Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

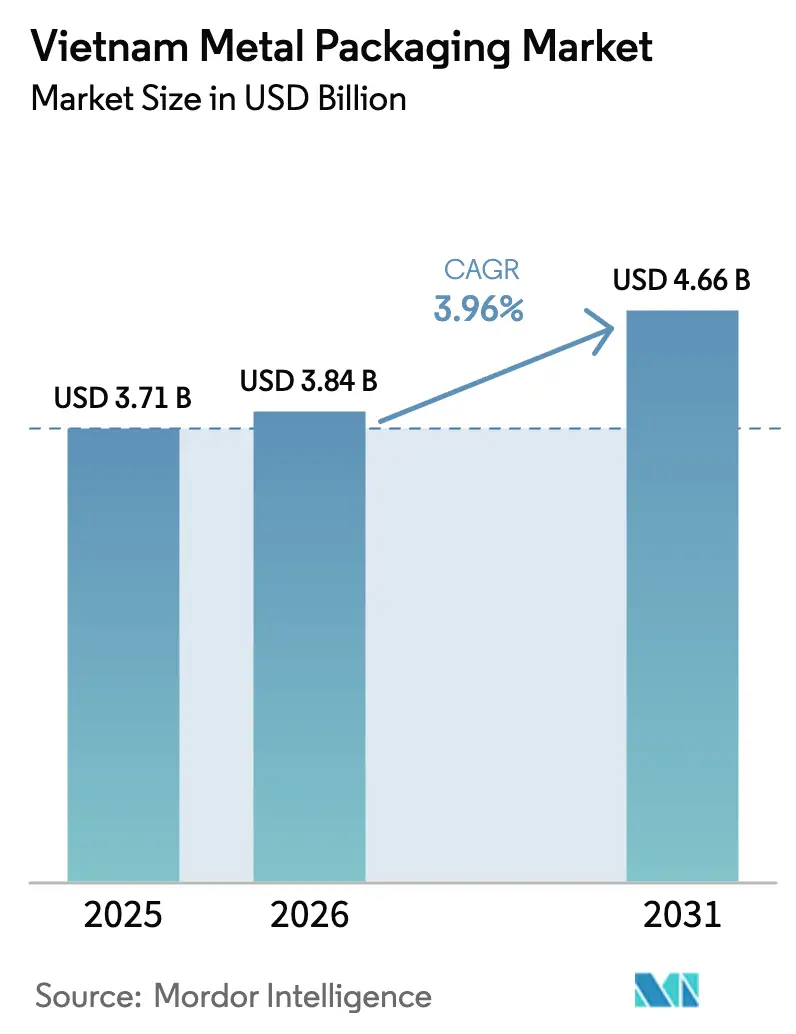

| Base Year Market Size (2025) | USD 3.71 Billion |

| Market Size (2026) | USD 3.84 Billion |

| Market Size (2031) | USD 4.66 Billion |

| Growth Rate (2026 - 2031) | 3.96% CAGR |

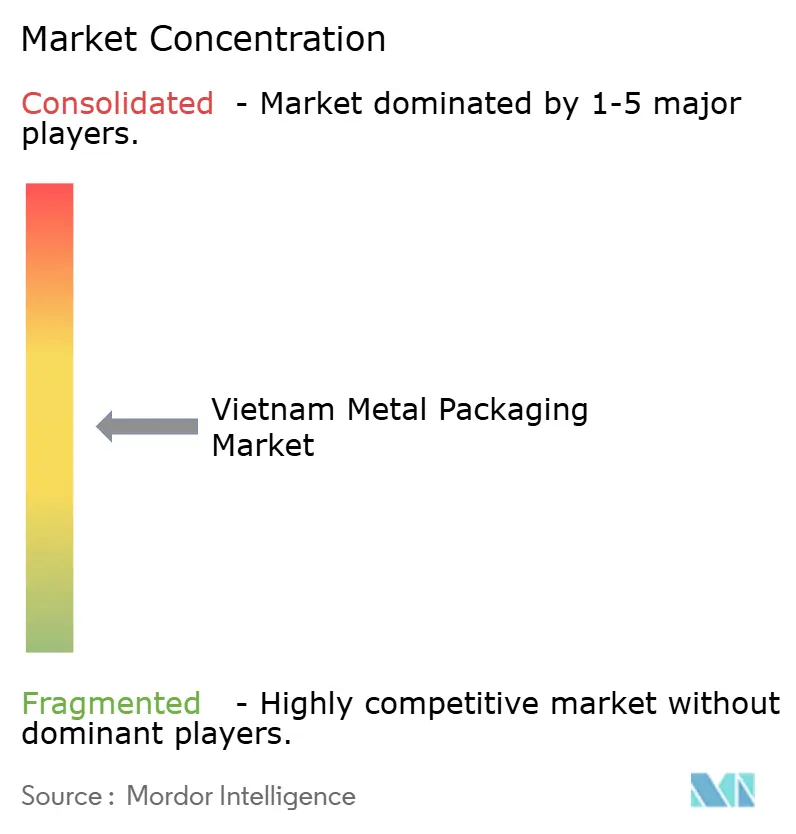

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Metal Packaging Market Analysis by Mordor Intelligence

The Vietnam metal packaging market size is expected to increase from USD 3.71 billion in 2025 to USD 3.84 billion in 2026 and reach USD 4.66 billion by 2031, growing at a CAGR of 3.96% over 2026-2031. A wave of beverage-canning investments, favorable circular-economy policies, and rising urban disposable incomes are reinforcing demand, while aluminum-coil price swings and flexible-plastic substitution temper momentum. Multinational brewers, soft-drink producers, and seafood exporters are collectively lifting unit volumes, yet raw-material inflation is squeezing EBITDA margins for can makers that import 95% of their coil feedstock. Steel’s comeback in industrial barrels and drums, the growing preference for single-serve beverage formats, and e-commerce’s need for dent-resistant containers provide fresh avenues for suppliers able to balance cost and sustainability imperatives. As brands race to meet a 70% recycling mandate by 2030, metal’s recyclability advantage underpins its competitive moat, protecting the Vietnam metal packaging market from aggressive price promotions in flexible pouches.

Key Report Takeaways

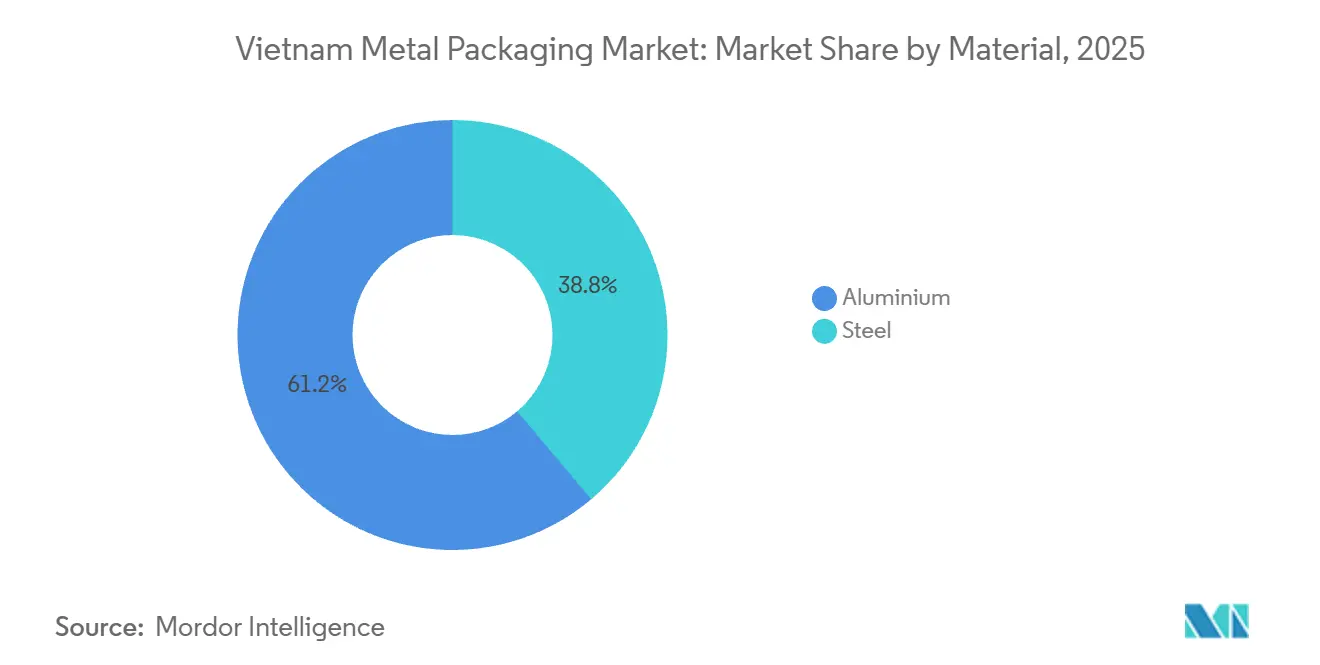

- By material, aluminum led with 61.17% of the Vietnam metal packaging market share in 2025, whereas steel is forecast to expand at a 4.86% CAGR through 2031.

- By product type, beverage cans commanded 58.52% of the Vietnam metal packaging market share in 2025, while shipping barrels and drums are projected to advance at a 5.33% CAGR to 2031.

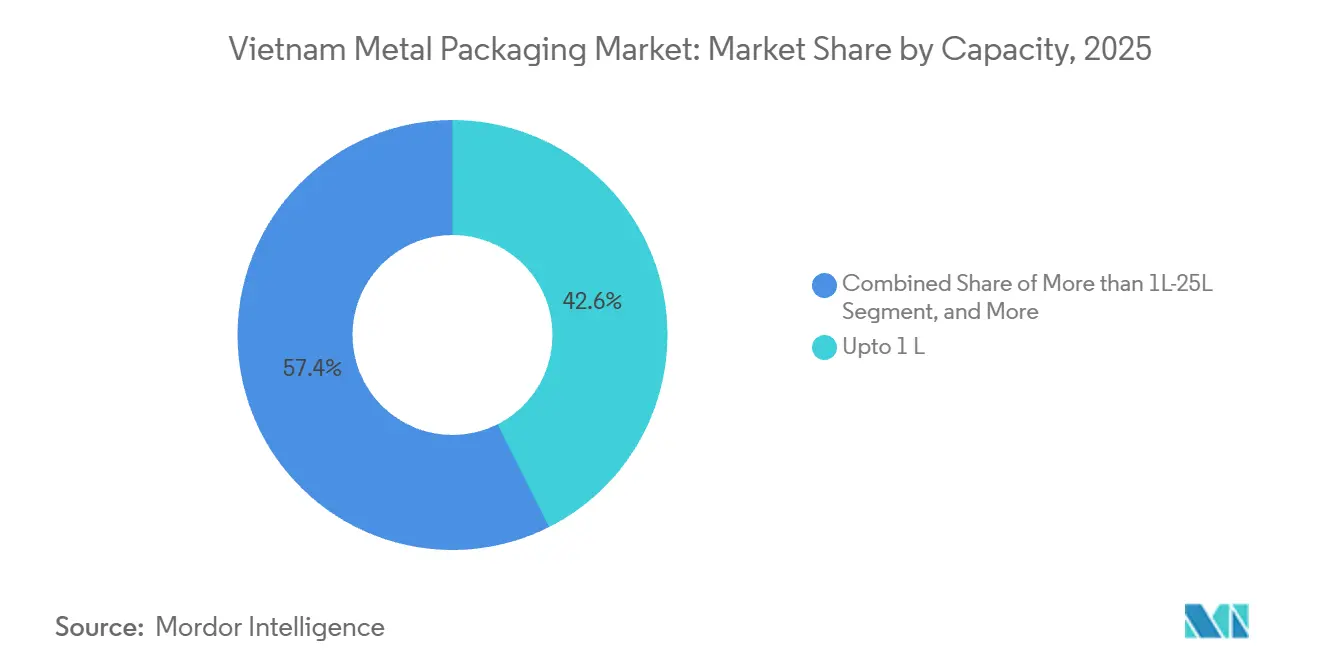

- By capacity, packages up to 1 liter accounted for 42.57% of the Vietnam metal packaging market share in 2025, and containers in the 1-to-25-liter bracket are expected to log a 4.48% CAGR through 2031.

- By end-use industry, beverages captured 38.23% share in 2025, yet industrial applications are on track to post a 5.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Metal Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for Convenient, Ready-to-Eat Meals | +0.7% | National, with early gains in Hanoi, Ho Chi Minh City, Da Nang | Medium term (2-4 years) |

| Rising Urban Middle-Class Consumption Power | +0.9% | National, concentrated in urban centers and provincial capitals | Long term (≥ 4 years) |

| Government Push toward Circular Economy Targets | +0.8% | National, with pilot programs in Hanoi, Ho Chi Minh City, Binh Duong | Medium term (2-4 years) |

| Expansion of Domestic Beverage Canning Capacity | +1.2% | National, with major investments in Binh Duong, Quang Nam, Ba Ria-Vung Tau | Short term (≤ 2 years) |

| Growth of Export-Oriented Seafood Processing | +0.6% | Coastal provinces: Kien Giang, Ca Mau, Ben Tre, Ba Ria-Vung Tau | Medium term (2-4 years) |

| E-commerce Adoption Requiring Robust Transit Packaging | +0.5% | National, with spillover to rural provinces via logistics hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Domestic Beverage Canning Capacity

Vietnam recorded more than USD 600 million of brewery and soft-drink line upgrades between 2024 and 2025, effectively doubling aggregate canning throughput and positioning the country as Southeast Asia’s aluminum-can hub. Heineken alone committed USD 540 million to boosting capacity in Binh Duong, while Suntory PepsiCo increased output by 65% to 825 million liters per year. Faster line speeds, exemplified by Sunrise Packaging’s 2,000-cans-per-minute installation in March 2025, have trimmed unit costs by 12% and encouraged a switch from glass to cans for mainstream beers. Capacity additions are cascading upstream as Marubeni’s NM2 Aluminum Recycling project targets 50,000 tonnes of coil per year, easing reliance on imports.[1]Marubeni Corporation, “Investment in NM2 Aluminum Recycling,” marubeni.com The resulting supply security and cost stability are expanding the addressable market for Vietnam's metal packaging market.

Rising Urban Middle-Class Consumption Power

Vietnam’s urban middle class surpassed 36 million citizens in 2025, each earning more than USD 5,000 annually and favoring premium craft beers, ready-to-drink coffee, and imported spirits. Metal containers offer extended shelf life without refrigeration, a key advantage given the uneven cold-chain infrastructure. TBC-Ball’s 850-million-can plant in Binh Duong fulfills this upscale demand, supplying sleek cans that enhance shelf presence and meet Aluminium Stewardship Initiative standards. The same demographic is fueling a boom in pressurized household-care aerosols, with 47 new SKUs arriving in metal formats during 2024-2025. These lifestyle upgrades keep the Vietnam metal packaging market on a steady growth footing despite macro-economic volatility.

Government Push toward Circular Economy Targets

Decision 222 and Decree 05/2025 oblige brands to collect and recycle 70% of their packaging by 2030. Aluminum cans currently achieve 75% recovery in pilot schemes, well above flexible plastic’s 28% rate, allowing beverage companies to comply at lower cost. Resolution 122 reinforces this policy thrust by requiring a 50% cut in single-use plastics by 2030, prompting SABECO to reduce can-lid gauge 8% and commit to 100% recyclable formats. Investments in reverse-logistics networks, including Marubeni’s recycling venture, align economics with policy goals. Together, these mandates give the Vietnam metal packaging market a structural tailwind.

Surging Demand for Convenient Ready-to-Eat Meals

Retail modernization and time-pressed urban lifestyles are stimulating demand for canned meals that offer long ambient shelf life. Food-processing output advanced to USD 79.3 billion in 2024, up 7.4% year-on-year. Steel cans withstand high-temperature retort sterilization at 121 degrees Celsius, making them indispensable for export-ready seafood and prepared meals. European and North American buyers typically pay a 15-20% premium for hermetically sealed cans over pouches, feeding volume growth in the Vietnam metal packaging market. Domestic processors have responded with USD 180 million in line upgrades across Kien Giang and Ca Mau, widening demand for can-grade steel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Competition from Flexible Plastics | -0.6% | National, with higher impact in food and personal-care segments | Short term (≤ 2 years) |

| Price Volatility of Imported Aluminum Coil | -0.8% | National, affecting all aluminum-can producers | Short term (≤ 2 years) |

| Environmental Opposition to Bauxite Mining | -0.3% | Central Highlands: Dak Nong, Lam Dong, Gia Lai | Long term (≥ 4 years) |

| Skill Gaps in High-Speed Can-Making Operations | -0.4% | National, concentrated in industrial zones lacking technical schools | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Imported Aluminum Coil

Spot aluminum hovered near USD 2,500 per tonne in early 2026 after peaking at USD 2,700 in 2024, a swing that compressed 8-12% EBITDA margins for can makers locked into annual supply contracts.[2]London Metal Exchange, “Aluminum Daily Cash Price,” lme.com Showa Aluminum reported coil costs climbing to 68% of cost of goods sold in its 2024 filing, up from 62% in 2022, despite hedging 40% of 2026 needs. Dong depreciation added a further 3.2% cost burden in 2024.[3]State Bank of Vietnam, “Annual Exchange Rate Summary,” sbv.gov.vn Until domestic smelters come online, the Vietnam metal packaging market remains exposed to global commodity cycles that can abruptly erode profitability.

Intensifying Competition from Flexible Plastics

Flexible pouches cost 30-40% less than cans and weigh 85% less, enticing processors of sauces, ready meals, and personal-care goods to launch 120 new pouch SKUs in 2024-2025. The format claimed 18% of ready-meal volume in 2025, up from 12% in 2023, nibbling at food-can demand. Yet Decree 05/2025’s 70% recycling threshold and Resolution 122’s crackdown on single-use plastics raise compliance costs for flexible packaging, giving metal a defensive moat. Crown Holdings is leveraging this gap with embossed 330-milliliter sleek cans that resonate with craft brands and offset price gaps through premium shelf appeal.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Aluminium Dominance Amid Steel Revival

Aluminum secured 61.17% share of the Vietnam metal packaging market in 2025 as beverage giants installed 3.2 billion cans of annual capacity. In parallel, steel is expected to log a 4.86% CAGR through 2031, surpassing aluminum’s pace as seafood processors and paint makers migrate from plastic jerrycans to steel pails compliant with hazardous-goods rules. The Vietnam metal packaging market size for aluminum remains anchored by its 75% post-consumer collection rate and 18% freight-weight advantage versus steel, aiding multinationals under tightening Extended Producer Responsibility targets. Conversely, domestic steel capacity from Hoa Phat’s Dak Lak complex offers price stability and shorter lead times, tempting industrial buyers who prize supply security.

Aluminum’s future trajectory hinges on Marubeni’s 50,000-tonne recycling line, which slashes carbon footprints 95% and could elevate recycled content in beverage cans beyond 75%. Steel’s leap is spurred by e-commerce, where pails survive last-mile courier knocks that puncture flexible plastics, driving order-fulfillment providers to favor metal. With both substrates widening their addressable niches, the Vietnam metal packaging market shows healthy dual-material growth rather than a zero-sum battle.

By Product Type: Cans Lead While Drums Accelerate

Beverage and food cans contributed 58.52% of market share in 2025, cementing their primacy in the Vietnam metal packaging market. Shipping barrels and drums, buoyed by USD 9.2 billion in seafood exports and USD 45 billion in chemical shipments, are forecast to outpace every other product group at a 5.33% CAGR through 2031. The Vietnam metal packaging market share for cans remains insulated from pouch incursion, thanks to carbonation needs and consumer preference for metal freshness cues. Meanwhile, aerosol cans captured 8% of 2025 output as personal-care brands embraced pressurized dispensers.

Greif’s Ba Ria-Vung Tau facility reported 18% volume gains in 2024 as 200-liter steel drums found takers among fish-sauce exporters complying with EU food-contact rules. Drum durability also resonates with chemical shippers seeking IMO-approved barrels. Crown Holdings’ embossed sleek can, adopted by 22% of microbreweries within six months, illustrates the ongoing premiumization in can design that sustains higher margins. These dual trends reinforce diversified growth across the Vietnam metal packaging market.

By Capacity: Single-Serve Formats Drive Volume

Packages up to 1 liter accounted for 42.57% of market share in 2025, as on-the-go consumption lifted 330-milliliter and 500-milliliter cans. Containers in the 1-to-25-liter band are set to grow 4.48% annually through 2031, driven by paint manufacturers replacing 40% of plastic jerrycans with steel pails to meet ISO 14001 targets. The Vietnam metal packaging market size for mid-volume pails benefits from lower damage rates in e-commerce, where metal withstands the last-mile journey better than flexible alternatives.

TBC-Ball’s 850-million-can line feeds demand for single-serve beverages, while online retailers in Ho Chi Minh City report 30% fewer returns for pail-packed DIY paints versus plastic equivalents. Industrial drums above 200 liters retain a 14% share thanks to seafood bulk exports, with processors in Kien Giang using steel barrels that tolerate retort sterilization. Collective demand across these capacity bands underscores the balanced expansion of the Vietnam metal packaging market.

By End-Use Industry: Beverage Anchors Industrial Surges

Beverage brands held 38.23% of market share in 2025, supported by USD 600 million in canning investments and per-capita beer consumption hitting 47 liters. Industrial applications, spanning paints, chemicals, and lubricants, are projected to clock a 5.24% CAGR to 2031, the sharpest climb among end-users. The Vietnam metal packaging market share for beverages benefits from carbonation integrity and premium branding, whereas industrial buyers value steel’s puncture resistance and compliance with IMDG codes.

Food processors account for 28% of volume, driven by canned tuna and tropical fruit exports that require hermetic seals for EU and U.S. distribution. Personal-care and pharmaceutical segments combined for 18% in 2025, with aerosol cans growing 12% year-on-year. Extended Producer Responsibility rules are nudging paint firms toward metal pails, while seafood exporters rely on drums to secure cold-chain integrity. This multipronged demand confirms the resilience of the Vietnam metal packaging market across consumer and industrial realms.

Geography Analysis

Southern provinces, including Binh Duong, Dong Nai, and Ba Ria-Vung Tau, host roughly 55% of installed capacity, leveraging proximity to Ho Chi Minh City’s 10 million consumers and export docks that channel seafood and chemicals abroad. TBC-Ball’s plant in Binh Duong’s Vietnam-Singapore Industrial Park IIA churns out 850 million cans annually for Heineken and craft breweries. Crown Holdings maintains twin lines in Ho Chi Minh City and Dong Nai, underpinning the Vietnam metal packaging market’s southern concentration.

Northern clusters around Hanoi contribute 25% capacity, buoyed by Sunrise Packaging’s 2,000-cans-per-minute upgrade in Bac Ninh. Logistics arteries connecting Haiphong port to China amplify export efficiency for shipping bulk lubricants in steel drums. Central Vietnam, anchored by Da Nang’s cargo throughput of 8.5 million tonnes in 2024, commands 12% of capacity, supported by Showa Aluminum’s unit in Quang Nam, which serves regional soft-drink bottlers.

The Mekong Delta accounts for 8% and specializes in steel cans for canned seafood and 200-liter drums for fish sauce. Capacity growth here lags due to fragmented infrastructure, yet rising EU demand for certified canned tuna is spurring new line installs in Kien Giang. Hoa Phat’s Dak Lak steel complex, commencing operations in June 2025, is expected to shorten coil lead times for central and northern can makers, reducing freight costs and balancing regional supply. Collectively, these geographic dynamics keep the Vietnam metal packaging market well diversified across the country’s north-south corridors.

Competitive Landscape

The Vietnam metal packaging market is moderately fragmented, including companies such as Crown Holdings, Ball Corporation, and Showa Aluminum. Scale economies favor multinationals; Crown’s embossed sleek can captured 22% adoption among microbreweries six months after launch, illustrating the branding leverage wielded by global suppliers. TBC-Ball secured Aluminium Stewardship Initiative certification in 2022, enabling premium craft labels to meet imported-content disclosure rules, a differentiator that smaller players struggle to match.

Technology investment is the contest’s second pillar. Sunrise Packaging’s USD 55 million Bac Ninh upgrade shaved unit costs by 12% and signaled a move from commodity to value-added production. Greif’s 200-liter drum line leverages robotics to deliver defect rates below 0.5%, critical for hazardous-goods transport. Meanwhile, Marubeni’s recycling joint venture secures closed-loop coil, insulating affiliated can makers from LME volatility.

Regional conglomerates are pursuing M&A to gain instant capacity. SCG Packaging achieved full control of Duy Tan in June 2025 for USD 108.8 million, positioning itself against metal incumbents through multimaterial offerings. Adjacent players such as Tetra Pak and Indorama Ventures have also invested heavily, confirming Vietnam’s status as a strategic packaging hub. Competitive intensity is rising as regulatory deadlines loom, and suppliers that combine high-speed lines, recycling capability, and sustainability accreditation are best positioned to grow share within the Vietnam metal packaging market.

Vietnam Metal Packaging Industry Leaders

Canpac Vietnam Co., Ltd

Nihon Canpack (Vietnam) Co., Ltd.

Crown Holdings, Inc.

Showa Aluminum Can Corporation

TBC-Ball Beverage Can VN Ltd (Ball Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Baosteel began construction of a flat-rolled steel plant aimed at the beverage-can and industrial-drum segments, leveraging Chinese oversupply to offer competitive coil prices.

- August 2025: Carlsberg started a new canning line at its Phu Bai brewery, adding 150 million liters of annual capacity.

- June 2025: Hoa Phat Group commenced Phase 1 of its USD 5 billion Dak Lak steel complex, targeting 6 million tonnes per year of coil for can and drum manufacture.

- June 2025: SCG Packaging finalized the USD 108.8 million purchase of the remaining stake in Duy Tan, consolidating rigid-plastic and flexible-film assets.

Vietnam Metal Packaging Market Report Scope

The Vietnamese metal packaging market is defined by the revenues from the sale of metal packaging products considered in the study. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry. Market estimations and growth rates over the forecast period have been included.

The Vietnam Metal Packaging Market Report is Segmented by Material (Aluminium, and Steel), Product Type (Cans, Bulk Containers, Shipping Barrels and Drums, Caps and Closures, and Other Product Types), Capacity (Up to 1 L, >1L-25L, >25L-200L, and Above 200L), and End-use Industry (Beverage, Food, Paint and Chemical, Industrial, and Other End-use Industries). The Market Forecasts are Provided in Terms of Value (USD).

By Material

| Aluminium |

| Steel |

By Product Type

| Cans | Food Cans |

| Beverage Cans | |

| Aerosol Cans | |

| Bulk Containers | |

| Shipping Barrels and Drums | |

| Caps and Closures | |

| Other Product Types |

By Capacity

| Upto 1 L |

| More than 1L to 25L |

| More than 25L to 200L |

| Above 200L |

By End-use Industry

| Beverage |

| Food |

| Paint and Chemical |

| Industrial |

| Other End-use Industries |

| By Material | Aluminium | |

| Steel | ||

| By Product Type | Cans | Food Cans |

| Beverage Cans | ||

| Aerosol Cans | ||

| Bulk Containers | ||

| Shipping Barrels and Drums | ||

| Caps and Closures | ||

| Other Product Types | ||

| By Capacity | Upto 1 L | |

| More than 1L to 25L | ||

| More than 25L to 200L | ||

| Above 200L | ||

| By End-use Industry | Beverage | |

| Food | ||

| Paint and Chemical | ||

| Industrial | ||

| Other End-use Industries | ||

Key Questions Answered in the Report

How big is the Vietnam metal packaging market in 2026?

The market reached USD 3.84 billion in 2026, reflecting solid growth driven by beverage-canning investments.

What is the expected CAGR for Vietnam’s metal packaging demand to 2031?

Aggregate value is projected to rise at a 3.96% CAGR, reaching USD 4.66 billion by 2031.

Which material is growing fastest within Vietnamese metal packaging?

Steel containers, especially barrels and drums, are forecast to grow 4.86% per year through 2031 as seafood and chemical exporters favor robust transit packaging.

How are government regulations shaping packaging choices?

Decree 05/2025 imposes a 70% recycling target by 2030, steering brands toward highly recyclable aluminum cans and steel pails.

Why do beverage cans dominate over pouches in Vietnam?

Carbonation integrity, premium branding, and higher recycling rates keep cans ahead, despite the lower cost of flexible plastics.

Which regions concentrate most metal-packaging capacity?

Southern provinces, led by Binh Duong and Dong Nai, account for about 55% of national capacity because of proximity to Ho Chi Minh City's consumer base and export ports.

Page last updated on: