Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

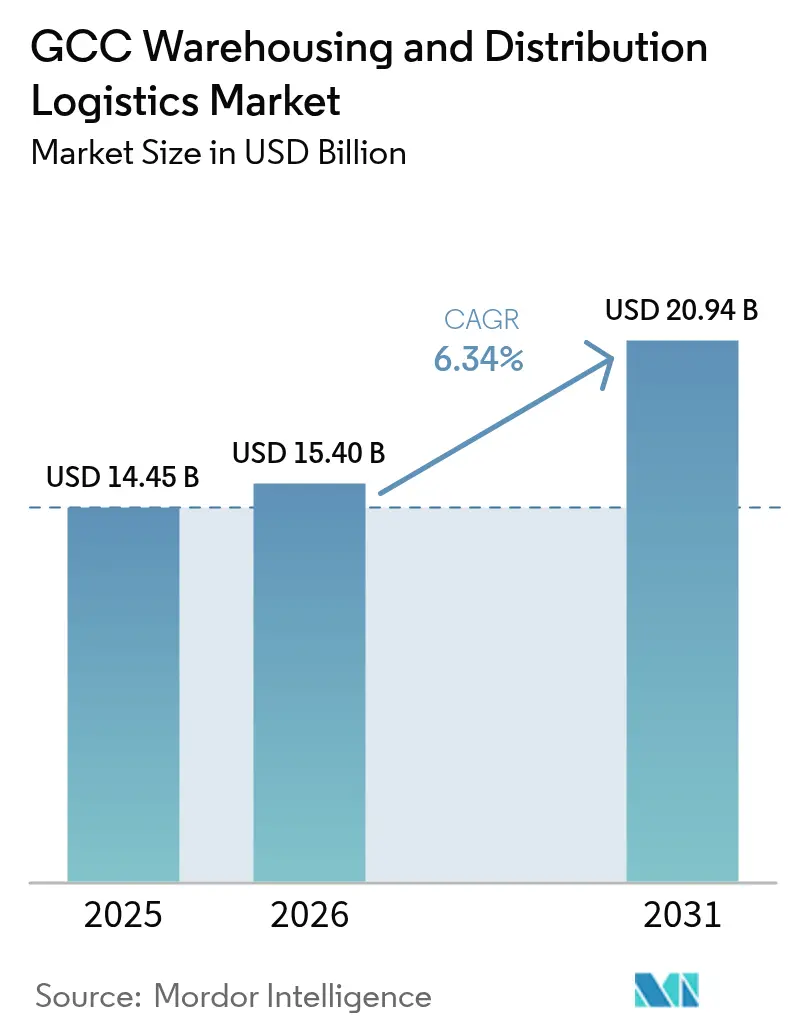

| Base Year Market Size (2025) | USD 14.45 Billion |

| Market Size (2026) | USD 15.40 Billion |

| Market Size (2031) | USD 20.94 Billion |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

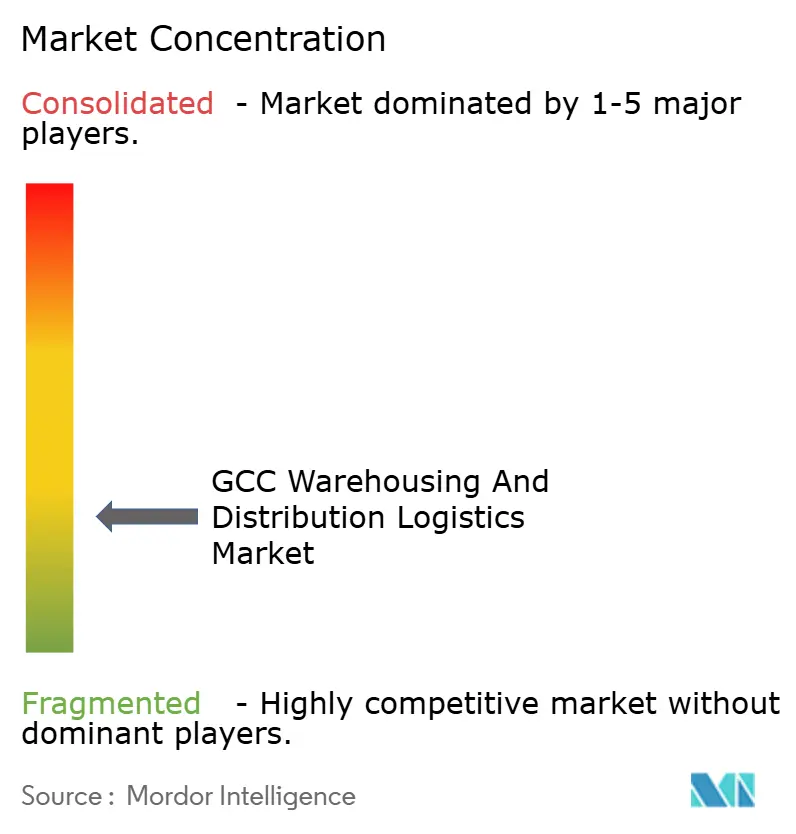

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Warehousing And Distribution Logistics Market Analysis by Mordor Intelligence

The GCC warehousing and distribution logistics market size is expected to grow from USD 14.45 billion in 2025 to USD 15.40 billion in 2026 and is forecast to reach USD 20.94 billion by 2031 at a 6.34% CAGR over 2026-2031.

A recalibration of regional supply chains is underway as 1,200-kilometer rail corridors such as Etihad Rail’s Stage Three create inland distribution nodes that relieve port congestion and cut door-to-door costs by up to 40%. Accelerating 3PL outsourcing among fast-moving consumer goods brands lifts contract logistics spending, while rising e-commerce volumes push operators toward micro-fulfillment hubs nested inside metropolitan areas. Cost headwinds from fuel-subsidy reforms and nationalization quotas spur warehouse automation, with early adopters achieving 35-40% savings per parcel handled. Preferential trade agreements that eliminate tariffs on up to 95% of goods cement the United Arab Emirates as a bonded re-export hub offering value-added kitting, labeling, and light assembly.

Key Report Takeaways

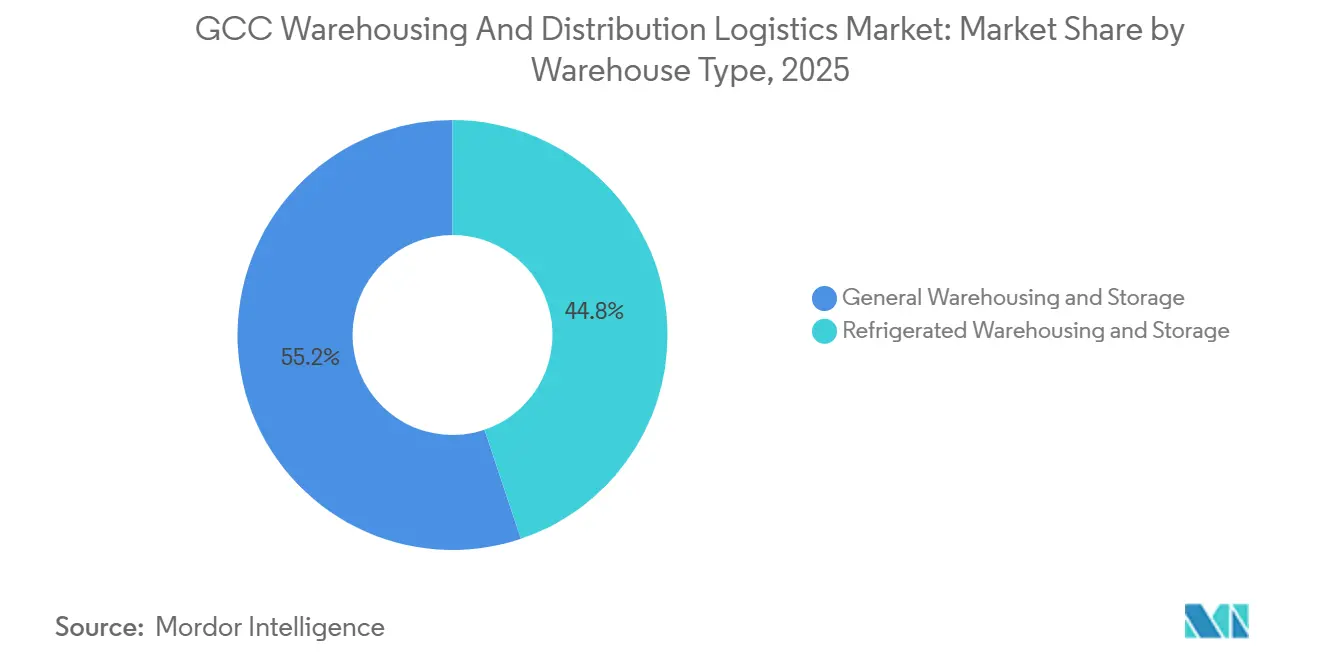

- By warehouse, general warehousing and storage captured 55.17% of the GCC warehousing and distribution logistics market share in 2025, while refrigerated warehousing and storage is projected to expand at a 6.81% CAGR through 2031.

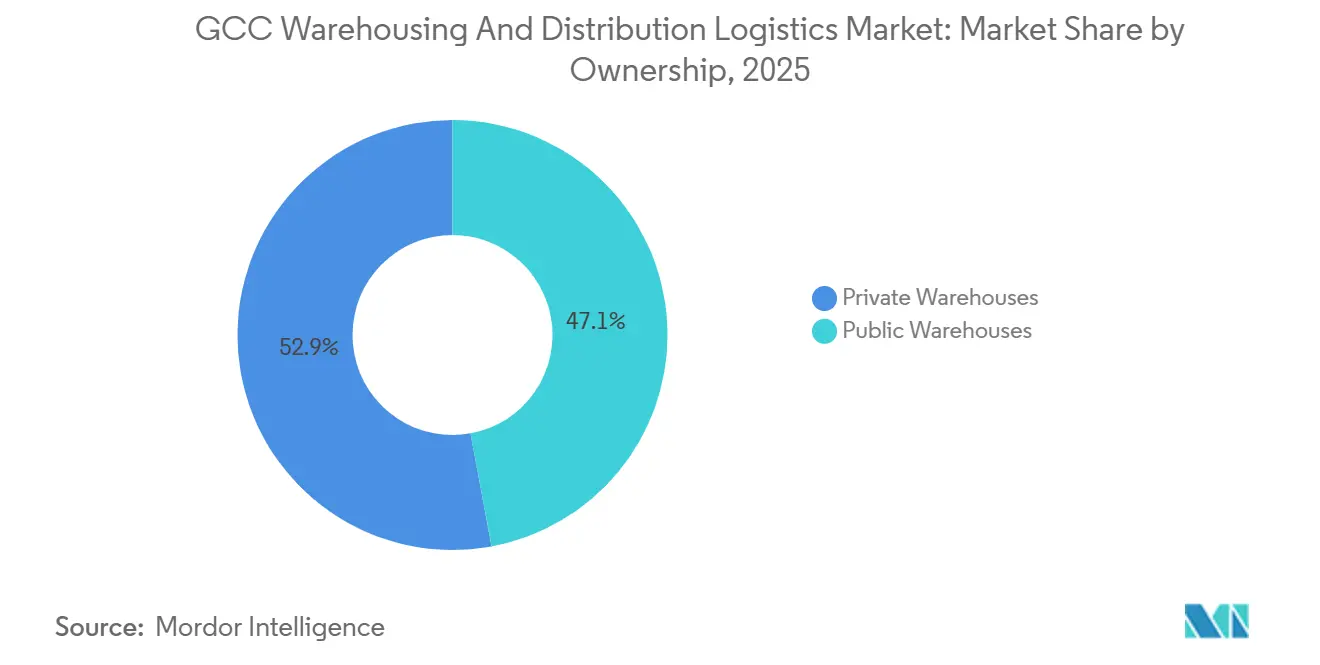

- By ownership, private warehouses held a 52.90% share of the GCC warehousing and distribution logistics market size in 2025, whereas public warehouses recorded the highest projected CAGR at 6.75% to 2031.

- By end-user industry, e-commerce and retail accounted for a 27.22% share of the GCC warehousing and distribution logistics market size in 2025, but the pharma and healthcare segment is advancing at a 9.40% CAGR through 2031.

- By country, Saudi Arabia led with 40.25% revenue share in 2025, while the United Arab Emirates is forecast to expand at an 8.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Warehousing And Distribution Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multimodal rail and land-bridge investments are accelerating inland DC demand | +1.4% | Saudi Arabia, UAE, Oman rail corridors | Long term (≥ 4 years) |

| Growing 3PL outsourcing by the FMCG and retail sectors | +1.2% | GCC-wide, concentrated in the UAE and Saudi Arabia | Medium term (2-4 years) |

| Emerging preferential trade agreements are boosting re-export flows | +1.0% | UAE primary, spillover to Bahrain and Oman | Medium term (2-4 years) |

| Warehouse automation and robotics are lowering unit handling costs | +0.9% | Urban centers in the UAE, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| Urban micro-fulfillment (“dark stores”) is proliferating same-hour delivery | +0.8% | Metropolitan areas across the GCC | Short term (≤ 2 years) |

| Reverse-logistics hubs driven by circular-economy mandates | +0.6% | UAE and Saudi Arabia sustainability zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Multimodal Rail and Land-Bridge Investments Accelerating Inland DC Demand

Extending rail infrastructure is redefining warehouse location economics by funneling containers to inland dry ports that clear customs and distribute to regional markets at materially lower costs. Etihad Rail’s Stage Three opens a 1,200-kilometer spine that links Abu Dhabi, Dubai, Fujairah, and the Saudi border. Logistics operators leverage the corridor to consolidate inventory and cut truck kilometers, avoiding driver shortages and elevated diesel prices. Saudi Arabia’s North-South Railway and the planned GCC Railway echo the same logic, drawing investment toward distribution campuses at rail interchanges. Larger warehouses with direct rail siding secure faster turnarounds and support value-added activities that previously clustered at congested seaports.

Growing 3PL Outsourcing by the FMCG and Retail Sectors

Manufacturers and retailers accelerate the hand-off of warehousing and transportation to third-party specialists as omnichannel complexity outstrips in-house capabilities. Shared infrastructure allows mid-sized brands to tap Grade A premises, standardized WMS platforms, and labor pools without heavy capital outlays. Unilever and Procter and Gamble cut regional warehouse footprints by 30% after pivoting to managed networks run by DHL Supply Chain and Agility. Contract terms increasingly bundle automation clauses, enabling 3PLs to amortize robotics across multiple accounts while still delivering custom dashboards. The shift is most pronounced in Saudi Arabia and the UAE, where retail chains juggle store replenishment, e-commerce fulfillment, and dark-store stocking under one inventory pool[1].Reuters, “Warehouse Automation in Middle East Accelerates,” reuters.com

Emerging Preferential Trade Agreements Boosting Re-Export Flows

Comprehensive Economic Partnership Agreements signed by the UAE with India, Indonesia, Turkey, and South Korea strip tariffs on up to 95% of goods. The result is a re-export model where consignments land duty-free, are re-packed or lightly assembled inside bonded warehouses, and exit to African or European destinations with savings that outstrip inland freight costs. Demand therefore spikes for customs-suspended storage close to Jebel Ali Port and Al Maktoum Airport, favoring operators that can offer multi-temperature chambers and rapid cargo turnaround. Bahrain and Oman capture spillover flows by positioning free zones as overflow capacity during Dubai peaks.

Warehouse Automation and Robotics Lowering Unit Handling Costs

Labor quotas raise baseline wages by 30-50%, making automated storage and retrieval systems (ASRS) attractive despite initial capex. Facilities equipped with autonomous mobile robots register 99.9% inventory accuracy and cut picker travel by 60%. Payback periods fall below five years as volume density rises, and energy-efficient motors reduce utility bills, which are index-linked to diesel in several GCC states. Flagship deployments by Aramex and Agility in Riyadh and Dubai set new throughput benchmarks that smaller rivals struggle to equal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationalization, labor quotas, and raising logistics wage bills | −1.1% | Saudi Arabia and the UAE are primary | Short term (≤ 2 years) |

| Diesel subsidy rollbacks are inflating road-freight costs | −0.9% | GCC-wide, acute in Saudi Arabia | Short term (≤ 2 years) |

| Fragmented dangerous-goods handling codes are slowing DG license approvals | −0.5% | Cross-border operations between GCC states | Medium term (2-4 years) |

| Limited insurance capacity for high-value cold-chain stock | −0.4% | Pharmaceutical and biotech corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nationalization, Labor Quotas, Raising Logistics Wage Bills

Saudization and Emiratization programs obligate private‐sector companies to employ rising percentages of nationals, immediately lifting payroll outlays in warehouse and transport roles where expatriates once dominated at lower wages. Saudi Arabia’s Nitaqat framework now requires 15-30% citizen representation in logistics, and non-compliance risks visa suspensions and exclusion from government contracts, compelling operators to add wage premiums and benefit packages to attract local talent. In the United Arab Emirates, firms must increase Emirati headcount by 2 percentage points each year through 2026 and pay minimum monthly salaries of AED 12,000 (USD 3,270), roughly double the typical expatriate warehouse rate. Higher labor costs squeeze already thin warehousing margins, especially for temperature-controlled facilities that require 24/7 staffing and accelerate the shift toward automated storage, voice-directed picking, and autonomous mobile robots that reduce head-count requirements. Companies also reconfigure labor mixes by assigning nationals to supervisory or administrative posts while outsourcing manual tasks to 3PLs operating in free zones where quotas are less stringent. The net effect is a short-term margin compression followed by a capital-intensive pivot toward technology that permanently lowers the labor share of operating expenses.

Diesel Subsidy Rollbacks Inflating Road-Freight Costs

GCC governments have been phasing out diesel subsidies since 2020, pegging domestic pump prices to international oil benchmarks and causing diesel to rise by 40-60% across the region by 2024. Logistics operators depend heavily on road transport for first-mile and last-mile legs, so higher fuel bills translate into a 12-15% jump in overall distribution costs, with refrigerated trucks hit hardest because they consume up to 30% more fuel than ambient vehicles. Passing surcharges to shippers is feasible when capacity is tight, but competitive lanes often force carriers to absorb part of the increase, squeezing EBITDA margins. Fleet managers are responding with route-optimization software, higher trailer fill rates, and trials of compressed natural gas or electric vans for urban deliveries, though infrastructure for alternative fuels remains nascent. Warehouse location strategy is also shifting: developers favor plots closer to consumption centers to shorten delivery radii and cut diesel exposure. Over the medium term, sustained high fuel prices make rail and coastal shipping more attractive for long-haul moves, hastening multimodal investments across the peninsula[2].Saudi Ministry of Human Resources and Social Development, “Nitaqat Program,” hrsd.gov.sa

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Ambient Dominance Masks Cold-Chain Velocity

General warehousing and storage retained 55.17% of the GCC warehousing and distribution logistics market share in 2025, reflecting entrenched demand for bulk ambient space from consumer goods and industrial cargoes. Unit storage rates remain below USD 8 per pallet-month, a cost profile that underpins supermarket and DIY supply chains. However, the refrigerated sub-segment is on track for a 6.81% CAGR to 2031, lifting its share of the GCC warehousing and distribution logistics market size as pharmaceutical firms, fresh-food importers, and specialty chemical distributors race to lock guaranteed capacity.

The cold-chain premium USD 25-35 per pallet-month stems from twin-compressor chillers, backup generators, and Good Distribution Practice validation that guard against temperature excursions capable of wiping millions off a single load. Scarcity is compounded by limited insurance capacity for high-value biologics, giving incumbents strong pricing power. Ambient developers, by contrast, battle double-digit vacancy in secondary zones built during 2020-2023’s speculative surge.

By Ownership: Private Control Persists Despite Capital Intensity

Private facilities represented 52.90% of the GCC warehousing and distribution logistics market share in 2025, underscoring a regional preference for inventory oversight and bespoke racking or automation layouts. Corporates in oil, petrochemicals, and FMCG often treat warehouses as strategic nodes that justify capex in exchange for full process transparency[3].CBRE Middle East, “Industrial & Logistics Market Report 2024,” cbre.com

Yet the public warehouse model is advancing at a 6.75% CAGR, fueled by retailers, quick-commerce platforms, and overseas SMEs that value operational flexibility over bricks-and-mortar control, JLL. Major 3PLs achieve 90-95% utilization via multi-tenant layouts that squeeze fixed costs per square meter and accelerate ROI. Hybrid strategies surface, pairing an owned mega-hub for slow movers with leased satellites closer to consumers for same-day delivery peaks.

By End-User Industry: Healthcare Velocity Reshapes Sector Priorities

E-commerce and retail held a 27.22% share of the GCC warehousing and distribution logistics market size in 2025 as online shopping surged. Still, pharma and healthcare logistics are sprinting ahead with a 9.40% CAGR, buoyed by government procurement of specialty medicines, halal drug exports, and medical-tourism inflows to tertiary hospitals in Dubai and Riyadh.

Healthcare consignments require GDP-certified storage, real-time validation, and temperature mapping to safeguard high-value biologics. Quick-commerce forces retail warehouses to morph into micro-fulfillment nodes inside city cores, shortening line-haul legs but multiplying last-mile touchpoints. Automotive inventory inches downward as electric drivetrains slash SKU counts versus internal-combustion engines. Manufacturing, engineering goods, and renewables benefit from megaprojects such as NEOM and Duqm that reshore value chains and widen the warehousing catchment.

Geography Analysis

Saudi Arabia accounted for 40.25% of the GCC warehousing and distribution logistics market revenue in 2025, leveraging its 36-million population and expansive retail footprint. Inland rail nodes at Riyadh Second Industrial City and King Abdullah Economic City attract multi-client distribution centers that cut reliance on Red Sea ports. The National Industrial Development and Logistics Program has 21 zones operational and 18 under construction, promising a lattice of 75 hubs by 2030. Saudization quotas of 15-30% raise payrolls, pushing operators toward autonomous reach-trucks and cross-belt sorters to curb headcount.

The United Arab Emirates is the velocity leader, with an 8.31% CAGR, propelling the GCC warehousing and distribution logistics market from 2026-2031. Jebel Ali Free Zone hosts 22.4 million TEU of quay capacity plus over 2 million square meters of grade-controlled warehousing. Abu Dhabi’s Khalifa Industrial Zone offers 50 million square meters of modular plots linked to a deepwater port and fast-track customs. Same-hour grocery platforms like Talabat and Deliveroo seed hundreds of micro-sites inside Dubai and Abu Dhabi, supported by Emiratization mandates that escalate local hiring targets by 2% annually.

Qatar, Kuwait, Oman, and Bahrain together held a significant market share, each carving discrete niches. Oman’s Salalah Port offers 200 weekly services to 86 global nodes, feeding transit volumes into Duqm’s 2,000-hectare logistics zone. Bahrain’s causeway delivers next-day truck access to Saudi Arabia’s Eastern Province, while its Bahrain Logistics Zone touts rapid license issuance. Kuwait concentrates on spare-parts depots for upstream energy services, whereas Qatar supports LNG spares, event catering, and growing tourist consumption. Unified GCC customs codes effective January 2025 simplify clearance across borders, but varied VAT regimes and local-content rules maintain operational complexity[4]Saudi Ports Authority, “Annual Statistics,” ports.gov.sa .

Competitive Landscape

Roughly 15-20 operators control 60-65% of GCC warehousing and distribution logistics market turnover, indicating low concentration. Outsized operators double down on warehouse management systems, blockchain traceability, and predictive analytics that smaller rivals cannot match financially.

Automation is the battlefield. DHL and Saudi Aramco’s ASMO venture integrates AI route planning with IoT sensors, cutting unplanned downtime by 25%. Agility opened a USD 150 million ASRS-equipped campus in Riyadh that processes 60,000 cases per hour at 99.9% accuracy. Kuehne + Nagel’s e-commerce site in Jeddah handles 50,000 orders daily for Western-Region same-day delivery.

Niche entrants hunt for white-space opportunities. Bahri Logistics debuts temperature-controlled capacity in Jeddah aimed at biologics importers. Digital freight platforms such as TruKKer aggregate under-utilized trucks and warehouse slots to serve spot-market demand. Dangerous-goods handling remains fragmented because licensing rules differ by emirate and kingdom, discouraging pan-GCC coverage. Insurance underwriters impose strict cargo-value ceilings for pharmaceutical stock, limiting new entrants without deep capital reserves.

GCC Warehousing And Distribution Logistics Industry Leaders

DHL Group

GWC

Aramex

DSV

Al-Majdouie Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: DHL Supply Chain committed EUR 120 million ( USD 138.70 million) to develop a 55,000 m² multi-user warehouse and contract logistics hub in Dubai South under a 38-year lease agreement, strengthening regional distribution networks near Al Maktoum International Airport.

- November 2025: DHL Supply Chain signed a strategic land lease agreement with the Special Integrated Logistics Zone (SILZ) in Riyadh to build a EUR 130 million (USD 150.25 million) regional logistics and distribution hub with 53,000 m² of multi-user warehouse space.

- April 2025: GWC partnered with Yellow Door Energy to deploy the GCC’s largest private solar energy project across Logistics Village Qatar, Bu Sulba Warehousing Park, and Al Wukair Logistics Park, improving sustainability across logistics and warehouse facilities.

- February 2025: GWC launched a new logistics hub in Ras Laffan, Qatar, including air-conditioned bulk storage warehouses and a distribution center designed to support the energy sector and large industrial supply chains in the GCC.

GCC Warehousing And Distribution Logistics Market Report Scope

By Warehouse Type

| General Warehousing and Storage |

| Refrigerated Warehousing and Storage |

By Ownership

| Private Warehouses |

| Public Warehouses |

By End-User Industry

| E-commerce & Retail |

| Food & Beverage |

| Pharma & Healthcare |

| Automotive |

| Manufacturing & Engineering Goods |

| Others |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Warehouse Type | General Warehousing and Storage |

| Refrigerated Warehousing and Storage | |

| By Ownership | Private Warehouses |

| Public Warehouses | |

| By End-User Industry | E-commerce & Retail |

| Food & Beverage | |

| Pharma & Healthcare | |

| Automotive | |

| Manufacturing & Engineering Goods | |

| Others | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

What is the projected value of GCC warehousing and distribution logistics by 2031?

The GCC warehousing and distribution logistics market size is forecast to reach USD 20.94 billion by 2031

Which segment is growing fastest within GCC logistics facilities?

Pharma and healthcare warehousing leads with a 9.4% CAGR as temperature-controlled demand escalates.

Why is the UAE outpacing the region in growth?

Comprehensive Economic Partnership Agreements and bonded re-export models drive an 8.31% CAGR for the UAE.

How are fuel cost increases affecting logistics operators?

Diesel subsidy rollbacks have lifted road-freight costs by up to 12%, accelerating investment in route optimization and alternative fuels.

What technologies are most widely adopted in GCC warehouses?

Autonomous mobile robots, ASRS, and AI-driven warehouse management systems dominate recent upgrades to trim labor and improve accuracy.

Which end-user vertical is growing fastest in warehouse space usage?

Pharma and healthcare leads with a 9.4% CAGR, driven by halal biologics exports and GDP-certified cold-chain requirements.

Page last updated on: