Hangover Rehydration Supplements Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

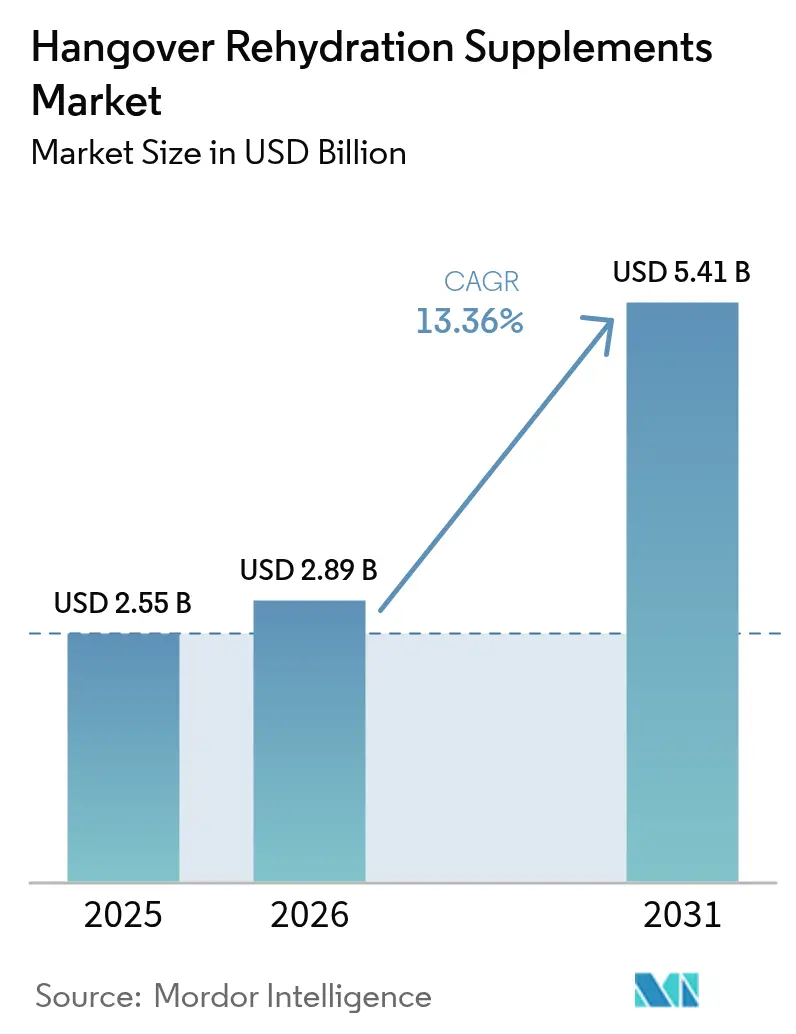

| Market Size (2026) | USD 2.89 Billion |

| Market Size (2031) | USD 5.41 Billion |

| Growth Rate (2026 - 2031) | 13.36% CAGR |

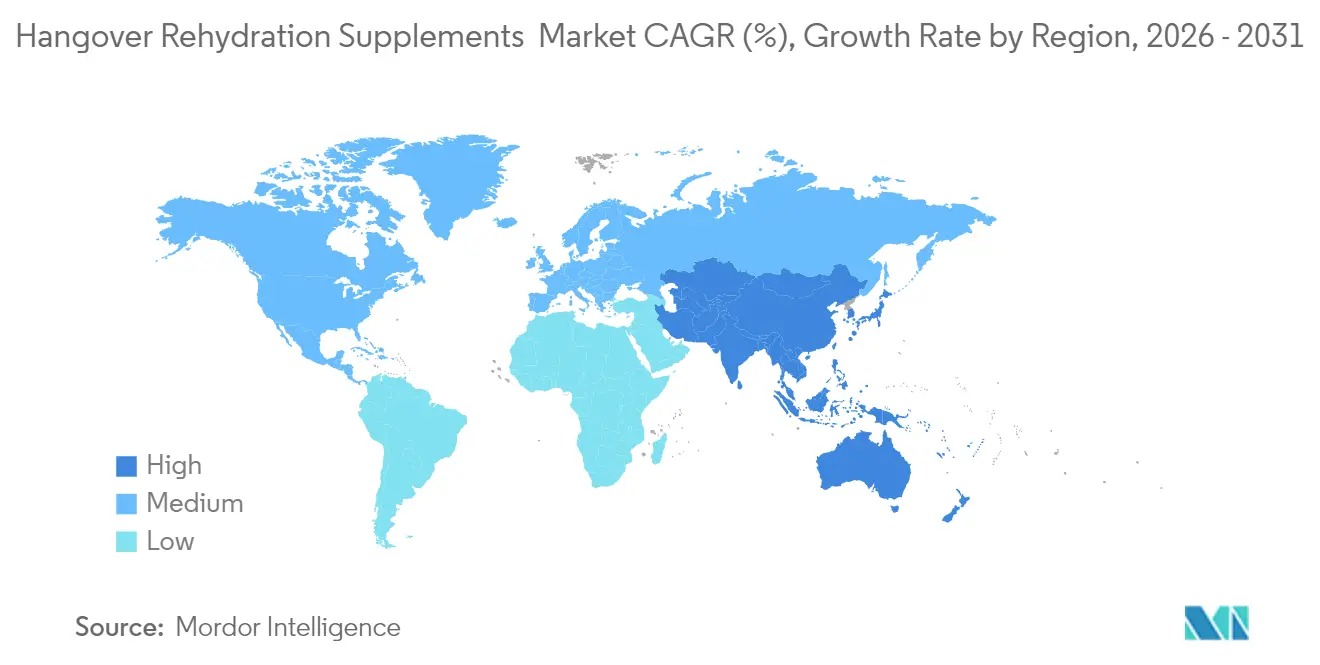

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hangover Rehydration Supplements Market Analysis by Mordor Intelligence

The hangover rehydration supplements market size is expected to grow from USD 2.55 billion in 2025 to USD 2.89 billion in 2026 and is forecast to reach USD 5.41 billion by 2031 at 13.36% CAGR over 2026-2031. Rising wellness consciousness among consumers in their 20s and 30s, along with continued alcohol-related dehydration, sustains robust demand. Regulatory scrutiny in 2024 pushed brands toward science-backed formulations instead of dampening category enthusiasm[1]U.S. Food and Drug Administration, “Warning Letters and Regulatory Updates on Hangover Products,” fda.gov. Fragmentation defines the competitive field because specialty start-ups and large nutraceutical firms innovate simultaneously. Convenience-oriented ready-to-drink (RTD) shots, probiotic ingredients that target acetaldehyde, and expanding e-commerce penetration remain the strongest growth catalysts.

Key Report Takeaways

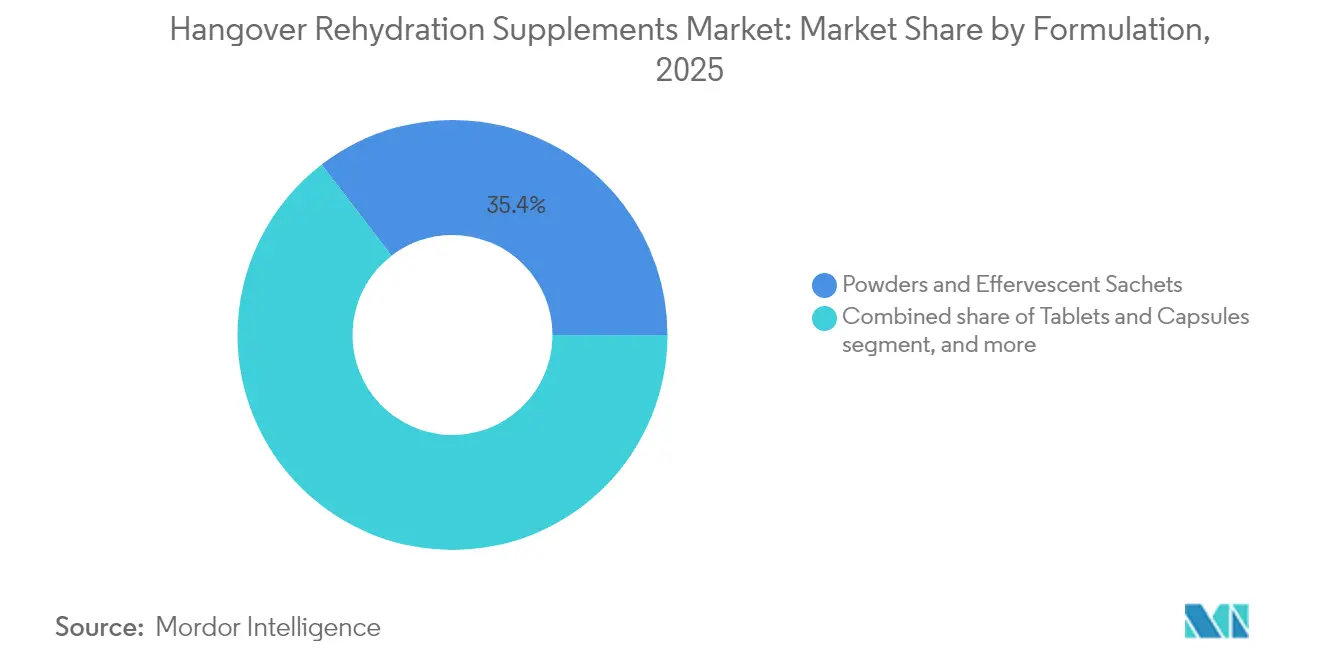

- By formulation, powders and effervescent sachets led with 35.42% of the hangover rehydration supplements market share in 2025, whereas RTD shots are forecast to grow at 15.02% CAGR to 2031.

- By functionality timing, post-drink recovery accounted for a 25.12% share of the hangover rehydration supplements market size in 2025, while in-drink maintenance products are advancing at 14.62% CAGR through 2031.

- By ingredient type, vitamin and mineral blends captured 30.21% revenue share in 2025; probiotic and enzyme-enhanced formulas are projected to expand at 14.29% CAGR to 2031.

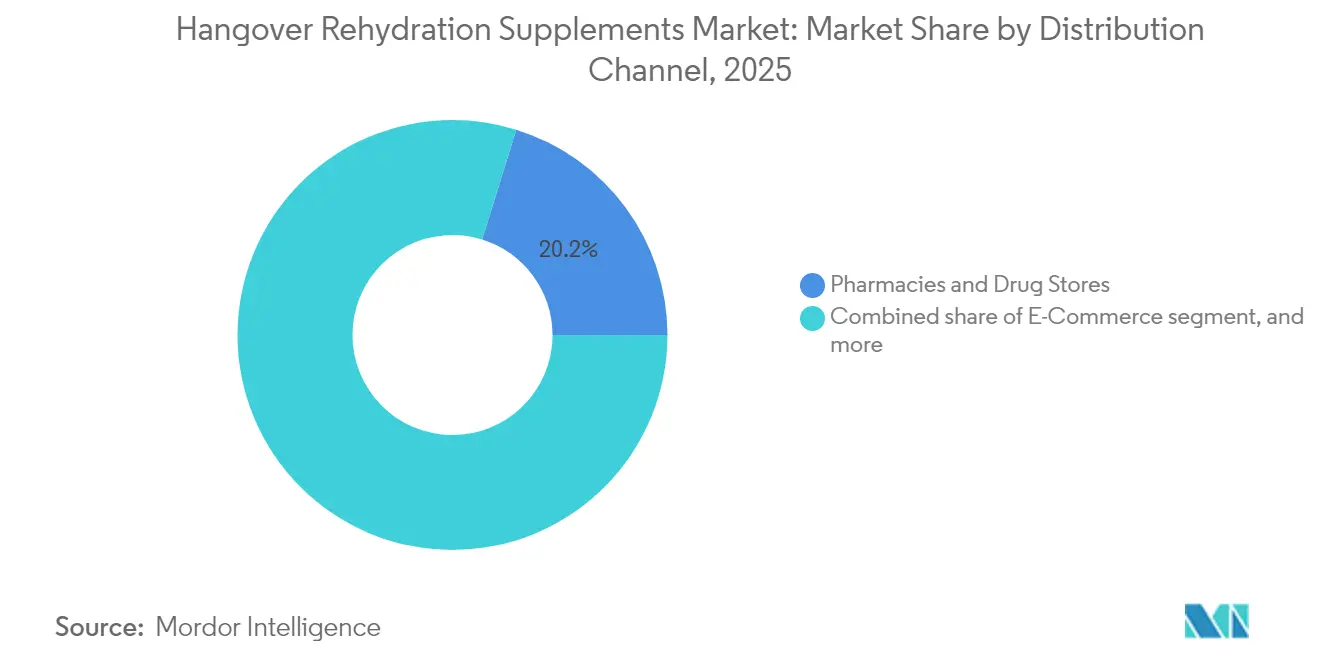

- By distribution channel, pharmacies held 20.21% of the hangover rehydration supplements market size in 2025 as e-commerce platforms post 15.96% CAGR through 2031.

- By consumer group, millennials held 39.58% of the hangover rehydration supplements market size in 2025 as Gen Z post 15.24% CAGR through 2031.

- By geography, North America commanded 38.05% of the hangover rehydration supplements market share in 2025; Asia-Pacific registers the fastest 14.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hangover Rehydration Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Global Alcohol Consumption Levels | +2.8% | North America & Europe | Medium term (2–4 years) |

| Rising Consumer Preference For Preventive Health Supplements | +3.2% | North America & APAC urban centers | Long term (≥ 4 years) |

| Expansion Of E-Commerce Distribution For Nutraceuticals | +2.1% | Global | Short term (≤ 2 years) |

| Growing Millennial And Gen Z Wellness Consciousness | +2.9% | Urban markets worldwide | Long term (≥ 4 years) |

| Corporate Workplace Wellness Programs Covering Hangover Recovery | +1.6% | Global corporate hubs | Medium term (2–4 years) |

| Emergence Of Functional Ingredients With Clinically Proven Hangover Efficacy | +2.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Global Alcohol Consumption Levels

Binge drinking among young adults holds steady despite moderation narratives, creating recurring need for hangover solutions. University‐led research on dihydromyricetin shows that new products target liver protection as well as symptom relief. Such evidence turns occasional users into routine buyers, because supplements are now viewed as proactive wellness tools. Academic studies also link frequent hangover-remedy usage with alcohol use disorder symptoms, which paradoxically enlarges the addressable pool of users.

Rising Consumer Preference for Preventive Health Supplements

Controlled trials by Morning Recovery reported 80% symptom reduction when the supplement is taken before drinking. Probiotic offerings such as Myrkl, priced at USD 25–35 per dose, can eliminate up to 70% of alcohol within 60 minutes. Employers now include these products in corporate wellness programs, which validates preventive usage while increasing unit throughput for vendors.

Expansion of E-Commerce Distribution for Nutraceuticals

Over-the-counter (OTC) products worth more than USD 40 billion migrate online at an annual 3.5% growth rate. Hangover brands that launch on Amazon regularly sell out within days, showcased by Safety Shot’s 2024 debut. Digital storefronts also educate buyers on enzyme science, strengthening trust and enabling subscription revenue streams.

Growing Millennial and Gen Z Wellness Consciousness

Gen Z integrates supplements into social drinking as routine self-care. The Los Angeles Times highlights how younger consumers eagerly test probiotic solutions despite expert caution. Millennials, holding 40.32% of the consumer base, pay premiums for clinically backed products, which encourages ongoing R&D investments among suppliers.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Uncertainty Regarding Hangover Claims | −1.8% | North America & Europe | Medium term (2–4 years) |

| Presence Of Counterfeit And Unverified Products Online | −1.5% | Global, higher in emerging markets | Short term (≤ 2 years) |

| Shift Towards Low Or No-Alcohol Beverages | −1.2% | North America, Europe, emerging APAC | Long term (≥ 4 years) |

| Social Stigma Around Reliance On Hangover Remedies | −1.0% | Global, conservative markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Uncertainty Regarding Hangover Claims

The FDA issued warning letters to 7 brands in 2024, forcing shifts from cure claims to structure-function statements. Legal and scientific compliance raises entry barriers for small operators but provides competitive differentiation for firms that complete rigorous clinical trials. The National Advertising Division’s acceptance of qualified claims shows that approval remains possible with strong data[2]NutraIngredients-Asia, “Dongsung Bio Pharm Secures Funding,” nutraingredients-asia.com.

Shift Toward Low or No-Alcohol Beverages

Moderation trends limit occasions for severe hangovers. Yet binge episodes persist, and some beverage producers now integrate turmeric or similar extracts directly into alcoholic drinks to retain consumers. As a result, demand for standalone supplements falls modestly instead of collapsing outright.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation: RTD Innovation Challenges Powder Dominance

Powders and effervescent sachets accounted for 35.42% of the hangover rehydration supplements market share in 2025. RTD shots, though smaller in base, are expanding at a 15.02% CAGR because on-the-go users prefer single-serve convenience. The hangover rehydration supplements market size for RTD products is therefore predicted to widen sharply between 2026 and 2031. Demand for tablets and capsules remains steady among traditional supplement buyers, while gummies and oral strips appeal to younger customers seeking novel delivery methods.

RTD innovation faces regulatory complexity. The FDA continues to refine guidance that differentiates liquid supplements from beverages, which can slow product approvals. C.L.Pharm’s orally dissolving films deliver faster absorption and command premium shelf prices. Asian consumer acceptance of these formats supports international rollouts that challenge established powder dominance.

By Functionality Timing: Prevention Gains Momentum Over Recovery

Post-drink recovery products led 2025 revenue with 25.12% of the hangover rehydration supplements market size, but in-drink maintenance items are pacing 14.62% CAGR. This reflects a shift toward proactive wellness where users consume supplements during or before drinking. Clinical data from ZBiotics demonstrates enzymatic acetaldehyde breakdown in real time bioRxiv. Morning Recovery has also shown efficacy for pre-drinking regimes, elevating demand for early-timing solutions.

Preventive tools benefit from subscription sales and corporate wellness adoption. Even so, many consumers still rely on familiar next-morning recovery sachets for immediate symptom relief. Dual-use portfolios, offering both pre- and post-drink products, give brands resilience against shifting consumption habits.

By Ingredient Type: Probiotics Challenge Vitamin Dominance

Vitamin and mineral blends held 30.21% market share in 2025, yet probiotic and enzyme formulations are advancing at 14.29% CAGR. The hangover rehydration supplements market largely credits ZBiotics’ engineered Bacillus subtilis strain for this pivot toward microbiome solutions. Botanical extracts such as Hovenia dulcis and Korean pear juice also gain ground after peer-reviewed trials confirm alcohol metabolism benefits.

Ingredient diversification draws pharmaceutical-style R&D budgets. Dongsung Bio Pharm invested KRW 570 million to explore endemic botanicals, reflecting regional innovation cycles. As clinical evidence grows, consumers trade up from basic B-vitamin blends to mechanistic probiotics, expanding average selling prices.

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Pharmacies kept 20.21% of 2025 revenue, but e-commerce posts the strongest 15.96% CAGR. The hangover rehydration supplements market size generated online is on track to double by 2030 as direct-to-consumer (DTC) models overcome geographic retail gaps. Amazon sell-outs prove online demand velocity, while brand websites capture subscription buyers.

Brick-and-mortar remains relevant. Cheers Health extended to 3,000 convenience outlets with Lil’ Drug Store Products. Grocery chains add mainstream visibility, and specialty stores offer expert guidance on complex formulas. This multichannel mix cushions suppliers against platform risk.

By Consumer Group: Gen Z Acceleration Challenges Millennial Leadership

Millennials commanded 39.58% revenue in 2025. Gen Z, however, increases spending at a 15.24% CAGR, narrowing the gap rapidly. The hangover rehydration supplements market finds Gen Z willing to adopt novel probiotics despite limited longitudinal data. Gen X and Boomers account for smaller yet higher ticket purchases because they favor premium science-backed options.

Digital nativity shapes buying journeys. Gen Z uses social media to discover brands, favoring transparent efficacy claims. Millennials, by contrast, respond to workplace wellness incentives and family-sized multipacks. Targeted messaging therefore differs across cohorts, requiring agile marketing.

Geography Analysis

North America led with 38.05% market share in 2025 and is expected to retain influence through 2031. FDA oversight creates both hurdles and strategic advantages for compliant firms. Brands such as Safety Shot secure patents and leverage strong retail infrastructure to sustain premium price points. Corporate wellness integration further entrenches category demand.

Asia-Pacific is the fastest grower at 14.11% CAGR. Rising disposable income and evolving social drinking norms accelerate category uptake in South Korea and Japan. Government-supported research into native botanicals, like Dongsung Bio Pharm’s project, modernizes traditional remedies with clinical evidence. Delivery innovations—including orally dissolving films—match the region’s appetite for convenient functional products.

Europe offers sizable but complex potential because regulations vary widely. Consumers embrace functional foods, and cross-border ingredient flows bring Korean pear juice and Hovenia dulcis products into EU channels. Companies that localize labeling and comply with varied health-claim standards can capture share. Regional moderation trends temper growth, yet premium preventive supplements offset lower volume with higher unit value.

Regulatory Landscape

In the United States, hangover-related products face elevated enforcement risk when marketing shifts into drug claims. In 2024, the US Food and Drug Administration (FDA) sent warning letters to seven companies for illegally selling hangover products. The guidance reinforced that claims to treat, cure, mitigate, or prevent hangovers can trigger classification as an unapproved new drug under the FD&C Act, so many brands have moved toward hydration and general wellness structure-function language while tightening substantiation.

In 2026, the FDA Office of Dietary Supplement Programs held a public meeting (March 2026, Docket FDA-2026-N-2047) to explore the scope of dietary supplement ingredients, tied to ongoing work on how ingredients fit within the dietary supplement definition. In the European Union, Regulation (EC) No 1924/2006 and the EU nutrition and health-claims framework (as reflected through EFSA processes and the EU Register of Health Claims) restrict hangover prevention or cure-type claims for food supplements. This has pushed companies toward more disciplined labeling and evidence-backed positioning that can pass review across member states.

Competitive Landscape

The hangover rehydration supplements market remains moderately fragmented. Top players hold limited combined share because ingredient knowledge and contract manufacturing lower entry barriers. Yet regulatory compliance costs and the need for published clinical data drive gradual consolidation. Biotech entities such as ZBiotics build defensible positions through patents and peer-reviewed evidence.

Strategic moves vary. Multinationals like Unilever entered the space by investing in Create Wellness in 2024, signaling broader consumer-goods interest. Digital-native brands pursue DTC subscription models, while pharmacy-oriented players cultivate healthcare professional endorsements. Intellectual-property portfolios around delivery formats and enzymes increasingly differentiate winners from commodity suppliers.

Technology adoption centers on improved bioavailability and real-time digital education. Firms invest in enzyme encapsulation, orally dissolving films, and AI-driven content to explain science in plain language. As clinical transparency grows, consumer skepticism declines, lifting category credibility.

Hangover Rehydration Supplements Industry Leaders

More Labs

Rally Labs LLC

Flyby

Himalaya Global Holdings Ltd

Safety Shot Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is concentrated in compliant, evidence-led positioning that frames products around hydration support and alcohol-occasion usage without triggering prohibited hangover cure claims. The 2024 FDA enforcement actions against seven companies, together with the 2026 focus on dietary supplement ingredient scope, increases the value of clinical substantiation, labeling discipline, and quality systems. That environment supports brands with published data (including engineered probiotic and enzyme approaches referenced in competitive positioning), and it favors portfolios that segment offerings into pre-drink prevention, in-drink maintenance, and post-drink recovery to match changing consumption patterns.

Format and channel expansion continues to be a practical route for volume growth. RTD shots and other convenience formats benefit from established beverage retail and distribution, while e-commerce and subscription models can carry the education-heavy story for probiotic and enzyme-enhanced formulas. Recent company actions highlight active expansion pathways, with More Labs broadening US distribution via a major alcohol-beverage distributor in 2026, and Liquid I.V. expanding its powdered hydration footprint across multiple European markets in 2026. These moves reinforce cross-over consumer interest in functional hydration that hangover-focused brands can target with compliant claims, localized labeling, and region-ready formulations.

Recent Industry Developments

- June 2026: More Labs announced a distribution agreement with Southern Glazer’s Wine & Spirits, effective June 1, 2026, to distribute its products across ten US states including California, Texas, and Florida. The partnership expands access through an established beverage distribution network, improving shelf reach for hangover-adjacent wellness shots across on-premise and off-premise accounts.

- June 2025: Safety Shot completed its acquisition of Yerbaé Brands Corp. following a previously announced arrangement agreement. The deal broadens Safety Shot’s functional beverage portfolio and adds an established distribution footprint, supporting cross-selling opportunities between hydration, energy, and recovery positioning.

- April 2025: More Labs announced a nationwide rollout into Sprouts Farmers Market stores. The retail expansion increases visibility in natural and wellness-focused channels, supporting trial and repeat purchases for preventive and recovery-oriented supplement formats.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers consumer products sold as hangover rehydration supplements that are taken before, during, or after alcohol consumption to support hydration and related recovery needs.

Scope exclusions: We exclude general sports electrolyte drinks that are not positioned for hangover use and intravenous recovery services.

Segmentation Overview

- By Formulation

- Tablets & Capsules

- Powders & Effervescent Sachets

- Ready-to-Drink (RTD) Shots

- Oral Strips & Gummies

- By Functionality Timing

- Pre-Drink Prevention

- In-Drink Maintenance

- Post-Drink Recovery

- By Ingredient Type

- Botanical Extract Based

- Vitamin & Mineral Blends

- Amino-Acid / NADH Focused

- Probiotic / Enzyme-Enhanced

- By Distribution Channel

- Pharmacies & Drug Stores

- E-Commerce

- Convenience & Gas Station Retail

- Grocery & Mass Retail

- Specialty Supplement Stores

- By Consumer Group

- Gen Z

- Millennials

- Gen X

- Baby Boomers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped map what is being sold, where it is sold, and how demand signals shift by geography and channel. We used public sources such as the US FDA (dietary supplement and labeling guidance), NIH Office of Dietary Supplements ingredient fact sheets, the US CDC (alcohol use indicators), and WHO alcohol health and consumption statistics to frame the demand pool and consumer triggers. For region-level context, we also referred to sources such as Eurostat and other national statistics portals where alcohol-related spending and health indicators are reported.

To connect the market definition to measurable numbers, we reviewed company filings and investor presentations, product labels, e-commerce listings, and credible press coverage to understand pack sizes, price points, and claims that affect purchasing. Where available, we also used paid subscriptions focused on company financials and intelligence, patent databases, and news and financials to confirm launches, distribution expansion, and ingredient positioning. These sources are illustrative, and additional public and paid references were used for data collection, cross-checks, and clarification during analysis.

Primary Interviews and Surveys

Primary work focused on checking how products are priced, how fast online sales are shifting versus retail, and what share of demand is truly hangover-specific rather than general hydration. We spoke with brand and channel stakeholders, ingredient and formulation experts, and downstream distributors across major regions so gaps from desk research could be closed and assumptions reconciled before final sizing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | APAC: 50% |

| Mid tier: 48% | Functional/Unit leaders: 33% | EMEA: 29% |

| Smaller Players: 16% | Managers: 54% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up flow where the demand pool is reconstructed from alcohol consumption patterns and the expected adoption of hangover-targeted hydration formats, and then translated into value using price and pack assumptions. On the demand side, we leaned on indicators such as adult drinking prevalence, frequency of binge drinking, growth in convenience-led purchases, e-commerce penetration for supplements, and regional differences in dietary supplement usage. Because the category spans multiple selling formats, we also tracked common formats (powders and effervescent sachets, tablets and capsules, RTD shots, strips and gummies) and typical pack sizes to avoid overstating value from high-priced trial packs.

Once the top-down totals were formed, they were corroborated using selective bottom-up approximations, including sampled SKU price checks across channels, a roll-up of visible brand revenues where disclosed, and channel checks on how much shelf space and promotional intensity is tied to hangover use. Where brand-level disclosures were incomplete, gaps were handled by applying channel-weighted average selling price (ASP) bands and adjusting volumes using interview feedback on repeat purchase rates. For forecasting, we used scenario analysis with a base case anchored on expected alcohol consumption stability, price and discounting trends, and mix shifts toward RTD shots and online bundles, and then adjusted by region based on expert views of regulation, claim scrutiny, and retail expansion.

Data Validation & Update Cycle

Validation was done through multiple checks so the final outputs remain consistent with real-world signals. We compared modeled values with independent markers such as channel growth rates, reported category growth in supplements, and observable pricing movement, then investigated outliers before sign-off. When large variances appeared, assumptions were re-tested through follow-up outreach and a second review pass so that scope, conversion logic, and price inputs stayed aligned.

Reports are refreshed annually, and interim updates are triggered when material events occur, such as major regulatory actions, rapid price changes, or notable distribution shifts. Before delivery, an analyst runs a fresh update pass to ensure clients receive the latest view tied to the most recent data and validated assumptions.

Mordor Intelligence's Hangover Rehydration Supplements Market Size Compared With Other Published Estimates

Published market values for hangover rehydration supplements can look far apart even when they sound like they cover the same space. The main reasons usually sit in timing of the base year, what counts as a hangover product versus general hydration, and how prices are normalized across fast-changing online and retail promotions.

In this category, the refresh cadence and currency timing matter because ASPs move quickly with discounting, bundle packs, and new format launches. That is why the model is rechecked using current-year price scans and channel-weighted conversion before the total is finalized, a step applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.55 B (2025) | |

| Industry Research Publisher A | USD 1.80 B (2026) | Uses a later start year and a broader multi-year forecast window, which can compress the near-term value if pricing is averaged and promotions are not channel-weighted. |

| Market Insights Firm B | USD 2.60 B (2024) | Anchors to an earlier year and appears to keep scope closer to general electrolyte solutions in some regions, which can shift totals depending on what is treated as hangover-specific positioning. |

Across the three figures, the spread is mainly explained by different year anchors and how each publisher treats pricing and channel mix during periods of heavy online discounting. Our approach stays traceable because the scope boundary is kept tight to hangover-positioned supplements, and the value is rebuilt from adoption signals and channel-weighted ASPs that are revalidated before the final number is published.

Key Questions Answered in the Report

What is the current value of the hangover rehydration supplements market?

The hangover rehydration supplements market is valued at USD 2.89 billion in 2026.

How fast is the hangover rehydration supplements market expected to grow?

The market is projected to expand at a 13.36% CAGR, reaching USD 5.41 billion by 2031.

Which formulation type is growing the quickest?

Ready-to-drink shots post the highest 15.02% CAGR through 2031 thanks to on-the-go convenience.

Why is Asia-Pacific the fastest-growing region?

Rising disposable income, evolving social drinking habits, and modernization of traditional remedies push Asia-Pacific growth at 14.11% CAGR.

How are regulations affecting new product launches?

FDA and EU authorities now require substantiated structure-function claims, which raises development costs but favors firms with clinical data.

Which ingredients are gaining popularity beyond vitamins?

Probiotic strains that break down acetaldehyde and botanical extracts like Hovenia dulcis are advancing quickly due to stronger scientific validation. . . . . . . . New Research

Page last updated on: