Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

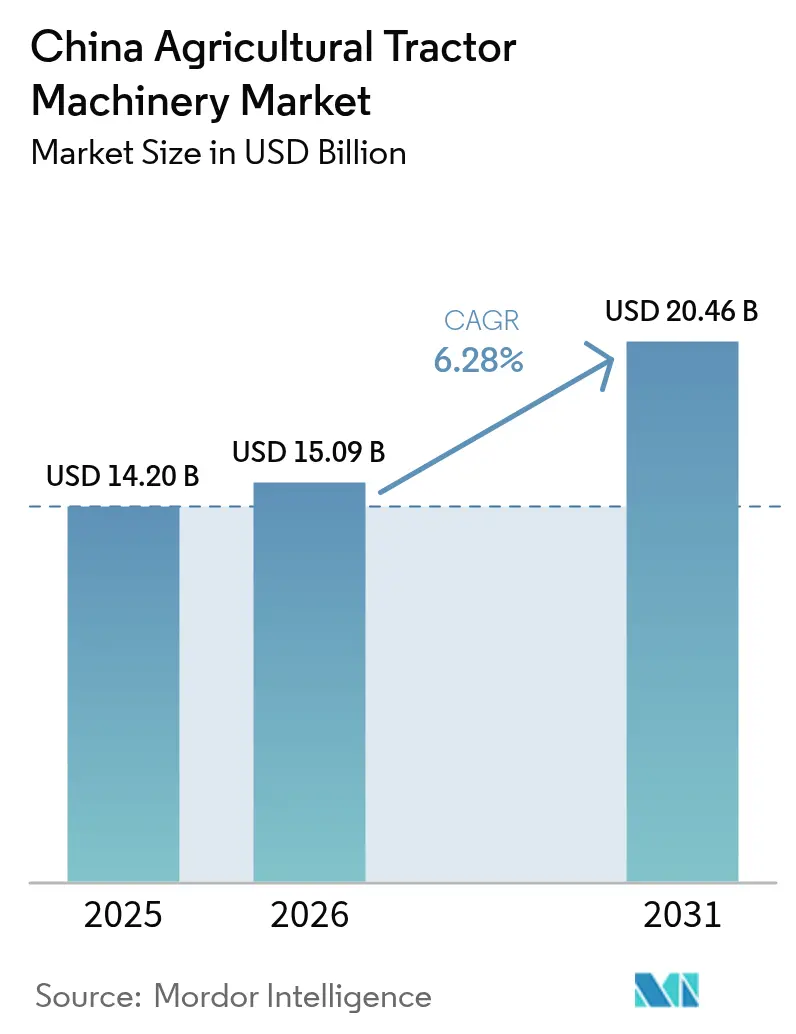

| Base Year Market Size (2025) | USD 14.20 Billion |

| Market Size (2026) | USD 15.09 Billion |

| Market Size (2031) | USD 20.46 Billion |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Agricultural Tractor Machinery Market Analysis by Mordor Intelligence

The China agricultural tractor machinery market size is expected to grow from USD 14.20 billion in 2025 to USD 15.09 billion in 2026 and is forecast to reach USD 20.46 billion by 2031 at 6.28% CAGR over 2026-2031. Robust trade-in subsidies now cover not just tractors but precision implements, helping growers replace underpowered seed drills and sprayers with high-tech, Beidou-enabled solutions that lift productivity while meeting National IV compatibility rules. Land-consolidation policies fuel demand for wider implements that single operators can run efficiently, while Beijing’s spectrum-fee waiver slashes the cost of field guidance packages. At the same time, rural wage inflation and an aging labor force are compressing seasonal windows, creating a clear business case for 12-row planters, eighteen-meter boom sprayers, and net-wrap round balers that significantly reduce labor hours. Yet adoption remains uneven, tight credit quotas and a shortage of International Organization for Standardization Bus-certified technicians lengthen the payback horizons for smallholders, slowing unit turnover and maintaining a two-speed equipment landscape inside the China agricultural tractor machinery market.

Key Report Takeaways

- By product type, plowing and cultivating machinery led with 43.55% of the China agricultural tractor machinery market size in 2025, and sprayers are forecast to expand at an 8.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Agricultural Tractor Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government trade-in subsidies for implements | +1.80% | National, strongest in Heilongjiang, Henan, and Shandong | Short term (≤ 2 years) |

| Rural labor shortage and aging workforce | +1.50% | Nationwide, and most acute in Northeast grain belt | Medium term (2-4 years) |

| Upgrade to National IV emission standards | +1.20% | Nationwide, and strict audits in Beijing-Tianjin-Hebei and Yangtze Delta | Short term (≤ 2 years) |

| Expansion of large-scale commercial farms | +1.10% | Northeast and Northwest, notably Xinjiang and Inner Mongolia | Long term (≥ 4 years) |

| Beidou-enabled autonomous guidance for implements | +0.70% | Nationwide, and early wins in Heilongjiang and Xinjiang | Medium term (2-4 years) |

| Telematics-based machinery service cooperatives | +0.40% | East and Central China, and radiating to Southwest | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Trade-In Subsidies for Implements

Beijing earmarked CNY 300 billion (USD 41.7 billion) for machinery upgrades through 2026, funneling roughly 28%, around CNY 84 billion (USD 11.7 billion) into implements that meet National IV compatibility, Beidou guidance, or variable-rate criteria.[1]Source: Ministry of Agriculture and Rural Affairs of China, “Agricultural Machinery Purchase Subsidy Implementation Guidance (2024-2026),” moa.gov.cn Rebates shave 12-18% off purchase prices, propelling the rapid retirement of 280,000 legacy implements in 2024 and tilting market share toward domestic brands that satisfy 55% local-content thresholds. The incentive cut replacement cycle was extended to eight years, giving the China agricultural tractor machinery market fresh momentum as provincial match funding stacked on top of central support.

Rural Labor Shortage and Aging Workforce

The farm workforce shrank by 8.3 million between 2020 and 2024, and the median age touched 56 years, forcing growers to pivot toward single-operator solutions.[2]Source: National Bureau of Statistics of China, “Statistical Communiqué on the 2024 National Economic and Social Development,” stats.gov.cn No-till planters reduced labor inputs by 44% per hectare, while net-wrap round balers reduced the number of baling crews from four individuals to one, helping to implement sales above a six-meter working width surge by 13.2%. The trend directly contributes to rising unit values and increased demand for pull-through parts within the China agricultural tractor machinery market.

Upgraded to National IV Emission Standards

Cleaner engines consume 8-12% more parasitic power, prompting implement manufacturers to redesign hydraulic circuits and replace fluid motors with electric drives, adding (CNY 12,000–CNY 25,000) USD 1,665–USD 3,470 to manufacturing costs.[3]Source: Ministry of Ecology and Environment of China, “Implementation Notice on National IV Emission Standards for Non-Road Mobile Machinery,” mee.gov.cn Regions with strict enforcement check for ISO 11783 compliance before granting subsidies, accelerating consolidation among suppliers, and nudging average selling prices higher across the China agricultural tractor machinery market.

Expansion of Large-Scale Commercial Farms

Land-transfer reforms have consolidated small plots into 500-mu blocks, particularly in Heilongjiang, Xinjiang, and Inner Mongolia. Large cooperatives are turning to 12-row planters and eighteen-meter sprayers that reduce field passes and conserve fuel, resulting in a 16.8% increase in wide-planter sales during 2024.[4]Source: Transactions of the Chinese Society of Agricultural Engineering, “Field Performance Evaluation of Beidou-Guided Precision Planters in Northeast China,” tcsae.org In turn, premium electric metering, heavy-duty coulters, and residue managers enter mainstream demand, raising the technical baseline of the China agricultural tractor machinery market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront price of precision implements | −0.9% | Nationwide, and toughest in Southwest and Central counties | Short term (≤ 2 years) |

| Farm-income volatility from commodity and weather swings | −0.6% | Nationwide, and heightened in rain-fed North and Southwest | Medium term (2-4 years) |

| Shortage of precision-implement technicians | −0.4% | Remote counties in Southwest and Northwest | Long term (≥ 4 years) |

| Tight rural credit quotas for smallholders | −0.3% | Nationwide, and severe where real-estate exposure is high | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Farm-Income Volatility from Commodity and Weather Swings

Significant corn price fluctuations, combined with climate-related yield losses, continue to reduce free cash flow for farmers, constraining their ability to invest in equipment upgrades. In provinces such as Henan and Shandong, these financial pressures have led to a 14–19% decline in cash purchases of agricultural implements in 2024. While larger farms are increasingly adopting lease-to-own arrangements, demand for high-specification or specialty attachments remains weak, limiting short-term growth prospects for the China agricultural tractor machinery market.

Shortage of Precision-Implement Technicians

Only 11% of rural dealerships employ technicians certified in ISOBUS (International Organization for Standardization Bus) diagnostics, resulting in extended repair times for electronic and precision-control faults. The average service turnaround time has reached nearly ten days, and limited technical expertise has driven repair costs to nearly three times the usual levels. This prolonged downtime discourages some farmers from adopting advanced, electronically integrated systems, leading them to continue relying on older mechanical gear-drive platforms. Consequently, the adoption of smart tractor-mounted technologies remains slow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sprayers Surge While Plowing and Cultivating Machinery Dominates Market

Plowing and cultivating machinery accounted for about 43.55% of the China agricultural tractor machinery market in 2025. This dominance is due to the continued importance of rotovators and strip-till cultivators in rice–wheat and wheat–maize rotations, which maintains their significance in farming operations. In the plowing segment, conservation-tillage equipment offers higher margins, with demand for strip-till units increasing significantly in 2024 as farmers responded to incentives promoting soil health. These agronomic and economic drivers ensure that conservation-tillage implements will remain a key element of the agricultural tractor machinery market in China. Sprayers register the fastest 8.02% CAGR as pesticide-reduction mandates encourage GPS-guided boom rigs and UAV applicators that cut chemical overlap by up to 25%.

Planting machinery is witnessing steady growth as cooperatives increasingly adopt electric-meter planters compatible with tractor ISOBUS (International Organization for Standardization Bus) terminals. The haying and forage equipment segment is also expanding, driven by demand from the dairy sector in regions such as Inner Mongolia and Xinjiang, where net-wrap balers are gaining significant traction. Additionally, specialty implements, including orchard sprayers and narrow-track cultivators, are benefiting from zero-emission regulations in peri-urban areas, contributing to sustained growth in these niche segments of the China agricultural tractor machinery market.

Geography Analysis

Northeast China remains a key hub for agricultural implement revenue, driven by the needs of large farms for wide planters, high-capacity sprayers, and net-wrap balers. The region benefits from a provincial smart-agriculture fund valued at (CNY 8 billion) USD 1.1 billion, which supports the adoption of Beidou-compatible machinery, fostering modernization. In North China, versatile cultivators and haying equipment are in demand, particularly to support Inner Mongolia’s livestock clusters. Together, these regions are shaping the demand for advanced implements and contributing to the growth of China’s tractor-mounted machinery market.

In East China, the prevalence of fragmented 1-hectare (15-mu) plots encourages the use of compact and efficient implements, such as small rotovators and rice transplanters, which are well-suited to the region's highly subdivided farm structures. Cooperative initiatives in Shandong are gradually shifting the machinery mix toward larger 8-row planters, increasing the average selling price of equipment. These developments highlight how smallholder consolidation and mechanization incentives are reshaping demand patterns, promoting the adoption of precision planting solutions while ensuring compatibility with existing tractor-mounted machinery.

Central and South China rely predominantly on rice–wheat double-cropping systems, sustaining steady demand for transplanters and related implements. In Southwest China, the hilly terrain has driven the adoption of UAV sprayers, which efficiently navigate steep slopes. Meanwhile, Northwest China, led by Xinjiang’s extensive cotton cultivation spanning 5.3 million hectares, is increasingly adopting drip irrigation and precision planting technologies, generating strong demand for advanced implements. Across these regions, mechanization trends are accelerating, enhancing farm productivity and expanding the adoption of tractor-mounted machinery in China.

Competitive Landscape

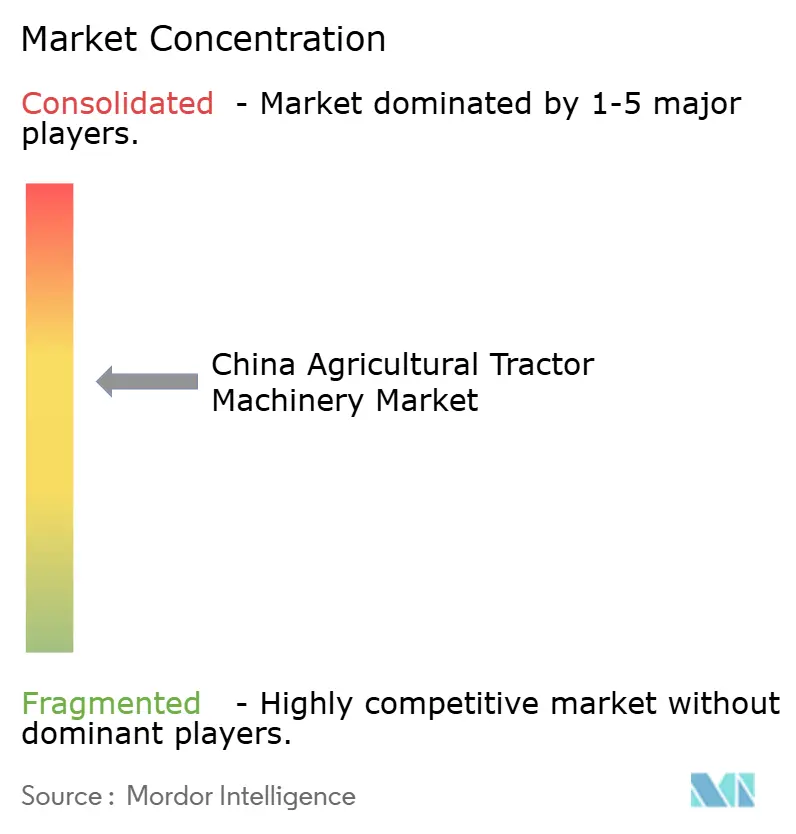

The China agricultural tractor machinery market is moderately fragmented, with the top five implement suppliers projected to account for a modest percentage of revenue in 2024. This leaves significant opportunities for niche innovators. Domestic manufacturers dominate the lower-priced segments by leveraging extensive dealer networks and locally produced electric seed meters. Leading companies, such as YTO Group Corporation and Lovol Heavy Industry Co., Ltd., have begun producing electric-drive meters and section valves in-house, reducing dependence on imports. Additionally, Zoomlion Heavy Industry Science & Technology Co., Ltd. has expanded its compact implement offerings through the acquisition of Changzhou Dongfeng Agricultural Machinery Group Co., Ltd., enhancing its market coverage.

Advanced technology is increasingly shaping competition within the market. Deere & Company offers integrated farm-management platforms that consolidate field data and support decision-making for large-acre operators. Domestic collaborations, such as Kubota Corporation-compatible systems equipped with BeiDou GNSS receivers, are reducing guidance costs while maintaining precision. Meanwhile, smaller players and startups are promoting the adoption of conservation-tillage implements and battery-electric rotovators, addressing environmental mandates in key regions. Companies that incorporate smart systems, data analytics, and precision guidance are gaining a competitive edge over less technologically advanced rivals.

Adherence to industry standards is becoming essential for securing market access and subsidies. Compliance with ISO 11783 and Green Agricultural Machinery certification enables manufacturers to qualify for higher subsidy tiers, providing a competitive advantage to well-resourced domestic and international OEMs such as YTO Group Corporation, Lovol Heavy Industry Co., Ltd., Zoomlion Heavy Industry Science & Technology Co., Ltd., Deere & Company, and AGCO Corporation. Investments in high-quality, standards-compliant implements are allowing these manufacturers to outpace smaller competitors, foster long-term customer loyalty, and strengthen their positions in both traditional and emerging segments of the China agricultural tractor machinery market.

China Agricultural Tractor Machinery Industry Leaders

Kubota Corporation

YTO Group Corporation

Lovol Heavy Industry Co., Ltd.

Deere & Company

Zoomlion Heavy Industry Science & Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: CLAAS KGaA mbH launched the CEREX 700 round baler, a tractor-mounted hay and forage implement with a variable chamber, HD belts, and 25 knives for higher bale density and fuel efficiency. Integrated with CLAAS Connect for digital fleet management, it highlights the role of smart, high-performance implements in driving productivity and growth in China’s agricultural tractor machinery market.

- October 2025: Lovol Heavy Industry Co., Ltd. launched 25 upgraded models at the SDHI·Weichai Power conference, including new implements for LOVOL P, M, and F series tractors. Produced at its new large-horsepower Shandong plant, the implements standardize hydraulic interfaces and cover the full tillage-to-harvest cycle. The rollout strengthens Lovol’s leadership in tractor-mounted attachments and aligns with China’s shift toward integrated, platform-based implement systems.

- October 2024: At the 2024 China International Agricultural Machinery Exhibition, Zoomlion Heavy Industry Science & Technology Co., Ltd. showcased IoT-enabled tractor-mounted systems for precision fertilizer application, irrigation, and spraying, enhancing input efficiency and reflecting the digitalization trend in China’s agricultural tractor machinery market.

China Agricultural Tractor Machinery Market Report Scope

The China Agricultural Tractor Machinery Market Report is Segmented by Product Type (Plowing and Cultivating Machinery, Planting Machinery, Sprayers, Haying and Forage Machinery, and Other Types). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Plowing and Cultivating Machinery | Plows |

| Harrows | |

| Rotovators and Cultivators | |

| Other Equipment | |

| Planting Machinery | Seed Drills |

| Planters | |

| Spreaders | |

| Other Planting Machinery | |

| Sprayers | |

| Haying and Forage Machinery | Mowers and Conditioners |

| Balers | |

| Other Haying and Forage Machinery | |

| Other Types |

| By Product Type | Plowing and Cultivating Machinery | Plows |

| Harrows | ||

| Rotovators and Cultivators | ||

| Other Equipment | ||

| Planting Machinery | Seed Drills | |

| Planters | ||

| Spreaders | ||

| Other Planting Machinery | ||

| Sprayers | ||

| Haying and Forage Machinery | Mowers and Conditioners | |

| Balers | ||

| Other Haying and Forage Machinery | ||

| Other Types | ||

Key Questions Answered in the Report

How large is the China agricultural tractor machinery market in 2026?

The market is valued at USD 15.09 billion in 2026.

What growth rate is projected through 2031?

Revenue is projected to rise at a 6.28% CAGR through 2031.

Which implement segment is growing fastest?

Sprayers, driven by guidance technology and pesticide-reduction mandates, are forecast at an 8.02% CAGR.

What technology saves the most inputs?

Beidou-guided row shutoff and section control can trim seed and chemical use by up to 25%.

Page last updated on: