Personal Lubricants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

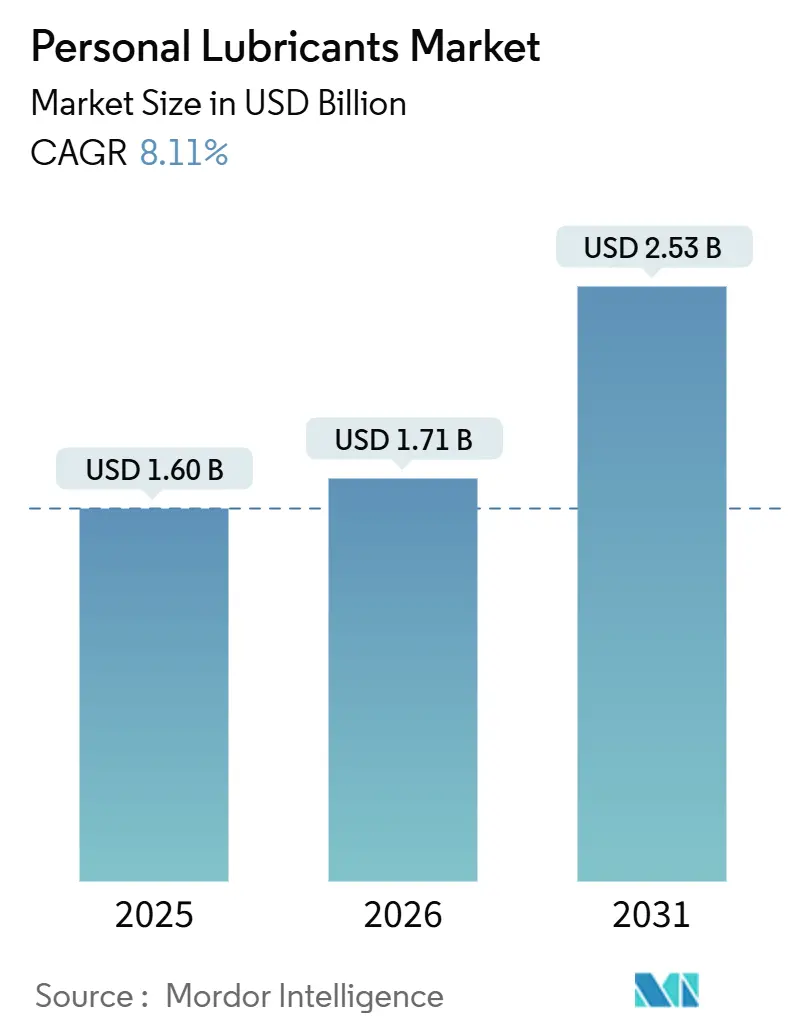

| Market Size (2026) | USD 1.71 Billion |

| Market Size (2031) | USD 2.53 Billion |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

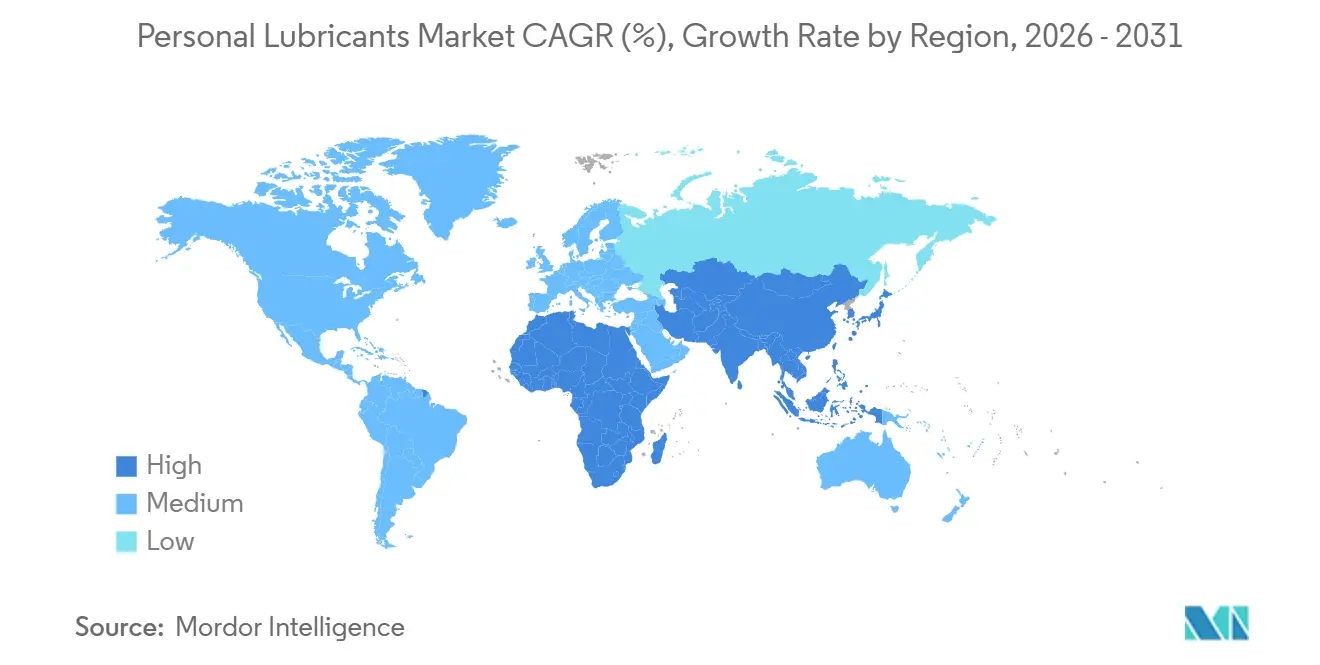

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Personal Lubricants Market Analysis by Mordor Intelligence

The Personal Lubricants Market size is projected to be USD 1.60 billion in 2025, USD 1.71 billion in 2026, and reach USD 2.53 billion by 2031, growing at a CAGR of 8.11% from 2026 to 2031.

This steady climb mirrors the broader normalization of sexual-wellness shopping, the swift rise of digitally enabled dispensing, and the growing clinical acceptance of lubricants as front-line options in menopause and fertility care. Water-based products still anchor volume, but hybrid and specialty formulations that blend water and silicone bases, balance pH, or carry FDA-cleared fertility claims are winning share on the back of stronger functional benefits. E-commerce platforms, often tied to subscription programs and FSA/HSA reimbursement, are outpacing brick-and-mortar traffic as consumers opt for anonymity and wider assortments. Regulatory friction remains a hurdle, yet players that clear the FDA’s Class II device pathway and offer evidence-based, allergen-free ingredients unlock premium price points and retail placement. Competitive attention continues to pivot toward inclusive product design, as gender-neutral branding expands the user base beyond legacy male-female binaries and pushes incumbents to rethink portfolio architecture.

Key Take Aways

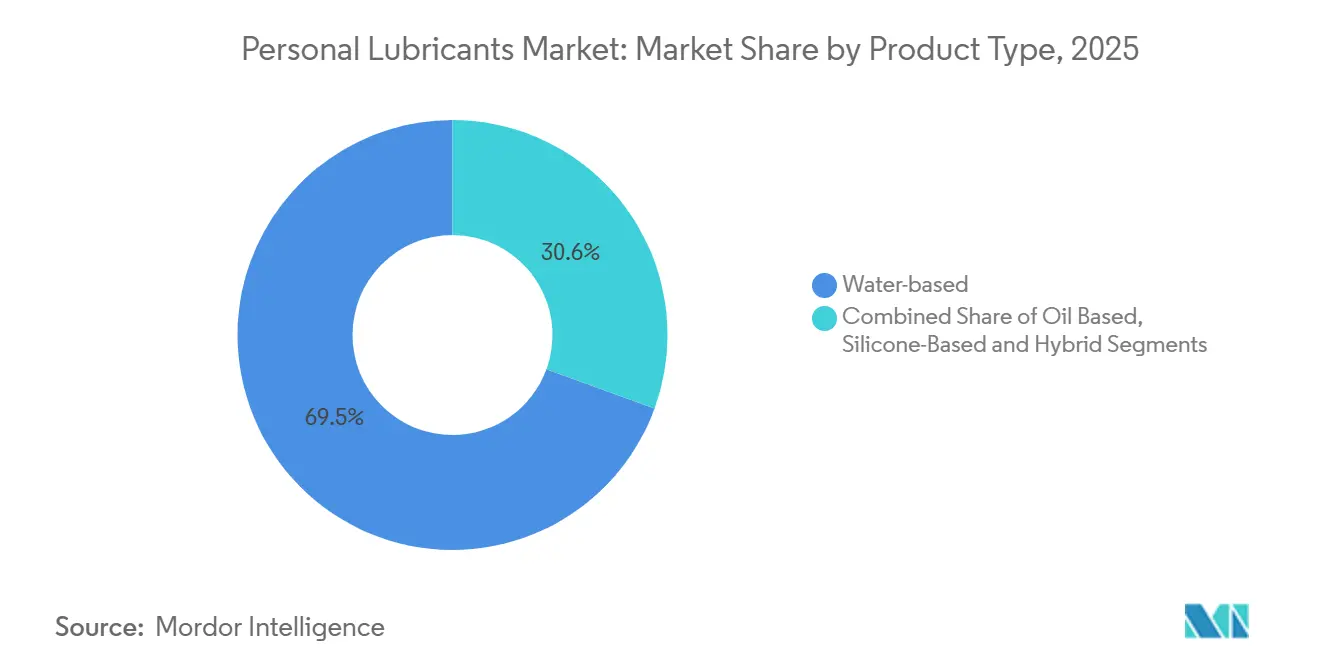

- By product type, water-based lubricants led with 69.45% revenue share in 2025, while hybrid and specialty variants are projected to expand at an 11.67% CAGR to 2031.

- By distribution channel, drug stores and pharmacies accounted for 41.77% of global sales in 2025, whereas e-commerce is set to grow at a 12.39% CAGR over the period.

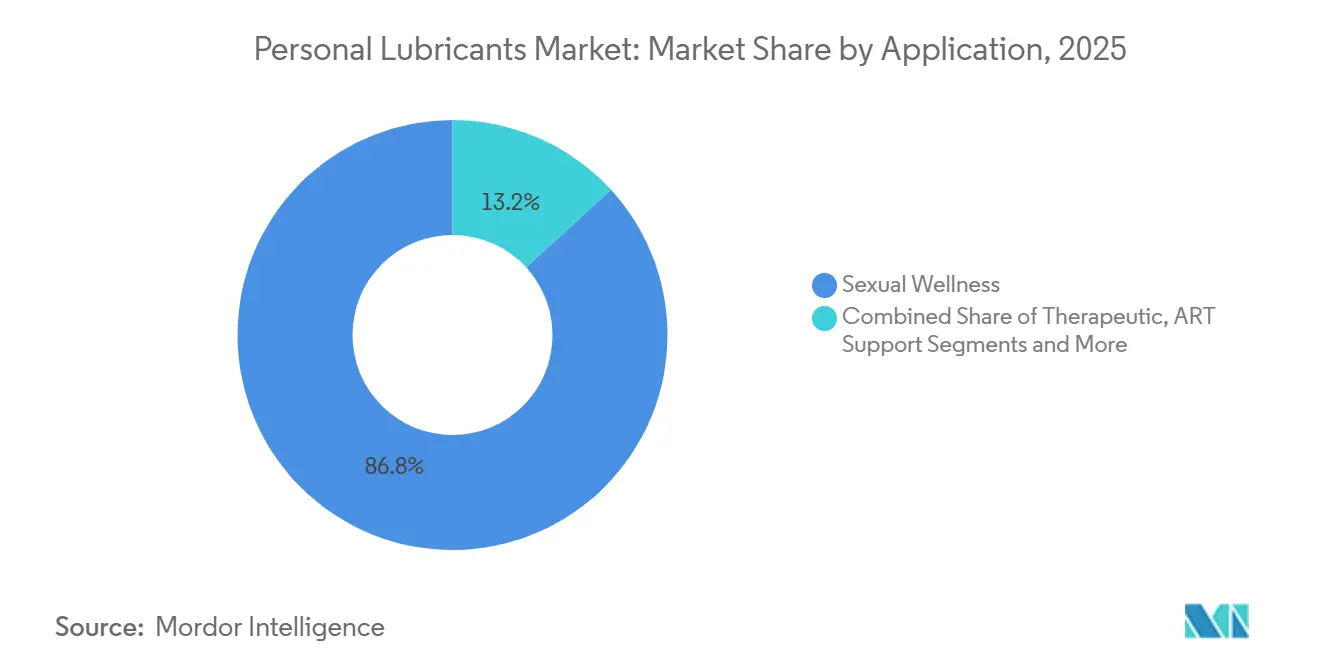

- By application, sexual wellness dominated with an 86.82% share of demand in 2025, whereas therapeutic usage for vaginal dryness and dyspareunia is advancing at an 11.43% CAGR through 2031.

- By end-user, women represented 53.58% of consumption in 2025, while the non-binary and LGBTQ+ cohort is rising at a 10.46% CAGR during the forecast horizon.

- By geography, North America captured 38.61% of global revenue in 2025, and Asia-Pacific is forecast to register a 10.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Personal Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Destigmatization of sexual-wellness products | +1.8% | North America, Europe | Medium term (2-4 years) |

| Explosive e-commerce penetration | +2.1% | Asia-Pacific core, spillover to North America and Europe | Short term (≤ 2 years) |

| Rising incidence of vaginal dryness | +1.5% | North America, Europe, Japan | Long term (≥ 4 years) |

| Demand for clean-label plant formulas | +1.2% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Hybrid formulations enable toy compatibility | +0.9% | Global | Short term (≤ 2 years) |

| Prescription integration via tele-health | +0.6% | North America, select European markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Destigmatization Of Sexual-Wellness Products

Pharmacy chains now display lubricants alongside menstrual care and contraceptives, a placement shift that elevates price points by 15-20% while trimming aisle embarrassment. CVS Health moved sexual-wellness SKUs to front-of-store wellness bays across roughly 6,700 outlets in January 2025 and paired the change with same-day delivery options that compress last-mile friction. Flexible spending and health savings accounts increasingly reimburse lubricants when physicians document therapeutic intent, expanding the market ceiling for menopause management. Walgreens’ March 2025 privatization sharpened its focus on higher-margin wellness categories, reinforcing shelf space for lubricants and related devices.[1]Greg Sleter, “Walgreens Sharpening Focus on Private Label,” Store Brands, storebrands.comAlthough in-store traffic rises, lingering consumer discomfort means much of the incremental demand still funnels online, where basket anonymity remains a core purchase trigger.

Explosive E-Commerce Penetration

Digitally native brands shave geographic barriers, normalize sexual-wellness shopping in culturally conservative locales, and leverage data-driven merchandising. China’s top marketplaces reported double-digit growth in sexual-wellness gross merchandise value during the 2024 Double 11 festival, well ahead of overall site averages. Maude scaled from launch to USD 10–20 million revenue by 2024 and now serves 33 countries through Shopify storefronts augmented by Sephora and Nordstrom shop-in-shop exposure. Subscription plans that mail quarterly refills at a 10-15% discount amplify retention in price-sensitive Asian markets by eliminating stock-out risk. While online growth softens the 41.77% brick-and-mortar share, platform governance gaps on counterfeits remain a gating factor for premium labels.

Rising Incidence Of Vaginal Dryness With Aging

Genitourinary syndrome of menopause affects roughly half of postmenopausal women, yet only one quarter seek intervention, leaving an addressable but under-treated pool.[2]Karen Carlson, “Genitourinary Syndrome of Menopause,” StatPearls Publishing, ncbi.nlm.nih.govProfessional societies urge non-hormonal lubricants as first-line therapy due to minimal systemic exposure. Tele-health providers such as Alloy bundle lubricants with estradiol cream in monthly kits, raising margins to 30-40% and boosting adherence. Japan’s super-aging demographic underscores the upside: residents aged 65 and older crossed 29.1% of population in 2024, and government wellness drives are chipping away at treatment reluctance.

Demand For Clean-Label, Plant-Derived Lubricants

Consumers increasingly read ingredient panels and reject petrochemical carriers. Good Clean Love reformulated its entire lineup with organic aloe, agar, and xanthan gum, winning USDA Organic and NSF seals that allow 20-30% shelf premiums. In September 2023, BioFilm Inc. launched ASTROGLIDE Lube Plus, a lubricant offering the same long-lasting performance as ASTROGLIDE's current products, with added intimate health benefits. Made with plant-based aphrodisiacs and adaptogens like Watermelon Extract, Hemp, Ashwagandha, and Menthol, it enhances sexual desire, performance, satisfaction, and relaxation.[3]BioFilm Inc., “Astroglide Introduces New Lube Plus Line of Lubricants With Added Benefits,” PR Newswire, prnewswire.com The YES Company secured EU Organic certification, which accelerated adoption in United Kingdom National Health Service clinics. Clean-label claims dovetail with ISO 10993 biocompatibility requirements, often shortening FDA review by minimizing irritant risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Allergic-reaction and irritation concerns | -1.2% | Global, heightened scrutiny in North America and EU | Short term (≤ 2 years) |

| Stringent medical-device regulatory pathway | -0.9% | North America, EU, Japan | Medium term (2-4 years) |

| Counterfeit products on online marketplaces | -0.7% | Asia-Pacific, spillover to global e-commerce | Short term (≤ 2 years) |

| Polyethylene glycol price volatility | -0.5% | Global, supply centered in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Allergic-Reaction And Irritation Concerns

A 2024 review showed 70% of Amazon’s top 50 lubricants contained at least one allergen, with propylene glycol leading at 38% presence. FDA MAUDE records from 2023-2025 link these ingredients to contact dermatitis and urinary-tract infections, prompting cautious physician recommendations. Reformulation toward hydroxyethylcellulose or aloe vera raises raw material outlays by up to 20%, squeezing margins for budget brands.

Stringent Medical-Device Regulatory Pathway

The FDA classifies personal lubricants as Class II devices, compelling 510(k) submission, ISO 10993 biocompatibility studies, and sometimes clinical testing, which jointly add USD 50,000–150,000 and 12-18 months to launch cycles. The EU Medical Device Regulation and Japan’s PMDA maintain parallel rigor, favoring incumbents that amortize the expense across broad SKU ranges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hybrid Formulations Capture Premiumization

Water-based lubricants controlled 69.45% of the personal lubricants market share in 2025, yet the sub-segment posted slower growth than the personal lubricants market average. Hybrid and specialty blends are poised to record an 11.67% CAGR to 2031 as consumers seek pH-balanced and fertility-friendly labels. Silicone-based offerings, while smaller in volume, secure above-average margins due to superior glide and hypoallergenic profiles. The personal lubricants market size for hybrid lines is projected to expand more than USD 350 million between 2026 and 2031. Specialty fertility lubricants obtained FDA 510(k) clearance and help preserve sperm motility, positioning them for physician recommendation during conception planning.

Hybrid growth also traces to rising toy compatibility. Pure silicone products degrade silicone toys, but water-silicone emulsions overcome that barrier, meeting ISO 4074 condom safety norms and ASTM D7661 toy standards simultaneously. Brands that patent low-osmolality recipes gain defensible differentiation. Coconut-oil derivatives supply clean-label cues yet must confront latex incompatibility, limiting mainstream uptake.

By Distribution Channel: E-Commerce Disrupts Pharmacy Incumbency

Drug stores and pharmacies retained 41.77% of 2025 revenue, but the personal lubricants market size contribution from e-commerce is expanding fastest, set to deliver a 12.39% CAGR over the outlook. Inventory breadth, anonymity, and subscription replenishment underpin digital traction. CVS Health combats share leakage with omnichannel fulfillment and curated front-of-store merchandising. Walgreens’ store rationalization signaled structural shifts, freeing capital to enhance higher-margin wellness aisles. Specialty sexual-wellness boutiques carve premium experiences in urban corridors, yet most units operate inventory-light showrooms that push shoppers online after trial. Counterfeiting on high-traffic marketplaces threatens continued acceleration, and stricter seller verification could temper headline growth.

By Utility/Application: Therapeutic Use Gains Clinical Validation

Sexual wellness comprised 86.82% of demand in 2025, yet therapeutic utility for vaginal dryness and dyspareunia is scaling at an 11.43% CAGR to 2031. The North American Menopause Society endorses lubricants as first-line therapy, placing them ahead of systemic hormonal approaches for many cases. Tele-health channels fast-track adoption by embedding lubricants into standardized care kits, thereby reaching patients previously deterred by pharmacy checkout. Assisted reproduction support remains under 3% of volume but enjoys rapid lift due to FDA-cleared sperm-friendly formulas. The personal lubricants market size for fertility-oriented SKUs could more than double by 2031 if insurers extend coverage for over-the-counter products prescribed in conception protocols.

By End-User: Non-Binary Segment Reflects Inclusive Design

Women commanded 53.58% of global volume in 2025, yet non-binary and LGBTQ+ consumers are the fastest climbers, advancing 10.46% annually. Inclusive packaging by Maude and gender-neutral tone from Good Clean Love resonate with Gen Z and Millennial shoppers who reject heteronormative positioning. Recommendation algorithms further blur gender lines, surfacing products according to user behavior instead of identity assumptions. Clinical trials rarely include transgender or non-binary cohorts, creating evidence gaps that could slow uptake if not addressed by future research. Nevertheless, sustained marketing investment and broader pronoun visibility keep momentum on an upward glide path.

Geography Analysis

North America held 38.61% of worldwide value in 2025, supported by pharmacy normalization, tele-health integration, and the ability to pay with FSA/HSA funds. CVS Health’s same-day delivery rollout bolsters convenience, while FDA Class II hurdles deter fragmented entrant waves, shielding established brands from immediate price erosion. Canada mirrors U.S. regulatory practice, whereas Mexico’s demand remains constrained by urban-centric availability.

Asia-Pacific is on track for a 10.62% CAGR through 2031, the highest among major regions. Cross-border e-commerce and domestic platforms accelerate category discovery in China and India, where discreet shipping overcomes cultural sensitivities. Double 11 festival tallies show sexual-wellness baskets rising faster than total platform sales. Japan’s sizable elderly base and rising menopause awareness drive therapeutic uptake. India’s shift to remove sexual-wellness goods from “obscene” classifications has opened formal retail channels and fueled domestic brand expansion.

Europe accounted for roughly 23% of 2025 sales, underpinned by EU MDR harmonization and dense pharmacy networks. Clean-label oil-based offerings from the YES Company gained NHS placement, giving institutional credibility to plant-derived claims. German pharmacists proactively recommend lubricants to menopausal clients, while French prestige retail houses stock premium SKUs alongside beauty staples. The Middle East and Africa combined remain below 10% share due to restrictive norms and low digital penetration, though South Africa’s HIV-prevention drives employ lubricants as risk-reduction tools. South America, led by Brazil, faces counterfeit infiltration but benefits from price-competitive domestic producers.

Competitive Landscape

Market concentration is moderate. Reckitt Benckiser and Church & Dwight control an estimated 35-40% share through entrenched pharmacy shelf rights and multi-platform campaigns. Reckitt’s 2024 Durex Naturals launch capitalizes on organic narratives, while K-Y rolled out Yours+Mine dual dispensers for partner enjoyment. Church & Dwight extended the Trojan umbrella with Bareskin Raw lubricants that cross-sell next to ultra-thin condoms. Ansell’s SKYN line pushes hypoallergenic positioning that aligns with latex-free condom equity.

Direct-to-consumer insurgents shift value toward online baskets. Maude leverages clean aesthetics and subscription logistics to win premium cohorts and now co-retails through Sephora, widening offline awareness. Fertility specialists BioGenesis, Natalist, and Pre-Seed exploit FDA 510(k) clearance to occupy a clinically endorsed niche that incumbents had overlooked. Lovehoney bundles lubricants with toys, lifting average order values by up to 20%. On the defensive side, counterfeit seizures in Singapore highlight ongoing brand protection gaps and reinforce the need for serialized packaging.

Personal Lubricants Industry Leaders

LifeStyles Healthcare Pte Ltd

Reckitt Benckiser Group plc

BioFilm Inc

Church & Dwight Co. Inc.

Trigg Laboratories Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: PH-D Feminine Health introduced Femme Glide, a water-based lubricant infused with organic aloe, vitamin E, and hyaluronic acid for enhanced hydration.

- February 2025: Durex launched the “Afterglow” campaign to position lubricant use as everyday self-care.

- January 2025: Peptonic Medical debuted VagiVital Active Glide, earning strong consumer feedback on soothing performance.

- January 2025: Americhem unveiled EcoLube MD, a PFAS-free internal lubricating compound engineered for medical-device applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the personal lubricants market as all over-the-counter liquids, gels, creams, sprays, and hybrid formats applied to genital skin or sex toys to ease friction and enhance comfort during sexual activity or for medically indicated vaginal dryness. According to Mordor Intelligence, the valuation covers branded and private-label products sold through retail pharmacies, mass-merchandisers, specialty stores, and e-commerce in 17 major countries, stated in USD at manufacturer selling price.

Scope exclusion: prescription-only topical estrogen creams and procedure-grade surgical lubricants are not counted.

Segmentation Overview

- By Product Type

- Water-based

- Silicone-based

- Oil-based

- Hybrid / Specialty

- By Distribution Channel

- Drug Stores & Pharmacies

- E-commerce

- Specialty Sexual-Wellness Stores

- Supermarkets & Hypermarkets

- By Utility / Application

- Sexual Wellness

- Therapeutic (Vaginal Dryness, Dyspareunia)

- Assisted Reproductive Technology Support

- Beauty & Grooming

- By End-user

- Female

- Male

- Non-binary

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview brand managers, contract manufacturers, gynecologists, and pharmacy buyers across North America, Europe, and Asia-Pacific. These conversations validate retail pricing spreads, water-based versus silicone uptake, and emerging medical-grade demand, letting us fine-tune elasticity and channel weights identified in secondary data.

Desk Research

We begin by mapping the demand pool with open datasets such as the WHO Global Survey on Sexual Health, the U.S. CDC National Survey of Family Growth, Eurostat population aging tables, and UN Comtrade trade codes for HS 300670 (gel preparations). Supplementary insight comes from trade associations like the American Sexual Health Alliance, FDA 510(k) device clearances, and investor filings retrieved through D&B Hoovers and Dow Jones Factiva. These sources reveal user prevalence, regulatory shifts, import flows, and typical wholesale price bands that anchor our starting estimates. The sources listed are illustrative; many additional public and paid references inform the desk analysis.

Market-Sizing & Forecasting

A top-down prevalence-to-demand model converts adult population cohorts experiencing dryness or seeking pleasure enhancement into unit consumption, which is then priced with regional average selling prices. Select bottom-up checks, supplier shipment roll-ups and sampled e-commerce sales, help align totals. Key variables include diagnosed vaginal dryness incidence, condom usage rates, e-commerce share of sexual wellness, average price differentials by formulation, and regulatory reclassifications that expand OTC positioning. Multivariate regression with price, aging index, and broadband penetration underpins five-year forecasts, while scenario analysis gauges adoption of natural formulations.

Data Validation & Update Cycle

Outputs pass a three-layer variance screen, peer review, and senior analyst sign-off. Models refresh every twelve months, with interim updates triggered by material events such as major FDA reclassification or double-digit price swings. Before report release, an analyst re-runs the latest data series to ensure clients receive up-to-date figures.

Why Mordor's Personal Lubricants Baseline Carries More Weight

Published estimates often differ; scope choices, pricing assumptions, and refresh frequency create wide gaps.

Key gap drivers include whether in-clinic procedure gels or prescription emulsions are folded in, the aggressiveness of e-commerce growth curves, and currency conversions frozen at outdated exchange rates. Mordor's base excludes prescription creams, applies live IMF rates, and is refreshed annually, whereas other publishers sometimes project uninterrupted double-digit growth from 2020 baselines.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.39 bn (2025) | Mordor Intelligence | - |

| USD 1.59 bn (2024) | Global Consultancy A | Includes prescription estrogen creams; static 2020 FX |

| USD 1.70 bn (2024) | Trade Journal B | Assumes uniform 10% e-commerce price premium worldwide |

In sum, our disciplined scope selection, live variables, and yearly recalibration give decision-makers a balanced, transparent baseline they can trace back to clear assumptions and replicate with confidence.

Key Questions Answered in the Report

What is the current global value of the personal lubricants market?

The market is valued at USD 1.71 billion in 2026.

Which product formulation is growing fastest?

Hybrid and specialty blends are projected to rise at an 11.67% CAGR through 2031.

How quickly is e-commerce expanding in this space?

Online sales are set to climb at a 12.39% CAGR over the forecast horizon.

Why are lubricants gaining medical traction?

Clinical guidelines now recommend non-hormonal lubricants as first-line therapy for vaginal dryness and dyspareunia.

Which region is anticipated to post the strongest growth?

Asia-Pacific is forecast to record a 10.62% CAGR, driven by e-commerce and demographic shifts.

What regulatory hurdle affects new entrants most?

The FDA’s Class II device pathway imposes 12-18 months of testing and up to USD 150,000 in compliance costs.

Page last updated on: