Antimicrobial Additive Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.51 Billion |

| Market Size (2031) | USD 7.45 Billion |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antimicrobial Additive Market Analysis by Mordor Intelligence

Antimicrobial additives market size in 2026 is estimated at USD 5.51 billion, growing from 2025 value of USD 5.19 billion with 2031 projections showing USD 7.45 billion, growing at 6.20% CAGR over 2026-2031. Heightened post-pandemic hygiene awareness, tighter infection-control rules in hospitals and pharmaceutical plants, and rapid integration of antimicrobial masterbatches into recycled plastics are reshaping demand patterns. The healthcare segment remains the pivotal growth engine as hospitals embed antimicrobial coatings into catheters, surgical tools, and implantables to curb biofilm formation and related infections. Silver-based inorganic systems continue to dominate owing to broad-spectrum efficacy against multidrug-resistant pathogens, yet accelerated uptake of plant-derived and bacteriocin-based organics reflects regulatory pressure to curb synthetic biocide exposure. Meanwhile, Asia-Pacific’s industrial expansion and antimicrobial resistance initiatives position the region as both the largest and fastest-growing geography, fostering competitive intensity among global majors and agile local suppliers.

Key Report Takeaways

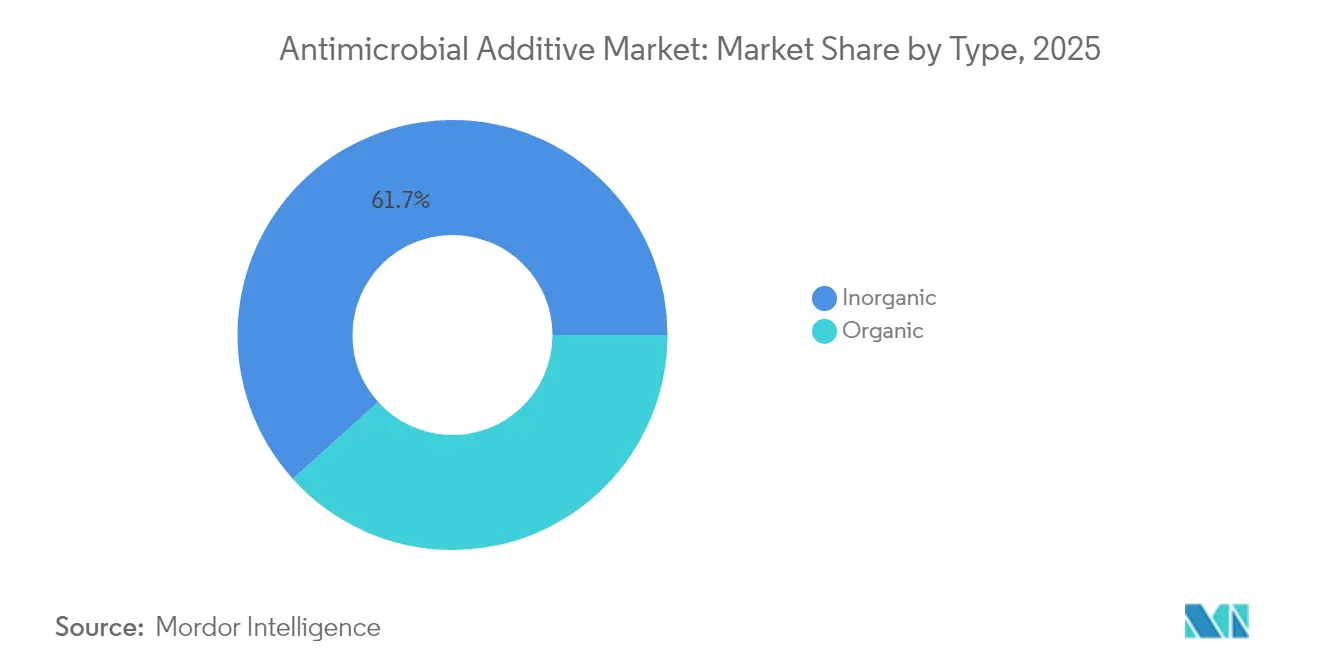

- By type, inorganic formulations led with 61.68% revenue share in 2025, while organic systems register the quickest pace at a 9.62% CAGR through 2031.

- By carrier material, plastics accounted for 42.15% of the antimicrobial additives market size in 2025, whereas textiles and fibers are projected to grow at 10.44% CAGR to 2031.

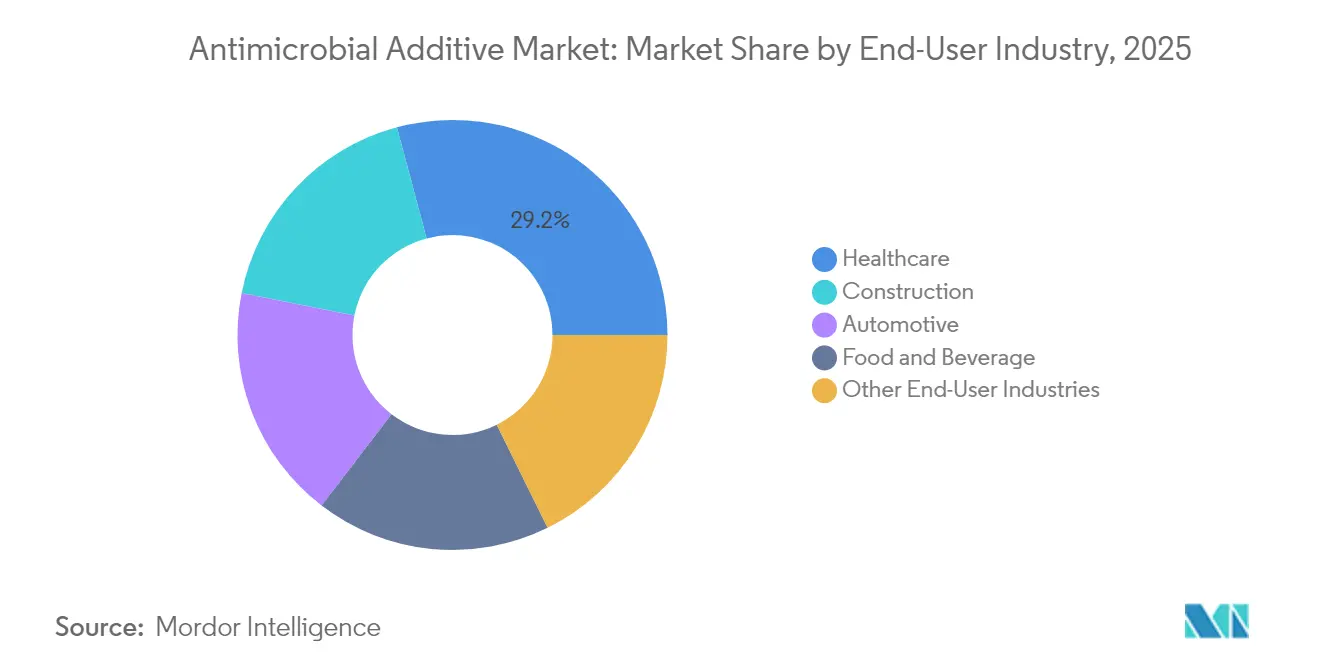

- By end-user industry, healthcare commanded 29.16% of the antimicrobial additives market share in 2025 and is expanding at an 10.98% CAGR to 2031.

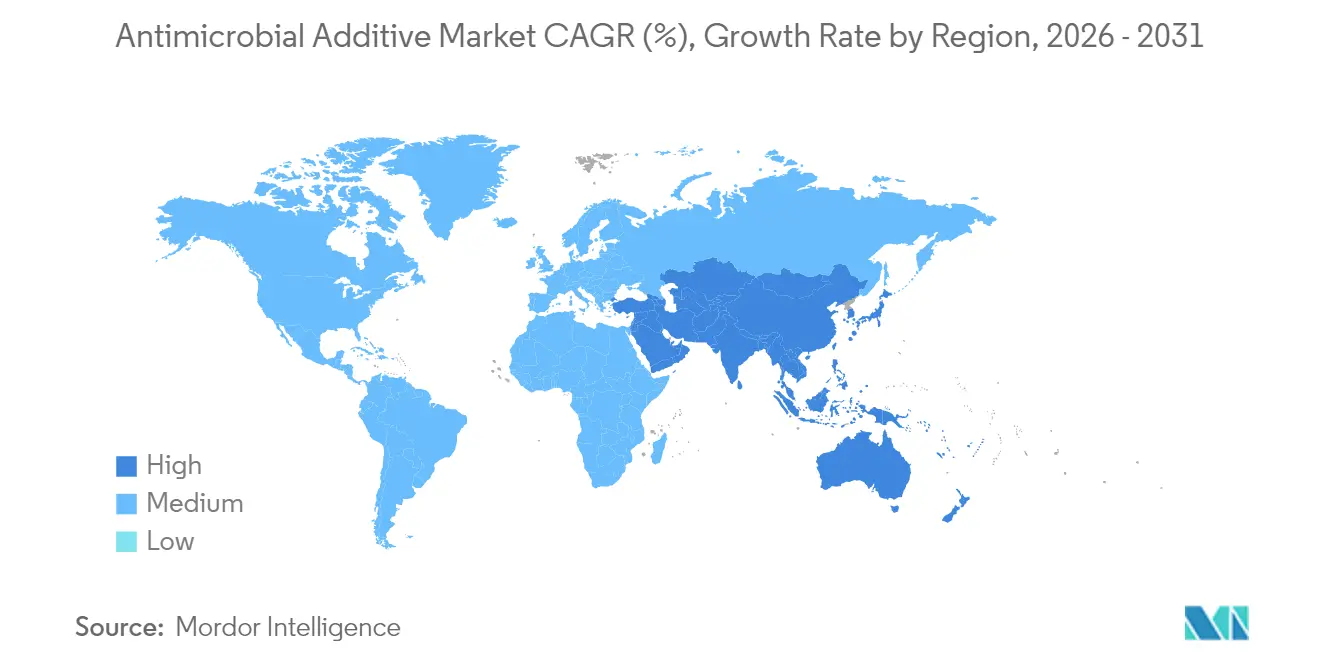

- By geography, Asia-Pacific captured 39.08% share of the antimicrobial additives market size in 2025 and is advancing at an 8.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Antimicrobial Additive Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Boom in hygienic food-grade packaging demand | +1.8% | North America, EU, global reach | Medium term (2-4 years) |

| Stricter infection-control norms in healthcare & pharma plants | +2.1% | North America, EU, APAC | Short term (≤ 2 years) |

| Surge in antimicrobial masterbatch used in recycled plastics | +1.2% | EU, North America, expanding to APAC | Long term (≥ 4 years) |

| Growing usage in plastic applications | +1.5% | APAC, North America, global | Medium term (2-4 years) |

| Expansion in the construction sector | +0.9% | North America, EU, emerging APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Boom in Hygienic Food-Grade Packaging Demand

Consumers now expect packaging that actively suppresses harmful microbes, prompting the antimicrobial additives market to supply silver, zinc oxide, and natural bacteriocin systems certified for direct food contact. Updated FDA guidance in 2024 simplifies clearance for novel actives, encouraging suppliers to embed controlled-release agents that extend shelf life by 30-50% while cutting food waste[1]U.S. Food and Drug Administration, “Guidance for Industry—Food Contact Substances: Notification Program,” fda.gov. Clean-label trends reinforce the pivot toward plant-based preservatives, and brand owners adopt QR-code traceability to evidence antimicrobial performance at retail. These developments intertwine safety and sustainability, driving global demand for next-generation active packaging.

Stricter Infection-Control Norms in Healthcare & Pharma Plants

Healthcare-associated infections cost the United States USD 4.6 billion yearly, intensifying hospital focus on antimicrobial surfaces. Accelerated FDA pathways established in 2024 shorten approval lead-times for coated devices by 40%, bringing copper-oxide nanoparticle catheters and silver-parylene surgical tools to market swiftly. Pharmaceutical cleanrooms likewise specify antimicrobial wall panels, flooring, and HVAC coatings to uphold aseptic production, recasting these additives from optional features into essential infrastructure.

Surge in Antimicrobial Masterbatch Used in Recycled Plastics

Food brands pursuing circular-economy targets lean on masterbatch solutions that insert precise antimicrobial doses during compounding, preserving hygiene as recycled content grows. Conformance with EU and U.S. food-contact rules accelerates adoption, while producers benefit from safer handling and reduced off-spec scrap[2]Microban International, “Integrating Antimicrobials into Recycled Plastics,” microban.com . As retailers publicize recycled yet hygienic packaging lines, the antimicrobial additives market broadens its opportunity set within rPET trays and HDPE closures.

Growing Usage in Plastic Applications

Plastics remain an indispensable vehicle for antimicrobial chemistry because they accept diverse actives without altering baseline mechanical properties. Silver-ion, zinc pyrithione, and new metal-free agents disperse uniformly during extrusion, giving consumer electronics housings, automotive interiors, and medical disposables persistent microbial defense. Compliance with REACH and RoHS steers innovation toward low-toxicity systems, cementing plastics as a stable anchor segment despite evolving environmental expectations.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxic nature of certain additives | -1.4% | EU, North America, global | Short term (≤ 2 years) |

| Volatility in raw material prices | -0.8% | Global, especially silver and copper supply chains | Medium term (2-4 years) |

| High production cost | -1.1% | Price-sensitive APAC and emerging regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Toxic Nature of Antimicrobial Additives

Rigorous EU Biocidal Products Regulation now demands extensive risk dossiers before market entry, placing triclosan and other legacy biocides under intense review[3]European Chemicals Agency, “Biocidal Products Regulation FAQs,” echa.europa.eu . U.S. agencies weigh endocrine and microbiome effects, spurring formulators to pivot toward biodegradable polymers and essential-oil actives. Concerns about silver nanoparticle accumulation in aquatic habitats push research into targeted delivery and lower dosage thresholds to uphold efficacy without ecological harm.

Volatility in Raw Material Prices

Silver prices swung 25–30% during 2024, raising cost pressure on dominant inorganic systems. Manufacturers hedge risk through multi-metal blends, recycling programs, and expansion of copper-oxide and zinc-based chemistries that track more stable price curves. Rising uptake of organics also cushions exposure to precious-metal swings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Inorganic Dominance Faces Organic Disruption

Inorganic formulations accounted for 61.68% of the antimicrobial additives market share in 2025, translating to a sizable portion of the overall antimicrobial additives market size and underscoring silver’s long-standing reputation for broad-spectrum efficacy. Silver nanoparticles rupture bacterial membranes through multiple oxidative mechanisms, delivering reliable kill rates against MRSA and carbapenem-resistant strains without prompting rapid resistance. Copper oxide and zinc pyrithione provide cost-effective alternatives, especially in construction paints and marine coatings where price sensitivity limits silver’s reach.

Organic systems, while representing a smaller revenue base today, are expanding at a 9.62% CAGR and steadily reshaping the antimicrobial additives market. Essential oils such as thyme, oregano, and cinnamon exhibit potent antimicrobial activity combined with biodegradability, appealing to regulators and eco-conscious buyers. Bacteriocins sourced from lactic-acid bacteria offer narrow-spectrum efficacy that spares beneficial flora, a trait valued in medical and food applications. Chitosan-derived polymers offer film-forming properties and natural antimicrobial action, broadening usage in wound dressings and sustainable packaging.

These dynamics indicate that although inorganic chemistries will continue to anchor the antimicrobial additives market through 2031, organic alternatives are set to capture incremental share as performance parity improves and regulatory incentives favor low-tox approaches.

By Carrier Material: Plastics Leadership Challenged by Textile Innovation

Plastics retained 42.15% of the antimicrobial additives market size in 2025, mirroring entrenched conversion infrastructure across extrusion, injection molding, and blow-molding lines. Ease of dispersing ions or plant-based actives into polymer matrices ensures consistent antimicrobial potency throughout the product life cycle. Building-product makers exploit these attributes to reduce mold growth in high-humidity zones, and electronics brands tout hygienic housings that resist odor-causing bacteria.

Textiles and fibers, however, exhibited the fastest climb at a 10.44% CAGR, reflecting fashion brands, healthcare providers, and hospitality chains that demand lasting antimicrobial protection embedded at the fiber stage. Silver ions, quaternary ammonium compounds, and increasingly plant-derived extracts are spun directly into polyester or polyamide, retaining effectiveness after repeated laundering. Sportswear labels promote odor-control benefits, while hospitals specify antimicrobial curtains and uniforms to cut cross-contamination. With comfort and sustainability co-equal priorities, R&D now emphasizes low-leach formulations that maintain hand feel and breathability.

Collectively, these trends underscore a gradual rebalancing of the antimicrobial additives market toward materials that align functionality with circular-economy imperatives, while plastics continue to dominate volume due to manufacturing versatility.

By End-User Industry: Healthcare Drives Innovation Across Applications

Healthcare maintained 29.16% share of the antimicrobial additives market in 2025 and is advancing at an 10.98% CAGR, reflecting relentless efforts to suppress healthcare-associated infections that afflict 1 in 20 U.S. patients each year. Catheters coated with silver-parylene blends exhibit 99.9% bacterial reduction even under repeated contamination cycles, while copper-oxide wound dressings support faster healing with reduced antibiotic reliance. Hospital facility planners increasingly specify antimicrobial flooring, HVAC linings, and privacy curtains to create holistic infection-control environments that complement device-level solutions.

Adjacent sectors also embrace antimicrobial protection. Construction markets broaden usage in drywall, ceiling tiles, and grouts to resist mold growth and prolong service life, especially in high-humidity geographies. Automotive OEMs incorporate antimicrobial additives into air-vent plastics and steering-wheel surfaces to elevate in-cabin hygiene. Food and beverage packaging leverages active antimicrobial films to extend perishables’ shelf life by up to 50%, dovetailing with sustainability goals through reduced waste.

These cross-industry deployments affirm healthcare’s role as the technology proving ground whose success stories cascade into mainstream industrial and consumer applications, deepening the addressable lattice for the antimicrobial additives market.

Geography Analysis

Asia-Pacific steered 39.08% of global revenue in 2025 and is climbing at an 8.78% CAGR, making it the fulcrum of the antimicrobial additives market. China’s ongoing hospital modernization, India’s scale-up of pharmaceutical manufacture, and Singapore’s bacteriophage research programs together fuel demand for advanced infection-control materials. Construction booms in Indonesia and Vietnam further amplify needs for mold-resistant paints and sealants. Multinationals such as BASF and Dow expand joint ventures to tailor formulations for local regulatory nuances, while regional challengers leverage cost advantages to supply mid-tier segments.

North America commands mature yet lucrative end-user bases in medical devices, food packaging, and advanced polymers. Recent FDA guidance that simplifies antimicrobial additive clearance for food contact materials stimulates pipeline movement, while healthcare procurement budgets prioritize proven, broad-spectrum coatings. Circular-economy targets accelerate use of antimicrobial masterbatch in recycled plastics, especially for contact-sensitive applications.

Europe maintains stringent biocide regulations that both elevate market entry barriers and stimulate R&D into greener chemistries. Builders adopt antimicrobial drywall and roofing membranes to meet mold-management standards in energy-efficient structures. Consumer preference skews toward natural and biodegradable solutions, prompting suppliers to emphasize transparency and eco-labels in marketing.

South America and Middle East & Africa, although smaller in absolute dollars, present rising opportunities. Brazil’s distributors broaden biocide portfolios for coatings and lubricants, while Gulf states align hospital investments with infection-control mandates. Regulatory maturation across these regions ensures that international best practices progressively shape antimicrobial procurement criteria.

Competitive Landscape

The antimicrobial additives market remains moderately fragmented. BASF, Clariant, and Avient occupy leading positions by integrating R&D depth with global manufacturing footprints. Technology differentiation centers on metal-free and biodegradable solutions. Biotech entrants harness generative AI to identify antimicrobial peptides with narrow-spectrum activity. These nimble challengers aim to sidestep heavy-metal cost volatility and regulatory scrutiny, positioning novel chemistries for next-decade growth.

Competitive intensity is heightened in Asia-Pacific, where domestic firms undercut on price while adopting silver-glass technologies licensed from Western peers. In response, incumbents pursue joint R&D ventures to customize formulations for local pathogen profiles and regulatory codes. Overall, intellectual-property depth, regulatory literacy, and raw-material security determine the pecking order as the antimicrobial additives market matures.

Antimicrobial Additive Industry Leaders

Clariant

BASF

Avient Corporation

Milliken & Company

SANITIZED AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Avient Corporation unveiled Cesa WithStand SX Low Haze Antimicrobial Additives for clear polycarbonate and plexiglass, optimizing aesthetics in products with recycled resin while safeguarding against bacterial and fungal growth.

- September 2023: Microban International, using an active, sustainable ingredient, launched Ascera, a patent-pending, metal-free antimicrobial technology for olefinic polymers and solvent-based coatings.

Global Antimicrobial Additive Market Report Scope

The antimicrobial additive market report include:

| Inorganic |

| Organic |

| Plastics |

| Paints and Coatings |

| Pulp and Paper |

| Textiles and Fibers |

| Silicone and Elastomers |

| Other Carrier Materials |

| Construction |

| Healthcare |

| Automotive |

| Food and Beverage |

| Other End-User Industries |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Inorganic | |

| Organic | ||

| By Carrier Material | Plastics | |

| Paints and Coatings | ||

| Pulp and Paper | ||

| Textiles and Fibers | ||

| Silicone and Elastomers | ||

| Other Carrier Materials | ||

| By End-User Industry | Construction | |

| Healthcare | ||

| Automotive | ||

| Food and Beverage | ||

| Other End-User Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the antimicrobial additives market?

The antimicrobial additives market stands at USD 5.51 billion in 2026 and is projected to hit USD 7.45 billion by 2031, based on a 6.20% CAGR.

Which end-use segment leads consumption?

Healthcare leads with 29.16% share in 2025 and continues to grow fastest at an 10.98% CAGR as hospitals and device makers embed antimicrobial coatings.

Which region shows the highest growth potential?

Asia-Pacific combines the largest share at 39.08% with the quickest expansion at an 8.78% CAGR thanks to healthcare infrastructure build-out and industrialization.

How are raw-material price swings influencing strategy?

Volatile silver and copper prices push suppliers to diversify into zinc-based and plant-derived chemistries while investing in recycling loops to stabilize margins.

Page last updated on: