Business Processing Outsourcing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

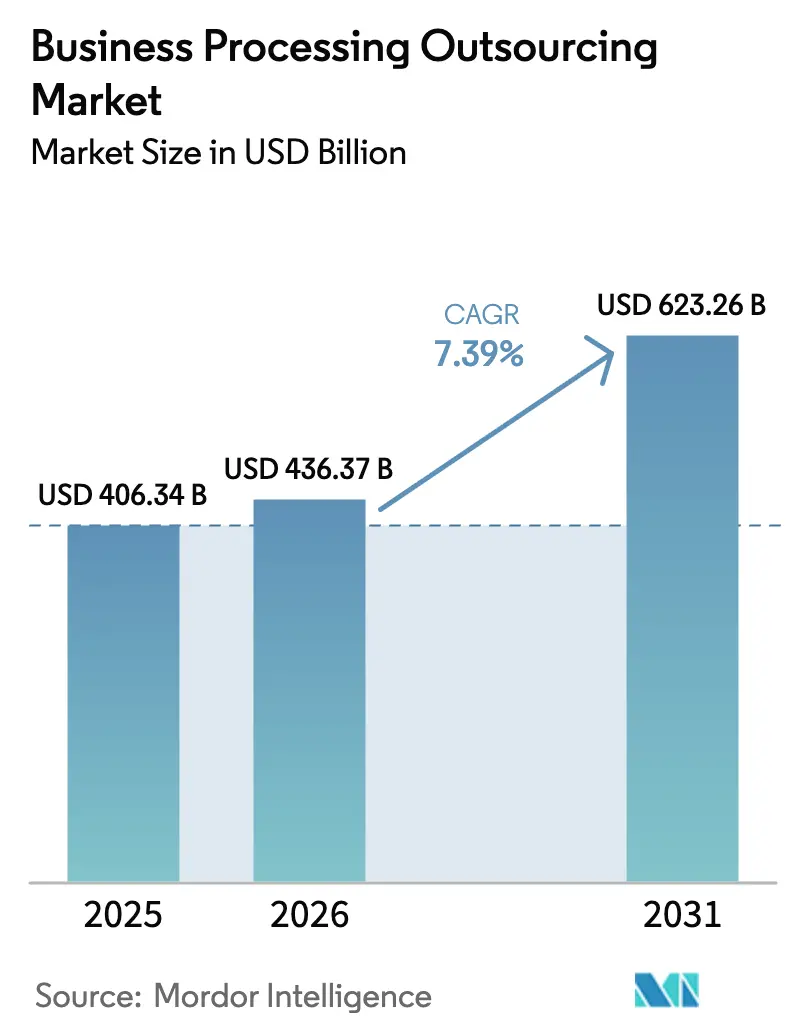

| Market Size (2026) | USD 436.37 Billion |

| Market Size (2031) | USD 623.26 Billion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Business Processing Outsourcing Market Analysis by Mordor Intelligence

The Business Processing Outsourcing Market size is projected to expand from USD 406.34 billion in 2025 and USD 436.37 billion in 2026 to USD 623.26 billion by 2031, registering a CAGR of 7.39% between 2026 to 2031.

Buyers are reallocating spend from labor arbitrage to value creation as digital transformation agendas combine with intelligent automation to lift productivity, improve service quality, and harden compliance in regulated workflows. Persistent talent scarcity in advanced economies supports demand for nearshore and offshore delivery even as pricing evolves toward outcomes and service-level attainment. Vendors that fuse AI-enabled workflows with secure data handling and audit-ready controls are positioned to win large, multi-year programs in sectors like financial services and healthcare. Regional delivery diversification continues as North American buyers balance onshore analytics with allied nearshore and offshore transaction processing to hedge data-sovereignty and geopolitical exposure.

Key Report Takeaways

- By application, customer services led with 32.14% revenue share in 2025, while human resources is projected to expand at a 10.01% CAGR through 2031.

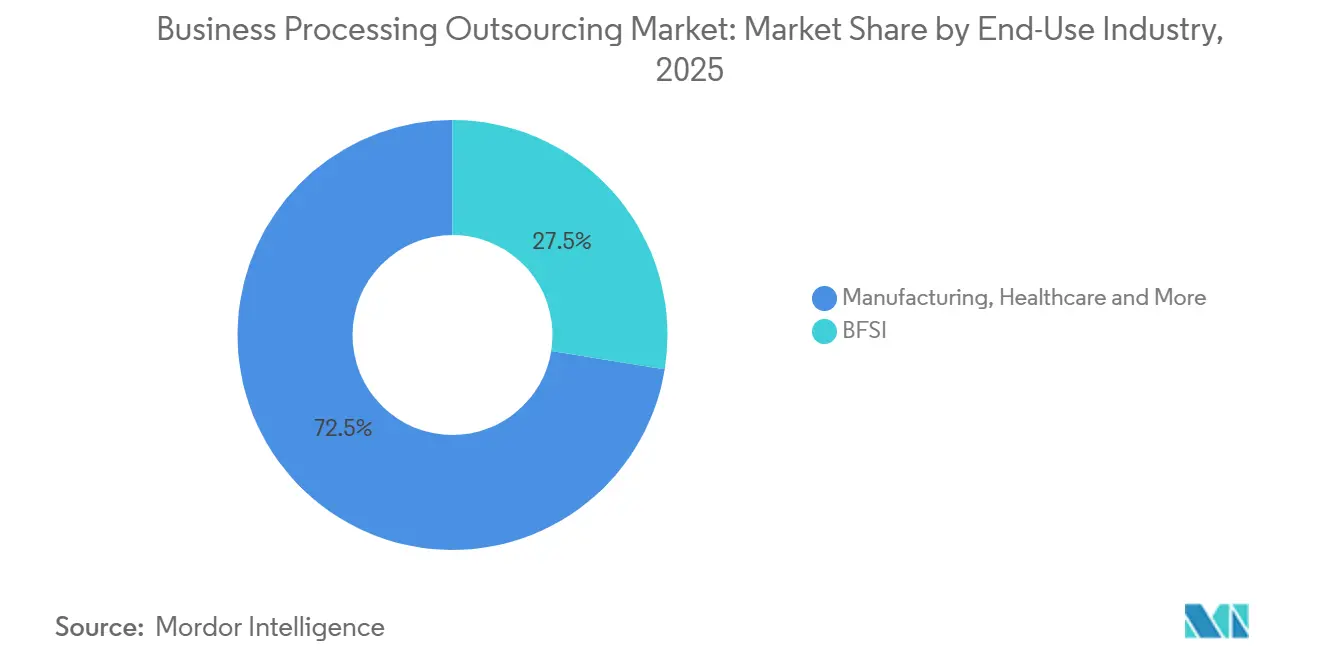

- By end-use industry, BFSI held 27.54% in 2025, while healthcare is set to grow at a 7.85% CAGR through 2031.

- By organization size, large enterprises accounted for 66.25% of spending in 2025, while small and medium enterprises are expected to advance at a 7.56% CAGR through 2031.

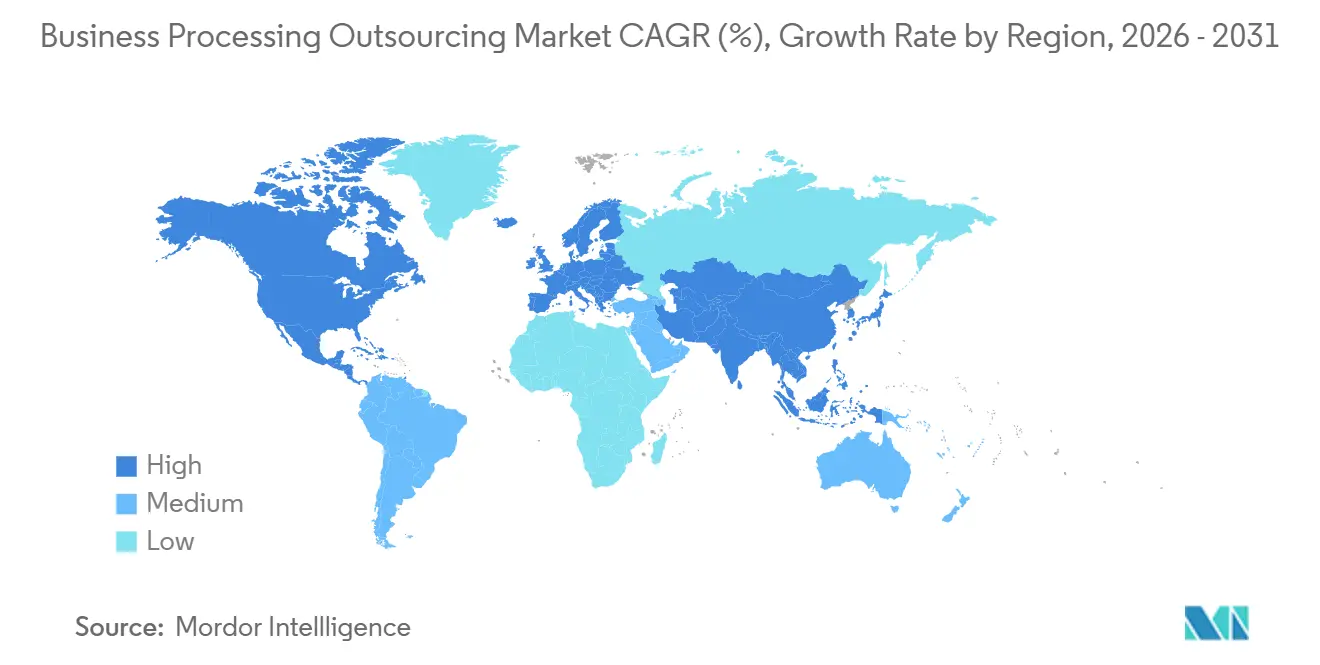

- By geography, North America retained a 43.28% share in 2025 while Asia-Pacific is projected to expand at a 9.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Business Processing Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Transformation & Hyper-Automation Demand | +2.8% | Global, highest in North America, Western Europe, Singapore, Australia | Medium term (2-4 years) |

| Cost-Optimization Amid Persistent Margin Pressures | +1.9% | Global, acute in retail, manufacturing, banking | Short term (≤ 2 years) |

| Talent Shortages In Developed Economies | +1.4% | North America, Western Europe, select Asia-Pacific | Medium term (2-4 years) |

| Rise Of As-A-Service & Outcome-Based BPO Contracts | +0.9% | North America, EU core, emerging in South America | Long term (≥ 4 years) |

| GenAI-Enabled Hyper-Personalized CX Offerings | +1.2% | Global, early in financial services, telecom, e-commerce | Medium term (2-4 years) |

| Wave Of Captive Shared-Service-Center Divestitures | +0.7% | North America, UK, Germany, emerging markets nascent | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation And Hyper-Automation Demand

Organizations face a structural imperative to digitize front and back offices, standardize processes, and embed automation at scale to sustain service levels as wage costs and compliance demands rise. Public-sector examples show how automation changes throughput and quality, with the United States General Services Administration reporting its Truman bot reviewed thousands of acquisition offers and saved more than 5,000 hours by automating form population and checks[1]Innovation Committee, CIO Council, “Robotic Process Automation in Federal Agencies,” CIO Council, cio.gov. The Social Security Administration cut processing time for returned Supplemental Security Income payments from minutes to seconds per transaction once software bots were deployed. In parallel, buyers place data governance and model oversight at the center of operating plans, especially where AI augments complex adjudication or customer support workflows subject to audit. This systemic shift rewards business processing outsourcing market providers that can orchestrate cloud platforms, automation, and supervised AI models within resilient, compliant architectures across multiple jurisdictions.

Cost Optimization Amid Persistent Margin Pressures

Operating costs from labor, energy, and regulatory compliance continue to compress margins in mature categories, sharpening the focus on variable cost models tied to service outcomes. Buyers in financial services and healthcare are re-baselining cost structures by routing transactional volume to specialized partners while retaining high-value analytics and decisioning onshore. The United States Department of Justice’s rule restricting certain bulk sensitive data transfers to specified countries is increasing design complexity and cost of data flows, which strengthens the case for hybrid models that match workload sensitivity with the right delivery location and control set. Vendors with proven certifications and audit-ready logging convert compliance responsibilities into a competitive edge, especially where they can demonstrate rapid integration with legacy systems. The business processing outsourcing market continues to evolve toward pricing that balances cost efficiency with measured outcomes such as first-contact resolution, clean claims rate, and on-time reconciliations.

Talent Shortages In Developed Economies

Labor tightness persists in 2026, particularly for roles with cognitive, digital, and interpersonal skill requirements. The United States labor market has exhibited a shortfall between job openings and available workers, and workforce participation remains below pre-2020 levels in some categories. Employers facing unfilled positions shift to global staffing models and partner with providers that can supply trained teams across time zones. The Philippines’ IT-BPM sector reported USD 38 billion in revenue and 1.82 million full-time equivalents in 2024, underscoring the depth of English-speaking talent and the role of fiscal incentives in expanding regional hubs. India’s technology sector sustained substantial employment and export momentum in fiscal 2025, reinforcing the strategic role of global capability centers and BPM delivery in closing skill gaps for multinational buyers. The business processing outsourcing market benefits when buyers rebalance their sourcing strategies to ensure continuity of service and access to scarce competencies.

Rise Of As-A-Service And Outcome-Based BPO Contracts

Contracts are shifting from seat- or effort-based billing to constructs that tie payment to resolved tickets, processed claims, verified quality checks, or other measurable outcomes. Buyers increasingly transfer efficiency risk to vendors in return for predictable unit economics and continuous improvement commitments across the term. This model requires providers to invest in analytics, workforce management, and automation to compress handle times and rework rates without compromising quality or compliance. Captive shared service centers are being divested or restructured, where third-party platforms can deliver scale, tool integration, and cost variability faster than in-house teams. The business processing outsourcing market is therefore seeing pricing innovation allied with delivery innovation, and the two reinforce each other as CIOs and CFOs seek transparency on performance and value realization over multi-year horizons.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy & Sovereignty Regulations Tightening | -1.3% | Europe, United States, China, India, global spillover | Medium term (2-4 years) |

| Rising Geopolitical Wage Inflation In Key Hubs | -0.8% | India, Philippines, Poland, Mexico, broader Asia-Pacific and South America | Short term (≤ 2 years) |

| Vendor Concentration Risk For Critical Processes | -0.5% | North America, EU financial services, and healthcare | Long term (≥ 4 years) |

| Near-Shoring Gaps, Time-Zone Staffing Bottlenecks | -0.4% | Asia-Pacific to North America corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy And Sovereignty Regulations Tightening

Cross-border data flows are re-architected as privacy and data-sovereignty regimes expand in scope, raise penalties, and demand stronger transfer safeguards. Under the European Union's GDPR, enforcement includes fines up to the greater of USD 23.5 million or 4% of global turnover, which has heightened executive attention in programs that use offshore centers to process personal data of European Union residents. The United States Department of Justice’s rule implementing Executive Order 14117 restricts certain bulk sensitive personal data transfers to countries of concern and imposes due diligence, security, and audit requirements for restricted transactions beginning October 2025. India notified rules to operationalize the Digital Personal Data Protection Act and established the Data Protection Board, setting breach notification timelines, delineating obligations for Significant Data Fiduciaries, and enabling restrictions on transfers to blocked jurisdictions[2]United States Department of Justice, “Preventing Access to U.S. Sensitive Personal Data and Government-Related Data by Countries of Concern,” Federal Register, federalregister.gov. The European Union Data Act is moving to full application, setting portability and interoperability obligations for cloud and edge services and adding safeguards against unlawful non-EU government access to non-personal data held in the European Union. These regimes require segmenting sensitive workloads, renegotiating contracts, and investing in audit trails and localized data handling, all of which increase delivery complexity and cost in the business processing outsourcing market.

Rising Geopolitical Wage Inflation In Key Hubs

Wage dynamics in established offshore and nearshore locations are tightening as demand for digital skills outpaces supply and as local inflation pressures vendor compensation budgets. Employers in multiple regions report difficulty filling roles, which sustains upward wage drift across contact center, finance, and specialized back-office positions. Buyers with long-duration contracts are seeing more frequent rate reviews to reflect local market conditions and the need to fund upskilling for AI-augmented workflows. Time-zone aligned hubs in the Americas remain attractive for North American buyers, yet rapid demand has lifted certain nearshore rates since 2024, prompting multi-country delivery footprints to reduce exposure. Public programs and industry associations in key hubs continue to invest in workforce development, but the net effect for the business processing outsourcing market is narrower arbitrage and a mix shift toward higher-value, knowledge-intensive services that justify premium pricing. These changes reinforce the importance of automation, performance management, and retention strategies to sustain margins without eroding service quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Customer Services Propel Demand Across Channels

Customer services accounted for 32.14% of the business processing outsourcing market in 2025, making it the largest application. Human resources is the fastest-growing segment, with a projected 10.01% CAGR through 2031. The dominance of customer services highlights the importance of omnichannel engagement across voice, chat, email, social media, and in-app support. Metrics like first-contact resolution and satisfaction scores directly impact revenue retention. Buyers are upgrading knowledge management, routing, and quality systems to ensure bots hand off complex issues to trained agents with access to context and history. Public-sector automation demonstrates how repetitive tasks can be streamlined while maintaining accuracy, influencing commercial service desk operations. Customer services now integrate analytics, coaching, and virtual assistants in multi-tier support models.

Human resources workflows are expanding as firms outsource recruiting, payroll, benefits administration, and compliance to partners who manage peak cycles and enforce standardized controls. Tight labor markets and evolving policies drive demand for partners skilled in onboarding, credentialing, and auditing across jurisdictions. Vendors focus on data privacy and consent management, especially for cross-border payroll records. AI-enabled document parsing for resumes and benefits forms is advancing, with human oversight for sensitive decisions. Finance and accounting, procurement, and sales and marketing remain critical domains, and their integration with HR and customer operations improves process visibility and forecasting for volumes and staffing.

By End-Use Industry: Banking Leads While Healthcare Surges

Banking, financial services, and insurance accounted for 27.54% of the business processing outsourcing (BPO) market in 2025, making it the largest end-use segment. Healthcare is projected to grow at a 7.85% CAGR through 2031. Financial institutions increasingly rely on partners for high-volume tasks like onboarding, reconciliations, and dispute resolution, emphasizing auditable controls and resilient technology. The EU’s Digital Operational Resilience Act, effective in 2025, tightened oversight of critical third-party ICT providers, raising standards for vendors supporting European financial entities. Program governance now includes contingency testing, incident reporting drills, and subcontracting transparency, paired with AI-augmented document handling under human supervision[3]European Commission, “Data Act enters into force: what it means for you,” European Commission, europa.eu.

Healthcare growth stems from administrative complexities, coding and claims burdens, and the need to protect sensitive health information. Delivery footprints are shifting toward onshore or allied-nation infrastructure for sensitive workloads. United States regulations and standards like HIPAA govern how vendors store and process personal health information. Providers are enhancing audit capabilities and role-based access to reduce risks and improve throughput. Vendors demonstrating clean claims rates, reduced accounts receivable days, and responsive patient scheduling while meeting compliance obligations are favored. Across manufacturing, retail, IT, and telecom, adoption varies by digital maturity and regulations, with a shared focus on measurable outcomes and AI-driven control assurance.

By Organization Size: Large Enterprises Dominant, SMEs Accelerating

Large enterprises accounted for 66.25% of the business processing outsourcing (BPO) market in 2025, driven by the scale and governance needs of global buyers. SMEs are projected to grow at a 7.56% CAGR through 2031. Big programs spanning geographies and functions require proven methodologies, interoperable platforms, and compliance with diverse regulations. Large buyers often use a hub-and-spoke model, retaining strategic functions in captive centers while outsourcing repeatable tasks to partners who adjust headcount and automation for seasonal peaks. Providers invest in transformation roadmaps and analytics to monitor quality and throughput in real time, with success measured by unit costs, accuracy, cycle times, and reduced re-work rates.

SMEs, while smaller in spending, are closing capability gaps with modular service catalogs. Cloud delivery and no-code tools enable service adoption without heavy capital investment. In 2025, India scaled tech exports and workforce, while the Philippines created jobs, expanding the talent pool for SMEs via managed services. Higher compliance overhead for SMEs drives vendors to bundle privacy and security controls. As these offerings mature, SMEs increasingly adopt multi-function engagements, combining customer service, finance, and HR support to enhance efficiency.

Geography Analysis

North America accounted for 43.28% of global spending in the business processing outsourcing market in 2025, with the United States driving demand for cost efficiency, talent augmentation, and compliance across regulated workflows. United States employers faced persistent vacancies across various occupations, maintaining reliance on offshore and nearshore partners for scalability and specialized skills. The United States Professional and Business Services supersector, including Administrative and Support Services tied to outsourcing, employed over 22 million people by late 2025, with average hourly earnings rising year over year. Federal regulations on sensitive data transfers prompted workload segmentation by sensitivity, with onshore or allied-nation infrastructure supporting critical use cases. Canada and Mexico remained key nearshore options for United States buyers seeking time-zone alignment and reduced cross-border risks.

Asia-Pacific is the fastest-growing region, projected to expand at a 9.11% CAGR through 2031. Buyers scaled programs in India, the Philippines, and other hubs, blending English proficiency with technical talent. The Philippines reported USD 38 billion in IT-BPM revenue and 1.82 million full-time equivalents in 2024, supported by policy incentives driving regional expansion. India’s technology sector saw growth in exports and employment in fiscal 2025, with its global capability centers reinforcing its role in complex operations. Governments in the region invested in digital infrastructure and skills to attract programs and move up the value chain. Vendors in Asia-Pacific are building capabilities in data labeling, model supervision, and automation maintenance to support AI-augmented work.

Europe’s market is shaped by strict privacy and operational resilience standards. The EU Data Act introduced interoperability rules for cloud and edge services, impacting BPO architectures reliant on multi-tenant platforms. Central and Eastern Europe attracted programs valuing proximity and EU-law alignment, with Poland’s business services sector increasing headcount and knowledge-intensive roles through 2024. Western Europe prioritized data governance and transparency, favoring providers with resilient operations. Nearshore hubs invested in language coverage and cybersecurity to meet procurement standards in financial services and healthcare, advancing under compliance-driven constraints.

Regulatory Landscape

Regulation affecting global BPO delivery is increasingly centered on data privacy, cross-border transfer controls, and operational resilience for regulated workflows. In the European Union, GDPR enforcement heightens executive scrutiny of offshore processing, with fines up to the greater of USD 23.5 million or 4% of global turnover, while the EU Data Act is moving to full application and introduces portability and interoperability obligations for cloud and edge services used in multi-tenant delivery models.

In the United States, the Department of Justice rule implementing Executive Order 14117 introduces restrictions and due diligence, security, and audit requirements for certain bulk sensitive personal data transfers to countries of concern, with restricted-transaction requirements beginning in October 2025. State-level privacy regimes are also tightening, with the California Privacy Protection Agency implementing updated CCPA requirements effective January 1, 2026, including risk assessments, automated decision-making technology controls, and cybersecurity audits, shaping how providers document controls and govern AI-assisted processes. India is operationalizing the Digital Personal Data Protection Act through notified rules and the Data Protection Board, adding compliance timelines and breach notification obligations that influence contract terms and delivery architecture for programs touching Indian and cross-border data.

Value Chain Analysis

The BPO value chain begins with client process discovery and transition (process mapping, baseline KPIs, and risk assessments), then moves into solution design and delivery that blends people, workflow tools, and increasingly AI-enabled automation. Providers assemble delivery using onshore governance, nearshore language and time-zone coverage, and offshore scale hubs, with shared technology layers for case management, knowledge, QA, workforce management, and security controls, including SOC 2 and ISO-aligned practices for regulated buyers. Third-party dependencies that shape service quality and compliance include cloud platforms, identity and access management, monitoring and logging, and data protection tooling, alongside local talent pipelines and industry-aligned training programs in major delivery locations.

Downstream, ongoing operations emphasize continuous improvement and commercial governance, with contracts shifting toward outcome-linked constructs that reward cycle-time reduction, first-contact resolution, clean-claims rates, and on-time reconciliations. Evidence of the chain shifting away from pure labor models shows revenue expansion with minimal workforce growth among large providers, supporting investment in platforms and automation to decouple throughput from headcount. At the ecosystem level, industry bodies and delivery hubs are also repositioning toward broader customer experience and higher-skill services, reflecting the move from traditional contact center work to CX management, analytics, and AI-augmented operations.

Competitive Landscape

The business processing outsourcing market is moderately fragmented. Global integrators secure multi-year, multi-country programs, while regional specialists and boutiques focus on specific verticals and languages. Large providers differentiate with proprietary platforms integrating workflow orchestration, analytics, and supervised AI, enabling outcome-linked pricing and continuous improvement. Buyers prioritize integrated solutions and reference architectures for secure data management, automated controls, and real-time performance monitoring. Compliance certifications are standard in banking and healthcare, with procurement teams demanding resilience and incident response capabilities. Regulatory changes, such as the DOJ's sensitive data transfer rule, favor vendors offering multi-jurisdiction delivery anchored in onshore or allied-nation data centers.

Strategic moves highlight the shift to technology-driven solutions. Teleperformance plans to roll out real-time AI-powered accent solutions in Indian centers by 2025, enhancing customer interactions and reducing churn risks through AI-augmented voice operations. TELUS International collaborates with software providers to integrate generative AI and sentiment analytics into live support[4]TELUS International, “Resources and Insights,” TELUS International, telusinternational.com. Konecta partners with a major hyperscaler to embed large language models for customer interactions, summarization, and workforce analytics, supported by enterprise collaboration tools. These initiatives reflect the convergence of contact center operations with AI and cloud technologies to reduce handling times and improve quality.

Operational transformation platforms drive contract renewals and expansions. Accenture digitizes finance, supply chain, and customer operations, leveraging embedded analytics and automation to streamline processes and minimize rework while ensuring rigorous controls. Genpact aligns incentives with client goals in claims, disputes, and financial operations through outcome-based structures and AI-driven diagnostics. Buyers under strict European or United States regulations prioritize providers with SOC 2 and ISO 27001 certifications, clear subcontracting oversight, and successful customer-led penetration tests. Competitive advantages now depend on performance transparency, governance maturity, and technological leverage, alongside geographic presence and scale.

Business Processing Outsourcing Industry Leaders

Accenture plc

Tata Consultancy Services Limited

Concentrix Corporation

Teleperformance SE

Genpact Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary whitespace is in regulated, audit-heavy operations where buyers want AI-enabled productivity without compromising governance, data minimization, and model oversight. Tightening rules on cross-border data handling and operational resilience are pushing more segmented delivery designs, with onshore or allied-nation locations for sensitive data and offshore for lower-risk volume. This creates opportunities for providers that can offer reference architectures, localized processing options, and audit-ready controls across multiple jurisdictions. In BFSI and healthcare, demand centers on capabilities such as secure workflow orchestration, traceable decision support, and measurable outcomes tied to risk controls and service quality.

Commercial models and service catalogs are also opening room for BPaaS-style offerings that package end-to-end functions on standardized platforms, allowing buyers to contract for outputs rather than effort. Adoption signals for AI-enabled services are strengthening: the US Census Bureau Business Trends and Outlook Survey reported in April 2026 that 62% of US firms in the Professional, Scientific, and Technical Services sector use generative AI, reinforcing enterprise familiarity with AI as an operating tool and raising expectations for automation embedded inside outsourced processes. Delivery hubs are simultaneously retooling toward higher-skill work as AI reduces reliance on labor scale alone, supporting opportunities in knowledge-intensive CX, finance operations, and model supervision services where providers can document control effectiveness and productivity gains.

Recent Industry Developments

- July 2026: Genpact partnered with Nestle Business Solutions to establish a new Global Capability Center in Hyderabad, India, combining process operations with AI and process intelligence capabilities. The partnership reflects client demand for hybrid models that blend third-party expertise with GCC structures to modernize finance and other back-office workflows. It also reinforces India’s role as a delivery and transformation hub for enterprise operating-model redesign.

- June 2026: Accenture agreed to acquire Industries eXcellence Group (IndX), a division of Engineering Group, to strengthen capabilities for software and automation solutions linked to Siemens Digital Industries. Expanding industrial software and automation expertise supports BPO-adjacent transformation programs where operational workflows converge with manufacturing, supply chain, and enterprise platforms. The deal adds depth in engineering-led process modernization rather than labor-centric outsourcing.

- March 2026: Accenture completed the acquisition of UK-based AI firm Faculty to broaden its enterprise AI governance capabilities across customer service and finance workflows. The acquisition broadens Accenture's AI engineering and model deployment capabilities across managed operations and regulatory-compliant process automation. It signals a deeper integration of AI assets within Accenture's managed services portfolio.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The market covers third-party delivered business process outsourcing services where an external provider runs defined front office and back office activities for a client, and charges on a contract basis (onshore, nearshore, or offshore delivery). It is measured as provider revenue for the service work completed.

Scope exclusions: Captive shared service centers and pure IT infrastructure outsourcing are excluded, and internal corporate labor costs are not counted as market revenue.

Segmentation Overview

- By Application

- Human Resource

- Procurement

- Information Technology

- Sales and Marketing

- Finance and Accounting

- Customer Service

- Other Applications

- By End-Use Industry

- BFSI

- Manufacturing

- Healthcare

- Retail

- IT and Telecom

- Other End Users

- By Organization Size

- Large Enterprises

- Small & Medium Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Benelux (Belgium, Netherlands, Luxembourg)

- Nordics (Sweden, Norway, Denmark, Finland, Iceland)

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

To build the basic structure of the market, we start with public statistics and reference series that explain how outsourcing demand rises and falls with the economy and business formation. Common starting points include sources such as the US Bureau of Labor Statistics, the World Bank, the OECD, and the International Labour Organization for macro and workforce indicators that influence outsourced process volumes.

We also review open information that shows how service providers and buyers are behaving, such as SEC filings, annual reports, investor presentations, and major contract announcements covered by reputable business press. For cross checks, we selectively use paid subscriptions for company financials and intelligence, news and financials, patent databases, and global contracts and tenders to confirm deal timing, client industries, and service line mix. The sources listed here are illustrative, and many other public and subscription sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test the service scope boundaries, validate pricing and delivery mix shifts, and confirm what share of spending is truly outsourced versus kept in house. We spoke with provider side leaders, delivery and pricing managers, and buyer side sourcing and operations teams across APAC, EMEA, and the Americas, and then we used those inputs to finalize assumptions where desk sources were thin.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 47% |

| Mid tier: 46% | Functional/Unit leaders: 31% | EMEA: 30% |

| Smaller Players: 15% | Managers: 57% | Americas: 23% |

Market-Sizing & Forecasting

Sizing begins with a top down build where outsourcing addressable spend is reconstructed from enterprise operations intensity and services spend signals, and then filtered through outsourcing penetration by function and industry. After that, results are corroborated with selective bottom-up approximations, such as sampled provider revenue by service line, checked ASP ranges, and a few channel checks around contract values, so totals can be adjusted when they drift from real buying patterns.

Inputs that matter for BPO include outsourced headcount intensity by process, deal signings and renewal cycles, onsite versus offshore delivery mix, wage inflation in key delivery locations, and the share of work shifting to more automated workflows (which changes both volumes and pricing). When a bottom-up datapoint is missing for a smaller geography or niche process, the gap is handled using peer market ratios and buyer mix indicators, and it is only kept if it matches interview feedback.

For forecasting, scenario analysis is used around a core demand outlook, because BPO spending can swing with macro conditions and cost takeout programs. The variable outlooks are anchored in what practitioners expect for pricing resets, productivity changes, and contract duration trends, followed by region level normalization to avoid overstating rebounds after one-off years.

Data Validation & Update Cycle

Validation is done in layers so that any single source does not over steer the final number. Model outputs are compared against independent signals such as large contract activity, provider revenue trend direction, delivery location wage moves, and regional enterprise spending indicators, and then variance checks are run to spot outliers by region and service type.

Before sign-off, the logic and math are reviewed by another analyst, and questionable jumps trigger a re-check of assumptions and, when needed, a short re-contact with sources who can clarify pricing or scope. Reports refresh annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the most current view available.

Mordor Intelligence's Business Processing Outsourcing Market Size Compared With Other Published Estimates

Published market sizes for BPO rarely line up perfectly because each publisher makes different choices on what counts as BPO revenue and how they time their currency conversions and price assumptions. In practice, even small differences in what is included as process outsourcing, and when it is counted, can move the total by tens of billions.

A refresh-led gap shows up when exchange rates and ASP resets are updated at different points in the year, which can shift the reported value even if underlying volumes are similar, and Mordor Intelligence ties the estimate to a defined update timestamp and re-validates pricing bands against recent contract and provider disclosures before locking the current-year figure.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 436.37 B (2026) | |

| Global Research Publisher A | USD 358.60 B (2026) | Uses a narrower revenue pool that appears to undercount non-voice back office work in some regions, and the implied pricing progression looks less responsive to recent wage inflation and contract repricing cycles. |

| Industry Publisher B | USD 434.99 B (2026) | The estimate is built around IT services spending definitions, so adjacent IT outsourcing and products can bleed into the total, and the currency conversion is applied on a different exchange-rate timing that shifts the reported USD value. |

The table shows that the spread mainly comes from scope boundaries plus how pricing and FX timing are handled in the year of measurement. By keeping assumptions traceable to contract cycles, delivery mix, and repeatable validation checks, we can explain where differences come from instead of leaving them as unexplained rounding noise.

Key Questions Answered in the Report

What is the business processing outsourcing market size in 2026, and how fast is it growing?

The business processing outsourcing market size is USD 436.37 billion in 2026 and is projected to reach USD 623.26 billion by 2031 at a 7.39% CAGR.

Which applications lead demand within business processing outsourcing, and which are growing fastest?

Customer services led with 32.14% of 2025 revenue, while human resources is projected to grow at a 10.01% CAGR through 2031.

Which end-use sectors drive the most spending and the highest growth?

Banking, financial services, and insurance held 27.54% in 2025, while healthcare is forecast to expand at a 7.85% CAGR through 2031.

How is regional demand distributed for business processing outsourcing?

North America held 43.28% in 2025, while Asia-Pacific is set to expand at a 9.11% CAGR through 2031, with India and the Philippines anchoring growth.

What regulatory changes most affect cross-border delivery models?

The DOJ’s rule on bulk sensitive data transfers and the EU Data Act’s interoperability and access safeguards are reshaping data flows and vendor selection criteria.

What signals the ongoing tightness in North American labor markets that sustains outsourcing demand?

United States labor data in 2025 show persistent tightness and rising wages in key services categories, supporting reliance on global delivery partners.

Page last updated on: