Web Filtering Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

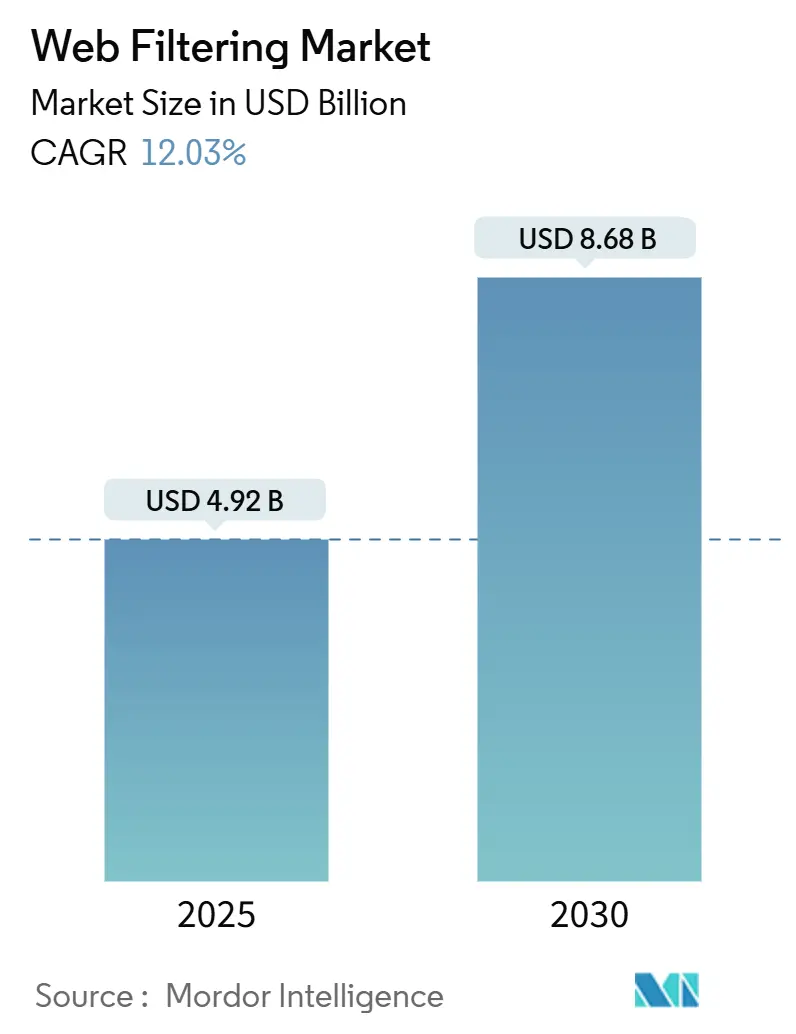

| Market Size (2025) | USD 4.92 Billion |

| Market Size (2030) | USD 8.68 Billion |

| Growth Rate (2025 - 2030) | 12.03% CAGR |

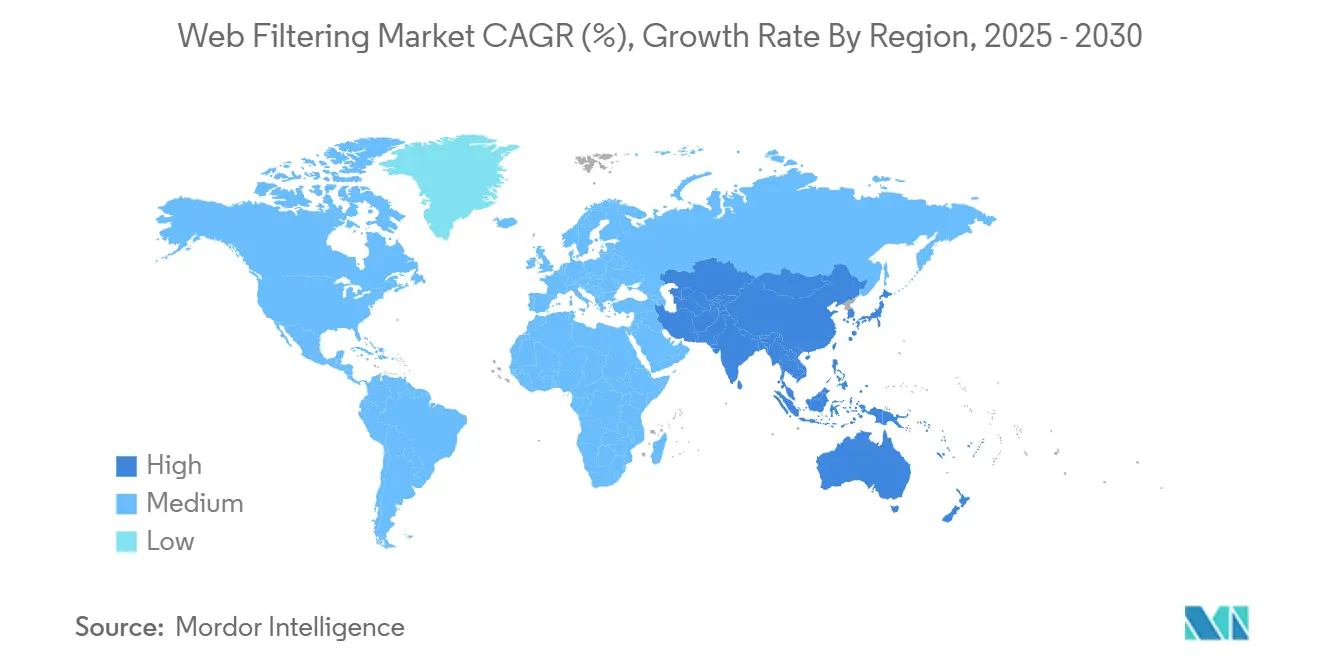

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

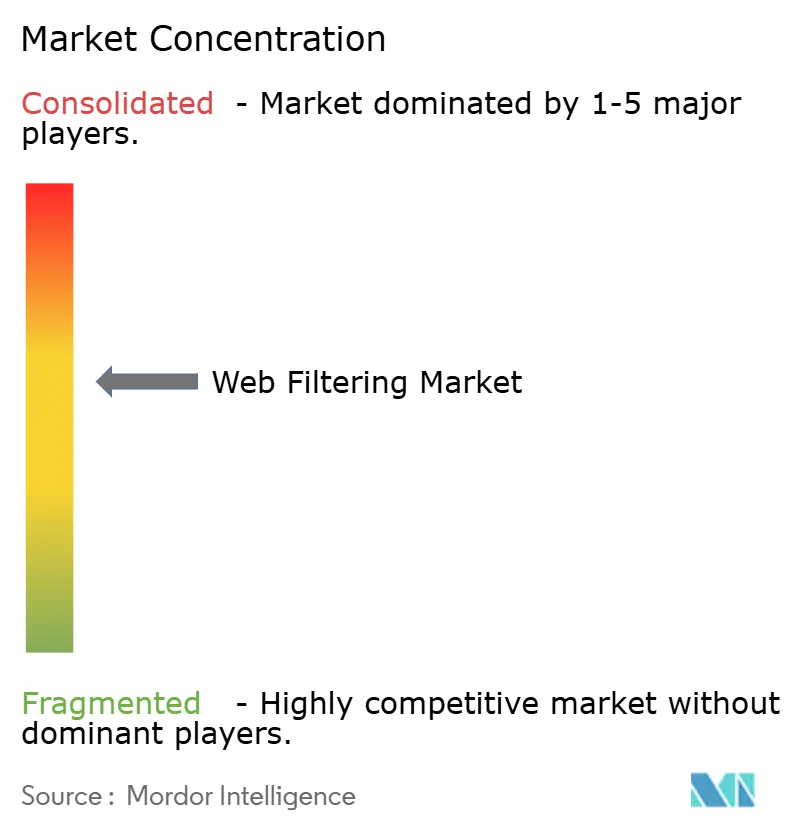

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Web Filtering Market Analysis by Mordor Intelligence

The web filtering market size stood at USD 4.92 billion in 2025 and is on track to reach USD 8.68 billion by 2030 at a 12.0% CAGR, demonstrating how essential advanced filtering has become for modern security stacks. Cloud-native architectures, Secure Access Service Edge (SASE) convergence, and zero-trust mandates are accelerating refresh cycles across enterprises, while AI-powered content inspection improves protection against encrypted threats. Regulatory pressure—from the U.S. Executive Order 14144 to Indonesia’s Regulation 17/2025—is forcing organizations to deploy policy-rich platforms that satisfy complex compliance checks[1]Executive Office of the President, “Executive Order 14144—Strengthening and Promoting Innovation in the Nation’s Cybersecurity,” Federal Register, federalregister.gov. North America remains the largest regional contributor, yet Asia-Pacific delivers the fastest growth amid sweeping data-protection laws and surging cloud adoption. Platform consolidation is changing buying behavior as enterprises favor integrated stacks that fold secure web gateway (SWG), firewall-as-a-service, and zero-trust network access into a single subscription.

Key Report Takeaways

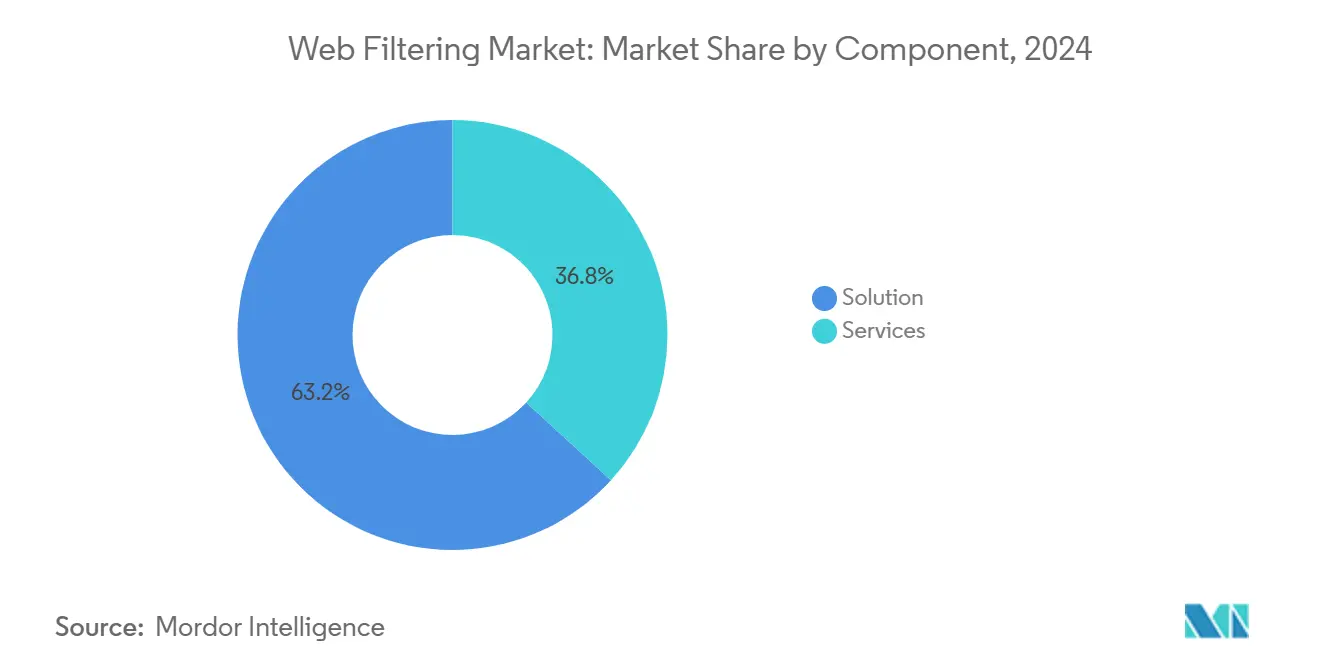

- By component, solutions led with 63.2% of web filtering market share in 2024, while services are forecast to grow at a 14.0% CAGR to 2030.

- By deployment mode, on-premises accounted for 69.5% share of the web filtering market size in 2024; cloud deployment is projected to expand at 14.3% CAGR through 2030.

- By filtering type, URL filtering captured 57.8% revenue share in 2024; keyword filtering is advancing at a 13.5% CAGR between 2025-2030.

- By organization size, large enterprises held 71% share of the web filtering market size in 2024, whereas SMEs record the quickest CAGR at 13.8% to 2030.

- By industry vertical, BFSI commanded 45.7% of the web filtering market share in 2024, yet education is the fastest-growing vertical at 12.5% CAGR through 2030.

- By geography, North America led with 37.3% revenue share in 2024; Asia-Pacific is set to grow at 13.1% CAGR to 2030.

Global Web Filtering Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict government regulations and compliance | +2.1% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Surge in BYOD and hybrid work | +1.8% | Global, led by North America and Asia-Pacific | Short term (≤2 years) |

| Sophisticated web-borne malware | +1.5% | Global | Long term (≥4 years) |

| SASE convergence refreshing SWG cycles | +2.3% | North America and Europe, expanding Asia-Pacific | Medium term (2-4 years) |

| AI-driven real-time content classification | +1.4% | Global, early adoption in developed markets | Long term (≥4 years) |

| Remote Browser Isolation as zero-trust tool | +1.2% | North America and Europe | Medium term (2-4 years) |

Source: Mordor Intelligence

Strict Government Regulations and Compliance Pressure

Governments worldwide are embedding zero-trust and encrypted DNS requirements into law, making compliance a non-negotiable investment driver for the web filtering market. Indonesia now compels operators serving minors to deploy content controls under Regulation 17/2025, pushing demand for pre-packaged policy templates that speed onboarding. In the United States, K-12 schools remain tethered to Children’s Internet Protection Act (CIPA) funding, sustaining steady procurement in education-focused filtering. Data-protection rules such as India’s DPDPA compound the compliance stack, nudging buyers toward consolidated platforms that simplify audits. Because penalties for non-compliance stretch into multimillion-dollar fines, budget holders increasingly allocate growth dollars to proven filtering vendors rather than discretionary IT projects.

Surge in BYOD and Hybrid Work Adoption

The permanent blend of office and remote work makes device-agnostic enforcement a baseline capability for the web filtering market. Zscaler now inspects more than half a trillion daily transactions, underscoring the scale of policy application required when workers connect from anywhere. Cloud-hosted SWGs maintain policy uniformity in branch offices, homes, and public Wi-Fi locations—all while encrypting traffic end-to-end. U.S. federal guidance on encrypted DNS highlights the operational puzzle: retain visibility while respecting privacy. Consequently, enterprises replace perimeter appliances with edge nodes that pull identity, device posture, and threat telemetry into every verdict.

Escalating Sophistication of Web-Borne Malware

Threat actors now automate phishing pages, waterholes, and malvertising through AI, forcing continual signature updates and real-time analysis inside the web filtering market. Cisco’s AI-driven Domain Generation Algorithm defender lifts detection rates by 30% and accuracy by 50%, illustrating vendor escalation in analytic horsepower[2]Cisco Systems Inc., “AI-Powered Detection of Domain Generation Algorithms,” blogs.cisco.com. Encrypted Client Hello further obscures domain metadata, limiting legacy URL filters in education networks. Modern filters pivot to machine-learning classifiers that scrutinize script behavior, page entropy, and user intent within milliseconds. Buyers expect these engines to scale without latency spikes as traffic volumes swell with video streaming and generative-AI usage.

SASE Convergence Accelerating SWG Refresh Cycles

Organizations consolidating SD-WAN, firewall-as-a-service, and zero-trust access under a single cloud fabric present fresh spend for the web filtering market. Fortinet’s Unified SASE annual recurring revenue reached USD 1.15 billion in Q1 2025, proving that integrated stacks entice buyers seeking simpler license bundles. Gartner’s reclassification of SWG under the broader Security Service Edge banner prompted incumbent vendors to unify consoles, policy engines, and billing. This convergence rewards suppliers with elastic global PoPs, predictable performance SLAs, and automated threat feeds that shrink time-to-protection.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-skills deficit for policy tuning | -1.3% | Global, deepest in emerging markets | Medium term (2-4 years) |

| Performance-latency concerns in cloud SWG | -0.9% | Global, acute in real-time trading and media streaming | Short term (≤2 years) |

| Encrypted DNS (DoH) circumvention | -1.1% | Global, divergent regulatory postures | Long term (≥4 years) |

| Vendor consolidation boosting price power | -0.8% | Global, concentrated in mature markets | Medium term (2-4 years) |

Source: Mordor Intelligence

Cyber-Skills Deficit for Complex Policy Tuning

Advanced filtering engines expose hundreds of toggles for machine-learning thresholds, app controls, and shadow-IT discovery, yet few security teams possess the know-how to calibrate them. Talent shortages are starker in emerging economies, where universities lag behind in cybersecurity curricula. Consequently, many buyers lean on managed service providers for 24x7 policy optimization, inflating total cost of ownership and dampening direct license growth. Vendors counter by shipping wizard-driven consoles and AI-recommended policy baselines that shorten ramp-up times. Skills gaps could widen as platforms add context-aware features reliant on identity and behavioral analytics.

Encrypted DNS (DoH) Circumventing Filters

DoH turns DNS lookups into HTTPS traffic, allowing users—or malware—to bypass on-premises resolvers silently. K-12 districts in the United Kingdom reported gaps after browsers enabled DoH by default, prompting new guidance on network-level interception. While privacy gains are undisputed, security teams must re-architect inspection points or deploy native DoH-aware gateways. Such retrofits drive extra capital spend and complicate maintenance for budget-constrained organizations, dampening short-term adoption in latency-sensitive environments.

Segment Analysis

By Component: Services Growth Outpaces Solutions

Services generated a 14.0% CAGR from 2025-2030, outstripping software even though solutions still captured 63.2% revenue in 2024. The web filtering market records mounting demand for professional services that configure AI policy engines, integrate identity feeds, and run threat-hunting playbooks. Vendors like Zscaler support over 8,600 customers with managed offerings that absorb operational burdens[3]Zscaler Inc., “Third Quarter Fiscal 2025 Financial Results,” zscaler.com. Growing complexity, coupled with the cyber-skills gap, cements services as a strategic revenue pillar.

Solutions continue to underwrite the bulk of the web filtering market because large enterprises pre-pay multiyear subscriptions for cloud gateways. Consumption-based billing now blurs lines between software and service, yet license value remains material. Menlo Security’s cloud-native Secure Enterprise Browser packages RBI and zero-trust controls into per-seat fees that mimic SaaS economics. Consequently, services revenues expand without cannibalizing core license flows, keeping total addressable opportunity robust.

By Deployment Mode: Cloud Migration Accelerates

On-prem appliances still held 69.5% of web filtering market size in 2024, reflecting historical capex cycles inside heavily regulated verticals. However, cloud deployment is the fastest-growing segment at 14.3% CAGR. The web filtering market benefits from enterprises peeling back branch boxes in favor of global point-of-presence (PoP) networks that scale elastically during traffic spikes. Cloudflare posted 27% top-line growth to USD 479.1 million in Q1 2025, partly on the back of nine-figure security contracts.

Latency myths are fading as PoP density climbs and vendors introduce smart-routing algorithms that steer sessions along optimal paths. Hybrid models—on-prem policy engines paired with cloud-fed intelligence—bridge migration for cautious buyers. Government agencies trial cloud gateways in sandboxed workloads, spurred by encrypted DNS mandates that demand modern inspection layers.

By Filtering Type: Keyword Filtering Gains Momentum

URL databases delivered 57.8% of 2024 revenue, but keyword filtering is projected to clock 13.5% CAGR, the quickest among all types. As attackers repurpose legitimate domains, keyword engines comb page text, metadata, and scripts to flag policy violations unseen by URL lists. That evolution keeps the web filtering market ahead of encrypted traffic growth because content inspection does not rely on domain visibility alone.

DNS filtering remains indispensable for zero-trust segmentation, supplying coarse blocklists that preempt known bad destinations. Meanwhile, AI-powered behavioral analytics fuse file-type and keyword logic to detect living-off-the-land exploits. Cisco’s DGA model exemplifies such cross-method synergies, yielding 50% higher accuracy. Education customers, juggling safety and academic freedom, now deploy nuanced keyword rules that weight context rather than raw terms.

By Organization Size: SME Adoption Accelerates

Large enterprises controlled 71% of 2024 spending thanks to hefty budgets and multi-layer security blueprints. Yet SMEs exhibit 13.8% CAGR as cloud delivery democratizes enterprise-grade protection. Affordable subscriptions permit small firms to harness the same policy engines processing cabinet-level U.S. agency traffic, shrinking the security maturity gap.

The web filtering market therefore sees volume expansion without trading down average selling prices, because per-user economics remain attractive. SMEs often select bundled SASE suites to sidestep integration chores, driving cross-sell momentum for leading platforms. Challenges persist around vertical-specific compliance, yet marketplaces of ready-made policy templates mitigate resource shortages.

By Industry Vertical: Education Sector Drives Growth

BFSI contributed 45.7% revenue in 2024 as compliance-heavy banks shield sensitive customer data from phishing and malvertising. However, education is the fastest-rising vertical at 12.5% CAGR. Georgia’s Senate Bill 351 obliges K-12 districts to filter social-media content by July 2026, spurring a wave of RFPs for classroom-compatible solutions. The web filtering market thus diversifies beyond corporate walls into public-sector budgets.

Higher-education institutions balance open research access with safeguarding students from malicious AI-generated pages, requiring granular identity-based policies. Suppliers roll out discounted licensing tiers and Chromebook agents engineered for bandwidth-constrained campuses. BFSI and healthcare continue as baseline revenue pillars, but incremental upside flows from government and telecom digital-trust initiatives that embed SWG into broader modernization projects.

Geography Analysis

North America retained 37.3% of global revenue in 2024 owing to mature regulatory mandates, zero-trust adoption, and incumbency of leading vendors. Budget turbulence from U.S. spending caps briefly delayed federal deals, yet Executive Order 14144 has reset urgency by codifying encrypted DNS timelines. Municipal school districts accelerate procurement to meet social-media filtering deadlines, expanding addressable spend.

Europe ranks next as GDPR, the Online Safety Act 2023, and diverse national privacy laws force service providers to deploy sophisticated inspection and data-loss prevention controls. Ofcom’s enforcement program obliges firms to submit illegal-content risk assessments, raising minimum baseline capability for SWG offerings. Digital-sovereignty demands drive interest in EU-hosted PoPs and local threat-intel feeds.

Asia-Pacific is the fastest-growing territory with 13.1% CAGR, propelled by India’s DPDPA, Indonesia’s child-protection regulation, and rapid cloud build-outs among digitally native businesses. Japan and South Korea craft smartphone security bills that will widen compliance scope to app stores, fortifying long-term demand. Fragmented maturity levels create openings for channel partners that bundle training, local language support, and regulatory guidance.

Competitive Landscape

The web filtering market remains moderately fragmented. Zscaler, Palo Alto Networks, and Cloudflare extend platform breadth through AI-driven modules and global PoP expansion. Zscaler processed 0.5 trillion daily transactions and posted USD 678 million Q3 2025 revenue, reflecting scale advantages that feed its threat-intel algorithms[4]Zscaler Inc., “Third Quarter Fiscal 2025 Financial Results,” zscaler.com. Palo Alto Networks eyes USD 15 billion annual recurring revenue by 2030 via unified Next-Generation Security bundles that knit SWG, SD-WAN, and autonomous SOC features.

Strategic mergers and acquisitions reshape competitive positioning. Google closed the USD 32 billion Wiz acquisition in March 2025, injecting cloud-security DNA into Google Cloud services. Fortinet followed with Lacework, boosting workload-visibility and runtime threat detection inside its Unified SASE line. Check Point added Perimeter 81 for secure access as incumbents chase platform breadth.

Technology differentiation hinges on machine-learning fidelity, latency optimization, and breadth of compliance toolkits. Cisco’s AI-powered DGA module and Menlo Security’s Secure Enterprise Browser exemplify innovation paths meant to reduce false positives and contain zero-days at the browser layer. Education-centric vendors such as Securly capture niche share through purpose-built dashboards, while telecom operators white-label large-vendor stacks to upsell security over fiber and 5G footprints. Consolidation pressure may lift average selling prices, yet customer churn stays low once PoP footprint and policy libraries are embedded.

Web Filtering Industry Leaders

-

Broadcom Corporation

-

Cisco Systems, Inc.

-

Palo Alto Networks, Inc.

-

McAfee, Inc.

-

Fortinet, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Zscaler appointed Kevin Rubin as CFO to steer financial operations amid 23% revenue expansion.

- May 2025: Fortinet finalized the Lacework acquisition, integrating AI cloud-security analytics into its Unified SASE platform.

- April 2025: Palo Alto Networks confirmed talks to buy Protect AI for USD 650-700 million to deepen AI threat-protection stack.

- March 2025: Google completed the USD 32 billion purchase of Wiz, the largest cybersecurity deal on record.

Global Web Filtering Market Report Scope

Web filtering is also recognized as content-control software. It is a specific type of program created to screen an incoming web page and decide whether some or all should have access. With the aid of this, accurate and valid authentication of any webpages can be achieved. It stops the origin or content of any web page against a set of practices provided by a company or a person who has installed the web filter.

| By Component | Solution | |||

| Services | ||||

| By Deployment Mode | On-premises | |||

| Cloud | ||||

| By Filtering Type | DNS Filtering | |||

| Keyword Filtering | ||||

| URL Filtering | ||||

| File-type and Other Filtering | ||||

| By Organisation Size | Large Enterprises | |||

| Small and Medium Enterprises (SMEs) | ||||

| By Industry Vertical | BFSI | |||

| IT and Telecom | ||||

| Government | ||||

| Education | ||||

| Other Industry Verticals | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| Australia and New Zealand | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| United Arab Emirates | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Rest of Africa | ||||

| Solution |

| Services |

| On-premises |

| Cloud |

| DNS Filtering |

| Keyword Filtering |

| URL Filtering |

| File-type and Other Filtering |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| IT and Telecom |

| Government |

| Education |

| Other Industry Verticals |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the web filtering market?

The web filtering market size reached USD 4.92 billion in 2025 and is projected to hit USD 8.68 billion by 2030 at a 12.0% CAGR.

Which component is expanding the quickest?

Services are the fastest-growing component, posting a 14.0% CAGR as enterprises seek managed expertise to configure complex AI-driven filters.

Why is Asia-Pacific the fastest-growing region?

New privacy statutes such as India’s DPDPA and Indonesia’s Regulation 17/2025, paired with rapid cloud adoption, fuel a 13.1% CAGR in Asia-Pacific.

How are encrypted DNS protocols affecting filtering strategies?

DNS-over-HTTPS can bypass legacy resolvers, so organizations are adopting DoH-aware gateways and identity-centric policy engines to retain visibility.

What role does SASE play in purchasing decisions?

Buyers increasingly bundle secure web gateways into broader SASE contracts, simplifying licensing and ensuring consistent zero-trust enforcement across users and locations.

Which industry vertical is growing fastest?

Education leads with a 12.5% CAGR due to new mandates such as Georgia’s SB 351 requiring comprehensive social-media filtering in K-12 schools.