Home and Property Improvement

9th JuneA Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

The Vietnam Home Textile Market Report is Segmented by Application (Bed Linen, Bath Linen, Kitchen Linen, Upholstery, and More), Material (Cotton, Linen, Synthetic Fibres, Other Materials), End-User (Residential, Commercial), Distribution Channel (B2C/Retail Channels, B2B/Direct From Manufacturers), and Geography (Northern Vietnam, Central Vietnam, Southern Vietnam). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

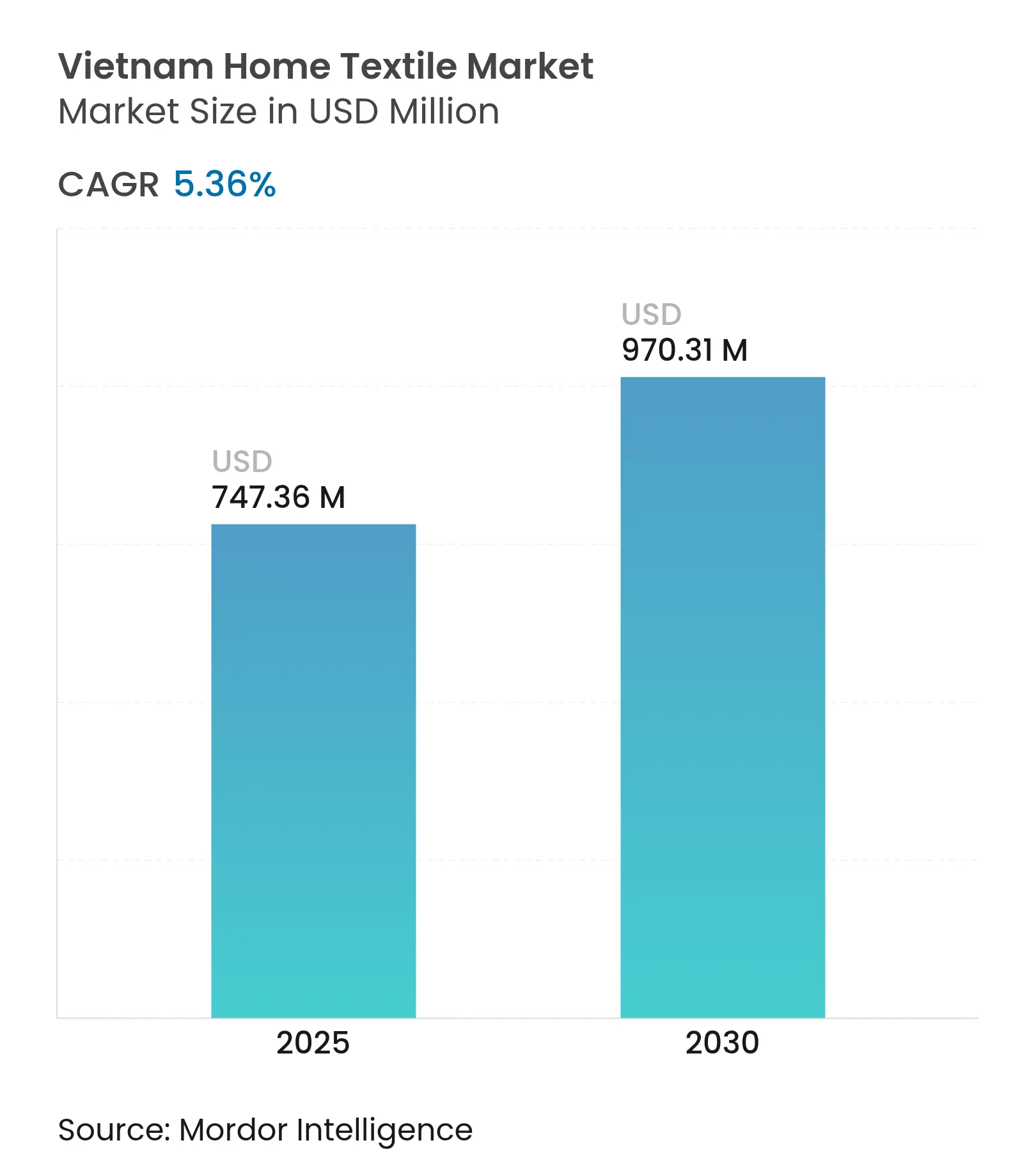

| Market Size (2025) | USD 747.36 Million |

| Market Size (2030) | USD 970.31 Million |

| Growth Rate (2025 - 2030) | 5.36 % CAGR |

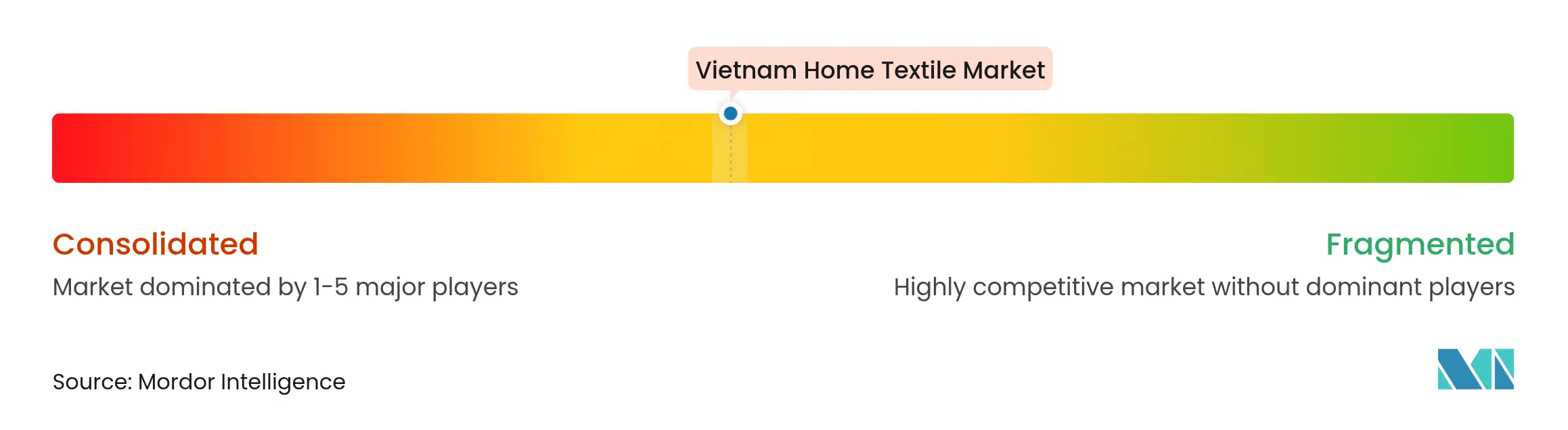

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Vietnam home textile market size stands at USD 747.36 million in 2025 and is forecast to expand to USD 970.31 million by 2030 at a 5.36% CAGR, underscoring sustained growth momentum across both residential and commercial demand segments. Vietnam’s role as the world’s third-largest textile exporter, coupled with USD 44 billion in textile export revenue during 2024, positions the Vietnam home textile market as a strategic beneficiary of global supply-chain diversification[1]Observatory of Economic Complexity, “Vietnam Textiles Profile 2024,” oec.world. Investment in affordable urban housing, rapid e-commerce adoption, tax incentives, and interest subsidies for green projects are reinforcing domestic consumption as well as production upgrades. Cotton remains dominant, yet alternative fibers such as bamboo and hemp are rising quickly as consumers embrace eco-conscious materials. Competition is intensifying as international retailers and sustainability-focused disruptors enter, elevating technology standards and design expectations.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising disposable income and urban migration

Rising disposable income and urban migration

| +1.2% | National (notably Ho Chi Minh City, Hanoi, Da Nang) | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

National (notably Ho Chi Minh City, Hanoi, Da Nang)

|

Impact Timeline

:

Medium term (2-4 years)

|

E-commerce boom in home-decor category

E-commerce boom in home-decor category

| +0.9% | National urban centers | Short term (≤ 2 years) | |||

Tourism-led hospitality expansion

Tourism-led hospitality expansion

| +0.7% | Central & Southern coastal regions | Medium term (2-4 years) | |||

Government textile-modernization subsidies

Government textile-modernization subsidies

| +0.6% | National industrial parks | Long term (≥ 4 years) | |||

Eco-conscious shift toward bamboo and hemp textiles

Eco-conscious shift toward bamboo and hemp textiles

| +0.4% | Export-oriented urban clusters | Long term (≥ 4 years) | |||

Condominium living fuels ready-made linens demand

Condominium living fuels ready-made linens demand

| +0.5% | Major metropolitan areas | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Disposable Income and Urban Migration

Vietnam recorded 6.93% GDP growth year over year in Q1 2025, while manufacturing output rose 9.28% and retail sales climbed 9.9%[2]Government Portal, “GDP Growth and Retail Sales Q1 2025,” baochinhphu.vn.. Vingroup’s pledge to build 500,000 affordable apartments drives household formation that, in turn, accelerates demand for standardized bedding, curtains, and kitchen linens. Each new urban dwelling typically purchases multiple coordinated textile sets, a trend that is strengthening average order values. Higher wages enable households to choose branded or premium products rather than purely price-driven options. This spending shift raises growth prospects for mid- to high-tier suppliers within the Vietnam home textile market.

E-Commerce Boom in Home-Decor Category

Short-form video shopping on TikTok Shop and live-stream deals on Shopee have changed how Vietnamese consumers assess texture, color, and quality, directly influencing conversion rates for home textile items. Competitive platform dynamics reduce logistics lead times and drive aggressive promotions, widening omnichannel reach for emerging domestic brands. Traditional chains such as Bach Hoa Xanh now deploy online-to-offline strategies that merge digital discovery with convenient pick-up or home delivery. Improved last-mile infrastructure diminishes previous trust barriers toward online textile purchases. The result is rapid penetration of digital channels within the Vietnamese home textile market.

Tourism-Led Hospitality Expansion

Vietnam is among the fastest-growing global hospitality destinations, attracting brands like Radisson, Marriott, and Accor to add coastal resorts and city hotels. Each opening requires volumes of commercial-grade bed linen, towels, and drapes that meet strict durability and laundering standards. Hotel interiors inspire domestic consumers to replicate premium looks at home, fostering an aspirational spillover effect. Suppliers able to certify to hospitality specifications are gaining a first-mover advantage in the Vietnam home textile market. Central Vietnam benefits most because seaside resort clusters cluster around Da Nang, Hoi An, and Nha Trang.

Government Textile-Modernization Subsidies

Qualifying textile investors receive 4 years of corporate tax exemption followed by nine years at half rates, plus 2% subsidized interest on green technology loans. The VIATT 2025 program prioritizes digital looms, energy-efficient steam systems, and wastewater recycling, raising national production capabilities. Small and medium manufacturers leverage these incentives to shift from cut-make-trim toward FOB and ODM models that capture higher margins. Upgrades help domestic players meet OEKO-TEX and ISO 14001 demands from foreign retail partners. Long-term policy stability, therefore, underpins the competitiveness of the Vietnamese home textile market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatile cotton prices

Volatile cotton prices

| −0.8% | Nationwide cotton-reliant facilities | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

−0.8%

|

Geographic Relevance

:

Nationwide cotton-reliant facilities

|

Impact Timeline

:

Short term (≤ 2 years)

|

Low-priced Chinese imports

Low-priced Chinese imports

| −0.6% | Mass-market urban and rural outlets | Medium term (2-4 years) | |||

Fragmented Tier-2 and Tier-3 distribution networks

Fragmented Tier-2 and Tier-3 distribution networks

| −0.4% | Smaller cities and rural districts | Medium term (2-4 years) | |||

Design and branding talent gap

Design and branding talent gap

| −0.3% | Manufacturing clusters | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Volatile Cotton Prices

Sharp price swings in global cotton futures compress margins for mills that lack long-term hedging tools. Vietnam imports a significant share of its cotton yarn from India and China, exposing factories to currency fluctuations. When cotton spiked in late 2024, smaller family-run weavers in Nam Dinh reported profit falls of up to 15%. The uncertainty delays capital expenditure and discourages product diversification. Consequently, earnings volatility reduces reinvestment capacity within the Vietnamese home textile market.

Low-Priced Chinese Imports

China exports competitively priced finished sheets and towels that undercut domestic lines in hypermarkets and online flash sales. Vietnamese producers depend on Chinese raw materials yet face direct rivalry from the same suppliers in consumer channels. Retailers in border provinces stock Chinese linens priced 10% lower than local equivalents, eroding share in the value segment. Sustained price pressure prompts rationalization among less efficient Vietnamese producers. This dampens the overall profitability of the Vietnam home textile market.

By Application: Bath Linen Gains Traction among Wellness-Driven Consumers

Bath linen experienced a 6.11% CAGR through 2025-2030, outpacing bed linen, curtains, kitchen linen, and rugs. Hygiene awareness, pampering rituals, and urban spa culture underpin this surge. Hotels propagating triple-sheeting and plush towels have raised expectations at home. Manufacturers install steam-generating heat pumps that cut energy by 30% while improving towel loft, aligning with sustainability pledges[3]Retail Asia Staff, “Heat Pump Pilot Reduces Textile Energy Use,” retailasiaonline.com. Beyond urban condominiums, provincial households increasing water-heater adoption also boost demand for absorbent bath textiles.

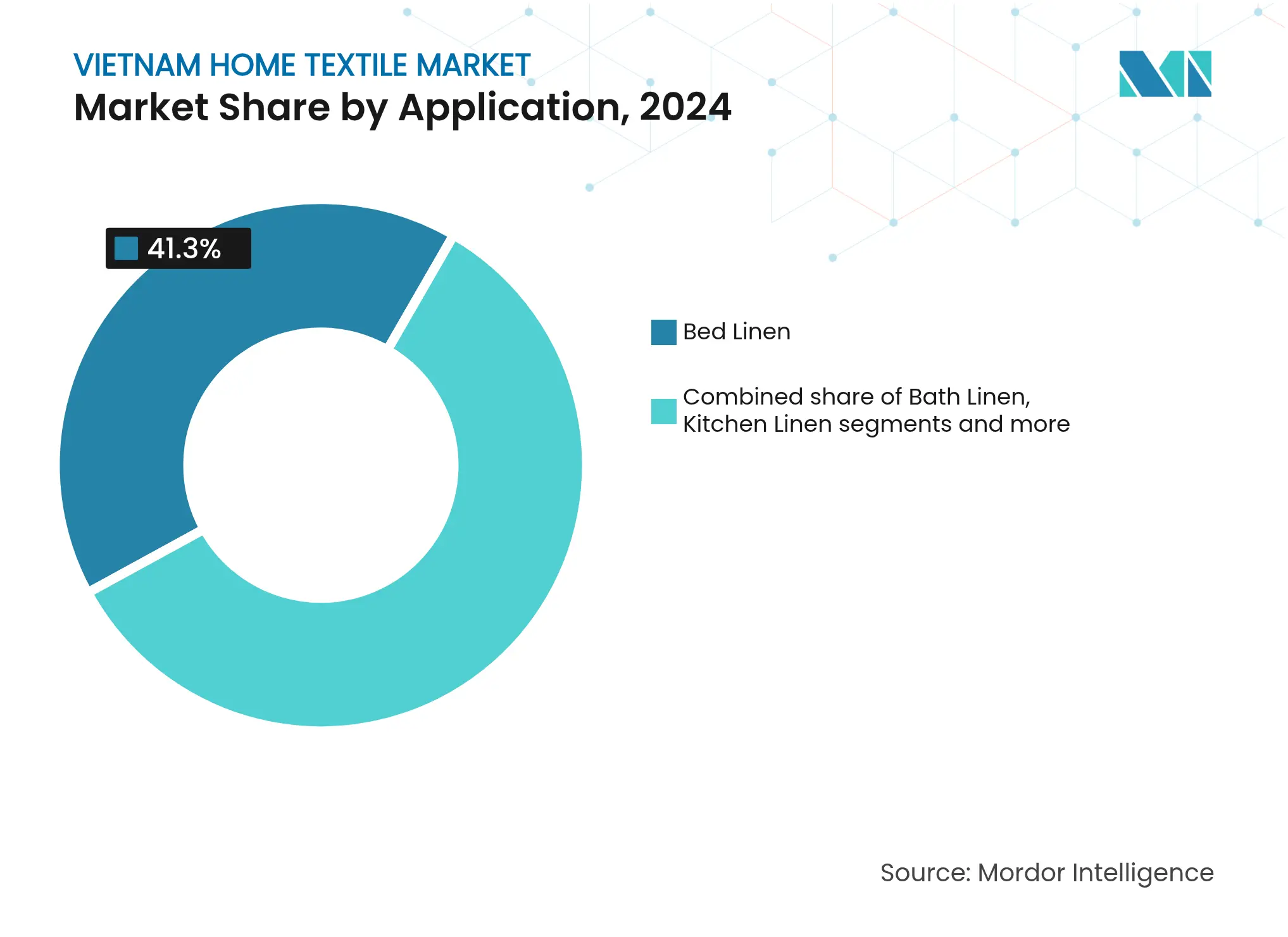

Bed linen remains the volume anchor, holding 41.3% of the Vietnamese home textile market share in 2024. Standardized mattress sizes simplify mass production of fitted sheets, duvet covers, and pillowcases, enabling economies of scale. Kitchen linen sales rise in tandem with the televised cooking trend. Upholstery and drapery benefit from condominium interior packages that include made-to-measure blinds. Carpets and rugs continue to cater to aesthetic preferences in central living spaces, though hot climates restrict usage in smaller apartments. Altogether, application diversity stabilizes revenue streams for the Vietnam home textile market.

Note: Segment shares of all individual segments available upon report purchase

By Material: Natural and Recycled Fibers Diversify the Mix

Cotton commanded a 49.2% share of the Vietnam home textile market size in 2024. It remains favored for softness, breathability, and price. However, bamboo viscose, hemp, silk blends, and recycled polyester are gathering momentum at a 5.91% CAGR. Consumers appreciate bamboo’s inherent antibacterial qualities, while hemp appeals for strength and moisture management in humid climates. SYRE’s upcoming USD 1 billion recycling plant in Bình Định will supply 250,000 tons of virgin-equivalent polyester annually by 2028[4]Government Portal, “SYRE Recycling Investment Approved,” baochinhphu.vn.. Local mills thus gain access to circular materials that satisfy brand sustainability scorecards.

Synthetic fibers still serve mid-priced mass markets needing wrinkle resistance and quick drying. Linen and silk retain niche premium allure, often blended to manage cost. Future growth hinges on certifications such as OEKO-TEX Standard 100, zero-discharge dyeing, and blockchain traceability. Diversifying raw-material portfolios shields players from cotton price volatility, thereby strengthening the resilience of the Vietnam home textile market.

By End-User: Commercial Demand Surges

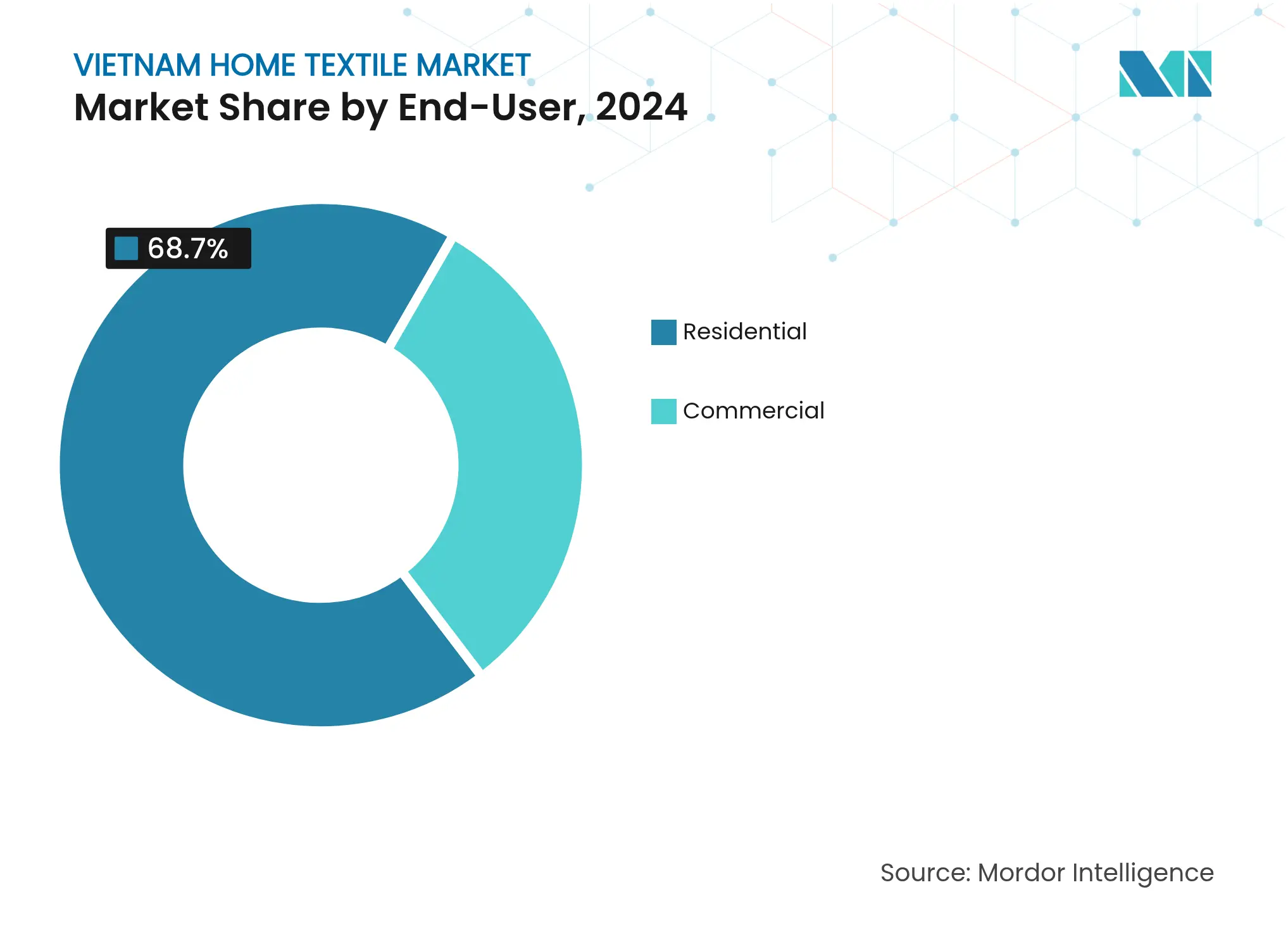

Residential buyers represented 68.7% usage in 2024, reflecting Vietnam’s 97.6 million population and steady household formation. Urban middle-class families refurbish every three to four years, driving repeated purchases. Post-pandemic nesting trends also encourage textile refresh to enhance comfort and style. However, commercial demand is growing faster at 6.03% CAGR on the back of hotel, restaurant, and office expansion. International hotel brands stipulate 300-thread-count linens and color-fast towels, compelling suppliers to invest in higher specification looms.

Healthcare facilities require hypoallergenic sheets and disposable curtains that limit pathogen spread, opening new niches. Corporate offices extend demand to custom cushions and acoustic drapes. The spillover from commercial specification upgrades elevates benchmarks that ultimately benefit the residential segment. As a result, rising B2B opportunities diversify revenue for participants in the Vietnam home textile market.

By Distribution Channel: Digital and Direct Models Gain Ground

B2C retail accounted for 72.1% in 2024 across hypermarkets, department stores, specialty chains, and e-commerce portals. Big-box outlets co-locate with apartment complexes, capturing move-in shopping trips. Specialty stores such as Nitori and local boutique chains offer curated assortments at higher price points, emphasizing Japanese or Scandinavian aesthetics. Live-stream selling has revolutionized online engagement, letting viewers evaluate weave density in real time.

B2B direct-from-factory sales to hotels and interior designers are set to grow at a 5.77% CAGR, aided by trade shows like Vietbuild and virtual sourcing platforms. Manufacturer showrooms in Ho Chi Minh City and Hanoi now host client workshops to finalize color lab-dips and custom embroidery. This direct route improves lead-time predictability and gross margins. A balanced omnichannel strategy, therefore, optimizes reach for the Vietnam home textile market.

Southern Vietnam retained a 34.6% hold in 2024 due to strong urban consumption and export-oriented factories in Ho Chi Minh City, Đồng Nai, and Bình Dương. Integrated logistics through Cát Lái Port and Cai Mep-Thị Vải deep-water terminals facilitate swift shipping for international buyers. The region also houses the country’s largest home-furnishing retail clusters, supporting quick replenishment cycles.

Central Vietnam is forecast to clock a 6.75% CAGR through 2030, bolstered by beach resort corridors and foreign direct investment in Chu Lai and Dung Quất economic zones. Uniqlo’s plan to open its inaugural Hue store in 2025 signals confidence in rising disposable incomes. Government road and airport upgrades shorten travel time between Da Nang and Quy Nhon, enhancing supply-chain agility.

Northern Vietnam, anchored by Hanoi, gains from infrastructure such as the Nội Bài–Lào Cai expressway and intermodal rail links to China. IKEA’s USD 450 million retail center will double as a Southeast Asian distribution hub, validating the region’s strategic value. However, proximity to Chinese imports intensifies competitive price pressure. Regional nuances collectively shape production allocation and sales strategies across the Vietnamese home textile market.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Market Concentration

Competition is moderate and intensifying. Domestic stalwarts such as Everpia, Hanvico, and Phong Phu leverage decades of manufacturing expertise, vertically integrated spinning, and nationwide retail networks. They face rising challenges, including sustainability-focused startups that emphasize bamboo and recycled polyester offerings. Foreign retailers like Nitori and H&M are scaling storefronts while deepening sourcing partnerships with 100-plus Vietnamese factories, spreading global standards across the supply chain.

Technology adoption differentiates leaders. Pilot deployment of steam-generating heat pumps achieved 20% energy savings, positioning early movers to comply with carbon-intensity targets set by European buyers. Digital design platforms reduce sample lead times from three weeks to five days, enabling quick response assortments that match fast-changing consumer tastes. Brands investing in 3D weaving and waterless dyeing win premium contracts and gain leverage in price negotiations.

Strategic moves include joint ventures, ODM expansion, and private-label collaborations with hypermarkets. For example, Hanvico supplies exclusive bedding lines to Aeon while Everpia’s Eskimo brand partners with Lazada for flagship live-stream campaigns. Market entry barriers remain low, yet differentiation through certified sustainability, omnichannel marketing, and rapid design refresh cycles is raising the threshold for success in the Vietnam home textile market.

*Disclaimer: Major Players sorted in no particular order

1. Table of Contents – Vietnam Home Textile Market

2. Introduction

3. Research Methodology

4. Executive Summary

5. Market Landscape

6. Market Size & Growth Forecasts (Value in USD)

7. Competitive Landscape

8. Market Opportunities & Future Outlook

Home textiles, fabrics, and garments tailored for residential furnishing serve functional and aesthetic purposes. In Vietnam, the home textile market is categorized by product, end user, and distribution channel. Products include bed linen, bath linen, kitchen linen, upholstery, and floor covering. End users are segmented into residential and commercial, with the commercial segment further delineated into hospitality and leisure, hospitals, offices, and other commercial end users. Distribution channels encompass supermarkets, specialty stores, online platforms, and other distribution channels. The report provides revenue forecasts in USD for each segment, painting a comprehensive picture of the Vietnamese home textile market.

A Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

Strategic Expansion in the Russia Laundry Appliances Market

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.