Vietnam Metal Can Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.17 Billion |

| Market Size (2026) | USD 2.23 Billion |

| Market Size (2031) | USD 2.58 Billion |

| Growth Rate (2026 - 2031) | 2.93% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Metal Can Packaging Market Analysis by Mordor Intelligence

The Vietnam metal can packaging market size was valued at USD 2.17 billion in 2025 and estimated to grow from USD 2.23 billion in 2026 to reach USD 2.58 billion by 2031, at a CAGR of 2.93% during the forecast period (2026-2031). This growth reflects a maturing regulatory environment that prioritizes recyclable substrates and rewards manufacturers capable of meeting mandatory collection targets. Rising urban disposable income supports steady beverage and food consumption, while government foreign-direct-investment incentives worth VND 66.38 billion (USD 2.68 million) channel capital into supporting-industry upgrades. The Vietnam metal can packaging market benefits from a new domestic hot-rolled-coil supply that reduces material lead times and insulates producers from anti-dumping duties on Chinese steel. In parallel, closed-loop pilots prove commercial feasibility for high-recycled-content cans, positioning the Vietnam metal can packaging market at the forefront of sustainability-driven innovation.

Key Report Takeaways

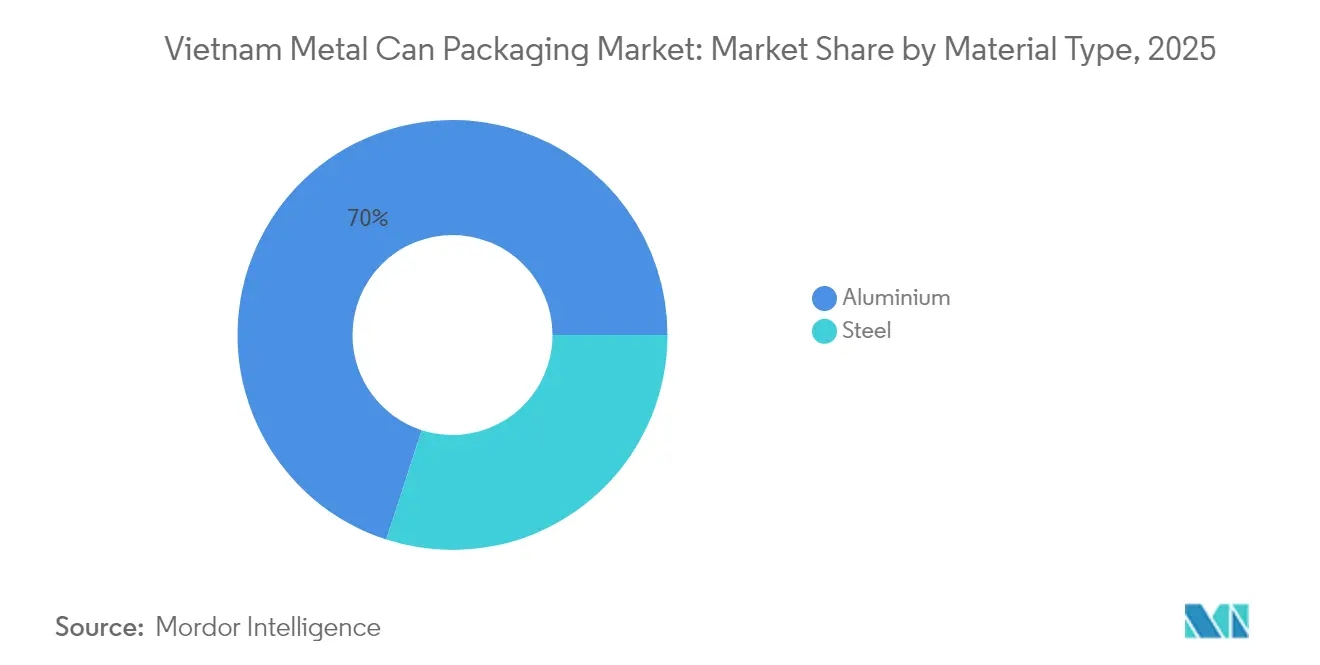

- By material type, aluminum captured 70.02% of the Vietnam metal can packaging market share in 2025 and grew at a 4.21% CAGR through 2031.

- By can structure, two-piece designs held 52.78% share of the Vietnam metal can packaging market size in 2025, Monobloc Aerosol is advancing at a 5.61% CAGR through 2031.

- By capacity, 250-500 ml formats commanded 31.05% revenue share in 2025, while ≤250 ml cans are projected to expand at a 4.73% CAGR between 2026-2031.

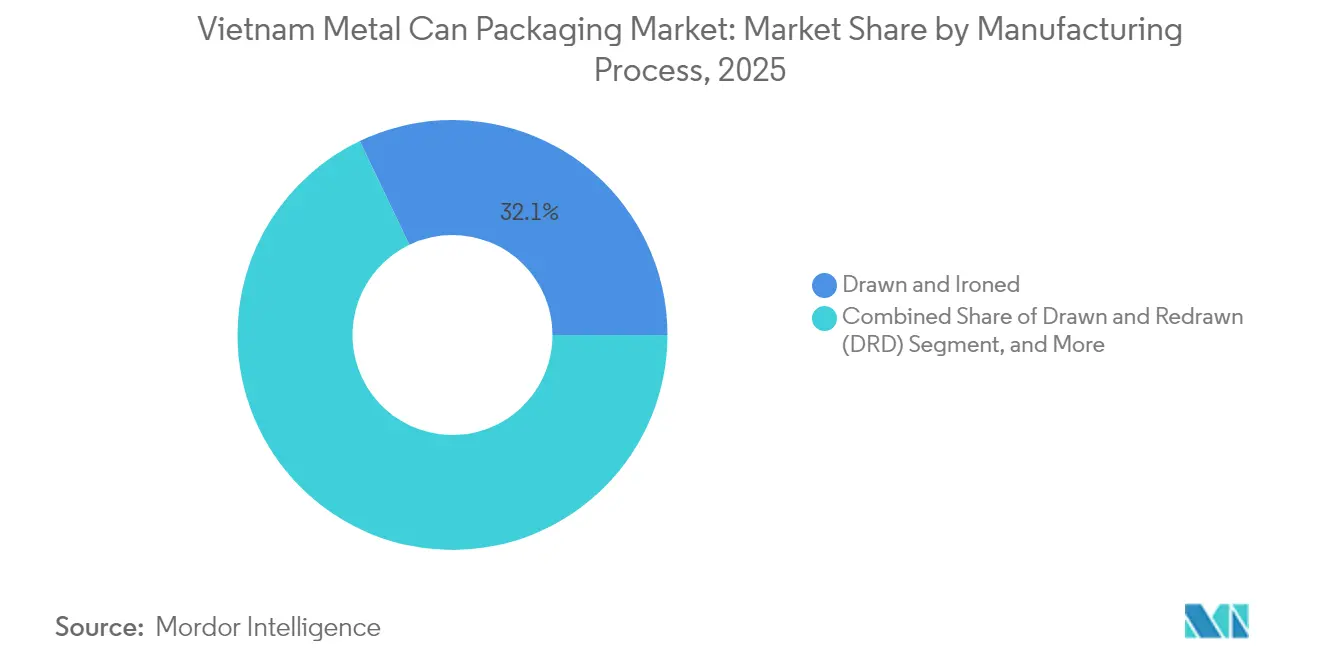

- By manufacturing process, D&I production accounted for 32.10% of the Vietnam metal can packaging market size in 2025; impact extrusion is set to grow at a 4.62% CAGR through 2031.

- By end-user, beverages led with 39.85% share of the Vietnam metal can packaging market size in 2025, whereas pharmaceuticals are advancing at a 4.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Metal Can Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for convenience food and beverages | +0.8% | Ho Chi Minh City, Hanoi, Da Nang | Medium term (2-4 years) |

| High recycling rates and sustainability commitments | +0.6% | National, pilot programs in major cities | Long term (≥ 4 years) |

| Expansion of modern retail and e-commerce networks | +0.5% | Urban centers, moving to secondary cities | Medium term (2-4 years) |

| Domestic HRC capacity expansion improving input supply | +0.4% | National, Dung Quat complex focal point | Short term (≤ 2 years) |

| Closed-loop beverage-can recycling pilots | +0.3% | Ho Chi Minh City and Hanoi | Long term (≥ 4 years) |

| Government FDI incentives for supporting industries | +0.2% | National industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Convenience Food and Beverages

Rapid urbanization is transforming grocery baskets and boosting single-serve formats. The food-processing sector expanded 7.4% in 2024 to USD 79.3 billion, and soft-drink consumption hit 4.658 billion liters, a 4.8% year-over-year increase.[1]General Statistics Office of Vietnam, “Vietnam Food Processing Industry 2024,” gso.gov.vn Domestic leaders such as Vinamilk posted Q2 2024 revenue of VND 11,850 billion (USD 478 million), reaffirming demand for shelf-stable, portion-controlled packages. The 250-500 ml range already dominates, yet ≤250 ml cans record the fastest CAGR due to e-commerce and on-the-go lifestyles. Premium ready-to-drink energy beverages and alcoholic seltzers further widen the application base, sustaining volume growth for the Vietnam metal can packaging market.

High Recycling Rates and Sustainability Commitments

Vietnam’s Extended Producer Responsibility law enforces a minimum 22% aluminum recycling rate from January 2024.[2]Ministry of Natural Resources and Environment, “Extended Producer Responsibility Regulations Implementation,” monre.gov.vn HEINEKEN Vietnam processed 850 tonnes of used cans in its 2024 pilot, while Crown Holdings targets a 92% beverage-can collection rate by 2030. These initiatives cut raw-material costs, unlock secondary-aluminum feedstock and burnish brand credentials, giving the Vietnam metal can packaging market a clear sustainability advantage over flexible plastic competitors.

Expansion of Modern Retail and E-Commerce Networks

Logistics turnover reached USD 40-42 billion in 2024, expanding 14-16% annually despite last-mile costs at 16.5% of GDP. New highways and Long Thanh Airport improve distribution speed, enabling omnichannel strategies that favor smaller cans with vivid graphics. Retailers demand standardized footprints, pushing two-piece cans to the forefront for both shelf appeal and automated palletization. Rising e-grocery penetration further anchors growth for the Vietnam metal can packaging market.

Domestic HRC Capacity Expansion Improving Input Supply

Hòa Phát’s Dung Quat 2 complex came fully online in Q4 2025, supplying 40,000 tonnes of crude steel daily and eliminating exposure to Chinese HRC antidumping duties of 19.38-27.83%. Lead-times for can-sheet fall to 15-20 days, freeing working capital and enabling agile production schedules. As local HR coil availability improves, the Vietnam metal can packaging market gains a durable cost cushion versus import-dependent peers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising competition from flexible plastic and paper formats | -0.7% | Nationwide, food packaging segment | Medium term (2-4 years) |

| Metal price volatility and emerging trade tariffs/CBAM | -0.5% | Global but affects local plants | Short term (≤ 2 years) |

| Limited domestic rolling capacity for can-sheet quality | -0.4% | Industrial clusters | Medium term (2-4 years) |

| Urban logistics bottlenecks raising last-mile costs | -0.3% | Ho Chi Minh City, Hanoi, Da Nang | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Competition from Flexible Plastic and Paper Formats

Paper-based Tetra Recart claims 85% lower emissions than cans and began domestic runs at Doveco Sơn La in late 2024.[3]Tetra Pak Vietnam, “Tetra Recart Vietnam Launch,” tetrapak.com SCG’s USD 27.3 million purchase of Starprint Vietnam accelerates lightweight paper solutions. Nearly 4,000 plastic firms allocate 39% of capacity to packaging, exerting pricing pressure. Weight savings matter for e-commerce, yet cans still excel in carbonation retention, tamper evidence and premium cues, sustaining core demand for the Vietnam metal can packaging market.

Metal Price Volatility and Emerging Trade Tariffs/CBAM

Aluminum spot prices swung sharply on the London Metal Exchange during 2024, forcing producers to hedge. The EU Carbon Border Adjustment Mechanism adds compliance costs to exporters, while U.S. tariff uncertainty keeps risk premiums elevated. Domestic manufacturers face higher power tariffs and compete for scrap as recycled-content mandates tighten. Vertical integration and long-term contracts partly offset volatility, but these external shocks trim margins and temper the CAGR for the Vietnam metal can packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum Dominance Strengthened by EPR Mandates

Aluminum captured 70.02% of the Vietnam metal can packaging market share in 2025, a lead cemented by the 22% recycling quota that came into force the same year. The Vietnam metal can packaging market size for aluminum-based formats is projected to expand at a 4.21% CAGR through 2031 as pharmaceutical and personal-care brands prioritize high-purity barriers. Domestic plans to expand bauxite-to-aluminum refining at Lâm Đồng promise future supply security while cutting freight emissions.

Steel retains a foothold in large-volume food cans where rigidity and cost advantages prevail, especially above 1,000 ml. Hòa Phát’s in-house HRC drives down delivered prices, but the metal’s heavier weight handicaps long-distance logistics. As brand owners pledge carbon neutrality, aluminum’s proven closed-loop recyclability keeps siphoning demand from steel, reinforcing the Vietnam metal can packaging market growth trajectory.

By Can Structure: Two-Piece Technology Delivers Scale and Graphics

Two-piece cans accounted for 52.78% of the Vietnam metal can packaging market in 2025 thanks to high-speed D&I lines and photo-quality printing. Continuous lightweighting shrinks wall gauges without sacrificing strength, lowering per-unit metal use and freight costs. The Vietnam metal can packaging market size for two-piece formats will increase in tandem with beverage output and omnichannel retail growth.

Monobloc aerosol containers exhibit a 5.61% CAGR to 2031, propelled by personal-care and pharma spray products that demand seamless walls for pressure resistance. CANPACK’s Quadromix short-run technology enables seasonal promotions, improving shelf visibility. While three-piece bodies serve bulky food packs, investments tilt toward flexible two-piece lines that maximize uptime and graphics flexibility.

By Capacity/Size: Convenience Packs Outpace Family-Sized Formats

Portion control drives the 250-500 ml category to 31.05% share in 2025 as urban consumers favor on-the-go beverages. The Vietnam metal can packaging market sees ≤250 ml models rising 4.73% annually because they tuck neatly into e-commerce mailers and appeal to calorie-conscious buyers.

Family-sized 500-1,000 ml cans still populate foodservice and at-home sharing occasions, yet slower velocity limits growth. Over 1,000 ml containers address industrial lubricants and bulk foods, niches insulated from immediate substitution. As smartphone retail apps proliferate, compact cans with tamper-evident ends will gain further ground, sustaining segment mix evolution within the Vietnam metal can packaging market.

By Manufacturing Process: Impact Extrusion Gains Regulatory Tailwinds

D&I remains the production workhorse with 32.10% share, favored for long beverage runs that surpass one billion units annually. Unit costs fall as line speeds exceed 2,000 cans per minute, reinforcing dominance in carbonated drinks. The Vietnam metal can packaging market depends on these efficiencies to keep pace with price-sensitive consumers.

Impact extrusion registers a 4.62% CAGR owing to pharma-grade aerosol demand. Seamless bodies satisfy drug-stability protocols under Vietnam’s Circular 12/2025/TT-BYT. Drawn-and-redrawn processes carve out space in odd-shaped food packs, but capital budgets prioritize extrusion upgrades that meet stringent good-manufacturing-practice audits.

By End-User Industry: Pharmaceuticals Lead Growth While Beverages Anchor Volume

Beverages delivered 39.85% of the Vietnam metal can packaging market size in 2025, bolstered by energy drinks and alcoholic seltzers. Soft drinks alone topped 4.658 billion liters that year, showing a resilient thirst for canned refreshment. Brands leverage two-piece aluminum to communicate premium cues and recyclability, a message that resonates with eco-aware Gen Z shoppers.

Pharmaceuticals expand 4.96% annually, the fastest among tracked sectors. Serialization and child-resistant closures become mandatory, fueling demand for compliant metal formats with barrier integrity. Food remains a steady baseline, while personal care absorbs monobloc aerosol systems for deodorants and hair sprays. Collectively, these applications diversify revenue streams and safeguard the Vietnam metal can packaging market against single-segment shocks.

Geography Analysis

Vietnam’s industrial corridors in Ho Chi Minh City and Hanoi collectively generate the bulk of can demand, reflecting dense populations and proximity to beverage, food and pharmaceutical factories. The Vietnam metal can packaging market size in the southern cluster benefits from direct access to the new Vung Tau deep-sea port and in-house steel supply, shaving logistics costs and transit times. Improved road infrastructure adds redundancy, making trucking into the Mekong Delta smoother during flood season.

Northern production zones leverage lower electricity tariffs and government incentives inside Bac Ninh and Hai Phong industrial parks. Cross-border trade with China supplies machinery but also exposes plants to tariff swings, so local executives hedge with multi-sourcing strategies. Rapid suburbanization around Hanoi increases grocery shelf space, translating into incremental volume for regional canners.

Secondary cities such as Da Nang and Can Tho emerge as satellite hubs, drawing FDI with cheaper land leases and vocational training grants. Crown Holdings’ Da Nang plant, recognized for water-saving technology, signals confidence in central Vietnam’s growth prospects. As 3,000 km of new highways open by 2025, distributors can shuttle finished cans nationwide within 48 hours, a critical service-level improvement that benefits the Vietnam metal can packaging market.

Competitive Landscape

The Vietnam metal can packaging market hosts a blend of global majors and agile domestic firms, yielding moderate fragmentation. Crown Holdings consolidated Ho Chi Minh City operations into its Vung Tau complex in 2024 to optimize two-piece line efficiency and lower urban rent. Ball Corporation maintains an equity investment without majority control, pursuing a capital-light posture until demand warrants greenfield expansion.

Domestic champion Hòa Phát wields upstream integration that translates into cost savings exceeding USD 60 per tonne versus import-dependent rivals. It supplies coils directly to can-making subsidiaries, insulating them from freight volatility and currency swings. Local newcomer Tan Tien Can applies impact-extrusion expertise to pharma aerosols, capturing contracts tied to Circular 12/2025 compliance.

Sustainability agendas now dictate procurement. HEINEKEN Vietnam’s successful 850-tonne closed-loop pilot persuaded retailers to prioritize cans containing verified recycled content. CANPACK’s Quadromix short-run facility supplies festival-themed editions, proving that agility can coexist with scale. Patent filings from Continental Can on double-seam monitoring systems underscore ongoing process innovation vital for quality consistency in the Vietnam metal can packaging market.

Vietnam Metal Can Packaging Industry Leaders

TBC-Ball Beverage Can Vietnam Ltd (Ball Corporation)

Hanacans Joint Stock Company

Crown Beverage Cans Vietnam Ltd

Kian Joo Can (Vietnam) Co. Ltd

Resonac Holdings Corporation.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vietnam Ministry of Health issued Circular 12/2025/TT-BYT prescribing marketing-authorization rules that require serialization and enhanced stability testing for pharmaceutical packaging.

- March 2025: Hòa Phát Group achieved full operational status at Dung Quat 2, producing 40,000 tonnes of crude steel daily and satisfying the entire local HRC demand.

- January 2025: The government allocated VND 66.38 billion (USD 2.68 million) to upgrade supporting industries, including can-making equipment modernization.

- December 2024: HEINEKEN Vietnam completed an 850-tonne can-to-can recycling pilot, validating a closed-loop model.

Vietnam Metal Can Packaging Market Report Scope

Metal cans have emerged as a favored packaging choice for Vietnam's mobile-centric consumers. Their portability makes them ideal for outdoor events, festivals, and beaches, unlike glass, which is often prohibited due to its fragility. The Vietnamese metal can packaging market’s growth is further fueled by the cost-effectiveness and recyclability of cans, the surging demand for energy drinks, and the introduction of new products.

The Vietnamese metal can packaging market is segmented by type (aluminum and steel) and end user (food, beverage, cosmetic and personal care, pharmaceuticals, paints, and automotive). The market sizes and forecasts are provided in terms of value USD for all the above segments.

| Aluminium |

| Steel |

| Two-Piece |

| Three-Piece |

| Monobloc Aerosol |

| ≤250 ml |

| 250–500 ml |

| 500–1,000 ml |

| >1,000 ml |

| Drawn and Ironed (D&I) |

| Drawn and Redrawn (DRD) |

| Impact Extrusion |

| Food |

| Beverage |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Paints and Industrial Chemicals |

| Automotive Fluids and Lubricants |

| Other End-User Industry |

| By Material Type | Aluminium |

| Steel | |

| By Can Structure | Two-Piece |

| Three-Piece | |

| Monobloc Aerosol | |

| By Capacity / Size | ≤250 ml |

| 250–500 ml | |

| 500–1,000 ml | |

| >1,000 ml | |

| By Manufacturing Process | Drawn and Ironed (D&I) |

| Drawn and Redrawn (DRD) | |

| Impact Extrusion | |

| By End-User Industry | Food |

| Beverage | |

| Personal Care and Cosmetics | |

| Pharmaceuticals | |

| Paints and Industrial Chemicals | |

| Automotive Fluids and Lubricants | |

| Other End-User Industry |

Key Questions Answered in the Report

What is the current value of the Vietnam metal can packaging market?

The Vietnam metal can packaging market size stood at USD 2.23 billion in 2026 and is on track to hit USD 2.58 billion by 2031.

Which material leads metal can demand in Vietnam?

Aluminum holds 70.02% share because the EPR law favors its 22% mandated recycling rate and robust closed-loop performance.

Which end-user sector is growing fastest for cans?

Pharmaceuticals post a 4.96% CAGR through 2031 as new regulations enforce serialization and higher packaging integrity.

How do domestic steel developments influence can production costs?

Hòa Phát’s fully integrated HRC facility cuts lead times to 15-20 days and avoids Chinese anti-dumping duties, giving local canners a cost edge.

What role does e-commerce play in driving can sizes?

Online retail fuels demand for ≤250 ml cans that fit shipping constraints and appeal to portion-control preferences among urban consumers.

How is Vietnam addressing sustainability in metal packaging?

A 22% aluminum recycling mandate backed by corporate pilots such as HEINEKEN’s 850-tonne closed-loop test is accelerating collection and recycled-content adoption.

Page last updated on: