Volumetric Display Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

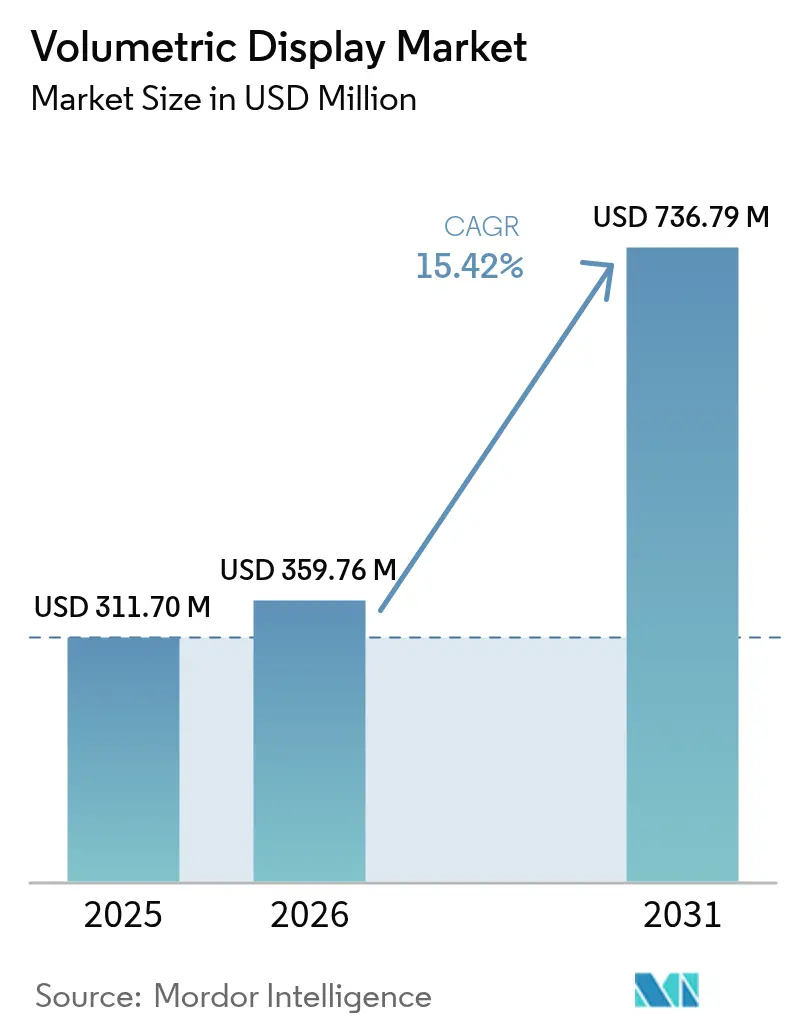

| Market Size (2026) | USD 359.76 Million |

| Market Size (2031) | USD 736.79 Million |

| Growth Rate (2026 - 2031) | 15.42% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Volumetric Display Market Analysis by Mordor Intelligence

The volumetric display market size was valued at USD 311.7 million in 2025 and estimated to grow from USD 359.76 million in 2026 to reach USD 736.79 million by 2031, at a CAGR of 15.42% during the forecast period (2026-2031). Over the forecast period the technology shifts from experimental novelty toward a core visualization platform across operating rooms, command centers, and advanced cockpits. Strong demand for 3D anatomical imaging, growing defense procurement of glass-free situational-awareness consoles, and automotive moves toward full-windshield 3D clusters underpin this climb. In parallel, projector costs per lumen keep falling while real-time hologram processors shorten latency, making premium user experiences available at lower total cost of ownership. Intensifying software innovation is tilting competitive advantage toward firms that control rendering engines and content ecosystems rather than only optical hardware, rewriting the basis of differentiation inside the volumetric display market.

Key Report Takeaways

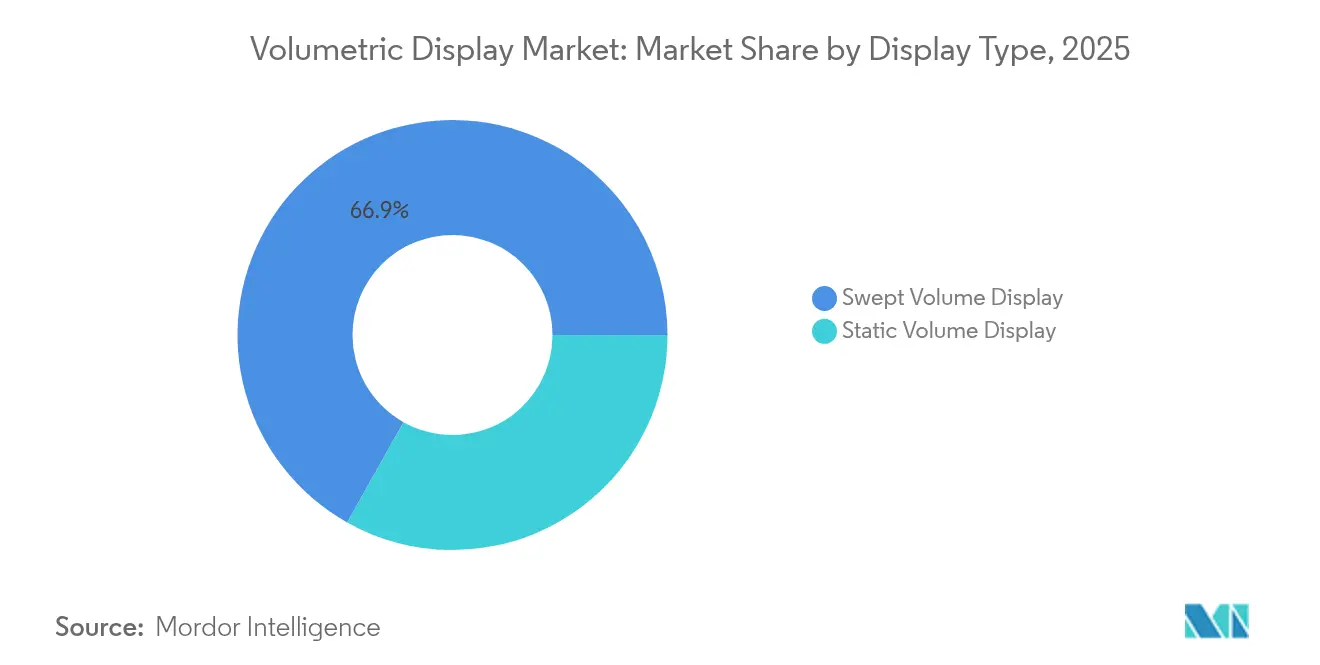

- By display type, swept-volume systems led with 66.85% revenue share in 2025; static-volume technology is forecast to advance at a 17.48% CAGR through 2031.

- By component, projectors and laser modules held 36.52% of the volumetric display market share in 2025, while rendering software & GPU hardware post the quickest growth at 16.31% CAGR to 2031.

- By display size, 24-40 inch 360-degree tables accounted for 50.05% share of the volumetric display market size in 2025; installations above 40 inch cubes are set to grow at an 18.01% CAGR.

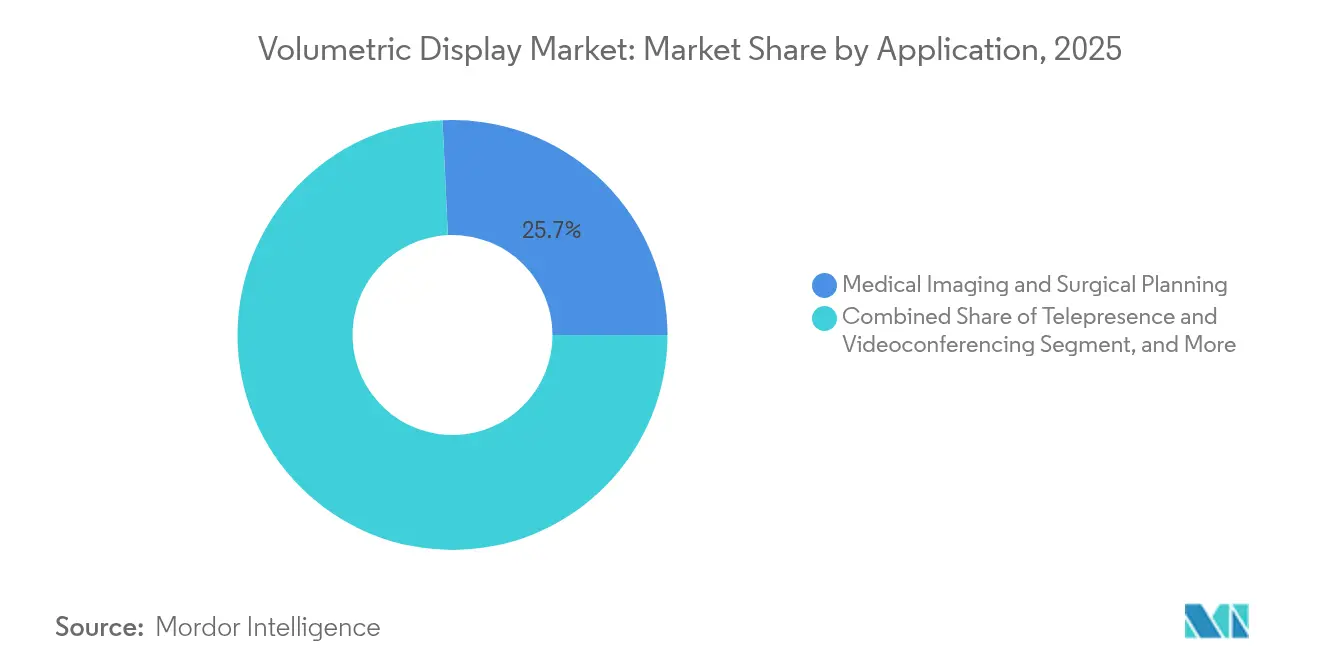

- By application, medical imaging captured 25.74% of the volumetric display market size in 2025, whereas telepresence is projected to rise at 17.22% CAGR.

- By end-user industry, healthcare providers held 23.96% share in 2025; media, sports & entertainment venues record the fastest CAGR at 15.63%.

- By geography, Asia-Pacific commanded 32.78% of the volumetric display market in 2025, while the Middle East & Africa expands most rapidly at a 16.92% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Volumetric Display Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of 3D anatomical visualization in minimally invasive surgeries | +3.2% | North America & Europe | Medium term (2-4 years) |

| Defense demand for glass-free 360° situational-awareness systems | +2.8% | Middle East, spillover to APAC | Short term (≤ 2 years) |

| Automotive HUD evolution toward in-cabin 3D instrument clusters | +2.1% | Germany, Japan, global reach | Medium term (2-4 years) |

| Media & entertainment pivot to location-based holographic attractions | +1.9% | Asia core, global rollout | Long term (≥ 4 years) |

| Falling projection cost per lumen via solid-state lasers | +2.4% | Global | Short term (≤ 2 years) |

| Telecom 5G rollout enabling real-time volumetric telepresence | +1.8% | United States & South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adoption of 3D Anatomical Visualization in Minimally Invasive Surgeries

Hospitals integrate volumetric displays to overcome the spatial constraints of flat monitors. Systems such as RealView Imaging’s Holoscope-i project interactive 3D/4D holograms that surgeons can inspect from any angle, lowering eye strain and shortening procedure times.[1]Susan Shepard, “Can Holograms Change 3D Medical Imaging?” MD+DI, mddionline.com Multi-institutional studies show surgical teams preferred holographic planning in 61% of cases over 2D images, reinforcing clinical momentum. As fluorescence-guided surgery merges with holographic output, the platform evolves from simple viewer to integrated surgical console. Purchasing patterns indicate the equipment will be standard in complex surgery suites by 2027, lifting annual hardware demand inside the volumetric display market.

Defense Demand for Glass-Free 360° Situational-Awareness Systems

Armed forces in the Middle East deploy volumetric displays inside command posts to let multiple officers share the same 3D battlespace view without headsets.[2]Avalon Holographics, “Holographics for Battlespace Visualization,” avalonholographics.com Tests funded by the US Air Force Research Lab confirm quicker target recognition and mission-planning cycles compared with tiled 2D maps. Budget allocations for ISR upgrades now earmark glass-free 3D tables, signaling steady procurement through 2026. As OEMs certify mil-spec housing and sand-dust tolerance, defense orders form a reliable revenue stream for the volumetric display market.

Automotive HUD Evolution Toward In-Cabin 3D Instrument Clusters

OEMs move beyond basic head-up overlays toward full-windshield holographic clusters that embed speed, ADAS alerts, and navigation cues at true depth. Hyundai Mobis previewed an all-windshield unit that sections the glass into separate viewing zones, proving scalability to mass-production lines. Eye-tracking fine-tunes parallax, cutting driver distraction and enabling passenger-specific content. European and Japanese regulators are drafting harmonized guidelines, clearing the legal road for series production in 2027. Resulting design-in contracts elevate the volumetric display market’s automotive pipeline.

Media and Entertainment Pivot to Location-Based Holographic Attractions

Asian theme parks install volumetric displays to offer immersive exhibitions that home media cannot replicate. Multi-user holographic stages boost dwell time and premium ticket tiers, raising venue EBITDA. Operators report social-media amplification that lifts secondary spend on merchandise. As solid-state lasers shrink capex, mid-tier attractions adopt the format, broadening addressable demand. This leisure wave brings repeat unit orders and steady content-refresh contracts into the volumetric display market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent sub-HD native resolution limiting clinical diagnostics | -2.1% | Global, acute in North America & Europe | Medium term (2-4 years) |

| High acquisition cost versus competing 3D visualization tools in SMEs | -1.8% | Global, stronger in emerging markets | Short term (≤ 2 years) |

| Limited content authoring ecosystem hindering mass adoption | -1.5% | Global | Long term (≥ 4 years) |

| Safety regulations around high-intensity laser sources | -1.2% | EU core, ripple to other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Sub-HD Native Resolution Limiting Clinical Diagnostics

Most current volumetric systems fall below the pixel density clinicians need for micro-vascular inspection or pathology review. Lower lateral resolution becomes more pronounced on large collaborative tables, forcing radiologists to revert to CT workstations for fine detail.[3]Huaying Wang et al., “Lateral Resolution of Digital Holographic System,” spiedigitallibrary.org Research into color-aware holographic optimization is closing the gap, yet diagnostic-grade prototypes remain in labs. Until pixel pitches match digital microscopy thresholds, the volumetric display market must rely on surgical planning rather than diagnostics for medical revenue.

High Acquisition Cost versus Competing 3D Visualization Tools in SMEs

For resource-constrained manufacturers and design studios, a full volumetric setup-hardware, rendering licenses, and service contracts-can exceed the total cost of ownership of VR headsets by an order of magnitude. ROI calculations are further stretched by the limited pool of turnkey content developers. Government programs such as NIST’s additive-manufacturing data initiatives aim to simplify file pipelines, but cost parity with mid-range 3D monitors sits several years away.[4]William Frazier, “Empowering Small and Medium-Sized Enterprises Through Effective Additive Manufacturing Data Management,” nist.gov This gap weighs on near-term unit volumes in the volumetric display market outside Fortune 1000 buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Display Type: Swept-Volume Dominance and Static-Volume Momentum

Swept-volume architectures capture 66.85% volumetric display market share in 2025 thanks to mature production tooling and field-proven reliability. Rotational persistence of vision enables bright images inside compact footprints, ideal for medical and defense consoles. Static-volume units, though smaller today, post the strongest 17.48% CAGR as holographic-laser-excited graphics eliminate moving parts, slashing maintenance cycles.

Recent demonstrations of color static-volume cubes show excellent environmental robustness, enticing laboratories that cannot tolerate mechanical vibration. As holographic materials scale, static-volume systems are forecast to erode swept-volume dominance, pushing the volumetric display market size for static architectures past USD 228.6 million by 2031. Vendors that master both paths hedge against future customer preference swings.

By Component: Software Rendering as the New Growth Driver

Optical hardware-projectors and laser engines-retains 36.52% share because brightness and color gamut still depend on photon efficiency. Yet rendering software and high-bandwidth GPUs accelerate at 16.31% CAGR, outpacing optics as buyers demand real-time 4K holograms. The volumetric display market size for compute subsystems is forecast to nearly double between 2026 and 2031 as processors with hologram-specific instruction sets reach commercial boards.

In response, hardware-centric firms form alliances with game-engine vendors to bundle SDKs, while pure-play software houses license IP blocks to projector manufacturers. The shift recasts value capture toward algorithms that compress interference patterns without visual artifacts, setting the next competitive battleground inside the volumetric display industry.

By Display Size: Large-Format Installations Capture Premium Spend

The 24-40 inch 360° table remains the workhorse holding 50.05% share in 2025 because it balances immersion with desktop ergonomics. Enterprise road-mapping sessions and surgical planning benches gravitate to this footprint. Conversely, installations above 40 inch cubes race ahead at 18.01% CAGR, adding scale for team-of-ten collaboration and auditorium demonstrations. A single 60 inch cube can replace multiple monitors, justifying loftier price points and service contracts that lift the volumetric display market size in the top tier.

Below 24 inch cubes stay relevant in education kits and concept demos, but face competition from lenticular 3D laptops. Suppliers therefore tailor optical-engine line-ups across three size tiers, preventing margin leakage when customers migrate upward.

By Application: Medical Imaging Leadership and Telepresence Acceleration

Medical imaging secured 25.74% volumetric display market size in 2025 as hospitals approved capital budgets to cut operating-room time through clearer depth cues. Neuro and cardiac specialists cite shorter planning loops and lower joystick manipulation fatigue. Telepresence delivers the quickest 17.22% CAGR on the back of 5G rollouts and rising hybrid-work norms. Live 3D calls let remote experts orbit around physical prototypes or patient avatars, removing the isolation found in VR headsets.

Advertising, engineering visualization, and defense command rooms round out demand. Each vertical values the same light-field core but diverges on brightness, field-of-view, and API openness. This variety insulates the volumetric display market from single-sector slowdowns.

By End-User Industry: Healthcare Providers Set the Pace

Hospitals and surgical centers accounted for 23.96% volumetric display market share in 2025, proving willingness to fund new visualization when outcome metrics improve. Capital budget committees find that a single volumetric console amortizes across multiple surgical departments. Entertainment venues, including esports arenas and theme parks, post the fastest 15.63% CAGR as operators seek social-media-ready spectacles that command premium ticket pricing.

Automotive design studios, aerospace primes, and academic labs together sustain a diversified demand base. As leading carmakers lock in windshield contracts, the automotive tier alone could represent more than USD 92.4 million of incremental volumetric display market size by 2031. Cross-industry adoption lessens cyclical risk and encourages component suppliers to standardize interfaces.

Geography Analysis

Asia-Pacific led with 32.78% share of the volumetric display market in 2025, anchored by Japanese, Chinese, and South-Korean conglomerates that combine semiconductor strength with large domestic entertainment spend. Japan’s decision to embed holographic portraits in new banknotes signals mainstream acceptance, catalyzing local optics suppliers. South-Korea’s telcos demonstrated live 5G hologram calls, drawing enterprise pilot projects. The region’s dense supplier base keeps lead-times short, accelerating refresh cycles.

North America ranks second, propelled by US surgical-robot makers and defense labs that integrate volumetric consoles into C2 suites. Federal funding for advanced manufacturing testbeds exposes SMEs to the technology, expanding mid-market prospects. Canada’s med-tech clusters in Ontario and British Columbia add clinical validation sites, reinforcing regional credibility.

Europe remains focused on automotive integration. German Tier-1s partner with optics specialists to engineer windshield-embedded holograms compliant with UN ECE glare rules. EU laser-safety norms slow deployments but ultimately raise baseline quality, building export appeal once certificates are issued.

The Middle East and Africa register the highest 16.92% CAGR through 2031 as defense ministries procure glass-free 360° tables for joint-ops centers. Sovereign funds in the Gulf finance entertainment complexes that feature holographic attractions, further boosting unit flow. Latin America shows nascent adoption, with Brazil’s universities piloting volumetric labs for industrial design curricula, seeding future demand across the continent.

Competitive Landscape

The sector exhibits moderate concentration: top five vendors collectively hold about 48% revenue, leaving room for specialists to differentiate. Sony blends proprietary micro-displays with a growing spatial-reality SDK, allowing content studios to port assets from existing pipelines. Microsoft leverages its mixed-reality software stack to position volumetric consoles as natural complements to HoloLens development kits.

Pure-plays such as Voxon Photonics and Looking Glass Factory sustain high innovation cadence by focusing on single-purpose volumetric engines. Voxon’s newest swept-volume core improved brightness by 35% while halving noise levels, addressing surgical-theater requirements. Looking Glass ships 16-inch and 32-inch light-field panels bundled with an easy-to-use Unity plug-in, reducing developer friction.

Strategic alliances rise in frequency. Optical-component maker Luminit partners with automotive Tier-1s to supply holographic windshield films, while GPU leaders collaborate with research institutes to co-design hologram-optimized instruction sets. Patent filings for diffractive optical elements and algorithmic compression soared 22% year-on-year, foreshadowing both defensive litigation and licensing revenue within the volumetric display market.

Volumetric Display Industry Leaders

Coretec Group Inc.

Voxon Photonics

Looking Glass Factory Inc.

Sony Corporation

LightSpace Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Sony Corporation released an upgraded Spatial Reality Display that supports 4K 3D viewing without headsets.

- March 2025: Electronics & Telecommunications Research Institute (ETRI) introduced a real-time 4K hologram processor with 30 ms latency.

- January 2025: Hyundai Mobis showcased a full-windshield holographic cluster scheduled for 2027 production vehicles.

- January 2025: Luminit Inc. demonstrated holographic windshield films that raise clarity in bright daylight driving.

Global Volumetric Display Market Report Scope

Volumetric displays allow the user to create a visual representation of an object into three physical dimensions providing the viewer with a 360-degree spherical viewing angle. This report segments the market by type, end-user industry, and geography.

| Swept Volume Display |

| Static Volume Display |

| Projectors and Laser Modules |

| Display Panels and Optical Elements |

| Rendering Software and GPU Hardware |

| Holographic Materials |

| Other Components |

| Below 360° Viewing Volume (Sub 24 inch cube) |

| 360° Table-Top (24 inch-40 inch cube) |

| Large-Format (Above 40 inch cube) |

| Medical Imaging and Surgical Planning |

| Telepresence and Videoconferencing |

| Education and Training Simulations |

| Advertising and Digital Signage |

| Entertainment and Gaming |

| Engineering and Design Visualization |

| Defence and Security Command Centers |

| Other Applications |

| Healthcare Providers |

| Automotive and Transportation |

| Media, Sports and Entertainment Venues |

| Industrial and Manufacturing |

| Aerospace and Defence |

| Academic and Research Institutes |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Display Type | Swept Volume Display | ||

| Static Volume Display | |||

| By Component | Projectors and Laser Modules | ||

| Display Panels and Optical Elements | |||

| Rendering Software and GPU Hardware | |||

| Holographic Materials | |||

| Other Components | |||

| By Display Size | Below 360° Viewing Volume (Sub 24 inch cube) | ||

| 360° Table-Top (24 inch-40 inch cube) | |||

| Large-Format (Above 40 inch cube) | |||

| By Application | Medical Imaging and Surgical Planning | ||

| Telepresence and Videoconferencing | |||

| Education and Training Simulations | |||

| Advertising and Digital Signage | |||

| Entertainment and Gaming | |||

| Engineering and Design Visualization | |||

| Defence and Security Command Centers | |||

| Other Applications | |||

| By End-user Industry | Healthcare Providers | ||

| Automotive and Transportation | |||

| Media, Sports and Entertainment Venues | |||

| Industrial and Manufacturing | |||

| Aerospace and Defence | |||

| Academic and Research Institutes | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the volumetric display market?

The market is valued at USD 359.76 million in 2026 and is projected to reach USD 736.79 million by 2031 at a 15.42% CAGR.

Which application leads revenue today?

Medical imaging holds 25.74% of the volumetric display market size in 2025, benefiting from measurable surgical-outcome gains.

Which regional market grows fastest through 2031?

The Middle East & Africa advance at a 16.92% CAGR, propelled by defense spending on glass-free 360° command-center consoles.

How are software advances influencing competition?

Rendering engines and GPU-based hologram processors are the fastest-growing component block at 16.31% CAGR, shifting value capture toward firms with algorithmic IP.

What major technological hurdle still restricts adoption?

Sub-HD native resolution limits diagnostic-grade use cases, constraining medical imaging expansion until pixel density improves.

Are volumetric displays viable for small businesses?

High acquisition and content-creation costs remain barriers for SMEs, though falling projection prices and open-source authoring tools are expected to narrow the gap over the next two years.

Page last updated on: