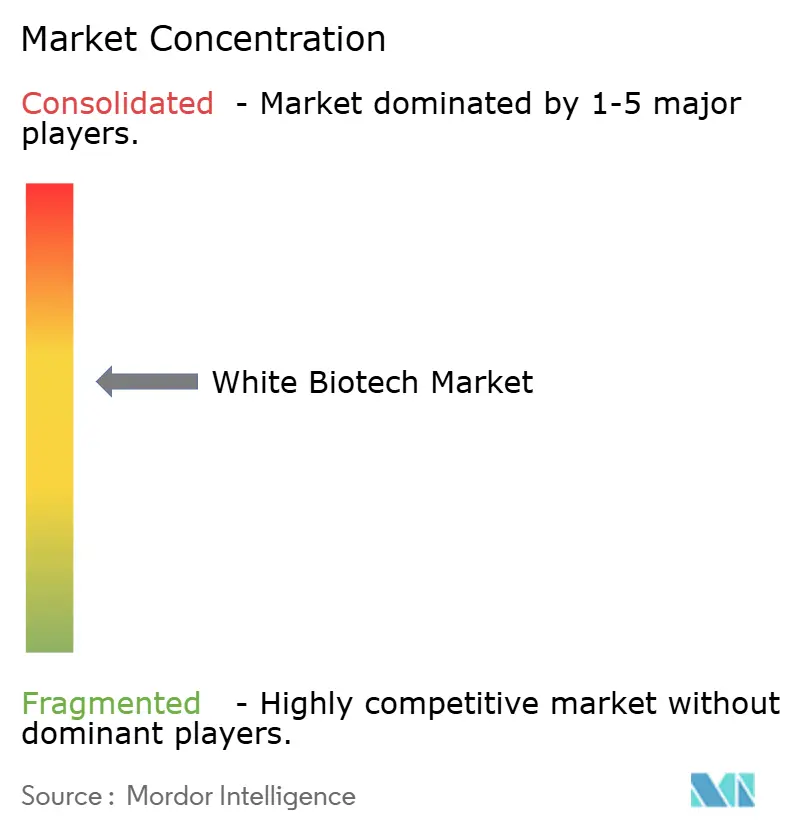

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

White Biotech Market Analysis by Mordor Intelligence

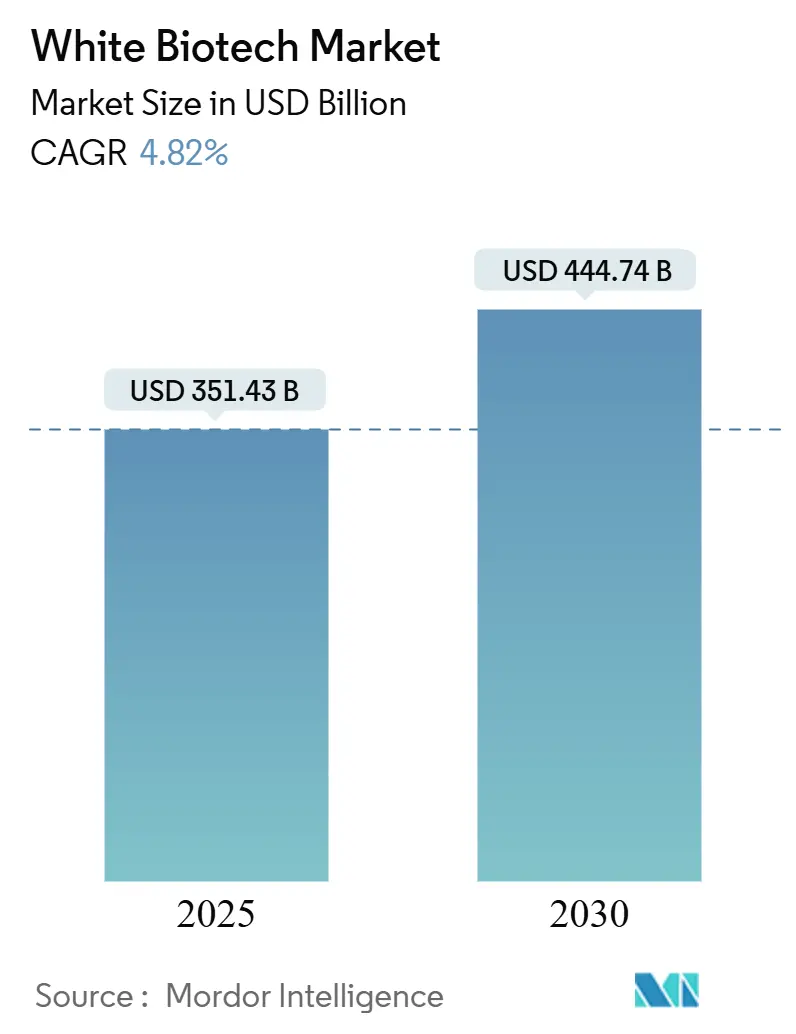

The white biotech market is expected to grow from USD 351.43 billion in 2025 to USD 444.74 billion by 2030, at a CAGR of 4.82%. Industrial biotechnology serves as a key component in transitioning from fossil-based to bio-based manufacturing processes for chemicals, materials, and fuels production. This shift represents a significant advancement in sustainable manufacturing practices, as bio-based processes typically consume less energy, produce fewer emissions, and utilize renewable resources. The integration of white biotechnology across various industrial sectors demonstrates its potential to revolutionize traditional manufacturing methods while addressing environmental concerns.

Key Report Takeaways

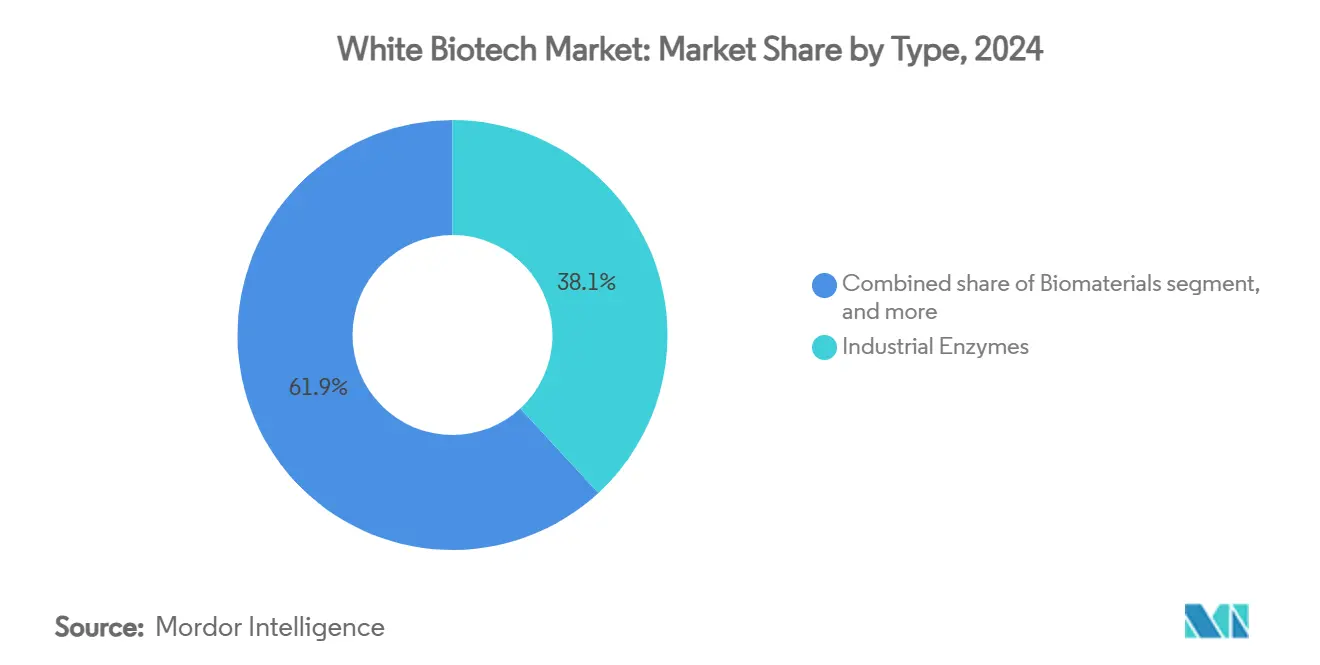

- By product type, industrial enzymes held 38.13% of the white biotech market share in 2024, whereas biofuels are set to register the fastest 5.97% CAGR during 2025-2030.

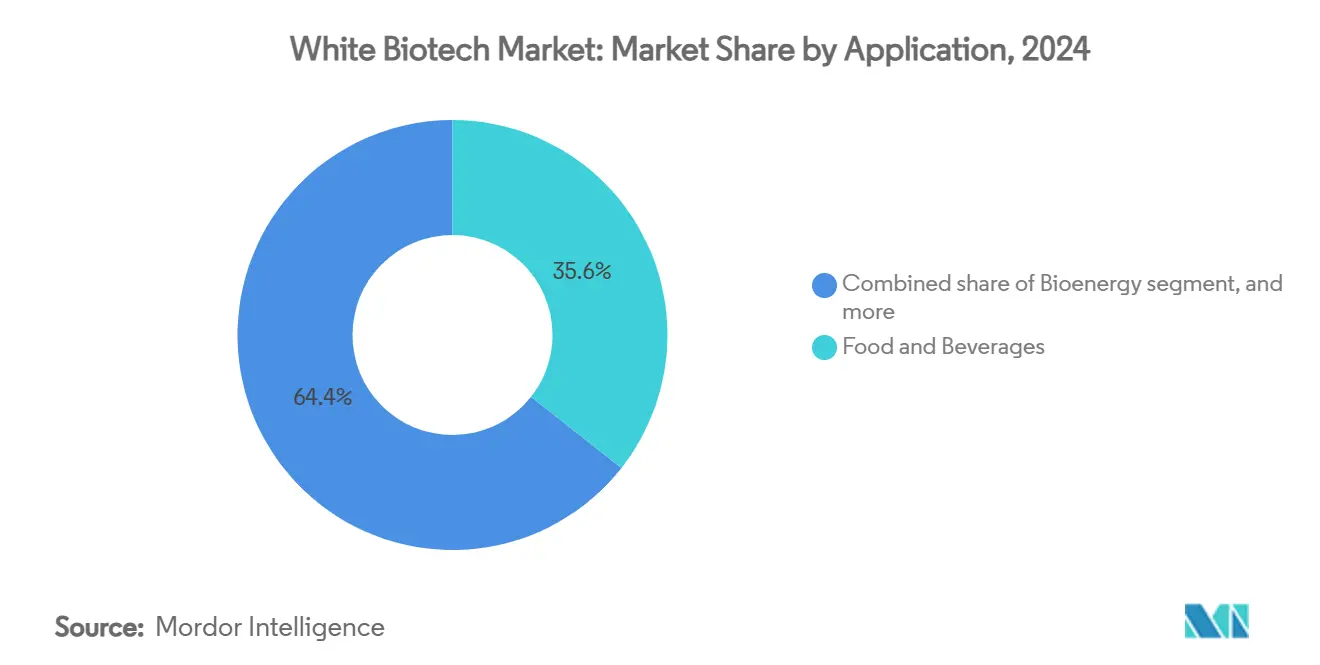

- By application, food and beverages accounted for 34.21% of the white biotech market size in 2024, while bioenergy applications are projected to rise at a 6.01% CAGR through 2030.

- By geography, North America led with a 39.88% revenue share of the white biotech market in 2024; Asia-Pacific is forecast to expand the quickest at a 6.32% CAGR to 2030.

Global White Biotech Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for sustainable industrial processes | +1.2% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Supportive regulatory frameworks and green incentives | +0.8% | North America and Europe, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Advancements in synthetic biology and metabolic engineering | +1.0% | Global, concentrated in United States, China, Europe | Long term (≥ 4 years) |

| Growing adoption of biofuels and bioplastics | +0.9% | Global, strong momentum in Brazil, India | Medium term (2-4 years) |

| Expanding applications of industrial enzymes in food and beverage | +0.6% | Global, particularly strong in Asia-Pacific | Short term (≤ 2 years) |

| Rising consumer preference for bio-based products | +0.5% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

Source: Mordor Intelligence

Increasing Demand for Sustainable Industrial Processes

The Biden Administration's comprehensive biomanufacturing targets for US chemical demand through sustainable processes have increased the adoption of bio-based manufacturing processes. Companies are implementing these processes not only for environmental compliance but also to mitigate risks from fossil fuel price volatility and supply chain uncertainties. The Defense Advanced Research Projects Agency (DARPA) Switch program combines artificial intelligence with synthetic biology to develop adaptable microorganisms, enabling flexible biomanufacturing that responds to changing market demands and raw material availability. This integration of advanced technologies with biological processes represents a significant shift in manufacturing approaches, offering enhanced production capabilities and improved resource utilization across multiple industrial sectors [1]Source: DARPA, "Programmability and Long-Term Stability," darpa.mil.

Supportive Regulatory Frameworks and Green Incentives

Regulatory harmonization across major markets is accelerating biotech commercialization. The EU Biotech Act and the coordinated U.S. regulatory framework from the EPA, FDA, and USDA establish streamlined approval processes, reducing investment uncertainty. The Horizon Europe program has allocated EUR 10 million in seed funding for scaling operations, while the UK has invested GBP 100 million across six engineering biology centers. In Asia-Pacific, China's approval of precision-fermented human milk oligosaccharides indicates increasing regional acceptance. The FDA's establishment of a specialized office within CBER aims to process 10-20 cell and gene therapy approvals annually by 2025, demonstrating expanded regulatory capacity for biotech innovations [2]Source: U.S. Food and Drug Administration, “EPA, FDA, and USDA Issue Joint Regulatory Plan for Biotechnology,” fda.gov.

Advancements in Synthetic Biology and Metabolic Engineering

Recent advances in genome editing are transforming production economics in the biotechnology industry. The Hi-TARGET protocol developed at Vienna University of Technology achieves 100% efficiency in modifying microbial carbon-monoxide metabolic pathways. The discovery of the CelOCE enzyme enables twice the ethanol production from waste biomass through autonomous peroxide generation. The Lynx platform accelerates enzyme optimization through artificial intelligence, while the Manus-Inscripta combination streamlines genome engineering and cell-factory development. Additionally, University of Science researchers demonstrated direct vanillin production from agricultural waste, showcasing metabolic engineering solutions for specialty chemical manufacturing challenges.

Growing Adoption of Biofuels and Bioplastics

Aviation and road transport policy mandates are driving the white biotechnology market toward low-carbon fuel development. The United States has experienced significant growth in sustainable aviation fuel production capacity. The second-generation biofuels market continues to expand with strong growth projections through the next decade. India has become Asia's largest ethanol producer, supported by fuel blending targets. The development of Halomonas engineered strains enables open-tank production of polyhydroxybutyrate bioplastics, reducing water consumption. The U.S. Department of Energy's substantial investment across numerous projects focused on algal and biochemical pathway improvements demonstrates government support for next-generation fuel development.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited availability of cost-effective feedstocks | -0.5% | Global, regional variations in biomass supply | Short term (≤ 2 years) |

| Lack of infrastructure for large-scale fermentation in emerging markets | -0.6% | Asia-Pacific, Latin America, Middle East and Africa | Long term (≥ 4 years) |

| High capital investment and infrastructure requirements | -0.9% | Global, particularly acute in emerging markets | Long term (≥ 4 years) |

| Complexity in scaling up bioprocesses | -0.7% | Global, with technology gaps in Asia-Pacific | Medium term (2-4 years) |

Source: Mordor Intelligence

Limited Availability of Cost-Effective Feedstocks

Regional differences in lignocellulosic biomass availability and fluctuating agricultural commodity prices limit consistent industry expansion across global markets. Brazil has significant sugarcane bagasse resources available for processing, while European manufacturers continue to face intense competition for feedstock from both the energy and paper industries. The adoption of circular feedstock approaches, including agricultural residues and municipal organic waste, is steadily increasing across regions. However, substantial logistics and pre-treatment costs reduce profit margins throughout the supply chain, impacting the white biotechnology industry's near-term growth potential in established and emerging markets.

Lack of Infrastructure for Large-Scale Fermentation in Emerging Markets

Several nations in Asia-Pacific and Latin America possess abundant biomass resources but lack essential infrastructure like stainless-steel reactors, cooling systems, and GMP-compliant utilities. The absence of large-scale contract development and manufacturing organizations forces companies to transport intermediates internationally, reducing environmental benefits. This transportation not only increases operational costs but also creates logistical challenges and extends production timelines. While government incentives address these infrastructure gaps through tax benefits and subsidies, extended procurement periods and equipment import duties lengthen project timelines. Additionally, regulatory compliance requirements and quality control measures in different regions further complicate the process. These combined factors continue to limit the white biotechnology market's growth potential, particularly in emerging economies where the biomass potential remains largely untapped.

Segment Analysis

By Type: Industrial Enzymes Lead Despite Biofuels Acceleration

Industrial enzymes hold a 38.13% market share in 2024, with applications spanning food processing, textiles, and biofuel production. The biofuels segment is growing at a 5.97% CAGR through 2030. The enzyme segment continues to advance through innovations such as Novozymes' Fortiva® Hemi liquefaction enzyme, which improves corn oil and ethanol yields to address the current 40-50% recovery rate limitation in ethanol plants.

The biofuels segment expansion is supported by enzyme discoveries and regulatory frameworks. Brazil's CelOCE enzyme development shows potential to double cellulose conversion efficiency, while India's ethanol production capabilities contribute to regional market growth [3]Source: Science X, “Natural enzyme capable of cleaving cellulose could transform biofuel production,” phys.org. The implementation of advanced biofuel technologies, including precision fermentation and gasification processes, enables commercial-scale production from non-food biomass. These developments address sustainability requirements while meeting aviation industry requirements for sustainable fuel adoption [4]Source: U.S. Department of Energy, “Sustainable Aviation Fuel,” energy.gov.

Note: Segment shares of all individual segments available upon report purchase

By Application: Food and Beverages Dominance Challenged by Bioenergy Surge

Food and beverages applications generated 34.21% of 2024 revenue, driven by enzymes that improve shelf life, texture, and nutritional value in dairy products, bread, and fruit juices. The production of vanillin through precision fermentation of agricultural waste demonstrates how metabolic engineering provides an alternative to traditional plant extraction methods. The market expansion continues with probiotic products like MindAble™ 1714™, which target stress management and gut health segments. Manufacturers implement continuous fermentation processes to minimize batch variations and reduce energy consumption, meeting retailer demands for supply chain transparency.

The bioenergy segment projects a 6.01% CAGR, supported by aviation industry mandates and Department of Energy (DOE) support for algal systems. Airlines' forward purchase agreements for drop-in fuels encourage financial institutions to support larger production facilities. The market diversifies through enzyme-based biogas upgrading and organic waste co-digestion. Improved financial performance enables bioenergy producers to participate in green-hydrogen credit markets, increasing their significance in the white biotechnology market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America held 39.88% of global sales in 2024, supported by an established network of pharmaceutical companies, contract manufacturers, and university spinoffs. Canada's precision-fermentation facilities and Mexico's fill-finish operations complete the regional value chain, though fermentation capacity remains limited compared to Europe. The venture capital ecosystems and intellectual property frameworks in the U.S. and Canada support continuous innovation in biomanufacturing. The increasing federal incentives for biomanufacturing aim to enhance domestic production capabilities and decrease import dependence.

Asia-Pacific is experiencing rapid growth at a 6.32% CAGR through 2030. The U.S. BioSecure Act's restrictions on Chinese suppliers have shifted Western outsourcing to Indian Contract Development and Manufacturing Organizations (CDMOs), increasing investment across South Asia. However, variations in regulatory review timelines may favor project placement in North American and European markets. Growing consumer awareness of sustainable products drives demand, creating opportunities across various Asian markets.

South America benefits from Brazil's sugarcane ethanol production and emerging enzyme discoveries. The Middle East and Africa are attracting initial projects through special economic zone incentives. These regional developments continue to shape the white biotechnology market landscape. The Middle East and African countries are offering incentives through special economic zones to attract biotechnology projects. The United Arab Emirates and Saudi Arabia are incorporating white biotechnology into their economic diversification strategies to decrease their reliance on oil revenues.

Competitive Landscape

The white biotech market demonstrates moderate concentration, where established companies maintain scale advantages while experiencing disruption from technology-driven startups and strategic partnerships. The market landscape is characterized by intense competition among major players who continuously invest in research and development to maintain their market position. The consolidation trend reflects the industry's need for enhanced operational efficiency and expanded technological capabilities to meet evolving market demands.

The market is transitioning toward platform-based competition, driven by technological advancements and increasing demand for innovative solutions. Companies like Ginkgo Bioworks are expanding partnerships across the research and development value chain, using synthetic biology capabilities to reduce product development timelines and commercialization risks. The partnerships facilitate knowledge sharing, resource optimization, and accelerated innovation in biotechnology applications across various industries.

Precision fermentation for food applications presents significant growth opportunities, particularly in developing sustainable protein alternatives and functional ingredients. Companies like Biomatter are introducing AI-powered enzyme optimization platforms that challenge traditional research and development methods, enabling faster product development and improved process efficiency. New market entrants utilize extremophilic bacteria and innovative fermentation methods to address water scarcity and energy consumption challenges, while established companies respond through acquisitions and technology licensing agreements to maintain their competitive edge in this rapidly evolving market.

White Biotech Industry Leaders

-

Lonza Group Ltd

-

International Flavors & Fragrances Inc.

-

Corbion NV

-

DSM-Firmenich AG

-

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Manus Bio and Inscripta merged to establish an industrial biomanufacturing platform that integrates genome engineering with cell factory technologies. The combined entity aims to reduce development times and enhance the economics of bio-based alternatives in the food, beauty, and agriculture markets.

- February 2025: Novonesis acquired DSM-Firmenich's share of the Feed Enzyme Alliance, strengthening its position in the animal nutrition enzyme market.

- November 2024: IFF developed TEXSTAR™, an enzymatic texturizing solution that enhances the texture of dairy and plant-based fermented products. TEXSTAR™ converts sucrose into poly- and oligosaccharides during fermentation through enzymatic processes, improving texture, smoothness, and shine without requiring additional stabilizers, unlike traditional starch-based stabilizers.

Global White Biotech Market Report Scope

White biotechnology, also known as industrial biotechnology, refers to the use of enzymes and microorganisms to produce bio-based products for use in sectors, such as chemicals, food and feed, healthcare, consumer goods, and automotive.

The white biotech market is segmented on the basis of type, application, and geography. Based on type, the white biotech market report is segmented into biofuels, biomaterials, biochemicals, and industrial enzymes. Based on application, the market report is segmented into bioenergy, pharmaceuticals, food and beverage, feed, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

The market sizing has been done in value terms in USD for all the above-mentioned segments.

| By Type | Biofuels | ||

| Biomaterials | |||

| Biochemicals | |||

| Industrial Enzymes | |||

| By Application | Bioenergy | ||

| Pharmaceuticals | |||

| Food and Beverages | |||

| Animal Feed | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Spain | |||

| Netherlands | |||

| Italy | |||

| Sweden | |||

| Poland | |||

| Belgium | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Indonesia | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Colombia | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | United Arab Emirates | ||

| South Africa | |||

| Nigeria | |||

| Saudi Arabia | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle Eastand Africa | |||

| Biofuels |

| Biomaterials |

| Biochemicals |

| Industrial Enzymes |

| Bioenergy |

| Pharmaceuticals |

| Food and Beverages |

| Animal Feed |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle Eastand Africa |

Key Questions Answered in the Report

What is the current size of the white biotech market?

The white biotech market stands at USD 351.43 billion in 2025 and is projected to reach USD 444.74 billion by 2030 at a 4.82% CAGR.

Which segment holds the largest share of the white biotech market?

Industrial enzymes command the largest slice at 38.13% of 2024 revenue.

Which region is growing the fastest in the white biotech market?

Asia-Pacific is forecast to grow the quickest, registering a 6.32% CAGR between 2025-2030.

What is the main driver for white biotech market expansion?

Rising demand for sustainable industrial processes, backed by corporate decarbonization goals and supportive regulations, contributes the biggest positive impact (+1.2% to CAGR).

What are the major restraints facing the white biotech market?a

High capital investment and the lack of large-scale fermentation infrastructure in emerging markets present the most significant hurdles, trimming roughly 0.9% from forecast CAGR.

Page last updated on: July 9, 2025