Wafer Biscuits Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

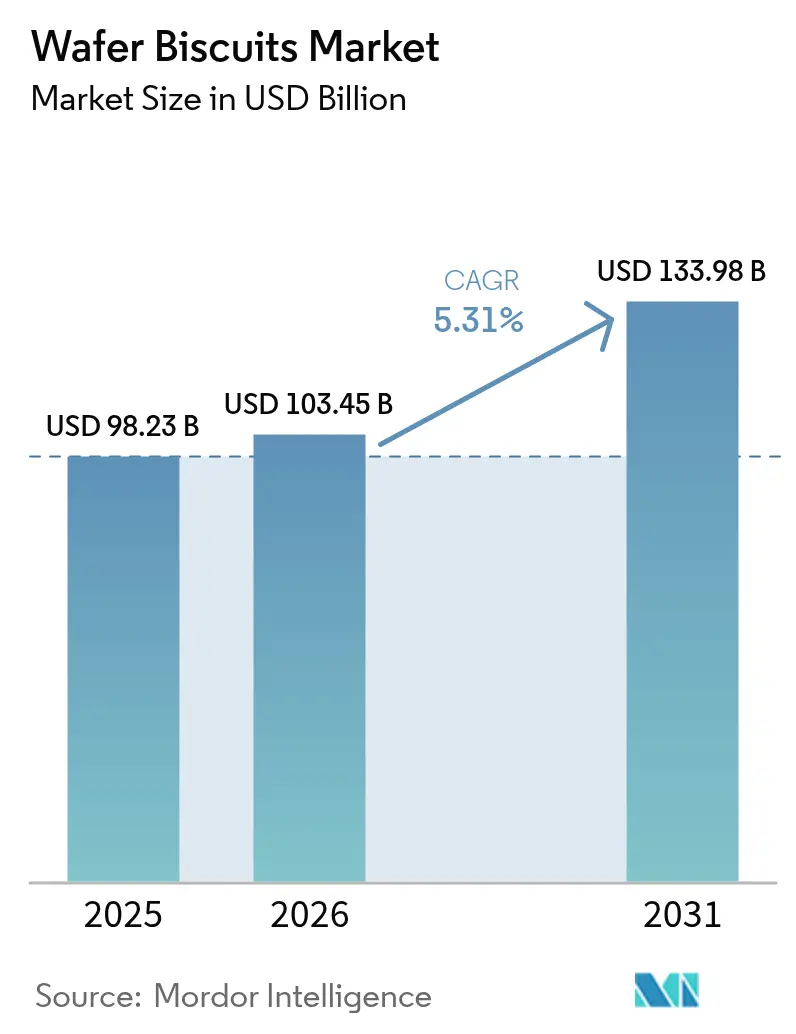

| Market Size (2026) | USD 103.45 Billion |

| Market Size (2031) | USD 133.98 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

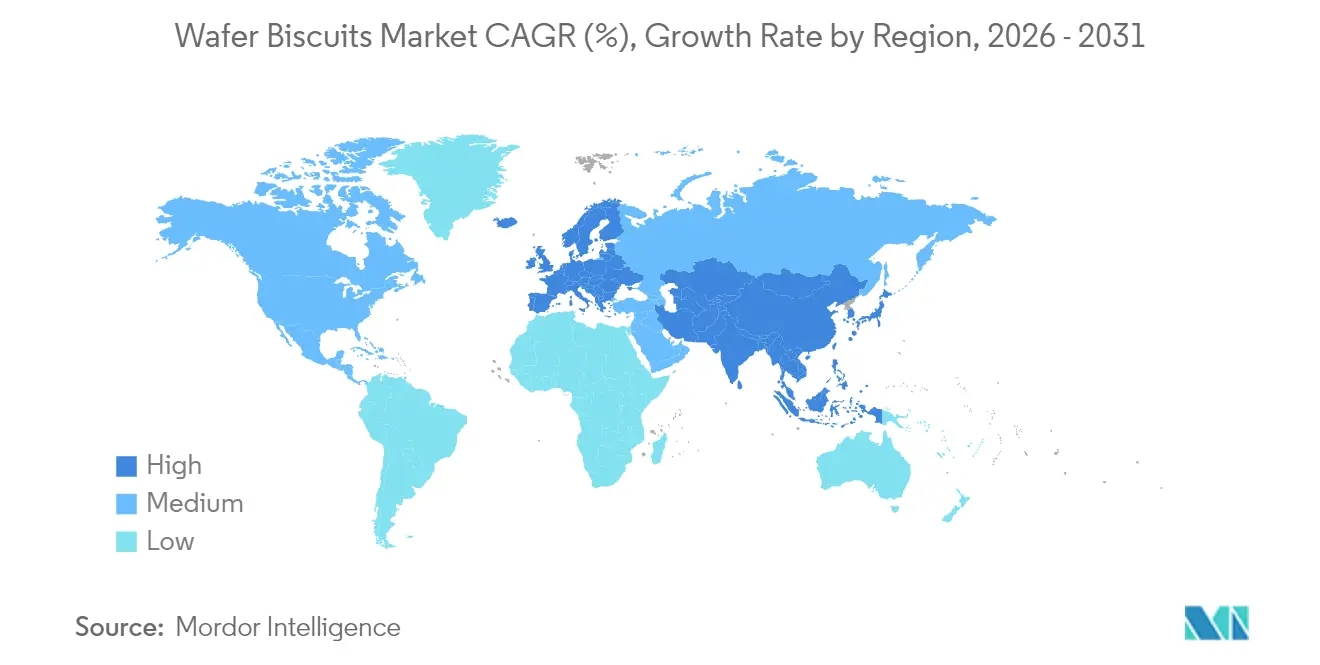

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Wafer Biscuits Market Analysis by Mordor Intelligence

Wafer Biscuits Market size in 2026 is estimated at USD 103.45 billion, growing from 2025 value of USD 98.23 billion with 2031 projections showing USD 133.98 billion, growing at 5.31% CAGR over 2026-2031. This growth trajectory reflects the sector's resilience amid evolving consumer preferences and supply chain pressures that have reshaped the confectionery landscape. The market's expansion is underpinned by fundamental shifts in snacking behavior, with 48.8% of consumers now snacking more than 3 times daily, driving sustained demand for convenient, portable formats [1]Source: The National Association of Convenience Stores (NACS), "Sweets & Snacks Expo 2025: The State of Snacking", convenience.org. The market benefits from continuous product innovation, with companies introducing new flavors, multi-layered wafer formats, and health-oriented options such as low-sugar, gluten-free, and high-protein wafers that attract a broad consumer base including health-conscious buyers. Moreover, the popularity of cream-filled and chocolate-coated wafers, which account for a significant share of sales, reflects consumers’ growing preference for rich, flavorful snacks. Regional growth is particularly strong in Asia-Pacific due to population density and increasing disposable income, alongside mature markets in Europe with demand for artisanal and organic products. Simultaneously, regulatory compliance burdens intensify as food safety standards evolve globally, requiring manufacturers to navigate complex labeling requirements across multiple jurisdictions. However, these challenges are offset by robust demand drivers including packaging innovations that extend shelf life, expanding e-commerce penetration, and the proliferation of health-oriented formulations targeting protein-conscious and reduced-sugar consumer segments.

Key Report Takeaways

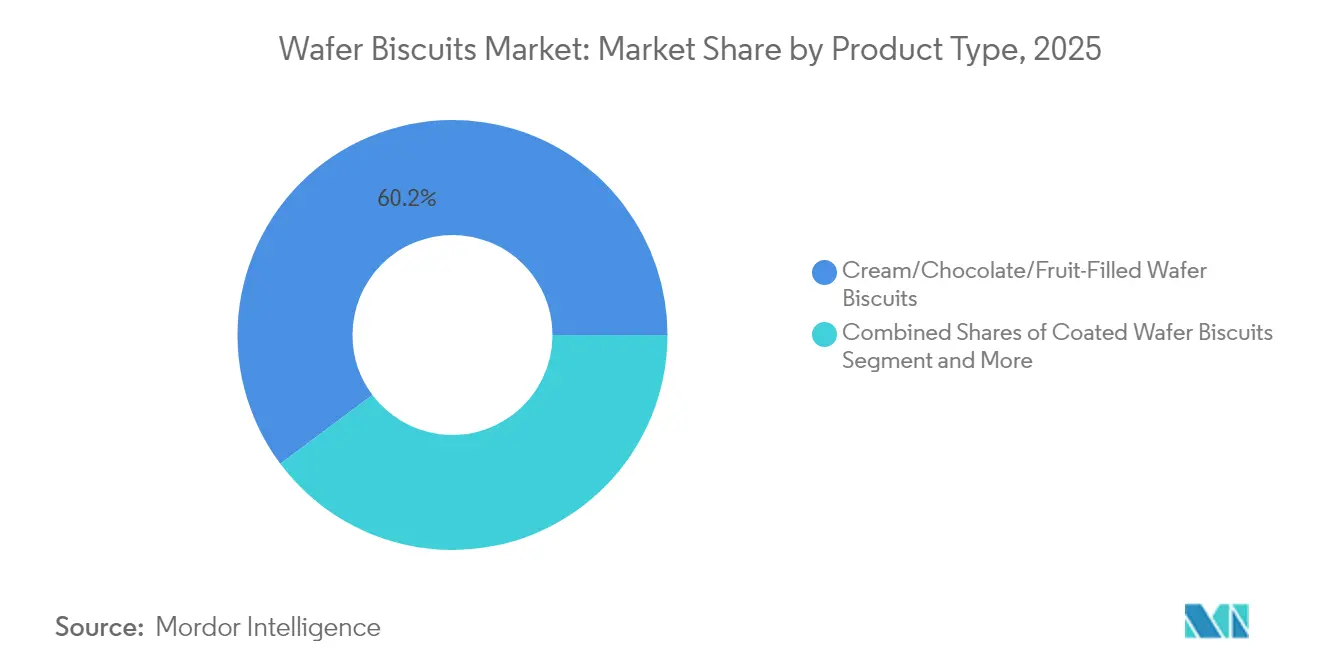

- By product type, cream/chocolate/fruit-filled lines led with 60.22% wafer biscuits market share in 2025, coated formats are projected to grow at a 5.58% CAGR to 2031.

- By category, conventional products accounted for 95.41% of sales in 2025; organic variants post the fastest 6.54% CAGR through 2031.

- By form, brick shapes held 92.10% of the wafer biscuits market size in 2025, whereas stick shapes expand at a 7.02% CAGR to 2031.

- By packaging, boxes captured 39.81% of 2025 revenue; stand-up pouches show a 7.05% CAGR through 2031.

- By distribution, supermarkets/hypermarkets generated 57.25% of value in 2025, while online retail rises at a 6.18% CAGR to 2031.

- By geography, Europe occupies 32.74% of value in 2025, while Asia-Pacific has the fastest growing share at a 6.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wafer Biscuits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenient, On-the-Go Snacking Demand | +1.2% | Global | Medium term (2-4 years) |

| Advances in Packaging for Freshness and Appeal | +0.8% | North America and Europe | Short term (≤ 2 years) |

| Product Innovation and Expanding Flavor Varieties | +0.9% | Global | Medium term (2-4 years) |

| Health-Oriented Options | +1.1% | North America and Europe, APAC (Asia-Pacific) emerging | Long term (≥ 4 years) |

| Brand Differentiation and Marketing Initiatives | +0.7% | Global | Short term (≤ 2 years) |

| Expansion of Modern Retail and E-commerce | +1.0% | Asia-Pacific core, spill-over to Middle-East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Convenient, On-the-Go Snacking Demand

Consumer snacking patterns have fundamentally shifted toward frequent, portable consumption occasions, with nearly half of consumers now snacking more than 3 times daily according to industry data. This behavioral transformation extends beyond traditional meal replacement, encompassing energy management throughout extended work days and social consumption moments. Wafer biscuits' inherent portability and extended shelf stability position them advantageously within this trend, particularly as urbanization accelerates across emerging markets. The "snackification" of meals has become especially pronounced among Gen Z and Millennial demographics, who prioritize convenience without compromising taste satisfaction. Premium positioning within this segment has proven sustainable, with 68.8% of consumers expressing willingness to pay elevated prices for perceived quality improvements. This willingness to trade up creates margin expansion opportunities for manufacturers who successfully communicate value propositions through packaging design and flavor innovation.

Advances in Packaging for Freshness and Appeal

Packaging technology evolution has emerged as a critical competitive differentiator, with active packaging systems incorporating antioxidant and antimicrobial agents extending product shelf life while maintaining sensory attributes. Smart packaging integration enables real-time quality monitoring, addressing consumer concerns about freshness while reducing waste throughout distribution channels. Edible coating technologies represent an emerging frontier, offering sustainable alternatives to traditional barrier materials while potentially enhancing nutritional profiles. Plant-based packaging materials are gaining traction as environmental consciousness influences purchasing decisions, though technical challenges around moisture barrier properties require continued innovation investment. The convergence of sustainability demands, and functional performance creates opportunities for manufacturers who successfully balance environmental credentials with product protection requirements. Stand-up pouches demonstrate the fastest growth at 7.32% CAGR, reflecting consumer preference for resealable formats that maintain product integrity across multiple consumption occasions.

Product Innovation and Expanding Flavor Varieties

Flavor experimentation has intensified as manufacturers seek new occasions and demographics. The National Confectioners Association’s 2025 State of Treating survey shows 63% of U.S. shoppers enjoy trying confectionery items with novel flavors, and 48% purchase at least one limited-edition seasonal SKU each year[2]Source: National Confectioners Association, "STATE OF TREATING 2025", candyusa.com. Rising demand for regional authenticity pushes brands to localize: a recent USDA Foreign Agricultural Service report notes that Chinese biscuit launches featuring matcha, red-bean, and lychee grew 22% year on year in 2024 [3]Source: USDA Foreign Agricultural Service, "Chinese biscuit launches", fas.usda.gov. Texture layering also drives premium perception; the International Cocoa Organization links coated formats to a 3% lift in average unit price because enrobing adds perceived indulgence. Rapid prototyping supported by modular filling equipment lets plants shift to new fillings in under 30 minutes, cutting the development cycle from weeks to days, according to the European Snacks Association 2025 processing benchmark. Social-media campaigns amplify these launches, with the NCA reporting that confectionery posts tagged #newflavor generated 1.4 billion views on TikTok in 2024, boosting trial among Gen Z and Millennials.

Health-Oriented Options

Global policy pressure to trim added sugars accelerates better-for-you wafer reformulation. The World Health Organization advises limiting free sugar to less than 10% of daily energy, guidance now adopted into national dietary policies in 54 countries as of 2025. In the United States, the Food and Drug Administration’s Nutrition Facts update mandating “Added Sugars” labeling led 38% of confectionery makers to cut sugar or launch reduced-sugar lines between 2020 and 2024 [4]Source: U.S Food & Drug Administration, "Changes to the Nutrition Facts Label", fda.gov. USDA’s 2025 Organic Survey shows organic snack sales climbed 8% in 2024 to USD 1.8 billion, with biscuits the fastest-growing subcategory at 11%. Functional fortification is likewise scaling: the Institute of Food Technologists reports that 27% of new global wafer SKUs launched in 2024 contained protein isolates, prebiotics, or added vitamins, up from 15% in 2021. Clean-label priorities remain strong; the International Food Information Council’s 2025 survey found 67% of U.S. adults scrutinize ingredient lists for artificial colors—prompting widespread shifts toward natural extracts such as beet and spirulina for tinting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Disruptions | -0.9% | Global | Short term (≤ 2 years) |

| Regulatory Compliance Burdens | -0.6% | Global, particularly European Union & North America | Medium term (2-4 years) |

| Growth of Healthier Snack Alternatives | -0.8% | North America & Europe | Long term (≥ 4 years) |

| High Technology Investment for Modern Processing | -0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Disruptions

Raw material price volatility has reached critical levels, with sugar costs achieving their highest point since 2011 due to climate-induced production shortfalls across major producing regions including Brazil and the European Union. Wheat supply chains face similar pressures, with global production forecasts indicating tightening supplies and reduced ending stocks for the 2024-25 season. Transportation cost inflation compounds these challenges, with energy price spikes following geopolitical tensions creating persistent margin pressure throughout the value chain. Labor shortages across agricultural and manufacturing sectors exacerbate supply constraints, particularly in developed markets where demographic shifts reduce available workforce participation. Manufacturers respond through vertical integration strategies and long-term supply agreements, though these approaches require significant capital commitment and reduce operational flexibility. The UK Food Security Report highlights interconnected vulnerabilities, with food inflation reaching 45-year highs despite global price moderation, indicating structural supply chain fragilities that extend beyond temporary disruptions.

Regulatory Compliance Burdens

Labeling and composition rules continue to tighten across major markets. In the European Union, Regulation (UE) 2024/1442 amends the Food Information to Consumers framework to mandate front-of-pack nutrient scoring beginning January 2026, requiring new artwork for every SKU sold in the bloc. The United Kingdom’s High Fat, Salt and Sugar (HFSS) placement restrictions, fully enforced from October 2025, prohibit impulse-zone display of qualifying wafers, compelling retailers to re-planogram checkout areas [5]Source: GOV.UK, "(HFSS) placement restrictions", gov.uk. In the United States, FDA’s Traceability Rule under the Food Safety Modernization Act now obliges lot-level record-keeping for key ingredients such as wheat and cocoa, expanding audit documentation by an estimated 400 hours per plant annually. Allergen regulations also rise; Australia and New Zealand’s 2024 Plain English Allergen Labelling standard requires wafer makers to spell out “Wheat” and “Soy” in bold font within ingredients panels, prompting packaging reprints for exports to Oceania. Finally, the proposed EU Packaging and Packaging Waste Regulation targets a 20% cut in single-use plastic by 2030, pushing wafer brands toward recyclable mono-materials or paper-based laminates that often carry higher material costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Filled Variants Drive Premium Growth

Cream/chocolate/fruit-filled wafer biscuits command 60.22% market share in 2025, reflecting consumer preference for indulgent flavor experiences and textural complexity. These products benefit from higher margin structures due to premium positioning and ingredient costs, enabling sustained investment in flavor innovation and packaging sophistication. Coated wafer biscuits, while holding smaller market share, demonstrate superior growth momentum at 5.58% CAGR through 2031, driven by successful premiumization strategies and expanding distribution through modern retail channels.

The filled segment's dominance reflects manufacturers' ability to differentiate through flavor variety and seasonal offerings, creating purchase occasions beyond basic snacking needs. Chocolate-filled variants particularly benefit from cocoa's established premium positioning, though rising cocoa costs present margin challenges that require careful pricing strategies. Fruit-filled options capture health-conscious consumers seeking perceived nutritional benefits while maintaining indulgence satisfaction. Coated variants' accelerated growth stems from successful texture innovation and visual appeal that commands premium pricing, particularly in gift and celebration segments where presentation drives purchase decisions.

By Category: Organic Acceleration Amid Conventional Dominance

Conventional wafer biscuits maintain overwhelming 95.41% market share in 2025, reflecting established consumer preferences and price sensitivity across mass market segments. However, organic variants are expanding rapidly at 6.54% CAGR through 2031, indicating sustained premium pricing power and growing consumer willingness to pay elevated prices for perceived health and environmental benefits. This growth trajectory suggests successful market education and distribution expansion beyond specialty channels into mainstream retail environments.

The organic segment's acceleration reflects broader consumer trends toward clean label products and sustainable consumption practices, particularly among higher-income demographics. Certification requirements create barriers to entry that protect established organic producers while limiting competitive intensity. Supply chain complexity for organic ingredients requires specialized sourcing relationships and inventory management, creating operational challenges that smaller manufacturers struggle to address effectively. Conventional products benefit from established supply chains and cost optimization, though manufacturers increasingly introduce organic line extensions to capture premium opportunities without cannibalizing existing volumes.

By Form/Shape: Stick Innovation Challenges Brick Tradition

Brick-shaped wafer biscuits dominate with 92.10% market share in 2025, leveraging established consumer familiarity and manufacturing efficiency advantages that enable competitive pricing strategies. Stick-shaped variants, despite smaller current share, demonstrate exceptional growth at 7.02% CAGR through 2031, driven by portion control benefits and enhanced portability that aligns with on-the-go consumption trends. This format innovation reflects successful product development that addresses evolving consumer needs without requiring significant manufacturing infrastructure changes.

Stick formats' growth acceleration stems from successful positioning as portion-controlled indulgence options that address health-conscious consumers' desire for moderation without complete category avoidance. The format enables individual wrapping that maintains freshness while creating sharing opportunities in social consumption occasions. Manufacturing advantages include reduced breakage during transportation and improved shelf presentation that enhances retail appeal. Brick formats maintain advantages in cost efficiency and consumer familiarity, though manufacturers increasingly offer both formats to capture diverse consumption preferences and usage occasions.

By Packaging: Pouches Gain Traction Through Convenience

Boxes maintain the largest packaging share at 39.81% in 2025, benefiting from established retail merchandising advantages and consumer perception of value through quantity. Stand-up pouches/bags demonstrate the fastest growth at 7.05% CAGR through 2031, reflecting successful positioning as convenient, resealable formats that maintain product freshness across multiple consumption occasions. This packaging evolution aligns with changing household sizes and snacking patterns that prioritize flexibility over bulk purchasing.

Pouch formats' acceleration reflects successful innovation in barrier properties and closure mechanisms that address consumer concerns about freshness and portability. The format enables premium graphics and shelf presentation while reducing packaging material usage compared to rigid alternatives. Packets/sachets serve portion control and sampling functions, particularly in emerging markets where affordability drives purchase decisions. Other packaging formats, including cans and plastic containers, address specific usage occasions and gift markets where presentation drives premium positioning. Regulatory compliance becomes increasingly complex as packaging materials face scrutiny for environmental impact and food safety considerations.

By Distribution Channel: Digital Commerce Transforms Retail

Supermarkets/hypermarkets command 57.25% distribution share in 2025, leveraging established consumer shopping patterns and category management expertise that optimizes shelf positioning and promotional effectiveness. Online retail stores demonstrate the strongest growth at 6.18% CAGR through 2031, reflecting successful adaptation to digital commerce trends and direct-to-consumer opportunities that bypass traditional retail margins. This channel evolution creates new competitive dynamics as manufacturers develop e-commerce specific packaging and marketing strategies.

Digital commerce growth enables direct consumer relationships and data collection that inform product development and marketing strategies, though fulfillment costs and delivery logistics present operational challenges. Convenience/grocery stores maintain significant share through impulse purchasing and proximity advantages, particularly for single-serve formats and immediate consumption occasions. The channel's success depends on strategic product placement and promotional support that drives trial and repeat purchase. Other distribution channels, including vending machines and institutional sales, address specific consumption occasions though represent smaller overall market shares. Modern retail expansion across emerging markets creates growth opportunities as infrastructure development improves product availability and consumer access.

Geography Analysis

Europe leads global wafer biscuits consumption with 32.74% market share in 2025, benefiting from established confectionery traditions and sophisticated distribution networks that enable premium product positioning. The region's mature market characteristics drive innovation toward health-conscious formulations and sustainable packaging solutions that address evolving consumer preferences. Germany, United Kingdom, Italy, and France represent core consumption markets where brand loyalty and quality perceptions support premium pricing strategies. However, growth rates remain modest as market saturation limits expansion opportunities beyond product innovation and market share competition.

Asia-Pacific emerges as the fastest-growing region at 6.41% CAGR through 2031, driven by rapid urbanization, rising disposable incomes, and expanding modern retail infrastructure across key markets including China, India, and Southeast Asia. Chinese consumers increasingly embrace discount snack retail formats, with store counts tripling to 25,000 since 2022, reflecting price-conscious purchasing behavior amid economic uncertainties. The Philippines snack market, valued at USD 2.6 billion in 2023, demonstrates 8% projected CAGR through 2028, with baked snacks including biscuits reaching USD 265 million according to the U.S. Department of Agriculture. North America maintains significant market presence through established brand portfolios and innovation capabilities, though growth rates moderate as health-conscious trends challenge traditional confectionery consumption patterns. The region's regulatory environment, including FDA labeling requirements and state-level nutritional disclosure mandates, drives product reformulation toward cleaner ingredient profiles. South America and Middle East and Africa represent emerging opportunities where economic development and urbanization create expanding consumer bases, though infrastructure limitations and import dependencies constrain near-term growth potential. Brazil's economic volatility affects consumer spending patterns, while Middle Eastern markets demonstrate growing appetite for Western confectionery formats adapted to local taste preferences.

Competitive Landscape

The wafer biscuits market exhibits moderate concentration with balanced competition between multinational corporations and regional specialists, creating dynamic competitive intensity that drives continuous innovation and strategic positioning. Market leaders leverage global distribution networks and brand portfolios to maintain competitive advantages, while smaller players focus on niche segments and local market expertise to capture specialized opportunities. Technology adoption increasingly determines competitive success, with automation investments enabling cost optimization and quality consistency that supports premium positioning strategies.

Strategic consolidation continues reshaping industry dynamics, exemplified by Mars' USD 35.9 billion acquisition of Kellanova, which significantly expands snacking portfolios and creates synergies across distribution channels according to the U.S. Securities and Exchange Commission. Mondelez International's acquisition of majority stake in Evirth, a Chinese cakes and pastries manufacturer, demonstrates geographic expansion strategies targeting high-growth emerging markets. Opportunities emerge in health-conscious formulations and sustainable packaging solutions, where regulatory compliance and consumer education create barriers to entry that protect early movers.

Capital spending constraints, with industry budgets declining 1.1% in 2025, force strategic prioritization toward automation and digitization rather than capacity expansion. Cost leadership increasingly depends on technology. Plants deploy vision systems and robotics to trim breakage and hit strict weight tolerances demanded by mass retailers. Pipelines focus on reduced-sugar and protein-fortified wafers ahead of EU front-of-pack nutrient scoring rules that start in 2026. Packaging sustainability now differentiates brands as Europe targets a 20% cut in single-use plastic, nudging the switch to recyclable mono-material pouches.

Wafer Biscuits Industry Leaders

-

Mars, Incorporated

-

Hostess Brands, LLC

-

Nestlé S.A.

-

Mondelēz International

-

LOTTE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: British 'free from' snacks specialist Crave expanded its biscuit portfolio with the launch of what it claimed to be the 'UK’s first' gluten-free and vegan pink wafer biscuits, Pink Cheetah Wafers. The new product, featuring pink wafers filled with vanilla cream, tapped into the rising consumer trend of nostalgia-driven purchases and the growth of the sweet biscuits market.

- September 2024: Hostess's Voortman brand, a U.S. purveyor of crème wafers, had recently launched a new snack-size version of its fan-favorite wafer cookies, available in vanilla and chocolate. The new Voortman Snack Size Wafers featured the brand's classic, crispy vanilla- and chocolate-flavored crème wafers packaged in a convenient on-the-go snacking format. The new Voortman Snack Size Wafers came in a 2.4-ounce pack with six wafers per pack and were available at select grocery retailers including Albertsons and Walmart.

- September 2023: Biscuit International proudly announced the launch of its 2023 innovation: the 'Wafer Sandwich'. This new treat featured a delectable wafer filled with chocolate and milk. Packaged in convenient portions of two, it's perfect for a quick indulgence between meals or on the go.

Global Wafer Biscuits Market Report Scope

Wafers are made by baking thin sheets of a very liquid batter between two very hot, heavy plates. Wafers provide a distinctive eating texture.

The wafer biscuit market is segmented by form, distribution channel, and geography. The market is divided into cream-filled and coated products based on their form. Based on the distribution channel, the market is segmented into supermarkets/ hypermarkets, convenience stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South Africa, and the Middle East and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

| Cream/Chocolate/Fruit-Filled Wafer Biscuits |

| Coated Wafer Biscuits |

| Conventional |

| Organic |

| Brick-Shaped |

| Stick-Shaped |

| Boxes |

| Stand-Up Pouches/Bags |

| Packets/ Sachets |

| Others |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Cream/Chocolate/Fruit-Filled Wafer Biscuits | |

| Coated Wafer Biscuits | ||

| By Category | Conventional | |

| Organic | ||

| By Form/Shape | Brick-Shaped | |

| Stick-Shaped | ||

| By Packaging | Boxes | |

| Stand-Up Pouches/Bags | ||

| Packets/ Sachets | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the wafer biscuits market by 2031?

The sector is forecast to reach USD 133.98 billion by 2031, reflecting a 5.31% CAGR from 2026.

Which region is expanding fastest for wafer sales?

Asia-Pacific leads with a 6.41% CAGR, benefiting from urbanization and rising disposable incomes.

How are supply chain pressures affecting manufacturers?

Sugar and wheat price spikes and freight inflation erode margins, prompting vertical integration and long-term sourcing contracts.

What packaging format is gaining share most quickly?

Stand-up pouches grow at 7.05% CAGR thanks to resealability and reduced material weight.

Page last updated on: