Vietnam Flexible Plastic Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

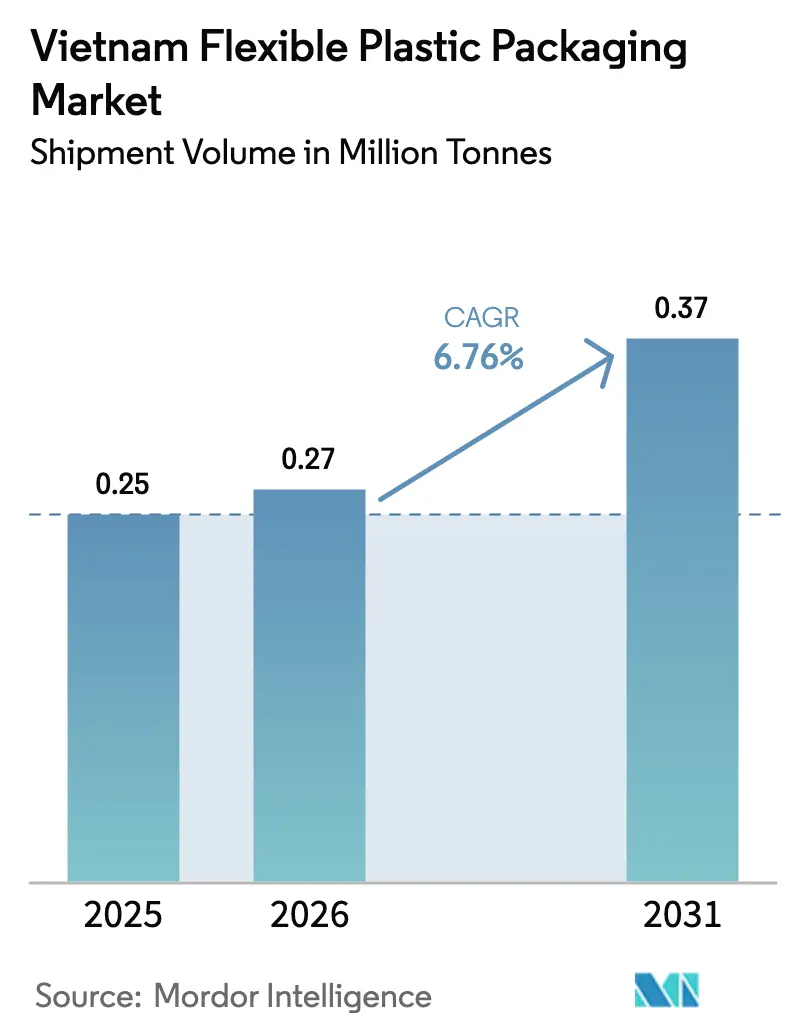

| Base Year Market Size (2025) | 0.25 Million tonnes |

| Market Volume (2026) | 0.27 Million tonnes |

| Market Volume (2031) | 0.37 Million tonnes |

| Growth Rate (2026 - 2031) | 6.76% CAGR |

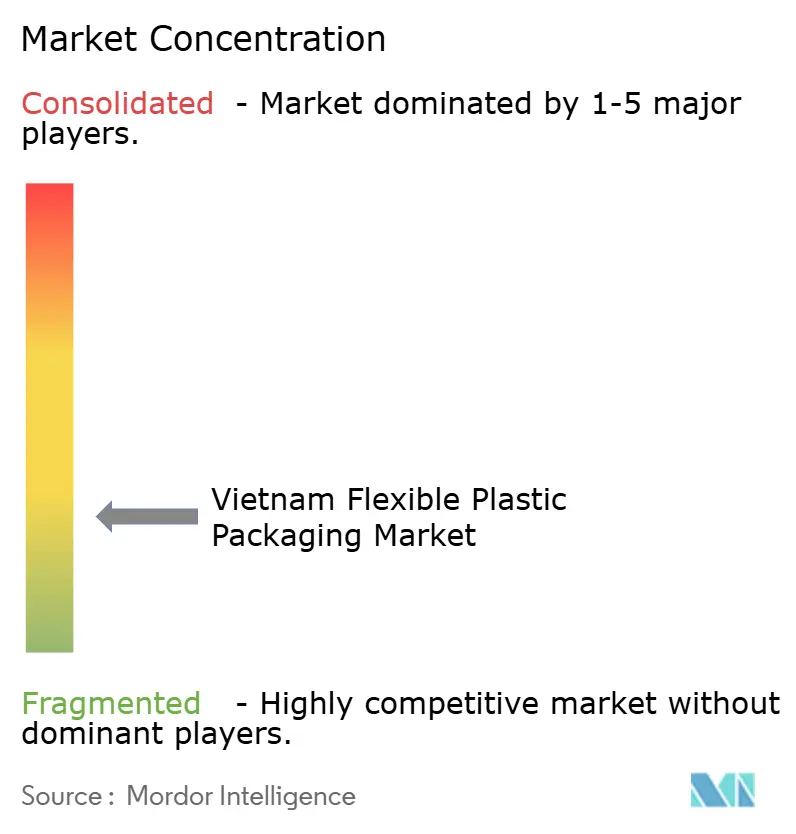

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Flexible Plastic Packaging Market Analysis by Mordor Intelligence

The Vietnam flexible plastic packaging market size is expected to grow from 0.25 million tonnes in 2025 to 0.27 million tonnes in 2026 and is forecast to reach 0.37 million tonnes by 2031 at 6.76% CAGR over 2026-2031. This upward trajectory rests on three intertwined forces: the country’s expanding food-and-beverage processing base, export-oriented tax incentives that lower converters’ effective tax rate to 15%, and the rapid pivot toward sustainable mono-material solutions that comply with emerging Extended Producer Responsibility (EPR) mandates. Strengthening e-commerce and meal-delivery ecosystems further amplifies demand for high-barrier pouches able to withstand thermal stress and preserve product freshness. Meanwhile, volatile polyolefin resin prices, up 15-20% in 2024, nudge converters to hedge input costs through multi-supplier contracts and to experiment with recycled or bio-based resins. The competitive field stays moderately concentrated: multinationals leverage advanced barrier technologies while agile local players win share through cost efficiency and quick design turnarounds.

Key Report Takeaways

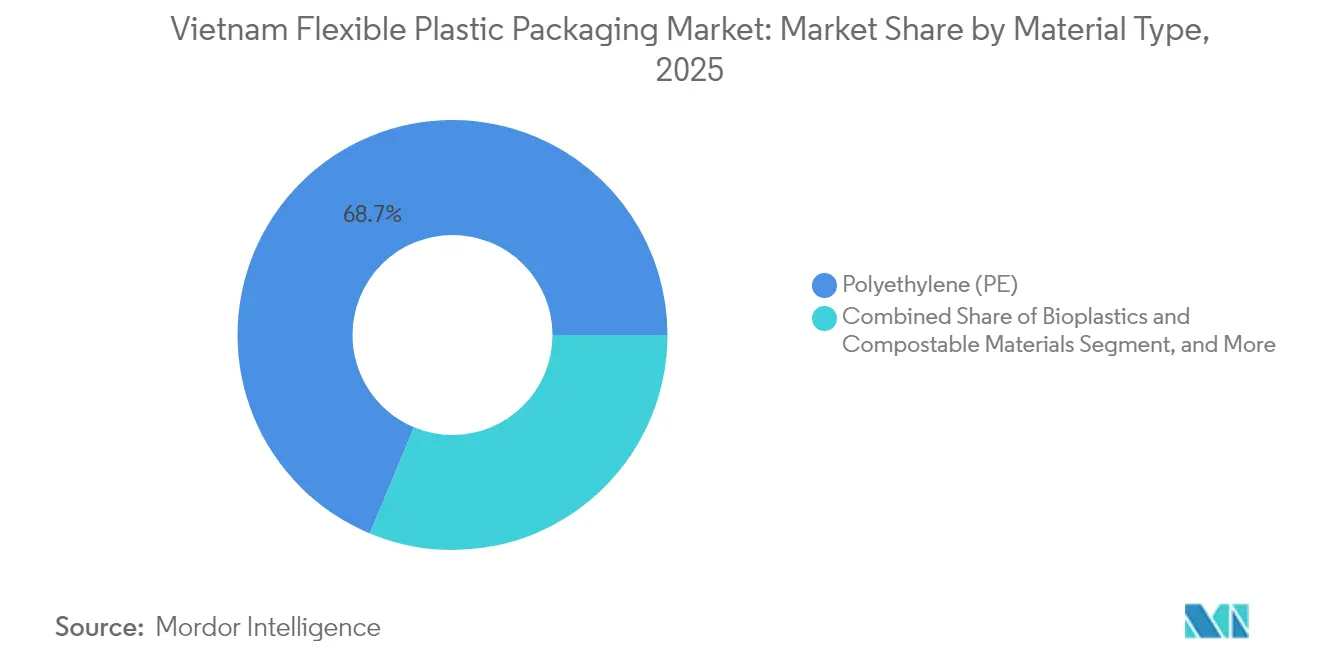

- By material, plastics retained 68.72% of the Vietnam flexible plastic packaging market share in 2025, whereas bioplastics and compostables are advancing at an 7.85% CAGR through 2031.

- By product, bags and pouches led with 47.53% of the Vietnam flexible plastic packaging market size in 2025, while sachets and stick packs are growing at 7.51% CAGR as single-serve formats proliferate.

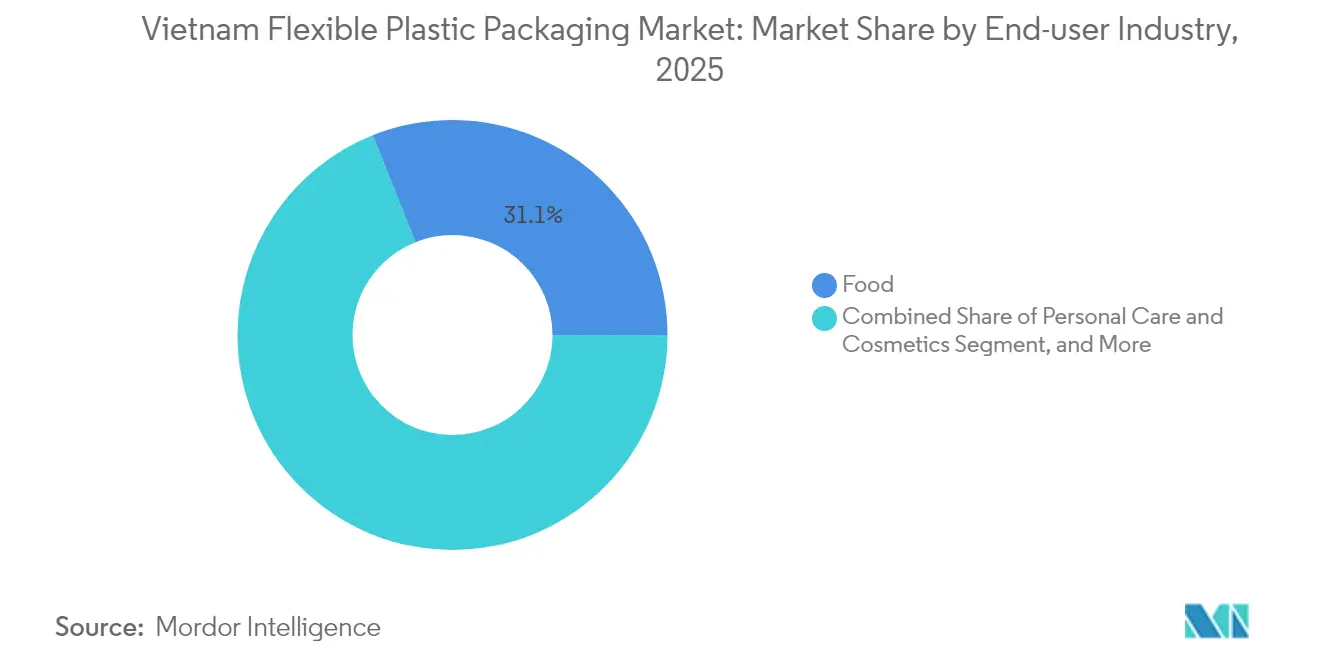

- By end user, food applications commanded 31.05% share in 2025; personal care and cosmetics is the fastest riser at a 5.62% CAGR to 2031.

- By printing technology, flexography accounted for 43.78% share in 2025, and digital printing is scaling at a 6.98% CAGR on the back of customization and short-run needs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

No country-level or regional dataset alone defines global value; it is assembled from all contributing countries and geographies, including Vietnam. Our global flexible plastic packaging market size reflects this full aggregation.

Vietnam Flexible Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of Vietnam’s F&B processing | +1.8% | Ho Chi Minh City, Hanoi | Medium term (2-4 years) |

| Expansion of modern retail & convenience | +1.2% | Tier-1 and fast-growing Tier-2 cities | Short term (≤ 2 years) |

| Export-oriented tax incentives | +0.9% | Industrial parks in Binh Duong, Dong Nai, Long An | Long term (≥ 4 years) |

| E-commerce demand for meal-delivery pouches | +1.4% | Cities with dense delivery networks | Short term (≤ 2 years) |

| Adoption of mono-material PE films | +0.8% | Nationwide, driven by EPR compliance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Vietnam’s F&B Processing Industry

Vietnam’s food-and-beverage sector recorded 7.4% sales growth in 2024, reaching USD 79.3 billion and solidifying its role as the single largest stimulus for the Vietnam flexible plastic packaging market. [1]VietNamNet, “Vietnam food & beverage market grows 7.4% in 2024,” vietnamnet.vn Processed meat and seafood lines have risen sharply, encouraging converters to install multilayer co-extruders that merge polyethylene with EVOH to achieve oxygen transmission rates below 0.1 cc/m²/day at 23 °C. Such barriers allow local brands to meet stringent ASEAN shelf-life requirements while substituting rigid cans or jars with lightweight pouches. Investments in EVOH-enabled films also enable Vietnamese exporters to capture margin-rich regional demand for instant noodles, ready-to-drink coffee, and frozen seafood. As capacity additions come online, processors favor domestic packaging partners to tighten supply chains and reduce lead times.

Expansion of Modern Retail and Convenience Formats

Modern grocery chains such as Aeon and Lotte grew store counts aggressively during 2024-25, compelling brand owners to invest in high-graphic flexible packs that stand out on well-lit shelves. Converters responded by upgrading to eight- and ten-color rotogravure lines while adding digital presses capable of same-day artwork changes. Stand-up pouches with zip closures gain traction for snacks, granola, and powdered beverages, underscoring consumers’ focus on portability and resealability. Sachet volumes rise in parallel because small packs allow price-sensitive shoppers to trial premium hair-care or seasoning brands without committing to large formats. Retailers’ insistence on exact pack dimensions and bar-coding accuracy further standardizes specifications across the Vietnam flexible plastic packaging market, fostering economies of scale for compliant suppliers.

Government Export-Oriented Tax Incentives for Flexible Converters

The Ministry of Planning and Investment reduced the corporate tax rate from 20% to 15% for converters incorporating solvent-free lamination, water-based inks, or renewable-energy systems, improving project internal rates of return and de-risking large-scale automation. Accelerated depreciation on high-efficiency flexographic presses and preferential land leases in designated industrial parks lower upfront costs, encouraging foreign entrants. QuickPack’s USD 31.7 million Long An plant, equipped with German gravure presses and in-line electron-beam curing, typifies the capital inflows catalyzed by these incentives. Over the long term, the policy framework positions Vietnam as an export hub that can funnel competitively priced rolls and pre-made pouches to ASEAN and EU buyers.

E-commerce–Driven Demand for High-Barrier Meal-Delivery Pouches

Food-delivery revenues ballooned in Ho Chi Minh City and Hanoi, steering packaging innovation toward retort-ready, three-layer PE/PA/EVOH pouches that endure 130 °C sterilization while preserving flavors for up to 18 months. Converters collaborate with cloud-kitchen brands to integrate laser scoring for easy opening and to embed QR codes that track temperature excursions during transport. Meal-kit companies pay premiums for these high-barrier constructs because reliable shelf life offsets the absence of refrigerated logistics. The niche accounts for a rising share of the Vietnam flexible plastic packaging market as culinary startups proliferate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EPR and single-use-plastic regulations | -0.7% | National, with stricter enforcement in major cities | Short term (≤ 2 years) |

| Volatile polyolefin resin pricing linked to crude oil swings | -1.1% | National, affecting all material segments | Short term (≤ 2 years) |

| Under-developed domestic recycling for multilayer laminates | -0.4% | National, particularly acute in rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent EPR and Single-Use-Plastic Regulations

Compliance costs escalate as converters must finance collection schemes, redesign multilayer pouches, and document recovery metrics audited by the Ministry of Natural Resources and Environment. [2]Vietnam Government, “Extended Producer Responsibility for Plastic Packaging Regulations,” gov.vnComplex laminates containing aluminum or EVOH face steeper eco-fees, forcing brand owners to absorb cost increases or reformulate packs. Smaller converters lacking capital for rapid machine swaps risk customer attrition. Conversely, early movers that commercialize recyclable solutions enjoy pricing power and preferred-supplier status.

Volatile Polyolefin Resin Pricing Linked to Crude Swings

The 15-20% resin price surge in 2024 shaved margins across the Vietnam flexible plastic packaging industry. Export-oriented plants quoting in USD struggled to pass through hikes in quarterly contracts, prompting greater uptake of long-term supply accords indexed to Brent, as well as spot hedging via polypropylene futures in Singapore. While larger players possess treasury bandwidth to execute such strategies, family-owned converters remain exposed, curbing capex appetite during volatile cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Bioplastics Accelerate the Sustainability Transition

The Vietnam flexible plastic packaging market size for materials was led by conventional plastics, which held 68.72% in 2025, yet regulatory momentum and corporate pledges are fueling an 7.85% CAGR for bioplastics. Polyethylene remains the dominant resin because it processes easily on existing blown-film lines and can now integrate 20-30% post-consumer content without performance loss. BOPP retains niche leadership in snack and confectionery webs that demand high gloss and stiffness, whereas CPP meets retort and heat-resistant applications. EVOH, although constituting a small tonnage, delivers disproportionate value in pet food and seafood exports owing to its ultra-low oxygen permeability.

Bioplastic penetration hinges on PLA and starch blends that meet EN 13432 compostability norms and can seal at lower temperatures, reducing energy costs per pouch. Brands pilot these formats for short-shelf-life dry products where barrier demands are moderate. As EPR surcharges on non-recyclable structures intensify, converters bundle bioplastic substrates with water-based inks and solvent-free adhesives, adding marketing heft to their sustainability claims in export pitches.

By Product Types: Sachets Capture the Single-Serve Wave

Bags and pouches dominated the Vietnam flexible plastic packaging market with 47.53% share in 2025 owing to their versatility across rice, coffee, and pet food. Their lightweight profile trims logistics costs by up to 60% relative to glass jars, a saving that aligns with food manufacturers’ margin objectives. Sachets and stick packs, on the other hand, are sprinting ahead at a 7.51% CAGR as FMCG brands communicate trial-size offers to cost-conscious shoppers. The format’s low resin requirement per unit also appeals to retailers looking to maximize shelf facings.

High-output form-fill-seal machines installed in 2025 churn out 300 sachets per minute with ±0.5 mm registration accuracy, enabling promotional campaigns with rapid artwork changes. Degassing valves integrated into coffee sachets preserve aroma, while laser micro-perforations allow easy tear without contaminating contents. Films and wraps continue steady growth fueled by e-commerce shippers that require stretch films for pallet stability. Labels and sleeves, though smaller in tonnage, capture premium margins through digital embellishments like variable QR codes linked to authenticity checks.

By End-User Industry: Personal Care Outpaces Food in Growth

Food retained 31.05% volume share in 2025, anchored by packaged seafood, instant noodles, and confectionery exports, which wrest cost advantages from flexible formats. High-barrier pouches extended chilled meat shelf life from seven to 14 days, cutting waste and easing distribution across Vietnam’s elongated geography. Yet the personal care and cosmetics category, scaling at a 5.62% CAGR, injects dynamism into the Vietnam flexible plastic packaging market. Rising disposable incomes propel demand for single-use facial masks, shampoo sachets, and airless lotion pouches.

Premium skincare brands specify multi-chamber pouches that segregate active ingredients until point of use, safeguarding potency. Decorative cold foils and matte varnishes upgrade shelf appeal, while precise spout fitments facilitate controlled dispensing. Pharmaceuticals and nutraceuticals provide incremental upside by adopting child-resistant closures and serialized coding, although regulatory audits extend qualification cycles.

By Printing Technology: Digital Accelerates Mass Customization

Flexography held a 43.78% share in 2025, thanks to its balance of cost and quality for runs exceeding 20,000 m². Gearless presses introduced servo-driven decks that minimize waste on job changeovers, mitigating ink and substrate losses. Rotogravure retains relevance for ultra-high-volume cereal webs where nine-color images demand flawless gradients. Digital inkjet, expanding at 6.98% CAGR, answers e-commerce’s appetite for hyper-localized designs and serialized packaging. Job-queue software now groups multiple SKUs on a single roll, slashing makeready times to minutes.

Hybrid presses combining flexo priming with CMYK inkjet overprints allow converters to amortize capital while offering short-run agility. Brands exploit versioning to print regional dialects, festival themes, or influencer collaborations, sharpening consumer engagement. As inkjet head reliability rises, downtime falls and cost per square meter narrows, bringing digital breakeven closer to 15,000 impressions, a tipping point that will reshape supply-chain economics over the next five years.

Geography Analysis

Southern Vietnam, encompassing Ho Chi Minh City and the industrial corridors of Binh Duong, Dong Nai, and Long An, contributes close to 59.40% of national flexible packaging output. The Vietnam flexible plastic packaging market size in this zone benefits from port access at Cat Lai and Cai Mep, enabling just-in-time export shipments to ASEAN and EU customers. QuickPack’s new Long An complex typifies FDI gravitating toward the south thanks to integrated logistics and abundant skilled labor.

Northern provinces centered on Hanoi and Hai Phong account for roughly 25.30% of capacity. Government incentives there emphasize high-tech and eco-friendly production, attracting investors that value proximity to the Sino-Vietnam border trade routes. However, longer trucking distances to the populous south elevate freight costs, encouraging dual-sourcing strategies among national brands.

Central Vietnam contributes the remaining 15.30%, spearheaded by Da Nang’s expanding tourism-driven F&B cluster and Can Tho’s agro-processing base. As highways and deep-sea ports under the North–South Expressway program near completion, converters are scouting secondary cities where land leases run 30-40% cheaper than Ho Chi Minh City. Geographic diversification increasingly features in boardroom discussions as firms weigh resilience against regional wage inflation and urban congestion.

The flexible plastic packaging market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as North America, Latin America, and Middle East and Africa, along with detailed country-level analysis for Thailand, Indonesia, Canada, Mexico, Nigeria, and Morocco.

Competitive Landscape

The Vietnam flexible plastic packaging industry hosts a balanced mix of international heavyweights and homegrown specialists. Amcor, Huhtamaki, and SIG leverage proprietary barrier films and global food-safety certifications to lock in multinational FMCG accounts. Domestic leaders such as An Phat Holdings, Rang Dong Long An, and Duy Tan stress competitive lead times, localized design services, and accelerating adoption of mono-material solutions. Mid-tier converters are carving niches by pairing digital printing with solvent-free lamination, winning agile brands seeking rapid product-launch cycles.

Strategic investments illustrate this evolutionary arc. Tetra Pak upgraded its Binh Duong factory to BRCGS AA+ and LEED Gold v4, underscoring its commitment to energy-efficient sterile carton production. [3]Vietnam Investment Review, “German QuickPack invests $31.7 million in Long An packaging facility,” vir.com.vn Marubeni boosted its annual capacity to 400,000 tonnes, signaling confidence in the Vietnam flexible plastic packaging market’s export runway. Local players respond by importing high-speed W&H Vistaflex presses and adopting ERP suites that provide end-to-end traceability, capabilities once exclusive to multinationals.

Collaboration along the value chain is intensifying. Resin suppliers co-develop tailored PE grades with converters, while brand owners engage in early-stage pack design to pre-qualify EPR-compliant structures. The result is a competitive ecosystem where technology, sustainability credentials, and supply-chain integration matter as much as price, tempering pure cost competition and raising the barrier to entry for non-specialist newcomers.

Vietnam Flexible Plastic Packaging Industry Leaders

Amcor Plc

Huhtamaki Oyj

SIG Group AG

Genpack Co., Ltd.

Ngai Mee Group Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tetra Pak demonstrated its retortable Tetra Recart solutions at ProPak Vietnam, touting 30% warehouse-space savings and 60% operating-cost cuts relative to metal or glass.

- February 2025: QuickPack inaugurated a USD 31.7 million machinery plant in Long An to localize production of high-efficiency laminators and slitters.

- January 2025: Marubeni expanded Vietnamese capacity to 400,000 tonnes, targeting surging e-commerce and processed-food demand.

- March 2024: Hiep Phu Green Packaging partnered with Koenig & Bauer to install flexo lines using water-based inks and solvent-free lamination, aligning with EPR directives.

Vietnam Flexible Plastic Packaging Market Report Scope

The study on the Vietnamese flexible plastic packaging market tracks the demand for flexible plastic packaging by material in terms of revenue. It tracks the market size for respective end-user types. The estimates for the Japan flexible plastic packaging market include all the costs associated with flexible plastic packaging manufacturing, from raw material procurement to end-use industries. The estimates exclude the cost of the content that is or is to be packed inside the flexible plastic packaging. The scope of the flexible plastic packaging market is limited to B2B demand. Market numbers are based on bottom-up and top-down approaches for segmentation, and volume has also been considered.

The Vietnamese flexible packaging market is segmented by material type (polyethylene (PE), bi-oriented polypropylene (BOPP), cast polypropylene (CPP), polyvinyl chloride (PVC), ethylene vinyl alcohol (EVOH), and other material types), product type (pouches, bags, films and wraps, and other product types), end-user industry (food [baked food, snacked food, meat, poultry, and seafood, candy/confections, pet food, and other food], beverage, personal care and cosmetics, and other end-user industries). The market sizes and forecasts are provided in terms of volume (tonnes) for all the above segments.

| Polyethylene (PE) |

| Bi-Oriented Polypropylene (BOPP) |

| Cast Polypropylene (CPP) |

| Ethylene Vinyl Alcohol (EVOH) |

| Bioplastics and Compostable Materials |

| Other Material Types |

| Bags and Pouches |

| Films and Wraps |

| Sachets and Stick Packs |

| Other Product Types |

| Food | Baked Goods |

| Snacks | |

| Meat, Poultry and Seafood | |

| Confectionery | |

| Pet Food | |

| Other Food Products | |

| Beverage | |

| Personal Care and Cosmetics | |

| Healthcare and Pharmaceuticals | |

| Other End-user Industries |

| Flexography |

| Rotogravure |

| Digital |

| Other Printing Technologies |

| By Material Type | Polyethylene (PE) | |

| Bi-Oriented Polypropylene (BOPP) | ||

| Cast Polypropylene (CPP) | ||

| Ethylene Vinyl Alcohol (EVOH) | ||

| Bioplastics and Compostable Materials | ||

| Other Material Types | ||

| By Product Types | Bags and Pouches | |

| Films and Wraps | ||

| Sachets and Stick Packs | ||

| Other Product Types | ||

| By End-user Industry | Food | Baked Goods |

| Snacks | ||

| Meat, Poultry and Seafood | ||

| Confectionery | ||

| Pet Food | ||

| Other Food Products | ||

| Beverage | ||

| Personal Care and Cosmetics | ||

| Healthcare and Pharmaceuticals | ||

| Other End-user Industries | ||

| By Printing Technology | Flexography | |

| Rotogravure | ||

| Digital | ||

| Other Printing Technologies | ||

Key Questions Answered in the Report

What volume is forecast for Vietnam’s flexible plastic packaging demand by 2031?

Demand is projected to hit 0.37 million tonnes by 2031, advancing at a 6.76% CAGR.

Which product type is growing fastest in Vietnam’s flexible packaging space?

Sachets and stick packs, expanding at a 7.51% CAGR as single-serve formats gain traction.

How are EPR regulations influencing material choices among Vietnamese converters?

They are accelerating a shift toward mono-material PE films that meet mandated recycling targets of 27% by 2025 and 65% by 2030.

Which printing technology is rising most quickly?

Digital inkjet printing is scaling at a 6.98% CAGR due to the need for rapid customization and short runs.

What regional hub dominates flexible packaging output in Vietnam?

The southern economic corridor anchored by Ho Chi Minh City accounts for about 59.40% of national capacity, leveraging port access and foreign investment.

Page last updated on: