Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

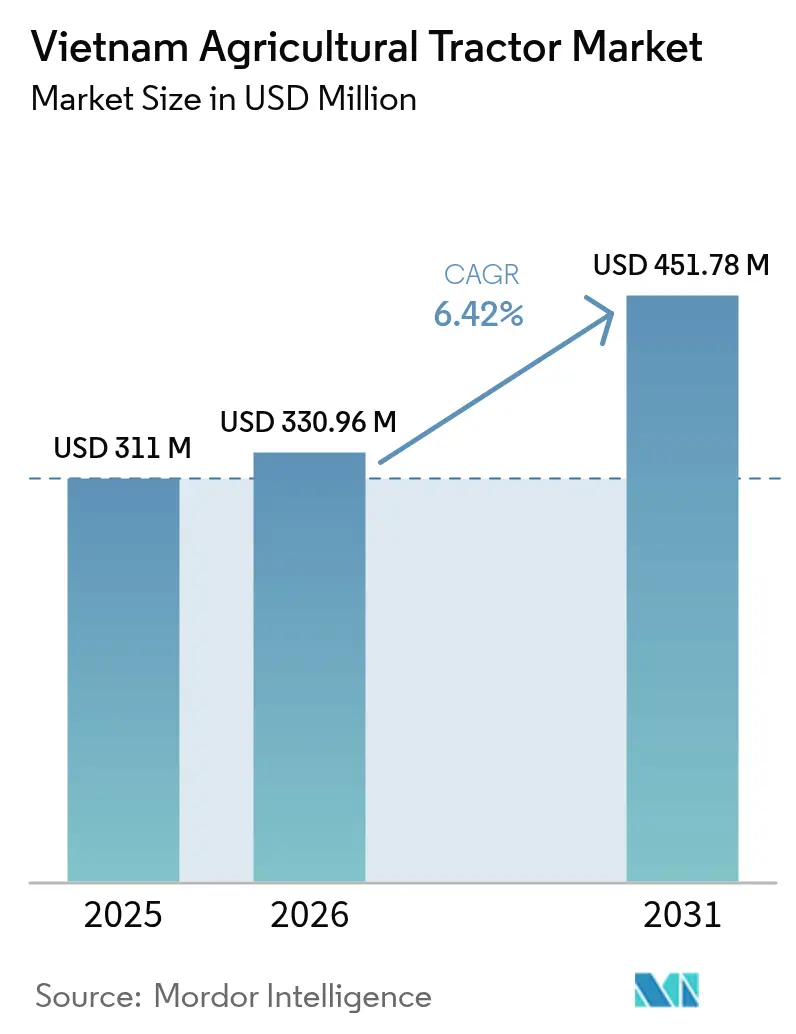

| Base Year Market Size (2025) | USD 311.0 Million |

| Market Size (2026) | USD 330.96 Million |

| Market Size (2031) | USD 451.78 Million |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

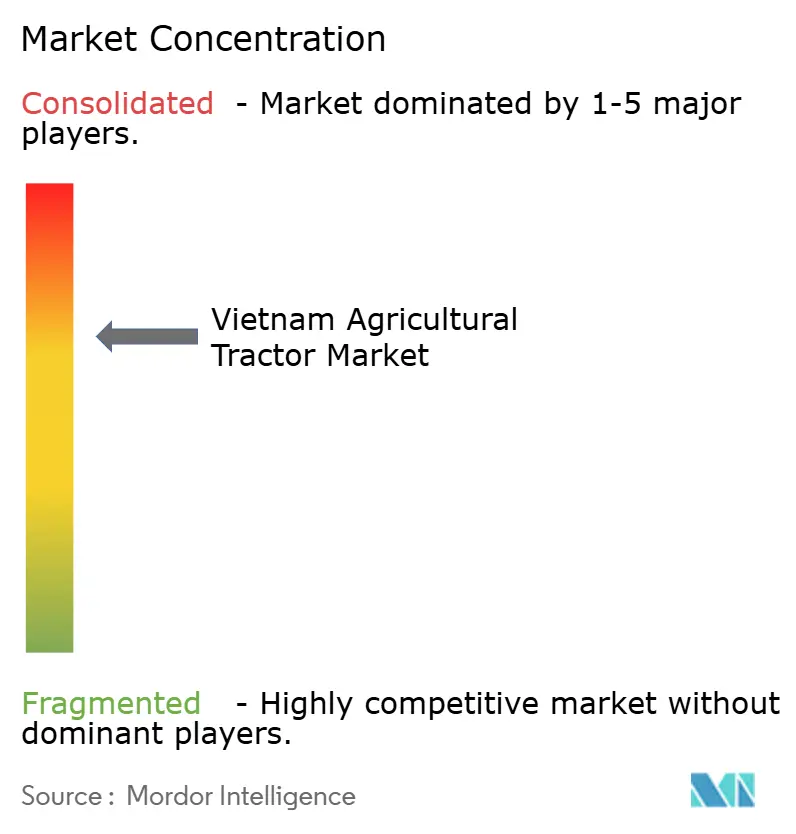

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Agricultural Tractor Market Analysis by Mordor Intelligence

The Vietnam agricultural tractor market size is expected to grow from USD 311.0 million in 2025 to USD 330.96 million in 2026 and is forecast to reach USD 451.78 million by 2031 at 6.42% CAGR over 2026-2031. This uptrend mirrors the country’s policy-led march toward agricultural mechanization, the reorganization of the Ministry of Agriculture and Environment, and the surge in low-interest credit lines that lower acquisition costs for farmers.[1]Bộ Nông nghiệp và Môi trường, “Quyết định 681/QĐ-BNNMT,” thuvienphapluat.vn Government Portal, “Socio-economic development plan 2021-2025,” vietnam.gov.vn Văn phòng Chính phủ, “Công văn 3399/VPCP-NN,” thuvienphapluat.vn Rural labor out-migration, rising rice export volumes, and escalating demand for precision farming are translating into higher unit sales across power bands, while financing programs stimulate nearer-term purchases. Four-wheel-drive formats dominate because they handle monsoon soil conditions and sloped fields more effectively, but compact two-wheel models still appeal to fragmented farms in the north. Electric and hybrid propulsion remain nascent yet gather pace on the back of a charging roll-out. At the same time, service-based machinery sharing schemes and contract-farming models allow smallholders to access equipment without incurring full ownership costs.

Key Report Takeaways

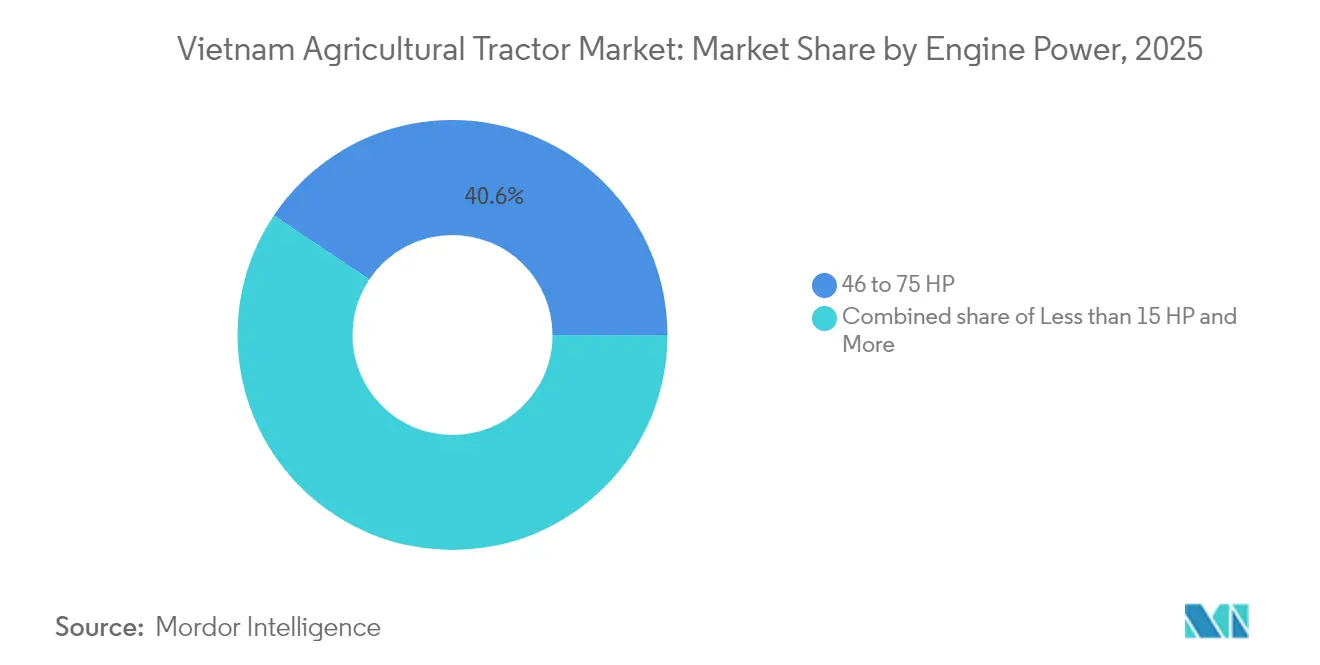

- By engine power, the 46 -75 HP band held 40.62% of the Vietnam agricultural tractor market share in 2025; the 31- 45 HP category is advancing at a 5.74% CAGR to 2031.

- By drive type, four-wheel-drive units accounted for 57.48% of the Vietnam agricultural tractor market size in 2025 and are growing at a 6.43% CAGR through 2031.

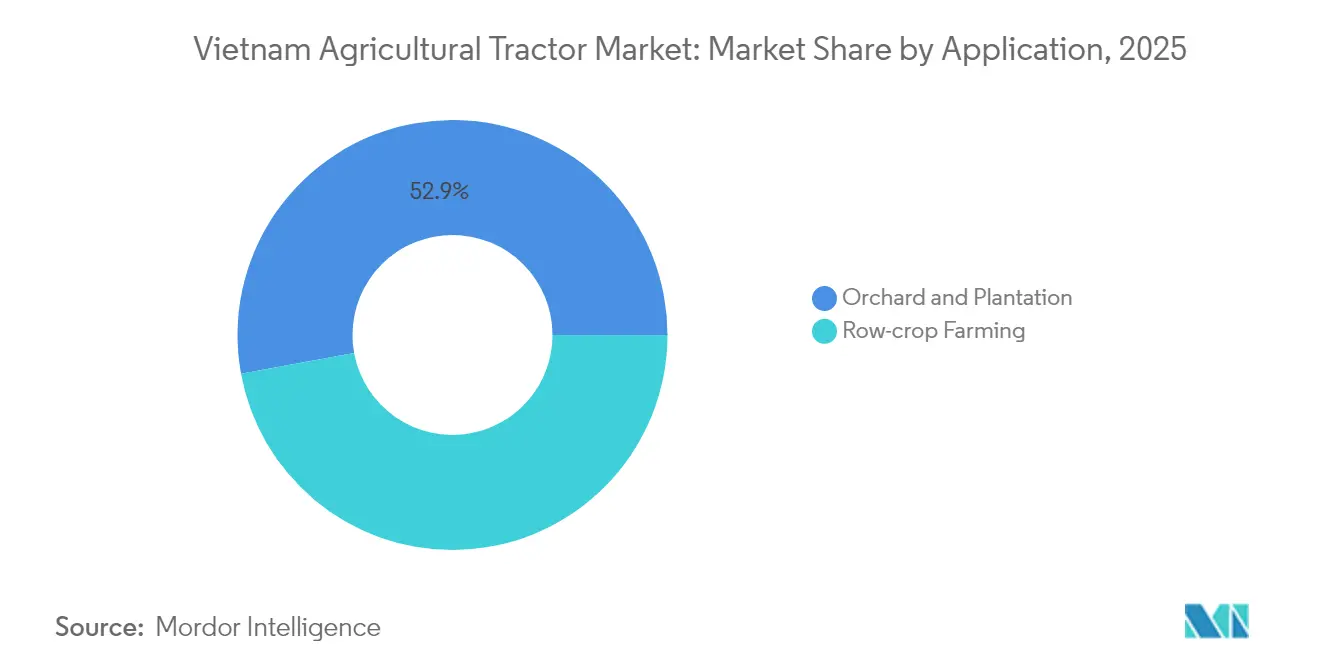

- By application, row-crop farming contributed 47.12% of the Vietnam agricultural tractor market size in 2025, while orchard and plantation use cases post a 6.05% CAGR toward 2031.

- By propulsion, Diesel engines control 92.55% of Vietnam agricultural tractor market share in 2025, and fully electric models are posting a 9.18% CAGR to 2031, outpacing diesel and hybrid alternatives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Agricultural Tractor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Focus on Farm Mechanization | +1.8% | National, with early gains in Mekong Delta, and Red River Delta | Medium term (2-4 years) |

| Surge in Government Mechanization Subsidies | +1.5% | National, concentrated in priority agricultural zones | Short term (≤ 2 years) |

| Growth of Contract-farming Programs | +1.2% | Mekong Delta, Central Highlands, spill-over to Northern regions | Medium term (2-4 years) |

| Expansion of High-value Crop Acreage | +0.9% | Central Highlands, Northern mountains, and coastal provinces | Long term (≥ 4 years) |

| Growing Trade Support for Agricultural Goods | +0.7% | Export-oriented regions and Mekong Delta dominance | Medium term (2-4 years) |

| Emerging Low-interest Agribank Credit Lines | +0.6% | National, with enhanced access in rural cooperatives | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Focus on Farm Mechanization

Labor migration to industrial centers is creating workforce gaps in agriculture, driving farms to adopt mechanization to maintain productivity.[2]Government Portal, “Socio-economic development plan 2021-2025,” vietnam.gov.vn National development plans encourage a shift from manual labor, increasing the need for machinery across rural regions. In coastal areas, machinery services have become an income stream, helping farmers access equipment without ownership costs. Larger plot sizes in fertile regions like the Mekong Delta support mechanized farming adoption. Inspection centers ensure equipment meets safety standards, increasing confidence in machine use and supporting the transition to technology-driven agricultural practices.

Surge in Government Mechanization Subsidies

Government financial initiatives are increasing agricultural machinery adoption through low-interest loans and support for local equipment manufacturers. These subsidies lower farmers' financial burden and encourage investment in productivity-enhancing tools. The programs strengthen domestic parts suppliers, reducing import dependence and shortening delivery times. Performance-based funding ensures subsidized equipment improves crop yields and operational efficiency. This approach modernizes farming practices and strengthens the agricultural supply chain, supporting rural economic development.

Growth of Contract-farming Programs

Contract farming transforms agricultural investment through guaranteed purchase agreements and stable income for growers. These structures make machinery investments more predictable for small-scale farmers. In the Mekong Delta, contract-based rice production with mechanization requirements drives equipment adoption. Cooperative models promote shared equipment use and improve utilization rates. This collaboration increases technology access, reduces individual costs, and supports sustainable community-based farming practices.

Expansion of High-value Crop Acreage

Agricultural policy prioritizes high-value crops over volume production, increasing demand for specialized machinery for crops like coffee and durian. Orchard and hillside plantation farmers invest in tractors with GPS, data logging, and slope-stability features to manage terrain and optimize harvests. Precision agriculture systems improve consistency and quality. This shift reflects the agricultural sector's focus on value-driven farming, where technology enhances profitability and global market competitiveness.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Highly Fragmented Landholding Structure | -1.4% | National, most severe in Northern regions, moderate in Mekong Delta | Long term (≥ 4 years) |

| Volatility in Farm Commodity Prices | -1.1% | Export-dependent regions, Mekong Delta rice, Central Highlands coffee | Medium term (2-4 years) |

| Limited Rural Charging Infrastructure for E-tractors | -0.8% | Rural areas nationwide, infrastructure gaps in remote provinces | Medium term (2-4 years) |

| Shortage of Skilled Farmers | -0.6% | National, acute in mechanized farming regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Highly Fragmented Landholding Structure

Vietnam's agricultural sector is characterized by small, fragmented landholdings, which restrict farmers' ability to invest in machinery due to limited economies of scale. The small plot sizes make individual equipment ownership financially impractical. Land-service providers have emerged as intermediaries, offering shared machinery access. In mountainous areas, steep terrain increases operational costs and limits the use of large machinery. Despite government initiatives for land consolidation to improve mechanization potential, traditional social practices and inheritance laws impede progress, forcing farmers to rely on informal sharing arrangements and community-based solutions.

Limited Rural Charging Infrastructure for E-tractors

The adoption of electric tractors faces obstacles due to insufficient rural charging infrastructure. While national plans include extensive charging station deployment targets, current implementation concentrates on urban areas, leaving agricultural regions underserved. This gap affects the feasibility of electric machinery for farmers who need rapid equipment turnaround during planting and harvesting periods. Despite private sector efforts to expand the charging network, the current infrastructure remains inadequate for supporting intensive agricultural operations. The limited availability of fast-charging stations in rural areas continues to restrict electric tractor adoption, particularly in regions where mechanization is essential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Power: Mid-Range Models Anchor Versatility

The 46-75 HP segment accounts for 40.62% of the 2025 Vietnam agricultural tractor market size, demonstrating its versatility across Vietnamese terrains. These mid-range agricultural tractors effectively handle plowing, harrowing, and transport tasks in rice paddies and upland fields. Their capacity to operate multi-row planters while navigating tight headlands makes them popular among farmers seeking balanced power and maneuverability. Compact 31- 45 HP units show the highest growth at 5.74% CAGR, driven by smaller farm sizes in regions like the Mekong Delta, where cost and agility are primary concerns.

Agricultural tractors under 15 HP maintain their presence in terraced northern plots, while units above 75 HP serve larger contract farms. The industry now incorporates GPS, ISOBUS compatibility, and telemetry in mid-power machines as standard features. These frames readily accommodate precision agriculture upgrades like variable-rate fertilization, and manufacturers focusing on 31-75 HP models for hybridization position themselves for increased volume and margins.

By Drive Type: Four-Wheel Traction Dominates Monsoon Fields

Four-wheel-drive tractors represent 57.48% of the Vietnam agricultural tractor market share in 2025, growing at a 6.43% CAGR. Their prevalence reflects the requirement for reliable traction in water-logged rice paddies and steep coffee estates. These machines reduce slippage, minimize soil compaction, and support heavier implements without stalling essential features in monsoon regions. Two-wheel-drive units remain viable in dry upland areas but decline as financing options improve four-wheel-drive accessibility.

Four-wheel-drive agricultural tractors record 18% more annual operating hours, improving investment returns. Electric variants face engineering challenges due to the increased power requirements of four-wheel systems. While intelligent torque vectoring manages power consumption, a reliable charging infrastructure remains crucial. Manufacturers now focus on power-train efficiency algorithms and traction optimization, competing on fuel or watt-hour consumption per hectare to meet data-driven farming needs.

By Application: Row-Crop Core with Orchard Upside

Row-crop operations, particularly rice cultivation, comprise 47.12% of agricultural tractor usage in Vietnam as of 2025. This segment's importance in food security and exports drives continued mechanization, supporting puddling, transplanting, and harvesting operations. These time-sensitive tasks, governed by monsoon seasons, benefit from mechanization to address labor shortages and maintain crop schedules.

Orchard and plantation applications exhibit 6.05% growth, driven by expanding cultivation of durian, longan, and pepper. The market offers narrow-chassis, high-clearance agricultural tractors with flexible PTO speeds for specialized equipment like pruning saws and mist blowers. As farms adopt drip irrigation and sensor networks, tractors serving as mobile power and data hubs gain importance, reflecting the transition toward precision farming practices.

By Propulsion Technology: Electric Momentum Builds from a Small Base

Diesel engines control 92.55% of the Vietnam agricultural tractor market share in 2025, supported by widespread fuel availability, lower initial costs, and simple maintenance requirements. These units remain essential for mechanized farming, particularly in remote areas lacking alternative fuel infrastructure. Their dependability suits farmers managing strict budgets and challenging field conditions.

The electric segment grows at a 9.18% CAGR, supported by decreasing battery costs and stricter carbon-reduction policies. Hybrid systems provide an intermediate option, offering fuel efficiency and regenerative braking for hydraulic operations. Manufacturers explore swappable battery systems and field-side micro-grids to address range limitations. These advancements indicate progression toward cleaner propulsion technologies, with electric and hybrid models anticipated to expand as infrastructure and policies develop.

Geography Analysis

The Mekong Delta, Vietnam's primary rice-exporting region, drives agricultural tractor demand through intensive crop rotations that require versatile machines for saturated soils and tight planting windows. Infrastructure improvements have increased field reliability, promoting higher tractor usage across seasons. The Red River Delta's proximity to Hanoi's network of dealers and component suppliers provides logistical advantages, reducing downtime and enabling upgrades to advanced models. Farmers in this region are adopting four-wheel-drive units due to better traction and performance in various field conditions.

The Central Highlands focuses on specialty-crop machinery for coffee cultivation, with tractors featuring slope-stability systems to protect root zones on uneven terrain. Sustainability certification programs influence equipment selection, as growers implement precision tools for consistent crop quality. The northern mountainous areas, despite lower overall demand, function as testing grounds for compact electric and hybrid tractors suited for steep terraces and offering reduced torque fluctuations. Coastal provinces utilize their port access for imported attachments and benefit from shared repair infrastructure through industrial cluster initiatives. Vietnam's varied geography creates specific needs across agricultural regions, requiring manufacturers to provide diverse tractor models and support services. Farmers need machines with different power ratings, chassis configurations, and terrain adaptability across saturated deltas and highlands. This diversity influences innovation in design and after-sales support, with suppliers developing solutions for local conditions. Government programs and regional logistics hubs influence purchasing decisions, particularly in export-oriented crop areas. The ability to match equipment to specific agronomic and environmental requirements determines market competitiveness as mechanization increases.

Competitive Landscape

The industry remains moderately concentrated. The Vietnam agricultural tractor market is dominated by several key players, with Kubota Corporation maintaining a strong market position through its extensive dealer network and integrated financing solutions. Truong Hai Group Corporation (THACO) has enhanced its market position by establishing local production facilities and developing strategic partnerships to minimize trade barrier impacts. Deere & Company (TTC Bien Hoa) has increased its market presence by providing precision agriculture solutions and autonomous machinery. These companies maintain their positions through established brand recognition, technical support networks, and product lines that meet Vietnam's diverse agricultural requirements, from rice cultivation to highland farming.

Yanmar Holdings Co., Ltd. and Vietnam Engine & Agricultural Machinery Corp (VEAM) are significant market players, utilizing their manufacturing expertise and regional production facilities. Yanmar specializes in dry-field applications, while VEAM's integration with local supply chains enables both companies to serve small landholdings and cooperative farms. These companies maintain market dominance by providing reliable machinery and comprehensive after-sales support. Their established networks ensure farmers have access to essential parts, training, and maintenance services across Vietnam's agricultural regions.

New market entrants are focusing on electric vehicles and digital agriculture solutions. Start-up companies are introducing service-based business models that reduce equipment ownership costs, while infrastructure companies develop charging network systems. Current regulations favor manufacturers with established safety and compliance measures, limiting unauthorized imports. Market leaders are integrating hardware with software and financial services, moving from single transactions to ongoing service relationships. This integration of technology, services, and regulatory compliance is transforming market competition and advancing agricultural mechanization.

Vietnam Agricultural Tractor Industry Leaders

Kubota Corporation

Truong Hai Group Corporation (THACO)

Yanmar Holdings Co., Ltd.

Vietnam Engine & Agricultural Machinery Corp (VEAM)

Deere & Company (TTC Bien Hoa)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Minsk Tractor Plant (Belarus) expanded its joint assembly facility in Vietnam to produce agricultural tractors locally. This expansion aligns with Vietnam's objectives to enhance domestic manufacturing capabilities in agricultural machinery.

- February 2025: Truong Hai Group Corporation (THACO) invested over USD 1 billion to establish a 786-hectare industrial park in Binh Duong, focusing on mechanical manufacturing, including agricultural tractors. The development is anticipated to generate 32,000 jobs and decrease the country's dependence on machinery imports.

- December 2024: Yanmar Holdings Co., Ltd. partnered with International Tractors Limited to distribute Solis tractors in Thanh Hoa Province. The partnership focuses on the dry-field farming segment and utilizes Yanmar Holdings Co., Ltd.'s existing service network to advance agricultural modernization.

Vietnam Agricultural Tractor Market Report Scope

A tractor is an industrial vehicle with one or two small wheels in front and two large wheels at the back for agricultural and other functions. It is used to move the attached implement that plows the field or performs other activities. For this report, tractors used in agricultural operations have been considered. The report does not cover other agricultural machinery and attachments to tractors. Tractors used for industrial and construction purposes are also excluded from the study. The Vietnam agricultural tractors market is segmented by engine power (less than 15 HP, 15 to 30 HP, 31 to 45 HP, 46-75 HP, and More than 75 HP). The report offers market estimation and forecasts in value (USD) for the above-mentioned segments.

By Engine Power

| Less than 15 HP |

| 15 - 30 HP |

| 31- 45 HP |

| 46 -75 HP |

| Above 75 HP |

By Drive Type

| Two-wheel Drive (2WD) |

| Four-wheel Drive (4WD) |

By Application

| Row-crop Farming |

| Orchard and Plantation |

By Propulsion Technology

| Diesel |

| Hybrid |

| Fully Electric |

| By Engine Power | Less than 15 HP |

| 15 - 30 HP | |

| 31- 45 HP | |

| 46 -75 HP | |

| Above 75 HP | |

| By Drive Type | Two-wheel Drive (2WD) |

| Four-wheel Drive (4WD) | |

| By Application | Row-crop Farming |

| Orchard and Plantation | |

| By Propulsion Technology | Diesel |

| Hybrid | |

| Fully Electric |

Key Questions Answered in the Report

How large is the Vietnam tractor market in 2026?

The market stands at USD 330.96 million in 2026 and is moving on a 6.42% CAGR path to USD 451.78 million by 2031.

Which engine power band sells most units?

Tractors rated 46-75 HP hold 40.62% of Vietnam Agricultural Tractor Market share, balancing versatility and fuel efficiency for diverse Vietnamese field conditions.

Why do four-wheel-drive tractors dominate?

Monsoon soils and hilly coffee zones require better traction; thus four-wheel variants make up 57.48% of sales and are growing faster than two-wheel models.

How concentrated is competition?

The industry remains moderately concentrated in terms of competition.

Page last updated on: