Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

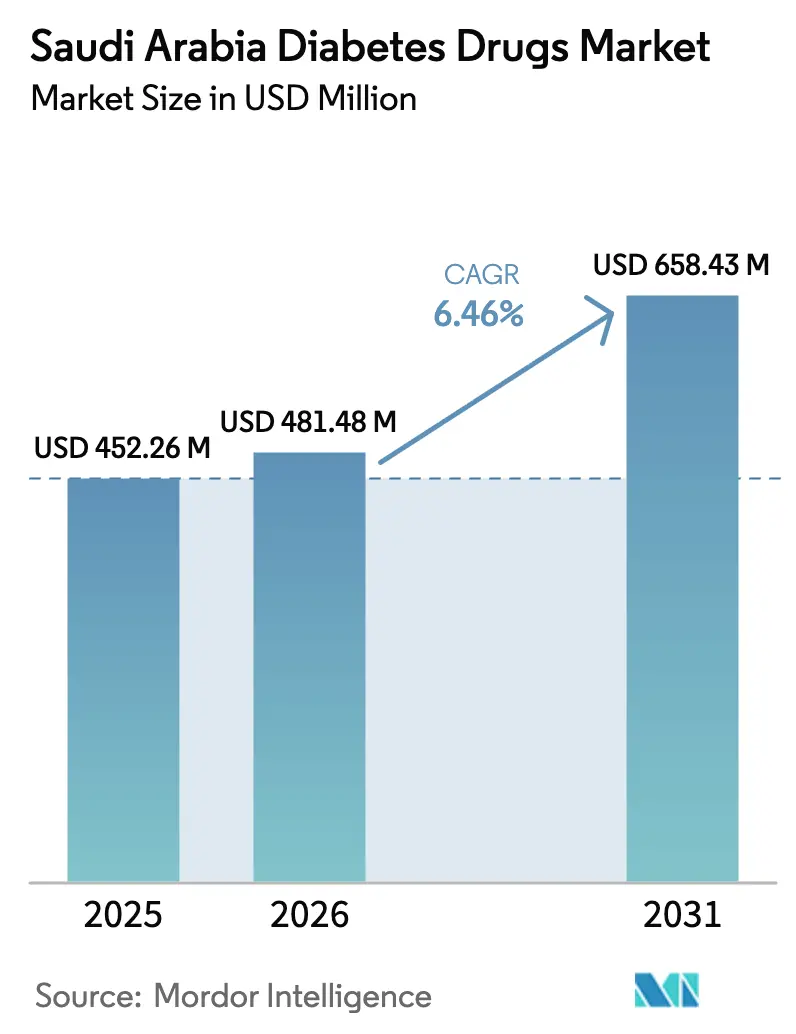

| Base Year Market Size (2025) | USD 452.26 Million |

| Market Size (2026) | USD 481.48 Million |

| Market Size (2031) | USD 658.43 Million |

| Growth Rate (2026 - 2031) | 6.46% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Diabetes Drugs Market Analysis by Mordor Intelligence

The Saudi Arabia diabetes drugs market size is expected to grow from USD 452.26 million in 2025 to USD 481.48 million in 2026 and is forecast to reach USD 658.43 million by 2031 at 6.46% CAGR over 2026-2031. Demand is climbing as prevalence has risen to 16.4% of the population, a trend linked to urbanization-related inactivity and dietary changes. Growth is further supported by the National Transformation Program, which allocated SAR 214 billion (USD 57.04 billion) to health and social development in 2024, thereby accelerating the development of chronic-disease infrastructure.[1]Global Health Saudi, “How Saudi’s Vision 2030 Is Going to Transform the Healthcare Industry,” globalhealthsaudi.com Regulatory streamlining by the SFDA is accelerating the approval of complex generics, catalyzing the entry of biosimilars.[2]Saudi Food and Drug Authority, “Regulatory Framework for Drug Approvals,” sfda.gov.sa Distribution is also shifting as hospital-based dispensing continues to dominate, but online pharmacies gain ground at a high CAGR, propelled by e-prescription rules and tele-pharmacy integration.

Key Report Takeaways

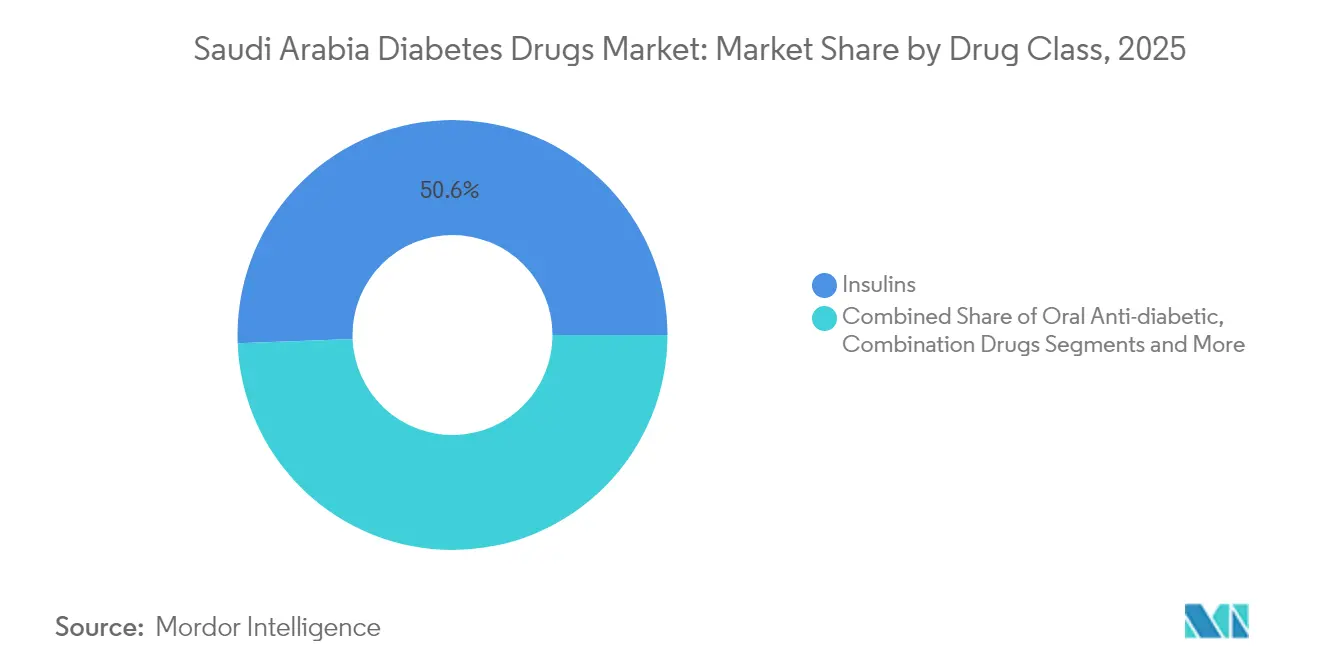

- By drug class, insulins led with 50.62% of Saudi Arabia diabetes drugs market share in 2025; non-insulin injectables are projected to post the highest CAGR at 9.03% to 2031.

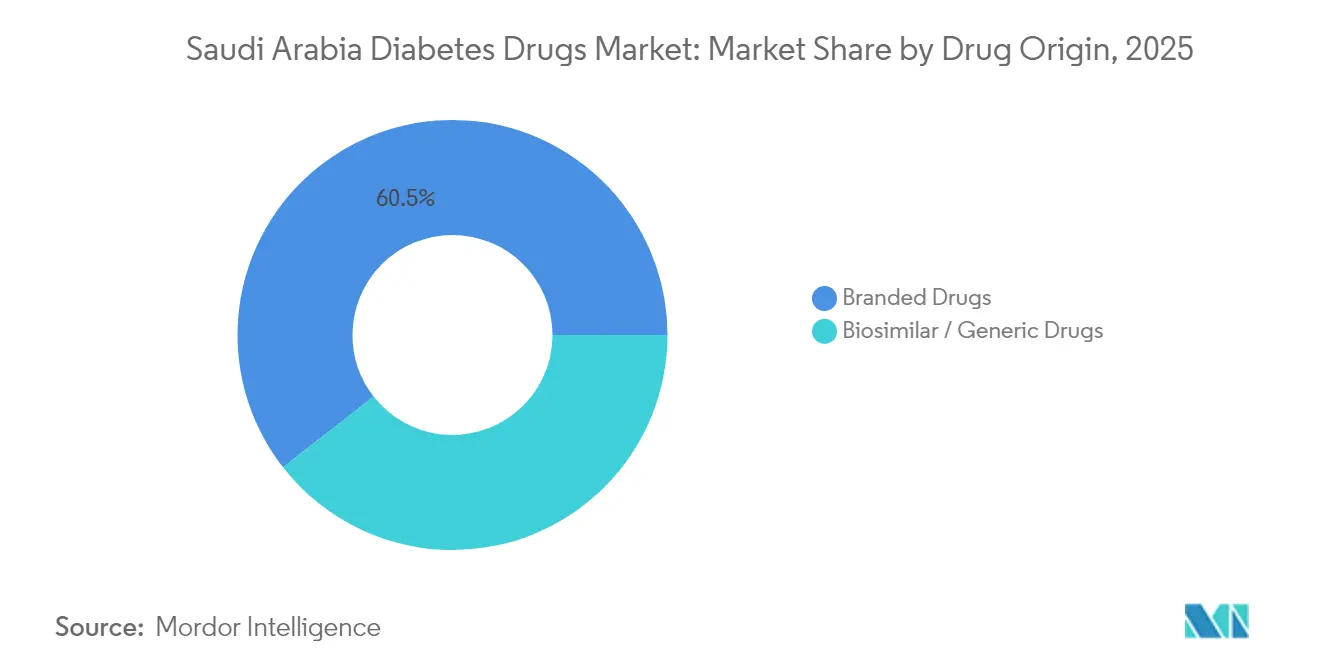

- By origin, branded products commanded 60.55% share of Saudi Arabia diabetes drugs market size in 2025, while biosimilars and generics are expected to climb at 7.78% CAGR through 2031.

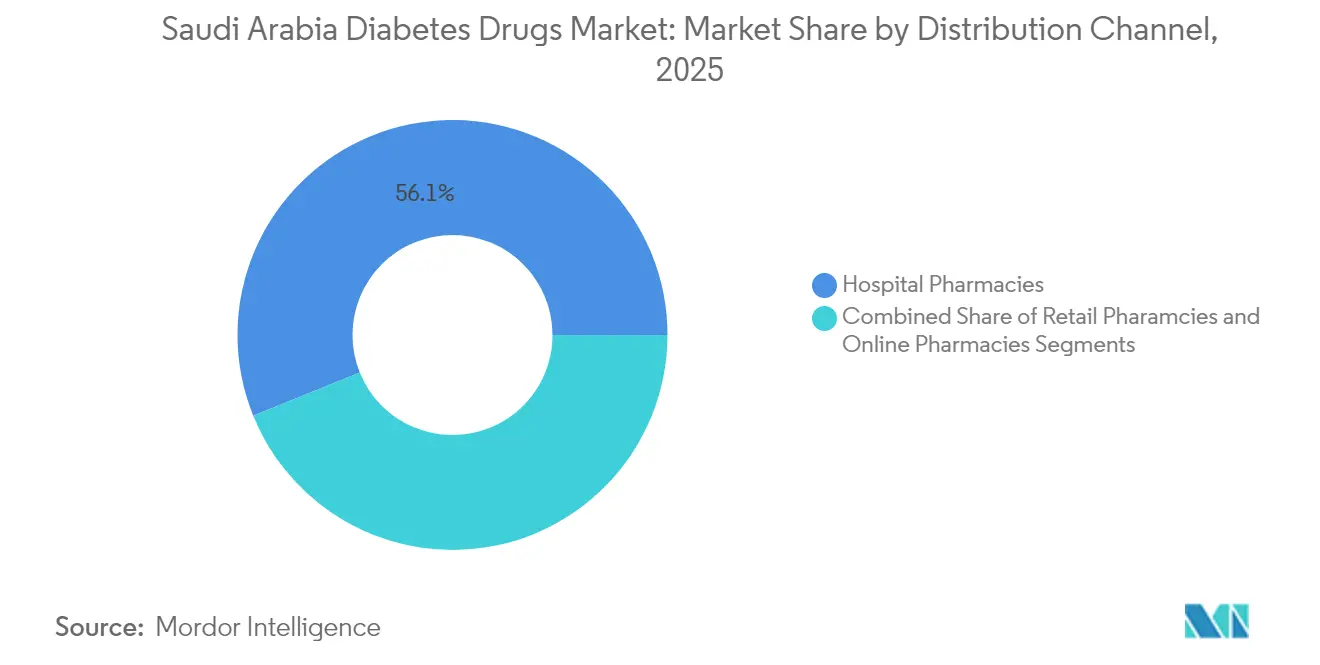

- By distribution channel, hospital pharmacies accounted for 56.12% of Saudi Arabia diabetes drugs market share in 2025; online pharmacies are forecast to expand at 10.01% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Diabetes Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of obesity & sedentary lifestyles | +1.5% | National, higher in urban centers | Long term (≥ 4 years) |

| Rising reimbursement for innovative antidiabetics | +0.8% | National, early adoption in major cities | Medium term (2-4 years) |

| National Transformation Program focus on chronic diseases | +0.6% | Nationwide with regional variation | Long term (≥ 4 years) |

| Expansion of private-sector specialty diabetes centers | +0.4% | Riyadh, Jeddah, Dammam metros | Medium term (2-4 years) |

| Surge in demand for long-acting and innovative drugs | +0.3% | National, premium segments | Short term (≤ 2 years) |

| AI-driven patient-support apps linked to prescription renewals | +0.2% | Urban areas with high smartphone use | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing prevalence of obesity & sedentary lifestyles

Obesity stabilized at 21.4% in 2023, yet 18.8% of obese Saudis already live with diabetes. Among people under 30, 14% now have the disease. Sugary beverages and fast food remain dietary staples, especially in cities, while adherence to the Ministry of Health guideline of 150 minutes of weekly exercise is weak. Demand therefore leans toward agents that address glycemic control and weight, positioning GLP-1 products as first-line injectable choices. The government spends USD 26 billion yearly on diabetes care, making prevention a parallel priority.

Rising reimbursement for innovative antidiabetics

The Council of Health Insurance’s Saudi Billing System has standardized codes and improved transparency, smoothing the path for premium therapies. Private-insurance uptake should widen by 2030, expanding access for urban professionals. Managed-entry agreements balance cost and value, allowing companies to collect real-world evidence while patients gain earlier access. Oral semaglutide cut HbA1c by 3.1% at 6 months in local studies, proof that outcomes-based payments can work. Pharmaceutical firms now invest more heavily in post-market surveillance, encouraged by these reimbursement shifts.

National Transformation Program focus on chronic diseases

NTP-driven primary-care reform pushed visits up 37.5% and improved satisfaction 4.7% since 2016. Systematic screenings uncover undiagnosed cases earlier, prompting timely drug initiation. Digital tools such as the Sehhaty app have delivered more than 1.6 million virtual consultations, streamlining prescription refills. The workforce plan to hire 175,000 health professionals by 2030 should relieve bottlenecks, while 100 public-private partnerships will inject USD 12.8 billion into new capacity.

Expansion of private-sector specialty diabetes centers

Vision 2030 aims to boost the private share of care to 65%. Almoosa Health’s IPO and 730-bed pipeline illustrate investor appetite. Centers employ multidisciplinary teams; King Saud University Medical City’s unit couples endocrinology and lifestyle coaching. Studies tie patient-centered care to higher satisfaction, especially in physical comfort and continuity. Angel and sovereign investors now target diagnostic and telehealth start-ups, further enhancing specialty-care capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of GLP-1s & novel dual agonists | -0.9% | National, stronger in price-sensitive segments | Medium term (2-4 years) |

| Stringent SFDA pharmacovigilance delaying biosimilar launches | -0.7% | National regulatory impact | Short term (≤ 2 years) |

| Physician inertia toward therapy intensification | -0.5% | Higher in smaller cities | Long term (≥ 4 years) |

| Growing preference for medical tourism to nearby Gulf states | -0.4% | Affluent patients in major cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost of GLP-1s & novel dual agonists

Premium pricing limits access even though GLP-1s lower complications over time. A global shortage has heightened prices; biosimilar competition is sparse because manufacturing is complex. Tirzepatide hits HbA1c goals for nearly two-thirds of local users, yet the out-of-pocket burden still deters uptake. Generic liraglutide by Hikma could narrow the gap, but material price relief remains gradual. Insurers test managed-entry models to widen coverage but progress varies across schemes.

Stringent SFDA pharmacovigilance delaying biosimilar launches

The SFDA demands extensive post-market safety data, which can extend launch timelines by up to 12 months. Authorities focus on pancreatitis risks seen in global GLP-1 reports, justifying the cautious stance.[3]N. Alfageh et al., “Overview of Online Pharmacy Regulations in Saudi Arabia and the GCC,” Frontiers in Pharmacology, frontiersin.orgBiosimilars rarely qualify for the breakthrough pathway, so queues form behind innovative filings. The industry seeks aligned standards with the EMA and FDA to reduce delays while maintaining safety rigor.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Insulins Maintain Dominance Amid Injectable Innovation

Insulins captured 50.62% of Saudi Arabia diabetes drugs market share in 2025. Stable treatment algorithms, broad physician familiarity and reimbursement support keep demand strong. Saudi Arabia diabetes drugs market size for insulins is projected to climb steadily though at a slower pace than innovative injectables. Once-weekly insulin icodec promises higher adherence, and localization efforts by NUPCO, Novo Nordisk and Sanofi strengthen supply security.

Non-insulin injectables are forecast to post a 9.03% CAGR to 2031, the quickest among all classes. Local evidence shows oral semaglutide trimming HbA1c by 3.1% at 6 months and tirzepatide enabling 64.1% of patients to reach targets within 40 weeks. Combined with notable weight reductions, these outcomes drive rapid uptake in insured urban cohorts. Biosimilar makers are preparing GLP-1 filings to ride the wave once regulatory clarity improves.

By Drug Origin: Branded Dominance Faces Biosimilar Pressure

Branded products accounted for 60.55% of Saudi Arabia diabetes drugs market size in 2025. R&D pipelines, physician trust and aggressive detailing underpin their edge. AstraZeneca alone aims for USD 80 billion global revenue by 2030, partly on new metabolic indications. Localization deals—Boehringer Ingelheim-Alpha Pharma, MSD-Jamjoom, Abdi Cigalah—align with Vision 2030’s sovereignty goals and may temper future price escalation.

Biosimilars and generics are expanding at a 7.78% CAGR, encouraged by SFDA guidance and payer cost pressure. Manufacturers benefit from tax incentives and new biotech clusters. Still, stringent surveillance and manufacturing complexity create barriers, so near-term penetration focuses on basal insulins and first-wave GLP-1s. Price competition is expected to intensify after 2027 as capacity scales.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Hospital pharmacies held 56.12% of Saudi Arabia diabetes drugs market share in 2025. Close integration with specialists, immediate lab access and dosing oversight make them indispensable for complex regimens. Tele-pharmacy pilots now link hospital pharmacists with remote clinics, expanding reach without eroding institutional dominance.

Online pharmacies are rising at 10.01% CAGR as digital-health adoption explodes. Penetration jumped from 3% in 2017 to 60% in 2023, thanks to clear e-prescription rules. Saudi Arabia diabetes drugs market size flowing through online channels will likely surpass retail volumes before 2030. Apps integrate with EHRs, and AI chatbots offer refill reminders, enhancing adherence. Controlled substances remain restricted, but chronic-care prescriptions see brisk demand.

Geography Analysis

Saudi Arabia diabetes drugs market demand concentrates in Riyadh, Jeddah and Dammam, where high incomes, insurance coverage and specialist centers drive premium drug uptake. Rural regions rely more on older oral agents and basal insulins. The Seha Virtual Hospital now links 224 facilities, providing remote endocrinology consults and e-prescriptions, which narrow access gaps for peripheral provinces.

Population aging heightens regional needs. More than 52% of citizens aged 60+ carry at least two chronic conditions, often including diabetes. Aseer studies predict 21.9% of residents will develop Type 2 diabetes within five years, emphasizing urgent preventive campaigns.

Vision 2030 earmarks USD 65 billion for new hospitals and PPPs. Over 100 projects worth USD 12.8 billion between 2022-2027 aim to add beds and ambulatory sites. Medical-tourism leakage to Gulf neighbors spurs investments in flagship hubs like King Abdullah Medical City. Regional competition should improve care quality while retaining domestic spending.

Competitive Landscape

The Saudi Arabia diabetes drugs market shows moderate concentration. Novo Nordisk and Sanofi lead in insulins and GLP-1s, reinforced by localization pacts with NUPCO. AstraZeneca’s cardiometabolic pipeline and weight-management ambitions add competitive tension.

Biosimilar entrants—Hikma, Alpha Pharma, Jamjoom—align with national biotech strategy to cut import reliance. Their success hinges on meeting SFDA’s surveillance requirements and scaling biomanufacturing.

Digital-health innovators amplify competition beyond molecules. AmplifAI Health’s AI-led foot-ulcer prevention tool, selected for Google’s Health-Growth Academy, illustrates convergence between software and pharmacotherapy. Companies able to bundle drugs with data-driven adherence or risk-sharing models may gain future share.

Saudi Arabia Diabetes Drugs Industry Leaders

AstraZeneca

Merck and Co.

Novo Nordisk A/S

Sanofi

Eli Lilly and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Saudi Arabia inaugurated its first local insulin manufacturing facility, marking a Vision 2030 milestone in pharmaceutical self-sufficiency.

- October 2024: During the Global Health Exhibition, NUPCO, Sudair Pharmaceutical, Sanofi and Novo Nordisk finalized an agreement to localize production of selected insulin products.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Saudi Arabia diabetes drugs market as the cumulative ex-factory sales value of all prescription pharmacologic agents, including insulins, oral anti-diabetics, non-insulin injectables, and fixed-dose combinations, approved by the Saudi Food and Drug Authority for glycemic control in type 1 and type 2 patients and distributed through hospital, retail, or online channels during the calendar year.

Scope exclusion: Over-the-counter supplements, diagnostic devices, and any veterinary formulations fall outside this assessment.

Segmentation Overview

- By Drug Class

- Insulins

- Oral Anti-diabetic Drugs

- Non-Insulin Injectable Drugs

- Combination Drugs

- By Drug Origin

- Branded Drugs

- Biosimilar / Generic Drugs

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed endocrinologists in Riyadh and Jeddah, hospital pharmacy buyers, regional wholesaler managers, and SFDA reviewers. Conversations clarified real-world insulin utilization, expected biosimilar penetration, average selling price shifts, and likely adoption timelines for SGLT-2s and GLP-1s, enabling us to adjust desk-based assumptions and close data gaps.

Desk Research

We began by mapping the treatment landscape with publicly available sources such as the Ministry of Health Annual Statistical Yearbook, the IDF Diabetes Atlas, GASTAT household health surveys, SFDA medicines price lists, and UN Comtrade import lines for insulin preparations. Company 10-Ks, investor decks, and leading Saudi press archives on Factiva enriched brand-level pricing and pipeline context. Additional directional checks were obtained from D&B Hoovers financial snapshots for local distributors.

These materials clarified patient pools, reimbursement rules, and historical procurement volumes, forming the initial demand benchmark. The sources cited above are illustrative; many other public records and specialized datasets supported data gathering, cross-checks, and context validation.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort build paired with selective bottom-up channel checks underpins the model. Adult diabetes prevalence, diagnosis rates, insured population coverage, average daily defined dose, branded-to-generic mix, and NUPCO tender pricing are the core variables. These inputs flow into a multivariate regression that forecasts unit demand, which is then validated against sampled ASP multiplied by volume roll-ups from leading suppliers. Where bottom-up data are partial, ratio imputation anchored to confirmed hospital share bridges gaps before final calibration.

Data Validation & Update Cycle

Outputs pass a three-step review: internal peer audit, variance scanning against external metrics, and anomaly callbacks with selected interviewees. Mordor refreshes the dataset annually, triggering interim revisions when material regulatory or tender changes surface, and every report receives a last-minute sense check before client release.

Why Mordor's Saudi Arabia Diabetes Drugs Baseline Stands Firm

Published estimates often diverge because firms vary in scope, price definitions, and update cadence.

Key gap drivers include whether devices are co-counted, if retail mark-ups or ex-factory prices anchor values, the aggressiveness of biosimilar uptake assumptions, and currency conversion dates. Mordor reports the 2025 ex-factory value for drugs only, applies quarterly SAR-USD averages, and refreshes every twelve months, whereas many peers extrapolate regional totals or bundle delivery devices.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 452.3 M (2025) | Mordor Intelligence | - |

| USD 829.6 M (2024) | Global Consultancy A | Includes wholesale and retail mark-ups; insulin pumps partially bundled |

| USD 1.87 B (2024) | Industry Research Firm B | Uses regional top-down allocation; assumes faster GLP-1 uptake; limited primary validation |

| USD 2.0 B (2024) | Regional Advisory C | Combines drugs and devices; employs list prices without tender discounts |

In sum, the disciplined scoping, variable selection, and yearly refresh practiced by Mordor Intelligence give decision-makers a balanced, transparent baseline that is traceable to real-world volumes and reproducible steps, minimizing the risk of over- or under-estimation faced elsewhere.

Key Questions Answered in the Report

What is the current value of the Saudi Arabia diabetes drugs market?

The market is valued at USD 481.48 million in 2026 and is set to reach USD 658.43 million by 2031.

Which drug class holds the largest share?

Insulins lead, representing 50.62% of Saudi Arabia diabetes drugs market share in 2025.

How fast are non-insulin injectables growing?

Non-insulin injectables, driven by GLP-1 and dual agonists, are forecast to grow at a 9.03% CAGR through 2031.

Why are online pharmacies expanding so rapidly?

Regulations now allow e-prescriptions, while integrated apps simplify refills, delivering a 10.01% CAGR for online channels.

What factors restrain market growth?

High prices of innovative injectables, stringent SFDA biosimilar reviews, physician inertia, and outbound medical tourism temper expansion.

How is Saudi Arabia encouraging local drug production?

Vision 2030 fosters localization via tax incentives, NUPCO supply deals and biotech clusters, recently culminating in the Kingdom’s first domestic insulin plant.

Page last updated on: