Website Builders Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.57 Billion |

| Market Size (2031) | USD 7.67 Billion |

| Growth Rate (2026 - 2031) | 16.58% CAGR |

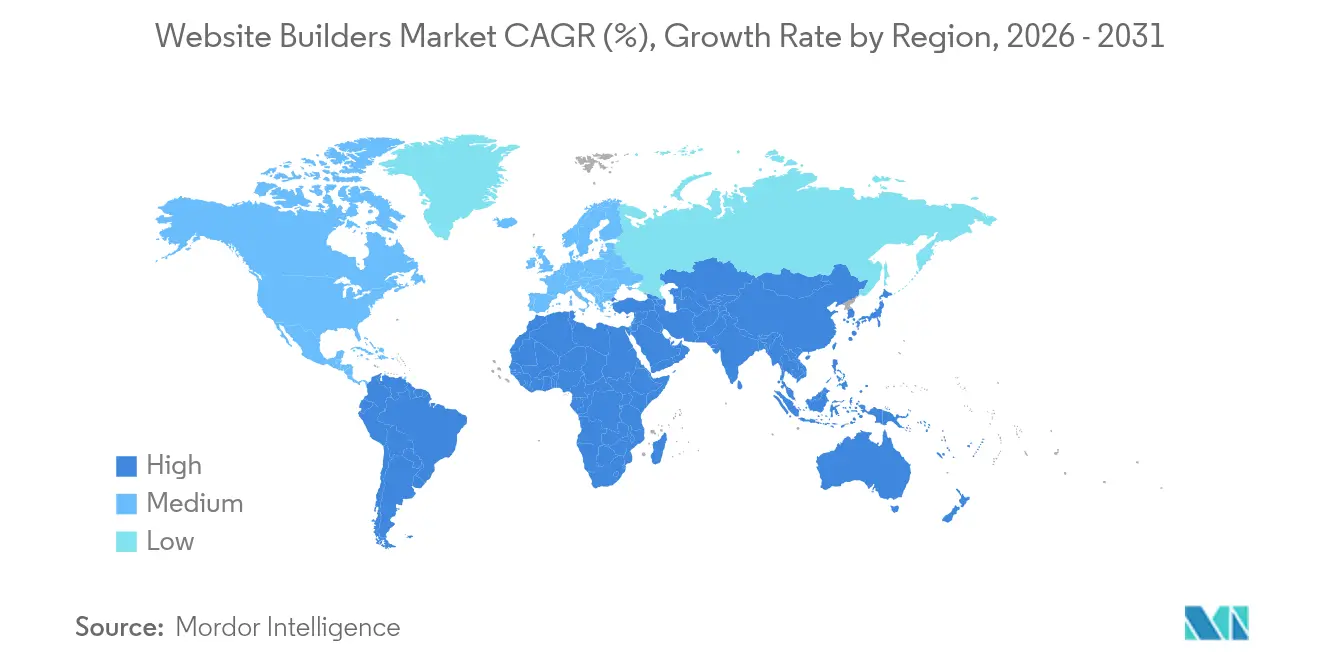

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

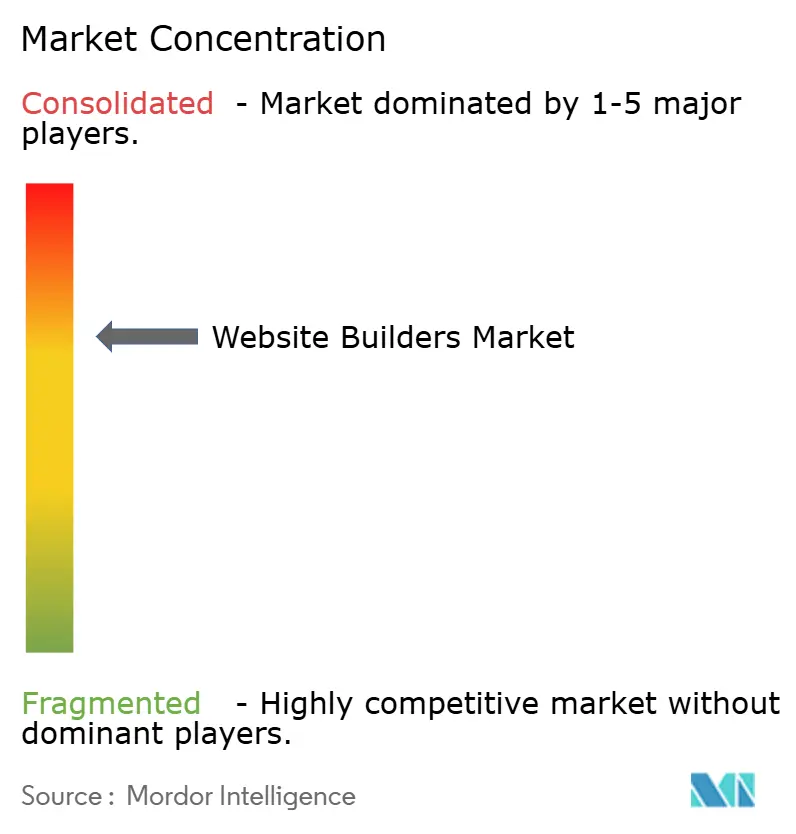

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Website Builders Market Analysis by Mordor Intelligence

Website builders market size in 2026 is estimated at USD 3.57 billion, growing from 2025 value of USD 3.06 billion with 2031 projections showing USD 7.67 billion, growing at 16.58% CAGR over 2026-2031. The sharp rise reflects faster digital transformation among small and medium businesses, growing low-code use, and the steady rollout of AI design assistants. Mobile-first internet adoption, expanding SaaS comfort levels, and government programs that back online commerce further accelerate demand. Consolidation is underway as large vendors acquire AI specialists, while private-equity funds inject capital into proven platforms. Meanwhile, data-privacy laws and mounting cybersecurity costs temper near-term upside yet also spur premium security offerings, widening revenue streams across the website builders market.

Key Report Takeaways

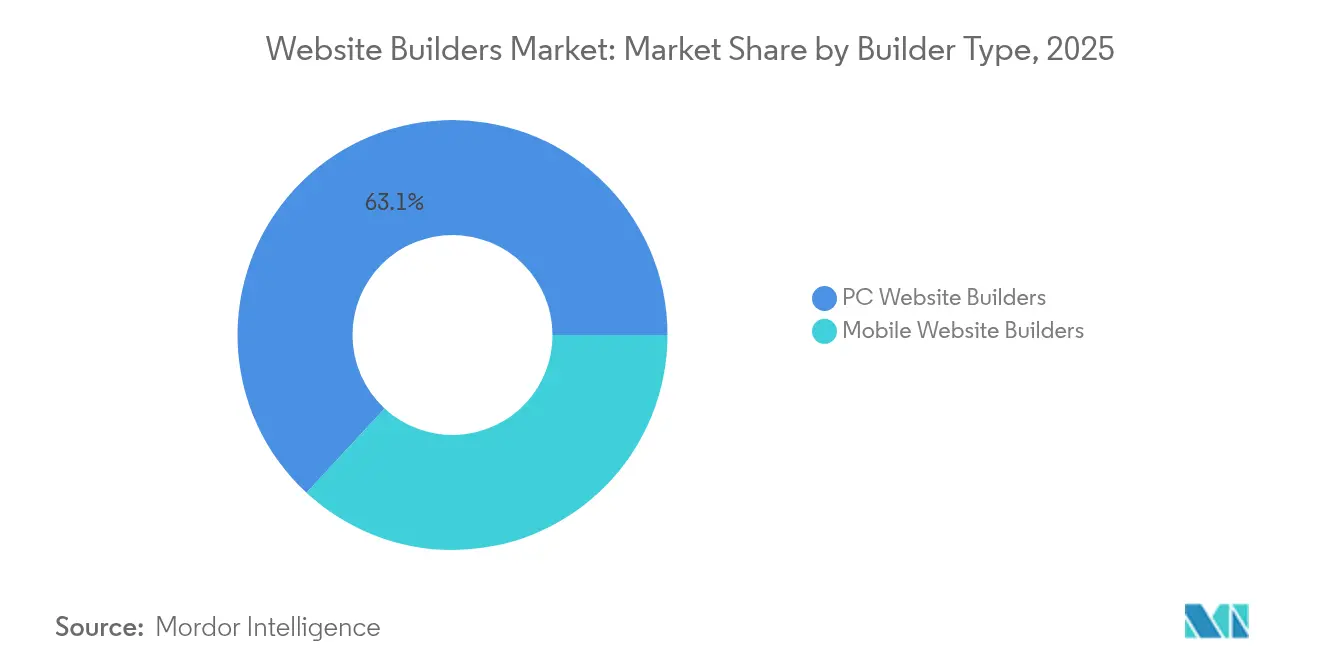

- By builder type, PC website builders held 63.12% of the website builders market share in 2025; mobile website builders are projected to post a 17.43% CAGR through 2031.

- By deployment, cloud models captured 81.08% revenue share in 2025; on-premises options remain niche but resilient among regulated enterprises.

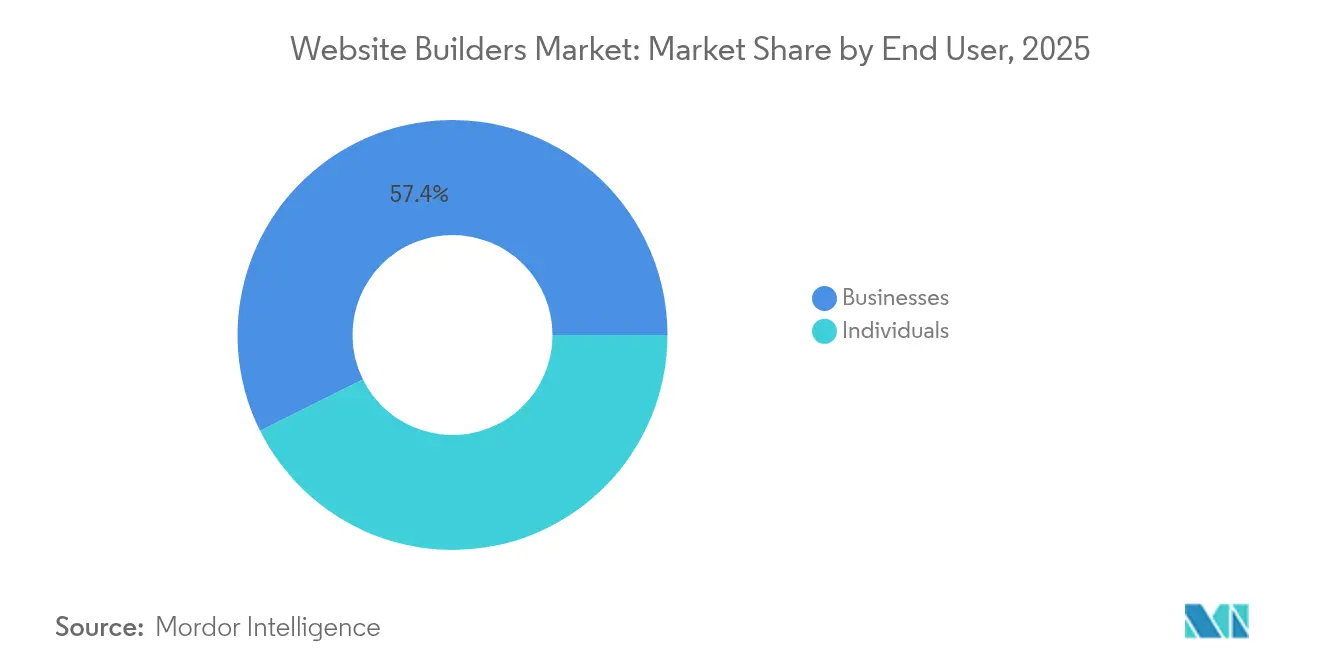

- By end user, the business segment accounted for 57.35% of the website builders market size in 2025, whereas the individual segment is set to register a 19.06% CAGR through 2031.

- By pricing tier, plans under USD 15 per month secured 38.10% demand in 2025; the USD 15-50 band is poised for a 19.72% CAGR during 2026-2031.

- By geography, North America commanded 38.25% revenue in 2025; Asia-Pacific is forecast to grow at a 18.76% CAGR between 2026 and 2031.

- Wix, Shopify and Squarespace together controlled over half of total 2024 revenue, yet rising AI-first entrants point to shifting competitive ground.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Website Builders Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in SMB-driven e-commerce storefront launches | +3.2% | Global, with concentration in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Mobile-first internet penetration | +2.8% | Asia-Pacific core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Low-/no-code adoption in digital transformation | +2.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| AI-generated site design and content creation | +2.1% | North America and EU early adoption, global expansion | Short term (≤ 2 years) |

| Google Core Web Vitals optimisation push | +1.8% | Global, with emphasis on mobile-heavy markets | Short term (≤ 2 years) |

| Rise of headless/JAMstack builders | +1.6% | North America and EU developer communities | Long term (≥ 4 years) |

| Surge in SMB-driven e-commerce storefront launches | +3.2% | Global, with concentration in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in SMB-driven E-commerce Storefront Launches

India’s GeM portal surpassed USD 24 billion in procurement value during FY 2023, signalling public-sector momentum that nudges SMBs online. Rising online grocery and fashion demand pushes regional merchants to seek turnkey stores, and website builders now package payment, shipping and tax modules to shorten setup time. B2B buyers also shift to self-service portals, expanding platform scope beyond pure retail. Tier-II and Tier-III cities contributed a sizeable 41.5% share of new sites in 2022, proving addressable demand extends well outside metros. Market leaders re-tool templates and partner presses to localize language, tax and logistics features for these growth pockets.

Mobile-first Internet Penetration

Mobile internet adoption transforms website builder architecture requirements, with the Asia-Pacific region hosting 1.8 billion mobile subscribers representing 63% of the population as of 2023.[1]GSMA Intelligence, “The Mobile Economy Asia Pacific 2024,” gsma.com Mobile technologies contributed 5.3% to the region's GDP, amounting to USD 880 billion, while supporting approximately 13 million jobs, demonstrating the economic imperative for mobile-optimized web presence. The shift toward 5G technologies and Open Gateway APIs enhances connectivity solutions, enabling more sophisticated mobile website functionalities. Generative AI integration in mobile platforms improves customer service and operational efficiency, creating opportunities for AI-powered mobile website builders. The mobile ecosystem's role in economic growth and digital inclusion positions mobile-first website builders as critical infrastructure for emerging market businesses.

Low-/No-Code Adoption in Digital Transformation

The low-code/no-code market trajectory toward USD 94 billion by 2028 reflects fundamental shifts in software development democratization, with 85% of business technology stacks expected to comprise SaaS solutions by 2025. This transformation enables non-technical users to create sophisticated websites without coding expertise, expanding the addressable market beyond traditional developer segments. Micro-SaaS solutions targeting niche markets emerge as significant growth drivers, while white-label SaaS platforms enable customization for specific industry verticals. Embedded analytics capabilities provide real-time data insights, enhancing website builder value propositions for data-driven businesses.

AI-generated Site Design and Content Creation

Artificial intelligence integration revolutionizes website creation workflows, with platforms like Wix AI enabling business-ready websites through conversational interfaces that generate site briefs and customizable themes.[2]Wix.com Ltd., “Wix AI: Build Your Website in Minutes,” wix.com AI-powered tools automate coding tasks and enhance user experiences, with GitHub Copilot reducing debugging time by 30-40% while improving development efficiency Machine learning algorithms enable personalized user experiences through content suggestions and UI optimization, creating competitive advantages for AI-integrated platforms. Webflow's acquisition of Intellimize for AI-driven personalization demonstrates industry recognition of AI's strategic importance in website optimization. The emergence of prompt-based development and natural language interfaces reduces technical barriers, expanding market accessibility to non-developer segments.

Data-privacy and cybersecurity concerns

GDPR and CCPA demand granular consent controls, driving builders to embed cookie banners, DPA templates and breach-alert flows. Platforms like Enzuzo now integrate legal policy generators directly into dashboards. Zero-Trust architecture adoption lifts baseline security spend just as SMB budgets tighten, making price points harder to defend. Malicious actors increasingly target SaaS site credentials, prompting vendors to add MFA and AI anomaly detection. Smaller entrants may struggle to fund these safeguards, amplifying consolidation forces inside the website builders market.

Intense competition from open-source CMS

WordPress still powers over 60% of content sites worldwide, buoyed by a vast plugin pool and active developer forums. Migration tools such as LitExtension reveal that nearly two-thirds of recent moves head toward open-source stacks, reflecting ongoing price and flexibility advantages. Headless CMS frameworks let businesses marry an open back-end with a commercial front-end, blurring category lines and squeezing proprietary builders on customization depth. To retain advanced users, vendors now expose APIs, custom code blocks and dev-mode sandboxes without diluting low-code simplicity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Builder Type: Mobile Platforms Drive Innovation

PC website builders retained 63.12% revenue in 2025, anchoring the website builders market through robust feature breadth, agency tools and multistore support. Yet mobile builders are carving share at an 17.43% CAGR through 2031 as smartphone usage eclipses desktop time in many regions. Responsive templates now open by default, and voice-led design wizards hasten launch for mobile-centric merchants. Wegic alone has created over 600,000 mobile-ready sites in 230 nations, highlighting crop growth among new entrants. Traditional PC platforms increasingly adopt adaptive canvases and one-tap layout swaps, foreshadowing a convergence where device labels fade and omnichannels remain.

Demand for seamless editing across phone, tablet and laptop steers vendors to cloud-hosted editors that save state continuously, a shift that reinforces the broader website builders market. Live preview on multiple breakpoints, auto-compress image handling, and lazy-load scripts help operators satisfy Google Core Web Vitals thresholds. Platform depth must now coexist with lean UIs to keep churn low among casual creators while satisfying agencies that demand granular CSS control, signaling product bifurcation ahead.

By Deployment: Cloud Dominance Accelerates

Cloud solutions held 81.08% of 2025 revenue, placing a commanding stamp on the website builders market. SaaS models bundle hosting, SSL, CDN and updates, relieving SMBs of upkeep tasks. Edge computing advances move assets closer to visitors, trimming latency and lifting SEO scores. Serverless back-ends unlock cost-efficient scaling during flash sales, a key draw for e-commerce users. On-premises installs linger in regulated sectors where data residency rules prevail, but roadmap investment tilts clearly toward cloud orchestration.

Composable web designs are gaining favor as Netlify’s acquisition of Gatsby demonstrates, letting developers swap commerce, search and auth services on demand. This module approach accelerates feature delivery while curbing technical debt. Providers that streamline plug-in vetting and enforce security scans create trust advantages, especially for non-technical buyers wary of scope creep and hidden fees. Consequently, cloud remains the gravitational center of innovation, ensuring its share within the website builders market size continues to climb.

By End User: Business Segment Leads Growth

Business accounts produced 57.35% of 2025 revenue, anchored by SMBs adding online storefronts and booking engines. Integrated payments, inventory sync and CRM links are now baseline expectations, pushing vendors to ink deeper ties with fintech and logistics APIs. India’s 100% FDI allowance in B2B e-commerce lifts multi-vendor catalog demand, spurring builders to prepackage RFQ and bulk-order modules. The individual user group, from freelancers to content creators, is set for a 19.06% CAGR as side-hustle culture expands and portfolio sites become digital résumés.

Freemium to premium upgrade funnels remain central. As AI copywriting and image generation mature, individuals perceive immediate quality gains that justify paid tiers beyond USD 15. Meanwhile, businesses adopt subscription bundles that tie email marketing, accounting and fulfillment dashboards together, raising lifetime values and reinforcing the website builders market size outlook.

By Pricing Tier: Affordable Plans Dominate

Subscriptions below USD 15 per month attracted 38.10% of spend in 2025, evidencing cost sensitivity among micro-enterprises and students. However, the USD 15-50 range is forecast to grow at 19.72% CAGR, buoyed by demand for abandoned-cart recovery, multilanguage sites and advanced SEO tooling. Platforms increasingly map higher fees to measured outcomes such as conversion lift or page-speed scores, aiding value-based pricing adoption. Enterprise bundles exceeding USD 50 cater to sizable catalogs, multi-seat governance and custom SLA requirements; although smaller in volume, their margins buffer RandD budgets.

App marketplaces complicate total-cost calculus as stacking extensions can eclipse base plan fees, prompting buyers to scrutinize recurring charges. Vendors that fold critical additions—analytics, AMP pages, sales tax automation—into mid-tier plans may widen adoption. Clear, predictable billing thus becomes a competitive lever within the website builders market.

Geography Analysis

North America generated 38.25% of 2025 revenue and remains a benchmark for feature launches and partner ecosystems. Mature credit-card penetration and fast broadband create fertile ground for premium upsells. AI rollouts debut in this region before global release, reinforcing its influence on roadmap direction. Yet saturation among micro-businesses leads vendors to pursue vertical niches and performance-linked pricing to sustain growth.

Asia-Pacific is the engine of future expansion, posting a projected 18.76% CAGR to 2031. Mobile-first behavior, a 51% mobile internet share, and supportive government digital agendas fuel uptake. Public programs such as Singapore’s AI grants and India’s ONDC network incentivize merchants to get online swiftly. Local payment gateways, multilingual checkout flows and low-bandwidth themes help international vendors adapt, while regional startups leverage cultural nuance to compete head-to-head. These dynamics position Asia-Pacific as the pivotal theatre where the website builders market proves its scalability.

Europe occupies a large, compliance-driven slice of demand. GDPR continues to shape feature priorities, and eco-hosting commitments gain weight as carbon accounting gains board-room visibility. Builders that deliver automated data-subject request tools and renewable-powered servers earn premium positioning. Latin America and the Middle East and Africa, although smaller, clock double-digit uptake thanks to rising internet penetration and social-commerce spill-overs. Strategic alliances with telecom operators and media houses facilitate trust and distribution in these regions, ensuring a geographically balanced trajectory for the website builders market.

Competitive Landscape

Market leadership rests with Wix, Shopify and Squarespace, whose combined control exceeds 50% of 2024 revenue. Each focuses on AI to harden moats: Wix invested USD 80 million to acquire natural-language specialist Base44, integrating prompt-driven site creation. Shopify pours RandD into unified commerce back-ends, enabling POS, ERP and fulfillment on a single login. Squarespace draws on Permira’s USD 7.2 billion backing to accelerate enterprise headless initiatives and international localisation.

Webflow, Duda and BigCommerce pursue composability, offering granular API layers beneath designer-friendly UIs. Netlify’s purchases of Gatsby and Stackbit underscore the value of composable ecosystems that slot into any tech stack. Vertical experts such as Ecwid target SMB retailers with lightweight carts, while regionally focused Mono Solutions partners with European directory publishers to embed white-label builders inside advertising bundles.

Competitive intensity heightens as open-source CMS communities accelerate plugin innovation and as generative-AI startups challenge incumbents with leaner cost bases. To stay ahead, established players emphasize marketplace curation, enterprise compliance tools and omnichannel commerce integrations. As consolidation persists, vendors with rich cash flow and defined partner networks stand best placed to extend reach within the website builders market.

Website Builders Industry Leaders

Wix.com Inc.

Automattic Inc

Squarespace, Inc.

Shopify Inc.

Shopify Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Wix completed an USD 80 million acquisition of Base44 to enhance natural-language software development capabilities, enabling users to create websites through conversational interfaces and expanding AI-powered automation features across the platform.

- May 2025: Shopify announced Q1 2025 revenue of USD 2.36 billion, achieving 27% year-over-year growth with Gross Merchandise Volume of USD 74.75 billion.

- February 2025: Webflow launched its AI Site Builder in beta, offering tailored website theme generation based on business details and enabling customization of layouts, colors and fonts through AI-powered tools.

- February 2025: Shopify reported Q4 2024 revenue of USD 8.88 billion with 26% annual growth, achieving operating income of USD 1.075 billion.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the website builders market as revenue generated by software platforms that let non-developers create, launch, and maintain websites through drag-and-drop or guided visual interfaces, delivered either through cloud SaaS portals or installable packages. This includes desktop-centric builders, mobile-first builders, bundled hosting plans, template marketplaces, and add-on ecommerce or SEO modules that are billed under the same plan.

Scope Exclusions: Custom-coded sites using traditional CMS frameworks or developer-only code editors are not counted.

Segmentation Overview

- By Builder Type

- PC Website Builders

- Mobile Website Builders

- By Deployment

- Cloud

- On-Premises

- By End User

- Individuals

- Businesses

- By Pricing Tier

- Freemium

- Subscription <USD (15 / mo)

- Subscription USD (15-50 / mo)

- Enterprise > USD (50 / mo)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Southeast Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with SaaS executives, hosting resellers, web-design agencies, and regional small-business federations across North America, Europe, Asia Pacific, and Latin America. These conversations clarified average selling prices, churn patterns, emerging AI-assisted design features, and regional payment preferences, helping us adjust preliminary desk findings.

Desk Research

We began with foundational datasets from bodies such as ICANN and Verisign (domain registrations), OECD and Eurostat (SME digitization), and national telecom regulators tracking broadband and 4G/5G penetration. Industry association white papers on low-code adoption, SEC 10-Ks of leading builder vendors, and global trade filings enriched the revenue split between subscription and freemium tiers. To vet corporate financials, we accessed D&B Hoovers, while trend and news sweeps were undertaken through Dow Jones Factiva. Additional insight came from W3Techs and BuiltWith scans that map active builder footprints. The sources listed illustrate the breadth of desk research; many other public and proprietary references were consulted to cross-verify statistics.

Market-Sizing & Forecasting

A top-down and bottom-up hybrid model anchors our estimates. We first reconstruct total addressable spend from active domain counts, SME formation rates, and penetration-rate based demand pools, then corroborate totals through sampled average subscription price × user volumes reported by leading suppliers and channel checks. Key variables feeding the model include monthly active domain additions, freemium-to-paid conversion ratios, smartphone share of web traffic, SaaS price dispersion, regional GDP-per-SME, and payment-gateway take-rates. Multivariate regression against these drivers produces the forecast, with scenario analysis layering upside or downside cases around AI-generated site adoption. Where supplier roll-ups under-represent emerging regions, gaps are filled using regional growth proxies derived from mobile data-traffic trends.

Data Validation & Update Cycle

Outputs undergo variance checks versus historical series, peer estimates, and newsflow; anomalies trigger re-contact with interviewees before analyst sign-off. Mordor refreshes every study annually and issues interim updates when material events, price hikes, major M&A, or regulatory shifts move the baseline.

Why Mordor's Website Builders Baseline Commands Confidence

Published figures often diverge because firms pick different feature scopes, price stacks, and refresh cadences. Our disciplined variable selection, yearly model rebuild, and dual-track validation give decision-makers a transparent, reproducible baseline.

Key gap drivers stem from narrower platform coverage, older base years, or reliance on static CAGR extrapolations used elsewhere, while Mordor's model captures mobile-first freemium growth, regional price localization, and AI-driven upsell dynamics.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.06 B (2025) | Mordor Intelligence | - |

| USD 1.97 B (2024) | Regional Consultancy A | Excludes mobile-only builders and freemium revenue; uses linear CAGR without primary validation |

| USD 1.80 B (2022) | Trade Journal B | Older base year, hardware sales proxy, limited geography |

| USD 1.84 B (2023) | Industry Association C | Bundles builder plug-ins within broader CMS, scant interview cross-checks |

Taken together, the comparison shows that Mordor's market value rests on up-to-date field input, full platform scope, and clearly tracked variables, giving stakeholders a balanced baseline they can trace and repeat with confidence.

Key Questions Answered in the Report

What is the current size of the website builders market?

The website builders market is valued at USD 3.57 billion in 2026 and is expected to reach USD 7.67 billion by 2031.

Which segment is expanding the fastest within the website builders market?

Mobile website builders show the quickest trajectory with an 17.43% CAGR forecast for 2026-2031.

How dominant is the cloud deployment model?

Cloud models hold 81.08% share today and continue to widen their lead thanks to SaaS convenience and edge-performance gains.

Why is Asia-Pacific critical for future growth?

High mobile-internet penetration, supportive government digitization programs and a 18.76% forecast CAGR make Asia-Pacific the prime growth engine.

How is artificial intelligence shaping competitive strategy?

Vendors are embedding AI for instant site design, personalization and performance optimization, as seen in Wix’s Base44 acquisition and Webflow’s AI Site Builder release.

Page last updated on: