Microbial Culture Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

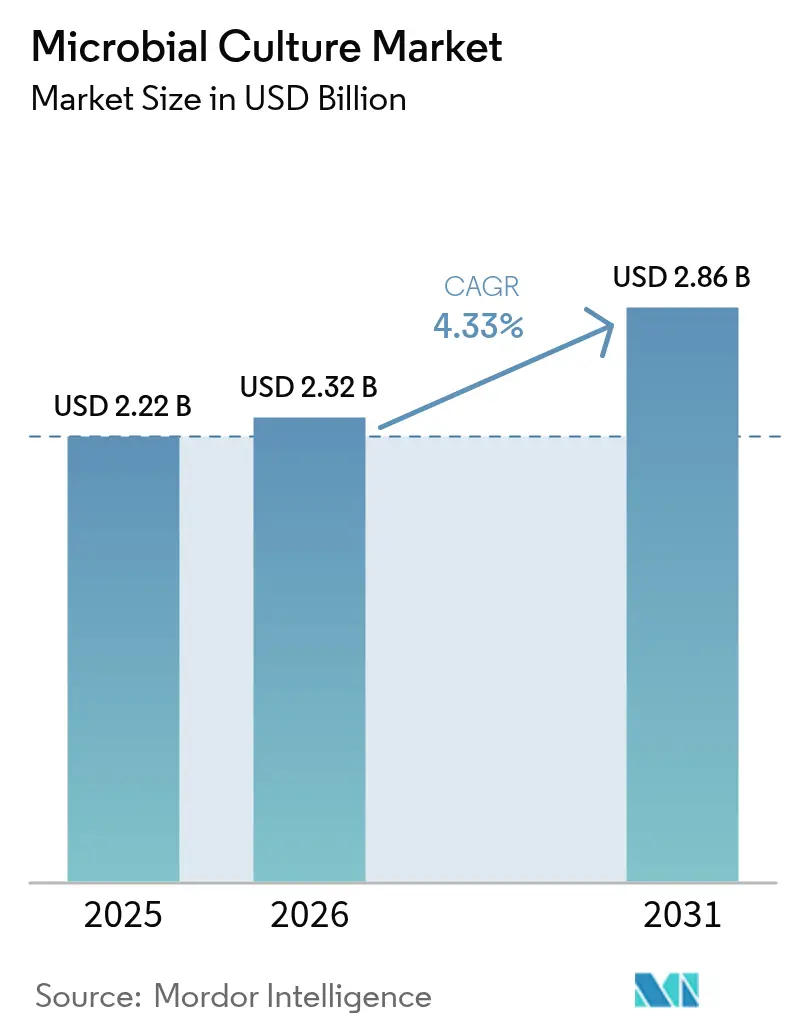

| Market Size (2026) | USD 2.32 Billion |

| Market Size (2031) | USD 2.86 Billion |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Microbial Culture Market Analysis by Mordor Intelligence

The microbial culture market size was valued at USD 2.22 billion in 2025 and estimated to grow from USD 2.32 billion in 2026 to reach USD 2.86 billion by 2031, at a CAGR of 4.33% during the forecast period (2026-2031). Investments are increasingly directed toward precision-fermentation platforms, which offer higher profit margins compared to traditional dairy production methods. Additionally, the rising demand for pharmaceutical-grade cultures is influencing price dynamics for specific bacterial and yeast strains. The market is also being shaped by consolidation among major ingredient suppliers, challenges in cold-chain logistics, and varying regulatory frameworks, which are driving changes in supplier strategies and risk assessments. While Europe remains the largest revenue contributor, the Asia-Pacific region is experiencing the highest incremental growth, driven by China's expanding fermented beverage market and India's growing focus on probiotic dairy products. Competitive advantages in the market are now determined by the depth of strain libraries, bioprotective functionalities, and the ability to achieve dual compliance with food and pharmaceutical standards without delaying market entry.

Key Report Takeaways

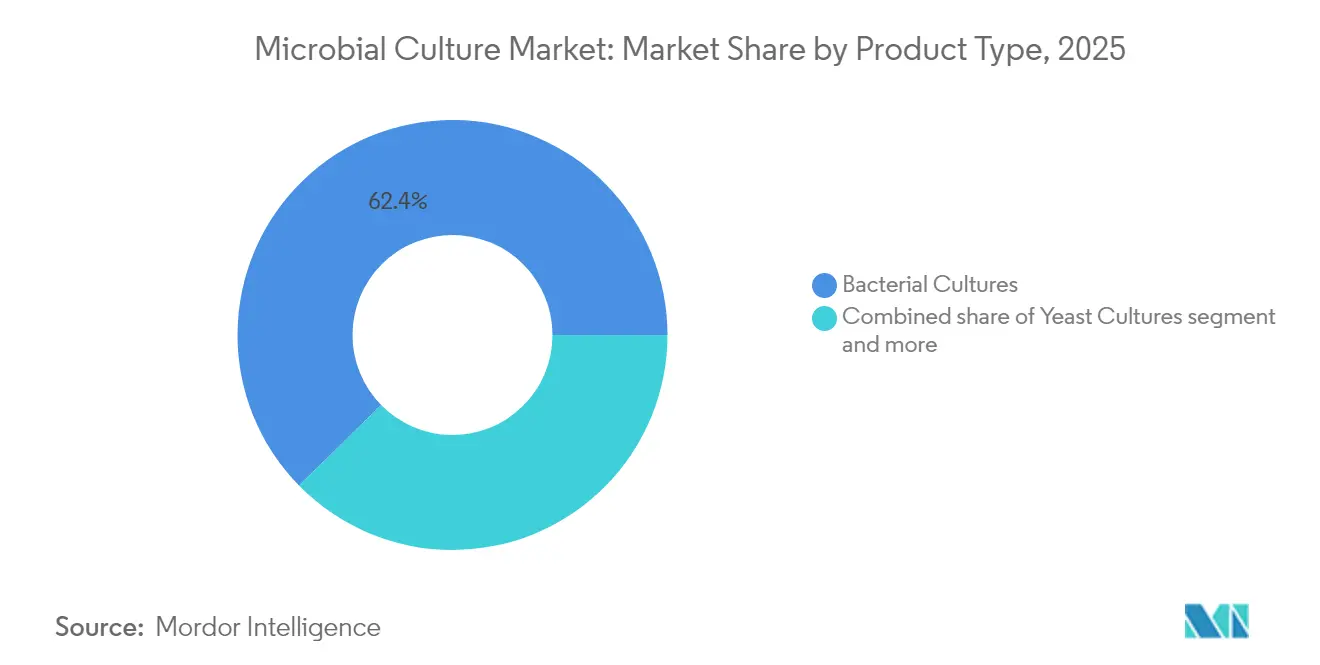

- By product type, bacterial cultures led with 62.35% of the microbial culture market share in 2025, while yeast cultures are projected to register the fastest 6.74% CAGR from 2026 to 2031.

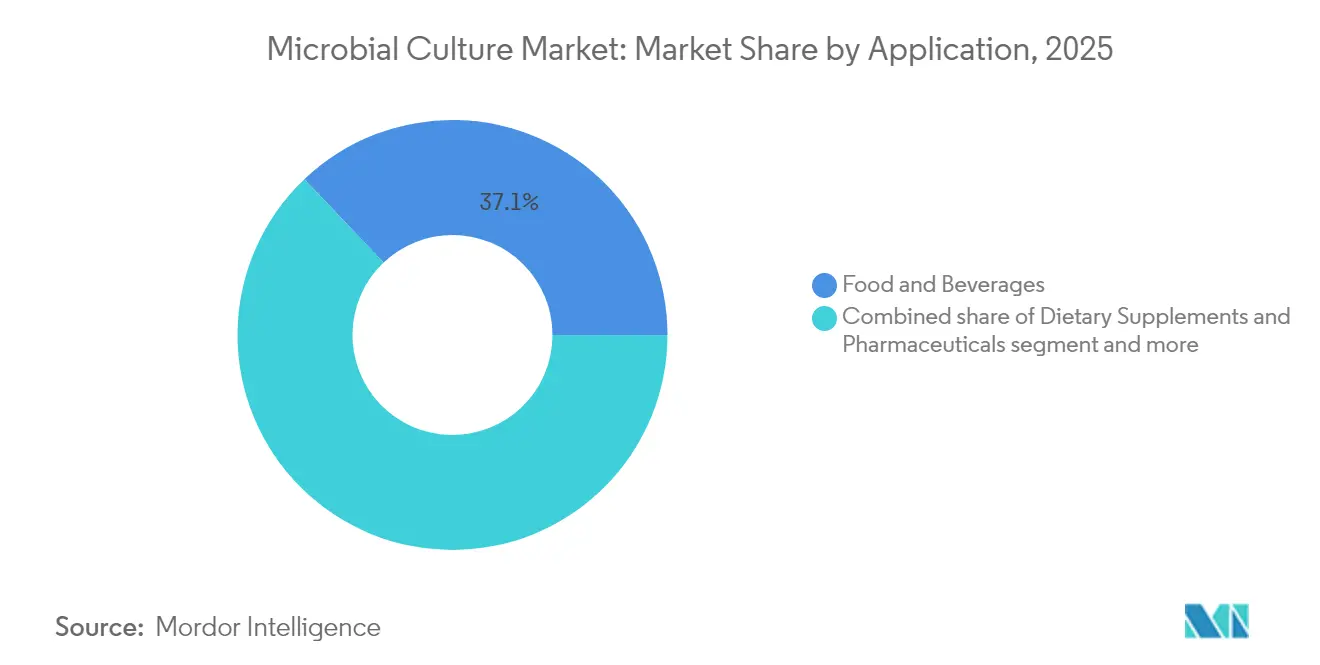

- By application, food and beverages held 37.10% of 2025 revenue, whereas dietary supplements and pharmaceuticals are forecast to expand at a 7.29% CAGR through 2031 in the microbial culture market.

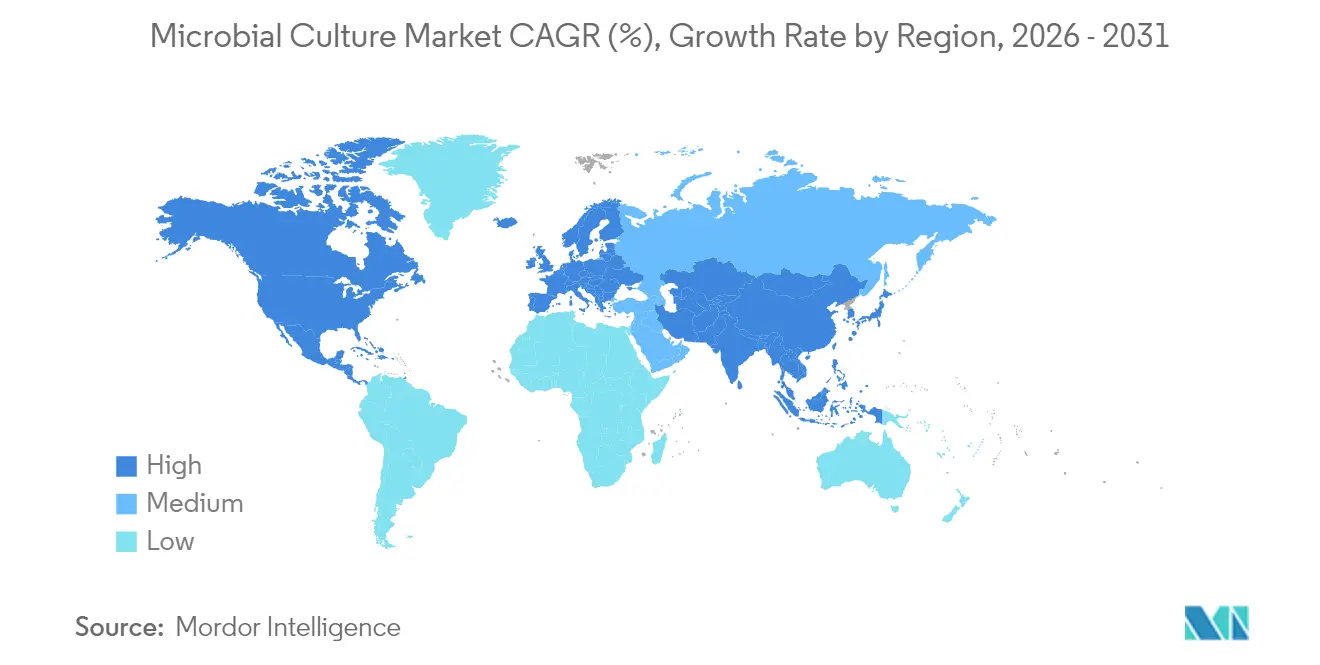

- By geography, Europe captured 31.65% of 2025 sales, but Asia-Pacific will grow the microbial culture market at a leading 5.74% CAGR in the 2026-2031 horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microbial Culture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for probiotic-rich functional foods | +1.2% | Global, with Asia-Pacific and North America leading | Medium term (2-4 years) |

| Expansion of industrial biopharmaceutical fermentation capacity | +0.9% | North America and Europe, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Shift toward clean-label natural preservatives in food and beverage industry | +0.8% | Europe core, North America following | Short term (≤ 2 years) |

| Rapid adoption of precision fermentation for alternative proteins | +0.7% | North America and Europe, pilot projects in Asia-Pacific | Medium term (2-4 years) |

| Carbon-negative bioprocessing incentives in climate policies | +0.5% | Europe (Green Deal), California (LCFS), emerging in China | Long term (≥ 4 years) |

| Rising adoption in agriculture and animal feed | +0.4% | Asia-Pacific core, Latin America, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for probiotic-rich functional foods

Consumer demand for gut-health-focused products is driving significant changes in dairy and beverage portfolios. Probiotic yogurt and kefir now represent over 40% of chilled-dairy shelf space in Western European retailers, reflecting a growing preference for functional foods. Strain-specific claims, such as Lactobacillus rhamnosus GG for immune support and Bifidobacterium lactis HN019 for digestive health, are increasingly transitioning from dietary supplements to mainstream food products. This shift necessitates the development of cultures that can withstand pasteurization, low pH levels, and extended shelf life while maintaining their efficacy. Furthermore, culture suppliers are actively entering co-development agreements with plant-based brands, focusing on creating stable and cost-effective strains capable of fermenting substrates such as oats, soy, or peas without producing off-flavors. These collaborations are critical as plant-based products continue to gain traction among health-conscious consumers. Regulatory developments, such as EFSA's 2024 update to its QPS list, which added three new Lactiplantibacillus species, are expected to streamline the approval process and reduce time-to-market for new product launches in Europe, further supporting innovation in this space [1]Source: European Food Safety Authority, "Qualified presumption of safety (QPS)," efsa.europa.eu.

Expansion of industrial biopharmaceutical fermentation capacity

The global biopharmaceutical fermentation capacity is expanding rapidly, driving significant growth in the microbial cultures market. With biologics, vaccines, antibody therapies, and recombinant proteins dominating pharmaceutical pipelines, large-scale microbial and mammalian fermentation has become a critical component of industrial bioprocessing. In 2024, contract development and manufacturing organizations (CDMOs) increased single-use bioreactor capacity at an unprecedented rate, adding over 500,000 liters of new stirred-tank bioreactor volume globally. A significant portion of this capacity is allocated to upstream production workflows. This expansion has directly increased the demand for microbial-derived inputs, including bacterial hydrolysates, yeast extracts, and peptones, which are essential nitrogen sources in cell-culture media. As biopharmaceutical manufacturers scale production from pilot to commercial levels, their need for consistent, high-purity microbial culture ingredients grows, driving market growth for culture media components and specialized fermentation-grade substrates.

Shift toward clean-label natural preservatives in food and beverage industry

Regulatory changes and shifting consumer preferences are driving the increased use of microbial culture as natural preservatives in the food and beverage industry. The European Commission’s 2024 revision of Regulation (EC) No. 1333/2008, which imposed stricter limits on sodium benzoate in ready-to-eat salads and restricted the use of nitrites and synthetic sorbates in meats and baked goods, has encouraged manufacturers to explore clean-label alternatives [2]Source: International Food Information Council, "2024 IFIC Food & Health SURVEY," ific.org. According to IFIC 2024, 11% of consumers now favor clean-label ingredients, which is boosting demand for bioprotective cultures that generate bacteriocins, organic acids, and antifungal metabolites directly within the product [3]Source: European Commission, "Additives," food.ec.europa.eu. The performance and effectiveness of these cultures are driving their adoption across Europe. For instance, Lactobacillus sakei and Pediococcus acidilactici are now commonly used in sliced deli meats in Scandinavia and Germany to control the growth of Listeria. Although bioprotective cultures add USD 0.02–0.05 per kg, a 15–25% premium compared to synthetic preservatives, their ability to align with regulatory requirements, retailer standards, and consumer preferences positions them as a significant growth factor for microbial culture in clean-label products globally.

Rapid adoption of precision fermentation for alternative proteins

The rapid expansion of precision fermentation for alternative proteins is a significant driver of growth in the global microbial culture market. Precision fermentation utilizes microbial hosts such as yeast, bacteria, and filamentous fungi to produce high-value protein ingredients, enzymes, and bioactive compounds with consistent quality and scalability. As plant-based and cell-cultured protein products gain popularity among consumers seeking sustainable, ethical, and functional alternatives to animal proteins, the demand for specialized microbial cultures, such as bacterial hydrolysates, yeast extracts, and growth-optimized strains, has increased. This trend has also driven innovation in microbial culture formulations, which are specifically designed for alternative protein applications. Companies now require cultures that enhance yield, improve functional properties, and support high-density fermentation, driving demand for performance-validated ingredients. Additionally, as precision fermentation achieves commercial scalability, microbial culture suppliers benefit from consistent demand for upstream media components and fermentation-grade nutrients. This positions precision fermentation as a long-term growth driver for the microbial culture market across the food, beverage, and nutraceutical industries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory approvals | -0.6% | Global, most acute in Europe and North America | Long term (≥ 4 years) |

| Volatility in raw material supply for culture media | -0.4% | Global, with acute pressure in Asia-Pacific and South America | Short term (≤ 2 years) |

| High risk of batch contamination and product recalls | -0.5% | Global, elevated in regions with fragmented cold chains | Medium term (2-4 years) |

| High cold-chain dependence drives up logistics complexity and costs | -0.3% | Asia-Pacific, Middle East and Africa, and Latin America most affected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory approvals

The divergence between food-safety and pharmaceutical-grade approval pathways creates a dual compliance challenge, particularly for smaller culture suppliers. While EFSA's QPS framework simplifies the process for established genera, it still requires whole-genome sequencing and antimicrobial-resistance profiling for novel strains. This process has recently taken 18 to 24 months and incurred costs ranging from EUR 300,000 to EUR 500,000 for submissions of Leuconostoc and Weissella. As a result, suppliers are strategically focusing on extending approved strains rather than developing entirely new species, which restricts the industry's capacity to address emerging applications such as fermented plant-based seafood or probiotic pet foods. Additionally, Japan's Ministry of Health, Labour and Welfare introduced new traceability requirements in 2024 for imported cultures. These regulations require country-of-origin documentation for every raw material in the growth medium, which extends lead times for non-Japanese suppliers by 8 to 12 weeks.

High cold-chain dependence drives up logistics complexity and costs

The viability of microbial culture declines rapidly above 8°C, yet temperature fluctuations during last-mile delivery remain prevalent in regions with unreliable refrigeration infrastructure. A 2024 study published in the Journal of Food Protection reported that 18% of probiotic yogurt samples in Southeast Asian markets had sub-therapeutic colony counts, attributed to cold-chain disruptions during retail distribution. This vulnerability increases logistics costs, as air-freight shipments with active temperature monitoring incur an additional USD 2 to USD 4 per kilogram compared to ambient cargo, representing a 40% to 60% premium that reduces margins for export-focused suppliers. As a result, there is a strategic shift toward lyophilized (freeze-dried) formats, which can withstand ambient storage but require rehydration protocols that food manufacturers are reluctant to adopt due to added process complexity. However, lyophilization increases production costs by USD 8 to USD 12 per kilogram, restricting its use to high-margin applications such as dietary supplements and pharmaceutical probiotics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bacterial Dominance Faces Yeast Acceleration

Bacterial cultures accounted for 62.35% of the microbial culture market in 2025, playing a key role in traditional dairy, vegetable, and meat fermentations. Lactic acid bacteria from the Lactobacillus, Lactococcus, and Streptococcus genera remain essential for cheese and yogurt production, with Novozymes’ FreshQ strains achieving significant market penetration in European dairies. Propionibacterium freudenreichii contributes to extended shelf life and vitamin B12 enrichment, while Leuconostoc and Pediococcus are utilized in localized applications such as sauerkraut and salami production. Yeast cultures, projected to grow at a 6.74% CAGR, are gaining traction due to clean-label trends in bakery products, flavor innovation in craft brewing, and their role in second-generation bioethanol co-products.

The market size for bacterial cultures is expected to grow steadily, however, yeast cultures are anticipated to capture a portion of the market share as non-dairy and bioethanol applications expand. Composite cultures, which integrate bacteria, yeast, and mold in a single inoculation, are gaining prominence in plant-based dairy alternatives. These multi-strain blends are instrumental in achieving traditional mouthfeel in such products. This trend is driving investments in strain libraries toward adaptable pipelines capable of serving both dairy and legume-based substrates while maintaining flavor consistency.

By Application: Pharmaceutical Surge Outpaces Food Maturity

Food and beverages accounted for 37.10% of the 2025 revenue and continue to dominate the microbial culture market. Within the food segment, dairy remains the leading category, although per-capita yogurt consumption is stabilizing in mature Western economies. Despite this dominance, dietary supplements and pharmaceuticals are projected to grow at a faster rate, with a CAGR of 7.29% through 2031. Growth in dietary supplements is primarily driven by the increasing demand for shelf-stable probiotic formats with guaranteed CFU counts, which cater to consumer preferences for convenience and efficacy.

Pharmaceutical live biotherapeutic products have become viable under the FDA’s 2024 guidance, marking a significant milestone for the industry. This regulatory development opens the door for insurance reimbursement, which could enhance profit margins while imposing stricter compliance requirements. Meanwhile, the "Others" category, encompassing animal feed and agriculture, is gaining momentum. The EU’s ban on prophylactic antibiotics has incentivized the adoption of Bacillus-based alternatives, which not only improve feed-conversion ratios but also align with the growing focus on sustainable and antibiotic-free farming practices.

Geography Analysis

Europe accounted for 31.65% of the microbial culture market in 2025, supported by stringent Protected Designation of Origin (PDO) rules that mandate the use of traditional cultures for heritage cheeses such as Parmigiano-Reggiano and Roquefort. Germany, France, and Italy collectively account for over 60% of European demand, driven by high cheese consumption and the increasing demand for clean-label requirements in processed meat products. Investments are also focused on probiotic feed additives, aligning with the EU Green Deal's goal of reducing antimicrobial use by 50% by 2030. Although Europe's mature market limits volume growth, incremental advancements are being observed in bioprotective meat cultures, plant-based dairy alternatives, and precision fermentation inputs.

The Asia-Pacific region is projected to grow at a compound annual growth rate (CAGR) of 5.74% through 2031, driven by factors such as China's expanding fermented-beverage market, India's cooperative upgrade program for yogurt quality, and Japan's nationwide promotion of fermented foods. In 2024, China approved 12 new domestic strains, thereby reducing its reliance on Western imports and localizing its supply chains. Meanwhile, India has launched a USD 50 million initiative to equip dairy cooperatives with culture-dosing equipment, addressing spoilage losses that currently exceed 15% of production.

North America remains a high-value market with a focus on innovation, supported by the FDA's live-biotherapeutic guidance, which paves the way for prescription probiotics. In Brazil, the poultry sector is scaling up the use of yeast-based probiotics to support antibiotic-free exports. In the Middle East, Saudi Arabia's Vision 2030 dairy investments are driving demand for microbial culture. Growth in these regions depends on suppliers capable of providing GMP-grade cultures and ambient-stable formats to address cold-chain limitations.

Competitive Landscape

The microbial culture market exhibits moderate concentration, with global leaders benefiting from scale advantages while leaving opportunities for niche players to innovate. Novonesis, formed through the 2024 merger of Chr. Hansen and Novozymes now operate across enzymes, cultures, and carbon-negative ethanol pathways, offering bundled solutions that reduce customers' reliance on vendors and expedite reformulation processes. Technology remains a critical differentiator. Lyophilized and microencapsulated formats enable suppliers like Lallemand and Kerry to access export markets previously hindered by weak cold chain infrastructure, despite production costs increasing by 60%–80% compared to frozen concentrates.

Patent filings highlight varying research and development priorities, for instance, Novonesis focuses on bacteriocin-producing strains for bioprotection, while IFF invests in multi-strain consortia tailored for plant-based dairy applications. Smaller competitors, such as Biena BioTech and Mediterranea Biotechnologie, gain market share by offering non-GMO, allergen-free cultures that meet EU organic standards. Advancements such as digital strain-screening tools, AI-driven fermentation, and GMP upgrades for pharmaceutical clients are expanding the capability gap between global leaders and regional players.

However, market opportunities persist in areas like precision-fermentation co-cultures for methanol or syngas feedstocks and live-biotherapeutic culture supply for prescription probiotics. Precision fermentation, in particular, holds potential for addressing sustainability goals by utilizing alternative feedstocks, while live-biotherapeutic cultures are gaining traction due to increasing demand for personalized medicine. Suppliers that address these niches with validated strain libraries, robust compliance infrastructure, and scalable production capabilities are well-positioned to achieve accelerated market share growth over the next five years.

Microbial Culture Industry Leaders

-

Novonesis A/S

-

International Flavors & Fragrances Inc.

-

dsm-firmenich

-

Lallemand Inc.

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: dsm‑firmenich launched a next-generation version of its Dairy Safe all-in-one culture solutions for semi-hard, hard, and continental cheeses. These cultures offer bioprotection against spoilage and phage contamination, ensure consistent acidification, control eye formation, and enhance flavor, enabling the production of high-quality, label-friendly cheese without artificial preservatives. Compatible with cow, goat, and sheep milk, and suitable for organic claims, these multifunctional cultures demonstrate the advancement of microbial solutions in supporting clean-label, preservative-free dairy products while maintaining safety and sensory quality.

- February 2025: Asahi Group Foods partnered with ADM Wild Valencia to distribute its proprietary Lactobacillus gasseri CP2305 strain internationally across North America, Europe, and Asia. Previously utilized exclusively in Asahi’s own products, this lactic acid bacterium will now be accessible to global manufacturers as a functional microbial ingredient, fostering growth in fermented foods, beverages, and other microbial-culture applications.

- February 2024: Lallemand Specialty Cultures has introduced two new dairy cultures, including Flav-Antage BLB1, designed for washed- and smeared-rind cheeses to enhance natural rind color and aroma, and Flav-Antage LN2, developed for blue cheeses to improve curd opening and ensure uniform mold growth. These performance-focused cultures support clean-label, consistent sensory properties, broadening the application of microbial cultures beyond traditional fermentation and driving growth in specialty dairy products worldwide.

Global Microbial Culture Market Report Scope

Global microbial culture market offers a wide range of products including starter cultures, adjunct and aroma cultures, and probiotics, applicable to bakery and confectionery, dairy, fruits and vegetables, beverages, and other end-user industries. The report further analyses the global scenario of the market in the regions of North America, Europe, Asia-Pacific, South America and, Middle East and Africa.

| Bacterial Cultures | Lactic Acid Bacteria |

| Propionic Bacteria | |

| Other Bacteria | |

| Yeast Cultures | |

| Mold/Fungal Cultures | |

| Mixed/Composite Cultures |

| Food and Beverages | Dairy and Dairy Products |

| Meat, Poultry, and Seafood | |

| Beverages | |

| Others | |

| Dietary Supplements and Pharmaceuticals | |

| Others (Animal Feed and Pet Nutrition, Agriculture) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Bacterial Cultures | Lactic Acid Bacteria |

| Propionic Bacteria | ||

| Other Bacteria | ||

| Yeast Cultures | ||

| Mold/Fungal Cultures | ||

| Mixed/Composite Cultures | ||

| By Application | Food and Beverages | Dairy and Dairy Products |

| Meat, Poultry, and Seafood | ||

| Beverages | ||

| Others | ||

| Dietary Supplements and Pharmaceuticals | ||

| Others (Animal Feed and Pet Nutrition, Agriculture) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the microbial culture market?

It stands at USD 2.32 billion in 2026, with a forecast to reach USD 2.86 billion by 2031.

Which application category is projected to grow fastest through 2031?

Dietary supplements and pharmaceuticals segment will expand at a 7.29% CAGR.

How large is Europe’s share in the starter cultures market?

Europe accounted for 31.65% of global revenue in 2025.

Which culture type is gaining the most momentum?

Yeast cultures will post the highest 6.74% CAGR driven by bakery and bioethanol demand.

Page last updated on: