Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

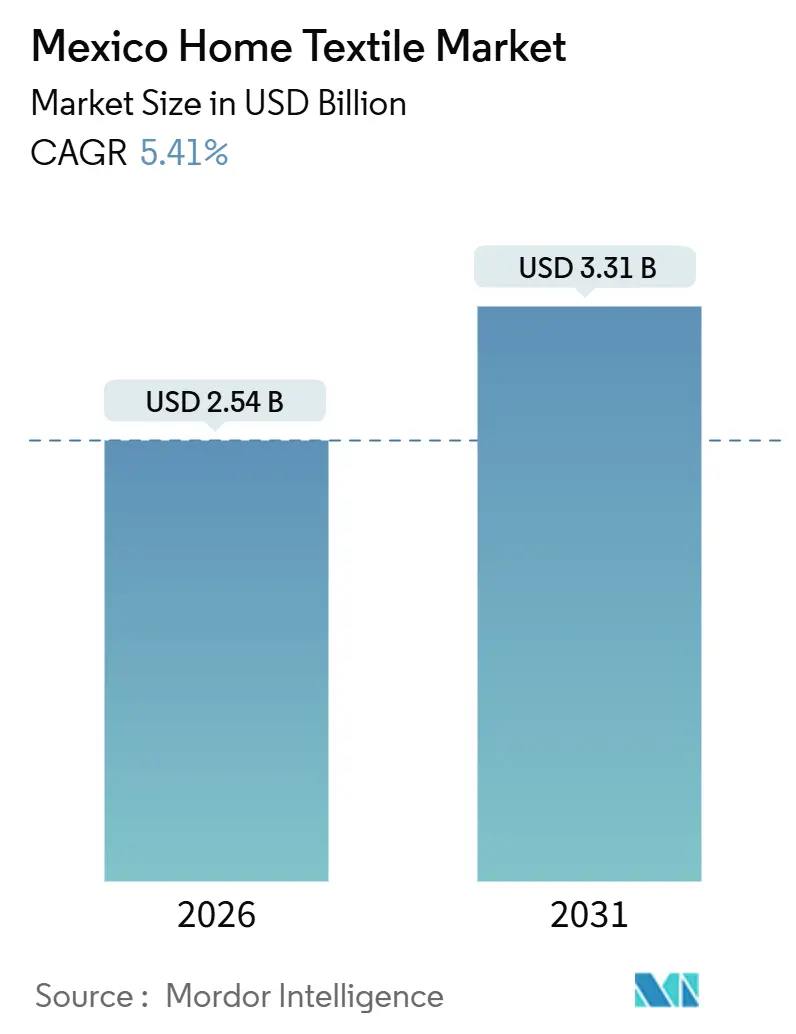

| Market Size (2026) | USD 2.54 Billion |

| Market Size (2031) | USD 3.31 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Home Textile Market Analysis by Mordor Intelligence

The Mexico Home Textile Market size is estimated at USD 2.54 billion in 2026, and is expected to reach USD 3.31 billion by 2031, at a CAGR of 5.41% during the forecast period (2026-2031).

The Mexico home textile market advances on structural drivers tied to housing formation, hospitality activity, and retail modernization that shorten replacement cycles and broaden assortment depth across price tiers. Momentum concentrates in Northern and Central metros where manufacturing inflows, retail investments, and logistics upgrades strengthen product availability and the uptake of premium and performance ranges in the Mexico home textile market. Nearshoring and foreign investment add office and hotel capacity, which intensifies demand for upholstery, linens, and technical fabrics used in frequent-use environments. Omnichannel retail builds scale as large chains enhance click-and-collect, two-day delivery, and marketplace assortments, a shift that accelerates style discovery and purchase frequency in the Mexico home textile market[1]Invest Monterrey, “Nuevo León Tops Mexico in Industrial Growth and Job Creation in 2025,” Invest Monterrey, investmonterrey.com.

Key Report Takeaways

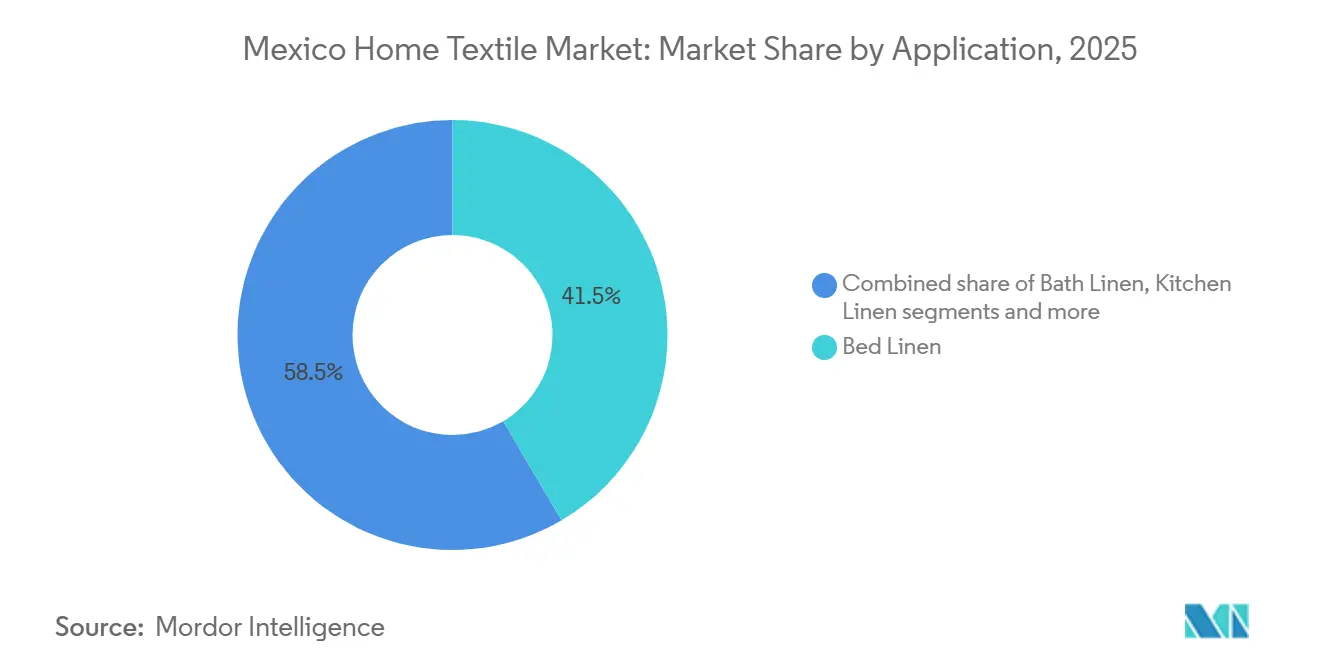

- By application, bed linen led with 41.53% of the Mexico home textile market share in 2025. Upholstery is forecast to expand at a 6.14% CAGR through 2031.

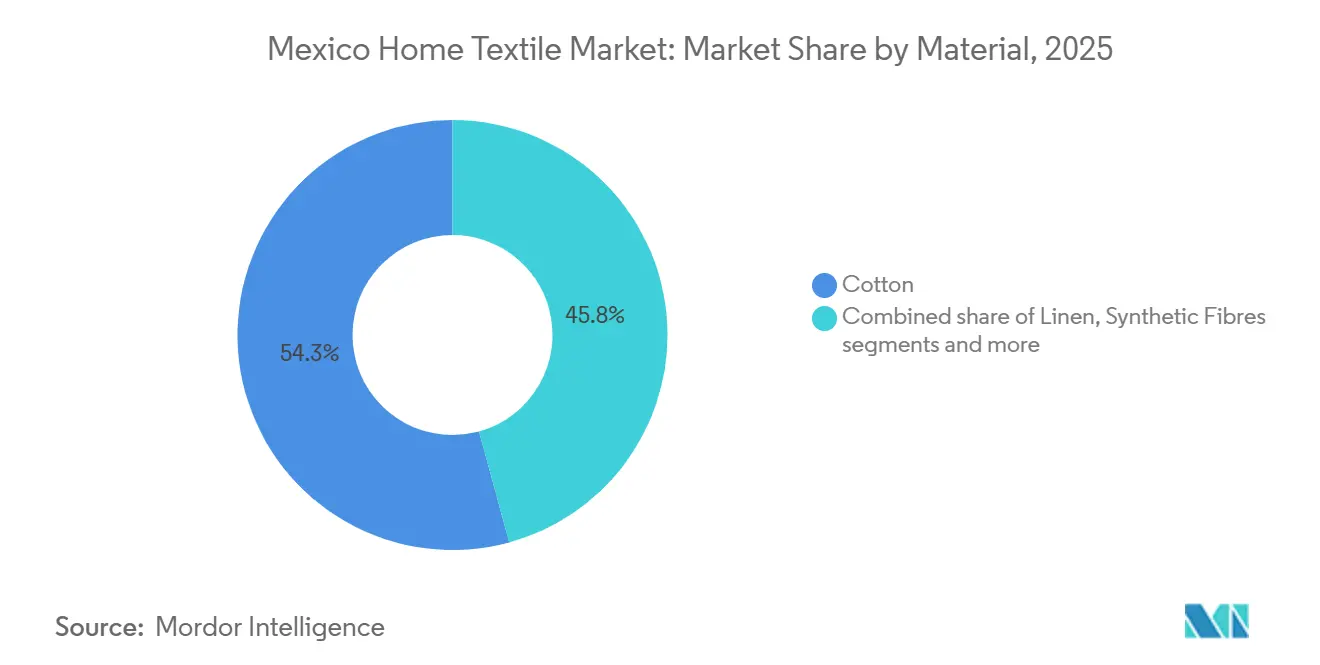

- By material, cotton accounted for 54.25% of the Mexico home textile market share in 2025, while synthetic fibres are projected to expand at a 5.93% CAGR through 2031.

- By end-user, residential held 67.92% of the Mexico home textile market share in 2025, while the Mexico home textile market size serving commercial end-users is projected to grow at a 5.62% CAGR through 2031.

- By distribution channel, offline captured 76.34% of the Mexico home textile market share in 2025. The Mexico Home Textile market size for online channels is projected to expand at a 6.45% CAGR through 2031.

- By geography, Central Mexico captured 35.31% of the Mexico home textile market share in 2025. Northern Mexico is forecast to grow at a 6.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Home Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Replacement-Driven Demand from Housing Resale & Rental Turnover | +1.2% | National; strongest in Mexico City, Monterrey, Guadalajara | Medium term (2-4 years) |

| Hospitality & Short-Stay Accommodation Refresh Cycles | +0.9% | Riviera Maya, Puerto Vallarta, Mexico City core | Short term (≤ 2 years) |

| Premiumisation through Wellness, Sleep Quality & Climate-Adaptive Fabrics | +0.8% | National, premium pockets in Central and Northern Mexico | Long term (≥ 4 years) |

| E-commerce-Led Product Discovery and Faster Style Obsolescence | +1.1% | National, led by metropolitan zones | Short term (≤ 2 years) |

| Sustainability-Linked Material Substitution | +0.7% | Export clusters and compliant retailers nationwide | Long term (≥ 4 years) |

| AI-enabled Demand Forecasting by Major Retailers | +0.6% | National networks of leading omnichannel retailers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Replacement-Driven Demand from Housing Resale & Rental Turnover

A persistent housing deficit and multi-year construction programs keep initial outfitting and replacement cycles elevated for sheets, towels, and curtains across ownership and rental units. Government-backed initiatives and lender commitments sustain homebuilding pipelines, while urban migration and nearshoring-related job growth add household formation that feeds steady demand in the Mexico home textile market. Northern metros such as Monterrey add formal jobs and attract investment, which supports residential leasing and resale activity and increases purchase frequency for everyday home textiles. Each completed dwelling requires a full initial kit of bed linen, bath sets, and basic window treatments, and turnover events trigger refresh cycles as landlords and sellers prepare units for the next occupant. The combined effect is a visible pull on high-velocity categories where value and durability matter, alongside selective premium upgrades where budgets allow.

Hospitality & Short-Stay Accommodation Refresh Cycles: High-Turnover Catalyst

New and refurbished hotels, plus professionally managed rentals, operate on intensive laundering and service schedules that accelerate wear, tightening replacement intervals for bed linens and bath textiles[2]Tecma, "Monterrey Attracts Foreign Investment Across Industries," tecma.com. The Mexico Home Textile Market benefits from openings in business hubs and tourist corridors, where occupancy peaks compress maintenance windows and raise the need for duplicate inventories. Hotel and rental operators prioritize consistent guest experience, which lifts demand for durable, easy-care textiles that retain quality through frequent wash cycles. Retailers that offer rapid fulfillment and broad assortments help operators refresh rooms on a tight timeline, reducing downtime and missed bookings. This steady cadence supports mix upgrades toward performance towels and higher thread-count sheets, where guest ratings and branding justify the spend.

Premiumization through Wellness, Sleep Quality & Climate-Adaptive Fabrics: A Strategic Shift

Consumers associate better sleep and wellness with breathable, skin-safe, and temperature-adaptive fabrics, which shifts selection criteria from price alone to material attributes and certifications. Retailers and brands respond with higher-spec collections and tighter quality control that elevate the perceived value of premium bedding and performance upholstery in the Mexico home textile market. Product roadmaps emphasize safe chemistry and circular design, aligning with global standards for restricted substances and aiming to reduce environmental load in production and use. Logistics and planning upgrades enable more frequent collection refreshes and faster flow of on-trend designs that still meet elevated durability requirements. The result is a gradual migration from basic cotton toward blends and specialty fibres where comfort, care ease, and longevity intersect.

Sustainability-Linked Material Substitution: From Compliance to Competitive Advantage

Circularity and low-impact inputs are becoming baseline expectations, pushing suppliers to shift from virgin materials toward recycled polyester and certified cotton where traceability is verifiable. Global brands driving circular initiatives transfer know-how into local sourcing and production practices that reduce water and energy intensity across the value chain. Social enterprise partnerships and repair, reuse, and recycling programs support closed-loop pilots that channel textile waste into new product lines. Domestic contract manufacturers that invest in cleaner processes and recycled inputs can differentiate on compliance and durability, a position that strengthens export and retail partnerships. Over time, these moves expand the premium subset of the Mexico home textile market while lowering the lifecycle cost and footprint of mainstream assortments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Cotton, Polyester & Yarn Input Costs | -1.0% | National, acute in the Puebla-Tlaxcala textile belt | Short term (≤ 2 years) |

| High Price Sensitivity Limiting Premium Textile Penetration | -0.7% | National; most acute in Southern and lower-income areas | Medium term (2-4 years) |

| High Water Footprint of Conventional Dyeing | -0.5% | Puebla, Tlaxcala, and Estado de México dyeing clusters | Long term (≥ 4 years) |

| Low Brand Loyalty and Intense Private-Label Competition | -0.8% | National; mass merchandiser channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Cotton, Polyester & Yarn Input Costs: The Perennial Margin Squeeze

Domestic cotton production is forecast to be lower while consumption and import needs persist, exposing mills to global pricing and currency swings that pressure margins. Mexico’s MY 2025/26 cotton production drop and higher imports highlight vulnerability to drought, input inflation, and supply disruptions that flow into yarn and fabric costs[3]Claudia Hernández, “Cotton and Products Update,” USDA Foreign Agricultural Service, apps.fas.usda.gov. Polyester costs also track petrochemical markets, complicating long-range pricing for blended fabrics even when capacity is available. High import content for textile inputs increases exposure to freight and tariff shifts, which filter into shelf prices in the Mexico home textile market.

High Price Sensitivity Limiting Premium Textile Penetration: The Affordability Ceiling

Households prioritize essentials when inflation bites, which constrains the addressable pool for high-thread-count or specialty-fibre linens in mass channels. Apparel and textiles carry a smaller budget share than food and staples, so upgrades must deliver visible quality and care benefits to justify the premium. Private labels and large-format retailers use scale to offer attractive value in core items, which sets a stringent reference price for national brands. E-commerce intensifies price transparency, and cross-border platforms raise competitive benchmarks on basic sheets, towels, and curtains. As a result, the premium subset of the Mexico home textile market leans toward affluent urban districts and design-led retailers while value-engineered blends dominate volume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Bed Linen Dominates, Yet Upholstery Surges on Commercial Renovation Wave

Bed linen commanded a 41.53% share in 2025, reflecting its ubiquity across residential, hospitality, and institutional buyers in the Mexico home textile market. Upholstery is the fastest-growing application at a 6.14% forecast CAGR to 2031 as office and hotel investments expand seating, lounge, and performance fabric needs. Rental turnover and resale staging reinforce frequent refreshes of sheets and pillowcases, and value-focused buyers emphasize durable, easy-care weaves for everyday use. Nearshoring brings multinational openings and fit-outs that favor stain-resistant and high-traffic upholstery selections for reception and break areas. Retailers with fast fulfilment and broad bedding assortments support short-dated refreshes that keep inventories aligned with seasonality and style shifts.

The Mexico home textile market size for upholstery is projected to expand at a 6.14% CAGR between 2026 and 2031, aided by commercial renovations and a growing base of professionally managed rentals. In bed linens, shoppers weigh thread count, fabric blend, and care needs, while hospitality buyers prioritize longevity across many laundering cycles. Decorative textiles such as throws and cushion covers benefit from social and influencer discovery, which drives small-basket, high-frequency purchases. Office expansions in industrial metros add upholstered seating demand to outfitting lists alongside blinds and basic soft furnishings. Together, these patterns support a balanced mix of everyday essentials and performance-driven upholstery within the Mexico home textile market.

By Material: Cotton Retains Share, Yet Synthetic Fibres Accelerate on Durability and Sustainability Pivots

Cotton retained a 54.25% share in 2025 on the strength of its breathability and familiar hand-feel in the Mexico home textile market. Synthetic fibres are set to grow at a 5.93% CAGR to 2031, reflecting care convenience, wrinkle resistance, and colorfastness that extend service life. Domestic cotton production is forecast to decline in the future while imports rise, increasing exposure to global pricing and supply cycles. These shifts keep cost discipline central for blended fabrics as mills react to import costs and the reliability of upstream inputs. As retailers emphasize durability and total cost of ownership, polyester-rich blends hold share where maintenance costs matter most.

Circular economy priorities also steer mix changes. The Mexico home textile market is adopting more recycled polyester and certified natural inputs as brands codify traceability and low-impact processing. Global sustainability programs align suppliers to reduce water and energy use and to manage chemicals in finishing. Social enterprise collaborations and textile waste repurposing pilots demonstrate scalable alternatives for fiber sourcing and product development. Domestic contract manufacturers invest in cleaner manufacturing and rPET supply lines to meet retailer standards while preserving price competitiveness. These material shifts favour blends that balance comfort, care ease, and environmental performance in the Mexico home textile market.

By End-User: Residential Prevails, Yet Commercial Accelerates on Nearshoring and Hospitality Expansion

Residential end-users accounted for 67.92% of the market in 2025, reflecting the large household base and steady replacement cadence for bed and bath essentials in the Mexico home textile market. Replacement frequency rises with tenancy turnover and lifestyle upgrades, with buyers trading up for better hand-feel and care characteristics in sheets and towels. Retailers’ digital tools and fast delivery ease periodic refresh cycles and support broader pattern experimentation in decor items. Local cloud infrastructure supports personalized product discovery and reliable order tracking in major metros. These dynamics anchor household-led volume while enabling gradual premium shifts in the Mexico home textile market.

Commercial end-users are forecast to grow at a 5.62% CAGR through 2031, with hotels, rentals, offices, and institutional buyers driving volume in high-duty textiles. Nearshoring brings corporate expansions and new offices that require upholstery and soft furnishings, along with basic linens for on-site accommodations. Business districts and logistics corridors see continuous outfitting and replacement as facilities open or scale capacity. Infrastructure projects in the south-east catalyze service growth that eventually boosts hospitality-related textile requirements. Over the forecast, this segment raises demand for performance materials and easy-care blends in the Mexico home textile market.

By Distribution Channel: Offline Dominance Persists, Yet Online Explodes on Omnichannel Maturation

Offline channels captured 76.34% share in 2025, anchored by mass merchandisers, department stores, and specialty formats that support tactile evaluation and immediate fulfillment in the Mexico home textile market. Large formats expand assortments and private labels in bed and bath basics, which set value points for national brands. Department stores invest in marketplace scale, fast delivery, and click-and-collect to blend in-store experience with digital convenience. Specialty home concepts push curated aesthetics and material innovation with strong visual merchandising. Together, these channels maintain category leadership while integrating digital journeys that lift conversion.

The Mexico home textile market size for online channels is projected to grow at a 6.45% CAGR through 2031, reflecting a mature omnichannel infrastructure and broader assortment online. Department stores report rising digital penetration and faster delivery windows that reduce cart abandonment for soft goods. Local cloud capacity improves app performance and recommendation latency, enabling higher degrees of personalization. Online marketplaces draw in long-tail sellers that extend choices in patterns, sizes, and bundle options. These elements reinforce a steady shift in discovery and replenishment toward digital paths within the Mexico home textile market.

Geography Analysis

Central Mexico is expected to hold 35.31% of the Mexico home textile market in 2025, supported by dense retail networks, strong department store presence, and higher-income households. Department stores in Mexico City lead omnichannel transitions, enabling two-day delivery across much of the region. Specialty home and lifestyle stores offer curated assortments for design-conscious consumers. Efficient last-mile logistics and digital adoption streamline replenishment, sustaining growth despite moderated housing demand in core neighborhoods.

Northern Mexico is projected to grow at a 6.18% CAGR through 2031, driven by manufacturing inflows, job creation, and corporate expansions. Monterrey and nearby areas see investments in transport, industrial real estate, and services, boosting demand for bed, bath, and upholstery products. New offices, hotels, and worker housing increase the need for durable, easy-care textiles. Retailers expand assortments and fulfillment capabilities to serve growth corridors, driving higher sell-through rates for home furnishings and above-average market gains.

Southern Mexico grows at a slower pace but includes hotspots tied to tourism and logistics improvements. Infrastructure projects like the Maya Train and the Interoceanic Corridor enhance connectivity and attract investments in services and manufacturing. Service sector growth drives demand for hospitality textiles in coastal municipalities and gateway cities. Retail penetration improves through new malls and omnichannel formats in second-tier locations, contributing to steady market growth over time.

Competitive Landscape

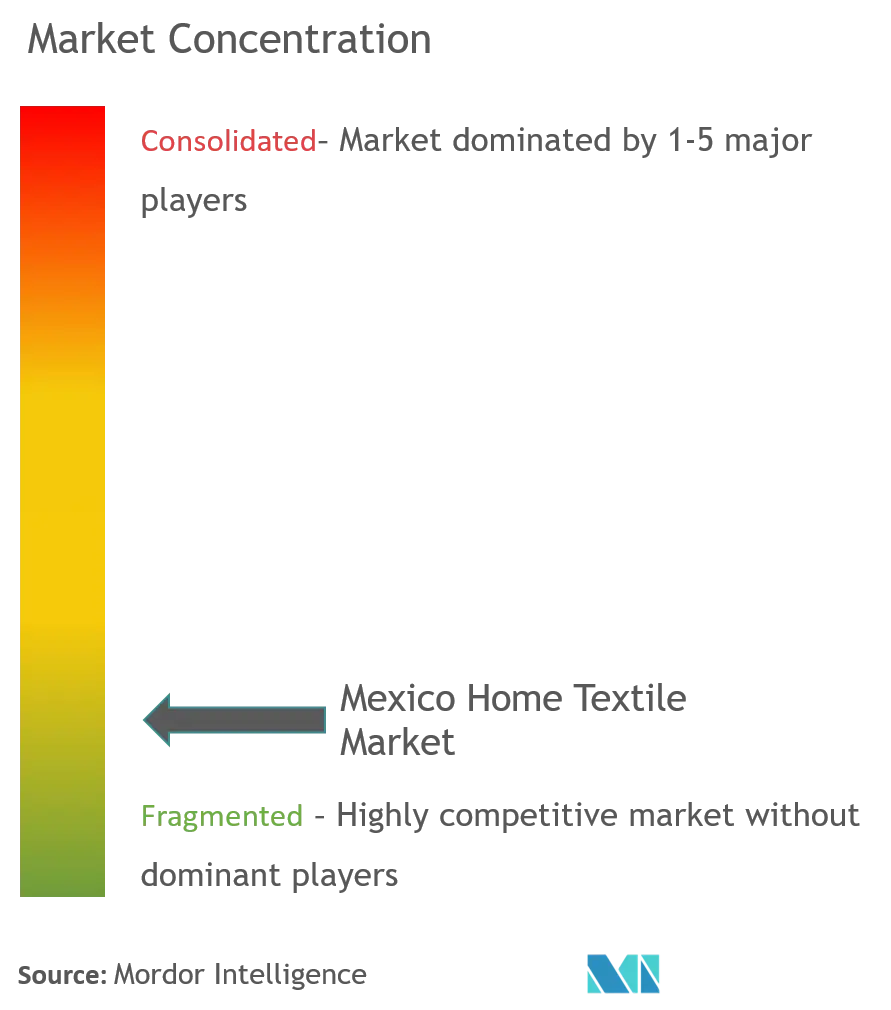

The Mexico home textile market is moderately fragmented, featuring global retailers, domestic brands, and strong private labels. Global retailers expand assortments and invest in circular material programs, setting benchmarks for suppliers. Fashion-driven players frequently update collections and enhance distribution to align with demand. Department stores combine marketplace scale with rapid delivery to capture replenishment and trend-driven purchases in bed and bath. Mass merchants grow private-label offerings, establishing competitive price points for entry to mid-tier categories.

Leading players demonstrate strategic directions. Inter IKEA invests in supply chain resilience and sustainability, influencing fiber selection, chemical management, and circular pilot programs. Inditex focuses on logistics upgrades and refreshed product cadences, enabling faster transitions and timely replenishment for home collections. Liverpool reports increased digital penetration, marketplace SKU growth, and faster deliveries, strengthening its omnichannel position. These strategies push suppliers to improve planning visibility, reduce lead times, and enhance quality assurance.

Private-label growth pressures mid-tier brands lacking differentiation. Costco’s Kirkland Signature sets price-value expectations and quality benchmarks, compelling national brands to meet these standards to maintain shelf presence[4]Costco Wholesale Corporation, “Annual Report 2025,” Investor Relations, investor.costco.com. Domestic brands launch seasonal collections and licensed designs to remain competitive, focusing on aesthetics and pricing. Some players invest in cleaner production, recycled materials, and waste reduction to secure partnerships with sustainability-focused retailers. The market is trending toward polarization between premium, sustainability-led offerings and value-driven private labels.

Mexico Home Textile Industry Leaders

-

Grupo Kaltex

-

Springs Global (Cannon Home)

-

Colchas Concord

-

Tramas y Cortinas

-

Svitex Home

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Circulose, a recycled textile pulp producer, partnered with Birla Cellulose, a sustainable textiles leader, to enhance textile recycling. Circulose will supply 100% recycled textile pulp, enabling Birla Cellulose to produce viscose staple fibre for Circulose's brand partners. This collaboration aims to advance circularity in the fashion industry and establish global sustainability benchmarks.

- November 2025: Mexico announced a USD 6.5 billion initiative to strengthen its textile and footwear industries. The Ministry of Economy, in partnership with BBVA and Nacional Financiera, introduces funding programs aimed at generating 50,000 jobs across multiple sectors, reflecting the government’s commitment to economic revitalization and employment growth.

- January 2025: AWS opened the AWS Mexico (Central) Region and plans to invest more than USD 5 billion over 15 years, adding local cloud capacity for analytics, personalization, and low-latency retail applications. The company projects more than USD 10 billion added to GDP and support for an average of 7,000 full-time equivalent jobs annually, which strengthens digital infrastructure for omnichannel retailers serving home textiles.

Mexico Home Textile Market Report Scope

The Mexico Home Textile Market is defined as the organized industry encompassing the production, distribution, and consumption of textile products used in residential and commercial interiors, including bed, bath, kitchen, upholstery, and floor coverings. The market reflects both domestic demand and export flows, shaped by evolving consumer preferences, housing dynamics, hospitality cycles, and sustainability imperatives.

The study provides a comprehensive assessment of the market landscape, highlighting drivers and restraints. Market segmentation is analyzed across application (bed linen, bath linen, kitchen linen, upholstery, carpets & area rugs), material (cotton, linen, synthetic fibres, other materials), end‑user (residential, commercial), distribution channel (offline mass merchandisers, home centers, specialty stores, other offline channels, online), and geography (Northern Mexico, Central Mexico, Southern Mexico). The report offers Market size and forecasts for the Mexico Home Textile Market in value (USD) for all the above segments.

By Application

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Carpets & Area Rugs |

By Material

| Cotton |

| Linen |

| Synthetic Fibres |

| Other Materials |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | |

| Specialty Stores | |

| Other Offline Channels | |

| Online |

By Geography

| Northern Mexico |

| Central Mexico |

| Southern Mexico |

| By Application | Bed Linen | |

| Bath Linen | ||

| Kitchen Linen | ||

| Upholstery | ||

| Carpets & Area Rugs | ||

| By Material | Cotton | |

| Linen | ||

| Synthetic Fibres | ||

| Other Materials | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | ||

| Specialty Stores | ||

| Other Offline Channels | ||

| Online | ||

| By Geography | Northern Mexico | |

| Central Mexico | ||

| Southern Mexico | ||

Key Questions Answered in the Report

What is the 2026 size and 2031 outlook for Mexico's home textiles?

The Mexico Home Textile Market is estimated at USD 2.54 billion in 2026 and is projected to reach USD 3.31 billion by 2031 at a 5.41% CAGR. Growth is anchored in housing formation and hospitality demand.

Which application category leads growth in Mexico home textiles through 2031?

Upholstery is the fastest growing application at 6.14% CAGR to 2031, while bed linen holds the largest share at 41.53% in 2025.

How is the material mix evolving in Mexico home textiles?

Cotton holds 54.25% in 2025, while synthetic fibres are set to grow at 5.93% to 2031 as buyers emphasize durability and easy care.

How is the channel mix shifting for Mexico home textiles?

Offline holds 76.34% in 2025, while online is set to expand at 6.45% to 2031. Liverpool delivered 54.8% of digital orders within 48 hours in Q2 2025, which supports faster replenishment.

Which regions in Mexico show the strongest momentum for home textiles?

Northern Mexico is forecast to grow at 6.18% to 2031, while Central holds a 35.31% share in 2025.

What risks could slow Mexico's home textile growth over the next two years?

Input cost volatility and water-intensive dyeing strain margins and compliance. Cotton production decline and higher import reliance add exposure to global price swings.

Page last updated on: