Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 13.56 Billion |

| Market Size (2026) | USD 14.17 Billion |

| Market Size (2031) | USD 17.67 Billion |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Metal Cans Market Analysis by Mordor Intelligence

The North America metal cans market size is projected to expand from USD 13.56 billion in 2025 and USD 14.17 billion in 2026 to USD 17.67 billion by 2031, registering a CAGR of 4.52% between 2026 to 2031. Rising extended-producer-responsibility fees on virgin plastics, tariff-driven import costs for tinplate, and brand owners’ premiumization strategies continue to redirect packaging demand toward infinitely recyclable aluminum cans. Converter margins improved after lightweighting trimmed 355-milliliter beverage-can weights to 12.2 grams, while nearshored capacity in Mexico shortened order-to-delivery cycles by 40%. High-purity can-sheet expansions in Alabama and the southeastern United States reduce freight outlays by USD 40-50 per tonne and cushion the market against London Metal Exchange price swings. Personal-care brands embracing monobloc aerosols and ready-to-drink alcohol producers shifting to sleek 355-milliliter profiles create incremental high-margin volume that offsets soft beverages and shelf-stable food declines.

Key Report Takeaways

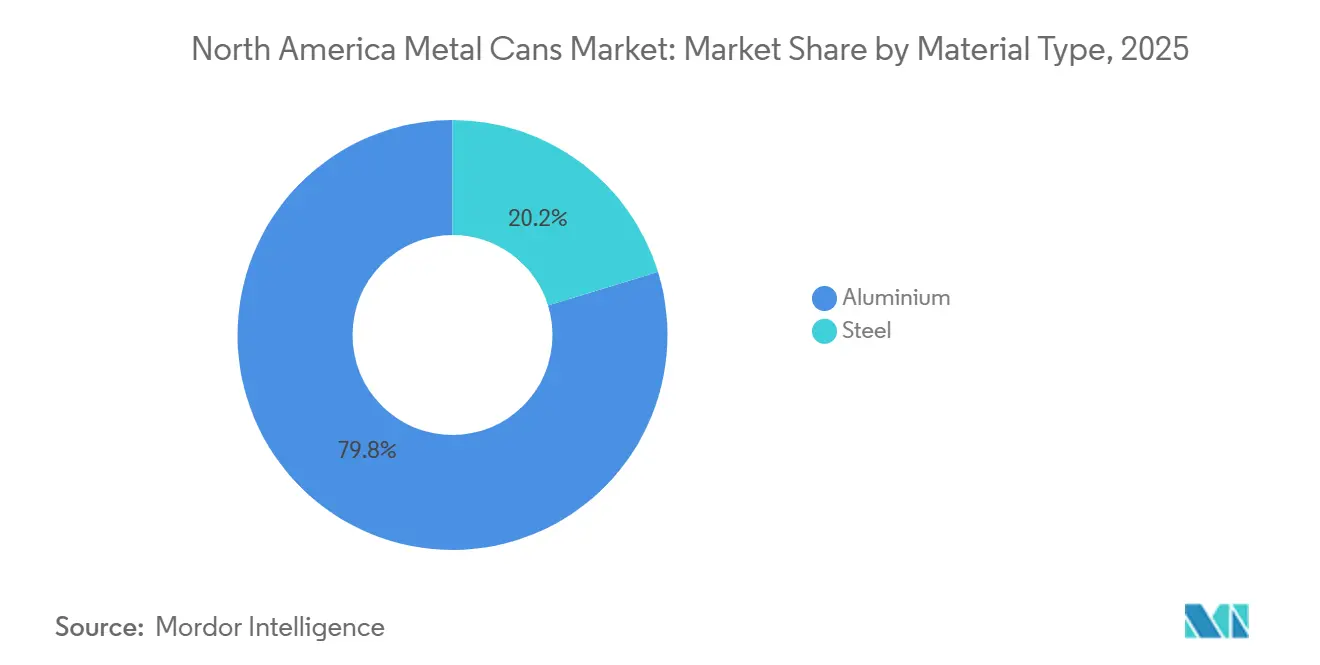

- By material type, aluminum led with 79.76% of the North America metal cans market share in 2025.

- By can structure, two-piece designs commanded 61.32% share, while monobloc aerosols posted the fastest CAGR at 5.07% through 2031.

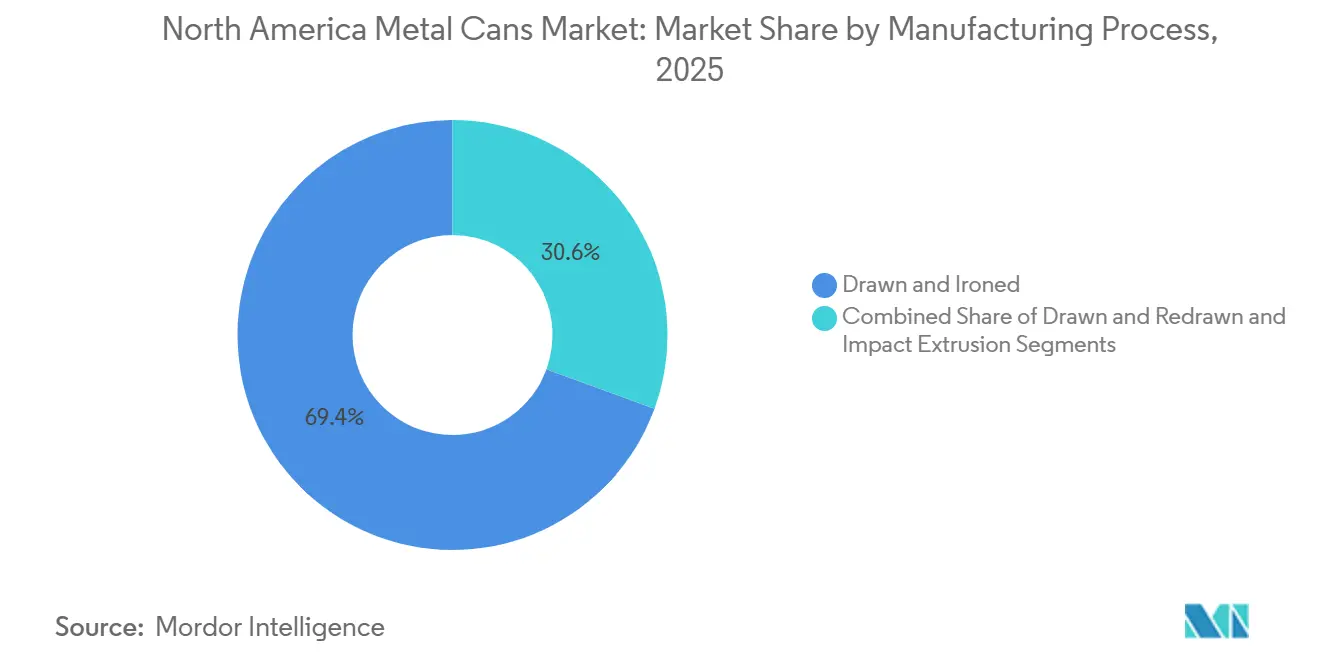

- By manufacturing process, drawn-and-ironed lines held 69.43% share in 2025; impact extrusion recorded the highest projected CAGR at 5.04% to 2031.

- By capacity, the 250-500 milliliter range captured 43.19% share in 2025 and is forecast to expand at 5.29% CAGR.

- By end-user, beverage applications held 52.12% share in 2025, whereas personal care and cosmetics are advancing at a 5.83% CAGR through 2031.

- By country, the United States held 63.23% of regional revenue in 2025; Mexico is the fastest-growing market at 5.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Metal Cans Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Beverage Industry In The Region | +1.2% | United States, Mexico, Canada | Medium Term (2–4 Years) |

| Shift Toward Infinitely Recyclable Aluminum Packaging | +1.0% | United States, Canada, Spillover To Mexico | Long Term (≥4 Years) |

| Premiumization Of Canned Wines And Cocktails (RTDs) | +0.8% | United States Urban Markets | Short Term (≤2 Years) |

| Expansion Of High-Purity Can-Sheet Mills In The United States | +0.7% | United States, Benefits To Mexico | Medium Term (2–4 Years) |

| On-Premise Restrictions Accelerating Take-Home Multi-Packs | +0.6% | United States, Canada | Short Term (≤2 Years) |

| Blockchain-Enabled Traceability Demands From Brand Owners | +0.3% | United States, Pilot Sites In Mexico | Long Term (≥4 Years) |

| Source: Mordor Intelligence | |||

Growing Beverage Industry in the Region

North American fillers consumed nearly 120 billion aluminum cans in 2025 as energy drinks, hard seltzers, and craft beer offset a 1.2% slide in carbonated soft drinks.[1]Aluminum Association, “Aluminum Can Recycling and Sustainability Report 2025,” aluminum.org Mexico’s beer output rose 4.3% in 2024 after a USD 1.2 billion expansion lifted annual capacity by 25 million hectoliters and shifted 36% of domestic packaging into cans. Ready-to-drink cocktails in the United States posted 18% retail-sales growth in 2024, with aluminum capturing 82% of volume at premium price points. Canada diverged, with beverage manufacturing sales contracting 1.7% in 2024 amid refillable-glass incentives. Cross-border supply realignment saw Mexican can exports to the United States climb 12%, while domestic U.S. capacity utilization hovered near 88%.

Shift Toward Infinitely Recyclable Aluminum Packaging

Seventy-five percent of all aluminum ever produced remains in use, underpinning a closed-loop advantage as California’s Senate Bill 54 mandates 65% recycled content by 2032. Oregon’s expanded deposit-return system is projected to lift redemption rates to 82% by 2026, compressing the virgin-to-recycled price spread by 38%. PepsiCo and Molson Coors pledged 100% recycled-content cans for select lines by 2027, redirecting 180,000 tonnes of annual scrap demand. These mandates elevate aluminum against polyethylene terephthalate’s 9% recycling rate and against flexible pouches that lack commercial reclamation streams.

Premiumization of Canned Wines and Cocktails (RTDs)

United States retail sales of canned wines and cocktails reached USD 8.4 billion in 2024, with aluminum formats accounting for 82% of units. Constellation Brands’ Fresca Mixed line achieved USD 120 million in first-year sales through 355-milliliter sleek cans that retail 30% above glass equivalents.[2]Constellation Brands, “Fiscal 2024 Investor Relations Report,” cbrands.com Canned wine penetration advanced to 12% of total wine volume as 250 milliliter offerings gained favor at outdoor venues where glass is restricted. Margin mathematics favor the format: aluminum units cost USD 0.18-0.22 versus USD 0.35-0.45 for comparable glass bottles, yet retail prices remain higher, widening producer gross margins by 4-6 percentage points.

Expansion of High-Purity Can-Sheet Mills in the United States

Novelis’s USD 2.5 billion Bay Minette mill, commissioned in January 2025, adds 600,000 tonnes of can-sheet capacity, 90% of which is sourced from post-consumer scrap within a 500-mile radius. A USD 290 million Ball-Manna joint venture contributes another 300,000 tonnes by late 2026, trimming order-to-delivery cycles to three weeks. Steel Dynamics targets late-2026 start-up of a 200,000-tonne tinplate line, easing 50% tariff pressure on imported tinplate. These investments rebalance North American supply chains and lessen exposure to London Metal Exchange volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of PET And Flexible Pouches In Food And Drink | -0.9% | United States, Canada | Medium Term (2–4 Years) |

| Volatile Aluminum And Steel Coil Prices | -0.7% | United States, Mexico, Canada | Short Term (≤2 Years) |

| Rising Refill-And-Reuse Legislation Challenging Single-Use Cans | -0.5% | United States, Canada | Long Term (≥4 Years) |

| Supply Bottlenecks In Body-Maker Equipment | -0.4% | United States, Mexico | Short Term (≤2 Years) |

| Source: Mordor Intelligence | |||

Proliferation of PET and Flexible Pouches in Food and Drink

Polyethylene terephthalate bottles and flexible pouches held 22% of North American juice and dairy packaging in 2024, eroding metal-can share in shelf-stable meals where transparency and resealability resonate. Ocean Spray and Tropicana each shifted up to 20% of their aseptic volume from steel cans to PET, citing unit costs up to 30% lower. Flexible pouches captured 18% of ready-to-eat meal volume in 2024 after brands leveraged 40-50% lighter weights and 60% smaller cube sizes compared to rigid cans.[3]Flexible Packaging Association, “Flexible Pouch Market Penetration 2024,” flexpack.org Mexican juice segments show even higher displacement, as cartons and PET hold a combined 68% share. Converters answer with lightweighting and digital printing, yet these actions address cost rather than core format preference.

Volatile Aluminum and Steel Coil Prices

Aluminum spot prices ranged from USD 2,150 to USD 2,650 per tonne during 2024-2025, lifting United States Midwest premiums to USD 580 per tonne.[4]London Metal Exchange, “Aluminum Spot Price Data 2024-2025,” lme.comBall Corporation reported USD 180 million in unrecovered metal inflation in 2024, equal to 2.1% of segment revenue. Steel coil for tinplate rose from USD 950 to USD 1,180 per tonne in 2024 after Section 232 tariffs doubled, raising landed costs by USD 150-200 per tonne. Crown Holdings hedged 75% of 2026 aluminum demand versus 55% in 2023, while Silgan negotiated 30-day price-adjustment clauses to cap exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum’s Recycled-Content Advantage Widens the Moat

Aluminum captured 79.76% of North America's metal can market share in 2025, outpacing steel as extended producer responsibility rules reward closed-loop recyclability. The North America metal cans market for aluminum applications is forecast to expand at a 4.93% CAGR, whereas the steel market grows at only 3.12%. Tariff hikes that doubled Section 232 duties in 2025 inflated imported tinplate costs by USD 150-200 per tonne, squeezing steel-can margins and reinforcing aluminum’s cost edge.

Novelis’s and Ball’s combined 900,000-tonne can-sheet additions fortify domestic supply and further lower freight outlays. Steel remains indispensable for retort-sterilized foods, paints, and industrial chemicals, but its 20.24% share in 2025 is expected to slip as flexible pouches chip away at three-piece formats. Material preferences also diverge geographically: Mexico’s 28% steel-can share reflects local tinplate availability, while the United States' share contracted to 18%.

By Can Structure: Monobloc Aerosol Disrupts Two-Piece Dominance

Two-piece drawn-and-ironed cans delivered a 61.32% share in 2025, serving high-volume beverages that demand seamless walls and low unit weights. Monobloc aerosols, however, exhibit the fastest 5.07% CAGR, offering tamper evidence, premium aesthetics, and 15% lighter weight than three-piece counterparts. Three-piece steel cans persist in paint and chunky soups, yet flexible pouches erode their growth to 3.21%.

Impact-extrusion presses enable monobloc geometry without side seams, but USD 8-12 million tooling bills curb smaller entrants. Retrofitting older three-piece lines with drawn-and-ironed tooling is an interim step for converters chasing beverage economics. As personal-care brands heighten demand for design flexibility, monobloc share is set to climb above 12% by 2031.

By Manufacturing Process: Impact Extrusion Scales Beyond Aerosol Niches

Drawn-and-ironed processes commanded 69.43% share in 2025, achieving 2,000-plus cans per minute and 92% material yields that underpin beverage economics. Drawn-and-redrawn kept 25.53% share, satisfying food and aerosol specifications that need thicker sidewalls. Impact extrusion held 5.04% share but is forecast to rise fastest after Ball’s recycled-slug patent trimmed scrap tolerance and cut monobloc weights by 15%.

Capital intensity differentiates the processes: drawn-and-ironed lines cost USD 45-55 million, whereas impact-extrusion presses require one-third of that figure, though with slightly lower material recovery ratios. Design versatility and premium positioning in personal care justify the trade-off, spurring converters to install hybrid lines that toggle between slug and cup feedstock.

By Capacity/Size: 250-500 Milliliter Formats Anchor Multi-Pack Economics

The 250-500 milliliter band accounted for 43.19% of North America's metal can market share in 2025 and is projected to expand at a 5.29% CAGR, buoyed by 12- and 24-pack take-home formats and energy drink demand. Formats under 50 milliliters remain niche for cosmetic samples and pharmaceuticals, representing an 8.12% share. Larger 500-1,000 milliliter sizes cater to craft beer and hard teas, while cans above 1,000 milliliters primarily target industrial paints.

Retail channel dynamics shape capacity preferences: convenience stores prioritize 355- and 473-milliliter cans that maximize cooler facings, whereas club stores drive bulk multipacks. Mexico’s format mix remains 68% 355-milliliter beer cans, while 473-milliliter offerings grew 14% year-over-year as brewers chase premium price points.

By End-User Industry: Personal Care Outpaces Beverage Maturity

Beverage applications maintained a 52.12% share in 2025, but personal care and cosmetics is the fastest-growing end-user at 5.83% CAGR through 2031. The North America metal cans market size for personal care aerosols is set to expand as deodorant, hairspray, and shaving-foam brands trade plastic for aluminum. Food can volume grows only 2.87% annually amid pouch substitution, while pharmaceuticals, paints, and industrial fluids deliver stable but modest increments.

Deodorant aerosols advanced by 9% in 2024, driven largely by the popularity of continuous-spray formats that secured premium shelf space and appealed to consumers seeking convenience and even application. This growth underscores how packaging innovation can elevate everyday categories into higher-value segments. In beverages, however, trends diverged sharply. Traditional carbonated soft drinks continued to contract as health-conscious consumers shifted away from sugary sodas, while energy drinks and hard seltzers surged ahead, fueled by demand for functional benefits and lifestyle-oriented refreshment. The contrasting trajectories balanced each other out, resulting in a steady net growth rate of 4.21% per year for beverage cans.

Geography Analysis

The United States accounted for 63.23% of North America metal cans market share in 2025. Domestic policy accelerates aluminum’s edge: California’s 65% recycled-content mandate and Oregon’s enlarged deposit system lifted can redemption to a projected 82% by 2026. High-purity can-sheet investments totaling 900,000 tonnes by 2026 shield converters from import tariffs and trim lead times to three weeks.

Mexico follows with the highest CAGR of 5.03% through 2031. Breweries invested USD 1.2 billion in capacity that channels incremental beer volume into cans, while six Crown Holdings plants plus a 2-billion-unit Envases Universales facility support rising domestic demand and growing south-to-north exports under duty-free USMCA terms.

Canada holds a 22.54% share and trails with a 3.76% CAGR. Beverage manufacturing sales slipped 1.7% in 2024 as refillable-glass incentives curtailed aluminum demand, yet growth in energy drinks and sparkling water helped cushion the decline. With can-sheet supplies anchored by Novelis’s Kingston mill running at 94% utilization, Canadian converters focus on food segments to sustain line rates.

Competitive Landscape

Ball Corporation, Crown Holdings, and Silgan Holdings together control roughly 60% of installed capacity, indicating moderate concentration. Ball redirected USD 1.3 billion from its aerospace divestiture into can-line automation that lowered 355-milliliter weights to 12.2 grams and raised throughput by up to 12%. Crown’s USD 3.9 billion Signode acquisition integrates transit packaging, opening cross-sell avenues with beverage and food clients. Silgan expanded Midwestern metal-container capacity by 8% to recapture brands reconsidering a return from pouches to retortable cans.

Niche aerosol and craft-beverage segments remain fragmented. Independent Can Company secured a five-year, 150-million-unit craft-beer pact by offering two-week lead times. CAN-PACK and Tecnocap each lifted impact-extrusion capacity above 15% in 2024-2025 to court personal-care brands needing bespoke monobloc shapes. Upstream, Novelis’s Bay Minette mill provides 600,000 tonnes of scrap-heavy sheet that insulates converters from Midwest premiums and Section 232 escalations, while Steel Dynamics’ 200,000-tonne tinplate line will temper imported-steel dependence when it starts in late-2026.

Technology differentiators include Ball’s recycled-slug patent, which cuts monobloc scrap tolerance to 0.3%, and Crown’s digital printing that allows 4-color graphics at full line speed, matching PET’s aesthetic flexibility without pre-printed stock. Smaller three-piece specialists remain vulnerable to pouch encroachment yet play a role in low-volume industrial and specialty food runs.

North America Metal Cans Industry Leaders

Ball Corporation

Crown Holdings, Inc.

Silgan Holdings Inc.

Ardagh Group S.A.

CANPACK S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Silgan Holdings commenced pilot production of lightweight retortable food cans containing 55% recycled aluminum at its Kansas facility, targeting soup and pet-food brands seeking extended-producer-responsibility compliance.

- November 2025: Crown Holdings opened a digital-printing center of excellence in Dayton, Ohio, enabling four-color graphics at headline speeds of 2,400 cans per minute and supporting short-run craft-beverage orders.

- September 2025: Ball Corporation completed a USD 110 million automation upgrade at its Goodyear, Arizona beverage-can plant, raising line speed by 10% and trimming unit weights to 12.0 grams for 355 milliliter cans.

- July 2025: Novelis initiated cold-rolling operations at its Bay Minette, Alabama complex, moving the USD 2.5 billion mill into limited commercial output six months ahead of schedule.

North America Metal Cans Market Report Scope

The North America Metal Cans Market Report is Segmented by Material Type (Aluminum, Steel), Can Structure (Two-Piece, Three-Piece, Monobloc Aerosol), Capacity/Size (Less than 50 ml, 250-500 ml, 500-1,000 ml, More than 1,000 ml), Manufacturing Process (Drawn and Ironed, Drawn and Redrawn, Impact Extrusion), End-User Industry (Food, Beverage, Personal Care and Cosmetics, Pharmaceuticals, Paints and Industrial Chemicals, Automotive Fluids and Lubricants, Other End-User Industries), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Aluminium |

| Steel |

By Can Structure

| Two-Piece |

| Three-Piece |

| Monobloc Aerosol |

By Capacity / Size

| Less than 50 ml |

| 250-500 ml |

| 500-1,000 ml |

| More than 1,000 ml |

By Manufacturing Process

| Drawn and Ironed (D and I) |

| Drawn and Redrawn (DRD) |

| Impact Extrusion |

By End-User Industry

| Food |

| Beverage |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Paints and Industrial Chemicals |

| Automotive Fluids and Lubricants |

| Other End-User Industries |

By Country

| United States |

| Canada |

| Mexico |

| By Material Type | Aluminium |

| Steel | |

| By Can Structure | Two-Piece |

| Three-Piece | |

| Monobloc Aerosol | |

| By Capacity / Size | Less than 50 ml |

| 250-500 ml | |

| 500-1,000 ml | |

| More than 1,000 ml | |

| By Manufacturing Process | Drawn and Ironed (D and I) |

| Drawn and Redrawn (DRD) | |

| Impact Extrusion | |

| By End-User Industry | Food |

| Beverage | |

| Personal Care and Cosmetics | |

| Pharmaceuticals | |

| Paints and Industrial Chemicals | |

| Automotive Fluids and Lubricants | |

| Other End-User Industries | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large will beverage-can demand be in North America by 2031?

Beverage applications are expected to surpass USD 9 billion in value by 2031, anchored by multi-pack beer, energy drinks, and RTD cocktails.

Which material is gaining share fastest within regional can production?

Aluminum is widening its lead, growing at a 4.93% CAGR as policy and recycling economics favor closed-loop packaging.

Why are monobloc aerosol cans attracting investment?

Personal-care brands value their tamper evidence, lighter weights, and premium shelf appeal, driving a 5.07% CAGR for the format.

What is pushing converters to add capacity in Mexico?

Nearshoring trims logistics lead times by 40% and leverages 30% lower labor costs while still accessing U.S. markets duty-free.

How are price swings in aluminum managed by leading players?

Major converters extend hedging coverage, adjust customer contracts to 30-day pass-throughs, and source sheet from new domestic mills.

Which end-user segment shows the strongest long-term upside?

Personal care and cosmetics leads with a 5.83% CAGR to 2031 as brands transition deodorant and hairspray lines from plastic to aluminum.

Page last updated on: