Vietnam OOH And DOOH Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

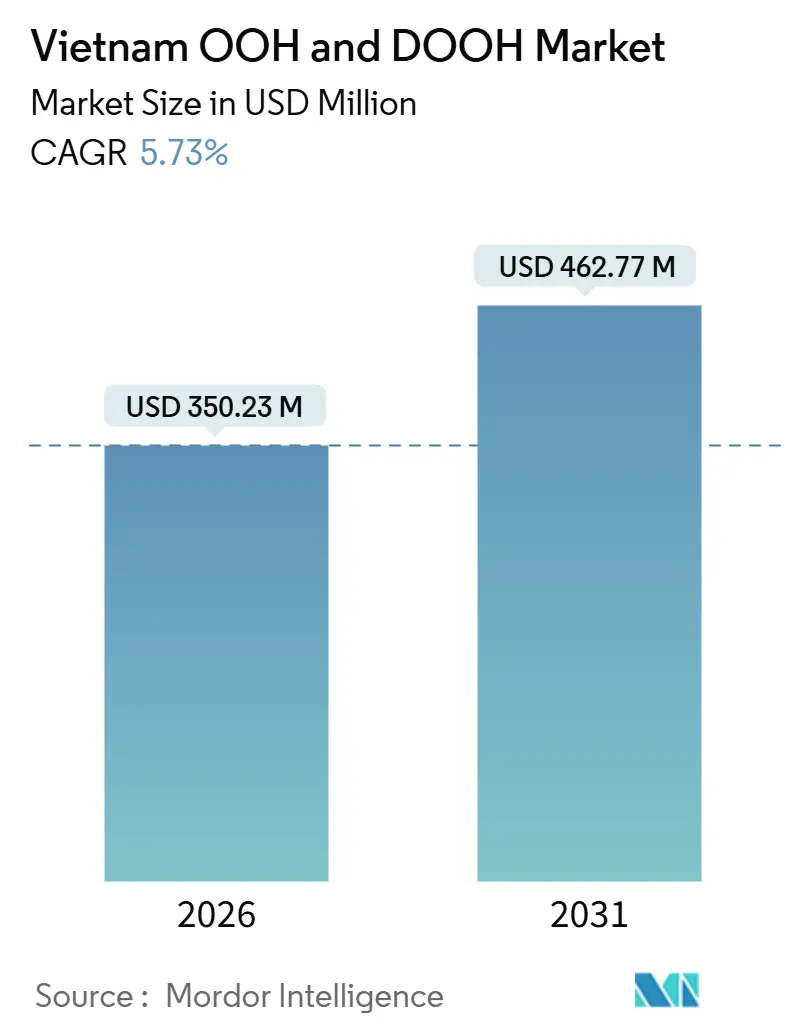

| Market Size (2026) | USD 350.23 Million |

| Market Size (2031) | USD 462.77 Million |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

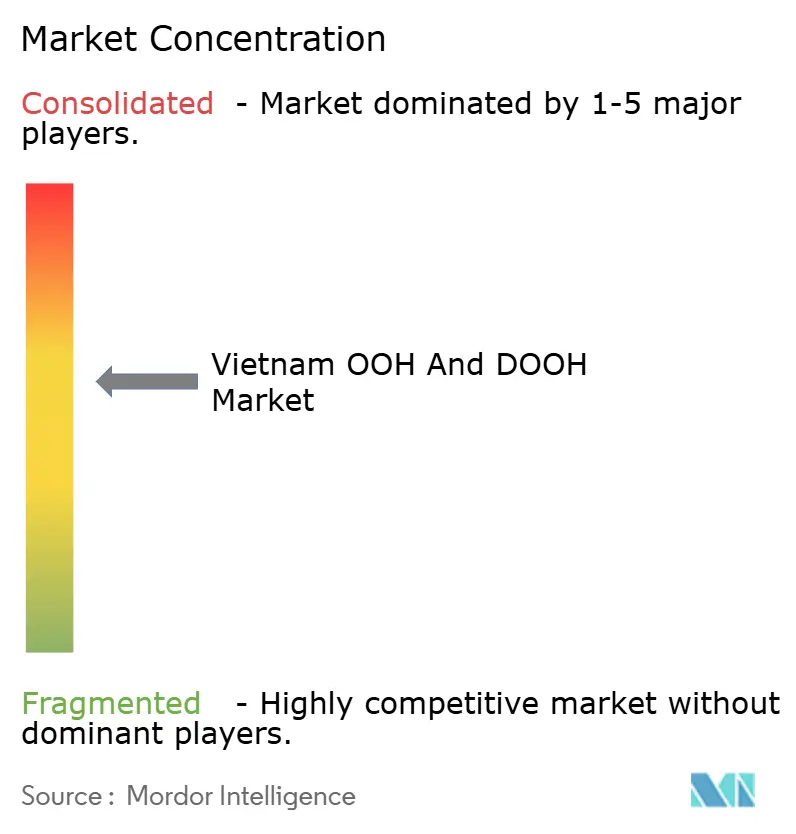

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam OOH And DOOH Market Analysis by Mordor Intelligence

The Vietnam OOH and DOOH market size stood at USD 350.23 million in 2026 and is projected to reach USD 462.77 million by 2031, advancing at a 5.73% CAGR. Growth stems from the steady pivot toward screen-based inventory that integrates with the nation’s smart-city build-out, metro expansion, and retail-modernization initiatives. Digital formats already dominate, and programmatic buying adds speed and targeting that static boards cannot match. Brands also favor high-dwell venues such as elevators, malls, and metro stations where exposure lasts far longer than on arterial roads. Recent legislation that clarifies permitting and mandates playback logs is curbing fraud while raising compliance costs, which favors larger operators able to absorb the incremental outlay.

Key Report Takeaways

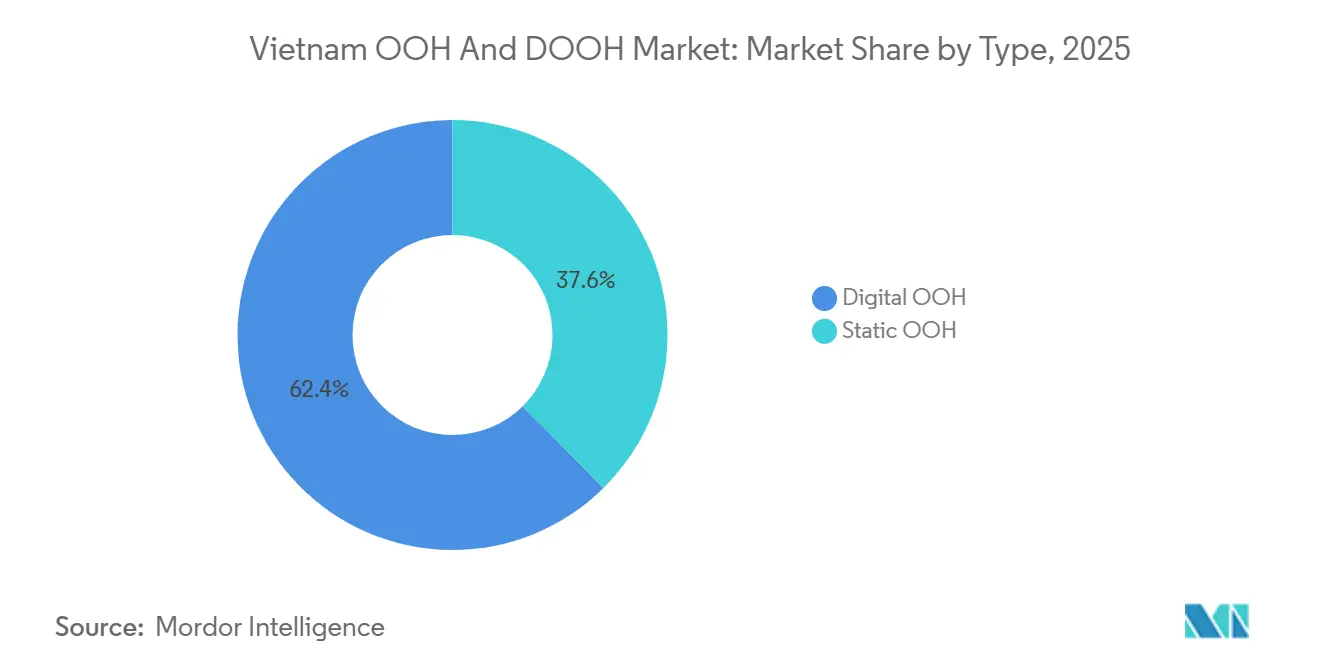

- By type, digital OOH captured 62.39% of Vietnam OOH and DOOH market share in 2025, while programmatic OOH is forecast to post the fastest 6.45% CAGR through 2031.

- By application, billboards led with 41.322% revenue share in 2025, whereas place-based media is on track to expand at a 6.11% CAGR to 2031.

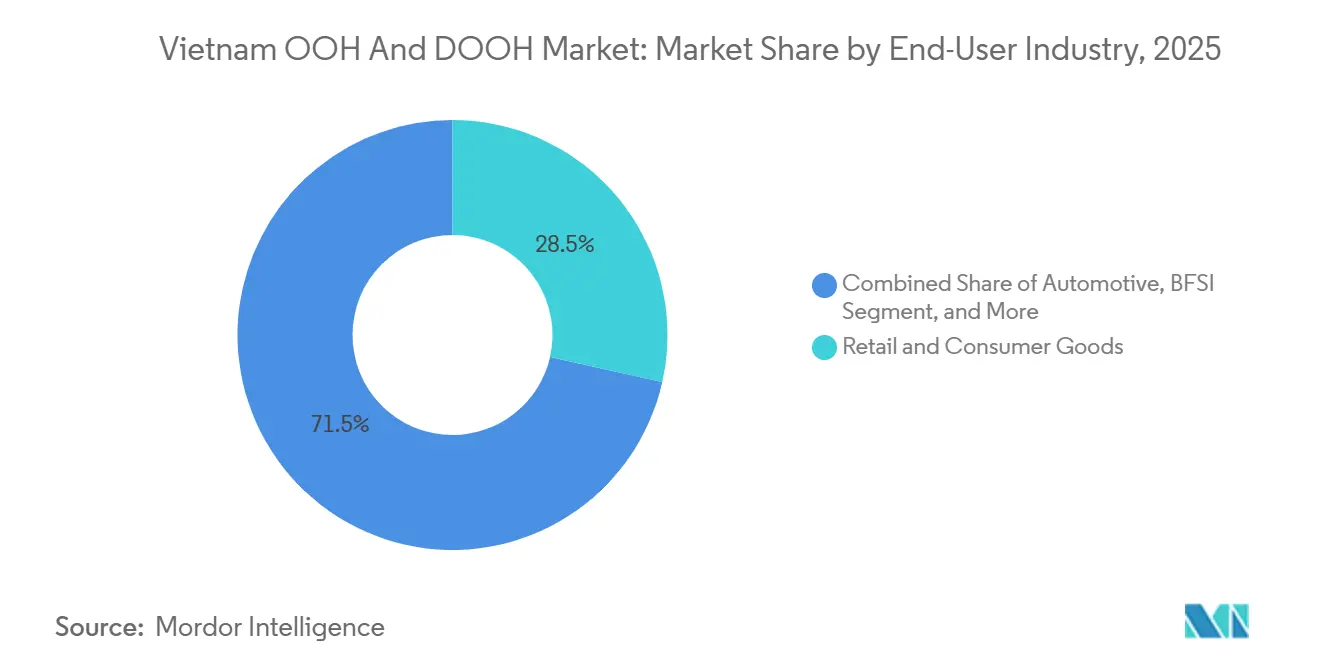

- By end-user industry, retail and consumer goods accounted for 28.51% of 2025 spending, while healthcare is projected to be the fastest riser at a 6.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam OOH And DOOH Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ongoing Shift Toward Digital Advertising Driven by Smart-City Projects | +1.2% | Hanoi, Ho Chi Minh City, Phu Quoc | Medium term (2-4 years) |

| Rising Adoption of Connected Screens Enabling Real-Time Campaign Optimisation | +0.9% | National, concentrated in Hanoi and Ho Chi Minh City | Short term (≤ 2 years) |

| Accelerating Growth of Programmatic DOOH Exchanges in Vietnam | +1.1% | National, early adoption in major cities | Medium term (2-4 years) |

| Integration of Mobile Location Data for Accurate Post-Exposure Attribution | +0.7% | Hanoi, Ho Chi Minh City, Da Nang | Medium term (2-4 years) |

| Government-Led Urban Transit Expansion Creating New Advertising Inventory | +1.0% | Ho Chi Minh City, Hanoi | Long term (≥ 4 years) |

| Retail-Media Networks Rolling Out Digital Screens Inside Modern Trade Stores | +0.8% | National, spill-over to tier-2 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Smart-City Projects Propel Digital Adoption

Vietnam’s national digital program targets 5G in all provinces by 2025, creating bandwidth that supports networked screens across elevators, kiosks, and transit platforms. Phu Quoc’s 2024 pilot installed 150 kiosks that sync tourism offers with ferry schedules, illustrating how civic connectivity yields fresh advertising real estate. Ho Chi Minh City’s USD 40 billion metro plan will add six lines by 2030 and roughly 2,000 panels, each capable of daypart scheduling and weather triggers. Hanoi already logs 120 million annual metro rides, giving advertisers captive dwell times of four to six minutes per trip. As infrastructure digitizes, budgets shift from highway billboards toward measured, high-traffic transit hubs.

Connected Screens Enable Real-Time Updates

Chicilon Media runs 36,000 elevator screens on a centralized CMS that lets brands toggle creative by building profile, hour, and tenant mix. An April 2024 pact with VTC Digital Television synchronized elevator screens with broadcast spots, completing a cross-channel loop that tracks users from lift exposure to online action. Admicro’s AdX platform, which serves 45 billion monthly impressions, ports dynamic-creative learnings back into DOOH in the same flight, tightening feedback cycles. Research shared at a 2025 industry forum showed 97% of respondents notice elevator screens and 69% trust the content, bolstering FMCG adoption. These findings accelerate spend toward venues where content can be swapped in minutes rather than days.[1]Vietnam Investment Review, “Phu Quoc Smart City Pilot Advances with IoT Sensors,” vir.com.vn

Programmatic DOOH Exchanges Gain Traction

Vistar Media went live in Vietnam in 2022 and now connects demand-side platforms to inventory from Asiaray, Globaltronics, and JCDecaux via a single API that supports reach modeling and device-ID passback. By late 2024 its Asia-Pacific roster added 35 media owners and 139,000 venues. Hivestack’s linkage with Broadsign means brands can bid for airport LEDs or metro pillars in real time, shrinking setup from weeks to hours. A 2023 joint venture between NTT DOCOMO and Vie BOARD injects mobile-location data so campaigns can be optimized by visit frequency and dwell time. Automation thus unlocks budget flexibility and aligns DOOH with the buying norms of online video and display.

Mobile Location Data Improves Attribution

Marketers now fuse handset pings with exposure logs to close the loop between impression and action. Device-ID passback enables retargeted mobile ads after a commuter views a metro-station screen, while Foursquare segments filter shoppers by category affinity. Early pilots show that weather-triggered beverage ads on station screens followed by synced promotions on ride-hailing apps lift redemption by 25% against static scheduling. As accuracy rises, planners feel confident shifting brand-building funds formerly ring-fenced for online video into high-reach DOOH environments that promise similar traceability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Measurement standardisation gaps | -0.6% | Nation-wide | Medium term (2-4 years) |

| High screen install and electricity costs in tier-2 cities | -0.5% | Can Tho, Hai Phong, Nha Trang | Short term (≤ 2 years) |

| Provincial zoning limits on new digital billboards | -0.4% | Hanoi, Ho Chi Minh City, provincial capitals | Long term (≥ 4 years) |

| Media fragmentation dilutes static reach | -0.3% | Nation-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Measurement Standardisation Gaps Limit Budgets

Compass Tech has drafted 33 metrics aligned with ESOMAR, yet media owners still publish traffic counts that omit visibility factors, forcing global advertisers to haircut Vietnam allocations by up to 15%. Law 75/2025 requires playback logs but stops short of third-party audience audits, leaving the proof-of-reach question unresolved. Without a body comparable to America’s Geopath, planners lack a neutral yardstick, so DOOH competes for spend on storytelling, not on verified delivery. Until a consensus methodology emerges, national budgets will stay weighted toward online channels where impressions are audited server-side.[2]Compass Tech, “Largest Outdoor Advertising Measurement Company in Vietnam,” compasstech.asia

High Screen Install and Electricity Costs in Tier-2 Cities

Electricity tariffs in Can Tho, Hai Phong, and Nha Trang run 20–30% higher than Hanoi averages, and certified technicians command premium wages, pushing LED payback horizons beyond acceptable thresholds for smaller owners. AD Mart’s 2025 investment in ten-color UV printing positions static boards as a cheaper fallback in these markets, but static units cannot provide rich analytics. Moreover, some provinces have yet to publish zoning maps required by Decree 342/2025, adding legal opacity. The result is a lopsided footprint in which the Vietnam OOH and DOOH market concentrates inventory in two megacities, hindering campaigns that target rising middle-income consumers in secondary locations.[3]Vietnam Electricity, “Electricity Tariff Schedule 2025,” evn.com.vn

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Programmatic Automation Reshapes Buying Workflows

Programmatic OOH is forecast to expand at a 6.45% CAGR through 2031, outpacing other digital sub-formats because brands crave real-time control over spend. Vistar Media’s integration of 139,000 regional venues, plus Hivestack’s airport and metro ties, means traders can buy premium panels through the same DSPs used for online video. This automated slice of the Vietnam OOH and DOOH market size is expected to command a larger share as sophisticated buyers migrate away from fixed-rate LED loops. Static OOH still held 37.61% share in 2025 and remains viable where electricity costs or zoning rules block LED rollouts.

Screen-based inventory benefits from Decree 342/2025, which obliges all networked units to store one-year logs and verify advertiser identity, a process that static posters cannot fulfill without laborious audits. Operators such as DatVietOOH are experimenting with QR codes on printed boards to capture mobile engagement, yet capital inflows clearly favor LEDs capable of generating audit trails. The regulation thus cements the long-term shift toward automated, measurable formats within the broader Vietnam OOH and DOOH market.

By Application: Place-Based Screens Capture Retail Footfall

Billboards retained 41.322% usage in 2025, but malls, elevators, and transit hubs are winning budget thanks to closed-loop attribution. Vincom Retail operates 88 malls that host screens at entrances, food courts, and parking lots, reaching 200 million annual visitors. WinCommerce plans 1,000–1,500 new stores in 2026, each outfitted with POS screens linked to loyalty data. These deployments signal why place-based assets are set to climb at a 6.11% CAGR and why advertisers find the Vietnam OOH and DOOH market size inside retail corridors so attractive.

Transport venues supply additional scale. Ho Chi Minh City’s metro Line 1 logged 15 million riders in its first quarter and displays 120 panels with average dwell times of five minutes. Goldsun Focus Media’s exclusive rights across 14 airports, now expanding to eight more, broaden reach among affluent travelers. While street furniture remains niche due to creative caps, the Ministry of Transport’s 2025 directive ensures every new mobility corridor will include revenue-sharing digital media, reinforcing the ascendancy of high-dwell placements.

By End-User Industry: Healthcare Campaigns Leverage Interactive Technology

Retail and consumer goods contributed 28.51% of 2025 outlays, yet healthcare is the fastest climber at 6.95% CAGR. MSD’s March 2025 HPV initiative used 3D projection mapping and AI avatars across three cities, engaging 50,000 participants and showcasing how interactive assets amplify public-health messaging. ADCREW’s Wi-Fi marketing in hospitals proves that screens can guide patient decisions while satisfying privacy rules. These breakthroughs ensure the Vietnam OOH and DOOH market remains a fertile canvas for pharmaceutical and wellness brands.

Automotive and BFSI still allocate robust sums to highway LED arrays and metro concourses to influence commuters with high disposable income. Real estate developers favor large-format boards near project sites, whereas consumer electronics vendors leverage mall-based LEDs for product demos via QR codes. Tourism authorities expect 10–15% higher hospitality spend in 2026 as international arrivals rebound, channeling fresh budgets into airport and coastal-transit panels.

Geography Analysis

Hanoi and Ho Chi Minh City jointly attracted close to 70% of national spend in 2025, a dominance driven by higher population density, diversified inventory, and metro lines that guarantee captive eyeballs. Line 1 in Ho Chi Minh City alone adds nearly 2,000 potential panels once the six-line build-out completes, creating a daily audience of 2 million riders. Hanoi’s three operational lines tallied 120 million journeys in 2024, offering four- to six-minute platform dwell windows that advertisers exploit for frequency gains.

Secondary cities confront cost headwinds. Electrical tariffs are up to 30% higher than in the capital, and the scarcity of skilled installers inflates project budgets. Regulatory lag compounds the issue; several provinces have yet to release zoning maps that legitimize digital signage, so operators postpone investment. Consequently, the Vietnam OOH and DOOH market maintains a bifurcated profile with premium reach clustered in two megacities and a long tail of static boards elsewhere.

Phu Quoc’s smart-city pilot shows the upside of municipal sponsorship. Its 150 kiosks synchronize hotel occupancy data with ferry times, delivering contextually relevant travel advertising. The Ministry of Culture, Sports and Tourism aims for up to 23 million international visitors in 2026, a goal that will incentivize coastal provinces to streamline permitting so they can monetize rising tourist footfall through digital kiosks and transit screens.

Competitive Landscape

Goldsun Focus Media commands 51% of traditional OOH via more than 15,000 screens across 2,000 buildings and holds exclusive rights in 14 airports, a moat deepened by plans to cover eight regional hubs by 2027. Chicilon Media rules elevator DOOH with a 92% slice of that micro-segment and has used a USD 38 million VinaCapital injection to extend into malls and transit. JCDecaux Vietnam and Koa-Sha Vietnam specialize in premium metro and airport concessions, while CPX Vietnam, Citicom, and Masscom compete in tier-2 markets where static boards remain economical.

Admicro bridges online and offline inventory through AdX, which handles 45 billion impressions monthly and now pipes programmatic buys into DOOH. Vistar Media and Hivestack orchestrate auctions that let global traders tap Vietnamese panels through the same consoles used for online video, though smaller owners struggle to fund the CMS and API integrations required. The new legal mandate for content-control and log retention imposes USD 5,000–10,000 per network in compliance costs, a barrier that entrenches the lead of well-capitalized incumbents.

White-space potential sits in healthcare-centric networks placed in hospital lobbies and pharmacies, arenas where dwell times run high and content can be precision-targeted. Operators that solve for measurement and privacy will attract pharmaceutical budgets seeking condition-specific audience clusters, further diversifying revenue streams within the Vietnam OOH and DOOH industry.

Vietnam OOH And DOOH Industry Leaders

JCDecaux Vietnam Co. Ltd.

Goldsun Focus Media Co., Ltd.

Koa-Sha Vietnam Advertising Co., Ltd.

Smart Digital Media Co., Ltd.

Vision Outdoor Advertising Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vingroup launched the Cần Giờ coastal urban tourism project, Vinhomes Green Paradise, adding 2,870 ha of potential OOH sites near new rail links

- May 2025: Bình Dương accelerated investment in Metro Line 2, creating 23 km of fresh transit media inventory

- August 2025: The government issued Decision 1838/QD-TTg to operationalize Law 75/2025 and ordered technical standards for outdoor media.

- March 2025: MSD and the Ministry of Health launched an HPV awareness campaign using 3D mapping and AI ambassadors across three major cities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Vietnam out-of-home (OOH) and digital out-of-home (DOOH) market as the gross revenue media owners collect for selling advertising space on roadside billboards, street furniture, transit assets, and networked digital screens that are viewable in public environments. This covers classic printed faces together with digital units running looped or programmatic content across Vietnam's cities and transport hubs.

Scope exclusion: indoor-only digital signage used at retail points of sale is not counted.

Segmentation Overview

- By Type

- Static OOH

- Digital OOH

- Programmatic OOH

- Other Digital OOH

- By Application

- Billboards

- Transportation

- Airports

- Other Transportation

- Street Furniture

- Place-Based Media

- By End-User Industry

- Automotive

- Retail and Consumer Goods

- Healthcare

- BFSI

- Other End-User Industries

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured discussions with media-owner executives, local planners, creative agencies, and brand marketers across Hanoi, Ho Chi Minh City, and Da Nang. Interviews explored average spot rates, load factors, typical campaign mixes, and the pace of static-to-digital conversion, helping us validate secondary ratios and fine-tune forecast drivers.

Desk Research

We began with publicly available statistics from bodies such as the General Statistics Office of Vietnam, the Ministry of Transport, and Ho Chi Minh City's Department of Culture and Sports, which publish data on urban footfall, vehicle counts, and sign-permit volumes. Trade associations, notably the Vietnam Advertising Association and the Outdoor Advertising Association of Asia, provided spend benchmarks and inventory audits. Company filings, investor decks, and press releases offered price lists and occupancy rates, while news archives on Dow Jones Factiva and D&B Hoovers helped us gauge contract wins and new screen roll-outs. Patent trends pulled from Questel, plus regulatory updates in provincial planning portals, further shaped supply assumptions. These sources are illustrative rather than exhaustive; many additional documents informed data checks and clarifications.

Market-Sizing & Forecasting

A top-down reconstruction of net advertising spending was built from official ad-spend tables and municipal panel inventories, then cross-checked through selective bottom-up supplier roll-ups. Key variables included installed billboard square meters, active digital screen counts, average selling prices, monthly load factors, smartphone-based traffic index growth, and regulatory license issuance. Missing values in bottom-up estimations were gap-filled using median industry coefficients before being stress-tested against primary inputs. For forecasting, a multivariate regression linked panel counts, nominal GDP, and urban population expansion to historical OOH revenue. An ARIMA overlay captured seasonality linked to Tet campaigns.

Data Validation & Update Cycle

Outputs pass a two-step analyst peer review, variance flags trigger source rechecks, and unusual shifts are re-confirmed with interviewees. Reports refresh annually, with interim revisions when material events, such as major concession tenders and price cap changes, occur. A final pre-publication sweep ensures clients receive the latest view.

Why Mordor's Vietnam OOH And DOOH Baseline Inspires Confidence

Published estimates often differ because firms choose distinct scopes, input series, and refresh cadences.

Key gap drivers include whether only digital formats or the full OOH spectrum is counted, use of ad-spend versus media-owner revenue, and the rigor with which local permit data are blended with traffic metrics. Mordor's model combines both static and digital formats, applies city-level audience data, and refreshes annually, yielding a grounded yet current baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 96.97 M (2025) | Mordor Intelligence | - |

| USD 107.50 M (2024) | Global Consultancy A | Digital-only scope inflates value; limited local permit data |

| USD 118.50 M (2025) | Industry Journal B | Top-down spend estimate, no supplier roll-ups or load-factor checks |

In short, by aligning real inventory counts with verified price and occupancy inputs, Mordor delivers a balanced, transparent baseline that decision-makers can reliably trace and replicate.

Key Questions Answered in the Report

How large is the Vietnam OOH and DOOH market in 2026?

The Vietnam OOH and DOOH market size was USD 350.23 million in 2026 and is tracking a 5.73% CAGR toward USD 462.77 million by 2031.

Which application is expanding the fastest?

Place-based media inside malls, elevators, and stores is growing at a 6.11% CAGR because it offers closed-loop attribution at the point of purchase.

Why is healthcare spending rising in Vietnamese OOH?

Public-health agencies and pharmaceutical brands favor interactive LEDs and augmented-reality screens that boost engagement and drive a projected 6.95% CAGR in healthcare allocations.

How will new regulations affect media owners?

Law 75/2025 and Decree 342/2025 mandate playback logs and identity verification, raising compliance costs that advantage well-capitalized operators over smaller rivals.

What role does programmatic buying play?

Programmatic platforms such as Vistar Media and Hivestack allow real-time bidding and audience targeting, accelerating budget shifts from static posters to dynamic screens.

Which cities contribute most of the spend?

Hanoi and Ho Chi Minh City account for nearly 70% of total investment thanks to dense populations, metro infrastructure, and a rich mix of premium digital inventory.

Page last updated on: