Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

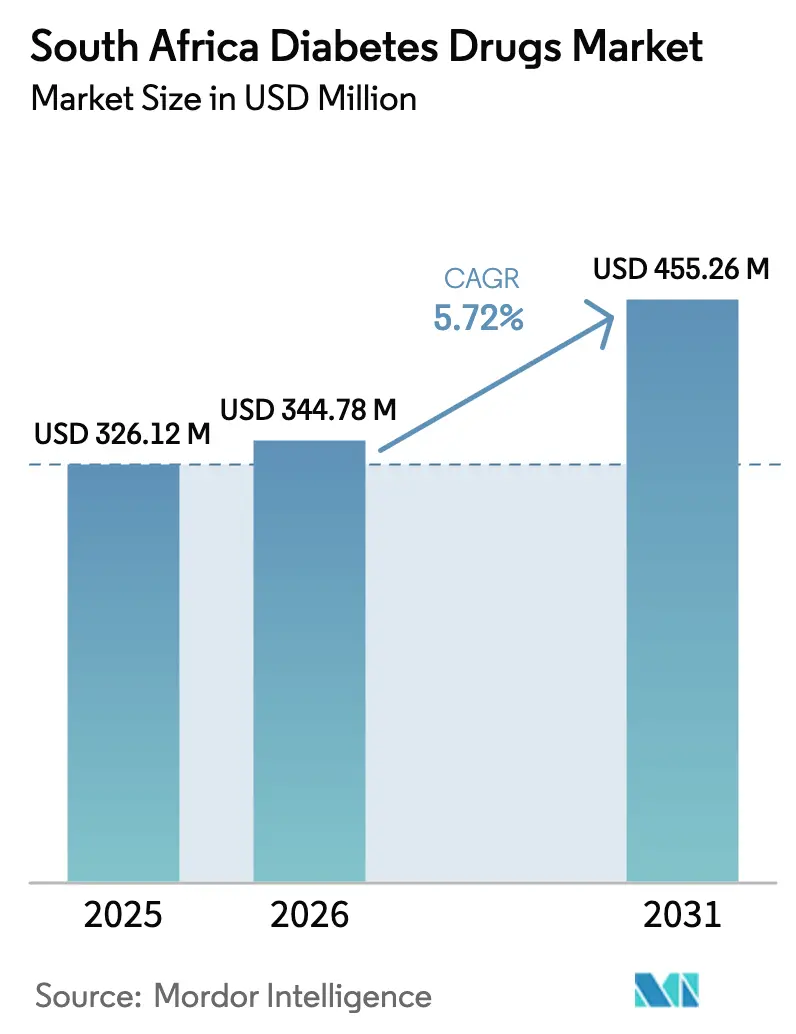

| Base Year Market Size (2025) | USD 326.12 Million |

| Market Size (2026) | USD 344.78 Million |

| Market Size (2031) | USD 455.26 Million |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Diabetes Drugs Market Analysis by Mordor Intelligence

The South Africa diabetes drugs market size is expected to grow from USD 326.12 million in 2025 to USD 344.78 million in 2026 and is forecast to reach USD 455.26 million by 2031 at 5.72% CAGR over 2026-2031. Escalating diabetes prevalence—now affecting more than 4 million residents—intersects with rising private medical-aid coverage and local manufacturing investments, creating a robust demand outlook. Uptake of SGLT-2 inhibitors and GLP-1 receptor agonists broadens therapeutic choices, while value-based reimbursement models nudge prescribers toward agents that demonstrate measurable cardiometabolic benefits. A moderate but steady shift of prescription volumes from public facilities to private sector channels mirrors stronger purchasing power in urban provinces, reinforcing differentiated access patterns. Concurrently, online pharmacies extend reach into semi-urban communities, signifying that the South Africa diabetes drugs market is pivoting toward digitally enabled distribution.

Key Report Takeaways

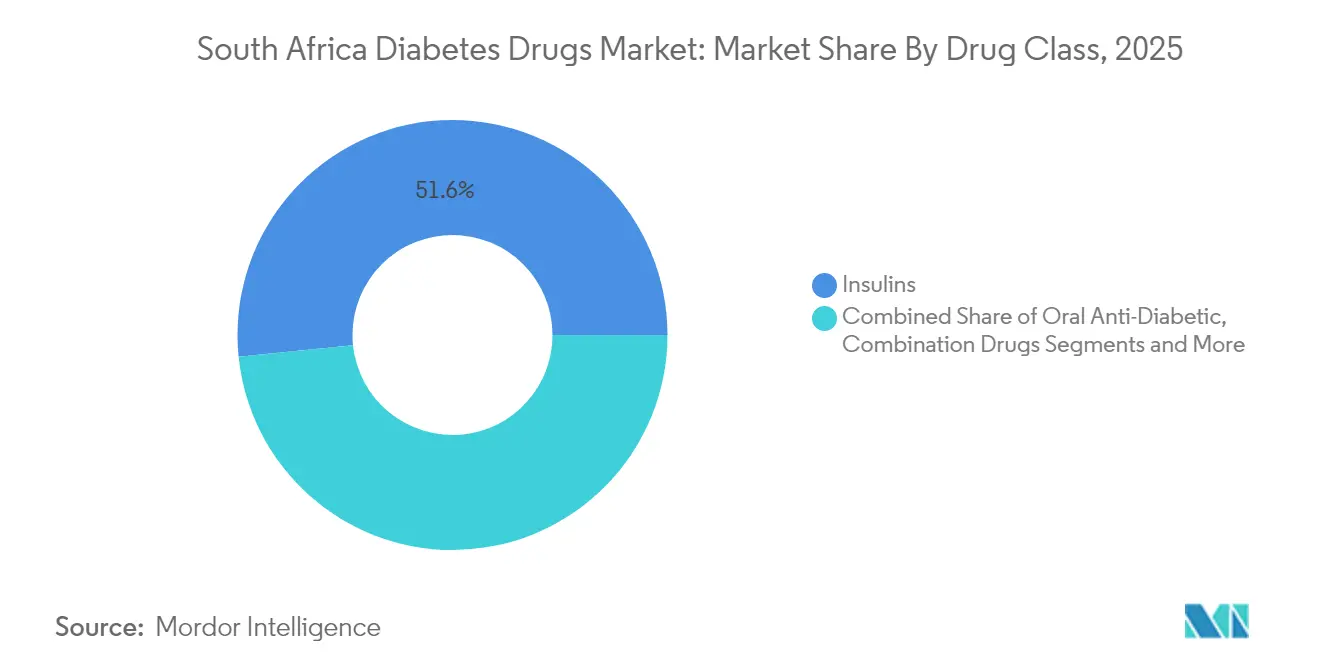

- By drug class, insulins led with 51.62% of the South Africa diabetes drugs market share in 2025; non-insulin injectables post the fastest CAGR at 9.88% through 2031.

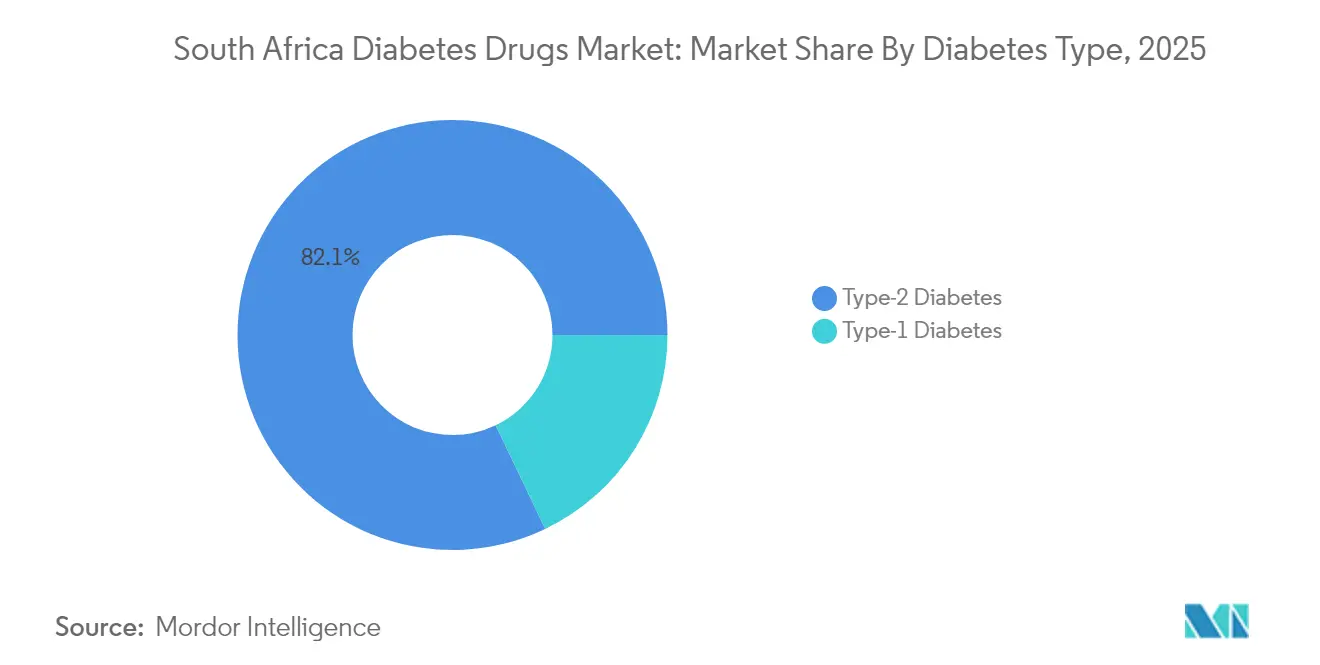

- By diabetes type, Type 2 diabetes accounted for 82.10% share of the South Africa diabetes drugs market size in 2025 and is advancing at a 6.83% CAGR to 2031.

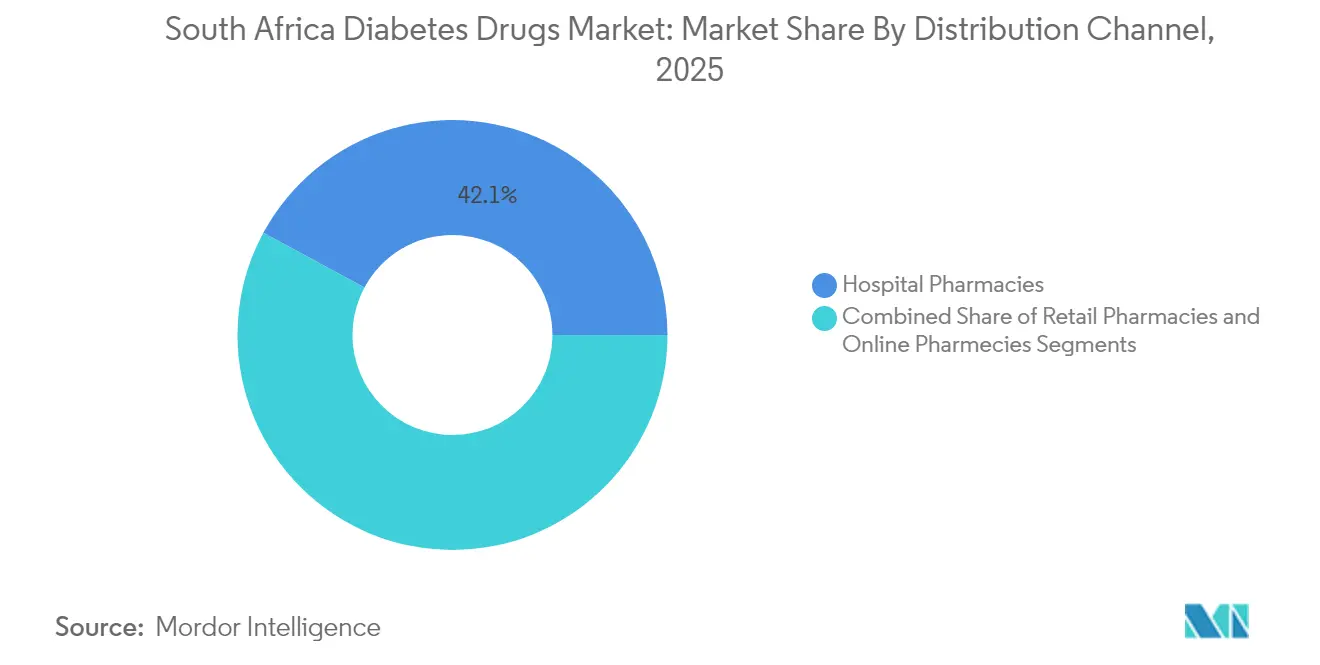

- By distribution channel, hospital pharmacies held 42.12% revenue share in 2025, whereas online pharmacies are projected to expand at a 9.35% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Diabetes Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating diabetes prevalence & earlier age of onset | +1.2% | National, concentrated in urban areas | Medium term (2-4 years) |

| Expansion of private medical-aid coverage for chronic medicines | +0.9% | National, higher impact in Gauteng, Western Cape | Short term (≤ 2 years) |

| Rapid uptake of SGLT-2 and GLP-1 classes in local guidelines | +0.8% | National, early adoption in private sector | Medium term (2-4 years) |

| Local contract-manufacturing & fill-finish capacity build-out | +0.6% | National, manufacturing hubs in Gauteng, KwaZulu-Natal | Long term (≥ 4 years) |

| Surge in tele-pharmacy platforms enabling e-prescriptions | +0.5% | National, accelerated in metropolitan areas | Short term (≤ 2 years) |

| Government initiatives and reimbursement | +0.4% | National, focus on public sector facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Diabetes Prevalence & Earlier Age of Onset

South Africa is experiencing a younger age of diabetes onset, shifting the therapy horizon from episodic to lifelong treatment. Mitochondrial dysfunction studies highlight genetic and lifestyle interplay unique to the region. Longer treatment journeys multiply cumulative drug volumes, enlarging the South Africa diabetes drugs market considerably. Urban dietary transitions toward energy-dense foods worsen glycaemic profiles, while declining physical activity amplifies insulin resistance. Clinicians now initiate pharmacotherapy earlier, including dual therapy at diagnosis, to curb long-term complications. Insurer analytics show that patients diagnosed before age 40 incur medication costs nearly two-and-a-half times higher than those diagnosed after 55. This demographic migration keeps demand resilient even if incidence stabilizes.

Expansion of Private Medical-Aid Coverage for Chronic Medicines

Discovery Health and other large schemes now list most guideline-recommended agents under chronic benefits, dramatically lowering member cost-sharing. Full benefit coverage for basal-bolus insulin regimens and partial cover for next-generation GLP-1 agonists reduce financial friction, encouraging rapid switching to premium therapies. Private schemes also pilot value-based formularies that reimburse at higher tiers when HbA1c targets are met, aligning stakeholder incentives. The net result is deeper penetration of newer drug classes in metropolitan areas, strengthening revenue density per treated patient. Spill-over effects occur as public guidelines observe private-sector outcome data and consider broader adoption. Consequently, the South Africa diabetes drugs market gains an accelerated path for innovative molecules.

Rapid Uptake of SGLT-2 and GLP-1 Classes in Local Guidelines

Local endocrinology societies have added SGLT-2 inhibitors as second-line therapy for patients with cardiovascular risk, and GLP-1 agonists for those needing weight reduction. A Western Cape cohort study confirmed that quarterly HbA1c testing coupled with these agents cut hospitalization days by 18% within twelve months.[1]Lize-Marie Doresha Williams & Robert Mash, “The Role of Community Health Workers in Non-Communicable Diseases,” BMC Primary Care, bmcprimcare.biomedcentral.com Although high prices restrict public-sector diffusion, private sector uptake proves the clinical pay-off. That evidence edges policymakers toward eventual tender inclusion, particularly once biosimilar versions gain SAHPRA approval. Prescribing momentum, once formed, rarely reverses, solidifying long-run volume growth.

Local Contract-Manufacturing & Fill-Finish Capacity Build-Out

Novo Nordisk’s alliance with Aspen Pharmacare to fill-finish human insulin vials at a ceiling ex-factory price of USD 3 channels substantial volumes through domestic plants. Similar lines are earmarked for cartridge and pen assembly, insulating supply from import-route shocks. Local production trims foreign-exchange exposure and shortens lead times, attributes that resonate after pandemic-era disruptions. Government incentive packages—tax holidays and equipment grants—further sweeten on-shoring economics. Over time, scale economies could spill into contract production of GLP-1 injectables, anchoring the South Africa diabetes drugs market as a regional export base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High out-of-pocket cost of novel therapies | -0.8% | National, higher impact in rural areas | Short term (≤ 2 years) |

| Frequent insulin & test-strip stock-outs in public sector depots | -0.6% | National, concentrated in rural provinces | Medium term (2-4 years) |

| Regulatory backlog for biosimilar approvals (SAHPRA) | -0.4% | National, affects all market segments | Medium term (2-4 years) |

| Patient adherence issues linked to traditional-medicine preferences | -0.3% | National, higher in rural and traditional communities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Cost of Novel Therapies

The best-in-class GLP-1 agonist regimen costs up to 14% of an average household’s post-tax income when purchased without full medical-aid subsidy. Such expense forces therapeutic rationing, sustaining a two-tier system. Patients in the lower-middle segment often cycle between public clinics for baseline care and private pharmacies for episodic refills, disrupting continuity. Clinicians report delaying therapy intensification by eight to ten months on affordability grounds, undermining glycaemic control. Manufacturers respond with limited co-pay vouchers, yet their scope remains urban-centric. Until broader subsidy or price re-negotiation occurs, uptake trajectories will remain flatter than clinical need suggests.

Frequent Insulin & Test-Strip Stock-Outs in Public Sector Depots

MSF documented a national stock-out of insulin pens in 2024, affecting thousands of users and triggering emergency transitions to vials.[2]“Insulin Pen Shortage Impacts Thousands in South Africa,” MSF Southern Africa, msf.org.zaSupply gaps stem from tender mis-forecasting, port congestion and funding lags. Rural provinces shoulder the brunt because replenishment logistics are slower. Each shortage episode drives temporary spikes in private pharmacy demand but entrenches distrust in public supply reliability. Chronic uncertainty prompts some patients to hoard inventories, aggravating cyclical shortages. For the South Africa diabetes drugs market, such volatility dampens long-range demand visibility and can blunt therapy innovation momentum in the public channel.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Insulin Dominance Faces Injectable Innovation

Insulins generated 51.62% of the South Africa diabetes drugs market revenue in 2025, thanks to indispensable usage in Type 1 diabetes and late-stage Type 2 cases. Basal-bolus regimens remain the cornerstone because they align with current national guidelines and are staples of provincial tenders. However, supply disruptions spotlight vulnerabilities that biosimilar entrants aim to exploit. Non-insulin injectables, chiefly GLP-1 receptor agonists, compound market dynamism with a 9.88% CAGR to 2031, reshaping therapeutic hierarchies despite price premiums. These molecules deliver dual glycaemic and weight-management outcomes, attributes that resonate with prescribers treating obese urban patients. Oral antidiabetic drugs—metformin, sulfonylureas and DPP-4 inhibitors—continue as first-line agents, serving as volume stabilizers when injectables face affordability pushback.

Pipeline innovations extend the insulin franchise into ultra-long-acting formats such as once-weekly insulin icodec. Early trial visibility has heightened clinician anticipation, even before formal South African registration, because reduced injection frequency addresses adherence drop-off. With fill-finish capacity now domestic, stakeholders expect pricing headroom for premium formulations. Nonetheless, competitive intensity will hinge on SAHPRA’s processing speed for biosimilar dossiers; every new approval promises to temper pricing discipline across the South Africa diabetes drugs market.

By Diabetes Type: Type 2 Complexity Drives Treatment Evolution

Type 2 diabetes accounted for 82.10% of diagnosed cases and steers therapeutic volume growth at a 6.83% CAGR, anchoring the South Africa diabetes drugs market size expansion through 2031. Lifestyle transition toward sedentary occupations and calorie-dense diets accelerates the metabolic shift, extending drug exposure windows. Complication-centric prescribing—focusing on cardiovascular and renal endpoints—encourages earlier integration of SGLT-2 and GLP-1 agents. In contrast, Type 1 diabetes remains a steady but smaller segment, monopolizing basal and rapid-acting insulin demand without significant class diversification.

Researchers link uncontrolled Type 2 diabetes to elevated ketogenesis metabolites, underscoring dietary non-compliance in many cases. Community Health Workers now lead education drives that explain carbohydrate counting and drug titration, helping curtail avoidable hospital admissions. These grassroots efforts, when coupled with digital glucose-monitoring apps, aim to push the proportion of patients meeting HbA1c targets beyond the current 23%. Improved outcomes would naturally escalate chronic medication lifespans, reinforcing volume stability for the South Africa diabetes drugs market.

By Distribution Channel: Digital Transformation Reshapes Access

Hospital pharmacies held 42.12% of overall revenue in 2025, reflecting their role in complex case management and integrated laboratory services. They remain critical for insulin initiation, titration and severe hypoglycaemia intervention. Retail community pharmacies cater to routine refills and acute counseling, benefiting from dense geographic coverage. Online platforms, while representing a single-digit share today, post a 9.35% CAGR as tele-consult workflows mature. A study found that 88% of e-pharmacies surveyed carry legitimate pharmacy licenses, although regulatory identifiers are displayed inconsistently.

Medical-aid electronic pre-authorization portals now push approved prescriptions directly to partnered online pharmacies, trimming delays. Automated refill scheduling and home delivery convenience drive higher adherence in tech-savvy patient segments. In rural settings, hybrid models emerge: virtual consultations link district hospitals to township collection points, preserving cold-chain integrity for insulin. Such channel blending ensures that the South Africa diabetes drugs market maintains synchronized volume streams across physical and digital storefronts.

Geography Analysis

Urban provinces, notably Gauteng and Western Cape, generate more than half of national diabetes prescription revenue, mirroring concentrated private insurance penetration. These areas also host leading tertiary hospitals that pioneer GLP-1 protocol adoption, thereby serving as early-adopter clusters for innovative therapies. KwaZulu-Natal follows, leveraging Durban’s port infrastructure for pharmaceutical import flows and recent investments in fill-finish plants. By contrast, Eastern Cape and Limpopo face sparse endocrinology coverage and periodic medicine stock-outs, dampening overall uptake.

National Health Insurance rollout seeks to homogenize access, but phased implementation means regional disparities will linger through most of this decade. Community Health Workers play bridging roles by coordinating medicine pick-ups and reinforcing adherence in remote villages. Tele-pharmacy pilots in Mpumalanga demonstrate how smartphone penetration can counter logistic bottlenecks when signal coverage is adequate. Over time, localized manufacturing hubs in Gauteng and KwaZulu-Natal will reduce lead-times to rural clinics, potentially narrowing geographic treatment gaps.

Cross-border opportunity also shapes strategic planning. South African producers eye Southern African Development Community markets, where compatible regulatory frameworks expedite export licensing. Bulk contracts with Botswana and Namibia health ministries already reflect such expansion moves. Consequently, provincial production capacity may overshoot domestic needs, but surplus can flow regionally, reinforcing South Africa’s pharma hub aspirations and stabilizing factory utilization rates within the South Africa diabetes drugs market.

Competitive Landscape

Multinational incumbents—Novo Nordisk, Sanofi and Eli Lilly—retain market leadership through well-established insulin and GLP-1 portfolios. Their combined volume share in insulin eclipses 60%, marking a moderate concentration level. Each firm embeds clinician-education programs and patient-support hotlines to reinforce brand loyalty. Recent shortages, however, exposed vulnerabilities that biosimilar manufacturers intend to exploit once SAHPRA clears regulatory backlogs.

Strategic alliances typify the current playbook: Novo Nordisk’s fill-finish deal with Aspen Pharmacare, Sanofi’s packaging collaboration in KwaZulu-Natal and Lilly’s IT partnership for cloud-based dose-adjustment tools. These moves localize value addition and mitigate import duties while sharpening supply-chain resilience. Digital therapeutics loom as a differentiator; companies integrate Bluetooth-enabled pens with mobile coaching apps, aligning with payer interest in verifiable adherence.

Regulatory dynamics shape competitive cadence. SAHPRA’s fast-track lane for biosimilars promises to open price-elastic segments, especially in basal insulin. Meanwhile, National Health Insurance negotiations prioritize lowest sustainable tender bids, incentivizing cost-efficient producers. Cultural acceptance of traditional medicine nudges innovators to craft communication campaigns that respect local healing narratives, reducing mistrust. Collectively, these trends maintain vigorous rivalry but also encourage collaboration around supply security within the South Africa diabetes drugs market.

South Africa Diabetes Drugs Industry Leaders

AstraZeneca

Merck

Novo Nordisk A/S

Eli Lilly

Sanofi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: University of Cape Town’s Medicines Information Centre confirmed high-dose Ozempic availability after supply worries, restoring access to advanced GLP-1 therapy.

- September 2024: SAHPRA released consolidated schedules under the Medicines and Related Substances Act, altering prescription rules for several diabetes agents.

- May 2024: MSF Southern Africa highlighted a nationwide insulin pen shortage that forced many patients onto vial formulations, underscoring supply fragility.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South Africa diabetes drugs market as all prescription medicines used to lower blood-glucose levels, including insulins, oral anti-diabetic agents, non-insulin injectables, and fixed-dose combinations, distributed through hospital, retail, and online pharmacies to type 1 and type 2 patients.

Scope Exclusions: blood-glucose monitoring devices, insulin pumps, herbal supplements, and over-the-counter nutraceuticals are excluded.

Segmentation Overview

- By Drug Class

- Oral Anti-Diabetic Drugs

- Insulins

- Combination Drugs

- Non-Insulin Injectables

- By Diabetes Type

- Type-1 Diabetes

- Type-2 Diabetes

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies / Tele-pharmacy

Detailed Research Methodology and Data Validation

Primary Research

We interviewed endocrinologists in Gauteng and KwaZulu-Natal, hospital pharmacists active in state tenders, private medical-scheme managers, and executives at two national distributors. Their insights on GLP-1 uptake, generic price erosion, and rural stock-outs refined penetration rates and weighted average selling prices, anchoring assumptions that secondary data alone cannot surface.

Desk Research

Mordor analysts first mapped the treatment landscape with tier-1 public data from the International Diabetes Federation, Statistics South Africa, National Department of Health tender bulletins, SAHPRA import registers, and peer-reviewed journals on medication adherence. Company filings and investor decks clarified price moves, while paid engines such as D&B Hoovers and Dow Jones Factiva supplied shipment values and launch timelines.

These inputs set outer demand bounds by quantifying diagnosed prevalence, dose intensity, and provincial procurement splits. The sources listed are illustrative only; many other public and subscription datasets were consulted for collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down prevalence-to-treated cohort build was executed, beginning with diagnosed adults, adjusting for therapy uptake, and multiplying by annual dose intensity and net ASP to yield value. Supplier roll-ups and sampled pharmacy basket checks, which we have then benchmarked against customs import totals, served as bottom-up reasonableness tests. Key variables tracked include obesity incidence, private insurance membership, insulin biosimilar price deflation, state tender budget growth, and new molecule approvals. Multivariate regression of these drivers generated the 2025-2030 CAGR; only after demand indicators, price curves, and procurement budgets are reconciled do we lock the base year value. Data gaps in bottom-up samples were bridged by moving-average prices from adjacent provinces and weighted volumes from comparable clinics.

Data Validation & Update Cycle

Outputs pass a two-step peer review, variance thresholds trigger re-checks with source owners, and anomalies are escalated before sign-off. Reports refresh annually, with mid-cycle updates when tender awards, reimbursement shifts, or major launches materially move the baseline.

Why Mordor's South Africa Diabetes Drugs Baseline Earn Trust

Published estimates often diverge because each firm selects its own scope, data vintage, and forecast logic.

Key gap drivers include whether combination therapies are pooled, how public-sector tender prices are blended with private list prices, the currency conversion date, and how frequently prevalence data are refreshed.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 326.12 mn (2025) | Mordor Intelligence | |

| USD 341 mn (2024) | Regional Consultancy A | excludes non-insulin injectables and applies static 2023 exchange rate |

| USD 332.82 mn (2023) | Global Consultancy B | relies on historic retail sales only, no public tender adjustment |

The comparison shows that when scope alignment and live tender pricing are applied, Mordor delivers a balanced, transparent baseline that decision-makers can replicate with verifiable inputs, ensuring dependable forward views.

Key Questions Answered in the Report

What is the current South Africa diabetes drugs market size?

The South Africa diabetes drugs market size is USD 344.78 million in 2026 and is projected to reach USD 455.26 million by 2031 at a 5.72% CAGR.

Which drug class holds the largest share in the South Africa diabetes drugs market?

Insulins lead with 51.62% market share in 2025 due to their indispensable role in Type 1 and advanced Type 2 diabetes management.

Why are GLP-1 receptor agonists gaining traction in South Africa?

GLP-1 agents offer combined glycaemic, cardiovascular and weight-loss benefits, aligning with updated local guidelines that prioritize complication reduction.

How is private medical-aid coverage influencing drug uptake?

Expanded chronic benefits enable broader access to premium therapies, accelerating adoption of next-generation agents in urban centers where medical-aid penetration is highest.

What challenges impede wider usage of novel diabetes therapies?

High out-of-pocket costs and intermittent public-sector stock-outs limit consistent access, especially in rural areas lacking robust medical-aid coverage.

How will local manufacturing partnerships impact future drug prices?

Fill-finish agreements such as Novo Nordisk’s deal with Aspen Pharmacare aim to cap insulin vial prices at USD 3, potentially lowering overall therapy costs and improving supply security.

Page last updated on: