Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

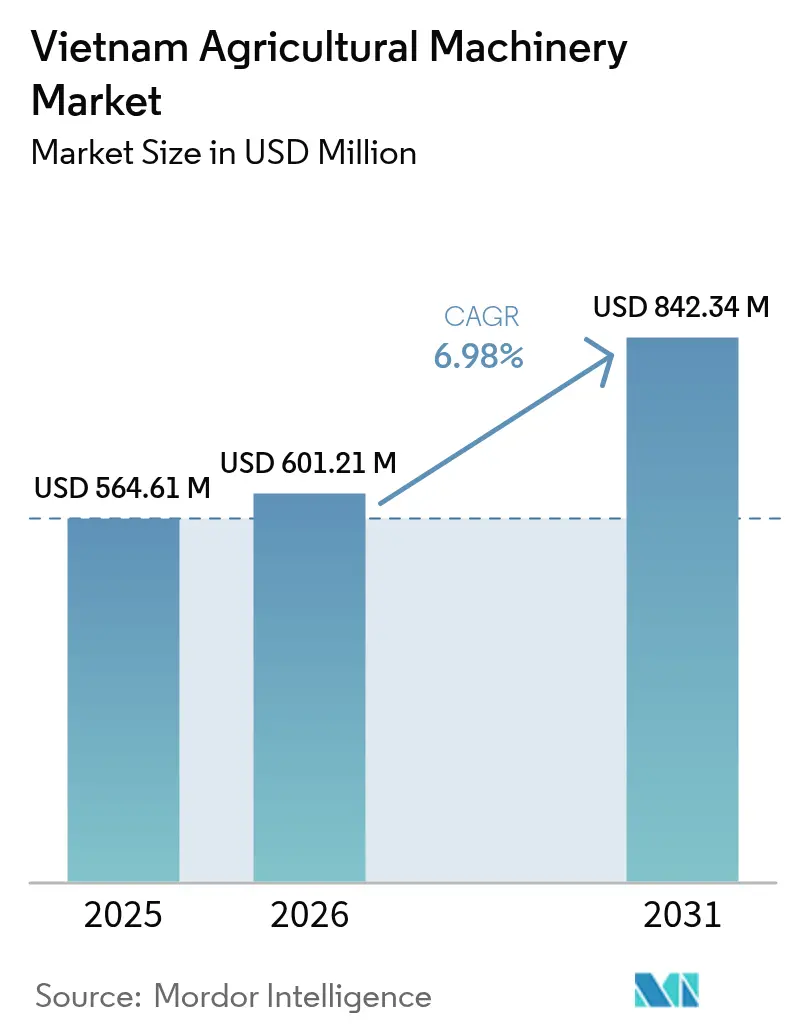

| Base Year Market Size (2025) | USD 564.61 Million |

| Market Size (2026) | USD 601.21 Million |

| Market Size (2031) | USD 842.34 Million |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

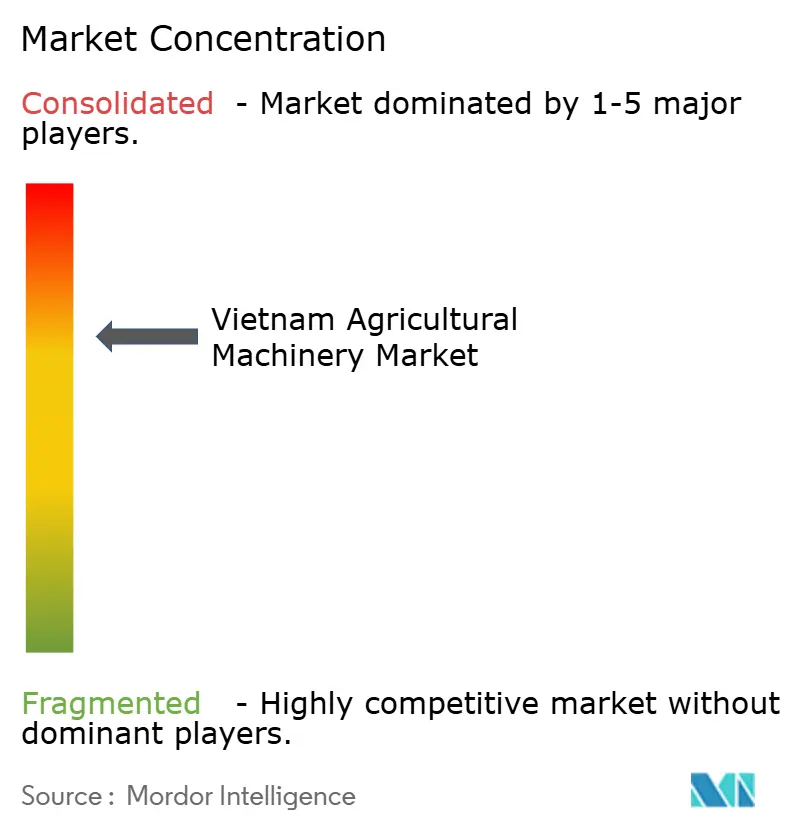

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Agricultural Machinery Market Analysis by Mordor Intelligence

The Vietnam agricultural machinery market size was valued at USD 564.61 million in 2025 and is estimated to grow from USD 601.21 million in 2026 to USD 842.34 million by 2031, at a CAGR of 6.98% during the forecast period (2026-2031). Labor scarcity, policy-linked credit incentives, and export-driven liquidity are shortening the payback period on new machines, even though the median farm still works less than one hectare. The push to certify one million hectares of low-emission rice is accelerating demand for telematics-enabled tractors, combines, and drones that can generate auditable field data. Rapid cost declines in drone-spraying services, together with provincial subsidies covering up to 50% of precision seeders, are tilting smallholders toward fee-for-service rather than outright ownership. Meanwhile, joint ventures between domestic assemblers and South Korean or European suppliers are localizing powertrains and raising domestic value content, creating mid-tier options that split the difference between premium Japanese brands and low-cost Chinese imports.

Key Report Takeaways

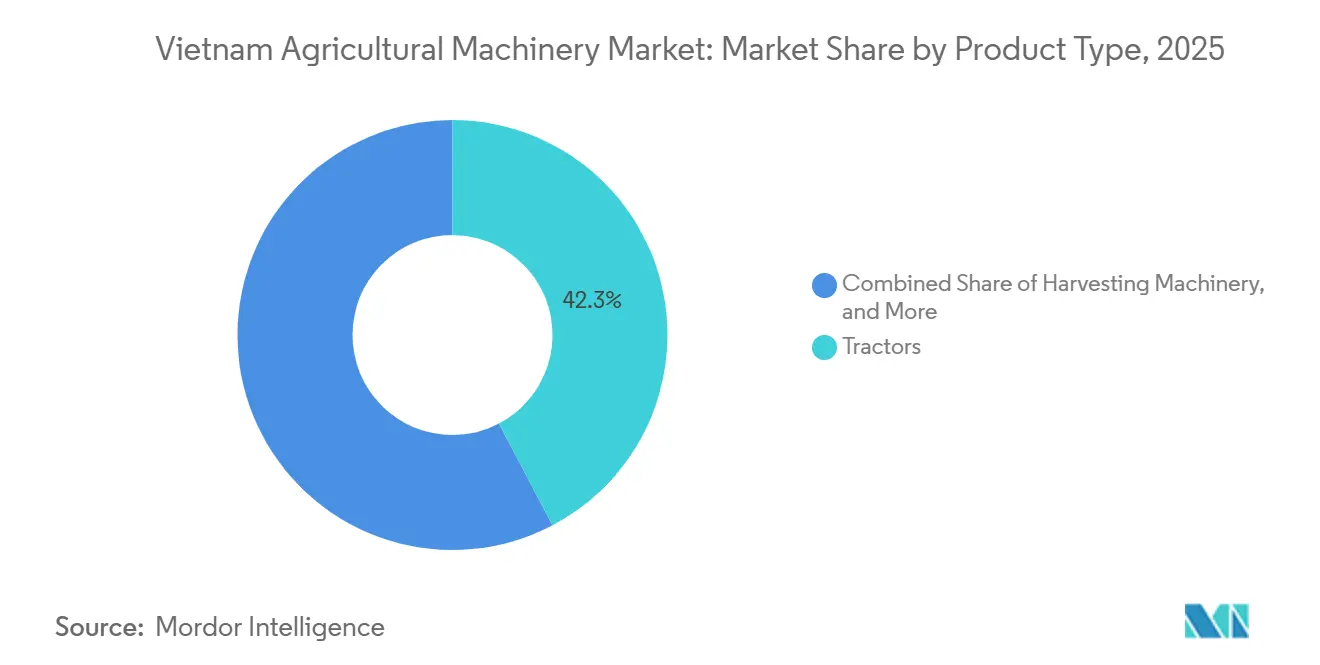

- By product type, tractors captured 42.3% of the Vietnam agricultural machinery market share in 2025, while spraying and drones are projected to expand at a 7.8% CAGR through 2031.

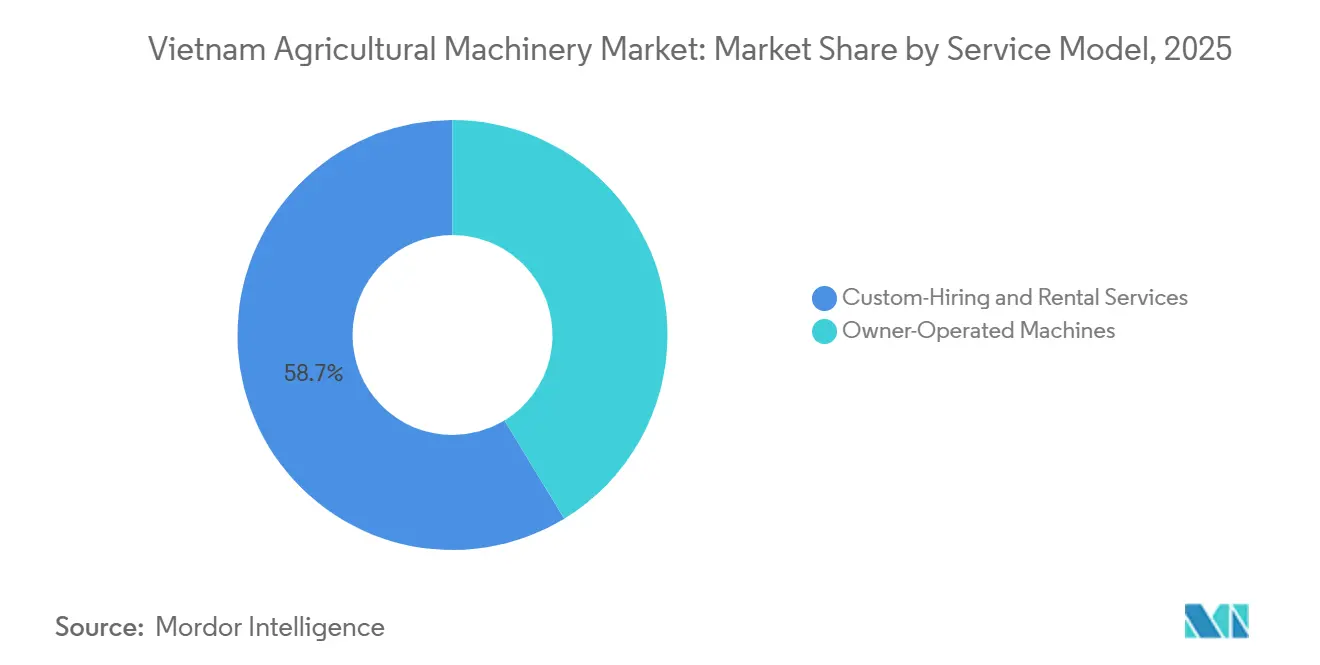

- By service model, custom-hiring and rental services accounted for 58.7% of the Vietnam agricultural machinery market size in 2025 and are forecast to grow at a 6.8% CAGR to 2031.

- The Kubota Corporation, Yanmar Holdings Co., Ltd., Vietnam Engine and Agricultural Machinery Corp (VEAM), Truong Hai Group Corporation (THACO), and Deere & Company (TTC Bien Hoa) accounted for significant market revenue in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking agricultural labor pool | +1.1% | National, strongest in Mekong and Red River Deltas | Medium term (2-4 years) |

| Expansion of government-subsidized mechanization credit lines | +1.0% | National, early uptake in Can Tho, An Giang, and Dong Thap | Short term (≤2 years) |

| Surge in rice-export cashflows funding machine upgrades | +1.1% | Mekong Delta provinces | Short term (≤2 years) |

| Rapid drop in drone-spraying service costs | +0.8% | National, dense in Red River and Mekong Deltas | Medium term (2-4 years) |

| Domestic original equipment manufacturer localization drive | +0.6% | Central provinces, and spillover to Mekong Delta | Long term (≥4 years) |

| On-farm data monetization platforms boosting telematics demand | +0.4% | Mekong Delta and Central Highlands | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Shrinking Agricultural Labor Pool

In 2025, the agricultural workforce in Vietnam accounted for 51.94% of the rural labor force, a 4.3% decrease from earlier benchmarks. The Mekong Delta witnessed the sharpest decline[1]Source: General Statistics Office of Vietnam, “Results of the 2024 Rural, Agricultural and Fishery Census,” gso.gov.vn. Out-migration, climate shocks, and an aging farmer base are forcing growers to replace manual labor with machinery, yet the pool of skilled operators able to handle Global Positioning System-guided combines is tightening. Custom-hiring services now dominate harvest windows, but operator wages spike during peak periods, pushing interest in autonomous and semi-autonomous equipment. Kubota’s January 2025 technical bulletin confirms research on wet-field automation tailored for monsoon conditions. As labor costs keep rising, mechanization becomes less an option and more a survival strategy.

Expansion of Government-Subsidized Mechanization Credit Lines

The July 2024 banking circular opened financial leasing for agricultural machinery, complementing a green credit portfolio that reached 730 trillion Vietnamese dong (approximately USD 29.5 billion) by late 2024[2]Source: State Bank of Vietnam, “Circular 26/2024/TT-NHNN on Financial Leasing for Agricultural Equipment,” sbv.gov.vn. Provincial programs in Can Tho, An Giang, and Dong Thap then layered subsidies covering up to half the cost of transplanters and precision seeders. World Bank capacity-building projects further reduce lenders' risk by anchoring public-private partnerships in value chains. Cooperative models, such as Vinh Cuong in Ca Mau, report per-hectare cost savings of USD 6 to USD 8 because the credit pipeline lets them scale fleets quickly. Domestic assemblers, pricing 10% to 20% below imports, benefit disproportionately because subsidies make their lower ticket prices even more attractive to smallholders.

Surge in Rice-Export Cashflows Funding Machine Upgrades

Rice export earnings hit USD 5.7 billion in 2024 despite lower volumes, channeling fresh liquidity into the Vietnam agricultural machinery market[3]Source: Vietnam Customs, “Vietnam Rice Export Statistics 2024,” customs.gov.vn. Premium fragrant varieties lifted margins, so growers in An Giang, Kien Giang, and Dong Thap replaced aging combines and invested in drone fleets. The one-million-hectare low-emission rice mandate links compliance to carbon-credit revenue, so machines that record geo-referenced field data are given priority on buyers’ shortlists. Alternate wetting and drying irrigation needs sensor-equipped pumps, further pushing telematics adoption. As premium rice attracts higher prices, the upgrade loop becomes self-reinforcing.

On-Farm Data Monetization Platforms Boosting Telematics Demand

The October 2024 launch of the RiceMoRe and FarMoRe platforms introduced geo-referenced monitoring and carbon-credit verification specifically for low-emission rice. These platforms aim to enhance sustainability by providing tools for precise monitoring and incentivizing environmentally friendly practices. In 2025, TTC AgriS’s AgriBrain platform will incorporate blockchain traceability and artificial intelligence analytics, enabling farmers to document yield gains of 15%-30% and monetize methane-reduction credits. This platform is anticipated to streamline data management and improve decision-making for farmers. The Ministry of Agriculture and Environment aims to connect 1 million hectares of rice fields by 2026, with tractors and combines transmitting real-time data. This initiative is anticipated to significantly enhance operational efficiency and data-driven farming practices. Field trials in Hai Phong indicate that 45% of large farms already own drones, showcasing the growing adoption of advanced technologies in agriculture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Highly fragmented farm sizes | -1.1% | National, worst in Red River Delta | Long term (≥4 years) |

| Low rural electrification hindering electric tractors | -0.7% | Remote provinces, poorest quintile households | Long term (≥4 years) |

| Rising cyber-security threats to connected machinery | -0.4% | National, densest where Internet of Things adoption is high | Medium term (2-4 years) |

| Skilled-operator shortage inflating service costs | -0.9% | National, acute in Mekong Delta and Central Highlands | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Highly Fragmented Farm Sizes

Vietnam has many farms spread across numerous parcels, with an average farm size of less than one hectare. Among these, the majority operate on small plots. This significant fragmentation limits economies of scale, as transporting machinery like combine harvesters to small plots diminishes efficiency gains. Additionally, irregularly shaped fields and narrow paths hinder the use of larger agricultural implements. Land laws impose restrictions on consolidation, limiting holdings in the Mekong Delta and other regions. Unless ultra-compact machinery is developed or land tenure regulations are revised, this structural limitation is projected to continue hindering the growth of the Vietnam agricultural machinery market.

Rising Cyber-Security Threats to Connected Machinery

Surveys reveal that many farm households lack access to information on digital agriculture, while others face financial constraints, underscoring concerns related to data sovereignty. As agricultural machinery uploads crop data to cloud-based dashboards, questions regarding ownership of yield data are becoming more prominent. The newly established Ministry of Agriculture and Environment plans to distribute satellite and sensor data across 1 million hectares, potentially increasing the risk of data breaches. Limited rural broadband access further complicates software updates, and no domestic original equipment manufacturers currently offer secure boot or multi-factor authentication as standard features. A successful cyberattack could disrupt machinery fleets during harvest, positioning cybersecurity as an increasingly significant cost factor.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tractors Anchor Mechanization Yet Drones Advance

Tractors held 42.3% of the Vietnam agricultural machinery market share in 2025, reflecting their central role in tillage across 7.7 million hectares of paddy. Sub-35-horsepower four-wheel-drive units dominate because they navigate narrow bunds and wet fields. The Vietnam agricultural machinery market for tractors is projected to grow in step with credit lines that cut upfront costs and localization that trims prices. Kubota Corporation and Yanmar Holdings Co., Ltd. are refining 20-40 horsepower models with autonomous features to bridge the labor gap, while domestic assemblers are chasing the sub-USD 10,000 tier. Farmers replacing two-wheel units favor compact four-wheel models that can double as transport, widening the addressable base.

Spraying and drones, though only a mid-single-digit slice of revenue today, will post the fastest growth at a 7.8% CAGR to 2031. Unit cost parity with manual spraying and up to 75% labor savings underpin that expansion. The Vietnam agricultural machinery market size for drones could accelerate further if pilot-licensing rules standardize safety and unlock insurance coverage. Registrations already top 2,800 units, and Real-time Robotics undercuts imports by 20%-30%. Because drones capture real-time crop imagery, they dovetail with carbon-credit verification, giving adopters a second revenue stream.

By Service Model: Custom-Hiring and Rental Services Dominates but Ownership Persists

Custom-hiring and rental services accounted for 58.7% of the Vietnam agricultural machinery market in 2025 and are the fastest-growing service with a CAGR of 6.8% during 2026-2031. The model suits a landscape where two-thirds of farms till under half a hectare and cannot amortize large assets. Lease-to-own financing, legalized in 2024, enables service providers to update their fleets more frequently, ensuring that newer machinery becomes accessible to smallholders. Cooperatives like Vinh Cuong demonstrate that shared resources can reduce per-hectare costs, making mechanization feasible even for subsistence farmers.

Owner-operated machines remain a significant area of expenditure, as 150,000 commercial farms, averaging six hectares each, surpass break-even utilization levels. Participation in carbon-credit programs is encouraging some growers to consider ownership due to the need for uninterrupted access to telematics logs. If verification platforms enable renters to access machine data seamlessly, custom hiring is likely to remain dominant. In the absence of such access, premium-export farmers may shift back toward owning specialized equipment, particularly drones equipped with integrated sensors.

Geography Analysis

The Mekong Delta remains the powerhouse of the Vietnam agricultural machinery market, having reached nearly full mechanized tillage by 2023 and processing 98% of rice with combines. Export earnings delivered sufficient capital for combine replacements and drone fleets. The region is also at the forefront of implementing low-emission rice protocols, which mandate telematics logging. Can Tho aims to have hectares under low-emission cultivation, indicating consistent equipment demand despite increasing climate risks.

The Red River Delta has the highest density of custom-hiring outfits, most holdings below 0.5 hectares, and significant labor shortages. Municipal budgets in Hanoi help fund drone purchases, while Hai Phong reports significant drone ownership among large farms. Ultra-compact machinery finds its main buyer base here, and any policy that eases land consolidation would unlock greater demand for tractor horsepower.

Central Highlands farms average 1.83 hectares, the largest nationally, and diversify into dairy and beef, so forage machinery sales grow from a low base. Northern uplands, constrained by grid instability, ranked 113th worldwide for electricity quality, remain diesel-reliant and lag in mechanization. Infrastructure gaps mean most electric-tractor pilots will happen in deltas first, widening the regional performance gap until grid upgrades reach mountainous areas.

Competitive Landscape

The Vietnam agricultural machinery market is moderately concentrated, with Kubota Corporation, Yanmar Holdings Co., Ltd., Vietnam Engine and Agricultural Machinery Corp (VEAM), Truong Hai Group Corporation (THACO), and Deere & Company (TTC Bien Hoa) accounting for a major share of the Vietnam agricultural machinery market in 2025. Kubota Corporation and Yanmar Holdings Co., Ltd. dominate the premium tractor and combine market. Their strength lies in nationwide dealer networks and uptime-focused service.

Domestic assemblers are scaling. Vietnam Engine and Agricultural Machinery Corp (VEAM) invests in robotic welding to raise quality and aims to lift tractor share by 2026. Truong Hai Group Corporation (THACO)’s joint venture with LS Mtron Co., Ltd. pursues 50% local content, aligning with tariff preferences. Kim Long Motor’s new engine plant reduces reliance on imported powertrains and enables exports to Cambodia and Laos.

Strategy now bifurcates: premium players race toward autonomy and data analytics, while mid-tier brands compete on price and localized after-sales. Real-time Robotics cuts drone costs while offering Vietnamese-language support. Agritech startups aggregate cross-brand machine data, reducing lock-in. White-space exists in ultra-compact robotic units for sub-hectare plots and in integrated carbon-credit platforms, areas yet to be tapped by incumbents.

Vietnam Agricultural Machinery Industry Leaders

Kubota Corporation

Vietnam Engine & Agricultural Machinery Corp (VEAM)

Yanmar Holdings Co., Ltd.

Truong Hai Group Corporation (THACO)

Deere & Company (TTC Bien Hoa)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Kim Long Motor Hue Joint Stock Company inaugurated its Yuchai engine manufacturing plant in Hue City, central Vietnam, and produced the first Yuchai engine, marking a significant milestone in its strategy to develop core technologies in Vietnam's engine manufacturing industry. This is the first facility in Vietnam with a modern production line capable of producing engines that meet international standards, serving the agricultural sector.

- March 2025: Enviacon International introduced German agricultural technology to Vietnam through strategic market exploration trips and high-level delegations. This initiative is part of an Export Promotion Program supported by the German Federal Ministry of Food and Agriculture. In collaboration with Source of Asia (SOA), DLG Markets GmbH, and VDMA Agricultural Machinery, Enviacon International organized a delegation of prominent German machinery companies to Vietnam.

- February 2025: Truong Hai Group Corporation (THACO) is committed to investing USD 1 billion to develop a 786-hectare industrial park in Binh Duong, dedicated to mechanical manufacturing, including agricultural machinery. This project aims to enhance domestic production capacity, decrease import dependency, and generate 32,000 jobs, strengthening Vietnam's agricultural equipment manufacturing capabilities.

Vietnam Agricultural Machinery Market Report Scope

Agricultural machinery refers to mechanical structures and devices used in farming and other agricultural operations. The Vietnam Agricultural Machinery Market Report is Segmented by Product Type (Tractors, Planting and Seeding Machinery, Harvesting Machinery, Spraying and Drones, Haying and Forage Machinery, and Other Product Types), and by Service Model (Owner-Operated Machines and Custom-Hiring and Rental Services). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Tractors | By Engine Power | Less than 15 HP |

| 15 to 30 HP | ||

| 31 to 45 HP | ||

| 46-75 HP | ||

| More than 75 HP | ||

| By Drive Type | Two-Wheel Drive | |

| Four-Wheel Drive | ||

| Harvesting Machinery | ||

| Planting and Seeding Machinery | ||

| Spraying and Drones | ||

| Haying and Forage Machinery | ||

| Other Product Types | ||

By Service Model

| Owner-Operated Machines |

| Custom-Hiring and Rental Services |

| By Product Type | Tractors | By Engine Power | Less than 15 HP |

| 15 to 30 HP | |||

| 31 to 45 HP | |||

| 46-75 HP | |||

| More than 75 HP | |||

| By Drive Type | Two-Wheel Drive | ||

| Four-Wheel Drive | |||

| Harvesting Machinery | |||

| Planting and Seeding Machinery | |||

| Spraying and Drones | |||

| Haying and Forage Machinery | |||

| Other Product Types | |||

| By Service Model | Owner-Operated Machines | ||

| Custom-Hiring and Rental Services | |||

Key Questions Answered in the Report

How fast will mechanization spending grow in Vietnam?

The Vietnam agricultural machinery market is projected to expand at a 6.98% compound annual growth rate from 2026 to 2031.

Which product category holds the highest sales share?

Tractors led with 42.3% of Vietnam agricultural machinery market share in 2025.

Why is custom hiring so common among Vietnamese farmers?

Two-thirds of farms cultivate less than 0.5 hectare, making rental services more economical than owning machines.

What is driving demand for agricultural drones?

Service costs have fallen to USD 4-USD 7 per hectare while labor savings reach up to 75%, making drones cost competitive.

How does government policy support machinery purchases?

A 2024 banking circular permits lease financing and provincial programs subsidize up to 50% of precision equipment costs.

Which regions generate the most machinery demand?

The Mekong Delta and Red River Delta dominate due to rice export orientation and high labor shortages.

Page last updated on: