Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

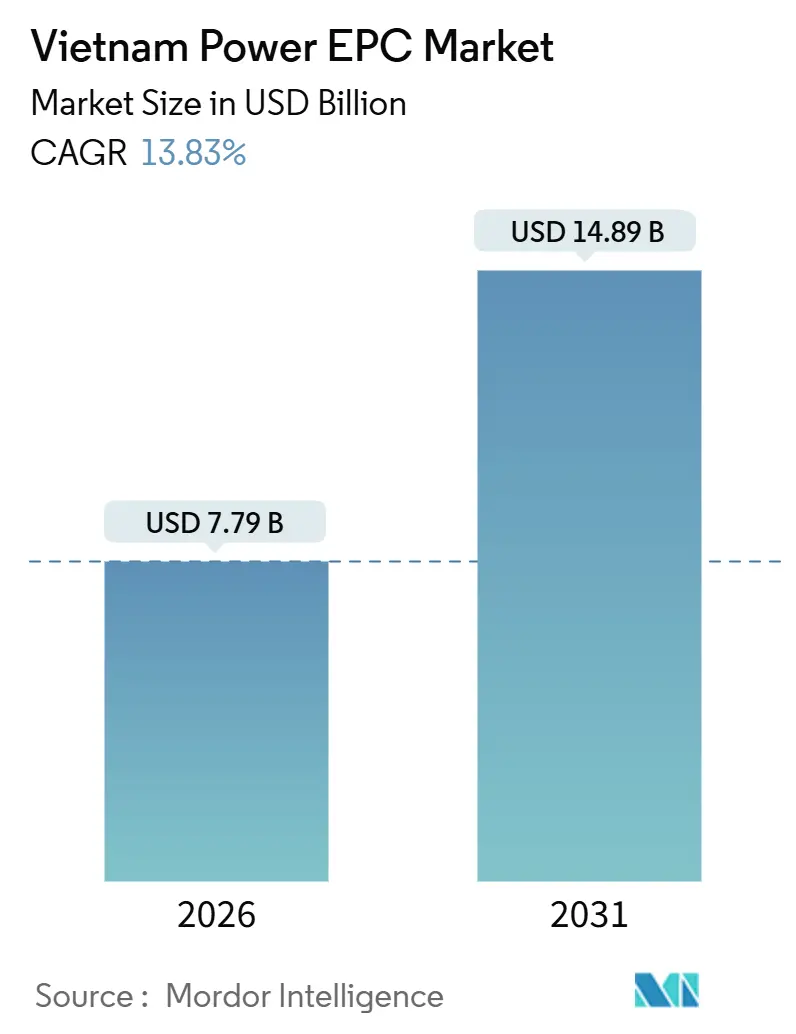

| Market Size (2026) | USD 7.79 Billion |

| Market Size (2031) | USD 14.89 Billion |

| Growth Rate (2026 - 2031) | 13.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Power EPC Market Analysis by Mordor Intelligence

The Vietnam Power EPC Market size is estimated at USD 7.79 billion in 2026, and is expected to reach USD 14.89 billion by 2031, at a CAGR of 13.83% during the forecast period (2026-2031).

Demand acceleration stems from the revised Power Development Plan 8, an 8.6 GW coal retirement schedule, and a 150 GW generation-capacity target for 2030, all of which redirect capital toward gas and renewable engineering-procurement-construction contracts.[1]Vietnam Government Portal, “Power Development Plan 8 Summary,” vietnam.gov.vn Industrial electricity consumption rose 8.7% year-on-year in 2025 as semiconductor fabs, data centers, and export-oriented manufacturers ramped operations, while three new LNG import terminals unlocked a USD 12 billion backlog of combined-cycle gas-turbine work. Direct power-purchase agreements (DPPAs) that debuted in 2025 now allow large commercial and industrial buyers to sign 10- to 20-year renewable PPAs, catalyzing a rooftop-solar surge and supporting the Vietnam power EPC market’s near-term growth path. Mandatory battery-storage add-ons equal to 10% of project capacity further expand EPC scopes, lifting balance-of-plant spending and deepening supplier ecosystems.

Key Report Takeaways

- Vietnam's power EPC market is segmented into power generation EPC and power transmission and distribution (T&D) EPC. Power generation EPC accounted for 61.7% of the market in 2025, while power transmission and distribution (T&D) EPC is projected to grow at a 16.14% CAGR through 2031.

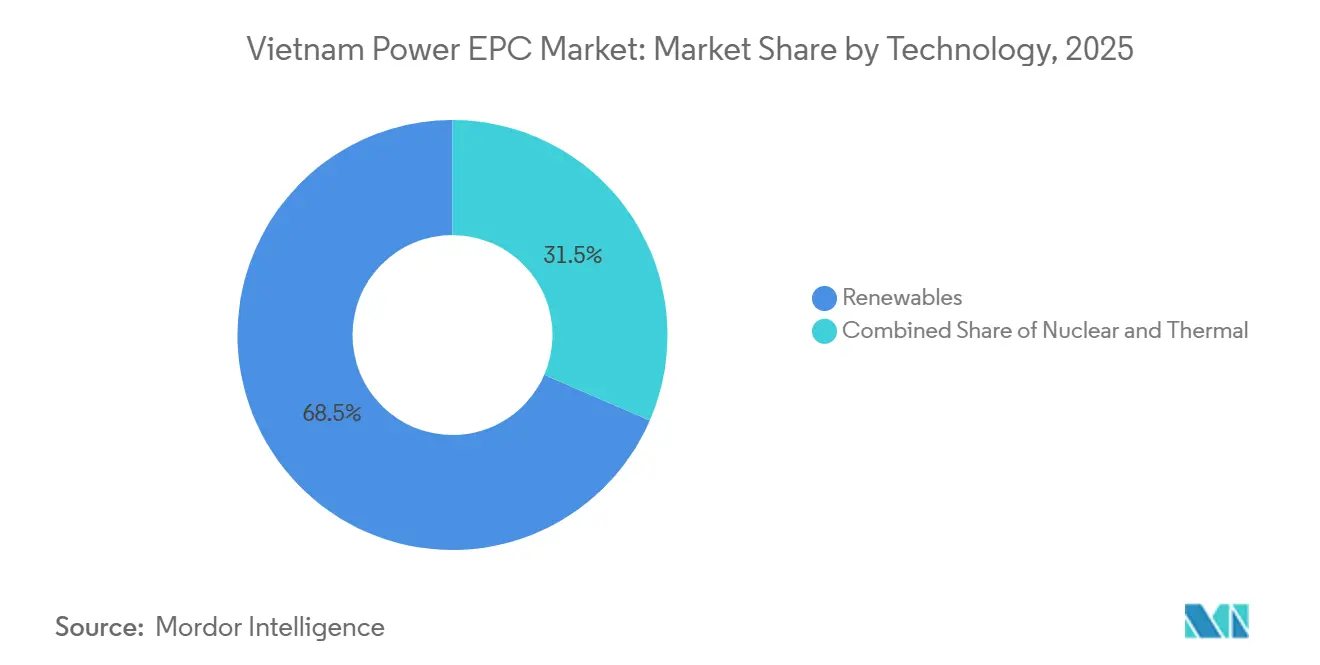

- By technology, renewables led with 68.5% of Vietnam's power generation EPC market share in 2025, whereas offshore wind is forecast to expand at a 15.3% CAGR through 2031.

- By capacity band, the 100 – 499 MW range captured 61.9% of the Vietnam power generation EPC market size in 2025, while the sub-100 MW distributed-energy-resource segment is poised to grow at a 16.5% CAGR to 2031.

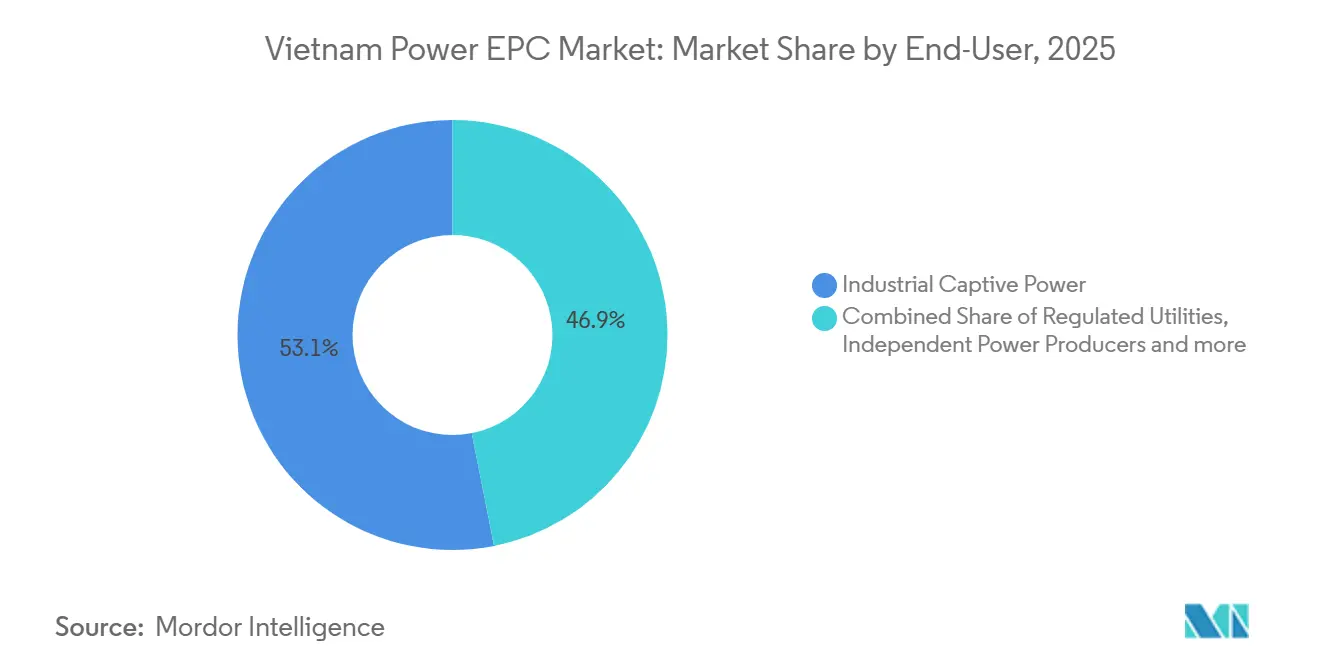

- By end user, industrial captive power accounted for 53.1% of Vietnam's power generation EPC market size in 2025; independent power producers are advancing at a 16.1% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Power EPC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid industrial & residential load growth | 2.8% | National, with concentration in Hanoi, Ho Chi Minh City, and Hai Phong industrial zones | Short term (≤ 2 years) |

| Revised PDP 8 upsizing generation & grid CAPEX pipeline | 3.2% | National, prioritizing northern coal-to-gas conversion and southern offshore wind zones | Medium term (2-4 years) |

| Surge in LNG-to-power projects unlocking gas EPC backlog | 2.1% | Southern provinces (Ba Ria-Vung Tau, Binh Thuan) and central coast (Quang Tri) | Short term (≤ 2 years) |

| DPPA framework catalysing C&I renewable build-outs | 1.9% | Industrial parks in Bac Ninh, Dong Nai, Binh Duong | Medium term (2-4 years) |

| Mandatory storage add-ons (>10% / 2-h) boosting BESS EPC scope | 1.5% | Renewable-rich provinces (Ninh Thuan, Binh Thuan, Tra Vinh) | Medium term (2-4 years) |

| Local content incentives for wind/solar equipment & EPC services | 0.9% | National, with manufacturing hubs in Hai Phong and Da Nang | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Industrial & Residential Load Growth

Vietnam’s electricity consumption climbed to 280 TWh in 2025, up from 257 TWh in 2024, with industrial users supplying 58% of incremental demand as new fabrication plants and data centers came online in northern provinces. Residential demand expanded 6.2% on air-conditioning penetration topping 70% in Hanoi and Ho Chi Minh City, and on 1.2 GW of evening-peak charging load from electric two-wheelers.[2]International Energy Agency, “Southeast Asia Energy Outlook 2025,” iea.org Sustained load growth forces utilities and IPPs to fast-track baseload additions, yet transmission constraints push industrial parks toward captive generation, fragmenting the Vietnam power EPC market into utility-scale and behind-the-meter segments. Export-processing zones in Bac Ninh and Hai Phong logged 47 unplanned outages in 2025, prompting multinationals to stipulate on-site backup capacity in lease contracts. The government plans to electrify all rural households by 2027, adding 3.5 GW of distribution upgrades, creating auxiliary EPC demand for low-voltage equipment.

Revised PDP 8 Upsizing Generation & Grid CAPEX Pipeline

The final Power Development Plan 8, approved in 2024, lifts the 2030 installed-capacity target to 150 GW, 30 GW more than the draft, and earmarks USD 18 billion for 500 kV corridors that will move offshore wind from the south-central coast to the Red River Delta. The policy retires 8.6 GW of subcritical coal by 2030 and sets a 15 GW LNG target, sustaining a double-digit EPC trajectory for cleaner thermal assets. Offshore wind allocation climbs from 6 GW to 10 GW, reflecting lower levelized costs in shallow-water sites once grid costs are socialized. A new “grid-first” rule means generation projects cannot reach financial close until EVN confirms substation availability, front-loading T&D EPC awards, and lengthening generation timelines. An Asian Development Bank USD 2.5 billion concessional loan package, signed in 2025, lowers weighted-average capital costs for 500 kV projects to 7.2%, allowing contractors to bid more aggressively. [3]Asian Development Bank, “Vietnam Grid Expansion Loan,” adb.org

Surge in LNG-to-Power Projects Unlocking Gas EPC Backlog

Three regasification terminals, Thi Vai, Son My, and Quang Tri, began service between January 2024 and September 2025, clearing the fuel bottleneck that had stalled 6.8 GW of combined-cycle projects. PetroVietnam Power and Samsung C&T’s 1,624 MW Nhon Trach 3 & 4 plant entered commercial operation in June 2025, using GE 9HA.02 turbines at 64% net efficiency, the region’s highest thermal benchmark. Quang Trach II broke ground in March 2025 under a USD 1.9 billion contract that features Siemens Energy SGT5-8000H turbines and air-cooled condensers to curb freshwater use. Indexing LNG tariffs to Henry Hub prices instead of oil benchmarks reduces offtaker risk, enabling 4.2 GW of new CCGT PPAs in 2025. OEMs secure 40-50% of lifecycle EPC value through long-term service agreements, exemplified by GE Vernova’s 20-year LTSA that guarantees 95% availability at Nhon Trach 3 & 4.

DPPA Framework Catalyzing C&I Renewable Build-Outs

Decree 57/2025 permits customers using more than 30 GWh annually to sign bilateral PPAs of up to 20 years, bypassing EVN and unlocking rooftop and ground-mount solar previously constrained by net-metering caps. By October 2025, 127 contracts totaling 890 MW had been registered, with textiles, steel, and electronics accounting for 73% of offtake. World Bank partial-risk guarantees launched in June 2025 cut solar borrowing costs by roughly 200 basis points, enabling non-recourse finance for projects as small as 5 MW. Rooftop-solar EPC margins eased to 8-9% as 34 domestic contractors entered the segment, yet the sub-100 MW band will post a 16.5% CAGR on the back of continued industrial-park expansion. Decree 135/2024’s removal of the 20% net-metering ceiling lets factories size solar to full daytime load, tripling the distributed-generation opportunity set.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion & curtailment risk inflating project IRRs | -1.8% | Southern provinces (Ninh Thuan, Binh Thuan, Tra Vinh) and central coast | Short term (≤ 2 years) |

| Retroactive FIT revisions eroding investor confidence | -1.2% | National, affecting projects commissioned 2019-2021 | Medium term (2-4 years) |

| Skilled EPC labour shortages for high-voltage & offshore works | -0.9% | Offshore wind zones and 500 kV transmission corridors | Medium term (2-4 years) |

| EVN credit-risk overhang on long-term PPAs | -1.4% | National, most acute for IPP-developed renewable projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid Congestion & Curtailment Risk Inflating Project IRRs

Solar and wind curtailment averaged 18% in southern provinces during H1 2025, equal to 1,240 GWh of lost output as 500 kV lines operated above rated capacity. Delays to the Thuan Nam-Phuoc Long upgrade forced operators to trim 2.1 GW of solar on 87 days, wiping USD 31 million from generator revenues. Developers now model 12-15% curtailment when pricing PPAs, pushing LCOE up USD 6-8 per MWh and squeezing equity IRRs below regional benchmarks. Land near spare-capacity substations trades 40-60% higher than parcels in congested zones, fragmenting the pipeline into smaller deals. EVN’s USD 6.2 billion southern transmission plan will not relieve congestion until 2028-2029, suppressing annual EPC awards in the interim.

Retroactive FIT Revisions Eroding Investor Confidence

Circular 02/2024 cut tariffs for 1,247 MW of 2019-2020 solar projects from USD 93.5 to USD 71.2 per MWh, prompting 23 arbitration claims and an 80-120 basis-point rise in borrowing spreads for new deals. Moody’s downgraded Vietnam’s regulatory-stability score to Ba1 in 2025, while lenders now require 20-year revenue floors or World Bank risk coverage, adding six to nine months to development timelines.[4]Moody’s Investors Service, “EVN Credit Opinion,” moodys.com Even projects with signed PPAs struggle to close; 340 MW of solar commissioned in 2025 remains unfinanced due to tariff-revision fears.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Offshore Wind Drives Renewable Dominance

Renewables commanded 68.5% of Vietnam's power generation EPC market share in 2025 and are set to expand at a 15.3% CAGR through 2031 as offshore wind shifts from study to execution, led by the 3.5 GW La Gan and 2.1 GW Hai Long blocks valued at USD 13.6 billion. Thermal capacity, primarily LNG-fired CCGT, occupied the remaining 31.5% but still anchors baseload with 9HA.02 turbines delivering 64% efficiency at Nhon Trach 3 & 4.

Offshore wind's engineering complexity, monopile foundations in 25-40 meter depths, and 220 kV subsea links of 80-120 kilometers, keep EPC costs at USD 3,200-3,800 per kW, far above utility-scale solar at USD 650-750 per kW. Thermal EPC share slips as financiers exit coal; 17 global banks adopted coal-exclusion policies during 2024-2025, forcing the 600 MW Quang Trach I upgrade to convert from coal to LNG mid-design. Still, PDP 8 caps renewable penetration at 47% by 2030 for grid stability, ensuring thermal EPC holds at least one-quarter of Vietnam's power generation EPC market value through 2031.

By Capacity Band: DER Segment Surges on DPPA Momentum

Projects sized 100-499 MW secured 61.9% of Vietnam's power generation EPC market size in 2025, the sweet spot for provincial auctions that balance scale with grid-connection feasibility. Sub-100 MW distributed resources, underpinned by DPPAs and net-metering reforms, will grow at a 16.5% CAGR, reflecting factory demand for rooftop solar and BESS hedges against future tariff hikes.

Above-500 MW ventures, namely offshore wind and LNG CCGT, accounted for 23% of the 2025 EPC value but require 54 months on average from feasibility to commercial operation due to complex environmental and guarantee procedures. The government's 2025 exemption of sub-30 MW projects from mandatory storage cut capital intensity 18-22%, lifting distributed-generation IRRs to 13-15% and spurring a wave of rooftop financings in H2 2025.

By End-User: Industrial Captive Power Leads, IPPs Accelerate

Industrial captive schemes held 53.1% of the Vietnam power generation EPC market size in 2025, as export zones faced 47 grid outages per site and mandated on-site generation for 99.99% uptime. Independent power producers will grow at a 16.1% CAGR, buoyed by an 8 GW renewable auction slated for 2026 and newfound ability to sell directly to C&I buyers under DPPAs.

Regulated utilities, mainly EVN subsidiaries, controlled 28% of EPC value in 2025 and are now prioritizing T&D assets, while SOEs such as PetroVietnam Power focus on strategic LNG and offshore wind projects requiring sovereign support. Captive power remains heterogeneous: 62% of 2025 spend was gas cogeneration, 28% rooftop solar plus BESS, and 10% diesel gensets converted to dual-fuel for emission compliance.

Geography Analysis

Southern Vietnam captured 48% of the 2025 EPC value thanks to industrial-park density and proximity to Thi Vai and Vung Tau LNG terminals. The south-central coast’s solar-and-wind cluster took 31%, though curtailment hit 18% because the Thuan Nam-Phuoc Long 500 kV line will not finish until mid-2026. Northern provinces held 21%, with a rooftop-solar tilt and coal-to-gas conversions on tap once north-south gas pipeline work begins in 2026.

Offshore wind priority zones in Binh Thuan and Tra Vinh enjoy expedited seabed leases, concentrating 4.8 GW of the national 10 GW target and attracting supply-chain clusters for monopile, cable, and vessel services. Northern rooftop solar benefits from higher industrial tariffs, USD 95 versus USD 82 per MWh in the south, shortening payback to 5.2 years despite 12% lower irradiation. The Mekong Delta remains underrepresented (below 3% of investment) due to land subsidence, raising foundation costs 30-40%.

Competitive Landscape

The top five contractors, Samsung C&T, Lilama, Doosan Enerbility, Siemens Energy, and GE Vernova, combined for 42% of the Vietnam power EPC market value in 2025, leaving the remainder to 17 domestic and 18 foreign rivals. Thermal EPC centers on incumbents with EVN ties; Samsung C&T secured three of five LNG contracts by pairing 6-8% margins with vendor financing that trims upfront capital 25-30%. Offshore wind alliances such as CIP-PetroVietnam corner early awards by mixing European know-how with state logistics assets.

Storage mandates open white space for integrators like Fluence and Wartsila, while Vietnamese steel makers Hoa Phat and Hoa Sen are backward-integrating into wind-tower fabrication to exploit 40% local-content incentives, undercutting imports by up to 18%. OEM differentiation hinges on efficiency patents: Vestas’ modular nacelle assembly trims on-site time 22%, and Siemens Energy’s hybrid cooling cuts auxiliary power 1.8 percentage points, protecting premium pricing amid margin compression.

Vietnam Power EPC Industry Leaders

IHI Infrastructure Systems Co.,Ltd.

Lilama Corporation

Doosan Enerbility Co. Ltd.

JGC Vietnam Co. Ltd

Power Engineering Consulting JSC 2 (PECC2)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: erex Co., Ltd. announced that its subsidiary, erex Tuyen Quang Biomass Power Co., Ltd., has signed an EPC (Engineering, Procurement, and Construction) contract for the Tuyen Quang Biomass Power Plant in Vietnam. The contract was inked with Power Engineering Consulting Joint Stock Company 2 (PECC2). The Tuyen Quang Biomass Power Plant is set to commence operations at the close of fiscal year 2027, aligning its timeline with the Yen Bai Biomass Power Plant.

- November 2025: EREX Yen Bai Biomass Power Co., Ltd., a subsidiary of erex Co., Ltd., and Power Engineering Consulting Joint Stock Company 2 (PECC2) recently signed the Engineering, Procurement, and Construction (EPC) Contract for the Yen Bai 1 Biomass Power Plant Project, boasting a total capacity of 50MW.

- September 2025: EVNGENCO2, the Power Generation Corporation 2, in collaboration with LIGEPS CONSORTIUM—a joint venture between Vietnam's Machinery Installation Corporation (LILAMA) and Power Generation Corporation 3 (EVNGENCO3)—celebrated the signing of the EPC Contract Package No. 5 (EPC-1).

- August 2025: In the Mekong Delta city of Can Tho, state-run Petrovietnam has commenced construction on its O Mon IV thermal power plant, a project valued at VND27.7 trillion (USD 1.05 billion). This 1,155 MW facility is pivotal to the Block B-O Mon gas-to-power chain, which boasts an estimated reserve of 100 billion cubic meters of gas. Annually, it will supply 5-6 billion cubic meters, translating to the generation of tens of billions of kilowatt-hours of clean electricity.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Vietnam Power Engineering-Procurement-Construction (EPC) market as the aggregated contract value earned by EPC contractors that design, procure equipment for, and build utility-scale thermal, gas, renewable, nuclear, and hybrid power generation projects within Vietnam's borders during the study period. Contract amendments and O&M revenues are excluded, so the figure reflects fresh turnkey project awards and progress-linked payouts only.

Scope exclusion: stand-alone transmission and distribution EPC packages fall outside this study.

Segmentation Overview

- Power Generation EPC

- By Technology

- Thermal

- Nuclear

- Renewables

- By Capacity Band

- Up to 100 MW (DER, micro-grid)

- 100 to 499 MW

- Above 500 MW

- By End-User

- Regulated Utilities

- Independent Power Producers

- Industrial Captive Power

- Public Sector and SOE

- By Technology

- Power Transmission and Distribution (T&D) EPC

Detailed Research Methodology and Data Validation

Primary Research

Interviews with EPC planners, project developers, lenders, and engineering consultants across Hanoi, Ho Chi Minh City, Singapore, and Seoul enabled us to verify typical EPC cost per megawatt, milestone payment structures, and likely slippage on key LNG-to-power projects. Follow-up surveys with equipment suppliers clarified lead-time assumptions for GT, boiler, and BOP packages.

Desk Research

Our analysts first mapped the universe of active and planned plants using publicly available project registers issued by Vietnam's Ministry of Industry and Trade, EVN annual data books, PDP 8 drafts, IRENA capacity statistics, and IEA investment trackers. Contract pricing clues were then gathered from press releases lodged on Doosan Enerbility, Lilama, and JGC investor portals, together with tender notices on Tenders Info and shipment trends on Volza. Paid databases such as D&B Hoovers and Dow Jones Factiva helped us capture corporate financials and deal milestones that rarely surface in press articles. The sources listed are indicative; many additional public and subscription datasets were consulted during validation.

Market-Sizing & Forecasting

The model begins with a top-down reconstruction of generation capacity additions from 2019 onward, converting megawatts into EPC dollars through technology-specific USD per MW benchmarks revealed in primary calls, and then adjusting for local content ratios and learning-rate discounts. Supplier roll-ups on ten representative projects provide a bottom-up cross-check that steers the final baseline. Key inputs include GDP growth, peak-load forecasts, committed PDP 8 pipeline, foreign direct investment in energy, average contract award lag, and renewable auction volumes. A multivariate regression, stress-tested through three demand scenarios, drives the 2025-2030 outlook.

Data Validation & Update Cycle

Outputs pass three layers of anomaly screening, variance checks against independent installation trackers, and peer reviews before sign-off. Reports refresh each year, and an interim update is triggered when project cancellations or major policy shifts move the baseline materially.

Why Mordor's Vietnam Power EPC Baseline Commands Reliability

Published numbers often diverge because firms adopt different project scopes, currency bases, and refresh cadences.

Key gap drivers include whether transmission jobs are mixed with generation EPC, how quickly PDP 8 revisions are captured, and the depth of contractor-level cross-checks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.33 B (2025) | Mordor Intelligence | - |

| USD 3.10 B (2024) | Regional Consultancy A | Omits LNG combined-cycle awards and converts at fixed 2022 VND rates |

| USD 0.31 B (2024) | Industry Journal B | Counts only renewable EPC and relies on published contract caps without progress payments |

These comparisons show that when full generation technologies, updated exchange rates, and verified milestone payments are combined, Mordor delivers a balanced, transparent baseline that decision-makers can trace to clear variables and repeat with confidence.

Key Questions Answered in the Report

What is the projected CAGR for power EPC spending in Vietnam from 2026 to 2031?

Spending is forecast to rise at a 13.83% CAGR, moving from USD 7.79 billion in 2026 to USD 14.89 billion by 2031.

Which generation technology is positioned to attract the most EPC capital during the forecast period?

Renewables, led by offshore wind, already held 68.5% of 2025 value and are expected to expand at a 15.3% CAGR through 2031.

How does the DPPA framework change corporate access to renewable electricity?

Decree 57/2025 lets commercial and industrial customers consuming more than 30 GWh per year sign 10- to 20-year power-purchase agreements directly with renewable generators, bypassing EVN and cutting financing costs by roughly 200 basis points.

Why is grid congestion a critical risk for developers in southern Vietnam?

Transmission delays pushed solar-and-wind curtailment to 18% of output in H1 2025, inflating levelized costs by USD 6-8 per MWh and lowering equity IRRs.

Which region currently accounts for the largest share of EPC spending and why?

The southern economic corridor captures 48% of generation EPC value thanks to dense industrial parks and nearby LNG terminals that support both captive gas power and large renewable builds.

Page last updated on: